Erectile Dysfunction Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

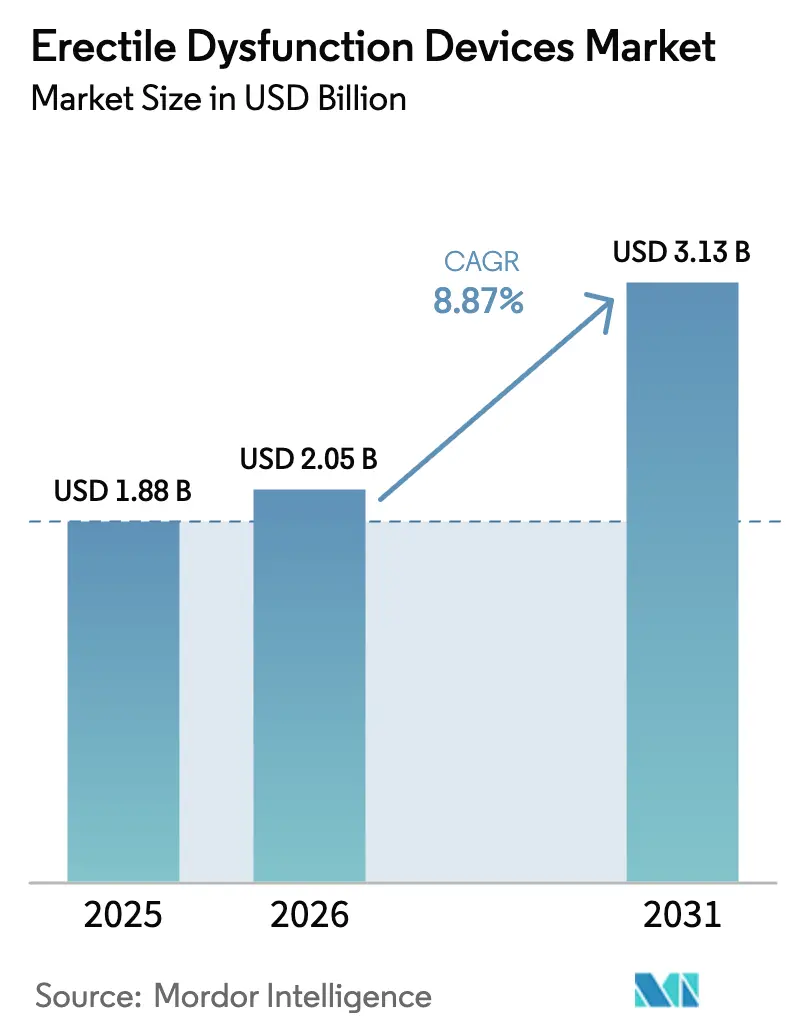

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 3.13 Billion |

| Growth Rate (2026 - 2031) | 8.87% CAGR |

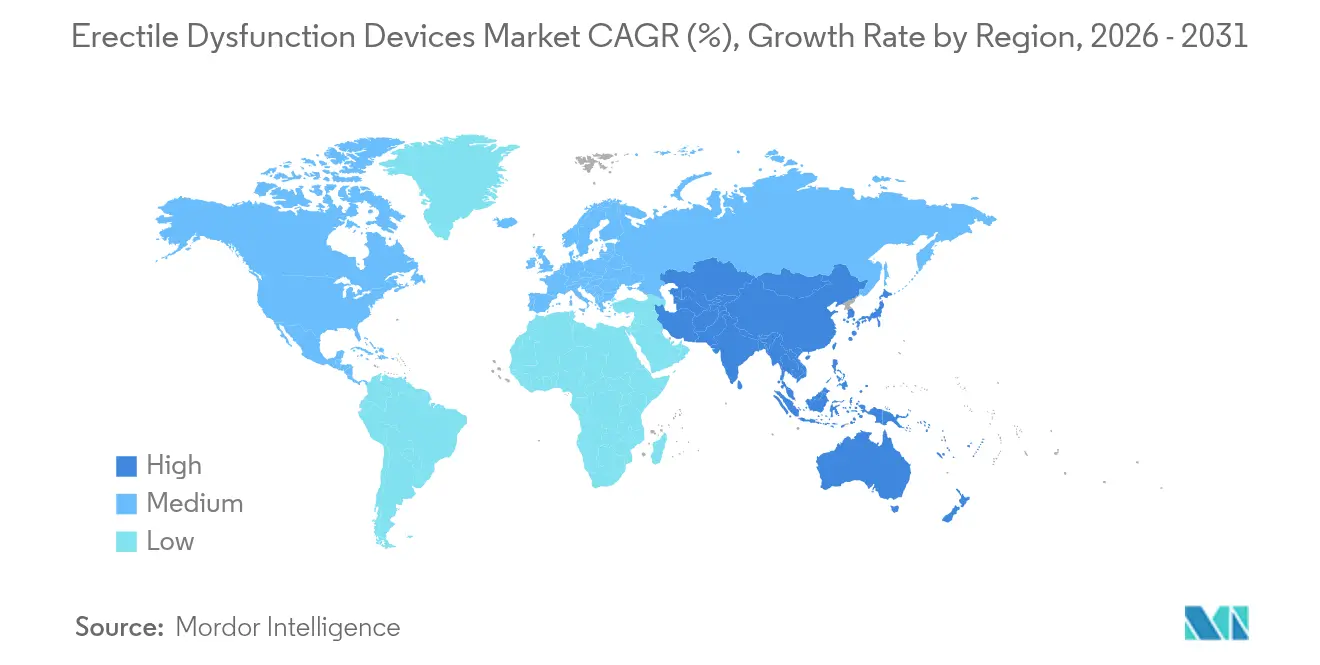

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Erectile Dysfunction Devices Market Analysis by Mordor Intelligence

The erectile dysfunction devices market size in 2026 is estimated at USD 2.05 billion, growing from 2025 value of USD 1.88 billion with 2031 projections showing USD 3.13 billion, growing at 8.87% CAGR over 2026-2031. Rising dissatisfaction with oral phosphodiesterase-5 inhibitors, which show more than 40% real-world non-response, accelerates patient migration toward mechanical or implantable therapies. Device makers are also benefiting from younger-onset prevalence trends, expanded post-prostatectomy protocols, and streamlined tele-prescription rules that support at-home therapy initiation. Concurrently, hospital cost-containment imperatives push outpatient centers to adopt minimally invasive techniques, improving operating margins for providers while preserving quality outcomes. On the supply side, manufacturers are re-engineering bill-of-materials to reduce exposure to silicone shortages and to comply with new vacuum device pressure-range coding, strengthening production resilience.

Key Report Takeaways

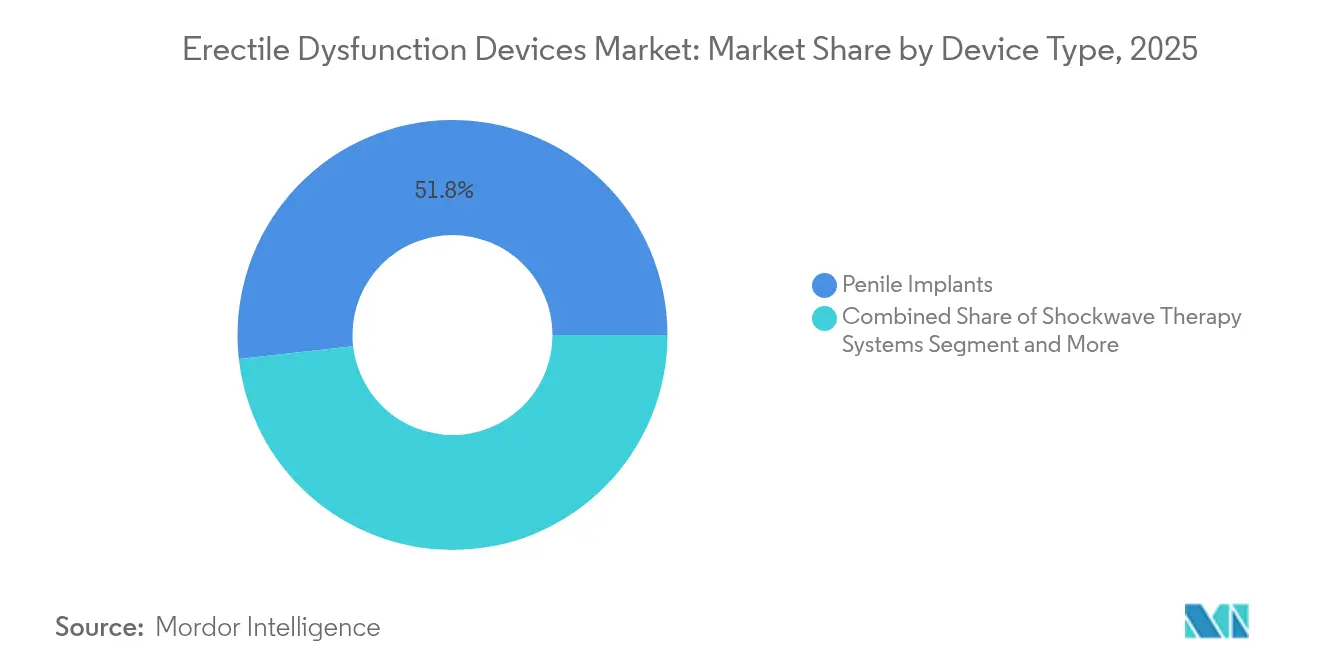

- By device type, penile implants led with 51.78% of erectile dysfunction devices market share in 2025, whereas low-intensity shockwave systems are projected to expand at a 12.03% CAGR through 2031.

- By cause, vascular disorders accounted for 60.01% share of the erectile dysfunction devices market size in 2025; neurological causes show the highest forecast CAGR at 10.63% to 2031.

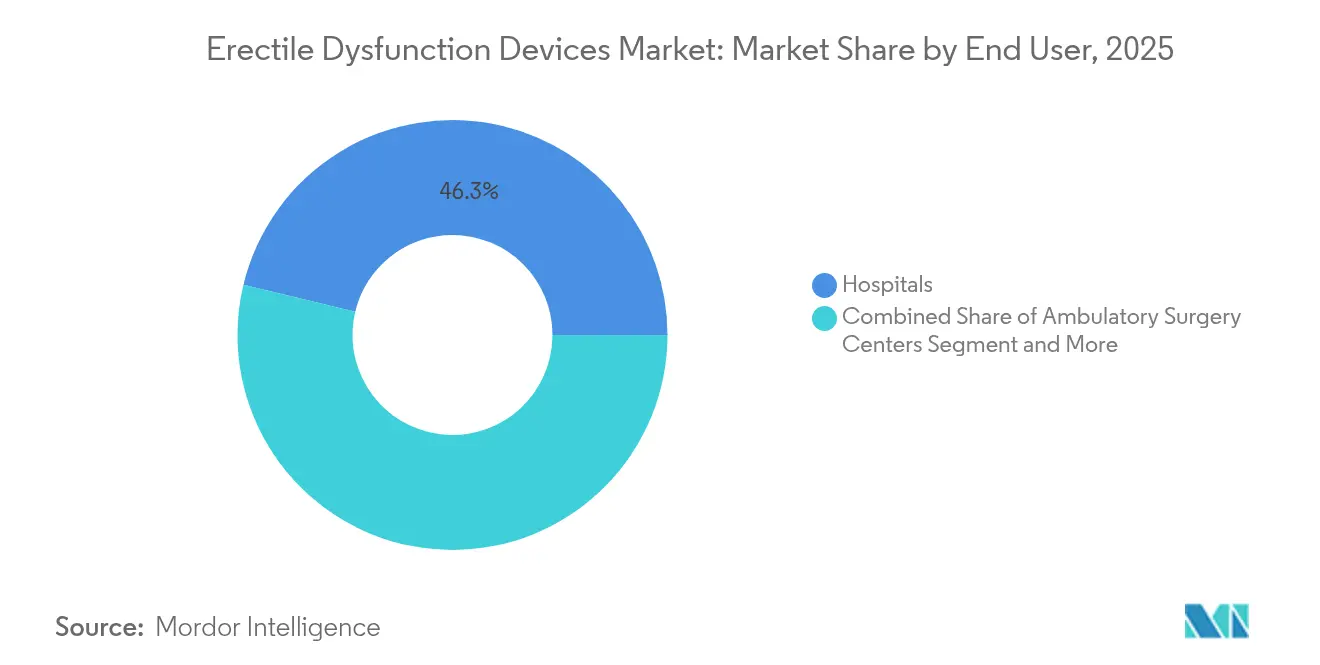

- By end user, hospitals commanded 46.25% of 2025 revenue, but ambulatory surgery centers are advancing at a 10.39% CAGR through 2031.

- By geography, North America captured 41.35% of 2025 revenue, while Asia-Pacific is on track for an 11.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Erectile Dysfunction Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of erectile dysfunction | +2.1% | Global, with highest concentration in North America and Europe | Long term (≥ 4 years) |

| Increasing post-prostatectomy rehabilitation demand | +1.8% | North America and Europe, emerging in Asia-Pacific | Medium term (2–4 years) |

| Rise in R&D and FDA approvals for next-gen ED devices | +1.5% | Global, led by US and EU regulatory pathways | Medium term (2–4 years) |

| High dissatisfaction with oral ED drugs | +1.4% | Global, particularly in developed markets | Short term (≤ 2 years) |

| Tele-prescription laws enabling at-home VED adoption | +1.2% | North America, expanding to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Mini-incision IPP techniques cutting cost and LOS | +0.9% | Global, early adoption in North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Erectile Dysfunction

Post-COVID vascular sequelae further swell the candidate pool, while Google Trends heat-maps uncover high search density in underserved counties, signalling pent-up demand[1]Tingrui Pan, “A Wearable Adaptive Penile Rigidity Monitoring System,” Nature Microsyst Nanoeng, doi.org. Manufacturers respond with culturally sensitive campaigns and discreet wearables, which appeal to younger users seeking reversible solutions. The demographic expansion underpins sustained double-digit unit growth across vacuum and wearable categories within the erectile dysfunction devices market. Momentum is unlikely to ebb as social attitudes toward men’s sexual health continue to liberalize in Asia-Pacific and South America.

Increasing Post-Prostatectomy Rehabilitation Demand

Roughly 58% of radical prostatectomy patients experience erectile dysfunction within two years, a statistic that is reshaping perioperative pathways. Simultaneous penile prosthesis and artificial urinary sphincter placement now supersedes staged procedures, cutting anesthesia time and boosting satisfaction indices. Vacuum erection devices (VEDs) serve as first-line rehabilitation in combination with phosphodiesterase inhibitors, elevating International Index of Erectile Function (IIEF-5) scores faster than pharmacotherapy alone. Medicare and private insurers increasingly reimburse these multimodal pathways, a trend likely to widen adoption beyond high-volume centers.

Rise in R&D and FDA Approvals for Next-Gen ED Devices

The 2024-2025 FDA docket lists multiple 510(k) clearances, including the rechargeable EDP MAX Rc erection device, signaling rapid design-refresh cycles. Boston Scientific’s TENACIO pump adds independent valving and a 27% faster refill rate, marking the biggest implant upgrade in a decade. Alongside implants, AI-enabled diagnostic wearables like the WARM system substitute cumbersome RigiScan tests with real-time rigidity analytics. These innovations funnel venture capital into the erectile dysfunction devices industry and open premium-priced niches that lift average selling prices.

High Dissatisfaction with Oral ED Drugs

Clinical meta-analyses show that 40% of men derive insufficient benefit from phosphodiesterase inhibitors, a gap most common in severe vascular or diabetic cohorts. Out-of-pocket costs amplify the discontent; Medicare modelling pegs annual therapy at USD 696 for sildenafil versus a one-time USD 1,600 co-pay for an inflatable prosthesis over a 10-year life. Physicians therefore escalate to mechanical options sooner, and start-ups pitch discreet wearables that circumvent systemic side-effects, accelerating share gains for the erectile dysfunction devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of pharmacologic alternatives | -1.6% | Global, strongest where generic PDE5 access is high | Long term (≥ 4 years) |

| Social stigma and low patient awareness | -1.3% | Asia-Pacific and Middle East, declining in West | Medium term (2–4 years) |

| Supply-chain fragility in medical-grade silicone | -0.8% | Global manufacturing, heavily Asian hubs | Short term (≤ 2 years) |

| Reimbursement downgrades for shockwave therapy | -0.7% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Availability of Pharmacologic Alternatives

Low-priced generics and mail-order telehealth platforms such as Roman and BlueChew prolong pill dominance in cost-sensitive cohorts[2]Lisa Catanese, “Need a Prescription for an ED Medication?,” Harvard Health, health.harvard.edu. Nasal and topical pipelines add formulation diversity and could stall device conversion rates. Even so, Viatris’ 2024 discontinuation of alprostadil urethral suppositories leaves a therapy void that favors vacuum systems and intracavernosal injections.

Social Stigma & Low Patient Awareness

Attitudinal surveys show 53.1% of Saudi respondents avoid medical advice for erectile dysfunction due to embarrassment, underscoring a continuing education gap. Telemedicine mitigates face-to-face discomfort and nudges uptake, but manufacturers must fine-tune messaging to cultural norms to unlock Asia-Pacific headroom.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Implants Lead Innovation Wave

Penile implants retained 51.78% revenue in 2025 and generated the majority of the erectile dysfunction devices market size attributed to surgical solutions. The latest AMS 700 with TENACIO pump shortens inflation cycles and delivers 10-year durability, features that pushed 2025 unit demand up by double digits in U.S. centers. Such improvements signal why implants still dominate a crowded field of vacuums, wearables, and shockwave consoles. Growth, however, now tilts toward non-invasive categories: low-intensity shockwave platforms logged a 12.03% CAGR and are popular in multidisciplinary men’s-health clinics where physicians package the therapy with platelet-rich plasma injections to lift response rates.

Vacuum constriction cylinders, newly coded under 2025 HCPCS guidelines, enjoy reimbursement clarity that widens payer coverage. Wearables such as Eddie by Giddy achieved FDA registration and posted 88.9% pain-free intercourse scores in a 2024 survey, crowding the niche for mild-to-moderate cases. These varied modalities collectively ensure that the erectile dysfunction devices market remains technologically pluralistic.

By Cause of Dysfunction: Vascular Dominance Drives Innovation

In 2025, vascular etiologies represented 60.01% of therapy volume, underscoring cardiovascular comorbidity as the prime target of emerging gadgets. Shockwave consoles promote neovascularization and yielded a 69% minimal clinically important difference in African trial cohorts three months post-treatment. The erectile dysfunction devices market size for vascular cases will deepen as diabetic and hypertensive patients flow into care pathways. Meanwhile, neurological causes are expanding at 10.63% CAGR, owing to post-COVID neuropathies that lengthen waitlists for specialized neuro-urology consults.

PNAS-reported microrobot technology, which ferries mesenchymal stromal cells directly into cavernous tissue, promises a regenerative alternative that could disrupt vascular and neurogenic treatment algorithms. Psychogenic categories also benefit from AI-assisted decision tools that elevate diagnostic accuracy, guiding clinicians toward bespoke device selections.

By End User: Ambulatory Centers Accelerate Growth

Hospitals accounted for 46.25% revenue in 2025, yet the shift to outpatient settings is unmistakable. Minimally invasive infrapubic approaches reduced infection rates to 0% in straightforward cases, enabling same-day discharge and catalyzing a 10.39% CAGR for ambulatory surgery centers. Clinics and physician-owned offices ride the telehealth wave by bundling vacuum or shockwave packages with virtual follow-up, giving them a cost edge relative to tertiary hospitals. Such dynamics realign value capture within the erectile dysfunction devices market, rewarding providers that can compress operating time while sustaining outcomes.

Geography Analysis

North America remains the fulcrum of revenue, holding 41.35% in 2025 on the back of robust payer frameworks and an installed base of high-volume urologists. Boston Scientific’s interventional urology sales hit USD 633 million in Q1 2025, with erectile prostheses a core component. The region’s clinicians increasingly bypass staged prosthesis-sphincter surgeries, further expanding procedure counts.

Asia-Pacific, however, is the fastest climber at 11.23% CAGR. Japanese retrospective studies validate next-gen vacuums, while China’s domestic producers of silicone reservoirs shrink import reliance. Medical tourism to Turkey, where Coloplast Titan procedures average EUR 10,000, attracts European and Middle Eastern patients seeking price relief. Together, these dynamics are enlarging regional slices of the erectile dysfunction devices market.

Europe exhibits mid-single-digit growth as MDR roll-outs stabilize and payer reviews temper shockwave reimbursements. Key markets such as Germany still fund implants for severe cases, sustaining baseline demand. Latin America and the Middle East are in earlier adoption cycles but benefit from improving cultural openness and international provider partnerships, positioning them as long-term contributors.

Competitive Landscape

The erectile dysfunction devices industry shows moderate concentration. Boston Scientific, Coloplast, and Rigicon control majority of implant unit shipments yet face insurgent wearable and shockwave entrants. Boston Scientific’s USD 3.7 billion acquisition of Axonics broadens its pelvic health continuum, allowing cross-selling into overactive bladder and fecal incontinence pathways. Coloplast’s Titan line secured 5% growth in FY 2024 despite raw-material inflationary pressure that squeezed margins.

Rigicon differentiates through complex-case ergonomics and collagen fleece grafting techniques that restore curvature, earning surgeon loyalty in tertiary referral centers. Start-ups like Ohh-Med and Reach Medical chase non-invasive niches with upgraded wearables and rechargeable vacuums, both benefiting from direct-to-consumer channels. Supply-chain continuity emerges as a battleground; firms investing in dual-source silicone molding or additive-manufactured reservoirs incur lower back-order risk during global shortages.

Erectile Dysfunction Devices Industry Leaders

Coloplast Group

Rigicon, Inc.

Boston Scientific Corporation

Promedon GmBH

Zephyr Surgical Implants

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Boston Scientific launches the TENACIO pump as part of its AMS 700 IPP system, offering a 27% faster refill and independent valve action.

- June 2024: Ohh-Med unveils an ergonomically enhanced wearable erectile dysfunction device to improve user comfort.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the erectile dysfunction devices market as all class-II and class-III medical devices that mechanically or electromechanically enable men to achieve and maintain penile rigidity, including surgically implanted inflatable or malleable prostheses, vacuum constriction systems, and approved low-intensity shockwave generators; ancillary disposables and replacement cylinders are included when sold with the base unit. According to Mordor Intelligence, accessories marketed purely for sexual wellness, oral pharmaceuticals, topical gels, and regenerative biologics are outside this boundary.

Scope Exclusion: Over-the-counter rings, herbal pumps, and investigational energy-based prototypes still in IDE trials are not modeled.

Segmentation Overview

- By Device Type

- Penile Implants

- Vacuum Constriction Devices (VED)

- Shockwave Therapy Systems

- Other Device Types

- By Cause of Dysfunction

- Vascular Disorder

- Neurological Disorder

- Other Causes

- By End User

- Hospitals

- Clinics & Specialty Centers

- Ambulatory Surgery Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing urologists, procurement managers in hospitals and ambulatory surgery centers, and regional distributors across North America, Europe, and Asia-Pacific. The discussions verified post-prostatectomy implant uptake, confirmed typical vacuum-pump replacement cycles, and refined shockwave device ASP progression before we finalized model assumptions.

Desk Research

We began with published device approval databases from the US FDA and the EU's EUDAMED, which clarified installed base and launch timelines. Trade statistics from UN Comtrade and Volza helped us approximate cross-border flows of silicone implants and pump kits, while hospital procedure volumes were benchmarked against the American Urological Association, Europe's EAU registries, and Japan's JUA statistics. Company 10-Ks, investor decks, and selected D&B Hoovers profiles supplied average selling prices and channel mixes, which were complemented by peer-reviewed studies in journals such as the Journal of Sexual Medicine and The Lancet Regional Health. These sources are illustrative; many additional publications and datasets informed desk research and validation.

Market-Sizing & Forecasting

A top-down reconstruction started with the prevalent ED population by age cohort, overlaid with treatment-seeking rates and device penetration ratios sourced from insurance claims and survey inputs; results were cross-checked with a bottom-up roll-up of leading manufacturers' shipments and channel checks to reconcile gaps. Key variables in the model include: 1) prostatectomy procedures, 2) diabetes prevalence, 3) outpatient reimbursement tariffs, 4) average selling price shifts, and 5) elective surgery deferral indices. Forecasts are generated through multivariate regression linking these drivers to historical device volumes, followed by scenario analysis to stress-test reimbursement or technology-adoption shocks. Where shipment data were missing, average implant lifespans and re-operation rates filled the void.

Data Validation & Update Cycle

Outputs undergo anomaly screening, variance checks against independent procedure and trade data, and two-step peer review before sign-off. The dataset refreshes each year, with interim revisions if material recalls, reimbursement changes, or landmark device approvals occur; just before publication, one analyst re-runs the latest quarter's inputs to keep clients current.

Why Mordor's Erectile Dysfunction Devices Baseline Commands Reliability

Published estimates often diverge because firms choose different device mixes, patient cohorts, and currency bases.

Key gap drivers include: some studies bundle drug revenues, others ignore shockwave systems, and a few convert prices at spot rates without inflation parity adjustments; Mordor's model anchors on clearly disclosed unit volumes, consistent 2024 real-term dollars, and an annual refresh that trims vintage bias.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.88 B | Mordor Intelligence | - |

| USD 1.81 B | Global Consultancy A | Excludes shockwave devices; uses 2023 exchange rates without inflation alignment |

| USD 1.70 B (2023) | Industry Association B | Bundles penile implants only; no vacuum device volumes; limited geographic rollout |

In sum, the disciplined device taxonomy, dual-path sizing logic, and continual refresh cadence give Mordor's baseline a balanced, transparent footing that decision-makers can replicate with confidence.

Key Questions Answered in the Report

What is the growth rate of the erectile dysfunction devices market from 2026 to 2031?

The market is projected to expand at a 8.87% CAGR, climbing from USD 2.05 billion in 2026 to USD 3.13 billion in 2031.

Which device type currently holds the largest market share?

Penile implants lead with 51.78% of 2025 revenue, buoyed by innovations such as Boston Scientific’s TENACIO pump.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to post the highest regional CAGR at 11.23%, driven by stronger healthcare infrastructure and diminishing cultural barriers.

Why are more patients moving from oral ED drugs to devices?

Around 40% of users do not respond adequately to PDE5 inhibitors and face rising out-of-pocket costs, so many shift to mechanical or implantable options for reliable results.

What fuels the rapid growth of ambulatory surgery centers in this market?

Mini-incision and no-touch implant techniques enable same-day discharge, propelling ambulatory centers to a 10.39% CAGR as procedures migrate from hospitals.

Page last updated on: