Thermal Spray Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.53 Billion |

| Market Size (2031) | USD 11.65 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thermal Spray Coatings Market Analysis by Mordor Intelligence

Thermal Spray Coatings Market size in 2026 is estimated at USD 9.53 billion, growing from 2025 value of USD 9.15 billion with 2031 projections showing USD 11.65 billion, growing at 4.11% CAGR over 2026-2031. Demand is fueled by hybrid additive-plus-spray repair methods that extend component life, widening medical applications that require bio-active surfaces, and aerospace programs that rely on advanced thermal-barrier stacks for higher engine temperatures. Growth also reflects rising adoption of cold-spray EMI shielding in e-mobility electronics, while digitalized “smart” spray cells are tightening process control and shortening development cycles. Regionally, Asia-Pacific’s manufacturing build-out is closing the gap with North America, even as tightening VOC rules in the United States accelerate the shift to low-emission electric-energy spray routes.

Key Report Takeaways

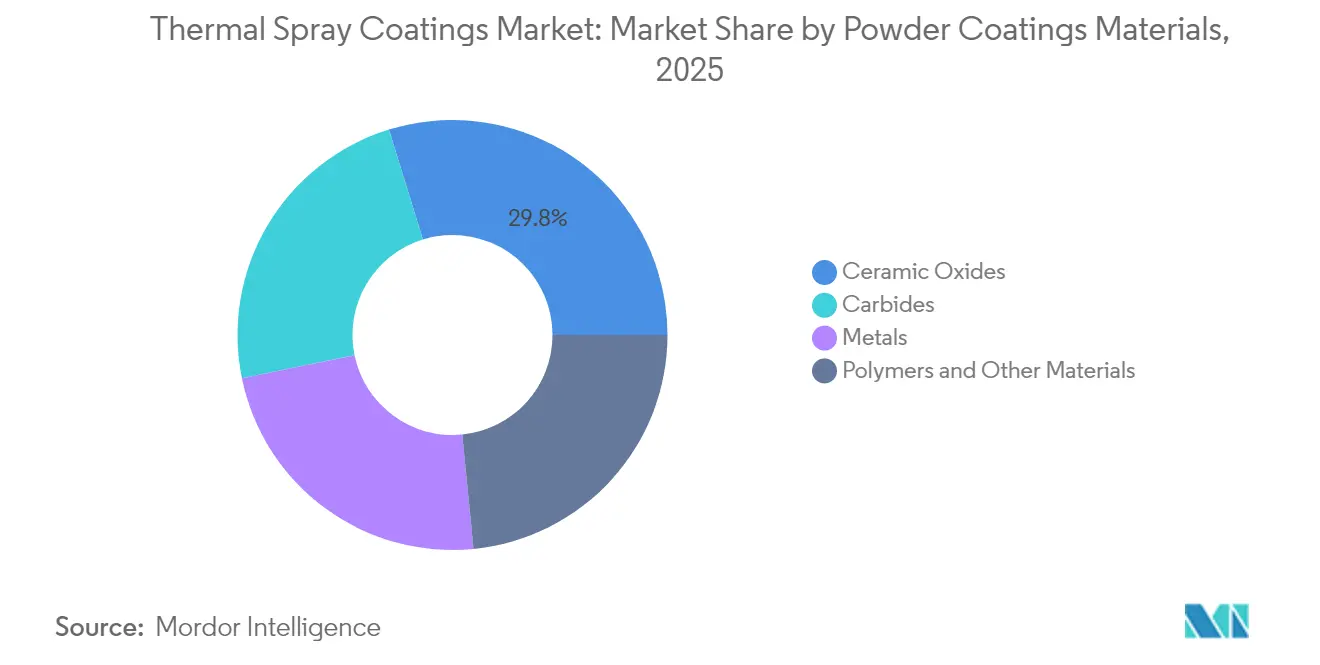

- By powder material, ceramic oxides led with 29.78% revenue share in 2025, while also posting the fastest 4.91% CAGR to 2031.

- By process, the combustion route held 61.92% of the thermal spray coating market share in 2025; electric-energy methods are projected to grow at 5.19% CAGR through 2031.

- By end-user industry, aerospace accounted for 31.55% of the thermal spray coating market size in 2025, whereas industrial gas turbines are poised for the highest 5.79% CAGR.

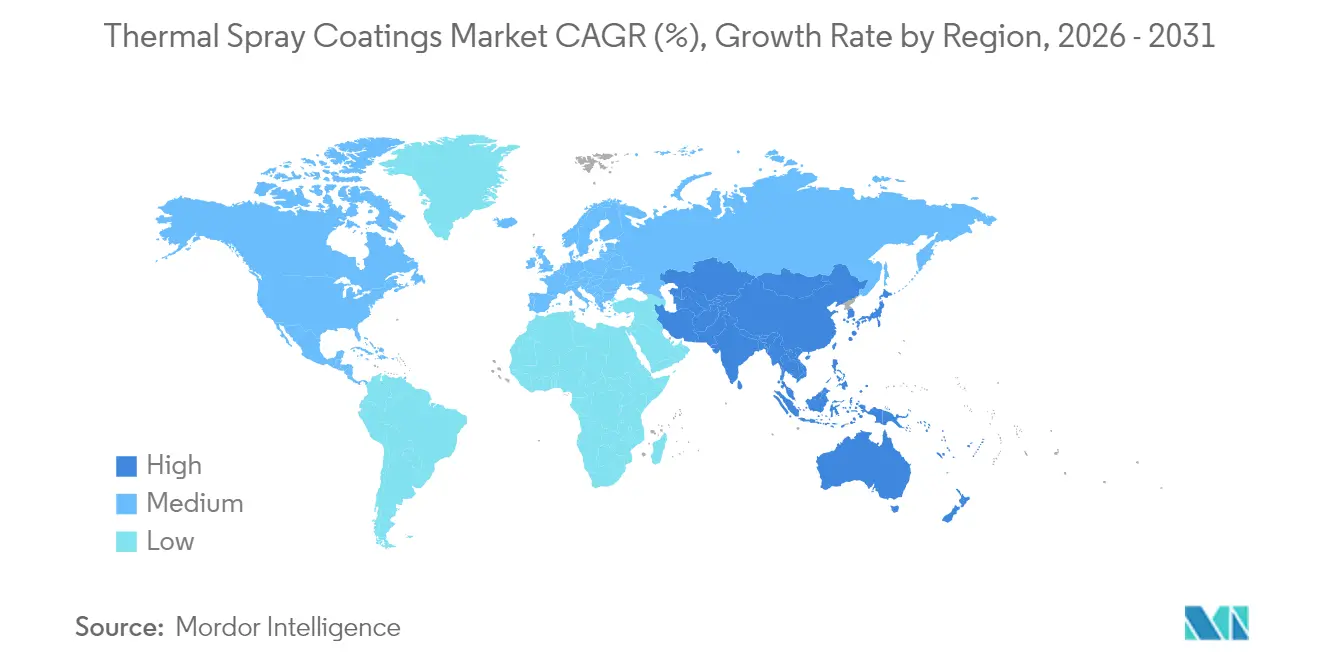

- By geography, North America commanded 33.86% share of the thermal spray coating market in 2025, but Asia-Pacific is forecast to register a 6.03% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Thermal Spray Coatings Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased usage in medical implants & prosthetics | +0.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing adoption in aerospace turbine & air-frame parts | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rising preference for ceramic-oxide barrier coatings | +0.9% | Global, led by industrial regions | Medium term (2-4 years) |

| Cold-spray EMI shielding for e-mobility components | +0.7% | Asia-Pacific core, spill-over to North America & Europe | Short term (≤ 2 years) |

| Additive-manufacturing repair of super-alloy parts | +1.0% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Usage in Medical Implants and Prosthetics

Medical-grade plasma-sprayed hydroxyapatite continues to be the only FDA-cleared coating technology for mass-produced orthopedic implants, and recent work with β-phase Ti alloys is reducing elastic-modulus mismatch to bone. High-power impulse magnetron sputtering and HVOF overlays are now being combined in layered constructs that supply antibacterial surfaces without compromising osseointegration. As 3-D printed lattice implants scale up, spray-applied bio-ceramic finishes allow patient-specific geometries to move through qualification more quickly, though regulators are still finalizing test protocols. Coating providers able to certify repeatable roughness and phase composition are winning new multi-year supply contracts.

Growing Adoption in Aerospace Turbine & Air-Frame Parts

Engine primes are raising turbine inlet temperatures and demanding smart factories that deliver tight thickness windows on every coupon. Digitalized spray cells developed by Oerlikon and MTU Aero Engines now employ closed-loop plume diagnostics that cut rework rates by 25%[1]Oerlikon Group, “Smart Thermal Spray Factories,” oerlikon.com. Cold-spray has become a frontline depot-repair tool, allowing aluminum flight-control housings and magnesium gearbox covers to be rebuilt without heat-affected distortion. Multilayer ceramic-oxide barrier stacks with oxidation-resistant inter-layers are extending engine overhaul intervals, enabling airlines to keep narrow-body fleets in service longer.

Rising Preference for Ceramic-Oxide Barrier Coatings

Nanostructured yttria-stabilized zirconia produced by suspension plasma spray is delivering double-digit gains in thermal-cycling life versus conventional air-plasma coatings[2]European Ceramic Society, “Nanostructured YSZ Coatings via SPS,” european-ceramic-society.org. Functionally graded layers now mitigate thermal-expansion mismatch, and rare-earth dopants are pushing endurance above today’s 1 200 °C ceiling. Gas-turbine OEMs are pairing these coatings with closed-loop cooling schemes, yielding higher firing temperatures and better combined-cycle efficiency. As hydrogen-capable turbines enter demonstration, the materials window for hot-section barrier coatings will widen further.

Cold-Spray EMI Shielding for E-Mobility Components

Battery-electric vehicles require lightweight, high-performance EMI shielding across battery packs and control modules. Dense Cu-Zn cold-spray coatings achieve 80 dB attenuation at 100 µm thickness with negligible substrate heating, which allows direct metallization of polymer housings. Asian tier-1 suppliers are already shipping cold-sprayed enclosures in mass-production programs, and North American automakers have launched pilot lines to localize supply. Integration with in-line machining creates a one-step structural-plus-shielding route, trimming takt times and scrap.

Restraints Impact Analysis of Thermal Spray Coatings Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reliability & coating-quality repeatability issues | -0.6% | Global, particularly in high-precision applications | Medium term (2-4 years) |

| Tightening VOC / dust-emission regulations | -0.9% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| Critical-powder supply volatility (WC, rare carbides) | -0.7% | Global, with Asia-Pacific most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reliability & Coating-Quality Repeatability Issues

Large OEMs now specify statistical process windows that smaller job shops struggle to meet. Particle size variance, plume dynamics, and substrate pre-heat all influence oxide content and porosity, which in turn dictate in-service wear. Automated vision and inline acoustic sensors are helping detect off-nominal conditions, but integration costs remain high for low-volume applications. Without global standards on real-time monitoring, qualification cycles lengthen, especially in aerospace and medical device programs.

Tightening VOC / Dust-Emission Regulations

The California Air Resources Board is assessing total metal particulate emissions from thermal spray booths and may impose capture-efficiency thresholds above 98%. The European Union’s newly published BAT conclusions for surface treatment with organic solvents slash VOC limits and mandate advanced filtration by 2027. Compliance requires high-energy plasma systems using inert shrouds or water-borne binders, driving capital upgrades across legacy lines. Operators who adopt electric-energy routes see double benefits of lower exhaust volumes and easier permitting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Thermal Spray Coatings Market Segment Analysis

By Powder Coating Materials:

Ceramic Oxides Sustain LeadershipCeramic oxides recorded 29.78% of 2025 revenue and will grow fastest at 4.91% CAGR. This dominance arises from outstanding high-temperature stability and bio-compatibility, making oxides the default for turbine, medical, and hydrogen infrastructure projects. Carbide blends follow for extreme wear tasks on oil-and-gas valves and mining tools. Metals such as Ni-Cr-Mo alloys serve corrosion defense of marine structures, while polymer-based overlays target electronics where dielectric properties matter. Nanostructured oxides fabricated via suspension plasma spray tighten thermal-cycling life and are unlocking future propulsion architectures. Manufacturers combining rare-earth-doped zirconia with functionally graded bond coats now market 50 000-hour durability guarantees, lifting the thermal spray coating market perception from protective to performance-enabling.

New powder atomization methods are also trimming tungsten carbide supply risk. Several Asian plants have begun recycling hard-metal scrap into agglomerated WC-Co feedstock, lessening exposure to Chinese primary tungsten. At the same time, hybrid spark-plasma-sintered rod stock is widening the choice of feed materials. These shifts will strengthen the thermal spray coating market by easing raw-material cost swings and opening the door to localized powder hubs.

By Process:

Electric-Energy Routes Gain MomentumCombustion guns held 61.92% share in 2025 thanks to low equipment cost and field portability. Yet plasma, arc, and induction systems together will post a 5.19% CAGR as customers demand finer microstructure control and lower emissions. Induction plasma torches now handle feed rates above 80 kg/h, supporting large-area cladding on wind-tower flanges. High-velocity oxygen fuel (HVOF) remains the go-to for carbide overlays on pump sleeves, delivering <1% porosity without melting carbides. Cold-spray’s solid-state impact bonding is carving out new business in aerospace repair and electric-vehicle EMI shielding, though capex remains twice that of classic HVOF sets. Net-shape additive builds followed by in-situ spray finishing illustrate how hybrid cells are changing the economics of repair. These process innovations reinforce the thermal spray coating market trajectory toward smarter, greener production lines.

By End-User Industry:

Energy-transition demand reshapes segment prioritiesAerospace commanded 31.55% of the thermal spray coating market share in 2025, reflecting the sector’s reliance on multilayer ceramic-oxide barriers that enable hotter turbine inlet temperatures and lower fuel burn. Engine primes are integrating smart factory spray cells that cut rework rates and certify every coupon in real time, which is accelerating line-side adoption of advanced coatings for rotating and hot-section parts. Naval and commercial aviation depots now rebuild magnesium and aluminum housings with cold-spray, a solid-state process that has restored more than 400 flight-critical components without heat-affected failures, saving millions in part replacement costs.

Industrial gas turbines form the fastest-growing customer base at 5.79% CAGR through 2031, driven by grid operators who need flexible, hydrogen-capable peaking units and combined-cycle plants with improved thermal efficiency. Hybrid thermal-barrier stacks that pair rare-earth-doped zirconia with cooling-air optimization are raising firing temperatures, boosting output, and expanding the thermal spray coating market size for energy producers. Automotive programs use arc-sprayed Fe-Cr-Al or plasma-sprayed Al-Si cylinder liners to cut friction and reduce fuel use by 2-4% in both diesel and gasoline engines. Electronics demand is climbing as cold-sprayed Cu-Zn EMI shields replace heavier stamped boxes in battery packs, while medical-device OEMs continue to specify plasma-sprayed hydroxyapatite as the only FDA-cleared orthopedic coating. Power-generation and oil-and-gas operators rely on HVOF or arc-sprayed Ni-based overlays to resist hot corrosion and chloride attack on boiler tubes and offshore structures, extending maintenance intervals well beyond uncoated carbon steel benchmarks.

Geography Analysis

North America Thermal Spray Coatings Market

North America led with 33.86% revenue in 2025 on the back of entrenched aerospace, defense, and medical device ecosystems. FAA-class repair shops now rely on cold-spray to redeposit material on magnesium gearboxes, avoiding costly part replacement, while the Department of Energy funds oxide-coating research for hydrogen-ready turbines. California’s air-quality probes add compliance uncertainty, but the region’s first-mover advantage in smart spray cells should preserve leadership during the forecast window.

APAC Thermal Spray Coatings Market

Asia-Pacific is projected to grow fastest at 6.03% CAGR as automotive electrification, consumer-electronics capacity, and gas-turbine build-outs surge. Chinese powder recyclers already supply carbide feedstock to local coaters, hedging tungsten risks identified by USGS. Japanese semiconductor plants are scaling plasma-resistant alumina coatings for sub-5 nm etch chambers, while Indian railways specify arc-sprayed steel overlays on high-speed track components. These projects illustrate how the thermal spray coating market is embedding itself across the region’s manufacturing spectrum.

EMEA Thermal Spray Coatings Market

Europe shows steady progress as tougher VOC caps push operators toward closed-loop plasma booths and water-borne binders. Offshore wind farms in the North Sea now specify Al-Zn thermally sprayed sacrificial anodes on monopile interiors, lengthening service life beyond 25 years. The European Commission’s “Fit-for-55” package indirectly boosts demand for efficiency-raising barrier coatings on industrial gas turbines. Middle East and Africa remain niche today but will see higher uptake as refinery revamps and desalination plants pursue long-life corrosion shields.

Competitive Landscape

The market is moderately consolidated around a core of integrated solution providers. Oerlikon Metco, Sulzer, and Praxair Surface Technologies operate global powder-to-service portfolios, while mid-sized specialists focus on regional wear or biomedical niches. Oerlikon’s 2024 launch of an AI-assisted spray cell halves parameter-setup time and has been adopted by MTU Aero Engines for scalable, serialized turbine manufacturing. Sulzer invested in on-site spray booths at gas-compressor OEM plants, cementing long-term maintenance contracts.

M&A remained active: Aalberts’ purchase of Steel Goode Products in October 2024 expanded its southern U.S. footprint by adding hard-chromium replacement capabilities. Patent filings reveal new carbide-graphene blends targeting brake-disc wear, signaling entry of automotive suppliers keen to curb particulate emissions. Cold-spray system builders are courting venture capital to scale nozzle-gas recycling technology that slashes helium cost. Environmental performance is emerging as the next competitive battleground, with companies touting closed-loop powder capture and VOC-free masking systems to win aerospace and medical device qualifications.

Investment in powder production is also rising. A U.S. startup opened a high-pressure water-atomization line in 2025 to localize Ni-base super-alloy feedstock, reducing dependence on European imports. Meanwhile, a Korean consortium commissioned a 500 t/y suspension-plasma-spray precursor plant, securing supply for nanostructured thermal barrier projects in Asia-Pacific jet-engine programs. These moves underscore how raw-material security and vertical integration are reshaping the thermal spray coating market calculus.

Thermal Spray Coatings Industry Leaders

-

OC Oerlikon Management AG

-

Chromalloy Gas Turbine LLC

-

Linde

-

Kennametal Inc.

-

Bodycote

- *Disclaimer: Major Players sorted in no particular order

Thermal Spray Coatings Market Companies Covered in this Report

- Abakan Inc.

- APS Materials Inc.

- Bodycote

- Chromalloy Gas Turbine LLC

- Curtiss-Wright Corporation (FW Gartner)

- Fisher Barton

- Flame Spray Technologies BV

- Hannecard Roller Coatings, Inc - ASB Industries

- Kennametal Inc.

- Linde

- OC Oerlikon Management AG

- Steel Goode Products, LLC

- Sulzer Ltd

- Thermion

- Tocalo Co. Ltd.

- TST LLC

Recent Industry Developments in Thermal Spray Coatings Market

- October 2024: Aalberts N.V. acquired Steel Goode Products, a thermal spray coating provider generating approximately USD 15 million in annual revenue, to enhance its service network in the Southern U.S. and expand geographic reach.

- July 2024: Oerlikon and MTU Aero Engines signed a development agreement to co-engineer digitalized thermal spray lines for next-generation aero-engine parts.

Global Thermal Spray Coatings Market Report Scope

Thermal spray is an industrial coating process that heats or melts metallic or ceramic materials and deposits them onto a surface. The market is segmented into powder coating materials, process, end-user industry, and geography. By powder coating materials, the market is segmented into ceramic oxides, carbides, metals, polymers, and other powder-coating materials. By process, the market is segmented into combustion and electric energy. By end-user industry, the market is segmented into aerospace, industrial gas turbines, automotive, electronics, medical devices, energy and power, and other end-user industries. The report also covers the market size and forecasts for the thermal spray coatings market in 16 countries across major regions. The market sizing and forecasts for each segment are based on value (USD million).

Segmentation Overview

| Ceramic Oxides |

| Carbides |

| Metals |

| Polymers & Other Materials |

| Combustion |

| Electric Energy |

| Aerospace |

| Industrial Gas Turbines |

| Automotive |

| Electronics |

| Medical Devices |

| Energy and Power |

| Oil and Gas |

| Others (Pulp and Paper, Mining, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Powder Coating Materials | Ceramic Oxides | |

| Carbides | ||

| Metals | ||

| Polymers & Other Materials | ||

| By Process | Combustion | |

| Electric Energy | ||

| By End-user Industry | Aerospace | |

| Industrial Gas Turbines | ||

| Automotive | ||

| Electronics | ||

| Medical Devices | ||

| Energy and Power | ||

| Oil and Gas | ||

| Others (Pulp and Paper, Mining, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the thermal spray coating market in 2026?

The thermal spray coating market size is USD 9.53 billion in 2026 and is projected to reach USD 11.65 billion by 2031.

Which material segment leads the market?

Ceramic oxides hold the top spot with 29.78% 2025 revenue share and are forecast to grow at 4.91% CAGR through 2031.

What is driving the shift toward electric-energy spray processes?

Stricter VOC rules and the need for finer microstructure control are steering users to plasma and arc systems that emit fewer pollutants and enable advanced materials.

Why is Asia-Pacific the fastest-growing region?

Rapid expansion of e-mobility, electronics, and industrial gas-turbine installations is lifting demand, giving the region a 6.03% forecast CAGR.

How are emission regulations affecting coating providers?

New rules in California and the European Union require higher capture efficiencies and greener chemistries, prompting investment in closed-loop plasma booths and low-VOC masking.

Page last updated on: