Medical Kiosk Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

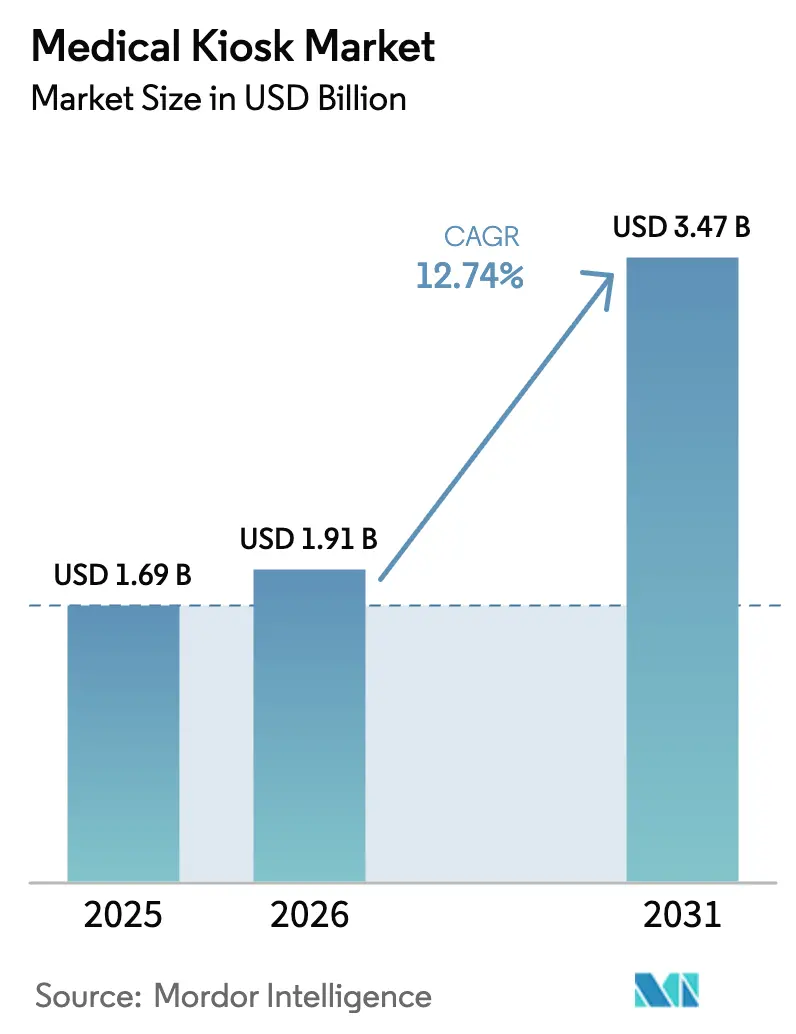

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 12.74% CAGR |

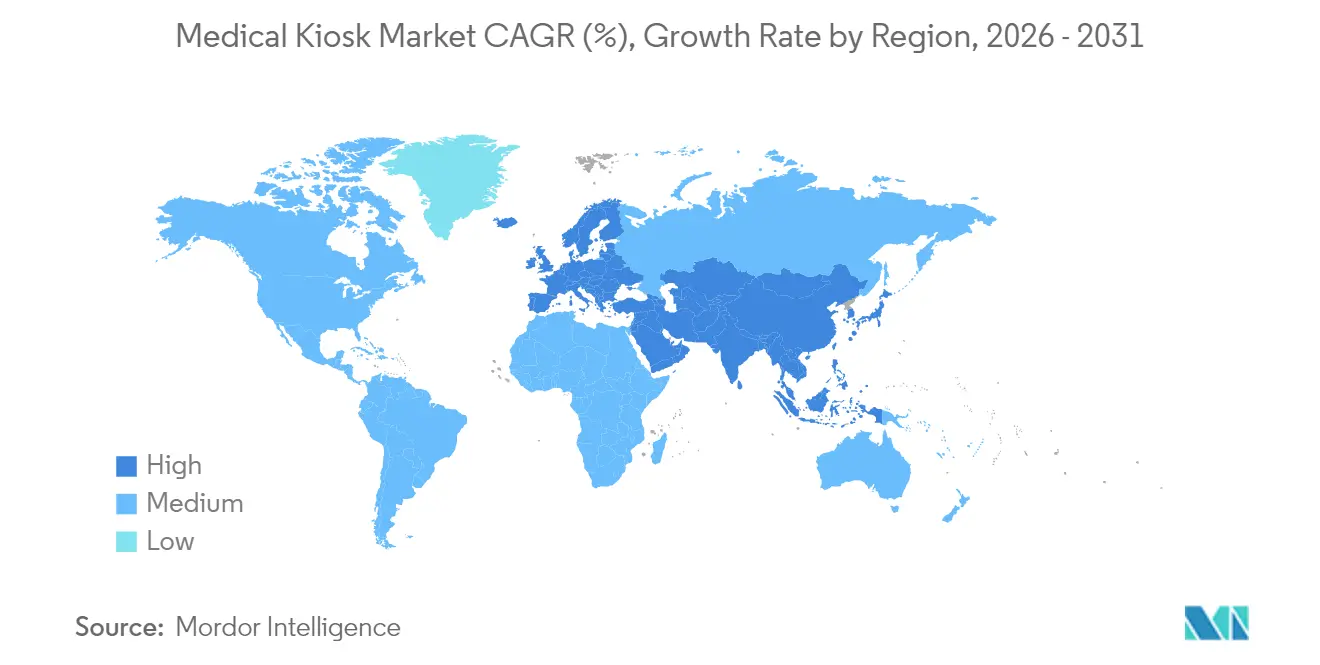

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

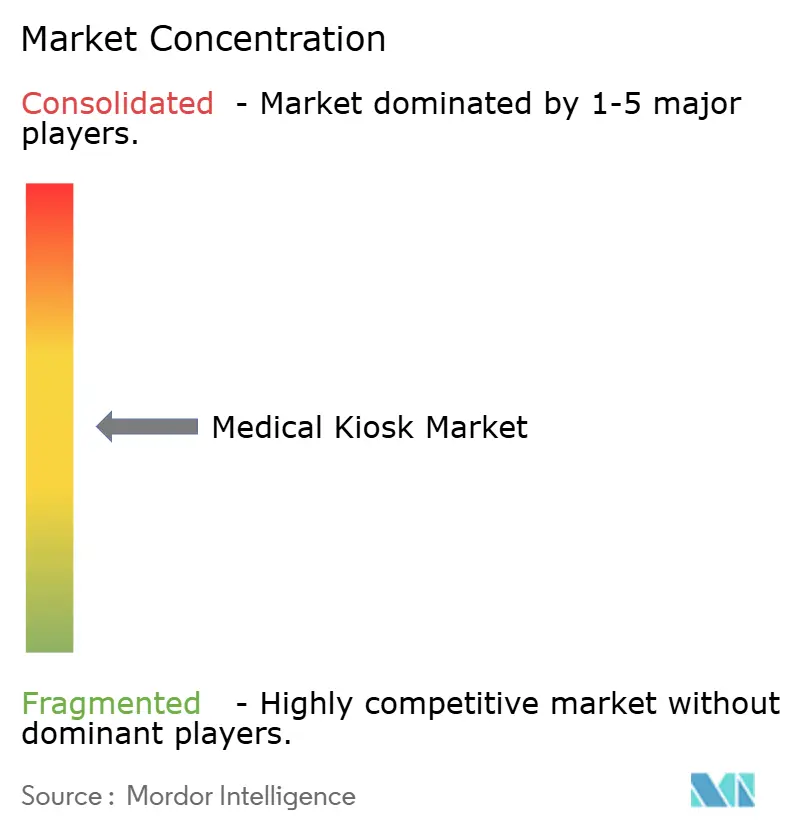

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Kiosk Market Analysis by Mordor Intelligence

The Medical Kiosk Market size was valued at USD 1.69 billion in 2025 and estimated to grow from USD 1.91 billion in 2026 to reach USD 3.47 billion by 2031, at a CAGR of 12.74% during the forecast period (2026-2031).

Strong digital health policies, fast-expanding 5G coverage, and AI-driven diagnostic modules position medical kiosks as core infrastructure of omnichannel care delivery networks. Providers view the units as a practical way to offset staffing shortages, meet chronic-care demand, and comply with post-pandemic infection-control norms. Vendors that bundle hardware, software, and integration services outpace product-only suppliers because health systems rank interoperability and cybersecurity oversight ahead of initial hardware costs. In parallel, retail pharmacies, community banks, and grocery chains deploy telemedicine kiosks to turn foot-traffic locations into care access points, enlarging the commercial addressable base of the medical kiosk market.

Key Report Takeaways

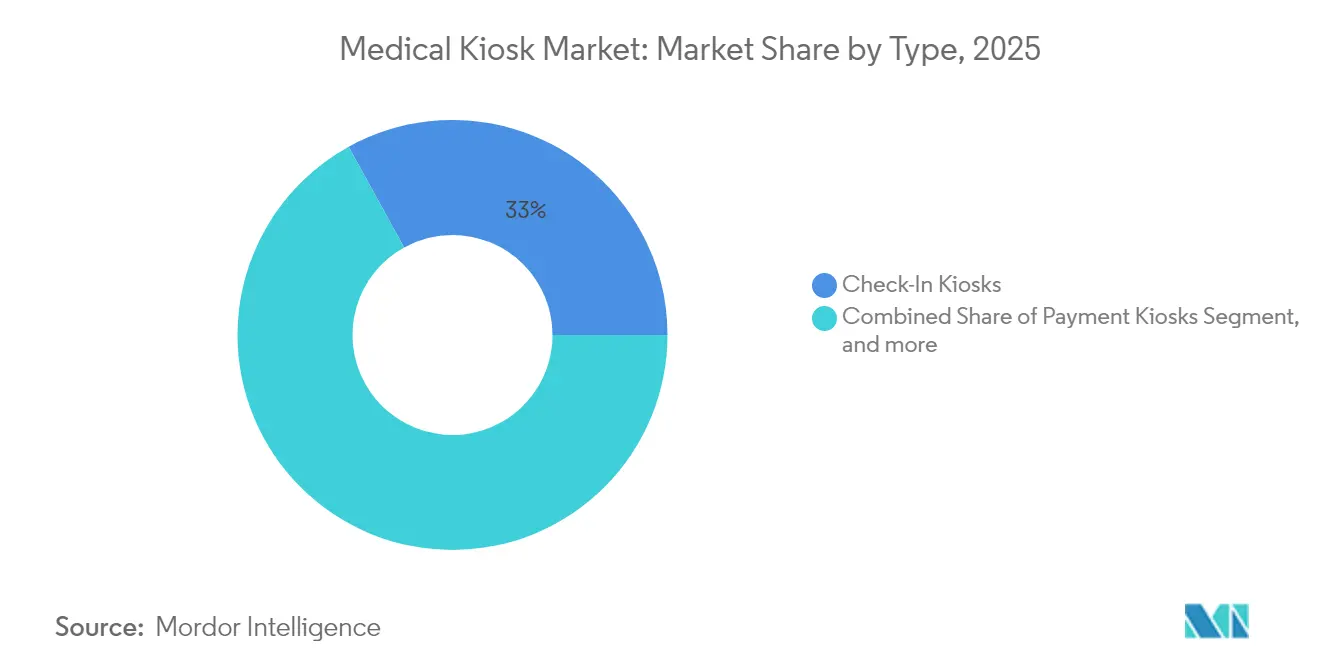

- By type, check-in kiosks led with 33.02% revenue share in 2025, while telemedicine kiosks are projected to expand at a 13.86% CAGR to 2031.

- By component, hardware accounted for 51.05% of the medical kiosk market share in 2025; services record the highest projected CAGR at 15.22% through 2031.

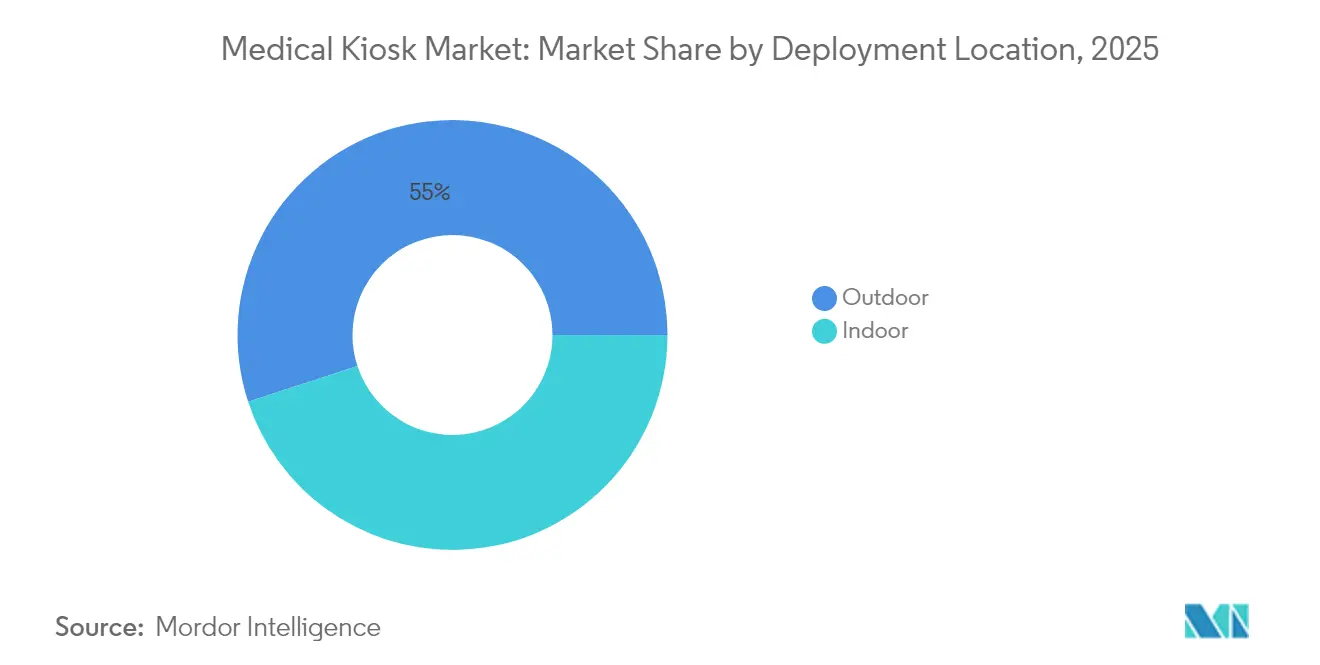

- By deployment location, indoor units held 44.98% of the medical kiosk market size in 2025; outdoor placements are advancing at a 15.59% CAGR through 2031.

- By mobility, freestanding formats captured 40.78% medical kiosk market share in 2025, whereas mobile/cart solutions post a 17.33% CAGR to 2031.

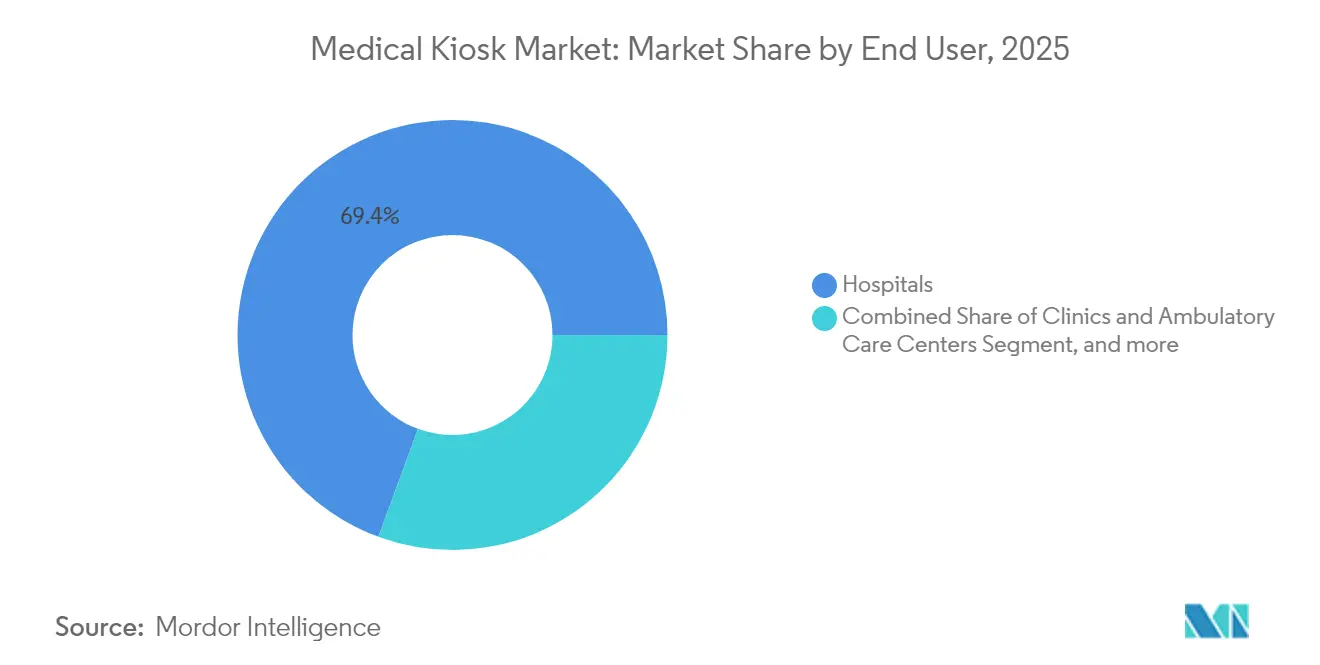

- By end user, hospitals led with 69.40% revenue share in 2025; pharmacies and drugstores are growing fastest at 18.52% CAGR through 2031.

- By geography, North America commanded 46.45% medical kiosk market share in 2025; Asia-Pacific is set to surge at a 19.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Kiosk Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G networks enabling real-time teleconsult | +2.1% | Global, earliest uptake in North America, China, Korea | Medium term (2-4 years) |

| Healthcare digitalization for remote monitoring | +2.8% | Global, spreading to emerging markets | Long term (≥ 4 years) |

| Demand for contactless self-service | +1.9% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Government reimbursement pilots | +1.7% | North America and EU core, expanding in APAC | Medium term (2-4 years) |

| AI-driven triage and diagnostics | +2.3% | Global, fastest in developed economies | Long term (≥ 4 years) |

| Chronic disease rise and physician shortage | +2.4% | Global, acute in rural North America and aging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of 5G Infrastructure Enabling Real-Time Care

Siriraj Hospital’s 5G Smart Hospital project lowered pathology turnaround to minutes and streamed ambulance vitals directly to specialists, proving that ultra-low-latency connectivity makes kiosks viable for critical care interactions.[1]GSMA, “Siriraj Hospital 5G Smart Hospital Case Study,” gsma.com Health systems now plan kiosks as network endpoints rather than stand-alone machines, boosting transaction capacity and reducing unit cost as more devices ride the same 5G backbone. Edge processing further shrinks lag, enabling HD video consults, AI image reads, and remote robotics. The result is a scalable fabric in which each kiosk strengthens the overall care grid—a dynamic underpinning the medical kiosk market worldwide.

Accelerated Healthcare Digitalization Streamlining Patient Remote Monitoring

Remote-monitoring platforms reached 35% AI adoption in 2024, integrating kiosks as public touchpoints for patients lacking connected devices.[2]JMIR Medical Informatics, “National Disease Management Platform Outcomes,” jmir.org Turkey’s Disease Management Platform already logged 73 million chronic encounters by syncing kiosk outputs with its electronic record hub, illustrating how large-scale digital ecosystems absorb self-service endpoints. The shift pushes vendors to certify HL7-FHIR connectors and population-health dashboards, deepening service revenue in the medical kiosk market.

Increased Demand for Contactless, Infection-Controlled Self-Service

Pandemic workstreams normalized touch-free triage. Singapore’s Pharmacy Smart Interface pairs automated dispensing with pharmacist video sessions, trimming queuing time and reducing surface contamination risk. Patient preference surveys show two-thirds of Gen Z users favor kiosk check-in over staffed desks, suggesting durable behavioral change that enlarges the medical kiosk market.

Government-Backed Reimbursement Pilots

US Medicare’s telehealth flexibilities, extended through March 2025, reimburse home and kiosk interactions equally, eliminating geographic barriers and heightening return-on-investment calculations for providers.[3]U.S. Department of Health & Human Services, “Telehealth Flexibilities Extended,” hhs.gov The proposed VA Telehealth Grant plan funds hardware in rural counties, a catalyst that makes kiosks financially feasible for low-volume clinics.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent cybersecurity and data-privacy rules | -1.8% | Global, especially EU and North America | Medium term (2-4 years) |

| High capital and integration costs | -1.4% | Global, strongest in cost-sensitive markets | Short term (≤ 2 years) |

| Limited elderly adoption | -1.1% | Global, notable in aging societies | Long term (≥ 4 years) |

| Vendor lock-in risk | -0.9% | Global, higher in fragmented payer landscapes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Cybersecurity and Data Privacy Regulations

FDA’s Software Bill of Materials mandate forces suppliers to list every code library, inflating compliance cycles and favoring firms with mature DevSecOps teams. The PATCH Act and HIPAA updates require live threat monitoring; 67% of US health systems admit they lack resources for 24/7 coverage, slowing purchase decisions.

High Capital Expenditure and Integration Costs

Full-featured telemedicine kiosks run into six-figure deployments once EHR connectors, cyber audits, and staff training are included. Smaller clinics often defer projects or choose pared-down hardware, compressing near-term uptake in some segments of the medical kiosk market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Telemedicine Kiosks Drive Clinical Transformation

Check-In Kiosks held 33.02% medical kiosk market share in 2025, yet telemedicine units are expected to grow with 13.86% CAGR between 2026 and 2031 outpaces every other type in the medical kiosk market. Check-in kiosks still dominate day-to-day workflows, but sustained reimbursement for video consults elevates diagnostic kiosks to enterprise-level priority. In busy ambulatory centers, a single telemedicine kiosk can conduct vitals, provide AI-triage, and connect to an off-site physician in one room cycle, freeing in-house staff for acute cases.

Vital-signs and pharmacy kiosks follow a similar clinical logic, supplying chronic-care data and immediate dispensing in one stop. Payment and way-finding models remain relevant for throughput but face mobile-app redundancy. As AI modules mature, suppliers bundle multiple functions, nudging buyers toward platform contracts and enlarging the medical kiosk market.

By Component: Services Growth Reflects Integration Complexity

Hardware held 51.05% medical kiosk market share in 2025, yet services clock the fastest trajectory at 15.22% as hospitals outsource HL7 integration, SBOM documentation, and patch management. Each regulatory cycle expands the service attach rate, turning managed-service agreements into multi-year revenue streams that stabilize vendor cash flow.

Software remains pivotal for user interface and AI inference engines. Still, license revenue often converts into subscription, blurring lines between software and services. Vendors emphasizing turnkey delivery now close larger deals, signaling that ecosystem capabilities trump hardware features in the medical kiosk market.

By Deployment Location: Outdoor Growth Signals Access Expansion

Outdoor units, projected at a 15.59% CAGR, transition kiosks from facility fixtures to community assets. Hartford HealthCare’s supermarket placements illustrate congestion relief at hospitals and meet patients where daily life unfolds. Ruggedized enclosures, solar backup, and multi-path connectivity mitigate uptime concerns, broadening geographic reach.

Indoor locations remain critical for high-acuity settings and controlled diagnostics and held 44.98% of overall revenue in 2025. Yet payers now reimburse outdoor kiosk encounters, tipping total cost of care models toward distributed placement. This flexibility widens the medical kiosk market size for vendors equipped to certify weatherproof designs.

By Mobility: Mobile Solutions Enable Flexible Care Delivery

Freestanding models dominate base installations with 40.78% in 2025, but mobile carts post a 17.33% CAGR through 2031, reflecting a pivot to event-based and outreach care. Philippine health authorities deploy cart units after typhoons to restore chronic services within 48 hours, underscoring mobility’s disaster-response value.

Mobile designs must balance battery life, connectivity, and onboard sterilization. Vendors that master these technical nuances capture incremental revenue from humanitarian agencies and employer clinics, enriching the medical kiosk market landscape.

By End User: Pharmacy Adoption Accelerates Retail Healthcare

Pharmacies and drugstores, with an 18.52% CAGR, merge dispensing and diagnostics, cutting refill cycles and adding immunization revenue streams. Walgreens’ robotic fulfillment rollout to 5,000 stores clears back-of-house space, leaving front-of-store areas for telehealth pods that elevate the medical kiosk market.

Hospitals, still the largest buyers commanding 69.40% of overall medical kiosk market size in 2025., integrate kiosks into command centers to distribute triage load. Banks, universities, and long-term-care chains follow as secondary adopters, each pushing new workflow requirements that spur iterative product upgrades.

Geography Analysis

North America generated 46.45% of global revenue in 2025 as Medicare policy continuity and grant funding de-risk capital outlays. Regional kiosk density now averages one unit per 42,000 residents, a ratio policymakers deem favorable for preventive-care access. Demand also benefits from cohesive broadband and cloud-hosting ecosystems, giving suppliers predictable service margins in the medical kiosk market.

Europe’s blend of aging demographics and universal payer models sustains steady replacement cycles. Yet GDPR’s rigorous consent protocols extend deployment lead times, compelling vendors to preload privacy-by-design features. Outdoor telehealth kiosks in Spain’s CostadelSol region now support tourist populations without local medical records, showing that interoperability hurdles can be cleared when public funds align with commercial expertise.

Asia-Pacific posts the fastest expansion at 19.56% CAGR, lifting regional procurement budgets for remote-care endpoints. Government smart-hospital grants in Thailand and India’s Ayushman Bharat digital mission keep the medical kiosk market in high gear. Meanwhile, South Korea pilots 5G-linked kiosks at metro stations, illustrating infrastructure convergence. Growth in the Middle East, Africa, and South America follows capital investment cycles but remains hampered by patchy connectivity and limited local service partners.

Competitive Landscape

The market is moderately concentrated. Large self-service vendors such as NCR leverage supply-chain scale and field-service footprints to win multisite deals, while focused players like OnMed and UniDoc Health differentiate on telehealth workflow and diagnostic scope. International standard ISO/IEEE 11073-10700:2024 now anchors device connectivity rules, rewarding firms that pursued open-architecture designs early.

Strategy pivots center on ecosystem partnerships. OnMed teamed with the US National Disaster Medical System to validate CareStation units for emergency deployments, demonstrating the brand equity that mission-critical trials confer. NCR’s software-defined kiosk roadmap signals intent to fold healthcare into its managed-service portfolio following an 8% rise in self-service banking revenue in Q4 2024.

Pricing power remains dispersed, yet vendors bundling cybersecurity monitoring and reimbursement coding see higher contract retention. As buyers consolidate around interoperable platforms, suppliers with narrowly framed offerings risk relegation to niche plays, an undercurrent shaping future share shifts inside the medical kiosk market.

Medical Kiosk Industry Leaders

Fabcon, Inc.

Meridian Kiosks

VeriFone, Inc.

XIPHIAS Software Technologies

RedyRef Interactive Kiosks

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NCR Atleos Corporation reported strong Q4 2024 financial results with self-service banking segment revenue of USD 718 million, representing 8% growth. The company's focus on enhancing self-service solutions and improving customer experiences aligns with growing demand for automated healthcare services, indicating potential expansion into medical kiosk applications.

- January 2024: Hartford HealthCare launched a partnership with OnMed to deploy Care Stations in Stop & Shop supermarkets across Connecticut. This initiative provides convenient healthcare access through virtual consultations and diagnostic capabilities, demonstrating the retail healthcare model's expansion beyond traditional pharmacy settings.

- November 2024: OnMed, CareSource, and Valley Healthcare collaborated to introduce the OnMed CareStation in Columbus, Georgia, marking the first federally qualified health center to offer hybrid care solutions. The USD 180,000 investment from CareSource supports healthcare access for underserved communities through self-contained medical units with advanced diagnostic tools.

- September 2024: Auburn University expanded its rural health partnership with OnMed, serving over 75,000 residents across five counties with plans to deploy 20 stations by year-end and 200 stations by 2025. This expansion addresses physician shortages and hospital closures in rural Alabama through innovative technology deployment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical kiosk market as the total annual revenues derived from self-service, patient-facing terminals that perform registration, payment, way-finding, clinical screening, or tele-consultation inside healthcare and pharmacy settings. Hardware sales, accompanying software licenses, and bundled integration services are all included, whereas standalone telehealth platforms without a physical enclosure are not.

Scope Exclusion: vending-style drug dispensing lockers and non-medical retail kiosks fall outside this assessment.

Segmentation Overview

- By Type

- Check-In Kiosks

- Payment Kiosks

- Way-Finding & Information Kiosks

- Telemedicine / Telehealth Kiosks

- Vital-Signs Measurement Kiosks

- Pharmacy / Medication-Dispensing Kiosks

- Patient Education Kiosks

- Others

- By Component

- Hardware

- Software

- Services

- By Deployment Location

- Indoor

- Outdoor

- By Mobility

- Freestanding

- Wall-Mounted

- Countertop

- Mobile / Cart

- By End User

- Hospitals

- Clinics & Ambulatory Care Centers

- Pharmacies & Drugstores

- Diagnostic Laboratories

- Long-Term Care Facilities

- Corporate & Industrial Health Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview kiosk OEM product heads, hospital CIOs, pharmacy chain operations managers, and digital-health regulators across North America, Europe, and Asia-Pacific. These discussions test pricing corridors, average refresh cycles, and real-world throughput gains, letting us reconcile secondary ratios with on-ground economics before model lock-in.

Desk Research

Mordor analysts first compile public-domain datasets, such as FDA 510(k) device clearances, U.S. Census outpatient facility counts, CMS outpatient visit volumes, and OECD Health-IT adoption indices, to map the installed base and utilization of self-service stations. Trade association white papers (HIMSS, Kiosk Manufacturers Association), customs shipment ledgers, and peer-reviewed studies on patient journey times then anchor regional penetration assumptions. Our paid feeds, notably D&B Hoovers for vendor financial splits and Dow Jones Factiva for deal flow, sharpen revenue attribution across hardware, software, and services.

Additional inputs arrive from national tenders portals, patent families retrieved via Questel, and state telehealth reimbursement rules, enriching trend direction for indoor versus mobile pod deployments. The desk-research list is illustrative; many other sources supplement validation and narrative building.

Market-Sizing & Forecasting

A top-down reconstruction begins with outpatient and pharmacy footfall, applies region-specific kiosk penetration rates, and multiplies the resulting unit counts by blended average selling prices. Select bottom-up checks, supplier revenue roll-ups and sampled service contracts, calibrate the totals. Key variables include kiosk penetration per 10,000 outpatient visits, average hardware ASP, paid software subscription attach rate, telemedicine visit growth, and capital budget allocation per hospital bed. Forecasts employ multivariate regression, where kiosk shipments track facility digitalization scores and broadband density, and ARIMA smoothing adjusts short-run shocks. Gaps in bottom-up inputs, for example, small-clinic volumes, are bridged using median utilization proxies gathered during primary calls.

Data Validation & Update Cycle

Outputs pass three-stage variance screening, peer review, and senior analyst sign-off. We refresh the model annually; mid-cycle triggers, major regulatory shifts or mergers, prompt expedited revisions, guaranteeing clients the latest perspective.

Why Mordor's Medical Kiosk Baseline Commands Reliability

Published estimates often diverge because firms differ on what constitutes a "medical kiosk," the share of services they monetize, and how often they refresh exchange-rate or ASP assumptions.

Key Gap Drivers: some publishers pool all self-service machines, others model only hardware units, several lift ASPs from limited pilots, and a few extrapolate global totals from single-country datasets. Our scope alignment, dual-track (top-down and bottom-up) build, and annual refresh cadence minimize such skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.69 B (2025) | Mordor Intelligence | - |

| USD 1.42 B (2023) | Global Consultancy A | Hardware-only scope; no service revenues; two-year-old FX rates |

| USD 1.76 B (2024) | Industry Association B | Uses global kiosk average ASP, not healthcare-specific; relies on voluntary vendor surveys |

| USD 1.50 B (2024) | Trade Journal C | Excludes Asia-Pacific; projects volumes from five hospital chains |

The comparison shows that when scope, ASP logic, and refresh cadence vary, so do numbers. Mordor's disciplined variable selection and transparent reconciliation steps give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the projected size of the medical kiosk market by 2031?

The market is forecast to reach USD 3.47 billion by 2031, reflecting a 12.74% CAGR over the period (2026-2031).

Which segment grows fastest within the medical kiosk market?

Telemedicine kiosks record the highest growth, expanding at a 13.86% CAGR as providers shift from administrative to clinical self-service.

Why are services outpacing hardware in revenue growth?

Integration with EHRs, cybersecurity compliance, and ongoing software support drive a 15.22% CAGR for services, exceeding hardware’s pace.

Which region leads in medical kiosk market share today?

North America holds 46.45% share due to mature IT infrastructure and supportive reimbursement policy.

How do pharmacies benefit from adopting kiosks?

Pharmacies leverage kiosks for teleconsults and automated dispensing, enabling an 18.52% CAGR in the segment by merging medication fulfillment with primary care.

What is the main regulatory hurdle for kiosk vendors?

Compliance with FDA’s Software Bill of Materials and broader cybersecurity mandates increases development and operational costs, especially for smaller manufacturers.

Page last updated on: