Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

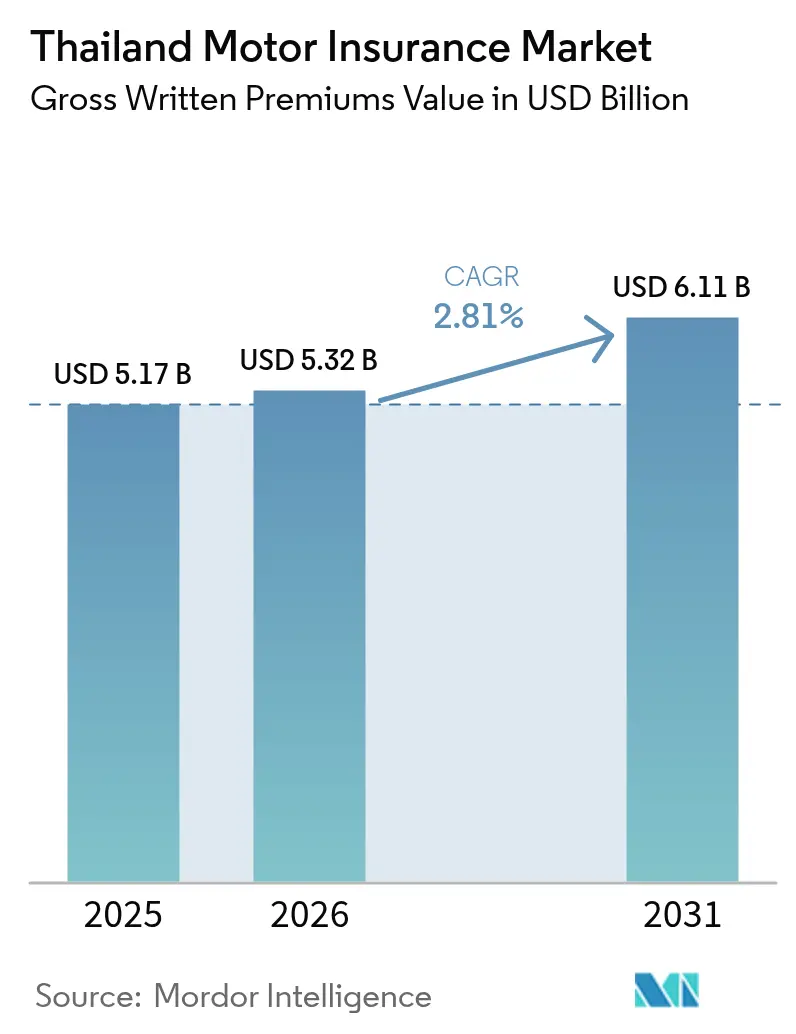

| Base Year Market Size (2025) | USD 5.17 Billion |

| Market Size (2026) | USD 5.32 Billion |

| Market Size (2031) | USD 6.11 Billion |

| Growth Rate (2026 - 2031) | 2.81% CAGR |

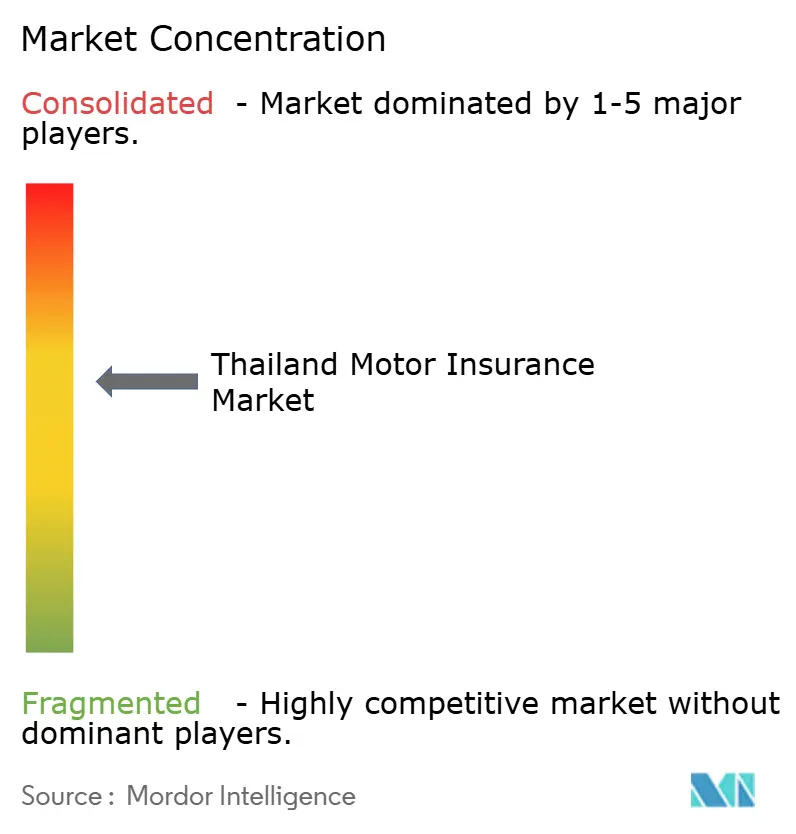

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Motor Insurance Market Analysis by Mordor Intelligence

The Thailand motor insurance market size is expected to grow from USD 5.17 billion in 2025 to USD 5.32 billion in 2026 and is forecast to reach USD 6.11 billion by 2031 at 2.81% CAGR over 2026-2031. Demand remains underpinned by compulsory third-party liability rules, while rising vehicle values and broader risk awareness keep voluntary products the primary revenue engine. Accelerating electrification, a steady turn toward digital buying journeys, and insurers’ adoption of data-driven underwriting are reshaping competitive strategy. Government pickup-loan subsidies have cushioned the 26% plunge in total new-car sales seen in 2024, and targeted EV incentives, supported by 537 public chargers installed by Central Pattana, open a fresh avenue for battery-centric covers. OIC-approved premium adjustments counter claims inflation linked to motorcycle accidents, which account for 83.8% of Thailand’s road fatalities and put pressure on loss ratios.

Key Report Takeaways

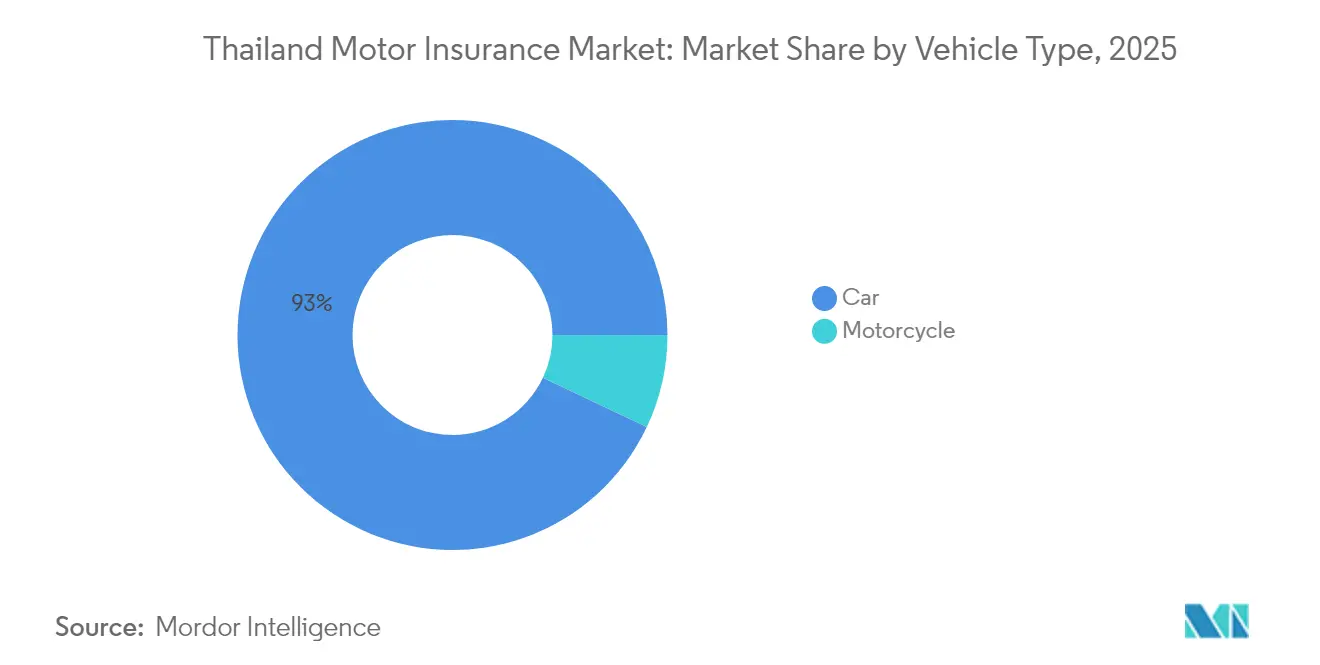

- By vehicle type, cars held 92.96% of Thailand's motor insurance market share in 2025, and the car segment is also the fastest growing at a 3.05% CAGR through 2031.

- By insurance type, voluntary coverage commanded 87.02% share of the Thailand motor insurance market size in 2025, while compulsory coverage is expanding fastest at 3.5% CAGR to 2031.

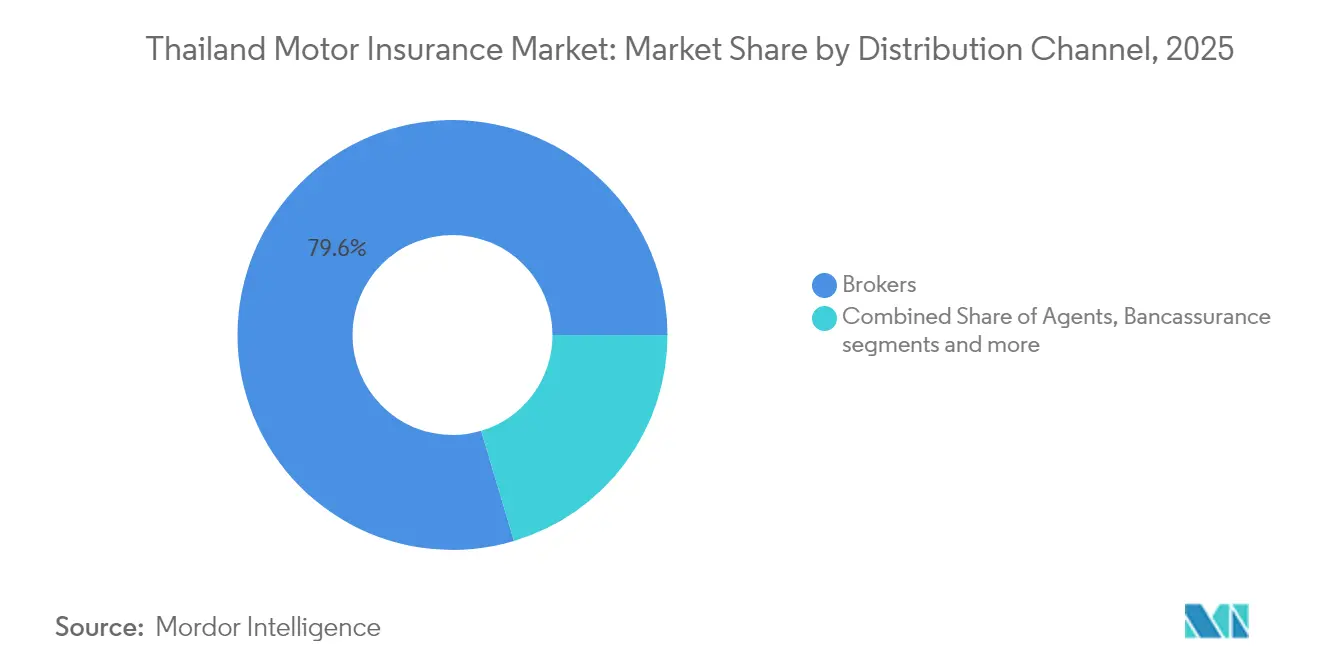

- By distribution channel, brokers retained an 79.62% share of the Thailand motor insurance market size in 2025, whereas agents posted the highest growth at a 3.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring EV registrations and EV-specific tariff codes | +0.8% | National, concentrated in Bangkok and major urban centers | Medium term (2-4 years) |

| Government stimulus for pickup loans & easier credit | +0.6% | National, with a stronger impact in the rural and commercial vehicle segments | Short term (≤ 2 years) |

| OIC-approved premium hikes on rising accident claims | +0.4% | National, with a higher impact on high-density traffic areas | Short term (≤ 2 years) |

| Digital direct-to-consumer platforms are scaling rapidly | +0.3% | National, led by urban millennials and tech-savvy demographics | Medium term (2-4 years) |

| Usage-based "drive-any-car" products are gaining traction | +0.2% | National, with early adoption in Bangkok and secondary cities | Medium term (2-4 years) |

| Embedded cover tied to ride-hailing & e-commerce fleets | +0.2% | National, concentrated in urban centers with high ride-hailing penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring EV registrations and EV-specific tariff codes

Electric vehicle registrations are projected to rise 40% in 2025 following multilayered government incentives that cut import duties, extend purchase rebates, and support charging-network expansion[1]Central Pattana PLC, “2024 Sustainability Report,” centralpattana.co.th. . Insurers that master battery degradation analytics, thermal-runaway probabilities, and residual-value swings tied to aggressive Chinese OEM pricing position themselves as preferred underwriters for both fleet operators and early adopters. The Office of Insurance Commission has introduced dedicated tariff codes for EVs, enabling precision risk-based pricing while separating loss experience from internal-combustion pools. Although early claims data remain limited, front-runners already bundle specialized battery-replacement guarantees and roadside charging support to justify premium differentials. Wider deployment of public chargers in secondary cities lowers range anxiety and broadens the addressable EV customer base, further enlarging Thailand's motor insurance market opportunities. Carriers that lock in partnerships with automakers and charging-station owners create embedded-insurance touchpoints that cement customer stickiness at the point of sale.

Government stimulus for pickup loans and easier credit

Thailand’s pickup-loan subsidy slashes upfront interest cost for buyers and relaxes credit scoring, which injects immediate demand into a segment vital for agriculture and small logistics[2]. The program directly links loan disbursement to proof of at least compulsory insurance, thereby driving instant policy growth in underserved rural districts. Easier credit, however, may admit higher-risk borrowers whose driving patterns involve heavier payloads and longer distances, elevating the frequency and severity of claims. Insurers now integrate bureau credit scores with real-time telematics monitoring to filter adverse-selection risks while preserving volume gains. The same stimulus helps diversify Thailand's motor insurance market premium sources beyond urban passenger cars, balancing portfolio exposures. Over the medium term, an expected hand-off from subsidy to organic commercial demand keeps the pickup niche on a path of steady premium generation even as the broader new-car market remains subdued.

OIC-approved premium hikes on rising accident claims

The OIC sanctioned multiple incremental premium increases in 2024 after accident severity outpaced prior pricing by more than 12%, with motorcycle collisions driving the spike. The regulator balanced solvency concerns against consumer affordability by allowing phased adjustments that vary by geography and vehicle class. Insurers seized the green light to realign loss ratios, but higher prices risk policy downgrades to bare-minimum cover among price-sensitive drivers. To safeguard growth, carriers rolled out modular add-ons that let customers mix and match benefits, thereby maintaining perceived value despite higher base tariffs. Enhanced enforcement of traffic laws, including lower BAC limits and expanded blood-alcohol testing, is expected to moderate claim frequency over time, giving carriers runway to rebuild reserves. Improved road-safety data feeds recursive pricing models that refine risk buckets, stabilizing Thailand's motor insurance market profitability during the forecast horizon.

Digital direct-to-consumer platforms are scaling rapidly

InsurTech start-ups such as Roojai and Sunday streamline quote-to-bind in under five minutes through API integrations that scrape DMV databases, verify driver identity, and auto-populate proposal forms. These platforms trim commission expense, capped at 18% under current rules, and redirect savings into customer acquisition incentives like instant cashback. Machine-learning engines leverage policyholder driving data to offer behavior-based discounts, building a virtuous loop that rewards safer drivers and enhances loss ratios. Incumbent carriers respond by spinning off digital subsidiaries or embedding their products in e-commerce checkouts, widening the choice set for younger buyers. The OIC sandbox accelerates innovation by letting firms test telematics, pay-as-you-drive, and on-demand coverage under close regulatory supervision, which lowers compliance risk. Over time, rising smartphone penetration and ubiquitous e-wallets are expected to push direct digital sales to a double-digit share of the Thailand motor insurance market premium.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 23.9% slump in new-car sales dampening premium growth | -0.7% | National, with a stronger impact in urban markets and luxury segments | Short term (≤ 2 years) |

| Inflation-driven parts & repair cost surge, squeezing margins | -0.4% | National, with a higher impact in metropolitan areas with premium repair facilities | Medium term (2-4 years) |

| Chinese EV price war heightening residual-value risk | -0.3% | National, with concentrated impact on EV-heavy urban markets | Medium term (2-4 years) |

| Data-privacy & telematics-consent hurdles | -0.2% | National, with a stronger impact among privacy-conscious urban consumers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

23.9% slump in new-car sales dampening premium growth

New-car registrations fell 26% in 2024 as household debt exceeded 90% of GDP, dampening discretionary purchases of passenger vehicles. The downturn cuts the pipeline for comprehensive policy originations because first-year coverage tends to be richest in scope and premium. Affluent urban consumers delay replacing existing cars, further eroding high-ticket policy volumes that traditionally buoy Thailand's motor insurance market profitability. Pickup-truck subsidies cushion some of the blow in rural markets but do not fully offset lost revenue from premium sedans and SUVs. Carriers pivot by upselling telematics-based savings to owners of older vehicles, converting retention risk into a cross-sell opportunity. Nevertheless, without a rebound in auto retail sales, the near-term drag on aggregate written premium remains material, shaving an estimated 0.7 percentage points off market CAGR.

Inflation-driven parts and repair costs surge, squeezing margins

Supply-chain dislocations, currency depreciation, and elevated energy prices pushed average spare-parts costs up by 14% in 2024, and labor rates at certified shops climbed in tandem, inflating claim severity. Imported bumper assemblies for premium European models now command 22% higher quotes than two years earlier, straining loss reserves even after OIC-approved tariff hikes. The IAIS 2024 Global Insurance Market Report noted that combined ratios in many non-life lines, including motor, edged toward the 100% break-even threshold, a pattern echoed in Thailand[2]International Association of Insurance Supervisors, “Global Insurance Market Report 2024,” iaisweb.org. Insurers negotiate volume-based discounts with parts suppliers and pilot refurbished-component programs to stem escalation, though customer acceptance varies by segment. EV repairs complicate cost planning because specialized tooling, battery-diagnostic software, and technician training introduce new fixed expenses, elevating the break-even premium per policy. Persistent inflationary pressure, therefore, trims underwriting margin and subtracts 0.4 percentage points from Thailand's motor insurance market growth unless productivity gains or further rate hikes emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Cars Remain Dominant Amid Growing Specialization

Cars contributed 92.96% to Thailand's motor insurance market size in 2025, reflecting their higher insured value and broader uptake of voluntary comprehensive policies. The segment is forecast to expand at a 3.05% CAGR, outpacing motorcycles and commercial vans, which underscores continued urbanization and rising household incomes. Despite commanding a small slice of premium income, motorcycles constitute the bulk of road-fatality cases, forcing carriers to manage frequency exposure through tighter underwriting criteria and premium differentiation. Electric sedans and crossovers accelerate share within the car category, prompting insurers to develop battery-warranty add-ons and charging-station liability clauses. In the fleet niche, ride-hailing companies shift toward EVs to comply with emission targets, furnishing carriers with bulk policy volumes tied to telematics-monitored safety programs. High-end sports cars remain heavily concentrated in Bangkok, creating localized high-severity exposure that carriers hedge with reinsurance.

The motorcycle line, although lower in premium per unit, offers scale that attracts specialized players who use mobile apps for instant compulsory-policy issuance at roadside checkpoints. Pickup trucks, buoyed by government stimulus, add a stable layer of growth in rural provinces by supporting logistics for agriculture and SMEs. Hybrid vehicles act as bridge technology, and their dual powertrains lead to nuanced pricing that factors both conventional engine parts and battery packs. Over the forecast horizon, portfolio balance across vehicle types is expected to make the Thailand motor insurance market less sensitive to any single segment shock.

By Insurance Type: Voluntary Coverage Propels Revenue While Compulsory Growth Adds Stability

Voluntary products captured 87.02% of Thailand's motor insurance market share in 2025 and remain the chief revenue engine because they bundle collision, theft, flood damage, and liability enhancements that raise average premiums. Usage-based insurance offers discounts up to 35% for low-mileage drivers, attracting urban residents who rely on mass transit during weekdays yet seek weekend mobility, thereby retaining voluntary penetration. Compulsory third-party liability policies, which pay medical benefits of THB 30,000-THB 80,000 and death benefits up to THB 500,000, provide the market floor and are growing at 3.5% CAGR thanks to stricter roadside checks and digital verification systems. Government e-citation programs now auto-populate fines for uninsured vehicles, causing an uptick in near-instant compulsory policy purchases via smartphone apps. The segmentation also shows increasing cross-sell of personal accident riders and roadside-assistance vouchers that push policyholders back into the voluntary fold. As climate volatility rises, insurers bundle parametric flood cover based on rainfall indices, adding another layer of differentiation that nudges customers toward comprehensive options.

The interplay of both policy types underpins market stability: compulsory insurance assures baseline premiums even during economic lulls, while voluntary enhancements drive profitability by carrying lower frequency yet higher severity. Insurers tracking lapse rates deploy SMS-based renewal reminders and flexible monthly payment plans to keep voluntary retention above 70%, maintaining Thailand motor insurance market size momentum even as macro headwinds wax and wane.

By Distribution Channel: Brokers Hold Share While Digital Agents Accelerate

Brokers controlled 79.62% of Thailand's motor insurance market share in 2025, anchored by decades-old commercial links and compliance know-how. Corporate fleets, ride-hailing operators, and multinational logistics firms still rely on brokers to structure multiline policies that knit together motor, cargo, and liability covers. Nonetheless, agency channels logged a 3.74% CAGR by packaging motor insurance with high-frequency consumer products like health, creating crossline collaborations that brokers often overlook. Bancassurance further boosts agency counts; KBank, for example, routes over half its non-life premium through in-branch agents who upsell motor coverage at the point of vehicle finance approval. Digital-only agents, licensed under OIC rules, now use chatbot engagement and AI-driven lead scoring to widen funnel reach, especially among millennial renters who prefer subscription-length policies.

Online comparison portals reduce search friction, letting buyers toggle among 15-plus insurers within seconds, which amplifies price transparency and compresses margins for intermediary-heavy players. Insurers respond by launching omnichannel campaigns that unify brokers, agents, and web contacts into a single CRM view, smoothing customer-journey handoffs. The OIC commission cap keeps the playing field level and motivates carriers to drain unnecessary frictional cost, reinforcing a gradual but definitive pivot in the Thailand motor insurance market toward direct engagement models that prize experience over pure distribution heft.

Geography Analysis

Bangkok and its peri-urban ring account for more than half of Thailand's motor insurance market size because vehicle density, higher average vehicle value, and elevated collision probability converge in the capital’s congested corridors. Insurers segment pricing down to sub-districts, incorporating telematics heat maps of rush-hour stop-and-go traffic, night-time accident flashpoints, and vehicle-theft hotspots. Claims-management efficiency in Bangkok benefits from a dense repair-shop network and plentiful spare parts, though rising labor cost in premium workshops inflates severity.

The Eastern Economic Corridor, anchored by Chonburi and Rayong, exhibits rising premium volume as industrial projects spur demand for company fleets and employee shuttles. Expansion of public charging stations in Pattaya and Rayong under Central Pattana’s network supports EV adoption outside the capital, creating localized niches for battery-focused covers. Northern hubs such as Chiang Mai witness growth tied to domestic tourism, which expands rental-car fleets and short-term insurance policies. Central plains provinces, where agricultural mechanization relies on pickup trucks, show stable compulsory-policy counts and increasing voluntary upgrades as produce exporters seek higher cargo-damage limits.

Southern coastal provinces face monsoon-driven flood risk that lifts demand for water-damage riders in both compulsory and voluntary lines. Insurers price these add-ons using satellite-rainfall indices and historical inundation maps, ensuring actuarial adequacy while maintaining simplicity for buyers. Digital marketing through telecom storefronts and e-wallet apps has broadened access in remote islands and mountain communities, trimming urban–rural disparity in insurance penetration over the past two years. Overall, geographic diversification dilutes catastrophic risk concentrations and sustains steady Thailand motor insurance market development across the nation’s varied topography.

Competitive Landscape

The Thailand motor insurance sector is moderately consolidated, with foreign and local insurers jockeying for both scale and specialization. Chubb’s USD 275 million purchase of LMG Insurance in March 2025 instantly expanded its footprint to 56 branches and 2,600 intermediaries, giving the group deeper broker access for commercial fleet accounts. ERGO Thailand, honored as 2024 General Insurance Company of the Year, doubled its branch count by absorbing Nam Seng Insurance and integrating 800 Syn Mun Kong employees, revealing how workforce leverage can accelerate geographic reach and service-level consistency[4]Asia Insurance Review editors, “ERGO Thailand wins top honor,” asiainsurancereview.com.

Domestic leaders Viriyah and Dhipaya fend off challengers through investment in AI-enabled claims triage that cuts settlement cycle time from five days to under 48 hours, improving customer satisfaction scores and lowering loss-adjustment expense. Japanese joint-ventures Sompo and Tokio Marine emphasize subscription-style monthly billing and repair-network partnerships in up-country provinces, staking out a share in fast-growing secondary markets. InsurTech disruptors Roojai and Sunday differentiate with behavior-based discount algorithms that reward smooth braking and off-peak driving patterns, a model that commands loss-ratio advantages yet tests data-privacy tolerance.

Reinsurers such as Swiss Re backstop catastrophic exposure and supply analytics on EV battery-failure curves, helping primary carriers refine tariff tables. Collaboration spaces in the OIC sandbox allow incumbents and start-ups to co-create micro-duration covers for ride-hail drivers who toggle between personal and commercial use, further fragmenting the product landscape. Competitive thrust now revolves around customer-experience differentiation, loss-ratio efficiency, and speed of product iteration, positioning Thailand motor insurance market for ongoing innovation as digital adoption deepens.

Thailand Motor Insurance Industry Leaders

The Viriyah Insurance

Dhipaya Insurance

Bangkok Insurance

Muang Thai Insurance

MSIG Insurance (Thailand)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sompo Thailand opened a Khon Kaen branch and rolled out “SOMPO ตามใจ,” a flexible monthly auto plan with 24-hour digital claims service.

- March 2025: Chubb completed its USD 275 million acquisition of Liberty Mutual’s Thai unit, adding 56 branches and 2,600 intermediaries to its network.

- September 2024: ERGO Thailand received General Insurance Company of the Year after integrating 800 Syn Mun Kong employees and acquiring Nam Seng Insurance.

- September 2024: Muang Thai Life Assurance introduced dynamic-pricing health covers for diabetes patients and extended entry age to 90 years, a framework adaptable to pay-how-you-drive motor lines.

Thailand Motor Insurance Market Report Scope

This report aims to offer a detailed analysis of the Thailand motor insurance market. It concentrates on the market dynamics, emerging trends in the segments and regional markets, and insights into various product and application types. Also, it focuses on the key players and the competitive landscape in the market. The Thailand Motor Insurance Market is segmented by Insurance Type (Third Party Liability, Comprehensive) and Distribution Channel (Agents, Brokers, Banks, Online, and Other Distribution Channels). The report offers market size and forecast values for the Thailand Motor Insurance Market in USD million for the above segments.

By Vehicle Type

| Car |

| Motorcycle |

By Insurance Type

| Voluntary |

| Compulsory |

By Distribution Channel

| Agents |

| Brokers |

| Bancassurance |

| Other Distribution Channels |

| By Vehicle Type | Car |

| Motorcycle | |

| By Insurance Type | Voluntary |

| Compulsory | |

| By Distribution Channel | Agents |

| Brokers | |

| Bancassurance | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current size and growth rate of Thailand's motor insurance market?

The market stands at USD 5.32 billion in 2026 and is projected to reach USD 6.11 billion by 2031 at a 2.81% CAGR.

How are electric vehicles affecting motor insurance in Thailand?

EV registrations are set to rise 40% in 2025, prompting insurers to create battery-specific warranties and charging-station liability covers while refining tariff codes.

Which distribution channel is expanding fastest?

Agents, including bancassurance and digital agents, show the highest growth at 3.74% CAGR as carriers emphasize direct engagement and tech-enabled onboarding.

Why did the OIC approve recent premium hikes?

Motorcycle accident severity raised claims inflation beyond prior pricing assumptions, so the OIC allowed phased increases to protect insurer solvency while safeguarding consumers.

How is repair-cost inflation impacting insurers?

Rising parts and labor costs, especially for imported components and EV repairs, push combined ratios toward 100%, squeezing industry profit unless countered with rate adjustments or efficiency gains.

Are compulsory policies becoming more common?

Yes, stricter enforcement and digital verification are driving compulsory third-party liability policies to grow at a 3.5% CAGR, improving overall risk pooling and compliance.

Page last updated on: