Thermally Conductive Filler Dispersants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 339.53 Million |

| Market Size (2031) | USD 481.13 Million |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

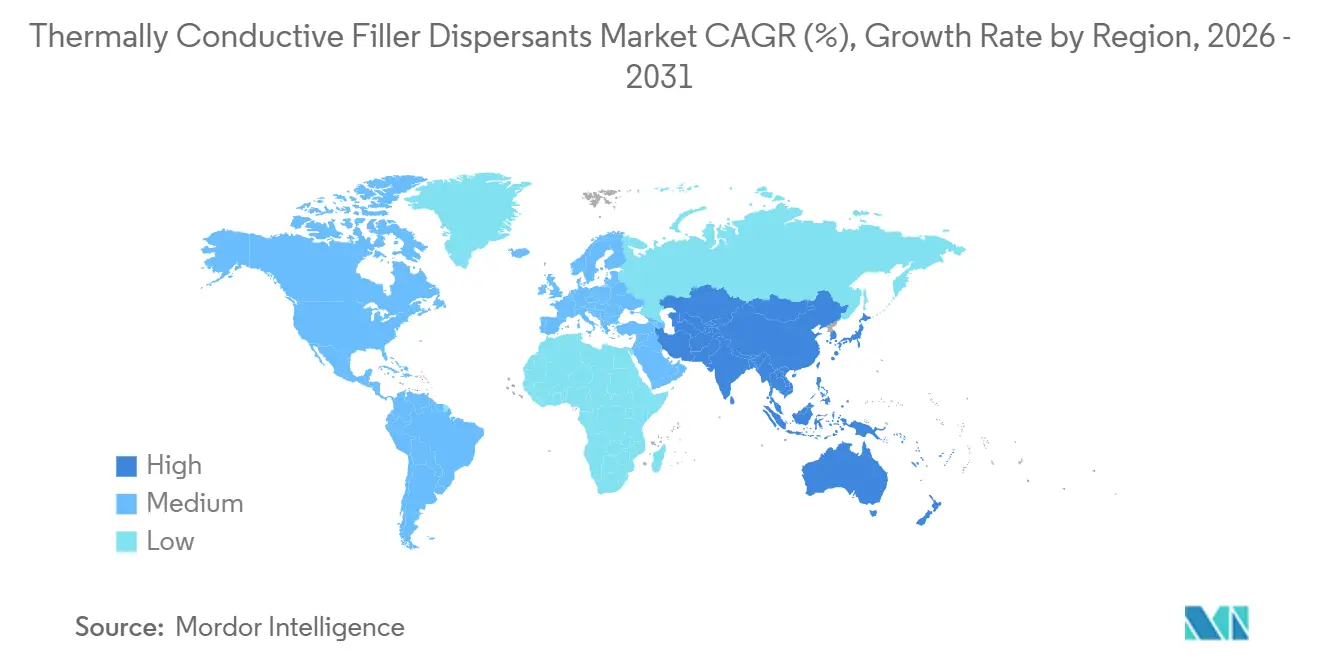

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermally Conductive Filler Dispersants Market Analysis by Mordor Intelligence

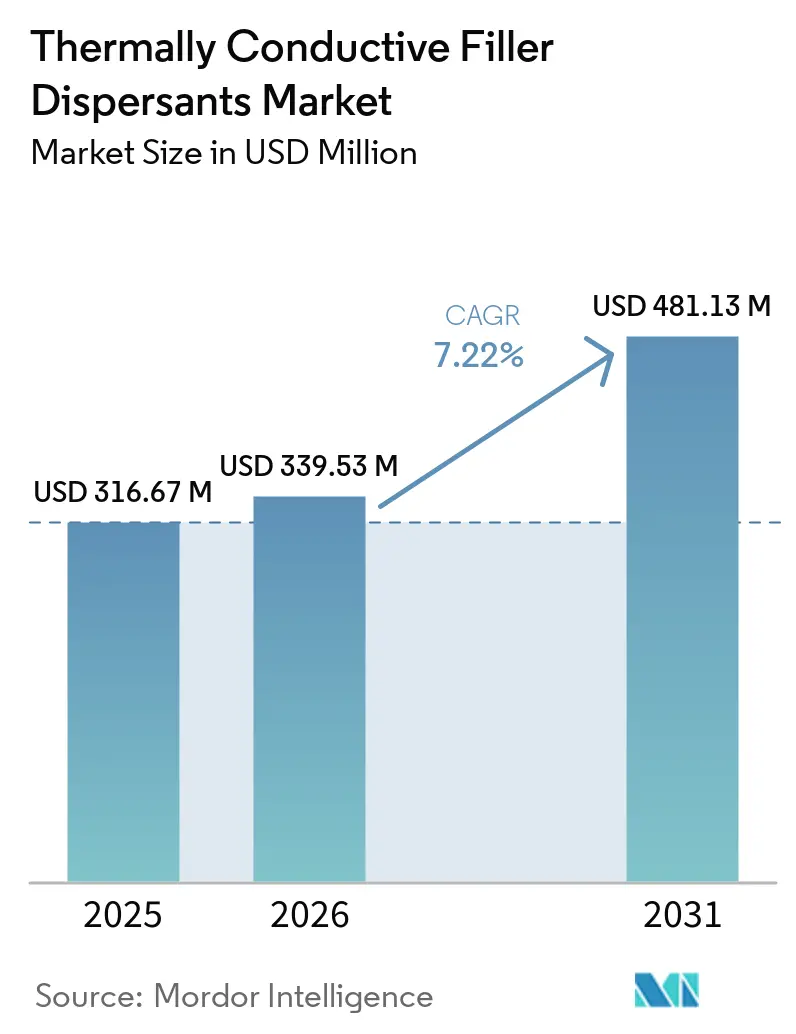

The Thermally Conductive Filler Dispersants Market size was valued at USD 316.67 million in 2025 and is estimated to grow from USD 339.53 million in 2026 to reach USD 481.13 million by 2031, at a CAGR of 7.22% during the forecast period (2026-2031). Rising heat-flux densities in EV battery packs and semiconductor hotspots, stricter PFAS regulations, and the expanding use of hybrid boron-nitride–graphene networks are altering cost-performance dynamics for formulators. The focus remains on stabilizing ceramic loadings above 80 vol% without excessive viscosity while transitioning away from fluorinated surfactants that previously enabled ultrahigh solids. In the Asia-Pacific region, adoption is driven by the use of cost-effective silane coupling agents and the rapid deployment of liquid-cooling infrastructure. Meanwhile, Western manufacturers are maintaining margins through ISO 22007-2 certification, which can delay product launches by up to 12 weeks. Across the value chain, suppliers leveraging recyclable chemistries and dual-filler architectures are securing design wins for 800 V drivetrains and 700 W AI accelerators, ensuring long-term demand for next-generation gap fillers.

Key Report Takeaways

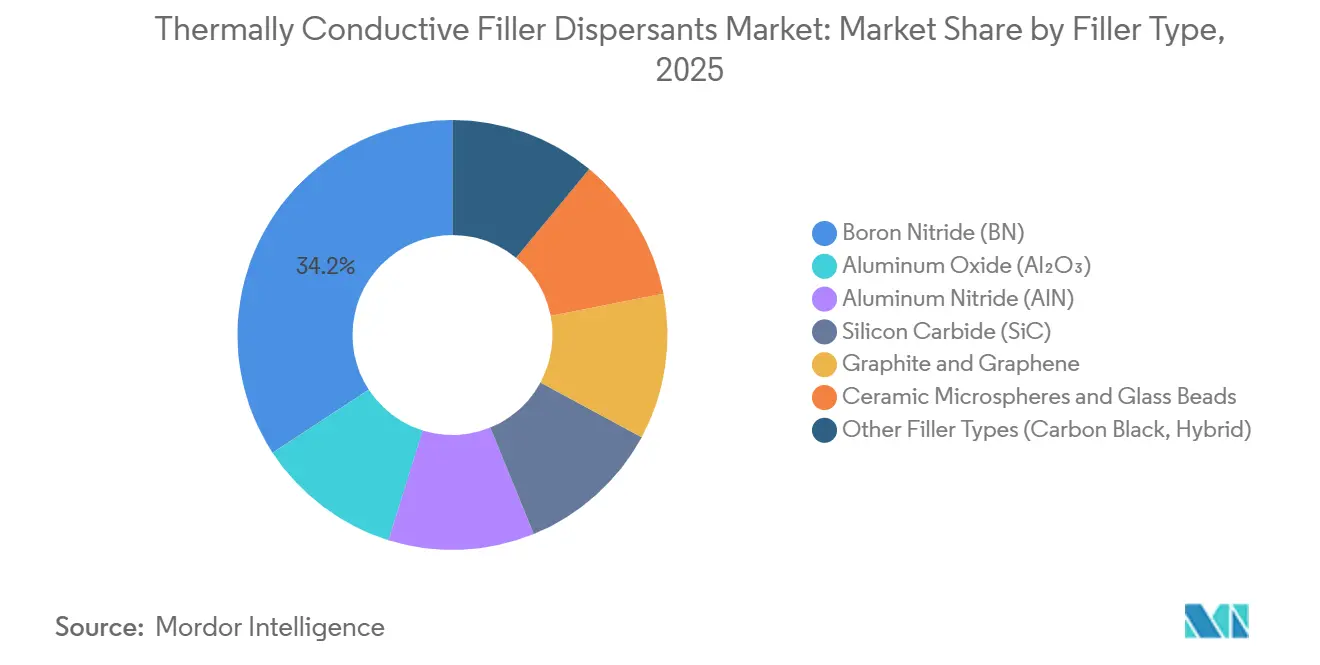

- By filler type, boron nitride commanded 34.22% of the thermally conductive filler dispersants market share in 2025, whereas graphite and graphene are forecast to expand at a 7.33% CAGR through 2031.

- By formulation, liquid dispersions captured 46.36% of the thermally conductive filler dispersants market share in 2025, yet paste and gel systems are forecast to expand at a 8.02% CAGR through 2031.

- By application, thermal interface materials accounted for a 39.34% of the thermally conductive filler dispersants market share in 2025 and are advancing at an 8.02% CAGR through 2031.

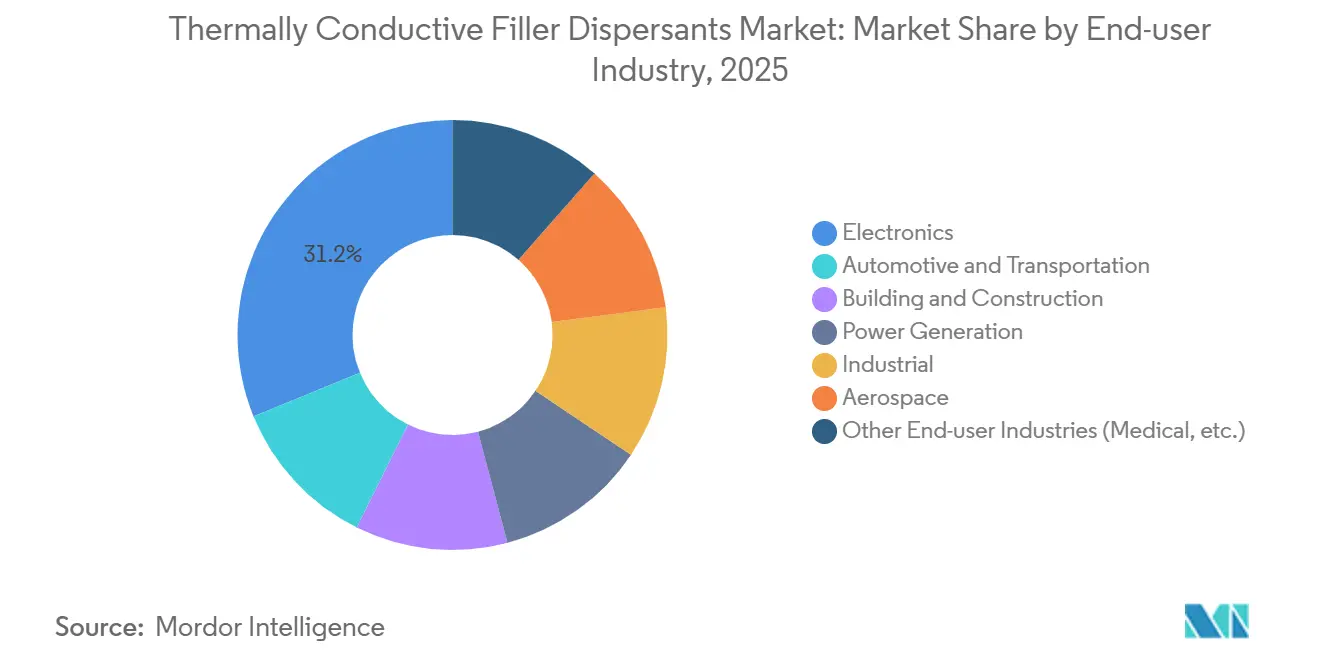

- By end-user industry, electronics led with 31.18% of the thermally conductive filler dispersants market share in 2025, while automotive and transportation is projected to grow fastest at an 8.11% CAGR through 2031.

- By geography, Asia-Pacific led with 44.45% of the thermally conductive filler dispersants market share in 2025 and is advancing at an 8.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thermally Conductive Filler Dispersants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV battery and power-module heat-flux density | +2.1% | APAC core (China, South Korea, Japan), spill-over to North America and Europe | Medium term (2-4 years) |

| Semiconductor node-shrink driven hotspot management | +1.8% | Global, concentrated in Taiwan, South Korea, United States (Arizona, Texas) | Short term (≤ 2 years) |

| Safety-driven shift to low-VOC, halogen-free dispersants | +0.9% | Europe (REACH), North America (EPA Safer Choice), APAC coastal cities | Medium term (2-4 years) |

| OEM decarbonization targets favor recyclable dispersant chemistries | +0.7% | Europe (automotive OEMs), North America (Scope 3 reporting), Japan | Long term (≥ 4 years) |

| Hybrid BN + graphene filler networks lowering dispersant loadings | +0.5% | APAC manufacturing hubs (Shenzhen, Suzhou), North America R&D centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in EV Battery and Power-Module Heat-Flux Density

Liquid and immersion cooling are now dominant in 300 Wh/kg battery packs, where local heat fluxes exceed 50 W/cm² at cell tabs. To maintain 5 W/m·K bond lines within 0.3 mm gaps, products like Evonik’s ORTEGOL DA 801 and DuPont’s BETAMATE 2090 utilize polyurethane-compatible dispersants that accommodate ±0.2 mm z-axis expansion while eliminating the need for energy-intensive oven curing. Chinese integrators, such as Shenzhen Feirongda, collaborate with CATL to co-design vapor-chamber assemblies, embedding dispersants within complete thermal modules to capture margins. However, as immersion cooling becomes more widespread, residual ionic impurities above 10 ppm remain a challenge, as they reduce dielectric-fluid resistivity below 1 GΩ·cm, prompting a shift toward ultrapure filler grades.

Semiconductor Node-Shrink Driven Hotspot Management

3D-stacked high-bandwidth memory and 200 W CPUs introduce up to four TIM interfaces per package, increasing thermal resistance by 0.15 K cm²/W per layer unless sub-50 nm filler spacing is maintained. Henkel’s Bergquist TLF 6500 CGel-SF and Infineon’s indium-alloy attach guidelines require dispersants that stabilize 85 vol% ceramic loadings within 25 µm bond lines while preventing sedimentation at 180 °C reflow temperatures. These advancements in packaging are expected to create an incremental addressable market of USD 85 million for high-solids paste formulations by 2026.

Safety-Driven Shift to Low-VOC, Halogen-Free Dispersants

The EPA’s January 2025 TRI expansion, which added 189 PFAS compounds to mandatory reporting, has led to the removal of perfluoropolyether surfactants that previously reduced surface tension to 18 mN/m[1]Environmental Protection Agency, “Toxic Release Inventory PFAS Expansion,” epa.gov. Evonik’s TEGO Dispers 761 W achieves UL 94 V-0 compliance without brominated additives by incorporating reactive phosphorus groups. However, water’s higher surface tension of 72 mN/m necessitates a 30% increase in dispersant dosage, raising costs by USD 1.8–2.4 per kg. Additionally, European REACH Annex XVII halogen bans introduce six-to-nine-month compliance cycles, favoring established players with comprehensive toxicology dossiers.

OEM Decarbonization Targets Favor Recyclable Chemistries

Automakers face pressure to reduce life-cycle emissions by 30%–50% by 2030 under Scope 3 mandates. Room-temperature-curing BETAFORCE adhesives eliminate 180 °C oven phases, saving 2.4 kWh per vehicle and facilitating disassembly for battery pack recycling. Thermoplastic BN-polypropylene composites retain 92% of their properties after three melt cycles, outperforming epoxy systems, which drop to 60%. However, only 28% of surveyed suppliers currently offer TIMs with recyclable matrices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer/filler compatibility limits in high-viscosity systems | -0.8% | Global, acute in North America and Europe (stringent rheology specs) | Short term (≤ 2 years) |

| PFAS phase-out tightening specialty-solvent availability | -0.6% | North America (EPA SNUR), Europe (REACH restriction), Japan (CSCL) | Medium term (2-4 years) |

| Shear-induced damage to high-aspect-ratio fillers during compounding | -0.5% | APAC manufacturing hubs (high-speed production lines), North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Polymer–Filler Compatibility Limits in High-Viscosity Systems

At ceramic loadings of 80 vol%, steric stabilization fails as inter-particle gaps shrink below twice the dispersant’s hydrodynamic radius. Bottlebrush polysiloxanes with octadecyl grafts achieve 87.8 vol% alumina and 8.181 W/m·K but are 40% more expensive than linear PDMS, limiting their application to AI accelerators. Compatibility issues arise during reliability tests, where amine-terminated dispersants migrate, reducing conductivity by 18% after 500 thermal cycles. In contrast, phosphonate variants retain 96% conductivity.

PFAS Phase-Out Tightening Specialty-Solvent Availability

The December 2024 SNUR on 329 inactive PFAS compounds has restricted the use of perfluoropolyether surfactants, reducing maximum alumina loadings from 83 vol% to 71 vol% and lowering conductivity from 9.2 W/m·K to 7.4 W/m·K in trials. Disposal costs for PFAS-laden waste now range from USD 4.5 to 6.8 per kg, prompting a shift toward water-based solutions like AERODISP W7330 that still requires 72 hours of drying, tying up working capital[2]Evonik Industries, “AERODISP W7330 Technical Bulletin,” evonik.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filler Type: BN Dominance Challenged by Graphene Scalability

Boron nitride secured 34.22% of the thermally conductive filler dispersants market share in 2025, attributed to its 300 W/m·K through-plane conductivity and 10¹³ Ω·cm resistivity. However, graphite and graphene, expanding at a 7.33% CAGR through 2031, are challenging this position as Chinese synthetic-graphite capacity increases by 4 million m² annually in Vietnam, benefiting from 35% lower labor costs. Aluminum oxide remains critical for cost-sensitive applications targeting 3–5 W/m·K, with bottlebrush polysiloxane dispersants reducing the performance gap to BN at one-fifth of the material cost.

Silicon carbide, with its 120 W/m·K conductivity, is the preferred choice for mechanical reinforcement in under-hood electronics, although its 950 °C oxidation step adds USD 8–12 per kg in processing costs. Moisture-sensitive aluminum nitride remains a niche material but benefits from Parylene-C passivation, which retains 97% conductivity after boiling-water immersion, enabling aerospace qualification pipelines.

By Formulation: Paste Systems Gain as Automation Demands Thixotropy

Liquid dispersions held 46.36% of the thermally conductive filler dispersants market in 2025, supported by viscosities below 15 Pa·s that allow jetting into sub-50 µm bond lines. However, paste and gel systems are growing at an 8.02% CAGR through 2031, driven by data-center operators' need for materials that can withstand ±0.5 mm stack tolerances without pump-out. Bergquist TGF 10000 demonstrates that thixotropy can coexist with thermal performance, maintaining 10 W/m·K and less than 5% thickness drift over 1,000 cycles.

Powder additives support thermoplastic compounders, while gel TIMs offer Shore 00 hardness of 60–70, conforming to irregular geometries. Screen printing reduces labor costs by USD 0.32 per unit, even after accounting for the 18% dose premium of thixotropic modifiers. The solids content ceiling remains at 85 vol%; exceeding this limit results in yield stress issues during dispensing. Bottlebrush-stabilized pourable liquids surpass this threshold but are limited to AI servers, where USD 28 per kg dispersant costs are justified by 700 W chip loads.

By Application: Thermal Interface Materials Lead the Segment

Thermal interface materials commanded 39.34% of the thermally conductive filler dispersants market size in 2025 and are advancing at an 8.02% CAGR through 2031 as HBM3E stacks increase the TIM layer counts. Electrically insulating compounds meet 15 kV/mm dielectric specifications for 800 V inverters, while gap fillers with 10 W/m·K accommodate ±0.5 mm tolerances in liquid-cooled servers. Encapsulation and underfills are expanding to protect 2.5D interposers from moisture and warpage.

Potting compounds for wind-turbine inverters and aerospace modules extend service life to 25 years at 150 °C, creating recurring aftermarket demand. Phase-change materials for satellite thermal storage and sub-100 µm conductive films for flexible devices represent an emerging 12% revenue segment, which could double by 2031 as wearables proliferate.

By End-user Industry: Automotive Electrification Outpaces Electronics

Electronics retained 31.18% share in 2025, yet automotive and transportation are advancing at an 8.11% CAGR through 2031. Chinese vendors gain share by bundling dispersants with vapor-chamber assemblies that achieve 60% gross margins. Industrial drives, LEDs, and building HVAC systems remain cost-sensitive, capping conductivity at 2–4 W/m·K with alumina fillers. Aerospace and medical applications demand silicone-free, MIL-STD-qualified TIMs priced up to USD 180 per kg for zero outgassing and cytotoxicity compliance.

Geography Analysis

Asia-Pacific generated 44.45% of 2025 revenue and is set to grow at an 8.38% CAGR through 2031 on the back of China’s AI-server build-outs and South Korea’s specialty silicone expansions. Shenzhen Feirongda reported RMB 5.031 billion (USD 693 million) 2024 revenue and greater than 110% 2025 profit growth from partnering with Huawei and BYD. China’s Siquan New Materials, running 97.47% utilization, is adding 4 million m² synthetic-graphite film capacity in Vietnam to leverage 35% cheaper labor. South Korea, buoyed by Wacker and Denka investments, positions Ulsan and Iksan as hubs for BN and silicone TIM innovation.

In North America, DuPont’s Battery Technology Center in Michigan aligns with Inflation Reduction Act sourcing rules, while Henkel’s USD 30 million Brandon expansion will raise Bergquist output 40% by 2027 to serve hyperscale data centers using 700 W GPUs. Canada’s demand is tied to electric-bus mandates, whereas Mexico supplies cost-optimized alumina TIMs to Tier 2 automotive plants.

Europe is anchored by strict REACH rules, pushing suppliers toward low-VOC water-based dispersions even as high energy costs squeeze margins. Dow is evaluating UK and German siloxane cutbacks but keeps its Alberta Path2Zero cracker on schedule for 2029 ethylene feedstock integration. Meanwhile, OEM decarbonization pledges accelerate recyclable thermoplastic TIM adoption, giving an opening to bio-based chemistries.

South America and Middle-East and Africa collectively hold lower shares. Brazil’s flex-fuel hybrids and Saudi Aramco’s petrochemical growth spur niche TIM demand, but limited local filler production continues to hinder rapid uptake.

Competitive Landscape

The thermally conductive filler dispersants market remains moderately fragmented. Henkel’s 60-day cadence launching Loctite TCF 14001 (14.5 W/m·K) and Bergquist TGF 10000 (10 W/m·K) underscores vertical integration in surface-treated fillers. Western leaders defend margins through ISO 22007-2 testing backlogs that add 8–12 weeks to customer qualifications. Chinese firms compete on cost by integrating silane synthesis and vapor-chamber assembly; Shenzhen Feirongda’s dispersant-plus-module model elevates gross margins to 60%.

Emerging disruptors include Siquan New Materials, scaling graphene film in Vietnam, and NAiEEL, introducing boron-nitride nanotubes for hybrid percolation pathways. Technology differentiation now pivots on bottlebrush versus linear dispersant architectures. Evonik’s PMVS-ODT outperforms linear PDMS by 79.9% in conductivity but costs 40% more, targeting AI accelerators and aerospace. Barriers to entry rise as UL 94 V-0 and IEC 62368-1 dossiers extend development timelines, advantaging incumbents with legacy compliance files.

Strategic expansion continues: Wacker’s double-digit-million-euro specialty silicone investment in Ulsan, Denka’s stake in NAiEEL, and Henkel’s Brandon capacity boost exemplify geographic hedging against trade frictions. White-space remains in recyclable bio-based dispersants and dual-filler chemistries, areas where only one-third of profiled players have published patents.

Thermally Conductive Filler Dispersants Industry Leaders

DuPont

3M

Dow

Wacker Chemie AG

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Henkel AG & Co. KGaA entered into a strategic partnership with Smart High Tech (SHT) to develop and commercialize graphene-reinforced thermal interface materials (TIMs). This collaboration contributed to advancements in the thermally conductive filler dispersants market by enhancing material performance.

- March 2025: Evonik Industries AG launched ORTEGOL DA 801, a dispersant designed for polyurethane (PU)-based thermal interface materials. It enabled ultra-high filler loadings of up to 90 wt.-% while reducing viscosity, a critical factor in producing high-performance EV battery adhesives.

Global Thermally Conductive Filler Dispersants Market Report Scope

Thermally conductive filler dispersants are additives specifically designed to evenly distribute conductive fillers, such as alumina or metal oxides, within polymer matrices. This ensures efficient heat transfer and prevents hotspots in electronic components. These dispersants improve the performance of thermal interface materials (TIMs), automotive batteries, and LED applications by reducing viscosity and enhancing filler loading.

The Thermally Conductive Filler Dispersants Market is segmented into filler type, formulation, application, end-user industry, and geography. By filler type, the market is segmented into boron nitride (BN), aluminum oxide (Al₂O₃), aluminum nitride (AlN), silicon carbide (SiC), graphite and graphene, ceramic microspheres and glass beads, and other filler types (carbon black, hybrid). By formulation, the market is segmented into liquid dispersions, powder additives, and paste/gel systems. By application, the market is segmented into thermal interface materials (TIMs), electrically-insulating compounds, thermal greases and adhesives, gap fillers and potting compounds, encapsulation and underfills, and other applications. By end-user industry, the market is segmented into electronics, automotive and transportation, building and construction, power generation, industrial, aerospace, and other end-user industries (medical, etc.). The report also covers the market size and forecasts for thermally conductive filler dispersants in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Boron Nitride (BN) |

| Aluminum Oxide (Al₂O₃) |

| Aluminum Nitride (AlN) |

| Silicon Carbide (SiC) |

| Graphite and Graphene |

| Ceramic Microspheres and Glass Beads |

| Other Filler Types (Carbon Black, Hybrid) |

| Liquid Dispersions |

| Powder Additives |

| Paste/Gel Systems |

| Thermal Interface Materials (TIMs) |

| Electrically-Insulating Compounds |

| Thermal Greases and Adhesives |

| Gap Fillers and Potting Compounds |

| Encapsulation and Underfills |

| Other Applications |

| Electronics |

| Automotive and Transportation |

| Building and Construction |

| Power Generation |

| Industrial |

| Aerospace |

| Other End-user Industries (Medical, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Filler Type | Boron Nitride (BN) | |

| Aluminum Oxide (Al₂O₃) | ||

| Aluminum Nitride (AlN) | ||

| Silicon Carbide (SiC) | ||

| Graphite and Graphene | ||

| Ceramic Microspheres and Glass Beads | ||

| Other Filler Types (Carbon Black, Hybrid) | ||

| By Formulation | Liquid Dispersions | |

| Powder Additives | ||

| Paste/Gel Systems | ||

| By Application | Thermal Interface Materials (TIMs) | |

| Electrically-Insulating Compounds | ||

| Thermal Greases and Adhesives | ||

| Gap Fillers and Potting Compounds | ||

| Encapsulation and Underfills | ||

| Other Applications | ||

| By End-user Industry | Electronics | |

| Automotive and Transportation | ||

| Building and Construction | ||

| Power Generation | ||

| Industrial | ||

| Aerospace | ||

| Other End-user Industries (Medical, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the thermally conductive filler dispersants market?

The thermally conductive filler dispersants market stands at USD 339.53 million in 2026 and is projected to reach USD 481.13 million by 2031.

Which region shows the fastest expansion for thermally conductive filler dispersants through 2031?

Asia-Pacific is advancing at an 8.38% CAGR through 2031, underpinned by China’s data-center liquid-cooling build-out and South Korea’s specialty-silicone investments.

Which application generated the highest revenue in 2025?

Thermal interface materials account for the largest revenue share at 39.34% in 2025.

How are PFAS regulations influencing product design?

EPA rules phasing out fluorinated surfactants are accelerating the switch to low-VOC, halogen-free, and bio-based dispersants, though they raise formulation costs and lengthen drying times.

Page last updated on: