Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

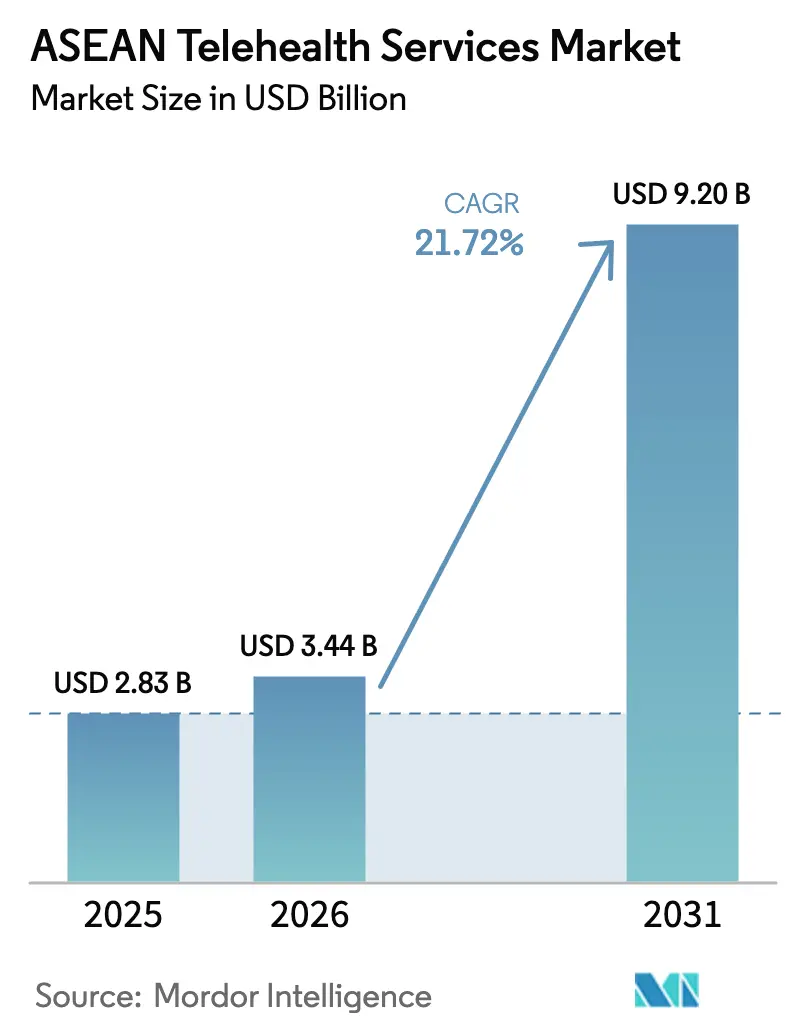

| Base Year Market Size (2025) | USD 2.83 Billion |

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 9.2 Billion |

| Growth Rate (2026 - 2031) | 21.72% CAGR |

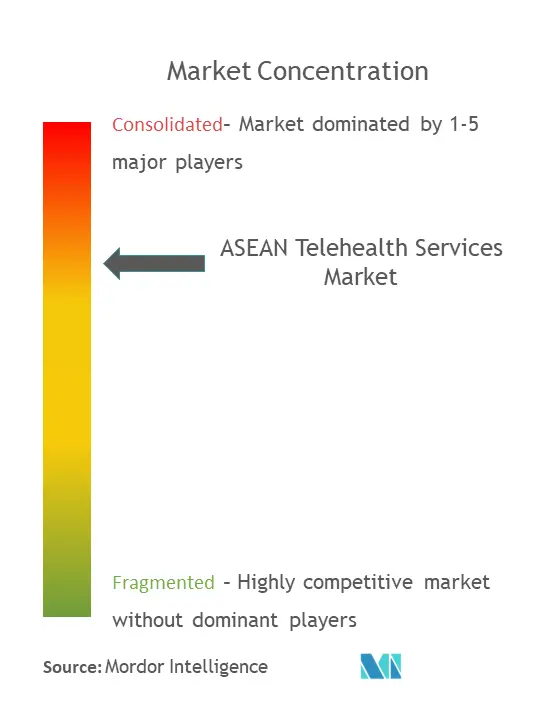

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Telehealth Services Market Analysis by Mordor Intelligence

The ASEAN Telehealth Services Market size was valued at USD 2.83 billion in 2025 and estimated to grow from USD 3.44 billion in 2026 to reach USD 9.2 billion by 2031, at a CAGR of 21.72% during the forecast period (2026-2031). Growth stems from post-pandemic regulatory parity for virtual care, massive 5G investment, and large-scale digitization programs such as Indonesia’s ‘Cek Kesehatan Gratis’ free-screening initiative covering 280 million citizens.[1]Source: Jakarta Globe, “Health Checks for All: A Historic Leap in Healthcare for Indonesia,” jakartaglobe.id Cloud-first deployment, strong venture-capital inflows, and insurer–platform alliances are aligning incentives across payers, providers, and patients. However, fragmented data-residency rules, rising cybersecurity costs, and physician-licensing hurdles temper scalability, leaving room for consolidation moves like WhiteCoat’s 2024 takeover of Good Doctor Indonesia.

Key Report Takeaways

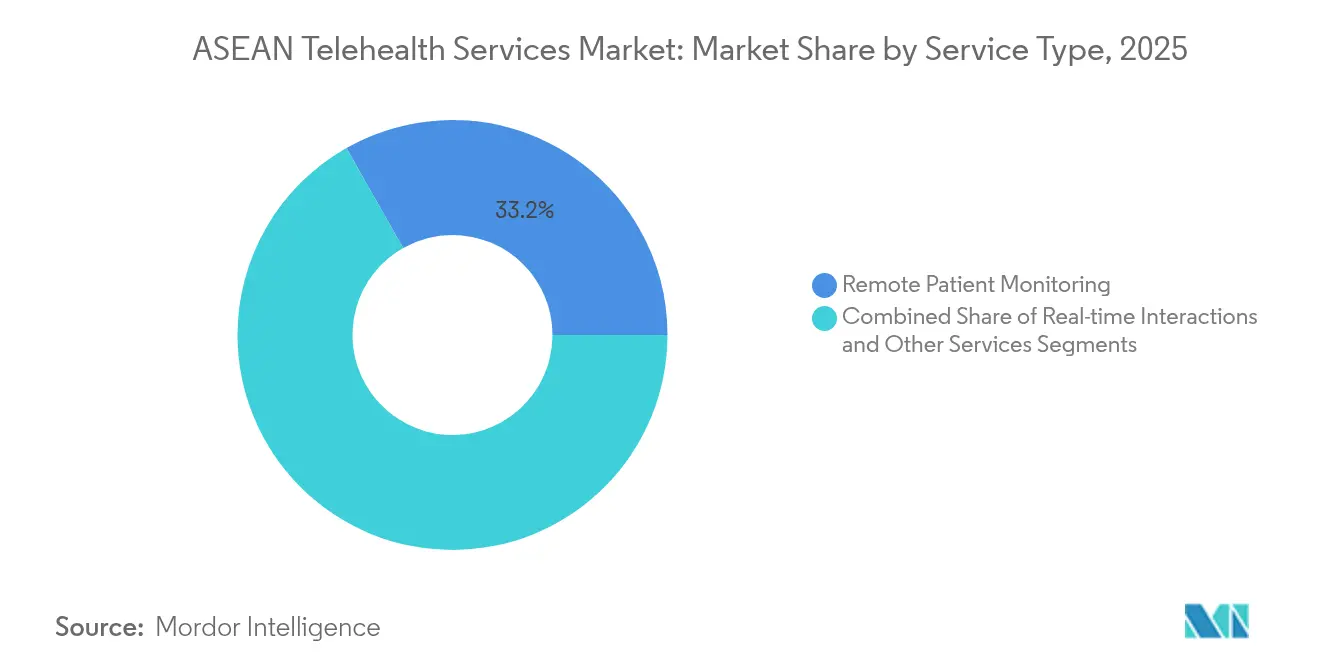

- By service type, remote patient monitoring commanded 33.21% of the ASEAN telehealth services market share in 2025, while real-time interactions posted the highest projected CAGR at 23.11% through 2031.

- By mode of delivery, cloud-based platforms held 47.88% of revenue in 2025; web-based tools are poised for a 22.31% CAGR to 2031.

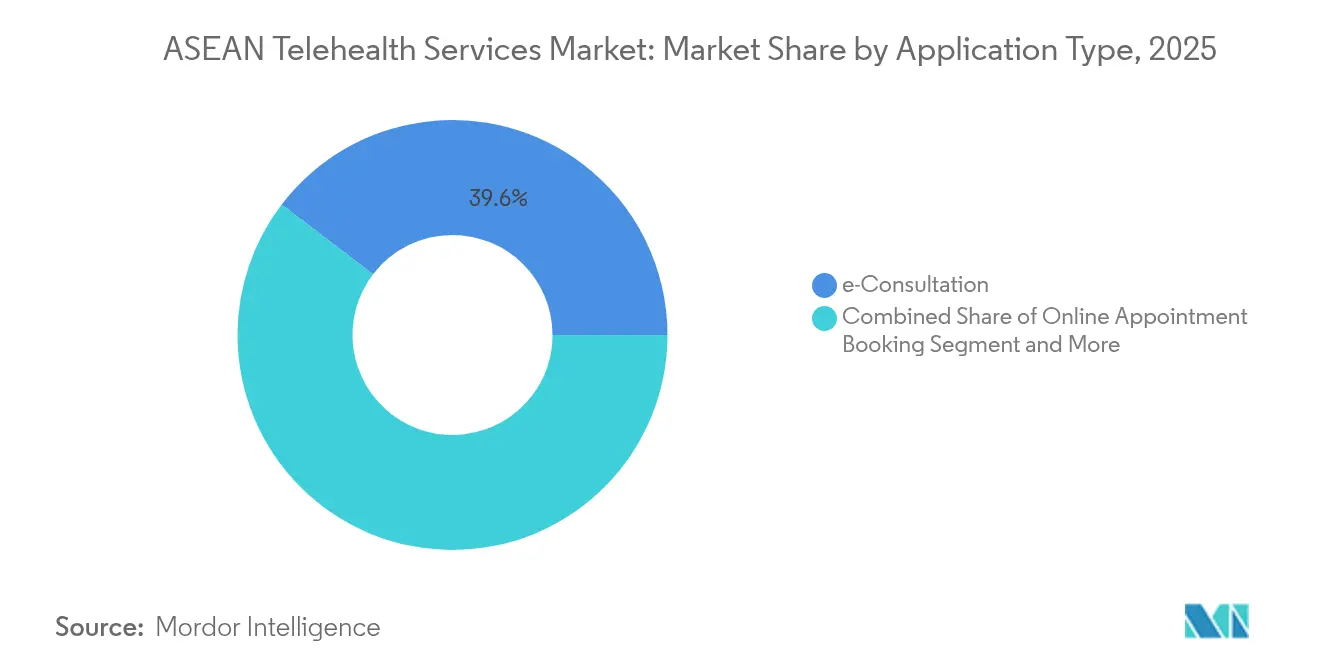

- By application type, e-consultation accounted for 39.62% of the ASEAN telehealth services market size in 2025, whereas tele-pharmacy/e-prescription is set to expand at 23.05% CAGR to 2031.

- By end user, providers retained 48.02% share in 2025; patient-direct services represent the fastest clip at 22.64% CAGR.

- By geography, Indonesia led with 24.89% revenue share in 2025 as Vietnam is forecast to grow the fastest at 22.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Telehealth Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID Reimbursement Parity and E-Prescription Rules | +4.2% | Indonesia, Thailand, Vietnam core markets | Medium term (2-4 years) |

| 5G and Broadband Roll-Outs Boosting Video Quality and Uptime | +3.8% | Singapore, Malaysia, Thailand urban centers | Short term (≤ 2 years) |

| Ageing Population and NCD Burden Raising Chronic-Care Demand | +3.5% | Singapore, Thailand, Malaysia demographic shift | Long term (≥ 4 years) |

| Surge in Venture Capital Funding and Insurer Partnerships | +2.9% | Singapore, Indonesia, Vietnam startup hubs | Medium term (2-4 years) |

| Cross-Border Medical-Tourism "Virtual Second Opinions" | +2.1% | Thailand, Malaysia, Singapore medical hubs | Medium term (2-4 years) |

| AI-Based Mental-Health Triage Chatbots Proving ROI | +1.8% | Urban centers across ASEAN markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-COVID Reimbursement Parity and E-Prescription Rules

Unified payment frameworks now place telemedicine on equal footing with in-person visits. Indonesia’s Presidential Regulation 59/2024 mandates universal insurance participation, closing historic reimbursement gaps.[2]Source: Pemerintah Pusat, “Peraturan Presiden Nomor 59 Tahun 2024,” peraturan.bpk.go.id Thailand’s Ministry of Public Health has followed suit, while Vietnam’s amended pharmacy law enables direct-to-consumer prescription fulfillment from July 2025. These moves support chronic-care monitoring and open cross-border scaling opportunities under consistent pay-rules.

5G and Broadband Roll-outs Boosting Video Quality and Uptime

Network upgrades eliminate historical bandwidth bottlenecks. Telkomsel aims to complete 1,400 5G base stations across Greater Jakarta by February 2025, posting 227 Mbps averages. Singapore’s hybrid 5G trials deliver surgical-grade sub-10 ms latency, while Thailand’s urban speeds of 196 Mbps dwarf outer-city rates yet still sustain HD video. Improved connectivity unlocks remote surgery guidance and continuous monitoring. Cambodia's nationwide 5G approval signals the technology's expansion beyond tier-1 markets, creating opportunities for telehealth platforms to penetrate previously underserved rural populations.

Ageing Population and NCD Burden Raising Chronic-Care Demand

ASEAN’s ≥60-year cohort will hit 22.2% by 2050, straining facility-based care. Non-communicable diseases dominate spending, prompting Indonesia’s BPJS Regulation 3/2024 to fund enhanced screening. Tele-monitoring turns episodic visits into continuous engagement, a model that raises patient lifetime value and supports subscription revenues. The shift toward preventive care models, exemplified by Indonesia's free health screening program for 280 million citizens, generates continuous patient engagement opportunities that telehealth platforms can monetize through subscription-based chronic care management. This demographic-driven demand is particularly valuable because chronic care patients demonstrate higher retention rates and predictable revenue streams compared to acute care episodes.

Surge in Venture-Capital Funding And Insurer Partnerships

Capital allocation patterns reveal strategic shifts toward integrated healthcare ecosystems that combine telehealth platforms with insurance and pharmaceutical distribution. East Ventures’ USD 30 million health fund and Hive Health’s USD 6.5 million pre-Series A confirm robust investor appetite. BPJS Kesehatan’s integration with Halodoc extends platform reach to 221 million Indonesians, proving that insurer hooks drive rapid scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regulatory and Data-Residency Requirements | -2.8% | Cross-border operations across ASEAN | Long term (≥ 4 years) |

| Heightened Cybersecurity / PDPA Compliance Costs | -2.3% | Malaysia, Indonesia, Vietnam data-sensitive markets | Medium term (2-4 years) |

| Inter-Country Physician-Licence Portability Gaps | -1.9% | Cross-border medical tourism corridors | Long term (≥ 4 years) |

| Low Public-Payer Reimbursement Outside Tier-1 Cities | -1.5% | Rural Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory and Data-Residency Requirements

Indonesia’s Personal Data Protection Law forces local data hosting, while Malaysia’s 2025 PDPA amendments require data-protection officers for large health processors. Vietnam’s privacy rules differ again, compelling multi-instance architecture that raises cost and slows regional scaling. Thailand's telemedicine regulations require patient location verification for licensing compliance, creating technical barriers for platforms serving mobile populations or cross-border medical tourists. These fragmented requirements force telehealth companies to develop market-specific solutions rather than leveraging economies of scale across the region.

Heightened Cybersecurity / PDPA Compliance Costs

Rising data protection standards across ASEAN are substantially increasing operational costs for telehealth platforms while creating competitive advantages for companies with robust cybersecurity infrastructure. New breach-notification protocols and stiff penalties demand enterprise-grade security. Smaller platforms struggle to fund encryption, SIEM, and 24/7 monitoring, accelerating consolidation toward well-capitalized players able to certify resilience. The compliance burden is disproportionately impacting smaller telehealth providers who lack the resources to implement enterprise-grade security infrastructure, creating market consolidation pressures that favor well-funded platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Remote Monitoring Drives Preventive-Care Scale

Remote patient monitoring represented 33.21% revenue in 2025, the largest slice of the ASEAN telehealth services market. Wearable biosensors now deliver 99% vital-sign accuracy, enabling early deterioration alerts that cut readmissions by 25%. Biofourmis’s January 2024 in-home ecosystem shows the shift from single-point devices to integrated care programs. Real-time interactions benefit directly from 5G latency drops below 10 ms, supporting complex remote diagnostics.

The ASEAN telehealth services market size for real-time interactions is poised to grow at a CAGR of 23.11% by 2031 as consumers accept video as default first touch. Platform stickiness rises when monitoring pairs with synchronous visits, creating bundled memberships attractive to insurers seeking outcome-based payment models.

By Mode of Delivery: Cloud Architecture Underpins Scale

Cloud-hosted platforms held 47.88% share in 2025 as hospital groups migrate data to hyperscale providers; IHH Healthcare moved Malaysia and Singapore records to Oracle Cloud in mid-2024. Web-based tools post a robust 22.31% CAGR, popular in low-bandwidth zones that rely on browser access rather than heavy mobile apps.

Southeast Asia's data center capacity is growing by up to 20% annually, with major technology companies committing billions to enhance cloud infrastructure that supports telehealth scalability. Cloud lets smaller clinics tap AI modules without capital hardware, while on-premises systems persist where legislation enforces strict data sovereignty. The ASEAN Digital Masterplan 2025 emphasizes cloud infrastructure development as essential for regional digital integration, creating supportive policy environments for cloud-based telehealth expansion.

By Application Type: E-Consultation Anchors Wider Digital Ecosystems

E-consultation captured 39.62% revenue in 2025, the entry point for most users. Tele-pharmacy and e-prescription, growing 23.05% CAGR, get a boost from Vietnam’s 2025 pharmacy-law amendments that legalize e-commerce drug sales. Zuellig Pharma’s eZRx+ serves 61,000 users across nine markets, illustrating the pharmaceutical pivot to digital.

ASEAN telehealth services market share for tele-pharmacy will climb as cross-border e-scripts allow patients in remote islands to refill chronic meds without traveling. AI-enhanced chatbots triage symptoms, reducing clinician load and funneling patients toward targeted drug regimens.

By End User: Direct-To-Consumer Momentum Accelerates

Providers still generated 48.02% of 2025 revenue, bolstered by large hospital roll-outs and insurer contracts. Yet patient-direct channels are expanding at 22.64% CAGR, driven by mobile apps like Halodoc’s Bidanku that reach maternal-care users directly.

ASEAN telehealth services industry players see higher margins in D2C mental-health subscriptions, where AI chatbots deliver personalized sessions at scale, supported by studies showing 21% symptom reduction. Payers increasingly reimburse these programs, aligning financial incentives for longer-term engagement.

Geography Analysis

Indonesia held 24.89% of 2025 revenue, underpinned by the ‘Cek Kesehatan Gratis’ budget of IDR 4.7 trillion (USD 287.9 million) and BPJS integration that links telehealth portals to 221 million insured citizens. ICT maturity scores of 2.74 across nine provinces reveal ongoing infrastructure gaps, presenting vendor opportunities for low-bandwidth solutions.

Vietnam, the fastest-growing at 22.21% CAGR, benefits from 100% insurance coverage for vulnerable groups and an AI virtual hospital pilot focused on telestroke management. Simplified drug registration encourages tele-pharmacy scale, while Microsoft collaborations advance cloud standardization.

Singapore, Thailand, Malaysia, and the Philippines combine mature digital infrastructure with niche growth catalysts. Singapore champions health-tech startups, Thailand leverages its new medical-tourism visa to spur virtual second-opinion demand, Malaysia tightens data-protection rules favoring cybersecurity-strong platforms, and the Philippines’ Hive Health raises new funding for SME care. Cambodia’s nationwide 5G approval foreshadows rural telehealth expansion across the remaining ASEAN states.

Competitive Landscape

Competition is fragmented but tilting toward scale players. WhiteCoat’s purchase of Good Doctor Indonesia created a 6.8 million-user group with 130 insurer links. Platforms vie on AI diagnostics, end-to-end drug logistics, and insurer APIs rather than head-to-head pricing.

Biofourmis teamed with GE HealthCare to commercialize at-home monitoring, integrating hospital-grade sensors with predictive analytics. Halodoc deepens vertical integration by adding lab services and medication delivery, locking consumers into a single app journey.

Future consolidation is likely in mental-health verticals where direct-to-consumer chatbots operate across borders yet face mounting compliance costs. Players with compliant multi-tenant architectures and insurer alliances will outpace niche apps limited by single-country regulation.

ASEAN Telehealth Services Industry Leaders

Doctor Anywhere

Halodoc

Aldokter

SeeYouDoc

Viettel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mobile-health Network Solutions unveiled an AI-enhanced tele-dentistry scan on its MNDR app in Singapore, promising expert review within 24 hours.

- June 2024: Doctor Anywhere partnered with Allianz Partners to extend telehealth benefits to members in Singapore, Malaysia, Thailand, and the Philippines.

- May 2024: MEASAT signed an MoU with Mudah Healthtech to deliver satellite-enabled telehealth to Malaysian remote communities.

- May 2023: ORA raised USD 10 million in Series A funding led by TNB Aura and Antler, marking Southeast Asia’s largest telehealth funding round to date.

ASEAN Telehealth Services Market Report Scope

The Telehealth Services Market in ASEAN is one of the growing and highly demanded Telehealth Services Market as people are more preferring the contactless health prescription and innovative platforms for which Telehealth Services are found much more efficient.

A complete background analysis of the Telehealth Services Market in ASEAN, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles is covered in the report.

The Telehealth Services Market in ASEAN is Segmented By Service Type (Remote Patient Monitoring, Real Time Interactions, Store and Forward), By Type (e-Consultation, Online Appointment Booking, Telemedicine, Diagnostics, and Fitness Monitors), By Mode of Delivery (Web-Based, Cloud-Based, and On-Premises), By End User (Providers, Players, and Patients), and By Geography (Indonesia, Singapore, Vietnam, Thailand and Rest of ASEAN).

By Service Type

| Remote Patient Monitoring |

| Real-time Interactions |

| Other Services |

By Mode of Delivery

| Cloud-Based |

| Web-Based |

| On-Premises |

By Application Type

| e-Consultation |

| Online Appointment Booking |

| Tele-pharmacy / e-Prescription |

| Diagnostics and Fitness Monitors |

By End User

| Providers |

| Patients |

| Payers |

| Others |

By Geography

| Singapore |

| Indonesia |

| Vietnam |

| Thailand |

| Philippines |

| Malaysia |

| Rest of ASEAN |

| By Service Type | Remote Patient Monitoring |

| Real-time Interactions | |

| Other Services | |

| By Mode of Delivery | Cloud-Based |

| Web-Based | |

| On-Premises | |

| By Application Type | e-Consultation |

| Online Appointment Booking | |

| Tele-pharmacy / e-Prescription | |

| Diagnostics and Fitness Monitors | |

| By End User | Providers |

| Patients | |

| Payers | |

| Others | |

| By Geography | Singapore |

| Indonesia | |

| Vietnam | |

| Thailand | |

| Philippines | |

| Malaysia | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the current value of the ASEAN telehealth services market?

The market stands at USD 3.44 billion in 2026 and is projected to hit USD 9.2 billion by 2031.

Which service type leads the ASEAN telehealth services market?

Remote patient monitoring leads with 33.21% revenue share as of 2025.

How fast is the tele-pharmacy segment growing in Southeast Asia?

Tele-pharmacy and e-prescription applications are forecast to advance at a 23.05% CAGR through 2031.

Why is Vietnam considered the fastest-growing telehealth market in ASEAN?

Progressive pharmacy law reforms, AI-hospital pilots, and universal insurance expansion push Vietnam’s market toward a 22.21% CAGR.

What regulation most affects telehealth data management in Malaysia?

The amended Personal Data Protection Act, effective June 2025, mandates data-protection officers and stricter breach protocols.

How are insurers influencing telehealth adoption in Indonesia?

BPJS Kesehatan’s integration with Halodoc instantly connects telehealth services to 221 million covered citizens, accelerating platform uptake.

Page last updated on: