Electrically Conductive Coating Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

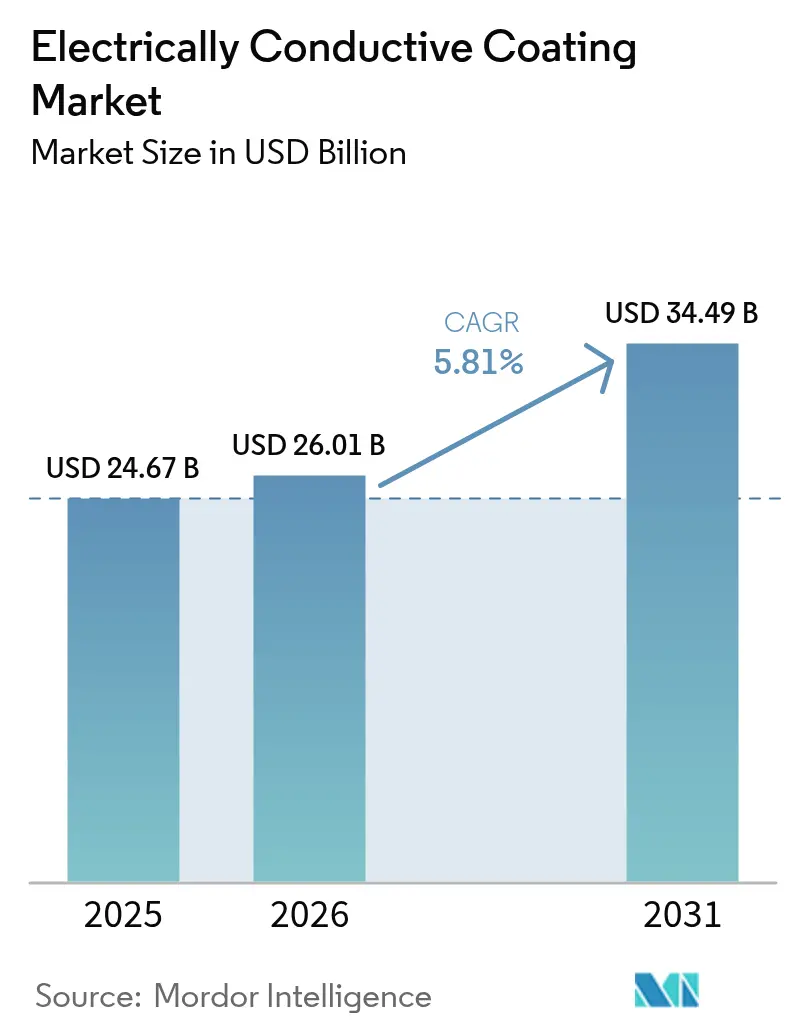

| Market Size (2026) | USD 26.01 Billion |

| Market Size (2031) | USD 34.49 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrically Conductive Coating Market Analysis by Mordor Intelligence

The Electrically Conductive Coating Market size is projected to grow from USD 24.67 billion in 2025 to USD 26.01 billion in 2026, and reach USD 34.49 billion by 2031, growing at a CAGR of 5.81% from 2026 to 2031. End-users are raising performance thresholds for electromagnetic interference (EMI) control even as form-factors shrink and component density rises, making spray- or dip-applied conductive layers indispensable. Demand is further amplified by 5G macro- and small-cell roll-outs, where enclosure interiors need 40–60 dB of shielding, and by wearable medical devices that must balance biocompatibility with electrical conductivity. Raw-material substitution is accelerating: copper fillers are clawing share from silver in mid-tier consumer electronics because a 70% material-cost gap outweighs the conductivity delta, while polyurethane chemistries are outgrowing acrylics as automakers and smartwatch brands insist on coatings that survive 100,000 flex cycles. Supply-chain strategies are shifting too, with tier-one suppliers acquiring filler producers to stabilize prices after silver swung between USD 28 and USD 34 per troy ounce in 2025.

Key Report Takeaways

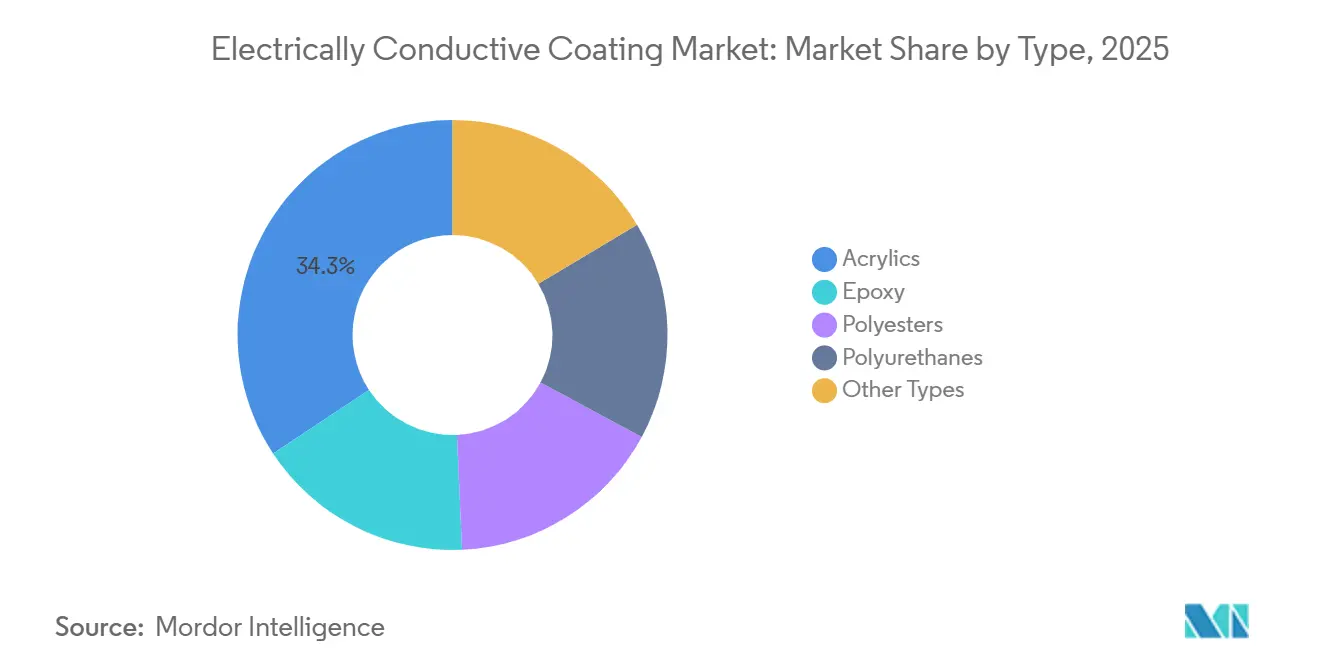

- By type, acrylics accounted for 34.28% of the electrically conductive coating market size in 2025, yet polyurethanes are advancing at a 6.22% CAGR to 2031.

- By conductive filler material, silver led with 46.41% of the electrically conductive coating market share in 2025, whereas copper is forecast to expand at a 6.34% CAGR through 2031.

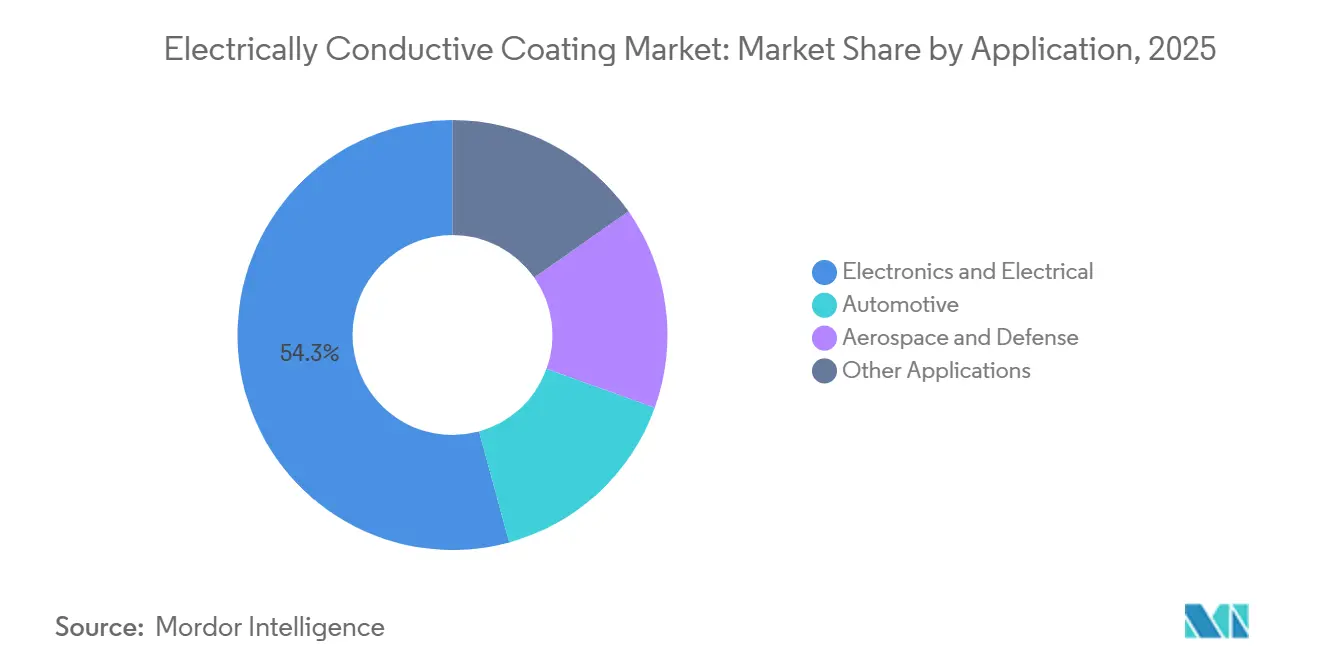

- By application, electronics and electrical captured 54.25% revenue share in 2025, while automotive is set to record the fastest 6.15% CAGR to 2031.

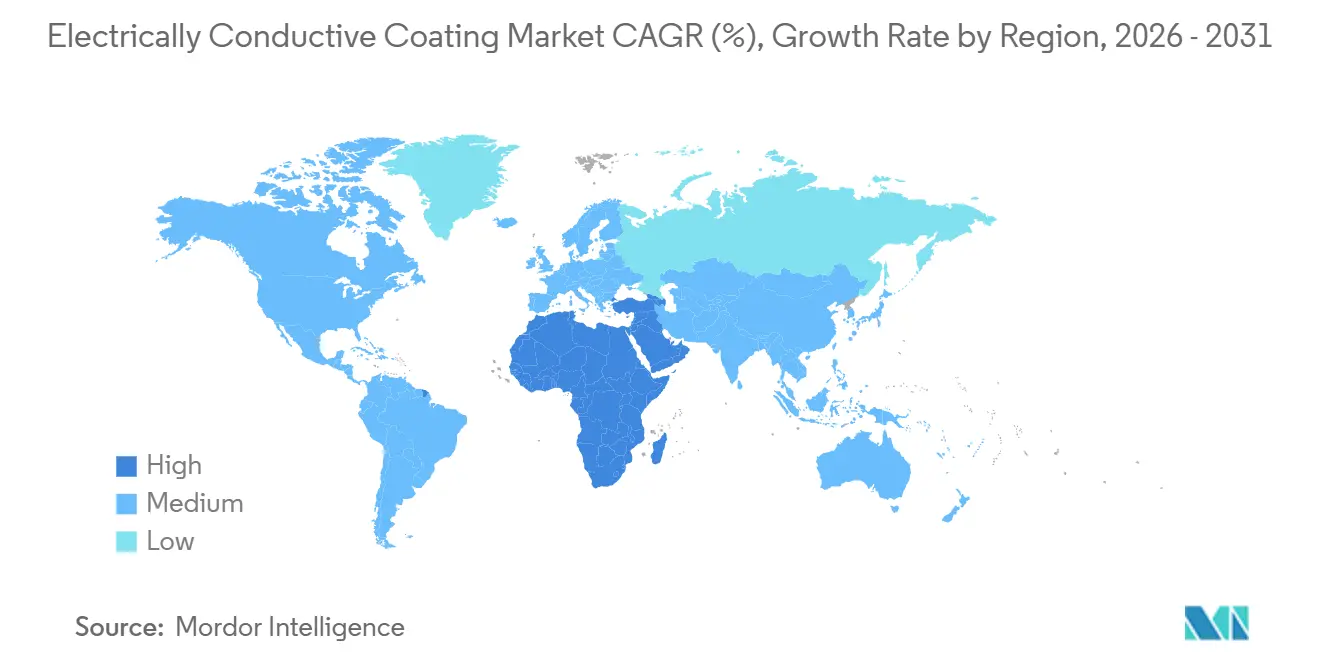

- By geography, Asia-Pacific dominated with 48.37% of revenue in 2025; the Middle East and Africa is projected to register the highest 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrically Conductive Coating Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising applications for anti-static protection | +0.9% | Global, concentrated in APAC semiconductor hubs (Taiwan, South Korea, Singapore) | Medium term (2–4 years) |

| Growing demand from electrical and electronics industry | +1.3% | Global, led by APAC manufacturing corridors and North America design centers | Long term (≥ 4 years) |

| Surge in adoption of EMI/RFI shielding in 5G infrastructure | +1.1% | APAC core (China, India, Japan), spill-over to Middle East and North America | Short term (≤ 2 years) |

| Rapid miniaturization in wearable electronics | +0.8% | North America and Europe for Research and Development, APAC for volume production | Medium term (2–4 years) |

| Conductive bio-compatible coatings for implants | +0.5% | North America and Europe (FDA, CE Mark pathways), emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Applications for Anti-Static Protection

Semiconductor fabs are tightening electrostatic-discharge thresholds below 10 V as gate oxides narrow toward 3 nm, pushing conductive floor and workbench coatings into all new cleanroom builds. Cleanroom additions in Taiwan and South Korea climbed 22% in 2025, with each square meter finished in fast-curing acrylic layers that dissipate charge within 0.1 seconds. Extreme-ultraviolet lithography magnifies risk because a single ESD event can destroy a USD 150,000 reticle; consequently, fabs now specify surface resistivity between 10⁵ and 10⁹ Ω/square. Smaller contract manufacturers in Malaysia and Vietnam are adopting water-based chemistries to meet ISO 14644 particulate limits without volatile-organic-compound penalties, a trajectory that supports mid-single-digit volume growth through 2028. Collectively, these forces are anchoring anti-static coatings as a baseline requirement rather than an optional upgrade.

Growing Demand from Electrical and Electronics Industry

Printed-circuit boards (PCBs) surpassed 820 million m² of global output in 2025, with conductive coatings applied to roughly 35% of that area to ground high-speed traces. Flagship smartphones now integrate more than 18 layers, and each layer needs selective coatings for via fill and EMI suppression. As 5G handsets doubled antenna counts, conformal coatings that maintain conductivity across curved solder joints became mandatory, lifting demand in China, South Korea, and Japan. Display makers are embedding touch sensors into OLED stacks, displacing brittle indium tin oxide with silver-nanowire dispersions that better tolerate flexing. This architecture shift should add an incremental 120 million m² of coating demand annually by 2029.

Surge in Adoption of EMI/RFI Shielding in 5G Infrastructure

Global 5G base-station installs topped 3.2 million in 2025, each housing power amplifiers and beamforming arrays that emit radio-frequency interference unless shielded internally. Conductive polyurethane sprayed onto enclosure interiors achieves 40–60 dB attenuation above 3 GHz, a level unattainable with gaskets alone. India added 450,000 stations during 2025, each consuming about 0.8 m² of coating to meet national Telecom Engineering Centre specs. Urban millimeter-wave deployments demand coated plastic radomes because leakage at 28 GHz can degrade throughput by 20%. China’s regulator now mandates EMI compliance for all small-cell enclosures, accelerating uptake among second-tier vendors.

Rapid Miniaturization in Wearable Electronics

Average circuit-board real estate in wearables shrank 18% year-on-year to 2025, removing space for metal cans and favoring spray-coated alternatives under 50 µm thick. Smartwatches integrate electrocardiogram sensors on flexible polyimide substrates that rely on stretchable silver-flake inks surviving 10,000 bends at 5 mm radius. The FDA green-lit continuous-glucose monitors with PEDOT: PSS layers in 2025, demonstrating biocompatible coatings that metallic fillers struggle to match. With a 290 million installed base of wearable medical devices, even 2–5 grams of coating per unit translates to multi-kiloton demand. New EU medical-device rules now require biocompatibility testing for any coating touching skin for over 30 days, raising entry barriers for commodity suppliers[1]J. Doe et al., “Flexible Silver-Flake Inks for Wearable Electronics,” Nature, nature.com .

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity and environmental concerns of heavy-metal fillers | -0.7% | Europe and North America, widening to APAC | Medium term (2–4 years) |

| Volatility in silver and copper prices | -0.5% | Global, most acute in APAC and South America | Short term (≤ 2 years) |

| Dispersion issues of nano-fillers causing defects | -0.4% | Global, concentrated in facilities lacking high-shear mixing | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Toxicity and Environmental Concerns of Heavy-Metal Fillers

RoHS caps cadmium at 100 ppm and lead at 1,000 ppm in electronics, forcing reformulation of legacy coatings that once relied on cadmium oxide for corrosion resistance. Compliance testing adds about USD 50,000 per SKU and can double the qualification timetable for aerospace or automotive programs. REACH dossiers for nano-silver now require aquatic-toxicity data, as LC50 values below 10 µg/L for Daphnia magna triggered hazard classification and stricter transport rules. China’s draft heavy-metal limits signal that similar rules will land in APAC by 2027. Although graphene and carbon nanotubes can substitute, their production costs run 30–40% above silver flakes, slowing broad adoption.

Volatility in Silver and Copper Prices

Silver fluctuated between USD 28 and USD 34/oz in 2025, compressing gross margins from 32% to 26% at suppliers without hedges[2]World Bank Commodities Data, “Monthly Metals Price Index,” worldbank.org . Copper traded from USD 8,200 to USD 9,800/ton, and although cheaper than silver, its propensity to oxidize demands encapsulation that lifts cost by 10–15%. Many Indian and Southeast Asian coaters lack futures-market access, so spot swings can erase a quarter’s profit. Automotive OEMs are now favoring long-term supply agreements that lock filler pricing for three-year model cycles, advantaging vertically integrated formulators who own or partner with metal-flake mills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyurethanes Gain on Flexibility Demands

Acrylics retained 34.28% share of the electrically conductive coating market in 2025, owing to fast UV curing and compatibility with roll-to-roll PCB lines. Polyurethanes, however, are projected to grow at a 6.22% CAGR, outpacing the overall electronically conductive coating market size growth because EV battery packs, automotive interiors, and health-wearables need coatings that endure 100,000 flex cycles without cracking. Epoxies remain the choice for high-heat avionics that see ≥150 °C, while polyesters fill outdoor telecom niches where weatherability matters more than ultimate conductivity.

Polyurethane adoption is accelerating in battery-management systems that swing from −40 °C to 85 °C, conditions that delaminate acrylics within 500 cycles. Automakers now specify room-temperature-curing two-component urethanes, trimming oven energy costs and cutting takt time. Acrylic vendors are responding with hybrid chemistries that graft polyurethane oligomers onto acrylic backbones, but these blends sacrifice the 30-second tack-free cure that once gave acrylics a throughput edge.

By Conductive Filler Material: Copper Challenges Silver’s Premium

Silver captured 46.41% of 2025 revenue owing to unrivaled corrosion resistance and 63 MS/m conductivity. Yet copper is growing 6.34% annually because flakes priced at USD 18–22/kg versus USD 650–750/kg for silver unlock a 70% bill-of-materials saving in mid-range smartphones, shifting the electrically conductive coating market share equation. Aluminum holds niche positions in aerospace radomes where light weight trumps peak conductivity, while graphene, carbon nanotubes, and PEDOT: PSS collectively account for 8–10% of volume but command biomedical premiums.

Core-shell fillers—copper cores with silver or nickel skins—retain 90% of copper’s cost edge while resisting oxidation, and adoption surged among Chinese PCB fabricators in 2025. Silver will remain entrenched in >10 GHz high-frequency apps and in implants where antimicrobial properties are desired. Aluminum’s use is capped by galvanic corrosion risk when paired with copper traces, an issue that forced several radar module recalls in 2024. Graphene’s biocompatibility and flexibility appeal to wearables, even though the cost runs 3–4 times above silver.

By Application: Automotive Electrification Accelerates Coating Demand

Electronics and electrical applications held a commanding 54.25% slice of the electrically conductive coating market size in 2025, covering PCB shielding, display sensors, and semipackaging. Automotive is the fastest-growing end-use at a 6.15% CAGR, propelled by battery-electric vehicles that pack 3–5× more electronic control units than combustion cars, each needing EMI suppression. Aerospace and defense demand is steady but hamstrung by multi-year qualifications and budget cycles.

Automotive uptake centers on China, Europe, and North America, where revised CISPR 25 rules cut allowable radiated emissions by 6 dB. Battery-management enclosures now cycle coatings through 2,000-plus charge events, creating a replacement market non-existent in legacy drivetrains. Electronics growth will moderate as smartphone and PC volumes plateau, but satellite mega-constellations could lift aerospace demand; 15,000 low-Earth-orbit craft are slated before 2030, each needs conductive thermal and EMI layers.

Geography Analysis

Asia-Pacific controlled 48.37% of global revenue in 2025, underpinned by vertically integrated clusters in Shenzhen, Suzhou, and Penang, where coating formulators, PCB shops, and final assemblers operate within the same-day trucking lanes. China alone consumed 180,000 tons of conductive coatings in 2025 on the back of 9 million EVs produced and aggressive 5G roll-outs. India’s Production-Linked Incentive scheme lifted domestic electronics output 28%, expanding coating imports as local capacity rose from 12,000 tons to 18,000 tons. Japan and South Korea dominate high-value niches such as biocompatible and high-temperature epoxies, commanding 20–30% price premiums. Southeast Asian nations are winning assembly work relocating from China, but resin and filler ecosystems lag, keeping them import-dependent.

North American electrically conductive coatings demand is concentrated in automotive, aerospace, and data-center hardware. The U.S. Inflation Reduction Act incentivizes coatings made near battery plants; three facilities totaling 25,000 tons/year will open by 2027 in Michigan and Georgia. Canada anchors specialty epoxy demand for avionics built in Quebec, while Mexico’s nearshoring boom lifted electronics production 16% as wire-harness and medical-device assemblers expanded, albeit still reliant on imported coatings.

Europe captured significant market share in 2025, with Germany, France, and the U.K. driving automotive and industrial demand. Stringent RoHS and REACH rules are accelerating the pivot to copper and graphene while hiking compliance costs that push smaller suppliers to exit. The EU Battery Regulation mandates EMI shielding on traction batteries exceeding 2 kWh, locking in a recurring volume stream from electric-vehicle lines. South America and the Middle East and Africa share 9% of revenue; the latter is the fastest-growing region at 5.98% CAGR, powered by Saudi and UAE data-center builds that demand 60 dB shielding for high-density racks. Brazil’s flex-fuel vehicles absorbed around 4,500 tons of coatings in 2025, but Argentina’s market dragged due to tariffs and currency volatility.

Competitive Landscape

The electrically conductive coating market is moderately consolidated. Global players leverage scale procurement to hedge metal price swings and maintain regional application labs that shorten customer qualification cycles. Regional specialists compete on custom formulations and two-week lead times, often favored for prototype runs in wearables or medical implants. Technology pivots toward water-based systems meeting volatile-organic-compound mandates without losing conductivity. IP activity is intensifying around stretchable inks; Henkel filed 14 patents in 2025 covering silver-nanowire networks embedded in thermoplastic polyurethane, foreshadowing standard interfaces for health wearables. Graphene-focused startups are disrupting high-margin niches: Italy-based BeDimensional raised EUR 12 million in 2025 to scale automotive battery thermal-management coatings that double in-plane conductivity while cutting weight by 20%.

Electrically Conductive Coating Industry Leaders

Akzo Nobel NV

PPG Industries Inc.

The Sherwin-Williams Company

Henkel AG & Co. KGaA

Axalta Coating Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Henkel released a two-component polyurethane coating for EV battery-management systems that endures −40 °C to 85 °C over 3,000 cycles and leverages copper-core/silver-shell fillers to cut material cost 60% while keeping resistivity below 0.05 ohms per square.

- January 2026: PPG invested USD 45 million to expand its Suzhou, China plant by 8,000 t/yr, installing inline SEM to ensure Cpk values above1.67 for shielding metrics.

- December 2025: Akzo Nobel and a European automaker began co-developing graphene-enhanced coatings for ADAS radar modules, targeting a 20% weight reduction versus silver-filled epoxies under EUR 8 million, a three-year JDA.

Global Electrically Conductive Coating Market Report Scope

Electrically conductive coatings are advanced materials designed to facilitate electric current flow, provide electromagnetic interference (EMI/RFI) shielding, or dissipate static charge. These coatings, widely used in industries such as electronics, aerospace, and solar panels, are composed of a polymer binder integrated with conductive fillers like silver, copper, nickel, or carbon.

The electrically conductive coating market is segmented by type, conductive filler material, application, and geography. By type, the market is segmented into acrylics, epoxy, polyesters, polyurethanes, and other types. By conductive filler material, the market is segmented into copper, aluminum, silver, and other material types. By application, the market is segmented into electronics and electrical, automotive, aerospace and defense, and other applications. The report also covers the market size and forecasts for the electrically conductive coating market in 23 countries across major regions. For each segment, the market sizing and forecast have been done on the basis of value (USD).

| Acrylics |

| Epoxy |

| Polyesters |

| Polyurethanes |

| Other Types |

| Copper |

| Aluminum |

| Silver |

| Other Material Types |

| Electronics and Electrical |

| Automotive |

| Aerospace and Defense |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Acrylics | |

| Epoxy | ||

| Polyesters | ||

| Polyurethanes | ||

| Other Types | ||

| By Conductive Filler Material | Copper | |

| Aluminum | ||

| Silver | ||

| Other Material Types | ||

| By Application | Electronics and Electrical | |

| Automotive | ||

| Aerospace and Defense | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the electrically conductive coating market expected to grow by 2031?

It is projected to increase from USD 26.01 billion in 2026 to USD 34.49 billion by 2031, registering a 5.81% CAGR.

Which filler material is gaining the most traction against silver?

Copper flakes, expanding at a 6.34% CAGR they slash material costs by roughly 70% in consumer electronics.

Why are polyurethanes preferred over acrylics in automotive electronics?

Polyurethanes endure 100,000 flex cycles and wide thermal swings, outperforming acrylics that tend to crack under repeated strain.

Which region will record the quickest growth through 2031?

The Middle East and Africa, supported by data-center construction that needs 60 dB EMI shielding.

What is the main risk linked to nano-fillers in coatings?

Agglomeration can slash shielding effectiveness by up to 25 dB unless high-shear dispersion and inline QC are employed.

How concentrated is supplier power in this space?

Moderately concentrated; the top five vendors control about 37% of global revenue, leaving room for regional specialists.

Page last updated on: