Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

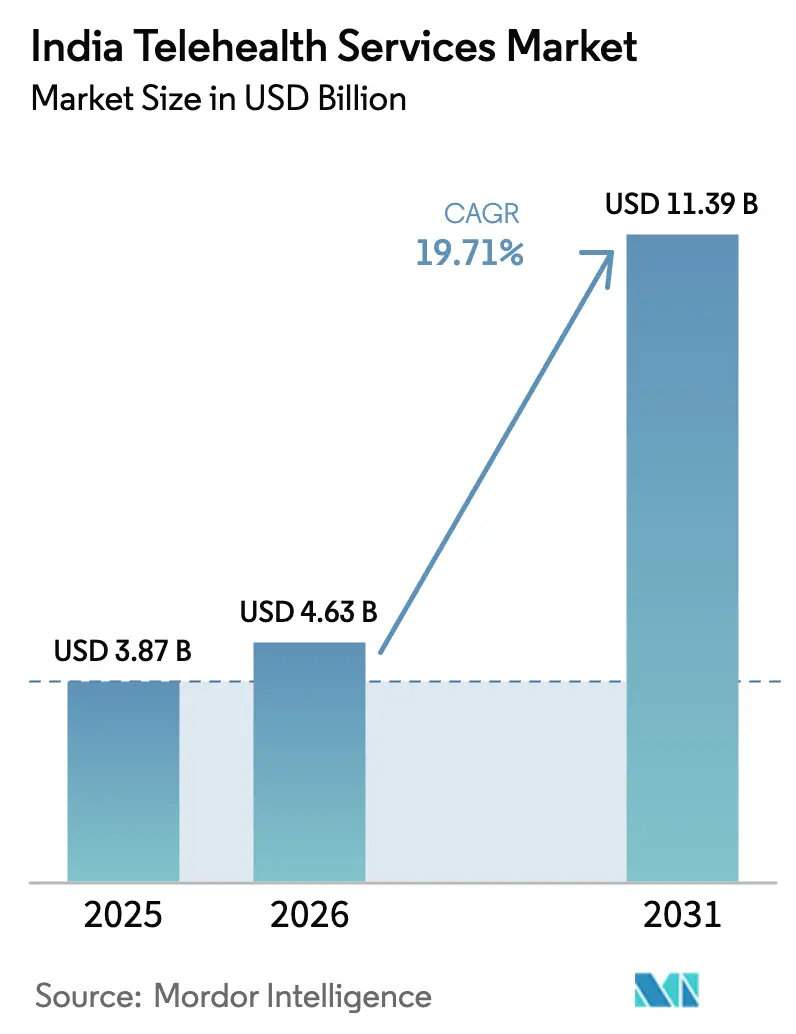

| Base Year Market Size (2025) | USD 3.87 Billion |

| Market Size (2026) | USD 4.63 Billion |

| Market Size (2031) | USD 11.39 Billion |

| Growth Rate (2026 - 2031) | 19.71% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Telehealth Services Market Analysis by Mordor Intelligence

India telehealth services market size in 2026 is estimated at USD 4.63 billion, growing from 2025 value of USD 3.87 billion with 2031 projections showing USD 11.39 billion, growing at 19.71% CAGR over 2026-2031. A nationwide push toward digital health infrastructure, the permanence of habits formed during the pandemic, and fast-rising broadband coverage are the primary growth engines. Government initiatives such as the Ayushman Bharat Digital Mission (ABDM) have already issued more than 650 million digital health IDs, giving providers an interoperable backbone for e-consultations.[1]Source: Ministry of Health & Family Welfare, “Initiatives & Achievements-2024,” pib.gov.in Private funding momentum—typified by Apollo HealthCo’s INR 2,475 crore capital infusion—signals continued confidence in scaling omnichannel care models. Meanwhile, real-time video platforms dominate patient preference, but asynchronous “store-and-forward” models gain traction as providers adapt to connectivity variations. Rising chronic disease prevalence, greater mental-health awareness, and vernacular AI chatbots round out the demand story, turning telehealth from a convenience into an everyday healthcare utility.

Key Report Takeaways

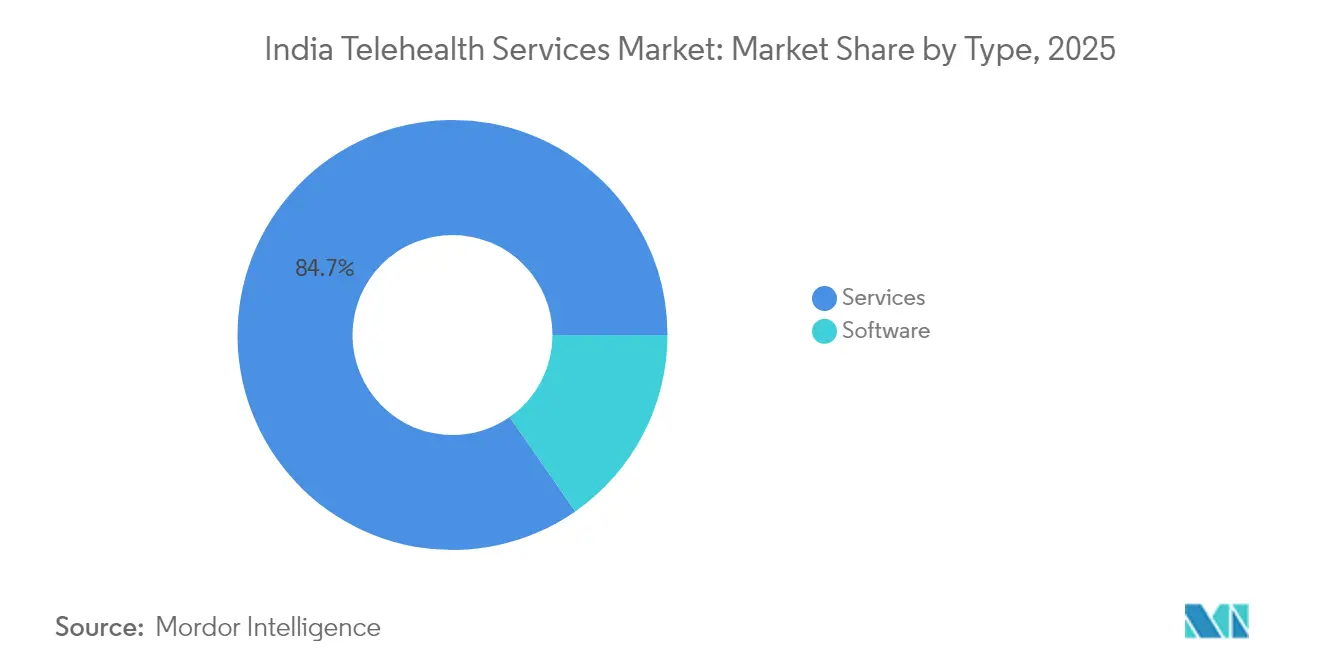

- By type, services led with 84.68% revenue share of the India telehealth services market in 2025, while Software is forecast to expand at a 20.38% CAGR to 2031.

- By technology, real-time platforms accounted for 58.97% of market revenue in 2025; the store-and-forward segment is growing at 20.12% CAGR through 2031.

- By application, tele-radiology held 30.11% share in 2025, whereas tele-psychiatry is advancing at 21.42% CAGR through 2031.

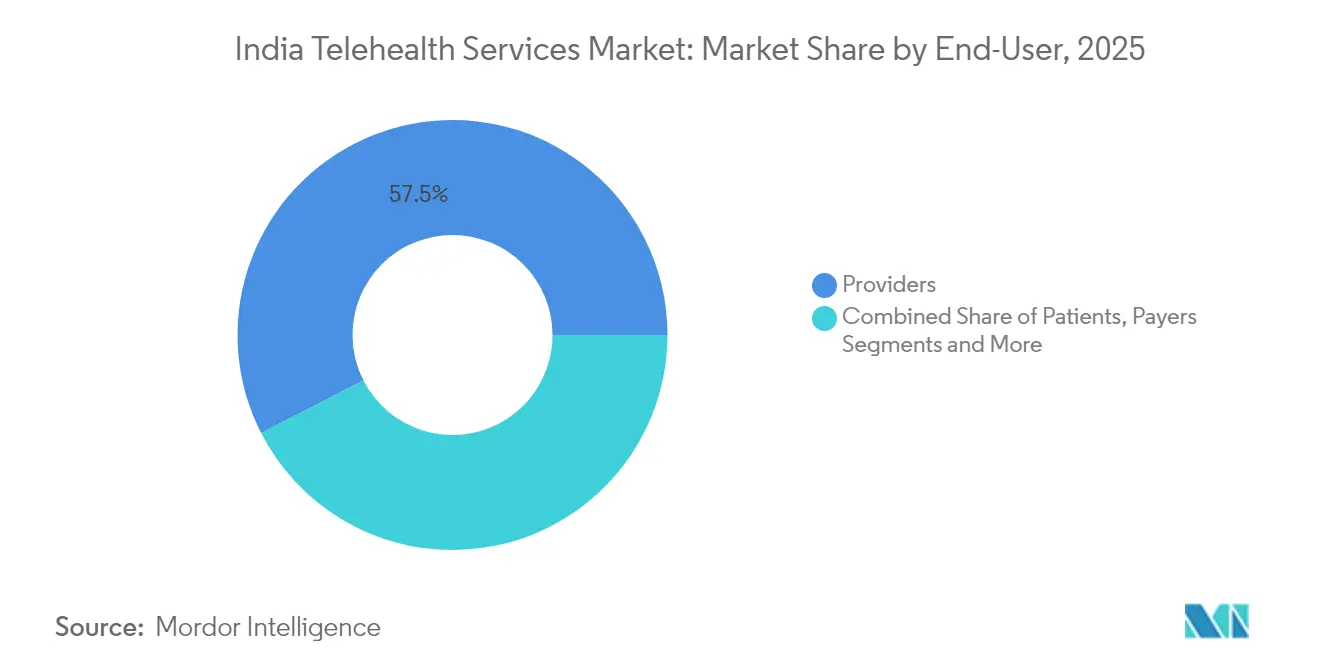

- By end-user, providers captured 57.54% of revenue in 2025; the patient self-service segment shows the highest projected CAGR at 21.58% to 2031.

- By delivery mode, audio-visual consultations commanded 68.21% of revenue in 2025 and continue to post the fastest CAGR of 21.19%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Telehealth Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone and Broadband Penetration Surge | +3.2% | National, with stronger impact in Tier-2/3 cities | Medium term (2-4 years) |

| Government Telemedicine and ABDM Push | +4.1% | National, with early gains in Karnataka, Tamil Nadu, Maharashtra | Long term (≥ 4 years) |

| Growing Chronic Disease Burden | +2.8% | National, with higher concentration in urban areas | Long term (≥ 4 years) |

| Tier-2/3 Digital-Payment Adoption | +2.3% | Tier-2/3 cities and rural areas | Medium term (2-4 years) |

| Vernacular AI Triage Bots Rollout | +1.9% | Regional focus on Hindi, Tamil, Bengali speaking areas | Short term (≤ 2 years) |

| ONDC Integration for Telehealth | +1.5% | National, with early adoption in metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Telemedicine and ABDM Push

The Ayushman Bharat Digital Mission has created an interoperable health-data backbone that links patients, providers, and payers under a single consent-driven architecture. More than 1,000 private firms are now ABDM-certified, letting e-pharmacies and hospitals exchange data through standardized APIs, which boosts network effects for every new participant. eSanjeevani’s 340 million cumulative consultations prove mass acceptance of government-backed teleconsultation pathways. The Digital Personal Data Protection Act 2023 and its forthcoming rules offer legal certainty, yet providers still seek granular guidance around consent flows and breach liabilities.[2]Source: Ministry of Electronics & IT, “Draft Digital Personal Data Protection Rules 2025,” pib.gov.in Expanded telemedicine nodes at 175,338 Ayushman Arogya Mandirs further widen the last-mile footprint. Collectively, these policies cement digital care as a mainstream delivery channel within the India telehealth services market.

Smartphone and Broadband Penetration Surge

Affordable handsets and nationwide 4G/5G rollout lift the technical ceiling on video quality, making real-time diagnostics viable outside metros. Rural residents gain faster access to specialty care because mobile-first workflows bypass the scarcity of brick-and-mortar clinicians. Vernacular interfaces boost usability among non-English speakers, as illustrated by TatvaCare’s 16-language deployment on Microsoft Azure. Seamless UPI payments remove purchasing friction, allowing direct-to-consumer models to flourish. Wearable integrations feed real-time vitals into cloud dashboards, letting physicians intervene earlier and reducing hospital admissions. These technology layers collectively accelerate adoption across the India telehealth services market.

Growing Chronic Disease Burden

NCD prevalence—particularly diabetes and hypertension—requires constant monitoring, something episodic in-person visits cannot provide cost-effectively. Telehealth platforms combine glucometer streams, BP cuffs, and AI analytics to flag anomalies before complications arise, lowering emergency admissions. Predictive algorithms segment high-risk cohorts, steering case managers toward patients who need intervention most urgently. For payers, these capabilities translate into lower claim ratios; for policymakers, they free up tertiary-care capacity for critical cases. The economic burden of NCDs is a strong motivator for continued public-private investment, reinforcing long-term growth in the India telehealth services market.

Vernacular AI Triage Bots Rollout

Advances in large-language models such as L2M3 support symptom triage in Hindi, Tamil, Bengali, and nine other languages, extending digital care to linguistically diverse populations. TinyML inference on low-cost smartphones permits offline symptom assessment, ensuring continuity even when data networks falter. These bots handle first-line queries, freeing clinicians for complex cases and reducing average wait times. Coupled with ABDM-linked e-prescriptions, they can complete end-to-end patient journeys in under 20 minutes. Early pilots show a 25% drop in unnecessary in-person visits, signalling cost and capacity benefits across the India telehealth services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and E-Pharmacy Regulation Gaps | -2.1% | National, with higher impact in metropolitan areas | Short term (≤ 2 years) |

| Low Digital Literacy Among Rural Elderly | -1.8% | Rural areas, particularly in Northern and Eastern states | Long term (≥ 4 years) |

| Doctor Attrition Over Payment Delays | -1.4% | National, with higher impact in private telehealth platforms | Medium term (2-4 years) |

| Rising Cyber-Insurance Premiums | -0.9% | National, affecting primarily large healthcare organizations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and E-Pharmacy Regulation Gaps

While the Digital Personal Data Protection Act lays a statutory baseline, sector-specific rules remain nascent, creating uncertainty over consent validity in clinical contexts.[3]Source: Government of India, “Digital Personal Data Protection Act 2023,” egazette.gov.in Parallel ambiguity in e-pharmacy licensing enables rogue vendors, eroding consumer trust. Hospitals now allocate up to 10% of IT budgets to cybersecurity, yet attacks persist, with healthcare ranking among India’s top five breached sectors. Absent a unified accreditation standard, smaller tele-pharmacies struggle to meet compliance costs, stalling scale. These gaps collectively shave growth from the otherwise buoyant India telehealth services market.

Low Digital Literacy Among Rural Elderly

Elderly patients in rural belts often lack the skills or confidence to navigate video-based care. Infrastructure deficits—spotty 4G and limited device ownership—compound the challenge. Community health workers serve as digital intermediaries, but scalability remains an issue given workforce shortages. Moreover, post-pandemic fatigue fuels a resurgence of in-person preferences for initial consults, requiring providers to blend physical and virtual pathways. Unless literacy programs accelerate, adoption in high-need cohorts will lag the broader India telehealth services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Dominance Drives Integration

Services represented 84.68% of 2025 revenue, underscoring the platform-centric nature of the India telehealth services market. High-margin subscription models let providers update features in weeks rather than quarters, ensuring alignment with evolving ABDM APIs. Software’s 20.38% CAGR reflects growing demand for various software solutions in telehealth.

The production-linked incentive (PLI) scheme for medical devices boosts domestic manufacturing, reducing import dependence and shortening supply chains. Seamless firmware updates and ISO-13485 compliance give local OEMs export-ready credibility. As devices proliferate, advanced analytics engines synthesize multi-parameter streams, generating outcome-based dashboards for clinicians and empowering patients to self-manage chronic conditions.

By Technology: Real-Time Leads Despite Connectivity Constraints

Real-time platforms held 58.97% of the India telehealth services market share in 2025, reflecting user preference for face-to-face interaction and the clinical necessity of synchronous examination in acute cases. Yet store-and-forward workflows, expanding at 20.12% CAGR, offer bandwidth efficiency and richer documentation, especially for radiology, dermatology, and pathology. Hybrid triage engines recommend the optimal mode via AI scoring that weighs urgency, available bandwidth, and clinician workload.

As 5G densifies urban clusters, latency falls below ophthalmology’s minimum threshold for retinal imaging, enabling near-real-time diagnostics. Conversely, in regions still reliant on 3G, compressed DICOM files sent asynchronously keep specialist feedback cycles under 6 hours. The India telehealth services market size contribution from store-and-forward is projected to climb substantially, cementing asynchronous modalities as a vital complement rather than a competitor to live video.

By Application: Radiology Leadership Faces Psychiatry Surge

Tele-radiology accounted for 30.11% of 2025 revenue due to established PACS integration and round-the-clock reading hubs that serve domestic and overseas health systems. Structured imaging datasets and AI annotation tools improve throughput, letting radiologists clear high-volume backlogs without compromising accuracy. In contrast, tele-psychiatry is scaling at 21.42% CAGR, fueled by destigmatization campaigns and insurance coverage for mental-health video consults. Chat-based cognitive-behavioral therapy bots augment human therapists, achieving 30% reductions in session frequency for mild anxiety cases.

COVID-19’s long tail of psychological distress sustained demand beyond the crisis stage, and 2025 insurance circulars mandating parity for mental-health reimbursements catalyze further uptake. Collectively, the two segments illustrate a shift from diagnostics-heavy to holistic care models within the India telehealth services market.

By End-User: Provider Focus Shifts Toward Patient Empowerment

Hospitals and multi-specialty chains captured 57.54% of revenue in 2025 as they embed digital modules into existing EMRs for continuity of care. Yet patient-driven platforms, registering a 21.58% CAGR, highlight the rise of consumer choice and direct-pay consults. Price-transparent apps show specialty rates side-by-side, and near-instant wallet settlements draw clinicians seeking predictable income streams.

Employers bundle telehealth into health-and-wellness perks to control absenteeism and claims. Meanwhile, payers adopt managed-care models where teleconsult touchpoints feed risk-scoring engines, allowing differential premiums. Together, these shifts redistribute negotiating power, making service personalization a key differentiator across the India telehealth service industry.

By Delivery Mode: Audio-Visual Dominance Faces Accessibility Challenges

Audio-visual channels remain the first choice, grabbing 68.21% of 2025 revenue on the back of HD cameras embedded in budget smartphones. Augmented-reality overlays let orthopedists mark joint angles live, improving diagnostic accuracy. Yet audio-only and text-based modes keep rural uptake alive when video bandwidth dips below 512 kbps.

Emerging privacy-preserving codecs allow pixelation of sensitive backgrounds without degrading anatomical clarity, relieving user anxiety over home-environment exposure. The India telehealth services market size for audio-visual delivery is forecast to grow in the coming years, underscoring its central role while highlighting the continued need for fallback channels.

Geography Analysis

Southern India leads with a significant market share in 2025, helped by Karnataka’s early adoption of ABDM APIs and Tamil Nadu’s fiber-to-village program that links 12,525 rural PHCs to district hospitals. Strong IT talent anchors collaborative pilots between health systems and SaaS vendors, producing rapid iteration cycles on vernacular UX. Multiple tertiary hospitals deploy hybrid tele-ICUs, cutting sepsis mortality by 18% within 12 months, further reinforcing regional dominance.

Northern India records the fastest growth, propelled by massive public-sector spending on 5G corridors and a young, mobile-first population. Digital health ID uptake surpasses 60% in tier-2 cities such as Lucknow, signaling readiness for integrated care pathways. Rural literacy programs anchored by ASHA workers reduce onboarding friction for elderly users, yet device affordability remains an obstacle that government loan schemes aim to mitigate.

Western India’s industrial hubs such as Mumbai and Ahmedabad exhibit strong willingness to pay for premium telehealth packages bundled with annual health checks, opening cross-sell opportunities for diagnostics labs. Eastern states lag due to lower per-capita income and infrastructure gaps, but pilot tele-ophthalmology vans using satellite backhaul demonstrate scalable promise. Collectively, regional diversification balances the overall growth trajectory of the India telehealth services market, ensuring nationwide penetration by 2030.

Competitive Landscape

India’s telehealth arena remains fragmented, with more than 200 active platforms spanning e-consultation, e-pharmacy, and RPM niches. Apollo HealthCo’s plan to merge with Keimed indicates a vertical-integration play that marries pharmacy distribution with virtual care to lock-in lifetime customer value. Tata Digital’s acquisition of 1mg adds a deep catalog of medicines and diagnostics to its super-app ecosystem, intensifying competition for wallet share.

Niche disruptors build defensible moats through AI IP, such as cloud-based ECG interpretation engines that deliver 95% sensitivity in under 30 seconds. Multilingual UX platforms win rural mindshare, while hospital-backed ventures emphasize clinical governance to attract risk-averse patients. Strategic alliances with non-banking finance companies unlock BNPL payment models for high-ticket procedures like oncology second opinions. A looming theme across the India telehealth services market is the pivot from growth-at-all-costs to profitability, spurred by reports that digital health startups hold a sub-9-month cash runway. Firms that integrate offline touchpoints—labs, clinics, or home-care—into digital journeys are better positioned to achieve margin resilience.

Looking ahead, entry barriers will rise as interoperability compliance, cyber-insurance, and data-localization requirements inflate fixed costs. This environment favors capital-rich incumbents or scale-seeking mergers, pointing toward accelerated consolidation by 2027. Providers who can couple tech prowess with domain depth will likely dominate the India telehealth services market as it matures.

India Telehealth Services Industry Leaders

TeleVital

Apollo TeleHealth Services

Tata 1mg Healthcare Solutions

Practo Technologies

Netmeds Marketplace

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Southern Railway introduced a telemedicine network connecting remote railway health units to specialist hubs in Perambur, enabling real-time video consults and remote diagnostics sharing.

- December 2024: The Union Ministry of Health and Family Welfare announced plans to extend telemedicine services to all AIIMS and PGI institutions nationwide.

- November 2024: Amazon launched Amazon Clinic, offering online consultations for more than 50 conditions directly through its Indian app.

- June 2024: Apollo Telehealth and the Government of Manipur opened a telemedicine-enabled primary health center in Borobeka to serve conflict-affected communities.

India Telehealth Services Market Report Scope

The Telehealth services market in India is growing and is highly demanded. It is preferred because it is a contactless way of being treated for various diseases. In this report, you will have a complete background analysis of the Telehealth Services Market in India, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles are covered in the report.

The Telehealth Services Market in India is Segmented By type (Services and Software), By Technology (Store and Forward, Real-Time, and Others), By Application (Tele-Psychiatry, General Consultations, Tele-Radiology, and Tele-Pathology), By End-User (Providers, Patients, and Players), By Delivery Mode (Audio-Visual, Only Audio, and Written), and By Type (e-Consultation, Online Appointment Booking, Telemedicine, Diagnostics and Fitness Monitors).

By Type

| Services |

| Software |

By Technology

| Store and Forward |

| Real-Time |

| Others |

By Application

| Tele-Psychiatry |

| General Consultations |

| Tele-Radiology |

| Tele-Pathology |

| Tele-Dermatology |

| Others |

By End-User

| Providers |

| Patients |

| Payers |

| Others |

By Delivery Mode

| Audio-Visual |

| Audio Only |

| Text / Written |

| By Type | Services |

| Software | |

| By Technology | Store and Forward |

| Real-Time | |

| Others | |

| By Application | Tele-Psychiatry |

| General Consultations | |

| Tele-Radiology | |

| Tele-Pathology | |

| Tele-Dermatology | |

| Others | |

| By End-User | Providers |

| Patients | |

| Payers | |

| Others | |

| By Delivery Mode | Audio-Visual |

| Audio Only | |

| Text / Written |

Key Questions Answered in the Report

What is the current size of the India telehealth services market?

The market is valued at USD 4.63 billion in 2026 and is on track to reach USD 11.39 billion by 2031.

How fast is the market growing?

A robust 19.71% CAGR is forecast between 2026 and 2031, powered by government digital-health programs and expanding broadband coverage.

Which region leads telehealth adoption in India?

Southern India commands major share of revenue due to strong digital infrastructure and proactive state policies.

Which telehealth application is expanding the quickest?

Tele-psychiatry is advancing at a 21.42% CAGR due to greater mental-health awareness and insurance reimbursement parity.

What technology model is gaining popularity alongside real-time video?

Store-and-forward workflows are growing at 20.12% CAGR as providers optimize for bandwidth variability while enhancing documentation.

How are regulations shaping market growth?

The Digital Personal Data Protection Act provides a legal framework, but pending e-pharmacy and sector-specific rules must clarify compliance to unlock full potential.

Page last updated on: