Telehealth Kiosk Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

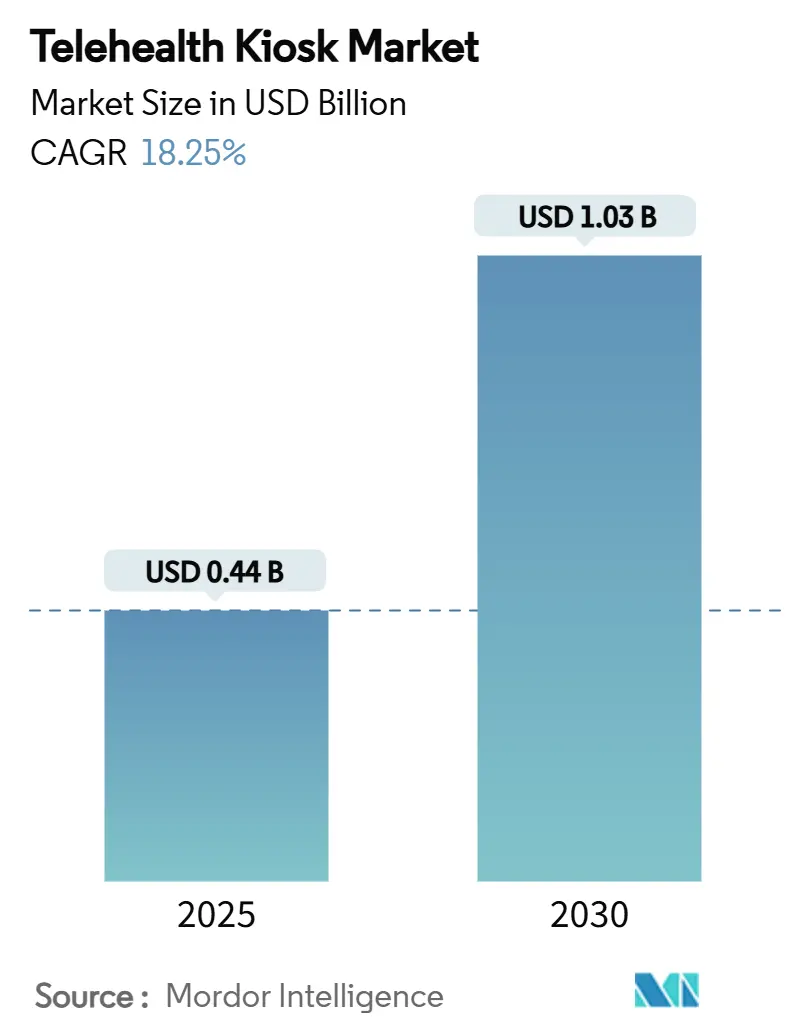

| Market Size (2025) | USD 0.44 Billion |

| Market Size (2030) | USD 1.03 Billion |

| Growth Rate (2025 - 2030) | 18.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telehealth Kiosk Market Analysis by Mordor Intelligence

The global telehealth kiosk market size stood at USD 0.444 billion in 2025 and is forecast to reach USD 1.028 billion by 2030, translating into an 18.25% CAGR over the period. The growth trajectory reflects post-pandemic digital health normalization, payer reimbursement certainty, and retail pharmacy chains’ shift toward in-store diagnostic hubs. Demand is reinforced by healthcare systems that view kiosks as a dual solution for clinician shortages and geographic care gaps, while technology vendors race to embed advanced point-of-care testing inside compact footprints. Competitive differentiation is tilting toward full-stack platforms that marry hardware, software, and wrap-around clinical services under subscription contracts. Strategic deployments in airports, corporate campuses, and rural community locations anchor near-term volumes, and regulatory alignment across major regions further de-risks provider investment in the global telehealth kiosk market.

Key Report Takeaways

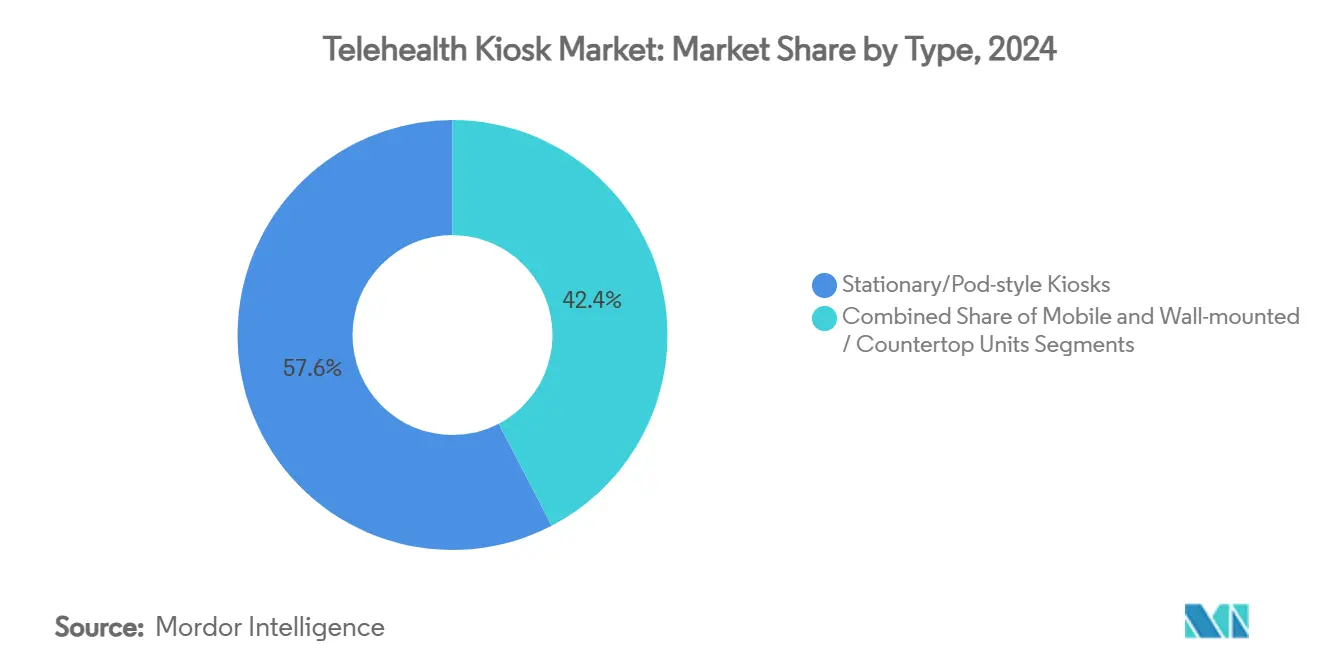

- By type, stationary pod-style kiosks led with 57.64% of the global telehealth kiosk market share in 2024. Mobile cart-based units are projected to grow at a 22.63% CAGR through 2030, the fastest among form factors.

- By component, hardware captured 44.23% of the global telehealth kiosk market size in 2024.Services will expand at a 21.33% CAGR to 2030, outpacing all other component categories.

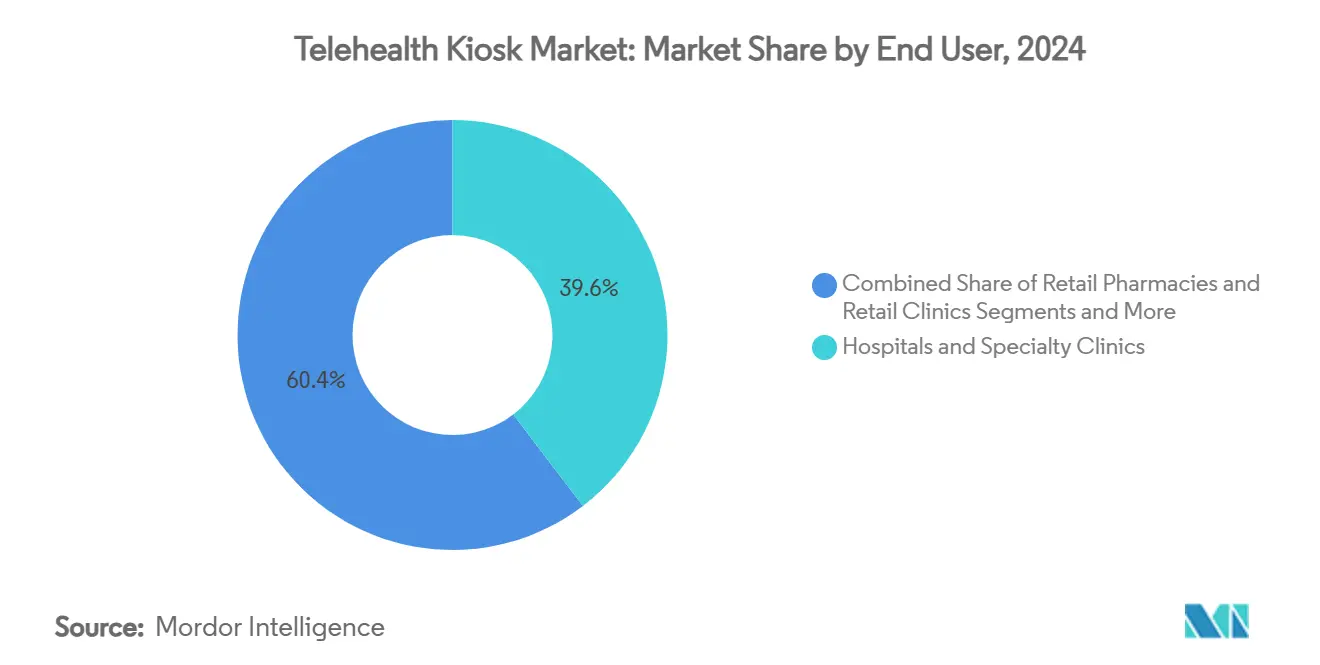

- By end user, hospitals and specialty clinics held 39.63% revenue share in 2024, while retail pharmacies are poised for 20.12% CAGR growth through 2030.

- By application, behavioral health visits are forecast to rise at a 21.36% CAGR, the highest among use cases, whereas primary care retained 36.24% share in 2024.

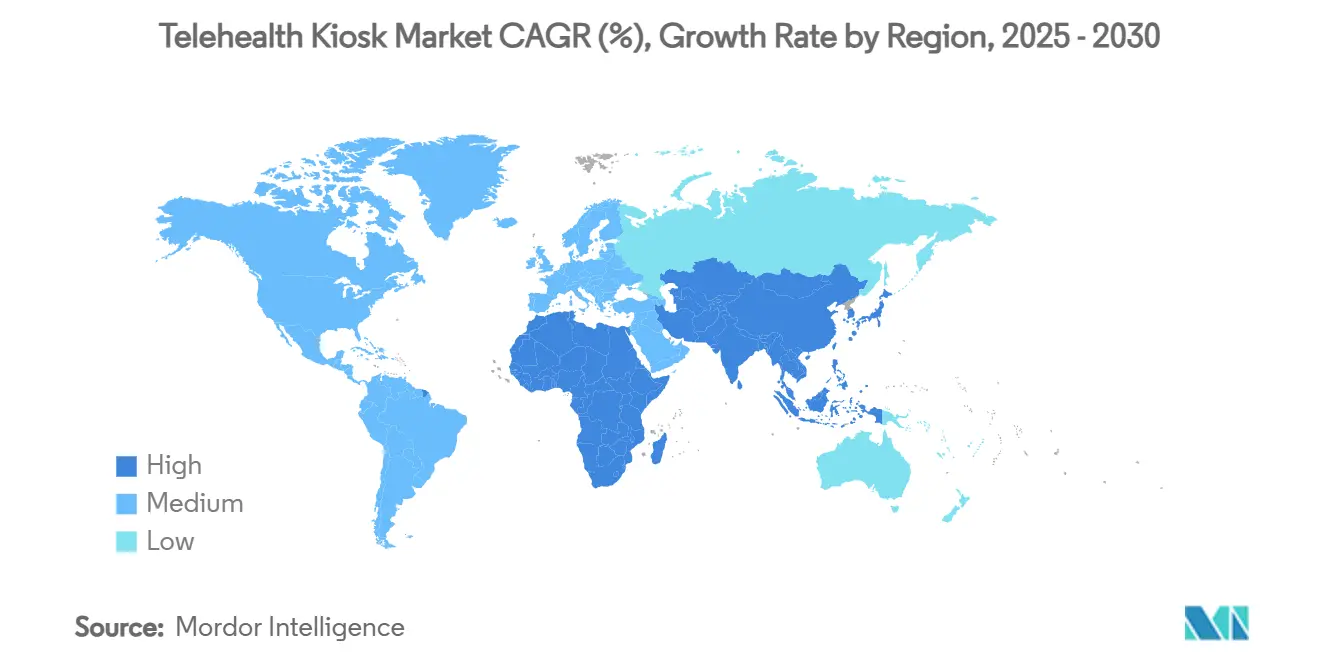

- By geography, North America represented 39.45% of the global telehealth kiosk market size in 2024; Asia-Pacific is set to post the quickest regional advance at 20.18% CAGR to 2030.

Global Telehealth Kiosk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Remote Healthcare & Convenience | + 4.2% | Global, with concentration in rural North America and APAC | Medium term (2-4 years) |

| Shortage Of Healthcare Professionals & Need For Efficiency | + 3.8% | Global, particularly acute in rural EU and North America | Long term (≥ 4 years) |

| Post-COVID Regulatory Support For Telehealth Reimbursement | + 3.1% | North America & EU, with emerging support in APAC | Short term (≤ 2 years) |

| Retail Pharmacy Chains Embedding Diagnostic Pods To Monetise Foot Traffic | + 2.4% | North America core, expanding to EU urban centers | Medium term (2-4 years) |

| Integration Of Advanced Point-Of-Care Diagnostics Inside Kiosks | + 2.6% | Global, led by North America and Japan | Medium term (2-4 years) |

| Shift To Value-Based Care Prompting Payers And Health Systems To Subsidize Telehealth Kiosks | + 2.3% | North America & EU, early adoption in Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Remote Healthcare & Convenience

Ninety-six percent of U.S. community health centers delivered some form of telehealth in 2024 compared with 24% in 2018, illustrating a structural shift in patient expectations.[1]Celli Horstman et al., “Community Health Centers’ Progress and Challenges,” commonwealthfund.orgRural pilots such as University of Rochester Medical Center’s bank-branch stations report that 75% of local patients live more than 10 miles from traditional care sites. OnMed’s airport CareStation demonstrates demand in transient, high-traffic venues. Employers also fuel usage as Fabric’s inherited MeMD network now supports 30,000 companies and 5 million employees. Collectively, these models normalize kiosk-based care points across daily life touchpoints.

Shortage of Healthcare Professionals & Need for Efficiency

Teladoc Health’s Virtual Sitter lets one staff member observe 25% more inpatients, illustrating how kiosks act as clinical force multipliers. Eyebot’s FDA-listed kiosk completes a comprehensive eye exam in 90 seconds without an on-site optometrist. Japan is rolling out Teladoc HEALTH units across six municipalities to offset physician shortages in remote islands. German nursing homes have cut emergency transfers through real-time remote consults funded by statutory insurer Techniker Krankenkasse. Each initiative illustrates how the global telehealth kiosk market closes workforce gaps.

Post-COVID Regulatory Support for Telehealth Reimbursement

Medicare’s telehealth waivers extend through September 2025, allowing home-originating sites and reimbursing audio-only consults.[2]U.S. Department of Health and Human Services, “Medicare Payment Policies,” telehealth.hhs.gov The FDA’s device transition guidance gives kiosk manufacturers a predictable compliance pathway post-PHE.[3]Center for Devices and Radiological Health, “FDA Issues Final Guidances to Assist Transition Plans for COVID-19-Related Medical Devices,” fda.gov HRSA funded 29 health centers to build virtual-care infrastructures that often include kiosks. Parallel reforms in the EU cement cross-border reimbursement, amplifying addressable demand.

Retail Pharmacy Chains Embedding Diagnostic Pods to Monetize Foot Traffic

CVS Health is scaling MinuteClinic primary-care services for Aetna members in three metro clusters. Twenty-six Oak Street Health clinics will sit inside CVS stores by end-2025. Although Walmart shuttered 51 clinics citing cost pressures, Walgreens’ move to a digital-first model across 30 states signals continued retail focus on virtual modalities. Success hinges on converting store traffic into clinical consults, a metric kiosks help pharmacies optimize.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy & Cybersecurity Concerns | -2.1% | Global, particularly stringent in EU under GDPR | Short term (≤ 2 years) |

| High Capital & Maintenance Costs For Hardware | -1.8% | Global, most acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Lack Of Standardised Clinical Workflows For Peripheral Device Calibration | -1.4% | Global, with regulatory complexity in North America and EU | Long term (≥ 4 years) |

| Persistently Low Daily Utilisation Rates At Many Installed Kiosks | -2.3% | Global, particularly challenging in rural and low-traffic locations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy & Cybersecurity Concerns

New FDA draft guidance on AI-enabled device software emphasizes bias mitigation and lifecycle security, elevating compliance costs. Kiosks sited in public areas face added vulnerability versus hospital-grade telehealth carts. Olea Kiosks integrates HID facial authentication to harden patient identity but triggers heightened privacy scrutiny under GDPR and state laws. The trust gap can dampen usage even when technical safeguards exist, restraining near-term growth in the global telehealth kiosk market.

Persistently Low Daily Utilization Rates

Forward’s kiosk program closure shows the break-even challenge when average daily consults fall below vendor assumptions. University of Rochester’s bank-branch pilot targets dense community sites to boost throughput yet still depends on consumer adoption drives. OnMed notes that its diagnostic suite resolves 85% of routine primary-care needs, raising utilization compared with video-only booths. Sustained patient education remains critical for higher usage rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mobile Units Drive Deployment Flexibility

Mobile cart-based kiosks represented the fastest-advancing form factor at a 22.63% CAGR through 2030. The global telehealth kiosk market size for mobile units is projected to expand in lockstep with disaster-response contracts and multi-site hospital networks. OnMed’s FEMA-aligned platform supports surge capacity during public-health crises. Japan integrates mobile Teladoc Health systems into island clinics to ensure real-time specialist input.

Stationary pods still dominated 2024 value with 57.64% global telehealth kiosk market share due to broad diagnostic suites suitable for airports, community centers, and tertiary hospitals. H3 Health Cube’s self-contained clinic underlines sustained innovation in this sub-category. Yet administrators increasingly weigh portability against capital intensity, shifting incremental budgets toward lighter carts and wall units.

By Component: Services Growth Outpaces Hardware

Hardware held 44.23% share in 2024, reflecting unavoidable spend on enclosures, medical peripherals, and networking. FDA alignment with ISO 13485 standards may lift compliance costs, nudging providers toward vendor-managed models.

Services revenue is rising 21.33% annually as providers favor subscription bundles. Teladoc’s USD 65 million Catapult Health buy secures downstream clinic services tied to kiosk deployment. Software upgrades now fold in AI triage and EHR connectivity, segmenting value beyond the initial hardware sale for the global telehealth kiosk industry.

By End User: Retail Pharmacies Emerge Despite Challenges

Retail pharmacies forecast a 20.12% CAGR, propelled by CVS MinuteClinic’s expansion and high footfall synergy. Success depends on converting prescription customers into primary-care consults, an area where kiosk immediacy helps. Long-term care homes adopt kiosks to bridge geriatric specialist gaps, mirrored by German pilots that lowered emergency transfers.

Hospitals and specialty clinics retained 39.63% share in 2024, leveraging mature IT stacks to integrate kiosks into perioperative and outpatient pathways. Government-funded community health centers, now at 96% telehealth penetration, rely on kiosks to conform to HRSA access mandates.

By Application: Behavioral Health Leads Growth

Behavioral health usage will climb at a 21.36% CAGR, reflecting payer coverage of audio-only sessions and AI-mediated mental-health screenings. A recent study reported positive user sentiment toward VR therapy delivered via telehealth kiosks.

Primary care maintained 36.24% share in 2024 as kiosks remain first-contact portals. Teladoc’s next-generation cardiometabolic program blends connected glucose meters with kiosk follow-ups to address chronic disease clusters.

Geography Analysis

Asia-Pacific is the fastest-growing theatre at 20.18% CAGR. Japan’s pediatric emergency vehicles equipped with Teladoc systems chart new mobile-care standards. Thailand’s public-hospital kiosk roll-out and China’s capsule-clinic strategy further widen reach into peri-urban districts.

North America still generated 39.45% of 2024 revenue. Medicare flexibility and FQHC grants headline tailwinds, while creative deployments—such as bank-branch units—extend rural access. Mexico and Canada mirror U.S. regulatory cues, expanding the contiguous market.

Europe shows heterogeneous uptake: Germany’s nursing-home telehealth law accelerates penetration, whereas Eastern Europe lags due to funding gaps. UniDoc’s conflict-zone kiosks underscore potential across the Middle East & Africa, where remote clinics often replace collapsed infrastructure.

Competitive Landscape

Industry fragmentation persists, yet consolidation is underway. Teladoc’s roll-up of Catapult Health and partnership with Amazon’s Benefits Connector reflect a push toward vertically integrated ecosystems. OnMed plans to scale from 17 to 200 stations by end-2025 via payer alliances, illustrating capital-light expansion.

Technology differentiation is sharpening: Eyebot’s 90-second autonomous eye exam widens addressable use cases. FDA lifecycle guidance on AI device software raises entry barriers, favoring well-capitalized firms. Emerging disruptors pursue niches in disaster medicine and employer wellness, avoiding direct confrontations with incumbents in general telehealth functions.

Telehealth Kiosk Industry Leaders

American Well (Amwell)

Olea Kiosks

OnMed

Medcube (HealthCube)

AMD Global Telemedicine

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Wemex equipped Japan’s first pediatric emergency vehicle with Teladoc HEALTH, enabling live specialist consults en route to hospital.

- July 2025: OnMed opened the inaugural U.S. airport CareStation at Bradley International Airport, offering walk-up diagnostics and e-prescriptions.

- April 2025: V-Cube announced the Telecube Clinic, a soundproof online consultation booth designed for workplace and community installations, targeting 500 units nationwide by 2026.

Global Telehealth Kiosk Market Report Scope

| Stationary/Pod-style Kiosks |

| Mobile/Cart-based Kiosks |

| Wall-mounted / Countertop Units |

| Hardware |

| Software |

| Services |

| Hospitals & Specialty Clinics |

| Retail Pharmacies & Retail Clinics |

| Employers & Corporate Campuses |

| Long-term Care & Assisted-Living Facilities |

| Government & Community Health Centers |

| Primary Care & General Consultation |

| Chronic Disease Management |

| Behavioral & Mental Health |

| Urgent Care & Triage |

| Preventive Screening & Wellness |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Stationary/Pod-style Kiosks | |

| Mobile/Cart-based Kiosks | ||

| Wall-mounted / Countertop Units | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By End User | Hospitals & Specialty Clinics | |

| Retail Pharmacies & Retail Clinics | ||

| Employers & Corporate Campuses | ||

| Long-term Care & Assisted-Living Facilities | ||

| Government & Community Health Centers | ||

| By Application | Primary Care & General Consultation | |

| Chronic Disease Management | ||

| Behavioral & Mental Health | ||

| Urgent Care & Triage | ||

| Preventive Screening & Wellness | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the global telehealth kiosk market expected to grow through 2030?

The market is projected to rise from USD 0.444 billion in 2025 to USD 1.028 billion in 2030, reflecting an 18.25% CAGR.

Which kiosk form factor will expand the quickest over the forecast period?

Mobile cart-based units should post the fastest growth, advancing at a 22.63% CAGR as health systems seek flexible, deploy-anywhere solutions.

Why are retail pharmacies investing in telehealth kiosks?

Chains such as CVS leverage kiosks to convert store traffic into reimbursable clinical consults, support primary-care expansion, and integrate medication management on-site.

What is the primary restraint facing large-scale kiosk roll-outs?

Persistently low daily utilization—and the resulting struggle to meet break-even thresholds—remains the biggest operational hurdle, especially in low-traffic settings.

Which region is expected to deliver the strongest growth?

Asia-Pacific leads regional expansion with a forecast 20.18% CAGR, driven by national digitization programs and mobile-clinic initiatives in Japan, Thailand, and China.

How are cybersecurity concerns being addressed?

Vendors now embed multi-factor authentication, encryption, and FDA-aligned AI lifecycle controls to comply with stringent privacy laws and bolster patient trust.

Page last updated on: