Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

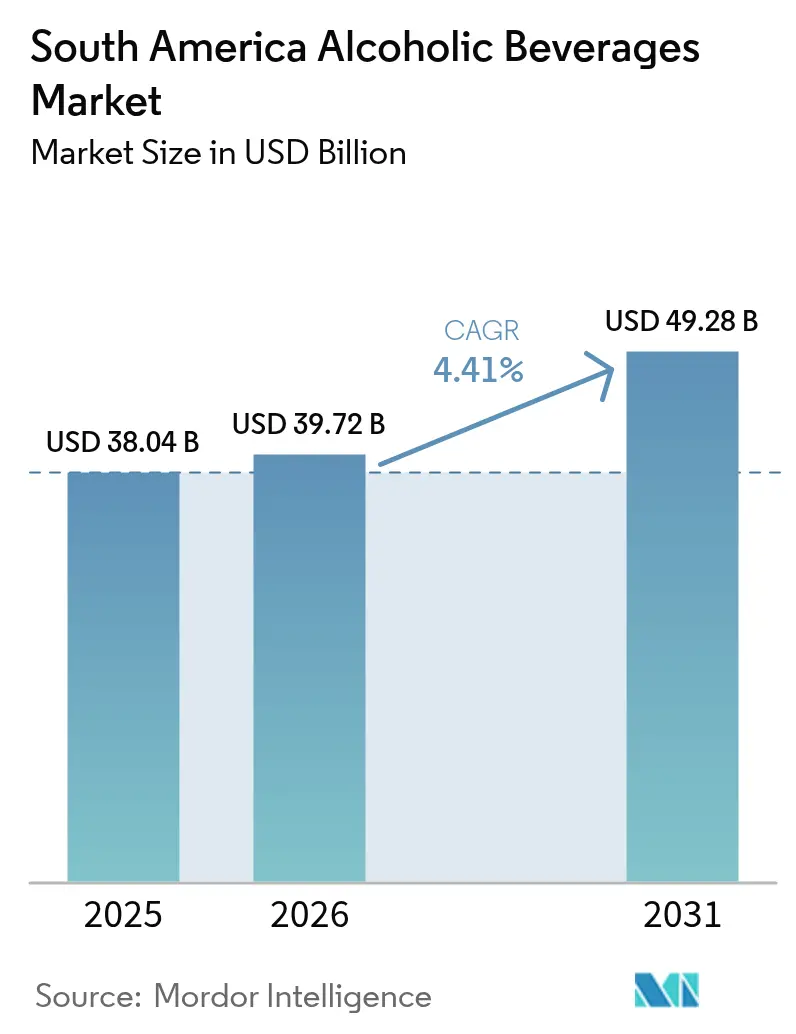

| Base Year Market Size (2025) | USD 38.04 Billion |

| Market Size (2026) | USD 39.72 Billion |

| Market Size (2031) | USD 49.28 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Alcoholic Beverages Market Analysis by Mordor Intelligence

South American alcoholic beverages market size in 2026 is estimated at USD 39.72 billion, growing from 2025 value of USD 38.04 billion with 2031 projections showing USD 49.28 billion, growing at 4.41% CAGR over 2026-2031. The market growth is primarily driven by shifting consumer preferences toward premium and craft beverages, particularly among younger demographics. Regulatory changes across South American countries, including revised taxation policies and distribution regulations, are reshaping the market landscape. Additionally, industry consolidation through mergers and acquisitions is helping companies navigate economic challenges while expanding their market presence. Furthermore, Regulatory shifts create both opportunities and challenges, with Brazil's 2025 tax reform potentially reducing compliance costs while Colombia introduces health-focused taxation on ultra-processed beverages

Key Report Takeaways

- By product type, beer led with 61.54% of South America's alcoholic beverage market share in 2025; spirits are forecast to expand at a 5.31% CAGR through 2031.

- By end user, male consumers held 68.02% share of the South America alcoholic beverages market size in 2025, while female consumption is advancing at a 4.93% CAGR to 2031.

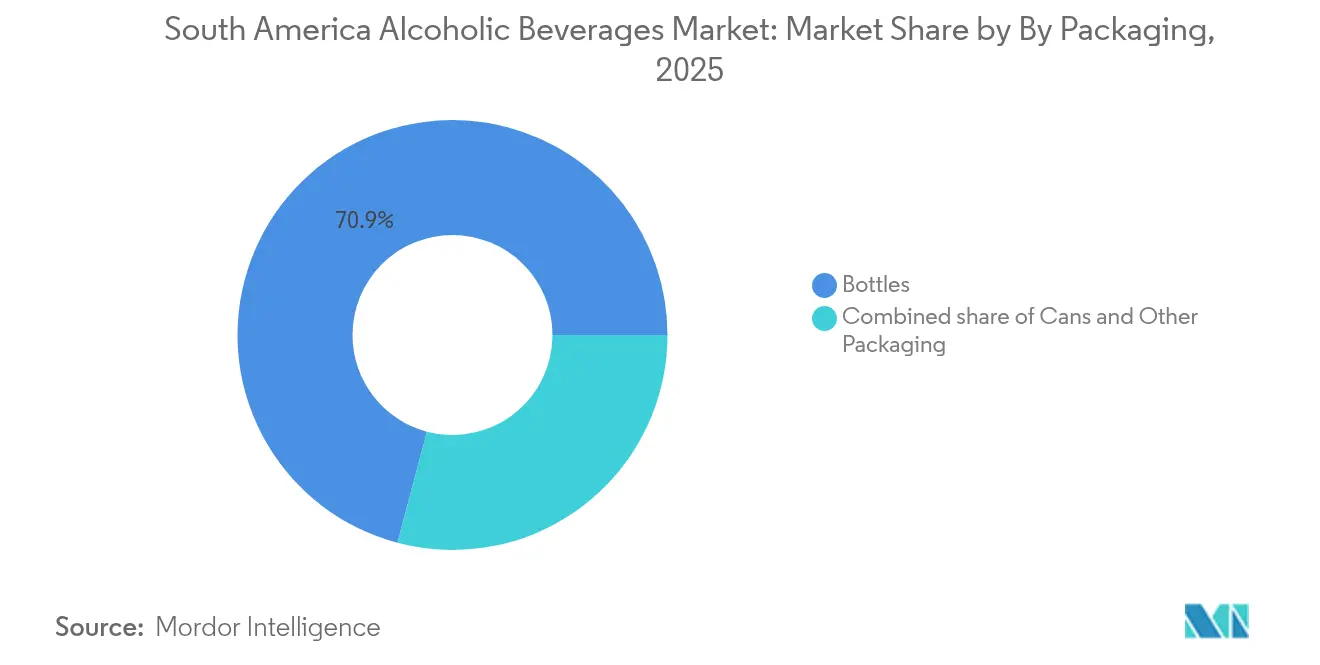

- By packaging, bottles accounted for a 70.88% share of the South America alcoholic beverages market size in 2025; cans record the quickest growth at 5.62% CAGR through 2031.

- By distribution channel, the off-trade segment captured 67.74% of South America alcoholic beverages market share in 2025, and it is poised for a 6.17% CAGR between 2026-2031.

- By geography, Brazil dominated with 47.85% revenue share in 2025; Peru is projected to post the highest 5.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Alcoholic Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and craft-product boom | +1.2% | Brazil, Chile, Argentina with spillover to Colombia, Peru | Medium term (2-4 years) |

| Product innovation and new flavors | +0.8% | Global, with early adoption in Brazil, Colombia | Short term (≤ 2 years) |

| Explosive growth of low and functional RTDs | +1.1% | Brazil core, expanding to Argentina, Chile | Short term (≤ 2 years) |

| Growing cocktail culture | +0.7% | Urban centers across Brazil, Argentina, Chile, Colombia | Medium term (2-4 years) |

| Cultural heritage and local traditions | +0.5% | National, with strong influence in Peru, Brazil, Argentina | Long term (≥ 4 years) |

| Influence of tourism and festivals | +0.4% | Tourism hubs in Brazil, Argentina, Chile, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization and Craft-Product Boom

The craft beer revolution transforms South America's alcoholic beverages landscape as consumers increasingly seek authentic, artisanal experiences over mass-market alternatives. Zero-alcohol beer in Brazil has experienced remarkable growth in recent years, highlighting how premiumization is expanding beyond conventional alcoholic beverages and gaining traction among health-conscious consumers. This trend reflects deeper consumer sophistication, where price sensitivity coexists with willingness to pay premiums for perceived quality and unique positioning. Regional craft breweries leverage local ingredients and cultural narratives to differentiate from multinational brands, creating micro-markets that command higher margins despite volume constraints. The premiumization wave extends to spirits, where aged rums, artisanal cachaças, and small-batch piscos gain traction among urban millennials and Generation Z consumers seeking Instagram-worthy experiences. Traditional players respond through acquisition strategies and premium line extensions, recognizing that craft positioning often translates to sustainable competitive advantages in saturated markets.

Product Innovation and New Flavors

Innovation cycles accelerate as beverage companies race to capture evolving taste preferences and lifestyle demands across South America's diverse consumer base. The ready-to-drink segment experiences explosive innovation, with Absolut and Sprite launching collaborative RTD products in Brazil during 2024, targeting consumers seeking convenience without compromising on brand prestige. Functional beverages gain prominence as health-conscious consumers demand products that deliver beyond basic refreshment, incorporating adaptogens, probiotics, and natural energy enhancers. Companies are forming partnerships to develop products such as non-alcoholic coffee beer, showcasing cross-category innovation that taps into regional coffee traditions while aligning with evolving preferences for mindful consumption. These innovations often succeed by combining familiar local flavors with international formats, creating products that feel both globally sophisticated and culturally relevant.

Explosive Growth of Low and Functional RTDs

Ready-to-drink beverages represent the fastest-evolving segment within South America's alcoholic beverages market, driven by urbanization, time-pressed lifestyles, and premiumization trends that favor convenience without quality compromise. Itaipava's October 2024 entry into canned cocktails demonstrates how traditional beer brands expand into higher-margin RTD categories to capture share from both spirits and wine segments. The functional RTD category particularly resonates with health-conscious consumers who seek alcohol products with added benefits, such as electrolytes, vitamins, or botanical extracts that align with wellness positioning. Low-alcohol RTDs address the growing moderation trend, allowing consumers to participate in social drinking occasions while maintaining health and lifestyle goals. These products often command premium pricing due to sophisticated flavor profiles and positioning, making them attractive for manufacturers seeking margin expansion. The segment benefits from e-commerce growth and convenience retail expansion, as RTDs align perfectly with impulse purchasing behaviors and on-the-go consumption patterns that characterize modern urban lifestyles.

Growing Cocktail Culture

Urban sophistication drives cocktail culture expansion across South America's major metropolitan areas, creating new consumption occasions and premium positioning opportunities for spirits brands. This trend benefits from social media influence, where visually appealing cocktails serve as lifestyle signaling and content creation opportunities for younger demographics. Bartending education programs and craft cocktail establishments proliferate in cities like São Paulo, Buenos Aires, and Bogotá, creating knowledgeable consumer bases that appreciate premium ingredients and artisanal preparation techniques. The cocktail renaissance also drives demand for super-premium spirits, bitters, and specialty mixers, expanding category boundaries and creating new revenue streams for established players. Home cocktail preparation accelerated during pandemic restrictions and continues growing as consumers invest in bar equipment and premium ingredients for entertaining, supported by online tutorials and social media inspiration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating excise taxes and complex regulations | -0.9% | Brazil, Colombia with regulatory spillover effects | Short term (≤ 2 years) |

| Rising health concerns and shift toward non-alcoholic alternatives | -0.7% | Urban centers across Brazil, Chile, Argentina | Medium term (2-4 years) |

| Climate-driven water stress hitting barley and grape yields | -0.6% | Argentina, Chile wine regions, Brazil agricultural zones | Long term (≥ 4 years) |

| Counterfeit products and informal alcohol trade | -0.4% | Peru, Colombia, border regions across South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Excise Taxes and Complex Regulations

Regulatory complexity intensifies across South America as governments balance public health objectives with revenue generation, creating compliance burdens that disproportionately impact smaller producers and importers. Colombia introduces health-focused taxation through DIAN forms targeting ultra-processed beverages in 2025, reflecting regional trends toward sin taxes that create pricing pressures and administrative complexity[1]Source: DIAN, “Ley de Impuestos Saludables 2025,” dian.gov.co. These regulatory shifts often favor large multinational corporations with dedicated compliance teams while creating barriers for craft producers and importers who lack the resources to navigate evolving requirements. Tax harmonization remains elusive across South American markets, forcing companies to maintain separate compliance systems for each jurisdiction and limiting economies of scale in production and distribution strategies.

Rising Health Concerns and Shift toward Non-Alcoholic Alternatives

Health consciousness accelerates across South America's urban populations, driven by wellness trends, fitness culture, and medical awareness campaigns that position alcohol consumption as incompatible with healthy lifestyles. The Pan American Health Organization's guidelines on alcohol policy create pressure for governments to implement stricter regulations and public health messaging that influence consumer behavior[2]Source: Pan American Health Organization, “Alcohol Policy in the Americas,” paho.org. Non-alcoholic alternatives gain sophisticated positioning and distribution, moving beyond traditional soft drinks to include complex botanical beverages, functional drinks, and alcohol-free spirits that deliver similar sensory experiences without intoxication effects. This trend particularly impacts premium segments where health-conscious consumers previously drove growth, forcing alcoholic beverage companies to develop non-alcoholic line extensions or risk losing share to specialized wellness brands. The moderation movement also influences consumption patterns, with consumers choosing quality over quantity and seeking lower-alcohol options that allow social participation without health compromise, creating both challenges and opportunities for established players willing to innovate beyond traditional formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirits Drive Premium Growth Despite Beer Dominance

Beer maintains commanding market leadership with 61.54% share in 2025, reflecting South America's strong brewing traditions and price-sensitive consumer base, yet spirits emerge as the fastest-growing segment with 5.31% CAGR through 2031. This growth divergence signals fundamental shifts in consumption patterns as urbanization and rising disposable incomes drive premiumization trends that favor higher-margin spirit categories. Wine occupies a stable middle position, particularly strong in Argentina and Chile, where domestic production advantages create competitive pricing and cultural affinity.

Spirits growth acceleration reflects cocktail culture expansion, premiumization trends, and strategic brand positioning that targets aspirational consumers seeking sophisticated drinking experiences. The segment benefits from tourism growth, urban nightlife development, and social media influence that positions premium spirits as lifestyle signaling tools. Beer's mature market position creates defensive strategies focused on innovation, packaging optimization, and distribution efficiency rather than aggressive volume expansion, while wine faces pressure from climate-related production challenges and international competition that constrains growth potential despite regional production advantages.

By End User: Female Segment Accelerates Amid Changing Demographics

Male consumers dominate with 68.02% market share in 2025, reflecting traditional consumption patterns and cultural norms across South America, while female consumption accelerates at 4.93% CAGR through 2031 as brands recognize this demographic's growth potential and purchasing power. This shift reflects broader social changes, including urbanization, workforce participation, and evolving gender roles that normalize female alcohol consumption across previously conservative markets. Female-targeted products emphasize lower alcohol content, sophisticated flavors, wellness positioning, and premium packaging that appeals to quality-conscious consumers willing to pay premiums for products that align with lifestyle aspirations.

The female segment's growth trajectory creates strategic opportunities for brands that successfully position products beyond traditional male-oriented marketing approaches. Marketing strategies increasingly emphasize social responsibility, health consciousness, and premium positioning that resonates with female consumers' decision-making criteria, while traditional male-focused beer marketing adapts to include broader demographic appeal without alienating core constituencies.

By Packaging: Cans Gain Momentum Through Sustainability and Convenience

Bottles retain a dominant market position with 70.88% share in 2025, supported by traditional preferences, premium positioning, and established supply chains across South America's diverse retail landscape, yet cans experience accelerated adoption at 5.62% CAGR through 2031, driven by sustainability concerns and on-the-go consumption trends. This packaging evolution reflects changing consumer priorities where environmental consciousness intersects with convenience demands, creating opportunities for brands that successfully communicate sustainability benefits while maintaining product quality and brand prestige.

Cans' growth acceleration benefits from several converging trends, including outdoor recreation popularity, e-commerce expansion, and sustainability positioning that appeals to environmentally conscious consumers. Itaipava's October 2024 entry into canned cocktails demonstrates how packaging innovation enables category expansion and premium positioning within traditionally bottle-dominated segments. Regulatory influences include container deposit schemes and recycling mandates that favor aluminum's recyclability advantages over glass transportation costs and breakage risks, while retail trends toward convenience formats and impulse purchasing support canned products' shelf placement and consumer accessibility across diverse retail channels.

By Distribution Channel: Off-Trade Dominance Strengthens Through Digital Integration

Off-trade channels command 67.74% market share in 2025 and accelerate growth at 6.17% CAGR through 2031, reflecting consumer preferences for convenience, price transparency, and product variety that traditional retail formats provide more effectively than on-premise establishments. This channel dominance intensifies through e-commerce integration, convenience store expansion, and retail format innovation that brings alcoholic beverages closer to consumers' daily shopping routines. On-trade establishments face structural challenges, including regulatory complexity and changing social behaviors that favor home consumption and private entertainment over traditional bar and restaurant experiences.

Off-trade growth is fueled by the expansion of convenience retail, as widespread store networks across Latin America enhance distribution reach, encourage impulse buying, and boost brand exposure. Specialty liquor stores within off-trade channels provide premiumization opportunities and expert curation that appeals to sophisticated consumers seeking product education and discovery experiences, while other off-trade channels, including supermarkets and hypermarkets, leverage scale advantages and promotional capabilities to drive volume growth across price-sensitive segments.

Geography Analysis

Brazil's market leadership with 47.85% share in 2025 reflects its demographic scale, economic development, and established beverage culture that supports both volume consumption and premiumization trends across diverse consumer segments. The country benefits from domestic production capabilities, sophisticated distribution networks, and regulatory frameworks that generally support industry growth despite periodic tax reform discussions. Argentina and Chile leverage wine production advantages and cultural sophistication to maintain strong positions in premium segments, though economic volatility and climate challenges create periodic disruptions that affect growth consistency.

Peru emerges as the fastest-growing geography with a 5.67% CAGR through 2031, driven by economic development, urbanization, and cultural openness to international brands and consumption occasions that expand beyond traditional patterns. The country benefits from tourism growth, mining sector prosperity, and demographic trends that favor younger consumers with higher disposable incomes and cosmopolitan preferences. Colombia demonstrates steady growth supported by economic stability, urban development, and cultural factors that embrace both traditional beverages like aguardiente and international brands seeking regional expansion.

Rest of South America encompasses diverse smaller markets including Uruguay, Paraguay, Ecuador, and others that collectively represent significant opportunities for regional expansion and niche positioning strategies. These markets often serve as testing grounds for new products and distribution approaches before broader regional rollouts, while also providing sourcing advantages for specific ingredients and production capabilities. Regulatory harmonization efforts through organizations like MERCOSUR create opportunities for streamlined operations and reduced compliance costs, though implementation remains inconsistent across jurisdictions and product categories.

Regulatory Landscape

Alcoholic beverage regulation in South America continues to shift across licensing, product standards, and manufacturing and trade controls, with Brazil, Argentina, Colombia, and Peru providing recent anchors for compliance teams. In Brazil, the Ministry of Agriculture and Livestock (MAPA) regulates beverages through product registration and related controls (including SIPEAGRO), and Portaria SDA/MAPA No. 1,343 (July 29, 2025) opened a public consultation on requirements and controls for beverage manufacturing practices and import/export processes, reinforcing ongoing standardization.

Argentina strengthened technical governance for wine and adjacent categories through the Instituto Nacional de Vitivinicultura (INV) and updates to the Argentine Food Code. INV Resolution 37/2025 approved a consolidated INV Regulatory Digest for production, industrialization, and trade of wine and wine derivatives, effective January 1, 2026, while INV Resolution 21/2025 set minimum real alcohol content limits for 2025 vintage wines. Colombia adjusted entry and operating requirements via Decree 1083/2025 (October 15, 2025), removing mandatory BPM (Good Manufacturing Practices) certification as a prerequisite for sanitary registration of alcoholic beverages, and shifting BPM toward a voluntary certification pathway under INVIMA. Peru advanced anti-adulteration and safety oversight through PRODUCE actions, including Ministerial Resolution 162-2025-PRODUCE (April 26, 2025) to publish a draft regulation supporting Law 29632 on eradicating informal/adulterated alcohol, and Directoral Resolution 00003-2026-PRODUCE-DGPAR (May 13, 2026) repealing a prior authorization format tied to methyl alcohol import/export controls.

Value Chain Analysis

The value chain runs from agricultural inputs and industrial materials (barley, grapes, sugarcane/molasses for spirits, and packaging inputs such as glass and aluminum) to brewing, distillation, fermentation, and bottling or canning. It then moves through route-to-market intermediaries including distributors, wholesalers, modern retail, proximity outlets, specialty liquor stores, and on-trade accounts. Market structure in the region favors scaled players that can absorb volatility in inputs and packaging while keeping compliant operations across multiple jurisdictions, and premiumization and RTD innovation are raising expectations for blending, flavoring, and packaging capabilities.

On the manufacturing and distribution side, capacity buildouts and vertical moves are tightening control over key links. For example, HEINEKEN expanded brewing capacity in Brazil (Igarassu, Pernambuco) in 2025, and Diageo added proprietary RTD manufacturing capability in Brazil in 2026 by inaugurating a Smirnoff Ice line at Itaitinga, Ceara, supporting faster replenishment and improved control over formulation and packaging for ready-to-drink products. Logistics remains a constraint, especially in Brazil, where export and import corridors depend heavily on major ports and congestion and infrastructure bottlenecks can lift lead times and costs for imported inputs (including certain wine and spirits materials) and for regional distribution. Companies increasingly respond through local production, packaging supply arrangements, and tighter planning and inventory practices to maintain service levels across off-trade and on-trade channels.

Competitive Landscape

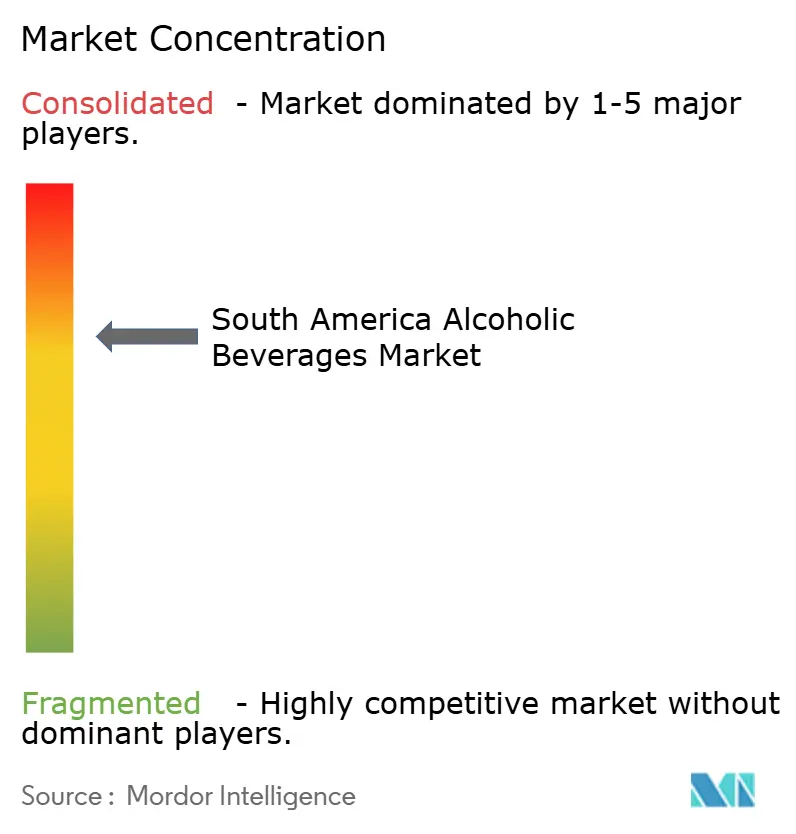

The South America alcoholic beverages market exhibits moderate concentration with a score of 7 out of 10, reflecting established multinational dominance alongside resilient regional players and emerging craft producers that challenge traditional market structures. Major players, including Ambev, Heineken, and Diageo, maintain significant market positions through scale advantages, distribution networks, and brand portfolios that span multiple categories and price points, yet face increasing pressure from premiumization trends that favor smaller, specialized producers with authentic positioning and local market knowledge.

Strategic patterns emphasize vertical integration, premium portfolio expansion, and digital transformation initiatives that enhance consumer engagement and operational efficiency across diverse geographic markets. White-space opportunities emerge in functional beverages, low-alcohol innovations, and sustainable packaging solutions that address evolving consumer preferences, while regulatory compliance creates barriers that favor established players with dedicated legal and regulatory teams.

Technology adoption accelerates across supply chain optimization, consumer data analytics, and direct-to-consumer sales channels that bypass traditional distribution intermediaries and create new competitive advantages. Emerging disruptors focus on sustainability positioning, health-conscious formulations, and digital-native marketing approaches that resonate with younger demographics seeking authentic brand experiences and social responsibility alignment.

South America Alcoholic Beverages Industry Leaders

Anheuser-Busch InBev

Heineken N.V.

Grupo Peñaflor

Diageo Plc

CCU S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premium beer, RTDs, and packaging localization are prominent whitespace areas as companies invest to secure supply and support faster innovation cycles. In Brazil, Ambev inaugurated a glass bottle factory in Carambeí, Parana (150 million euros; 600 million bottles per year) and announced an additional R$ 300 million to expand premium beer production at its Cervejaria Equatorial plant in Sao Luis, Maranhao, signaling continued portfolio upgrading alongside supply resilience. Upstream reinforcement is also visible in malting expansion, such as Agraria securing BNDES financing (R$ 49.8 million) to expand its malting plant in Guarapuava, Parana, targeting a 25% production capacity increase, which supports brewers managing raw material availability and cost.

Trade and standards changes are also reshaping competitive spaces for wine and spirits while creating new differentiation levers. The Mercosur-EU agreement entering its implementation phase on May 1, 2026, with phased tariff reductions for European wines over eight years, raises the premium import challenge while sharpening incentives for domestic producers to compete through sparkling wines, higher-value SKUs, and stronger distribution. In spirits, quality and safety compliance can become a market lever as standards tighten, illustrated by Peru updating national technical standards (NTP) for vodka and anisado in July 2026 to reinforce production and commercialization criteria. At the same time, regulatory uncertainty around alcohol taxation and enforcement intensity across markets keeps the focus on compliant product design (including lower-alcohol and no/low alternatives) and channel strategies that balance on-trade activation with the region's off-trade scale.

Recent Industry Developments

- July 2026: Heineken submitted materials to Brazil's antitrust authority Cade alleging Ambev breached a 2023 settlement related to exclusive supply arrangements with bars and restaurants, while Ambev publicly denied non-compliance. The dispute keeps exclusivity and on-trade contracting practices under heightened scrutiny, with direct implications for route-to-market access and promotional execution in Brazil.

- June 2025: Gunnen, a pure malt low-carb beer, launched in Brazil's Southeast region across Sao Paulo, Minas Gerais, Rio de Janeiro, and Espirito Santo. The launch underscores continued product reformulation and segmentation around moderation and wellness positioning within beer, particularly in high-consumption states where new propositions scale fastest.

- October 2024: Itaipava entered the canned cocktails space, extending a mainstream beer brand into RTDs and leveraging can formats for convenience-led consumption occasions. The move reflects how established brewers are using RTDs to capture higher-margin occasions and diversify beyond traditional beer demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of alcoholic beverages sold for consumption across South America, covering products such as beer, wine, and spirits through on-trade and off-trade routes.

Scope exclusions: Non-alcoholic or zero-alcohol drink variants and non-beverage alcohol uses (industrial, medical, or fuel) are excluded from this sizing.

Segmentation Overview

- By Product Type

- Beer

- Ale Beer

- Lager

- Non/Low-Alcohol Beer

- Others

- Wine

- Fortified Wine

- Still Wine

- Sparkling Wine

- Other Wine Types

- Spirits

- Brandy and Cognac

- Liqueur

- Rum

- Tequila and Mezcel

- Whiskies

- White Spirits

- Other Spirit Types

- Others

- Beer

- By End User

- Male

- Female

- By Packaging

- Bottles

- Cans

- Others

- By Distribution Channel

- On-Trade

- Off-Trade

- Specialty/Liquor Stores

- Other Off Trade Channels

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting fact base for production, trade, taxation, and consumption context across key South American countries. We relied on public statistics and reporting such as national statistics offices, customs and trade portals, central bank macro series, and health and alcohol-control agencies where available.

To keep assumptions grounded, we also reviewed sources such as alcohol and beverage trade associations, peer-reviewed journals on alcohol consumption patterns, and official tariff and excise frameworks that influence pricing. Company filings, investor presentations, and reputable press were then used to understand portfolio shifts, route-to-market changes, and premiumization signals. In parallel, we used a paid subscription database for company financials and news, and an import-export shipment-level database to sanity-check cross-border flows where it mattered. These examples are not exhaustive, and we also used other public and paid sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and survey inputs were used to confirm what is happening on the ground across beer, wine, and spirits, especially around channel mix, pricing moves, and demand elasticity. We spoke with brand owners, distributors, importers, retailers, and on-trade operators, then used follow-ups to close gaps that desk research could not resolve consistently across countries. Since this is a multi-country market, we balanced responses across APAC, EMEA, and the Americas based on where decision makers and trade flows connect most directly to South America coverage.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 37% |

| Mid tier: 48% | Functional/Unit leaders: 28% | EMEA: 37% |

| Smaller Players: 22% | Managers: 56% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a mix of top-down and bottom-up checks, so the totals stay practical and explainable for South America coverage. On the top-down side, alcohol demand pools are reconstructed using country consumption signals and value translation, then aligned to South America coverage with consistent currency timing and channel treatment. After that, selective bottom-up approximations are used to verify the outputs, such as supplier and distributor roll-ups in sampled countries, and price per liter checks against observed retail and on-trade menus.

Key inputs used in the model include population of legal drinking age, per capita alcohol consumption trends, on-trade versus off-trade share shifts, excise tax and duty movements that affect shelf pricing, and import dependence for specific beverage types. We also track premiumization indicators (mix shift toward higher priced SKUs) and inflation pass-through behavior, because these can change value growth even when volumes are stable.

Forecasts are produced using scenario analysis supported by a simple multivariate regression layer for the biggest drivers, followed by analyst adjustments informed by interview consensus on pricing, channel recovery, and regulation. Where bottom-up visibility is uneven for smaller markets, gaps are handled by using proxy indicators from similar countries and then tightening them through channel checks and trade flow reasonableness tests.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and then reviewed for outliers before sign-off. If a country shows a sharp swing that is not supported by tax changes, trade data, or channel commentary, we reopen the assumption and trigger interview callbacks to confirm what changed.

A multi-step analyst review is followed so calculations, currency conversions, and scope mapping errors are caught early. Reports are refreshed annually, with interim updates added when material events occur such as major tax reforms or step-changes in inflation and pricing rules. Before delivery, we do a fresh pass on key inputs so clients get the most current view available at the time.

Mordor Intelligence's South America Alcoholic Beverage Market Size Versus Other Published Estimates

It is common to see different market sizes for alcoholic beverages, even when the geography name looks the same. In most cases, the gap comes from what product set is counted, how channels are treated, which year is used as the anchor, and whether pricing is modeled using stable average prices or fast-moving retail inflation.

Some published figures broaden the scope to all of Latin America and often add ready-to-drink cocktails and online-only alcohol retail as a distinct counted category. In Mordor Intelligence, the total is kept to South America and is counted through beer, wine, and spirits across on-trade and off-trade, which avoids double counting channel overlap and keeps the value tied to a consistent beverage definition.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 38.04 B (2025) | |

| Industry Publisher A | USD 37.05 B (2025) | Uses a broader Latin America framing but the definition and country coverage are not clearly reconciled, and channel treatment is presented at a high level that can miss on-trade pricing effects. |

| Regional Consultancy B | USD 38.04 B (2025) | Includes RTD alcoholic beverages and adds online as a separate channel layer, which can inflate totals if sales are already counted within off-trade and if RTD is not separated consistently across countries. |

The table shows that the spread is mostly explained by scope and counting logic, not by a single demand assumption. When product types and channels are defined in a clean, repeatable way, the market value can be traced back to consumption signals, price movement, and country coverage choices, which makes the final number easier to compare year over year.

Key Questions Answered in the Report

What is the forecast value for South America alcoholic beverage market by 2031?

The market is projected to reach USD 49.28 billion by 2031, reflecting a 4.41% CAGR.

Which product type is expanding fastest in South America alcoholic beverages market?

Spirits are set to grow at a 5.31% CAGR, outpacing beer and wine.

Why are cans gaining popularity in South America alcoholic beverage market?

Aluminum’s recyclability and on-the-go convenience drive a 5.62% CAGR for canned formats.

Which country shows the highest growth momentum in alcoholic beverages?

Peru leads with a predicted 5.67% CAGR through 2031 owing to tourism and rising incomes.

Page last updated on: