Substrate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

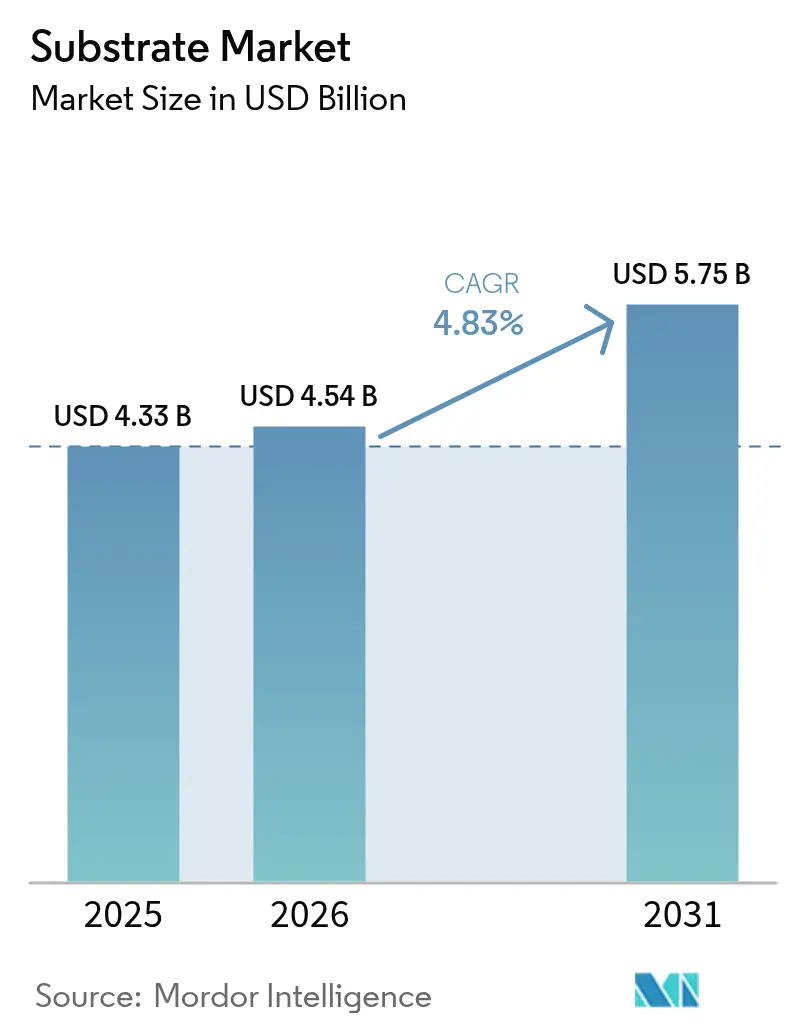

| Market Size (2026) | USD 4.54 Billion |

| Market Size (2031) | USD 5.75 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Substrate Market Analysis by Mordor Intelligence

The substrate market size was valued at USD 4.33 billion in 2025 and estimated to grow from USD 4.54 billion in 2026 to reach USD 5.75 billion by 2031, at a CAGR of 4.83% during the forecast period (2026-2031). Demand is rising as AI accelerator architectures, 5G radio deployments, and electric-vehicle (EV) power-electronics broaden the application base for advanced packaging laminates. Expansion is moderate because traditional printed-circuit infrastructure is mature, yet design wins linked to heterogeneous integration are raising average substrate value per device. Competitive intensity is shaped by supply-chain exposure to high-Tg resins, the capital burden tied to new fabrication lines, and sustainability mandates curbing halogenated laminates. Asia Pacific keeps a leadership edge thanks to clustered semiconductor assembly operations, swift capacity additions in Taiwan, South Korea, and China, and regional policy support that lowers production costs.

Key Report Takeaways

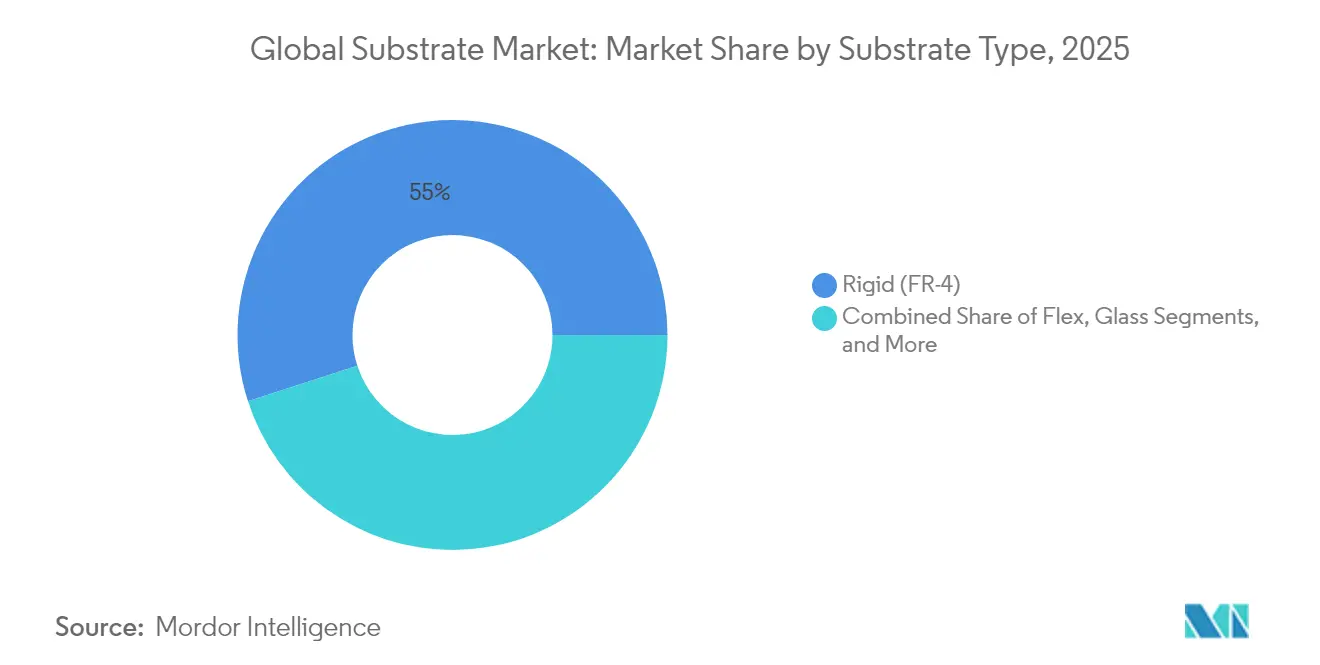

- By substrate type, rigid FR-4 captured a 54.98% share of the substrate market in 2025, while glass substrates are set to grow the quickest at a 5.54% CAGR through 2031.

- By material, FR-4 epoxy glass held 41.88% of the substrate market size in 2025; glass materials record the fastest 5.42% CAGR to 2031.

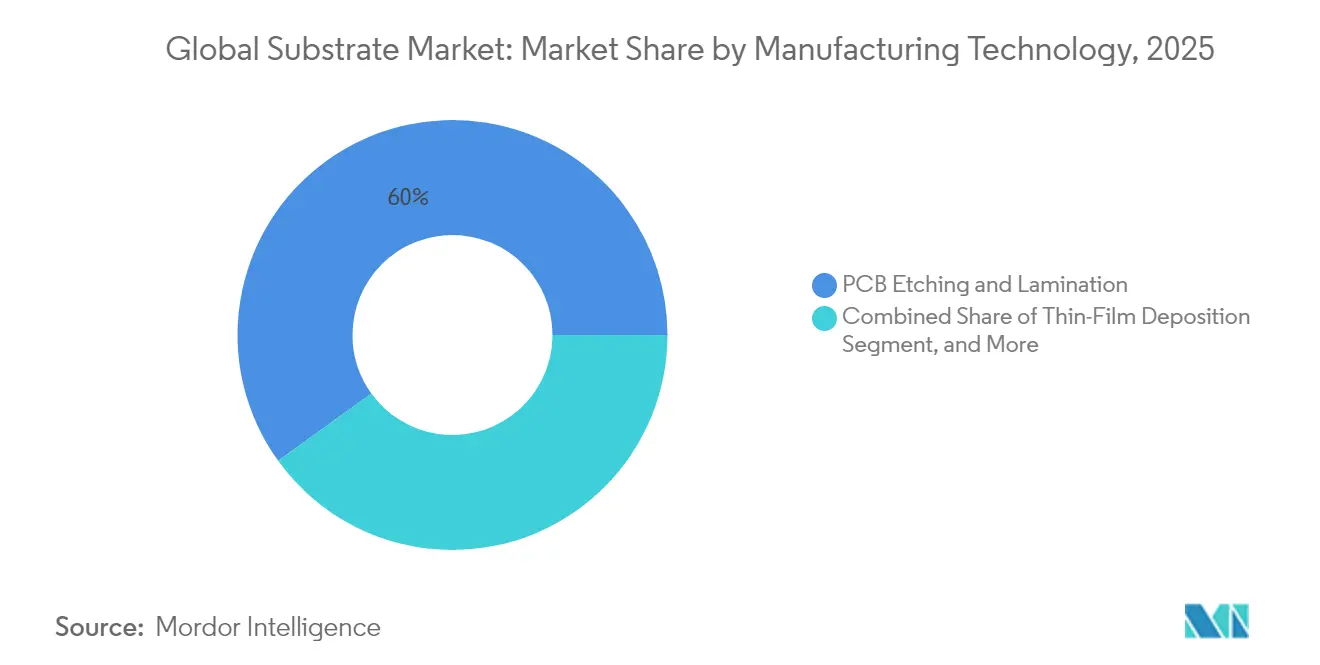

- By manufacturing technology, PCB etching and lamination represented 59.95% of the substrate market share in 2025, whereas fan-out wafer-level packaging is projected to expand at a 5.62% CAGR.

- By end-user industry, computing and data storage accounted for 29.22% of the substrate market in 2025, yet automotive and transportation is advancing at a 5.12% CAGR.

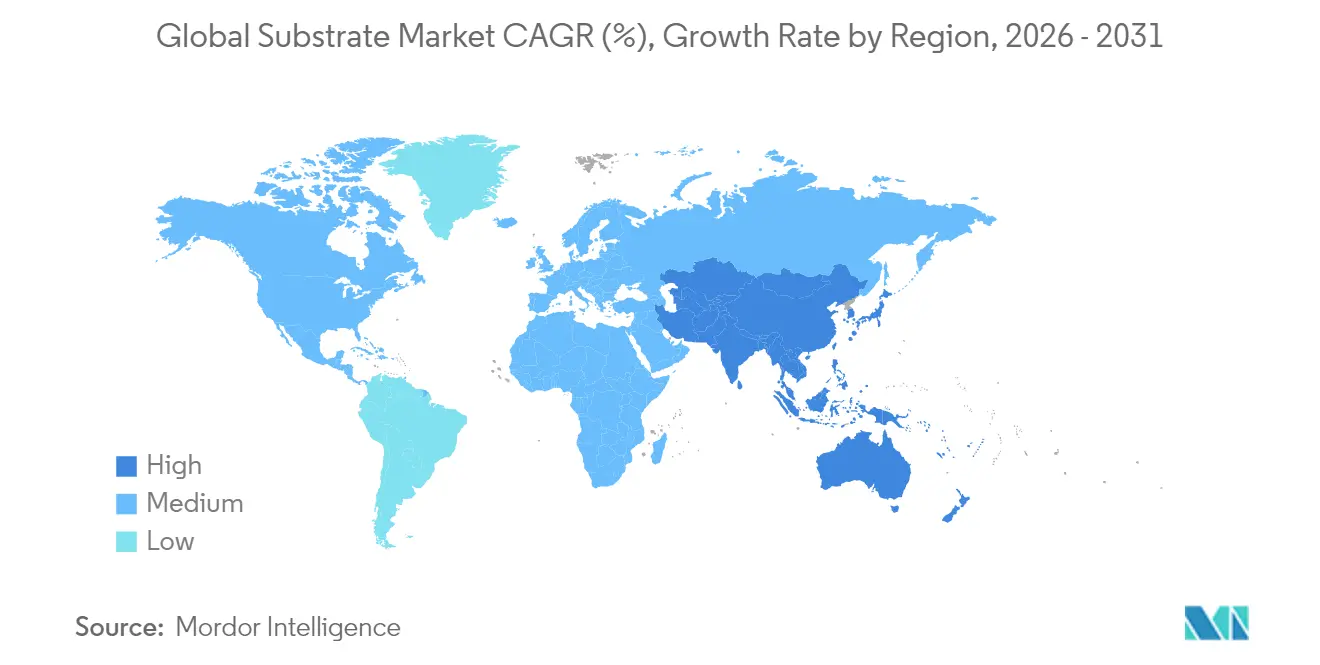

- By geography, Asia Pacific commanded a 37.92% share in 2025 and continues as the fastest-growing region with a 5.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Substrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of heterogeneous integration in AI accelerators | +1.2% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Miniaturization demand in mobile and wearable devices | +0.8% | Global, led by APAC manufacturing hubs | Short term (≤ 2 years) |

| 5G roll-outs boosting high-frequency RF substrates | +0.9% | North America, Europe, APAC core markets | Medium term (2-4 years) |

| EV power-electronics adoption of ceramic and metal-core substrates | +0.7% | Global, with early gains in Europe, China, North America | Long term (≥ 4 years) |

| Emergence of chiplet-based packages | +1.0% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Regional semiconductor subsidy races | +0.6% | North America, Europe, select APAC regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Heterogeneous Integration in AI Accelerators

Heterogeneous integration allows multiple specialized dies to work together inside a single package, raising substrate complexity requirements. Intel targets 10 × higher interconnect density over organic laminates using glass substrates, enabling logic, memory, and accelerator chiplets to coexist without signal-integrity losses.[1]Intel Corporation, “Glass Substrate Technology Roadmap,” newsroom.intel.com Organic FR-4 cannot match these routings at fine pitches, which encourages designers to transition toward glass, advanced organic, and ceramic options. Package architectures now mix high-speed interfaces next to sensitive analog rails, so dielectric loss, coefficient of thermal expansion, and via reliability become critical selection criteria. Fabricators invest in higher-resolution lithography and laser drilling to meet line/space rules under 10 µm. As AI workloads continue scaling, packaging-centric performance gains are as important as front-end node shrinks, sustaining premium pricing for advanced substrates.

Miniaturization Demand in Mobile and Wearable Devices

Smartphone boards are shrinking while component counts rise, pressing suppliers to deliver thinner, denser, and more flexible substrate constructions. Rigid-flex designs with polyimide cores help route high-speed buses around fold lines without cracking. Wearables further compress stack-ups, forcing the adoption of embedded passive components inside the core layers. Makers in China, South Korea, and Vietnam doubled orders for flexible laminates after 2024 design cycles, lifting utilization in flex substrate factories. Tighter component clearances heighten heat buildup; hence, metal-core variants with aluminum backing are entering high-end mobile segments. These dynamics keep substrate market revenue expanding even when handset unit volumes plateau because value per board creeps higher.

5G Roll-Outs Boosting High-Frequency RF Substrates

Millimeter-wave base stations operate beyond 28 GHz, demanding ultra-low dielectric loss. Rogers Corporation commercialized PTFE-based laminates with stable Dk and Df across −40 °C to 105 °C, capturing multi-layer antenna array designs.[2]AMD Inc., “Chiplet Architecture and Advanced Packaging,” amd.com OEMs request controlled-impedance stack-ups with copper roughness less than 2 µm to limit insertion loss. Equipment makers simultaneously lower board cost by blending high-frequency cores only where needed, sandwiching them between less costly prepregs. Because 5G densification is staggered by region, substrate suppliers enjoy a multi-year revenue runway as operators phase upgrades. North America and Japan drove initial demand in 2024, while Europe and India scale orders through the forecast window.

EV Power-Electronics Adoption of Ceramic and Metal-Core Substrates

EV inverters and onboard chargers switch at hundreds of kilohertz, creating thermal hotspots that overwhelm standard epoxy-glass. Ceramic substrates using aluminum nitride offer thermal conductivity above 150 W/mK while still isolating high voltages, enabling smaller module footprints. Manufacturers such as Kyocera qualified ceramic boards for automotive reliability grades in 2025 testing cycles, boosting order backlogs for 2026 model launches. In mid-power cases, metal-core substrates with aluminum plates dissipate heat at one-third the cost of full ceramic, supporting a tiered product mix. As global EV sales approach 40 % of new-vehicle volumes in 2030, every power-module supplier requires a thermally enhanced substrate strategy, driving continuous adoption across price bands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility for high-Tg resins | -0.8% | Global, with acute impact in APAC manufacturing | Short term (≤ 2 years) |

| CAPEX intensity of advanced substrate lines | -1.1% | Global, concentrated in advanced manufacturing regions | Medium term (2-4 years) |

| Technological lock-in risk for legacy PCB fabs | -0.6% | North America and Europe, with spillover to APAC | Medium term (2-4 years) |

| Sustainability pressure on halogenated laminates | -0.4% | Europe and North America, expanding to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility for High-Tg Resins

Only a handful of chemical producers offer resins that survive above 170 °C glass-transition temperatures, so any outage tightens spot supply and spikes pricing. Trade restrictions on epoxy precursors raised lead times to 24 weeks during 2024, forcing substrate vendors to hold larger safety stocks. Inventory carrying costs erode margins, especially for small and mid-size shops. Automotive and aerospace customers mandate high-Tg boards for under-hood and avionics assemblies, so substitution with standard FR-4 is not feasible. Suppliers negotiate long-term contracts yet remain vulnerable to geopolitical disruptions around major resin-manufacturing centers in East Asia.

CAPEX Intensity of Advanced Substrate Lines

A single advanced glass-substrate fab demands over USD 100 million in precision lithography, plasma etch, and metrology tools, yielding depreciation charges that can outstrip operating profits in a down cycle. Smaller PCB firms struggle to finance upgrades while maintaining legacy revenue streams, prompting mergers or facility closures. Equipment lead times exceed 12 months, so capacity cannot be added swiftly once demand surges. The high investment hurdle slows industry response to new design wins, sometimes handing orders to vertically integrated giants that can self-fund expansions. Capital scarcity therefore tempers substrate market growth despite strong end-market pull.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Type: Glass Substrates Drive Next-Generation Packaging

Rigid FR-4 retained a 54.98% slice of the substrate market share in 2025, reflecting entrenched infrastructure and low unit costs. The segment addresses mainstream notebooks, televisions, and home appliances that prize cost per square inch over bleeding-edge performance. In contrast, glass substrates record a 5.54% CAGR, the fastest pace across types, because AI accelerators and switch-ASIC roadmaps now mandate up to 10 × interconnect density. That requirement pulls demand toward glass interposers capable of tighter dimensional tolerances and low CTE mismatch. Ceramic substrates occupy a stable niche in power-dense circuits, while metal-core boards pick up LED lighting and mid-power designs. Flex and rigid-flex constructions hold share in foldable phones and automotive infotainment panels where bend radii beat rigid boards. Looking forward, the substrate market size for glass lines is projected to exceed USD 1.07 billion by 2031 as yield learning curves trim per-layer costs. Suppliers split capacity between high-layer glass and cost-optimized FR-4 to hedge cyclical swings.

A growing list of chip vendors adopt glass for reticle-sized interposers, lifting order visibility for specialty panel fabs and sparking partnerships with equipment makers. Pilot production runs delivered defect densities under 50 ppm in 2025, supporting volume ramps from 2026 onward. Yet rigid FR-4 remains relevant for price-sensitive consumer electronics, and its deep supply base provides negotiating leverage to OEMs. Hybrid stack-ups that laminate glass cores inside FR-4 shells emerge as a bridge technology, helping customers transition without wholesale redesigns. Overall, coexistence rather than outright replacement defines the next five-year substrate mix.

By Material: Advanced Materials Challenge FR-4 Dominance

FR-4 epoxy glass held a 41.88% revenue share in 2025 thanks to its balanced mechanical strength, flame retardancy, and low price. Glass materials, however, chart the leading 5.42% CAGR through 2031 by enabling finer line/space and reducing warpage in large substrates. BT resin provides lower dielectric constants suited to high-speed serial links, capturing advanced networking cards. Polyimide layers withstand continuous service up to 260 °C, supporting aerospace and down-hole drilling electronics where FR-4 fails. Ceramic plates of aluminum nitride or alumina reach thermal conductivities above 150 W/mK, making them indispensable in SiC-based EV inverters. Metal-core laminates combine copper or aluminum backers with prepreg, offering an intermediate thermal step that balances cost and performance for LED drivers.

Material innovators tailor filler chemistry to lower loss tangent at mmWave bands, an attribute critical for 5G front-end modules. Sustainability drives demand for halogen-free alternatives compliant with RoHS and REACH, spurring incremental product launches from resin suppliers. As heterogeneous integration tightens line widths, coefficient of thermal expansion convergence between substrate and silicon becomes essential, giving glass an edge at high layer counts. Taken together, the substrate market continues fragmenting by material family as no single option satisfies every performance and cost target.

By Manufacturing Technology: Traditional Methods Face Advanced Packaging Pressure

PCB etching and lamination generated 59.95% of 2025 revenue, underpinned by amortized equipment and widespread engineering knowledge. These subtractive techniques remove copper to delineate traces and press multiple cores into a stack. Yield rates exceed 98% for four-layer consumer products, keeping per-panel costs low. Fan-out wafer-level packaging, though, charts a 5.62% CAGR, propelled by chiplet adoption and the wish to eliminate silicon interposers. Redistribution layers (RDL) in fan-out stacks achieve sub-10 µm wiring and incorporate under-fill molds to support die. Thin-film deposition processes, using sputtering and electroplating, address niche RF multilayers where uniformity across large panels is paramount. Additive manufacturing, such as aerosol jet printing, cuts material waste during prototyping and allows conformal routing on complex shapes.

Embedded-die construction embeds active silicon inside cavities milled into the substrate, slashing parasitic inductance and height profiles. However, reliability testing extends time-to-market, limiting mainstream adoption until automotive-grade qualifications are expected to complete in 2026. In the near term, customers select technology based on cost-per-I/O and electrical performance. Large-volume handset boards will continue running on incremental FR-4 lines, whereas AI accelerators and high-speed network switches move to fan-out or glass panel routes. Therefore, the substrate market size growth hinges on hybrid production setups melding established etching with advanced RDL cells.

By End-User Industry: Automotive Growth Challenges Computing Leadership

Computing and data-storage systems consumed 29.22% of 2025 shipments, reflecting hyperscale data-center builds and enterprise server refresh cycles. Each new CPU socket packs larger interposers and more DDR channels, so server boards add layers and area. Automotive and transportation, however, is forecast to expand at a 5.12% CAGR through 2031, the steepest trajectory among verticals. The pivot to battery-electric drivetrains and advanced driver-assistance systems multiplies electronic control units per vehicle, many of which demand ceramic or metal-core substrates for thermal headroom. Infotainment domain controllers adopt rigid-flex to route video over LVDS links through cramped dashboards.

Consumer electronics remains a steady base, with smartphones and wearables leaning on flex and rigid-flex for slim form factors. Industrial automation embraces higher-grade FR-4 and polyimide to survive factory temperatures and vibration. Medical devices adopt biocompatible coatings and tight trace geometries for implantable pumps and diagnostic cartridges. Telecom infrastructure gains from 5G deployments that favor low-loss laminates in active-antenna systems. The net effect is a portfolio shift toward high-value, performance-driven applications, reinforcing dollar content growth even where unit shipments stay flattish.

Geography Analysis

Asia Pacific maintained a 37.92% revenue share in 2025 and advances at a 5.29% CAGR through 2031 thanks to scale economies across Taiwanese, South Korean, and Chinese supply chains. Korea’s Samsung Electro-Mechanics and LG Innotek are upgrading to panel-level fan-out lines, funded partly by national innovation grants. Taiwan’s Zhen Ding Technology and Unimicron synchronize expansions with leading GPU and networking ASIC roadmaps to secure multiyear loadings. Mainland Chinese vendors pursue glass substrate independence to mitigate export-license uncertainties, organizing government-backed consortia to localize key tooling.

North America witnesses resurging activity as the CHIPS Act provides a 25% investment tax credit for advanced-packaging equipment, reducing effective capital intensity. Texas earmarked USD 1.4 billion in grants for substrate fabs co-located with new wafer facilities, and Oregon projects USD 40 billion semiconductor spending by 2030. OEMs value near-shoring for secure supply and faster engineering turns, prompting substrate makers to weigh smaller but higher-margin domestic plants.

Europe focuses on strategic autonomy, aligning subsidies with its automotive electrification roadmap. Ceramic substrates see higher penetration because German Tier-1 suppliers shift inverter assembly lines in-house. The European Union’s proposed Eco-Design regulation elevates scrutiny on halogenated materials, favoring FR-4 alternatives. Policy-driven demand shapes a premium market segment that rewards environmentally compliant suppliers.

Across regions, currency fluctuations influence sourcing decisions, and logistics bottlenecks incentivize closer proximity to final assembly. Diversification dilutes Asia Pacific’s share only modestly, yet regional competition yields multiple growth nodes for the substrate market.

Competitive Landscape

The substrate market shows moderate concentration: the top five players control around 55% of global revenue, giving buyers options yet enabling leaders to achieve economies of scale. Ibiden leverages vertical integration from resin synthesis through substrate finishing, ensuring cost control during resin shortages. Unimicron operates panel-level packaging lines reaching 25 µm line width, appealing to AI accelerator vendors that push I/O counts. Samsung Electro-Mechanics co-designs flexible substrates with smartphone OEMs, shortening ramp times for flagship launches. Smaller firms concentrate on niche materials such as aluminum nitride ceramics or low-loss PTFE to avoid direct price wars.

Strategic moves center on capacity expansion and technology licensing. LG Innotek allocated USD 3 billion for its Dream Factory fab that pairs glass-substrate tooling with fan-out capability. Ibiden earmarked USD 500 million to add glass plating cells, strengthening its position in data-center compute modules. Start-ups deploy additive manufacturing to prototype conformal RF boards within days, offering value-added engineering though still lacking high-volume throughput. Patent filings in glass interposers more than doubled in 2024 on IEEE Xplore, reflecting an innovation race among incumbents and challengers. Supply-chain bargaining power shifts toward well-capitalized firms that can secure scarce high-Tg resin allocations and fund multi-year development programs.

Legacy PCB houses unable to finance upgrades look for merger partners or exit commodity product lines, tightening market concentration. Meanwhile, tier-two specialists find white-space opportunities in ceramic and hybrid substrates for EV and aerospace use. The contest between volume players and specialty innovators keeps competitive dynamics fluid and merger and acquisition activity elevated.

Substrate Industry Leaders

Ibiden Co., Ltd.

Unimicron Technology Corp.

Samsung Electro-Mechanics Co., Ltd.

AT&S AG

LG Innotek Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: LG Innotek completed its Dream Factory in South Korea, a USD 3 billion facility dedicated to next-generation packaging substrates for AI accelerator and automotive power modules.

- August 2025: Intel outlined a glass substrate roadmap that targets production in 2026, claiming 10 × interconnect density gains over organic boards.

- July 2025: Ibiden expanded Japanese capacity with a USD 500 million glass-substrate line for data-center applications.

- June 2025: AMD disclosed chiplet-based CPUs that employ organic substrates embedding silicon bridges to link functional block.

Global Substrate Market Report Scope

The study tracks the substrate industry into four base categories - PCB, FHE, SLP, and SIP.

A printed circuit board (PCB) connects electrical or electronic components using conductive tracks and supports them mechanically. They are used in almost all electronic products, including passive switch boxes.

FHE is the convergence of additive circuitry, passive devices, and sensor systems typically manufactured using printing methods and thin, flexible silicon chips. These devices differ from traditional electronics in terms of size and flexibility. The technology finds applications due to the economies and unique capabilities of printed circuitry that are capable of forming a new class of devices for consumer electronics, the Internet of Things (IoT), medical, robotics, and communication markets.

The PCB Market is Segmented by Application (Computing, Consumer, Industrial/Medical, Communication, Automotive, and Military/Aerospace). The substrate Like PCB (SLP) Market is Segmented By Application (Consumer Electronics, Automotive, Communication, and Other Applications). The System In the Package (SIP) Market is Segmented By Application (Telecom and Infrastructure (Servers and Base Stations), Automotive and Transportation, Mobile and Consumer, Medical and Industrial, Aerospace and Defense).

The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| Rigid (FR-4) |

| Flex |

| Rigid-Flex |

| Ceramic |

| Glass |

| Other Types |

| Epoxy Glass (FR-4) |

| Polyimide |

| BT Resin |

| Ceramic (Alumina, AlN) |

| Glass |

| Metal-Core (Al, Cu) |

| Other Materials |

| PCB Etching and Lamination |

| Thin-Film Deposition |

| Additive Manufacturing / Printing |

| Fan-Out Wafer-Level Packaging |

| Embedded Die |

| Other Technologies |

| Computing and Data Storage |

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Medical |

| Telecom and Infrastructure |

| Aerospace and Defense |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Taiwan | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Substrate Type | Rigid (FR-4) | ||

| Flex | |||

| Rigid-Flex | |||

| Ceramic | |||

| Glass | |||

| Other Types | |||

| By Material | Epoxy Glass (FR-4) | ||

| Polyimide | |||

| BT Resin | |||

| Ceramic (Alumina, AlN) | |||

| Glass | |||

| Metal-Core (Al, Cu) | |||

| Other Materials | |||

| By Manufacturing Technology | PCB Etching and Lamination | ||

| Thin-Film Deposition | |||

| Additive Manufacturing / Printing | |||

| Fan-Out Wafer-Level Packaging | |||

| Embedded Die | |||

| Other Technologies | |||

| By End-User Industry | Computing and Data Storage | ||

| Consumer Electronics | |||

| Automotive and Transportation | |||

| Industrial and Medical | |||

| Telecom and Infrastructure | |||

| Aerospace and Defense | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Taiwan | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the substrate market in 2026?

The substrate market size is USD 4.54 billion in 2026 and is forecast to reach USD 5.75 billion by 2031.

Which substrate type is growing fastest?

Glass substrates post the highest 5.54% CAGR because AI and high-performance computing demand higher interconnect density.

What end-use sector will add the most growth?

Automotive and transportation deliver the steepest 5.12% CAGR as EV power-electronics drive ceramic and metal-core substrate adoption.

Why are glass substrates important for AI accelerators?

Glass provides 10 × interconnect density over organic boards, supporting chiplet integration and improved thermal expansion alignment.

How do government incentives influence substrate capacity?

Programs such as the U.S. CHIPS Act and EU subsidy schemes lower capital costs, encouraging new packaging fabs in North America and Europe.

Page last updated on: