Thailand Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.31 Billion |

| Market Size (2026) | USD 2.4 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

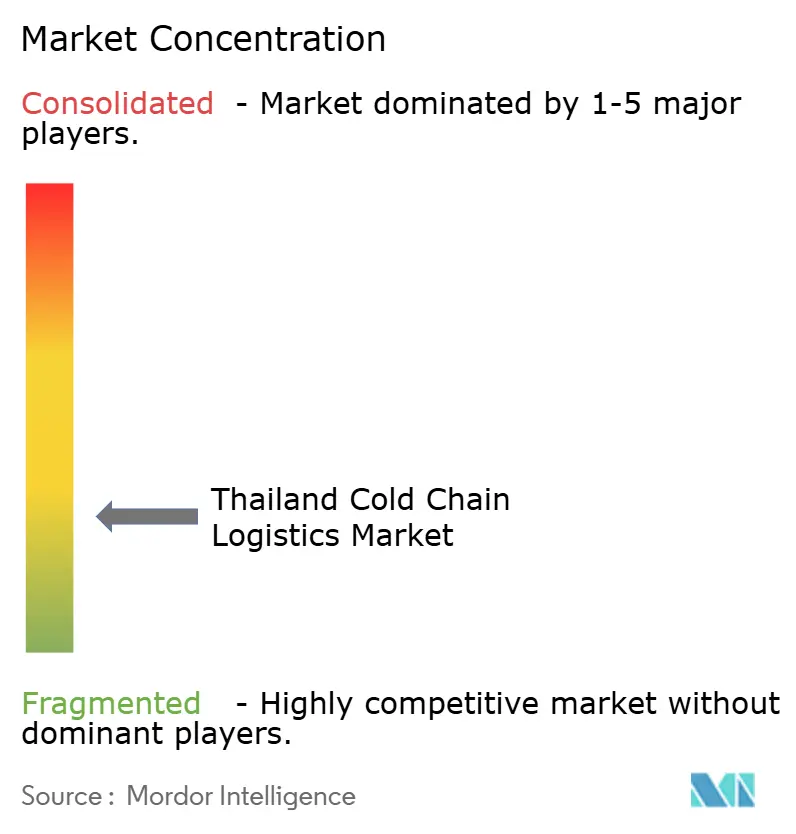

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Cold Chain Logistics Market Analysis by Mordor Intelligence

The Thailand Cold Chain Logistics market size is expected to grow from USD 2.31 billion in 2025 to USD 2.4 billion in 2026 and is forecast to reach USD 2.89 billion by 2031 at 3.79% CAGR over 2026-2031.

Consistent government outlays of THB 2.68 trillion (USD 78 billion) for multimodal infrastructure, coupled with the Eastern Economic Corridor’s (EEC) magnet effect on foreign direct investment, keep capital flowing into temperature-controlled storage and transport assets[1]Thailand Government PR Department, “Transport Min Launches 2.68 Trillion Baht Infrastructure Project,” thailand.prd.go.th. Energy-related cost relief, brought about by a scheduled tariff cut from THB 4.15 (USD 0.12) to THB 3.70 (USD 0.1) per unit, promises THB 100 billion (USD 2.9 billion) in annual savings for warehouse operators and retailers, sharpening the near-term competitiveness of the Thailand cold chain logistics market. Strategic automation—exemplified by PepsiCo’s 16,520-pallet automated storage and retrieval system—offsets a chronic labor shortfall while raising throughput accuracy. Intensifying vertical integration among food processors, drug distributors, and 3PLs is spurring consolidation, with the SCG-JWD merger forming a nationwide, multimodal platform able to bundle storage, transport, and value-added services into one offering.

Key Report Takeaways

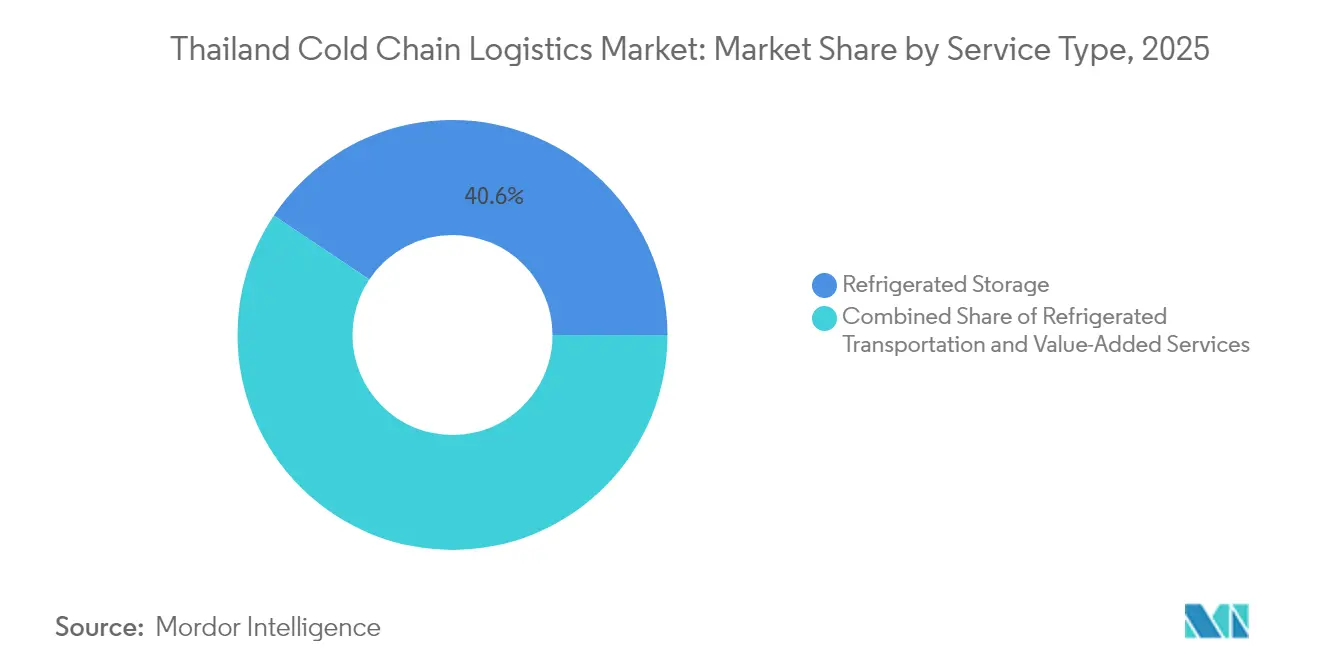

- By service type, Refrigerated Storage led with 40.62% of Thailand cold chain logistics market share in 2025, while Value-Added Services is poised for a 4.63% CAGR through 2031.

- By temperature band, Frozen storage held 52.55% of the Thailand cold chain logistics market size in 2025; Deep-Frozen/Ultra-Low facilities are forecast to expand at a 5.14% CAGR through 2031.

- By application, Meat & Poultry captured 21.74% of Thailand cold chain logistics market share in 2025; Pharmaceuticals & Biologics is projected to post a 5.88% CAGR to 2031.

- By region, the Central corridor commanded 28.72% of the Thailand cold chain logistics market size in 2025, while the Eastern region should realize a 4.18% CAGR on the back of EEC incentives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in Thailand includes both locally based firms and those operating across multiple regions. The market landscape in the global cold chain logistics industry research shows how these players are arranged internationally.

Thailand Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in online grocery & meal-kit delivery | +0.8% | Central & Eastern | Short term (≤ 2 years) |

| Expansion of vaccine & biologics distribution network | +1.2% | Central hubs nationwide | Medium term (2-4 years) |

| Government EEC infrastructure subsidies | +0.9% | Eastern, spillover Central & Southern | Long term (≥ 4 years) |

| Automation & IoT for real-time temperature visibility | +0.7% | National | Medium term (2-4 years) |

| Rapid-freeze protocols for China fruit import rules | +0.5% | Northern & Central | Short term (≤ 2 years) |

| Net-zero warehousing incentives | +0.4% | Industrial zones nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Boom in Online Grocery & Meal-Kit Delivery

E-commerce adoption has accelerated the Thailand cold chain logistics market, especially for chilled and frozen grocery orders delivered within metropolitan Bangkok and EEC industrial towns. Reduced electricity charges under the tariff cut create margin headroom for last-mile couriers operating energy-intensive hubs[2]US-ASEAN Business Council, “Thailand's Electricity Price Cut Gains Private Sector Support,” usasean.org. Kerry Express and Betagro now co-brand the “Kerry Cool” network, letting retailers ship poultry, ready-to-eat meals, and desserts in insulated shippers overnight to 77 provinces. A rebound in Chinese tourist arrivals has lifted demand for meal-kit services catering to condo rentals and hotels, widening the addressable base. Ongoing Thai FDA consultations around beverage and ice labeling signal tighter hygiene oversight, which in turn boosts requirements for traceable, temperature-verified supply chains. Operators such as WICE Logistics are investing in cloud-based transport management systems and handheld scanners to deliver item-level visibility from dock to doorstep.

Expansion of Vaccine & Biologics Distribution Network

Thailand’s ambition to become a regional vaccine exporter aligns squarely with the Thailand cold chain logistics market. UPS Healthcare, DHL, and Logisteed have rolled out -20 °C freezers, 2-8 °C coolers, and -80 °C ultra-cold bays that comply with WHO GDP guidelines. The National Vaccine Policy’s 2023–2027 action plan positions domestic makers such as Siam Bioscience and BioNet Asia to scale biologic output, amplifying ultra-low demand in Central-region science parks. Real-time IoT sensors, pioneered locally by DataKind pilot programs, transmit humidity and shock alerts directly to qualified persons in charge, cutting excursion risk for live-virus formulations[3]DataKind, “AI & Data Science for Vaccine Deployment,” datakind.org. DHL Supply Chain has doubled dedicated healthcare pallet spots near Suvarnabhumi Airport, bundling customs brokerage, validated packaging, and final-mile dispatch. Economic modeling shows routine dengue vaccination could curb symptomatic cases by 41%-57%, underscoring the social payoff of resilient sub-zero infrastructure.

Government EEC Infrastructure Subsidies

Long-horizon subsidies and a 17% flat income tax for EEC investors de-risk green-field warehouse construction, making the corridor a beehive for multinational 3PLs. Laem Chabang Port’s Phase 3 upgrade lifts container capacity to 18 million TEUs by 2026, shortening dwell time for reefer boxes destined for China and Japan. Land sales in EEC industrial estates jumped 53% in H1-2024, pushing land prices to THB 6.7 million (USD 196,430) per rai, a signal that operators want proximity to dual-carriage expressways and LNG-ready power grids. Sumisho Global Logistics now positions dedicated reefer trucks in Chonburi to service automotive, dairy, and plasma derivative cargo in one circuit. Smart-port roadmaps mandating shore-power hookups and customs single-window systems trim clearance cycles, giving exporters a cost-per-kilogram edge when routing frozen chicken or durian pulp to North Asia.

Automation & IoT for Real-Time Temperature Visibility

Labor shortages, particularly certified refrigeration mechanics, have sped up capital spending on conveyor robotics, shuttle systems, and predictive maintenance platforms. PepsiCo’s Rojana facility leverages a Dematic AS/RS—Thailand’s tallest at 32 meters—to double throughput per square meter while keeping variance within ±0.5 °C across 16,520 pallets. CP Foods loops edge-AI cameras into hatcheries and grow-out barns, enabling batch-level tracing from farm to distribution dock. AutoStore’s Rayong robot plant will supply cube-storage modules that fit into Thailand's cold chain logistics market depots as small as 500 sqm, opening automation to mid-tier distributors. MOL’s OMEGA 1 Bang Na complex, set for 2027 delivery, stacks ambient and 0 °C rooms in mezzanine tiers to shrink travel distance between pick faces. Predictive analytics tie compressor vibration readings to maintenance support tickets, raising uptime and preserving product quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity tariffs & fuel surcharges | -0.6% | National | Short term (≤ 2 years) |

| Cold-room equipment breakdown & downtime risk | -0.4% | National | Medium term (2-4 years) |

| Shortage of certified refrigeration technicians | -0.3% | National | Medium term (2-4 years) |

| Costly retrofit to low-GWP refrigerants | -0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Electricity Tariffs & Fuel Surcharges

Energy still commands as much as 30% of warehouse operating cost despite the tariff cut, and EGAT’s debt overhang may force surcharge reinstatements after 2026. Switching to CO₂ systems cuts kilowatt-hour consumption but entails a USD 0.5 million retrofit for a 10,000-pallet site, a hurdle for SMEs. Betagro sidesteps this by coupling rooftop solar with ice-bank thermal storage to shave peak-hour demand. Haulers face similar fuel surcharges, with biodiesel B20 adoption providing only marginal cost relief.

Cold-Room Equipment Breakdown & Downtime Risk

Compressor failures threaten batch loss worth USD 250,000 per incident for pharmaceutical cargo. A 2024 survey showed 69% of SME warehouses lacked vibration sensors to flag bearing wear, prolonging unplanned outages. Konoike Cool Logistics implements monthly thermographic scans and boroscopic inspections, reducing chiller downtime by 18% year-on-year. Industry training pipelines remain shallow; only 420 technicians nationwide hold Category II ammonia certifications. Predictive maintenance platforms tether IoT probes to cloud algorithms, generating work orders before anomalies escalate—a practice that trimmed inventory holding costs in Northern Thai factories by up to 55% between 2022 and 2024.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Infrastructure Drives Market Foundation

Refrigerated Storage accounted for 40.62% of Thailand's cold chain logistics market share in 2025, underpinning nationwide distribution hubs that feed retail, food-service, and healthcare channels. Warehousing landlords capitalize on land-use incentives near the EEC, where MOL’s OMEGA 1 Bang Na will add multi-temperature bays across 100,000 sqm by 2027. Users demand racking to -25 °C, cross-docks with 12-meter clear heights, and shuttle-based carton retrieval to accelerate SKU churn.

Value-Added Services, although only 9.12% of 2025 revenue, will expand at a 4.63% CAGR through 2031, the fastest within the Thailand cold chain logistics market. Services such as kitting, blast-freezing, labeling for halal certification, and GDP documentation command 20%-plus gross margins, enticing 3PLs to bundle them into existing contracts. Retailers lean on these ancillary streams to localize product assortment without committing capex.

By Temperature Type: Frozen Dominance With Ultra-Low Growth

Frozen storage retained 52.55% of the Thailand cold chain logistics market size in 2025, mirroring robust export orders for chicken, shrimp, and ice cream. Productivity hinges on tunnel freezers able to process three tons per hour and hold set-point within ±1 °C, critical for meeting Japanese import protocols.

Deep-Frozen/Ultra-Low chambers will chart a 5.14% CAGR as vaccine filling and genomic therapy pipelines proliferate. DHL Supply Chain opened -80 °C capacity adjacent to its existing 2-8 °C bays at Bang Na, trimming order-to-ship lead times for monoclonal antibody vials to under four hours. Sustainability mandates push chilled rooms toward natural refrigerants; CO₂ transcritical systems meet Global Warming Potential thresholds while cutting energy use 8% compared with R-404A baselines.

By Application: Pharmaceuticals Lead Growth Transformation

Meat & Poultry maintained 21.74% of Thailand's cold chain logistics market share in 2025, anchored by 2.6% production growth and new bilateral protocols with Saudi Arabia and China. CP Foods’ AI-enabled welfare monitoring automates feed adjustments, raising weight gain while preserving animal health certificates.

Pharmaceuticals & Biologics will clock a 5.88% CAGR, outpacing food segments as new drug approvals and regional distribution mandates require rigid temperature assurance. UPS Healthcare’s Thai network adds Phase-Change Material shippers capable of 120-hour hold time, enabling transport from Suvarnabhumi to Yangon without dry-ice replenishment. The shift brings higher revenue per pallet—often triple that of frozen seafood—supporting margin expansion across the Thailand cold chain logistics market.

Geography Analysis

The Central corridor, anchored by Bangkok, accounted for 28.72% of Thailand's cold chain logistics market share in 2025, benefiting from the density of supermarkets, pharma depots, and quick-service restaurant commissaries. Dematic-enabled automation at PepsiCo’s Ayutthaya site illustrates how firms embed high-bay storage within commuter belts to slash last-mile latency. Tariff relief worth THB 100 billion (USD 2.9 billion) annually further sweetens operating economics for chilled DCs serving Greater Bangkok.

The Eastern region will post a 4.18% CAGR through 2031 as the Thailand cold chain logistics market pivots around the EEC’s THB 1.34 trillion (USD 39 billion) smart-city spend that embeds fiber, LNG pipelines, and dual-gauge rail. Laem Chabang’s Phase 3 berths, with automatic straddle carriers and hydrogen-ready reefer points, underwrite faster gate-turns for containerized fruit and chilled salmon bound for Shanghai.

Mordor Intelligence tracks the cold chain logistics market across other major regions such as Africa and South America, with additional country-level coverage spanning Indonesia, Mexico, Sweden, and Netherlands, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Thailand cold chain logistics market is moderately fragmented. SCGJWD’s 2024 merger pooled 1.2 million pallet positions and 4,000 vehicles into a platform spanning ambient to -40 °C coverage. Thai Yokorei retains leadership in deep-frozen tuna and poultry exports, but DHL Supply Chain is scaling healthcare racks to erode that dominance in life-science verticals.

Competitive advantage now rests on automation, sustainability, and cross-border reach. AutoStore’s Rayong robot hub ensures Thai 3PLs receive cube-storage modules with 30% shorter lead times than importing from Norway. WICE Logistics layers blockchain timestamps onto transport management feeds, satisfying EU deforestation-free regulation audits for frozen cassava.

Strategic tie-ups are proliferating. Kerry Express secures food-grade volume via Betagro, while Sumisho Global Logistics piggybacks on Sumitomo’s supplier ecosystems for auto parts and frozen noodles. Foreign entrants face licensing checks under the Thai FDA, though investor visas and waived import duties on automation parts lower barriers. Pricing pressure persists from e-commerce platforms building in-house fleets, but higher service expectations favor incumbents with validated processes.

Thailand Cold Chain Logistics Industry Leaders

JWD Group

Thai Yokorei Cold Storage

Linfox Thailand

DHL Supply Chain (Thailand)

Kerry Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DHL Express launched its 15th service center in Thepharak, Thailand, boosting cross-border shipment services across its international network.

- January 2025: Logisteed Thailand opened its newest logistics center at Samut Prakan, near Bangkok. The hub boosts supply chain efficiency for a wide range of sectors by managing goods that require varying temperature ranges.

- December 2024: Linfox International Group expanded in Thailand with a 19,000-square-meter warehouse that features 28,000 pallet spaces, 34 loading bays, and temperature-controlled chambers.

- June 2024: Kerry Express partnered with Betagro to strengthen its 'Kerry Cool' services, delivering customized cold chain solutions for businesses across Thailand.

Thailand Cold Chain Logistics Market Report Scope

Cold chain logistics is the technology and process that safely transports temperature-sensitive goods and products along the supply chain. It relies heavily on science to evaluate and accommodate the link between temperature and perishability.

A comprehensive background analysis of the Thailand cold chain logistics market covers the current market trends, restraints, technological updates, and detailed information on various segments and the industry's competitive landscape. The report also covers the impact of COVID-19 on the market.

The Thailand cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature type (chilled and frozen), and application (fruits and vegetables, dairy products, fish, meat and poultry, processed food, pharmaceuticals, bakery, and confectionary and other applications). The report offers market size and forecasts in values (USD) for all the above segments.

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

| Central |

| Eastern |

| Northern |

| North-Eastern |

| Southern |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

| By Region (Thailand) | Central | |

| Eastern | ||

| Northern | ||

| North-Eastern | ||

| Southern | ||

Key Questions Answered in the Report

What is the value of the Thailand cold chain logistics market in 2026?

The Thailand cold chain logistics market size is valued at USD 2.4 billion in 2026.

How fast will the Thailand cold chain logistics market grow through 2031?

It is projected to expand at a 3.79% CAGR, reaching USD 2.89 billion by 2031.

Which service segment is expanding the quickest?

Value-Added Services is the fastest-growing segment, with a forecast 4.63% CAGR through 2031.

Where is the strongest regional growth expected?

The Eastern region should post the highest growth, at a 4.18% CAGR, driven by EEC incentives.

Which application is expected to outperform overall market growth?

Pharmaceuticals & Biologics will advance at a 5.88% CAGR, outpacing food categories.

How are operators mitigating energy-related cost pressures?

They are deploying rooftop solar, CO₂ refrigeration, and predictive maintenance platforms to lower kilowatt consumption and improve uptime.

Page last updated on: