Microspheres Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

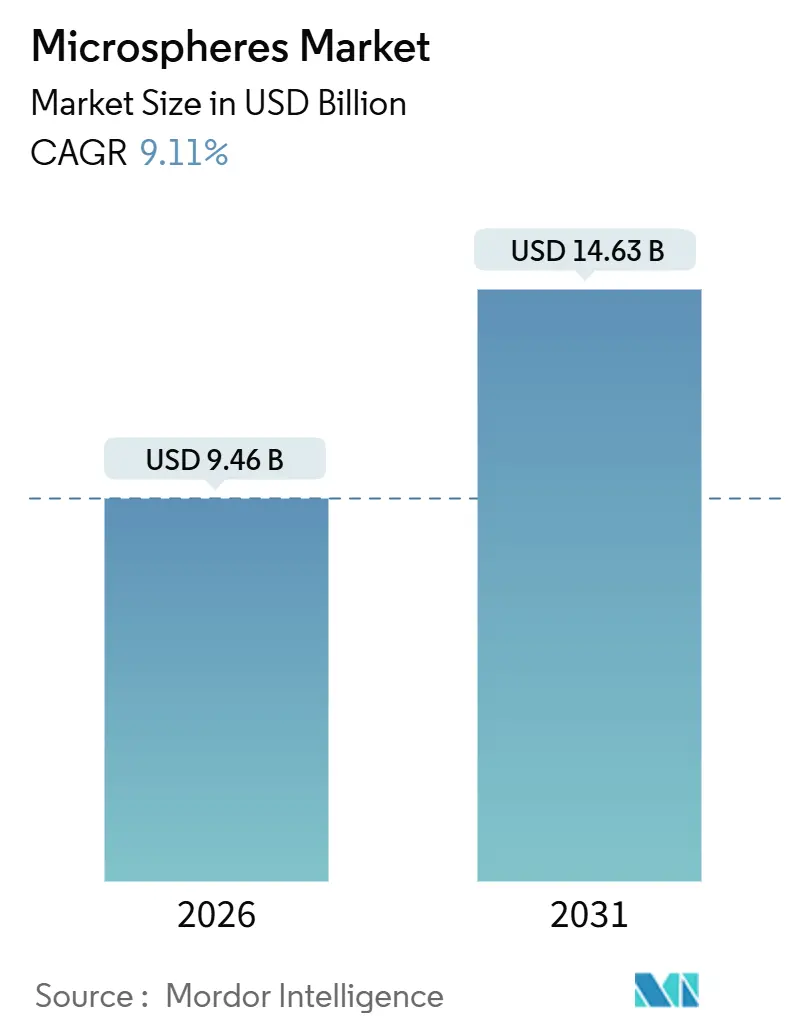

| Market Size (2026) | USD 9.46 Billion |

| Market Size (2031) | USD 14.63 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

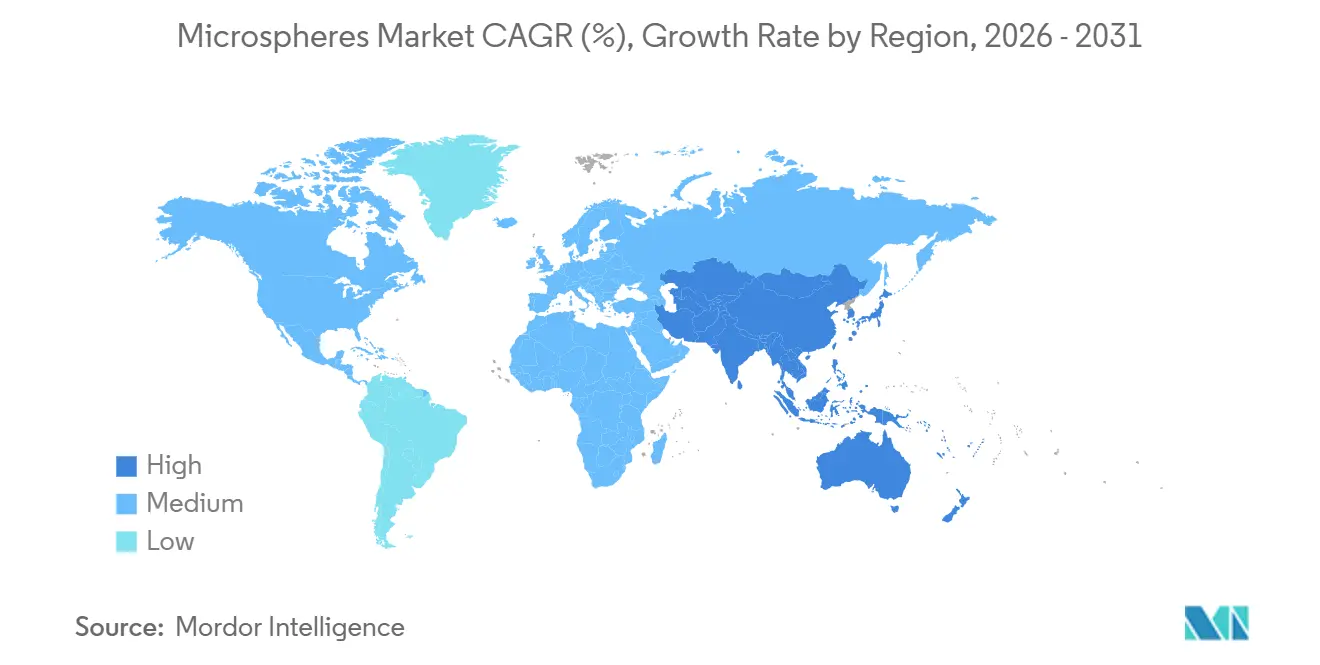

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microspheres Market Analysis by Mordor Intelligence

The Microspheres Market size is estimated at USD 9.46 billion in 2026, and is expected to reach USD 14.63 billion by 2031, at a CAGR of 9.11% during the forecast period (2026-2031). Persistent demand stems from precision-medicine radioembolization, lightweight structural composites in electric vehicles and aerospace, and smart-city road‐safety coatings. FDA-approved yttrium-90 glass microspheres strengthen revenue visibility in interventional oncology, while hollow variants continue to win share in syntactic foams, drilling fluids, and thermoplastic compounding. Regional production shifts toward Asia Pacific, where new glass-bubble capacity targets electric-vehicle battery enclosures, consolidating the microspheres market’s long-run cost curve. Meanwhile, Europe’s phased microplastic ban forces formulators to swap polymer beads for mineral or bio-attributed alternatives, tilting raw-material preferences toward glass and biodegradable polymers.

Key Report Takeaways

- By raw material, glass captured 47.71% of the microspheres market share in 2026 and is forecast to grow at a 10.83% CAGR through 2031.

- By type, hollow variants accounted for 67.59% of the microspheres market size in 2026 and are poised to expand at a 10.39% CAGR to 2031.

- By application, medical technology led with 40.57% revenue share in 2026 and represents the fastest-growing pocket at a 10.74% CAGR to 2031.

- By geography, North America held 39.62% share of the microspheres market in 2026, while the Asia-Pacific is projected to clock the highest 11.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microspheres Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing application in advanced medical imaging and targeted drug delivery | +2.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Lightweighting push in electric vehicle and aerospace composites | +2.4% | Global, with concentration in North America, Europe, China | Long term (≥ 4 years) |

| Surge in reflective and insulating road-marking paints for smart-city projects | +1.6% | APAC core, spill-over to Middle-East and Africa | Short term (≤ 2 years) |

| Decentralised 3-D microfluidic fabrication boosting custom sphere demand | +1.2% | North America, Europe, select APAC hubs | Long term (≥ 4 years) |

| Adoption in additive-manufactured concrete for off-planet construction | +0.7% | North America, Europe (space-agency clusters) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Application in Advanced Medical Imaging and Targeted Drug Delivery

Yttrium-90 glass microspheres have emerged as the gold standard for transarterial radioembolization in treating hepatocellular carcinoma. This follows the impressive outcomes demonstrated in Boston Scientific’s TheraSphere and Sirtex’s SIR-Spheres, as highlighted in the LEGACY trial and the DOORwaY90 study[1]Y.-90 Radioembolization clinical outcomes, “Yttrium-90 Radioembolization for Hepatocellular Carcinoma,” PMC, pmc.ncbi.nlm.nih.gov. In 2024, polymer spheres, like Eye90, which carry contrast agents, successfully navigated first-in-human safety assessments, bolstering intraprocedural visualization. Meanwhile, PLGA-encapsulated carbon nanoparticles achieved preclinical validation for lymph-node tattooing, offering a non-toxic alternative to conventional dyes. While the FDA’s 510(k) pathway expedites commercialization, it demands stringent testing on particle size and radionuclides. This requirement underscores the need for precision in the microspheres market. Furthermore, as hospitals increasingly adopt localized therapies, it solidifies and boosts the recurring revenue streams for suppliers of glass microspheres.

Lightweighting Push in Electric Vehicle and Aerospace Composites

Electric-vehicle battery packs are prompting OEMs to turn to hollow glass microspheres. By integrating these microspheres into thermoplastic housings and underbody shields, OEMs are achieving a significant reduction in component mass without sacrificing impact resistance. 3M’s K- and S-series bubbles are paving the way for lightweight finished parts with high tensile moduli. Major aerospace players are now turning to microsphere-filled syntactic foams for applications like radomes and fairings. Following the lead of the Boeing 787 and Airbus A350, these innovations are making their way into next-generation airframes. The advantages of lower resin viscosity, enhanced dielectric properties, and reduced voids bolster the appeal of hollow variants, ensuring continued growth for the microspheres market.

Surge in Reflective and Insulating Road-Marking Paints for Smart-City Projects

Type I and Type IV glass beads, when embedded in thermoplastic road paints, achieve high retroreflectivity. This performance aligns with the thresholds set by DoD UFGS-32 17 23.16 and AASHTO M 247. Countries like India, China, and various ASEAN nations are intensifying their use of reflective markings. This move aims to reduce nighttime fatalities, which constitute a significant portion of road deaths in conditions of poor visibility. Additionally, hollow ceramic microspheres are effective in reducing pavement temperatures, helping to alleviate urban heat islands. Consequently, these factors bolster short-cycle demand in the microspheres market, especially with the backing of smart-city budget allocations.

Decentralized 3-D Microfluidic Fabrication Boosting Custom Sphere Demand

Microfluidic platforms, utilizing droplet technology, produce uniform microspheres, surpassing the limitations of traditional batch emulsification. Both academic laboratories and Contract Development and Manufacturing Organizations (CDMOs) are now able to provide tailored particles for diagnostics and cell therapies within days, enhancing design flexibility. NASA's designation of a Technology Readiness Level 5 for regolith-polymer composites highlights their growing importance in space construction. The rise in throughput from parallelized reactors indicates a notable increase in specialty-grade volumes within the microspheres market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile acrylonitrile and glass-grade soda-ash prices | -1.4% | Global, acute in Europe and Asia | Short term (≤ 2 years) |

| Tightening bans on micro-plastics in cosmetics | -0.9% | Europe, North America, select APAC markets | Medium term (2-4 years) |

| Capacity bottlenecks in expandable-microsphere blowing-agent supply | -0.6% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Acrylonitrile and Glass-Grade Soda-Ash Prices

In June 2025, U.S. prices for acrylonitrile remained steady, while in China, it was more affordable. However, European prices surged, driven by propylene shortages that tightened margins for polymer microspheres. Meanwhile, restrictions on soda ash in both China and Turkey have intensified cost fluctuations for producers of glass microspheres. Spot buyers are grappling with significant price swings within the quarter, adding complexity to the project economics of syntactic foams and buoyancy modules.

Tightening Bans on Microplastics in Cosmetics

By October 2027, EU Regulation 2023/2055 mandates the elimination of synthetic polymer microspheres in rinse-off cosmetics, followed by a similar ban on leave-on products by October 2029[2]Regulation (EU) 2023/2055, EUR-Lex, eur-lex.europa.eu. This regulation compels brand owners to pivot towards mineral or biodegradable alternatives. Meanwhile, the U.S. Microbead-Free Waters Act has already imposed restrictions on rinse-off products. In 2024, both South Korea and Taiwan introduced similar regulations. Additionally, the demand for cosmetics-grade microspheres is witnessing a decline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Glass Dominance Anchored in Medical and Composite Applications

Glass held 47.71% of 2026 revenue and is forecast to outpace other raw materials at 10.83% CAGR through 2031. Its dual pull comes from yttrium-90 radioembolization beads and hollow soda-lime spheres used in syntactic composites for aerospace and deepwater drilling. Glass also satisfies AASHTO M 247 mandates for road-marking refractive index, preserving a baseline volume stream. Polymer grades rank second; Nouryon’s bio-attributed Expancel BIO launch in December 2024 meets sustainability audits without compromising expansion ratios. Ceramic, fly-ash, and metallic spheres each address niche needs—high-pressure proppants, low-cost lightweight concrete, and additive manufacturing of dense parts—ensuring a diversified raw-material palette across the microspheres market.

Regulatory compliance shapes preferences: ISO 13320 laser diffraction confirms particle-size, while ISO 11357 DSC profiles expansion temperatures, embedding quality discipline across supply chains. The microspheres industry, therefore, rewards producers that pair material breadth with analytical rigor. Emerging EU nano-material bans (Regulation 2024/858) restrict styrene-acrylate nano-copolymers, redirecting demand to larger-sized polymer or glass options. Glass producers benefit from vertical silica integration, insulating them from soda-ash volatility. Polymer players, however, must hedge acrylonitrile swings or adopt bio-routes. Consequently, glass’s share within the microspheres market is likely to rise through the decade, especially in oncology, aerospace composites, and smart-city infrastructure.

By Type: Hollow Microspheres Command Volume Through Density Advantage

Hollow grades captured 67.59% of 2026 volume and are projected to grow at a 10.39% CAGR to 2031, driven by density-sensitive EV, aerospace, and oil-and-gas use cases. Hollow spheres reduce part mass, enhancing fuel economy and drilling efficiency. Solid spheres play a pivotal role in high-surface-area applications. These include Luminex’s xMAP multiplex assays, abrasive blasting, and chromatography media, ensuring a stable and diverse demand.

Expandable microspheres, a hollow subset, facilitate water-based expansion processes, aligning with California's VOC regulations. Janus particles, featuring dual chemistries and core-shell constructs, challenge traditional boundaries, suggesting a shift towards more fluid functional segmentation. With such innovations, hollow grades are poised to be the primary growth driver in the microspheres market through 2031.

By Application: Medical Technology Leads on Radioembolization and Diagnostics

Medical-technology uses commanded 40.57% of 2026 revenue and are set to rise at 10.74% CAGR through 2031 as DOORwaY90 trial data extend radioembolization into bridge-to-transplant protocols. In multiplex immunoassays, diagnostic spheres are enhancing therapeutic outcomes. The automotive sector, now the second-largest user, integrates microsphere-infused sealants, acoustic foams, and lightweight trims into vehicles. In aerospace, composites utilize these spheres for radar transparency and dielectric control, while paints and coatings benefit from consistent funding through municipal road-marking budgets.

Deepwater cementing and high-pressure hydraulic fracturing are seeing a growing adoption in the oil and gas sector. While cosmetics, traditionally a stronghold, grapple with regulatory challenges, suppliers are shifting towards cellulose and bio-attributed beads to maintain their market presence. This diverse application landscape supports a stable growth trajectory for the microspheres market.

Geography Analysis

North America generated 39.62% of 2026 revenue. Minnesota and Massachusetts, with their concentrated medical-device clusters, bolster the market for radioembolization beads. Meanwhile, composite hubs in Seattle and Wichita are fueling the demand for glass bubbles in next-generation airframes. Nouryon expanded in Green Bay, establishing local supply lines for EV sealants catering to markets in Michigan and Ontario. Updated road-marking specifications from the DoD ensure consistent procurement of glass beads by state DOTs. Additionally, Canadian oil-sands well-cementing and automotive interiors in Mexico further solidify North America's dominant position in the microspheres market.

Asia Pacific is forecast to log an 11.89% CAGR to 2031. China's production of EV units boosts the demand for glass bubbles in battery housings. Crerax, based in Shanghai, provides a range of spheres - glass, polymer, ceramic, and metallic - reflecting the market's demand diversity. Kureha from Japan operates research and development hubs in both Tokyo and Houston, assisting global composites clients in qualifying new grades. India's push for reflective road markings on national highways is driving up glass-bead imports. In South Korea, solid polymer spheres are being utilized for filter validation in semiconductor cleanrooms. Furthermore, ASEAN's emergence as a hub for automotive components adds another layer of growth potential for the microspheres market.

Europe faces challenges with Regulation 2023/2055, which prohibits polymer microbeads in cosmetics, and Regulation 2025/2365, which enforces controls on pellet loss. While German automotive OEMs are incorporating expandable spheres into EV battery enclosures, the costs associated with REACH compliance are raising capital expenditure challenges. Aerospace leaders in France are turning to microsphere-filled prepregs, and the offshore wind industry in the U.K. is utilizing syntactic-foam buoyancy modules. Nouryon's facility in Sundsvall is playing a pivotal role in meeting Europe's demand for bio-attributed grades. Although South America and the Middle-East and Africa collectively hold a smaller share of the global market, Brazil's pre-salt drilling activities and road-safety initiatives in Saudi Arabia are generating sporadic surges in demand, ensuring a geographically diverse microspheres market.

Value Chain Analysis

The microspheres value chain begins with feedstocks and utilities, including silica and soda ash for glass, petrochemical monomers such as acrylonitrile-based inputs and blowing agents for polymer and expandable grades, and ceramic and fly-ash streams for specialty spheres. This is followed by energy-intensive melting or polymerization and encapsulation steps, depending on the microsphere chemistry.

Producers then move into classification and surface treatment, focused on tight particle-size distribution, crush strength, refractive index, and functional coatings. ISO-driven analytical control, for example ISO 13320 particle sizing and DSC-based thermal profiling referenced in the report, becomes a gating requirement for medical technology, aerospace composites, and road-marking applications. Downstream, supply typically splits across direct OEM or Tier purchasing (medical-device manufacturers and composite formulators), specialty chemical distribution for coatings, plastics, and construction additives, and device-oriented distribution for regulated healthcare products. Key bottlenecks and risk points cluster around expandable-microsphere blowing-agent availability noted in the report restraints and soda-ash cost and supply swings tied to restrictions referenced in the report. Qualification cycles also matter, since end users validate new grades for EV thermoplastics, syntactic foams, and AASHTO M 247-aligned road-marking beads. Increasingly, traceability and certified content (for example ISCC PLUS-verified bio-attributed offerings such as Nouryon Expancel BIO) shape purchasing as formulators replace restricted polymer beads in Europe and re-optimize material choices toward glass, mineral, and biodegradable alternatives.

Competitive Landscape

The microspheres market is moderately consolidated. Glass-sphere leaders capitalize on silica feedstock integration and proprietary fusion processes that yield crush strengths above 20,000 psi. Polymer specialists tune blowing-agent chemistry; Expancel grades span 80-200 °C expansion windows and attain 60× volume ratios. Medical-device incumbents Boston Scientific and Sirtex command premium pricing in radioembolization niches, defended by FDA approvals and clinical data moats. Niche disruptors such as Cospheric and Crerax occupy white spaces—ultra-low-density cenospheres for aerospace, metallic spheres for thermal-spray coatings—leveraging agility over scale. ISO 13485 and ISO/IEC 17025 certifications increasingly differentiate suppliers where end-use regulation is stringent.

Microspheres Industry Leaders

Nouryon

3M

Potters Industries LLC

Chase Corporation

Trelleborg AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Application-specific grades create whitespace for microspheres to shift from generic lightweight fillers to engineered performance enablers. In paints and coatings, new product development such as Nouryon Expancel XS200 for interior decorative paints targets lower density while maintaining surface finish, which supports additional use in building interiors and renovation-focused coating portfolios. In packaging and paperboard, Nouryon introduced a new Expancel grade in 2026 to increase bulk and reduce fiber use, positioning microspheres as a materials-efficiency lever in fiber-based substrates rather than only in plastics and elastomers.

Regulatory and procurement changes continue to redirect demand toward alternatives that meet microplastic restrictions and audit requirements. The EU microplastics restriction timeline (Regulation 2023/2055) is already pushing cosmetics formulators away from synthetic polymer beads, while bio-attributed and biodegradable routes such as Expancel BIO and biodegradable microsphere ingredient platforms distributed by major specialty distributors broaden compliant options. On the commercial side, distribution and channel expansion is also contributing to adoption, including the Brenntag Specialties agreement to distribute 3M glass bubbles into coatings, plastics, and construction, which supports wider geographic reach and faster formulation cycles for hollow glass microspheres used in lightweighting and insulation applications.

Recent Industry Developments

- April 2026: Nouryon introduced a new Expancel microsphere grade (Expancel 081) for paperboard production to increase bulk and reduce fiber use, highlighting microspheres as a materials-efficiency tool beyond traditional plastics and elastomers. The launch broadens the addressable set of packaging and paper applications and ties product value to measurable substrate performance and resource reduction goals.

- December 2025: A Macquarie Asset Management-led consortium agreed to acquire a majority stake in Potters Industries LLC from TJC, with completion targeted in the first half of 2026. The transaction signals continued consolidation around glass bead and microsphere supply, with potential knock-on effects for capital allocation, capacity footprint, and service levels across Potters' manufacturing and logistics network.

- April 2024: Nouryon launched Expancel WB microspheres for white shoe soles, positioning expandable microspheres as a lightweighting and aesthetics enabler in footwear compounds. This expands penetration in consumer-facing applications where density reduction and visual appearance are both required, supporting downstream adoption by compounders and brand supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The microspheres market is defined as revenues generated from selling engineered micro-sized spherical particles (typically 1 to 1,000 microns), across hollow and solid forms, used to deliver specific performance in industrial and medical end uses.

Scope exclusions: We exclude upstream feedstock commodities and any in-house captive production that is not commercially sold as microspheres.

Segmentation Overview

- By Raw Material

- Glass

- Polymer

- Ceramics

- Fly Ash

- Metallic

- Others

- By Type

- Hollow

- Solid

- By Application

- Automotive

- Aerospace

- Cosmetics

- Oil and Gas

- Paints and Coatings

- Medical Technology

- Composites

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to map the value chain and keep assumptions tied to observable signals before we speak with the industry. We start by aligning definitions around particle size ranges, common materials, and typical end-use pull, then we build an initial regional view of where demand is likely to sit.

For inputs, we rely on public and official sources such as trade and customs statistics for relevant chemical and material categories, government industrial production and manufacturing indices, and environmental and chemicals regulations from agencies like EPA and ECHA. We also use standards body publications that outline testing methods and material-performance guidance. In parallel, we review patent databases to see where activity is increasing, and we cross-check adoption signals using company annual reports, investor presentations, reputable press coverage, and association publications.

Where available, paid subscriptions focused on company financials and shipment-level trade flows are used to sanity-check scale and direction, particularly for cross-border supply patterns. These examples are not exhaustive, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to test the early model and replace weaker assumptions with ranges that practitioners consistently describe. We interview manufacturers, distributors, and downstream users across key application areas such as paints and coatings, automotive, aerospace, cosmetics, oil and gas, composites, and medical technology, then reconcile differences by region to reflect local pricing and adoption behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 47% |

| Mid tier: 57% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 16% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the demand pool from end-use activity and material consumption signals, then distributes it across key applications and regions using adoption rates and typical loading levels. For microspheres, the model is anchored around inputs such as paints and coatings output, lightweighting intensity in automotive and aerospace parts, construction and composites activity, medical procedure volumes where relevant, and observed import-export flows for related specialty materials.

After producing the first totals, we corroborate them with selective bottom-up checks, including sampled price-per-kilogram ranges by material type, channel markups discussed in interviews, and supplier revenue splits where disclosures allow a clean read. Where bottom-up visibility is incomplete, we handle gaps by using conservative penetration ranges and then retesting through follow-up calls, especially when a segment produces unusually high implied volumes.

For forecasting, we rely mainly on scenario analysis supported by multivariate regression checks, because demand tends to move with a mix of industrial output, construction cycles, and regulatory shifts that influence material substitution. Price progression, mix shifts between hollow and solid, and regional growth rates are refined using consensus ranges from primary respondents, and the final forecast is generated with year-by-year drivers that can be repeated and updated.

Data Validation & Update Cycle

Validation is done by triangulating final market totals against independent signals, so the result remains coherent even when a single data stream is noisy. Checks include variance reviews versus trade flow direction, implied consumption per end-use, and whether pricing and mix assumptions produce realistic revenue per unit across regions.

Before sign-off, anomalies are flagged and reviewed in a multi-step internal process, and the team re-contacts selected interviewees when the model moves outside reasonable ranges. Reports are refreshed annually, with interim updates when a material event occurs, for example a major regulatory change affecting polymer use or a sharp shift in end-market demand. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Microspheres Market Size Versus Other Published Estimates

Published market values for microspheres often do not match, even when the topic sounds the same, because each publisher makes different choices on what to count and how to project it forward. The spread usually comes from scope, how prices are treated across materials, and how quickly assumptions are refreshed when regulations or end markets shift.

In this market, the biggest gap drivers tend to be whether adjacent micro-particle products are grouped with microspheres, how hollow versus solid products are priced and blended, and whether medical technology demand is modeled from procedure-linked indicators or assumed as a flat share of a broader specialty materials pool. Some estimates also use more aggressive or more conservative base cases, or apply a single currency conversion timing across regions, which can move the value materially in years with volatility. The table reflects these differences, including the choice to keep the scope to commercial microspheres by material, type, and application, with a 2026 starting point at USD 9.46 B, which is treated this way by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.46 B (2026) | |

| Industry Publisher A | USD 8.98 B (2025) | Uses a different base year and a healthcare-leaning segmentation lens, which can shift mix assumptions and smooth over industrial demand swings that show up more clearly when end-use activity indicators are used. |

| Industry Publisher B | USD 7.60 B (2025) | Applies a 2025 base with a lower growth path and relies more on historical trend extension, which can understate step-changes from regulation-driven substitution and lightweighting adoption in industrial applications. |

Taken together, the comparison shows that year choice, included product perimeter, and price-mix handling explain most of the difference. By keeping the steps traceable to end-use activity, material mix, and interview-validated price ranges, the resulting estimate stays balanced and easier to reproduce when the model is updated.

Key Questions Answered in the Report

What is the current value of the microspheres market?

The microspheres market size reached USD 9.46 billion in 2026 and is forecast to rise to USD 14.63 billion by 2031, registering a CAGR of 9.11%.

Which segment generates the highest revenue?

Medical-technology applications lead, capturing 40.57% of 2026 revenue and projected to grow at 10.74% CAGR.

Why are hollow microspheres in high demand?

Their low true density allows OEMs in EVs, aerospace, and drilling to cut component weight without sacrificing strength.

How will EU regulations affect polymer microspheres?

Regulation 2023/2055 bans microbeads in cosmetics by 2029, compelling producers to shift toward mineral or biodegradable alternatives.

Which region is expected to record the fastest growth?

Asia Pacific is projected to expand at 11.89% CAGR through 2031, driven by China’s EV output and Japan’s specialty-polymer exports.

Page last updated on: