Fibrate Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 5.11 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fibrate Drugs Market Analysis by Mordor Intelligence

The fibrate drugs market size was valued at USD 3.77 billion in 2025 and estimated to grow from USD 3.97 billion in 2026 to reach USD 5.11 billion by 2031, at a CAGR of 5.19% during the forecast period (2026-2031). Demand remains steady as cardiovascular risk factors surge worldwide and research broadens fibrate use beyond lipid lowering. The number of adults living with hypertension and diabetes—two key drivers of hypertriglyceridemia—is climbing sharply, with U.S. prevalence alone projected to hit 61.0% and 26.8%, respectively, by 2050. The successful therapeutic repurposing of fenofibrate for diabetic retinopathy, validated by the 27% disease-progression reduction reported in the 2024 LENS trial, further expands the market opportunity. Intensifying generic output—particularly from India and China—keeps prices in check, yet branded competitors are capturing growth through extended-release designs, fixed-dose combinations, and pharmacogenomic positioning. Meanwhile, emerging RNA-based lipid therapies have proven superior triglyceride reduction in Phase II results, signalling stiffer competition but also reinforcing the clinical importance of triglyceride control.

Key Report Takeaways

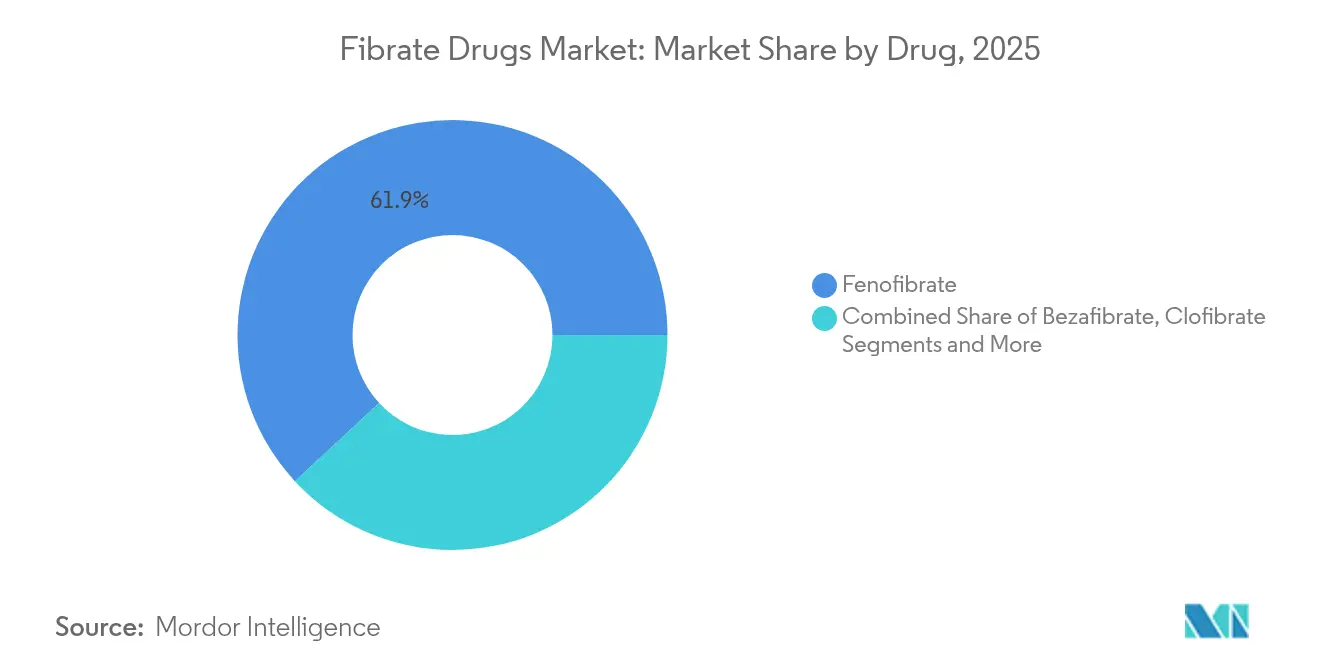

- By drug class, fenofibrate led with 61.90% of fibrate drugs market share in 2025; bezafibrate is forecast to register the fastest 7.12% CAGR through 2031.

- By product type, generics dominated 2025 revenue with a 74.85% stake, while branded offerings are projected to expand at 6.73% CAGR to 2031.

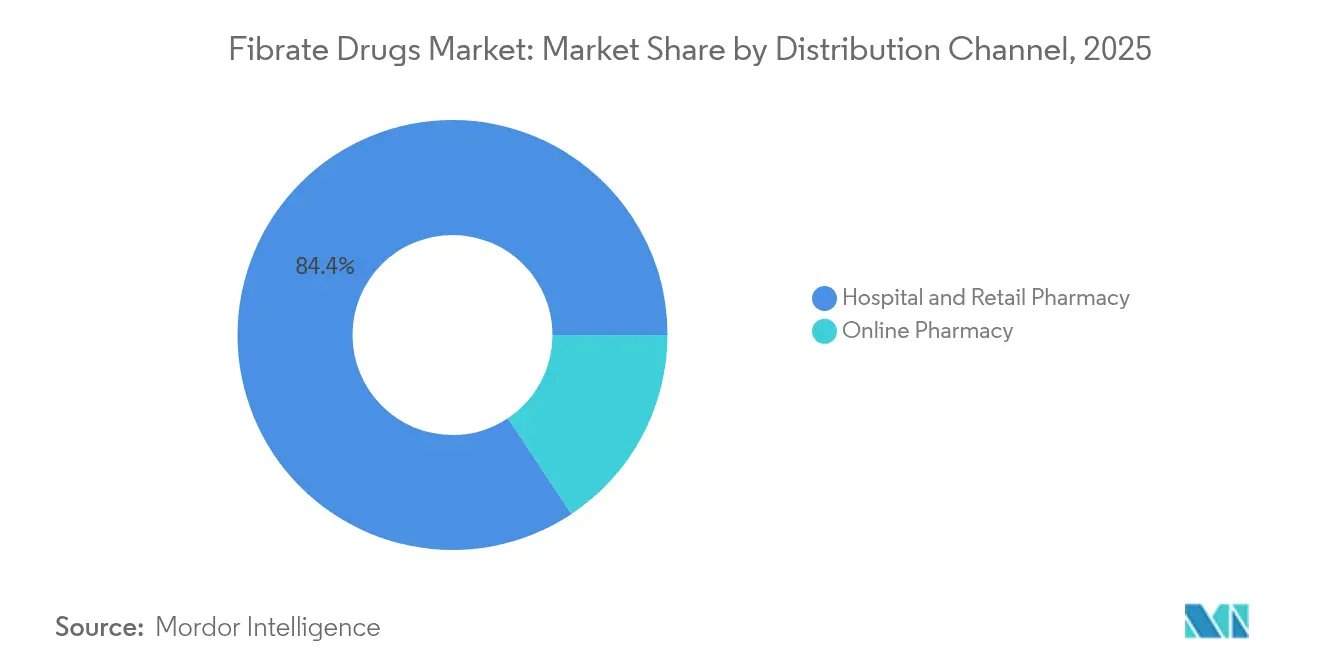

- By distribution channel, hospital and retail pharmacies commanded 84.35% of the market in 2025; online pharmacies represent the fastest-growing channel at an 11.03% CAGR.

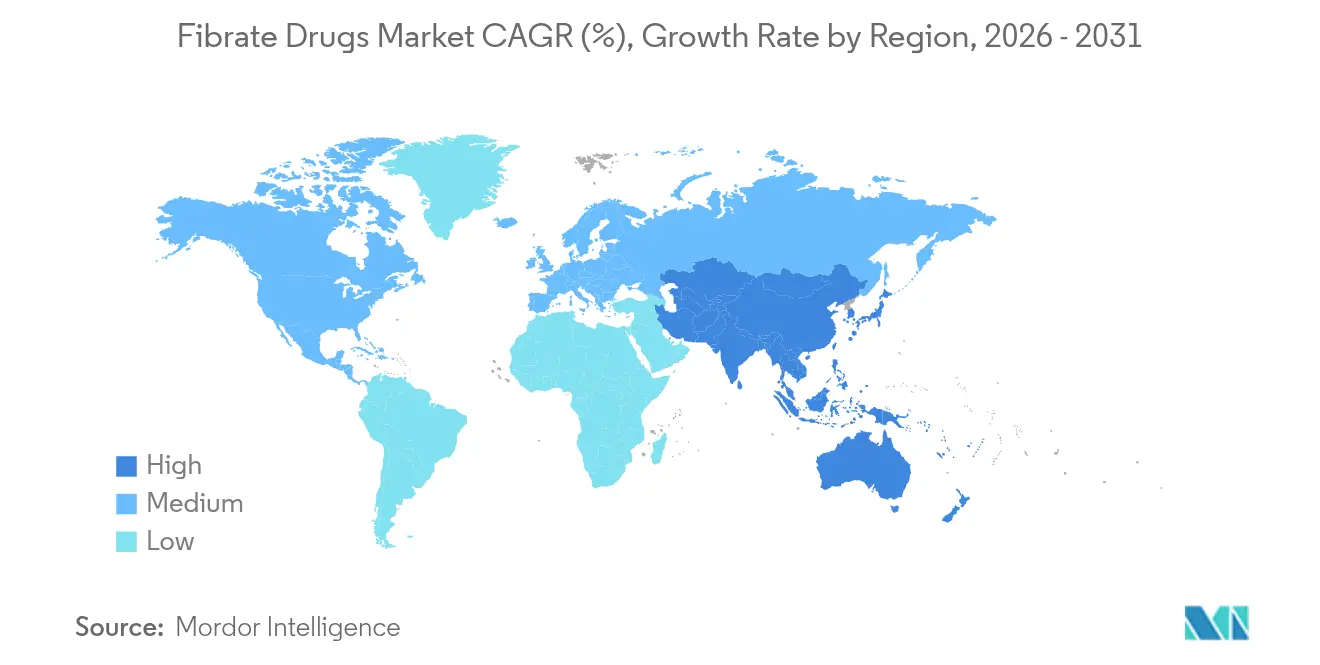

- By geography, North America held 38.20% of 2025 revenue; Asia-Pacific is poised to deliver the highest 8.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fibrate Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence Of Cardiovascular Diseases | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| High Investment In R&D Of Lipid–Lowering Drugs | +1.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Rising Incidence Of Metabolic Syndrome & Hypertriglyceridemia | +1.5% | Global, with early gains in Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Expanding Generic Manufacturing Capacity In Emerging Markets | +0.9% | APAC core, spill-over to MEA and South America | Short term (≤ 2 years) |

| Therapeutic Repurposing For Diabetic Retinopathy & CKD | +0.7% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Precision-Medicine Tools Enabling Targeted Fibrate Therapy | +0.4% | North America & EU initially, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Cardiovascular Diseases

Cardiovascular morbidity is climbing worldwide, pushing continuous demand for triglyceride-lowering agents. Chinese adults under 40 exhibited a 2.26-fold higher cardiovascular risk in the top triglyceride quartile, underscoring the contribution of elevated TG to early-age events. The American Heart Association’s 2024 update projects sustained expansion of diabetes and hypertension, enlarging the clinical pool for fibrate prescriptions. Hypertriglyceridemia-induced acute pancreatitis already causes one-fifth of global cases, with the burden highest in Asia[1]Jiongdi Lu et al., “Hypertriglyceridemia-Induced Acute Pancreatitis,” BMC Gastroenterology, bmcbio.com. Together, these patterns keep the fibrate drugs market firmly positioned within standard lipid-management algorithms.

High Investment in R&D of Lipid-Lowering Drugs

Capital inflows into lipid science spur innovation that often complements fibrate therapy. Breakthrough RNA therapeutics plozasiran and olezarsen lowered triglycerides far beyond conventional benchmarks in 2024 ACC presentations. Separately, Croda’s USD 133 million project to expand lipid-systems capacity—bolstered by USD 75 million in U.S. federal backing—signals supply-chain confidence in lipid-based technologies[2]Croda International, “U.S. Government Support to Expand Lipid Systems,” croda.com. Such investment nurtures combination-product pipelines pairing fibrates with statins or novel biologics.

Rising Incidence of Metabolic Syndrome & Hypertriglyceridemia

Metabolic syndrome prevalence is accelerating, led by urbanizing economies adopting Westernised diets. In Mongolia, 19.7% of adults screened in 2024 recorded high triglycerides, with abdominal obesity as a chief predictor. Korean cohort data showed the triglyceride-glucose index outperforming HOMA-IR as a predictor of future metabolic syndrome. Women of child-bearing age now carry a heavier metabolic burden, boosting the patient pool eligible for fibrate therapy.

Expanding Generic Manufacturing Capacity in Emerging Markets

India and China continue upgrading capacity, reliability, and compliance, lowering overall cost of therapy. India targets a USD 120 billion pharmaceutical footprint by 2030 and supplies one-fifth of U.S. generic volume. China secured 71% of 2024 NRDL drug listings for domestic firms, reinforcing domestic affordability. These trends underpin cost-effective access and intensify competitive pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frequent Product Recalls & Discontinuations | -0.8% | Global, with highest impact in regulated markets | Short term (≤ 2 years) |

| Stringent Regulatory Framework | -1.1% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Payer Preference For Statins & PCSK9 Inhibitors | -1.3% | Developed markets with advanced reimbursement systems | Long term (≥ 4 years) |

| Environmental Curbs On Fluorinated Intermediates Supply Chain | -0.6% | Global manufacturing, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Payer Preference for Statins & PCSK9 Inhibitors

Reimbursement bodies prioritise statins and, increasingly, PCSK9 inhibitors, relegating fibrates to second line unless severe hypertriglyceridemia persists. Claims data reveal 30.95% PCSK9 prescriptions were denied despite price cuts, exposing formulary pressure. Cost-effectiveness models for inclisiran call for an 88% price haircut in China before parity with statin therapy frontiersin.org. Such dynamics reduce fibrate volume where payers enforce step-therapy protocols.

Environmental Curbs on Fluorinated Intermediates Supply Chain

The 2024 EPA rules mandate phasedown of hydrofluorocarbons and close TSCA exemptions for new PFAS, forcing costlier solvent management[3]EPA, “Phasedown of Hydrofluorocarbons,” federalregister.gov. Wastewater studies show fluorinated drugs form up to 75% of extractable organofluorine, intensifying pressure for greener synthesis. Manufacturers lacking alternative chemistries face higher compliance outlays and potential shortages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug: Fenofibrate Dominance Faces Emerging Competition

The fibrate drugs market remains led by fenofibrate, which captured 61.90% of global revenue in 2025, a level equal to the largest fibrate drugs market share across any therapeutic class. This anchor position reflects broad clinical familiarity, once-daily dosing, and robust evidence for triglyceride lowering. Growth now centres on repurposing; LENS data show a 27% decline in diabetic-retinopathy progression, enlarging the addressable base within ophthalmology. Bezafibrate, meanwhile, enjoys the quickest uptake, advancing at a 7.12% CAGR as clinicians value its balanced safety-efficacy profile, especially in metabolic-syndrome cohorts. Gemfibrozil retains a niche role where statin interactions are mitigated, while ciprofibrate and clofibrate shrink in volume following legacy safety concerns.

Continued investment in real-world safety monitoring shapes competitive positioning. FDA adverse-event surveillance flagged 68 signals for rosuvastatin-fenofibrate combinations, 28 of which are absent from current labels, underscoring vigilance needs. That scrutiny benefits bezafibrate’s reputation for lower myopathy risk. RNA-based antagonists, though not yet direct fibrate replacements, spotlight the triglyceride pathway’s clinical weight, keeping the fibrate drugs market essential within multimodal lipid control regimens.

By Product Type: Generic Dominance With Branded Innovation

Generics supplied 74.85% of 2025 volume, reflecting mature chemistry, widespread Active Pharmaceutical Ingredient (API) availability, and aggressive tender pricing, chiefly from South Asian producers. The segment delivers predictable revenue but strained margins. Branded products, however, are set to grow 6.73% annually, buoyed by fixed-dose statin-fibrate combinations and extended-release micro-encapsulation that lifts adherence. Where PPARA genotyping identifies likely responders, premium positioning is increasingly defended—an approach that keeps the fibrate drugs industry anchored in value-based care.

Adoption of continuous-flow manufacturing and higher Good Manufacturing Practice thresholds in emerging markets should uplift overall quality, limiting the risk of product recalls that have periodically dented category trust. As a result, branded players that cultivate supply-chain transparency and pharmacovigilance may outsprint generic rivals despite headline price gaps.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital and retail pharmacies sustained an 84.35% share in 2025 thanks to embedded prescribing pathways and insurance ties. Yet, online pharmacies—supported by e-prescription mandates and telehealth norms established during the pandemic—are scaling at an 11.03% CAGR, the briskest within the fibrate drugs market. Automated refill systems and last-mile logistics enhance treatment continuity for chronic indications requiring daily dosing. Traditional channels respond by integrating click-and-collect services and digital counselling, underlining a migration to hybrid dispensing. This shift aligns with payer objectives to improve adherence metrics and cut cardiovascular readmissions, reinforcing market growth.

Two-way data flow between pharmacies and prescribers also feeds population-health analytics, enabling targeted adherence interventions for patients whose pharmacy claims flag poor refill behaviour. Consequently, digital competence is emerging as a differentiator for marketing teams within the fibrate drugs industry.

Geography Analysis

North America generated 38.20% of 2025 global revenue, anchored by comprehensive reimbursement and clinical guidelines that endorse fibrates for persistent hypertriglyceridemia. Wider access to combination pills further elevates prescribing. Yet, PCSK9 coverage denials affecting nearly one-third of claims expose gaps that fibrates cost-effectively fill. Environmental restrictions raise compliance costs for U.S. producers, but established quality systems mitigate severe disruption. Canada’s public-drug programs and Mexico’s growing private insurance segments both widen access, sustaining regional sales momentum.

Asia-Pacific records the fastest 8.76% CAGR, driven by sizable untreated populations, rising obesity rates, and state incentives for metabolic-drug makers. India’s Production Linked Incentive scheme aims at 2026 roll-out, brightening export prospects and enhancing fibrate drugs market size for regional producers. China’s Strategic National Drug negotiations push price ceilings downward, preserving high volume uptake. Japan and South Korea emphasise triglyceride-specific indices, promoting earlier specialist referral. Australia leverages parallel-import policy to keep formularies cost-competitive, widening patient access.

Europe maintains a balanced outlook with payer scrutiny capping unit pricing but real-world evidence rewarding drugs that show additive cardiovascular benefit. Central and Eastern member states adopt generics aggressively, while Western Europe leans on branded innovations backed by head-to-head data. In the Middle East and Africa, economic diversification plans are raising healthcare budgets, yet uptake remains modest relative to disease prevalence. South America’s macroeconomic fluctuations hobble consistent procurement, though Brazil’s cardiac risk-screening expansions support gradual growth. Collectively, these patterns distribute the fibrate drugs market across a broad economic spectrum, insulating revenue from single-region shocks.

Competitive Landscape

The fibrate drugs market features moderate fragmentation. A cadre of multinational generics houses controls a majority of supply, yet no single entity exceeds the 20% threshold, positioning the market at a competitive equilibrium. Strategic moves in 2024-25 illustrate rivalry on three fronts. First, asset diversification: several incumbents launched fixed-dose rosuvastatin-fenofibrate tablets to head off RNA-drug incursion. Second, geo-expansion: Indian firms acquired Latin American packaging lines to skirt tariff barriers and secure tender bids. Third, technology differentiation: speciality pharma players began bundling PPARA genotype testing kits with premium fenofibrate packs to justify higher reimbursement tiers.

Emergent therapies exert external pressure. Plozasiran and olezarsen, each posting >70% triglyceride reductions in mid-stage trials, may erode fibrate share in severe-hypertriglyceridemia cohorts upon launch. Nevertheless, fibrates retain cost and chronic-safety advantages, especially where payer gatekeeping curbs biologic adoption. Market participants that leverage digital-pharmacy alliances and demonstrate environmental-footprint transparency are best placed to sustain margins in the face of price audits and green-chemistry mandates.

Fibrate Drugs Industry Leaders

Sun Pharmaceutical Industries

Abbott Laboratories

Lupin Ltd

Cipla Ltd

AbbVie Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gilead Sciences presented Livdelzi (seladelpar) Phase III data at EASL 2025, reporting 60% biochemical response rates in patients previously treated with fibrates, and received conditional EU approval for primary biliary cholangitis.

- June 2024: The LENS trial confirmed fenofibrate’s 27% reduction in diabetic-retinopathy progression, redefining its therapeutic scope.

Global Fibrate Drugs Market Report Scope

As per the scope of this report, fibrate drugs are the therapeutics that belong to the class of amphipathic carboxylic acids that lower triglyceride levels in the blood by inhibiting hepatic extraction of free fatty acids, which results in increased activity of endothelial lipoprotein lipase. The Fibrate Drugs market is segmented by Drug Type (Clofibrate, Gemfibrozil, Fenofibrate, and Other Drug Types), Product Type (Branded and Generic), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Online Distribution Channel), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Clofibrate |

| Gemfibrozil |

| Fenofibrate |

| Bezafibrate |

| Ciprofibrate |

| Other Drugs |

| Branded |

| Generic |

| Hospital & Retail Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug | Clofibrate | |

| Gemfibrozil | ||

| Fenofibrate | ||

| Bezafibrate | ||

| Ciprofibrate | ||

| Other Drugs | ||

| By Product Type | Branded | |

| Generic | ||

| By Distribution Channel | Hospital & Retail Pharmacy | |

| Online Pharmacy | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the fibrate drugs market?

The global fibrate drugs market size is USD 3.97 billion in 2026 and is projected to reach USD 5.11 billion by 2031.

Which drug holds the largest share of sales?

Fenofibrate leads with 61.90% of 2025 revenue, anchored by extensive clinical use and expanding ophthalmic indications.

Why is Asia-Pacific growing fastest?

High metabolic-disease prevalence, rising healthcare budgets, and capacity expansion in India and China drive an 8.76% CAGR for the region.

How are online pharmacies influencing market dynamics?

They are the fastest-advancing channel at an 11.03% CAGR, improving adherence through automated refills and home delivery.

What new therapies may compete with fibrates?

RNA-based agents such as plozasiran and olezarsen achieved superior triglyceride cuts in 2024 trials, potentially challenging fibrate use in severe cases.

How is precision medicine affecting fibrate adoption?

PPARA genotyping identifies responders, enabling targeted therapy and supporting premium pricing for differentiated formulations.

Page last updated on: