Tanzania Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

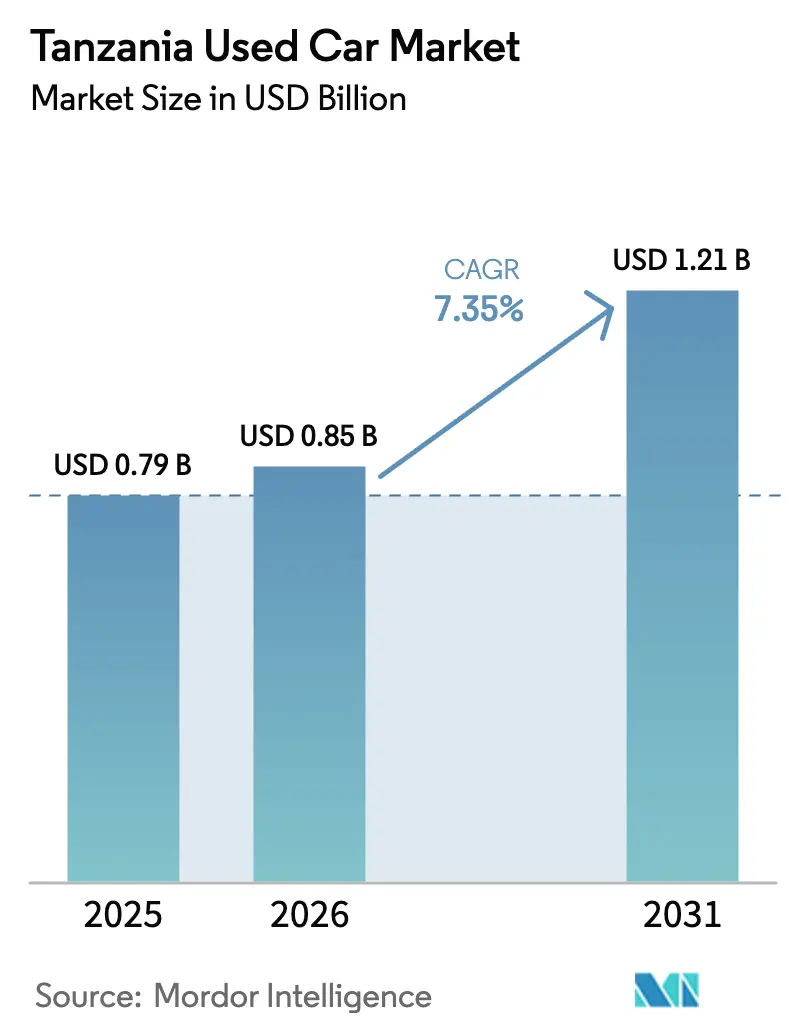

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tanzania Used Car Market Analysis by Mordor Intelligence

Tanzania's used car market size in 2026 is estimated at USD 0.85 billion, up from USD 0.79 billion in 2025, with 2031 projections of USD 1.21 billion, growing at a 7.35% CAGR over 2026-2031. Robust urbanization, an expanding middle class, and steady digital adoption continue to broaden access to pre-owned vehicles, especially for first-time buyers seeking affordable mobility solutions. Mobile-first classifieds now anchor search and discovery, while improved road infrastructure underpins demand beyond Dar es Salaam into secondary cities. Local banks, fintechs, and mobile money operators are deepening credit penetration and lowering entry barriers for younger consumers. Import duty rebates on hybrid, CNG, and battery-electric vehicles are accelerating a gradual transition away from fuel types, expected to reshape model availability over the next five years.

Key Report Takeaways

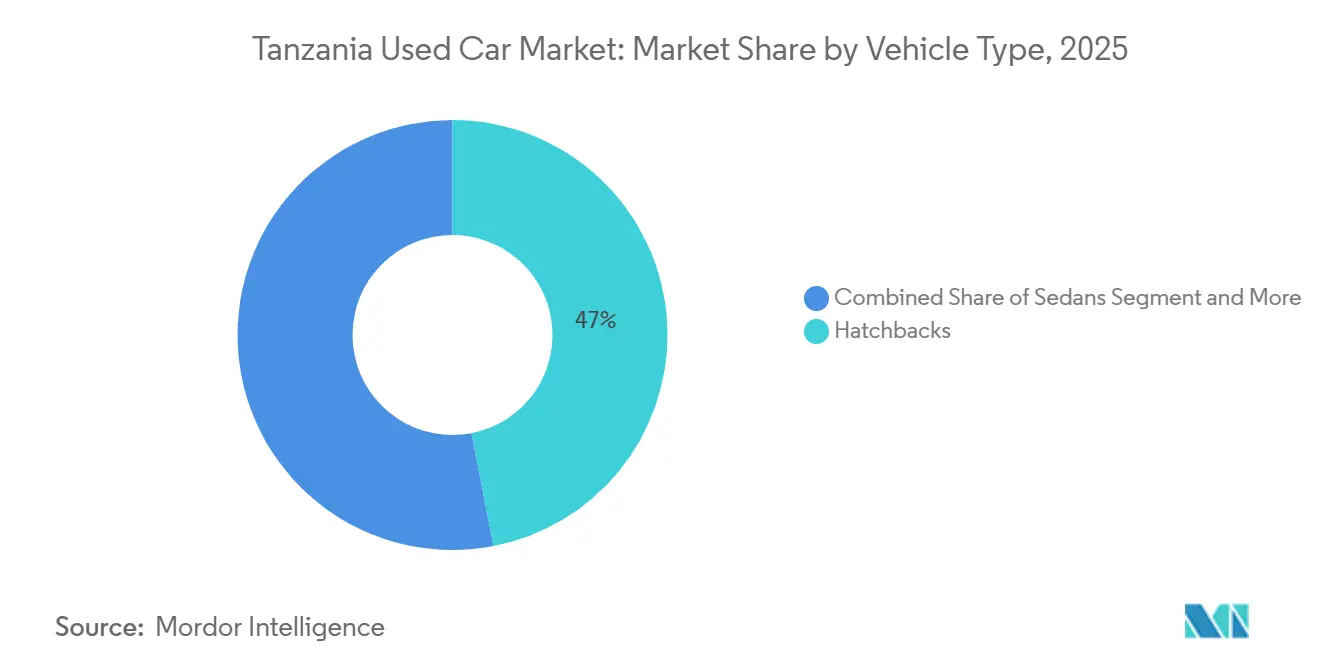

- By vehicle type, hatchbacks led with 46.95% of Tanzania's used car market share in 2025, whereas SUVs recorded the fastest CAGR at 11.16% through 2031.

- By vendor type, the unorganised channel held 71.99% of the Tanzania used-car market in 2025, while organised dealers advanced at a 9.44% CAGR toward 2031.

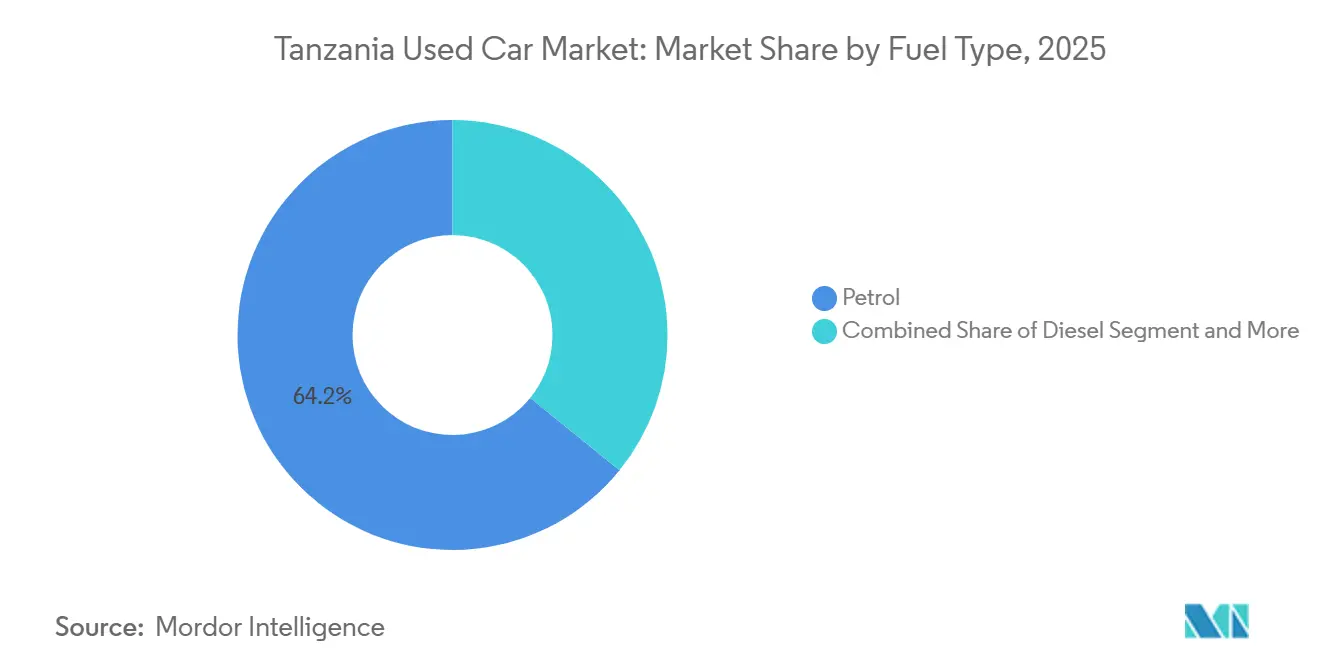

- By fuel type, petrol models dominated with 64.17% share in 2025, but battery-electric vehicles expanded at 20.29% CAGR over the forecast period.

- By vehicle age, the 3 to 5-year band captured 38.29% of the market in 2025; 0 to 2-year units will show the highest CAGR at 10.35% toward 2031.

- By price segment, models below USD 5,000 represented 44.29% of 2025 sales, yet the USD 20,000 to 29,999 band is set to expand fastest at 11.16%.

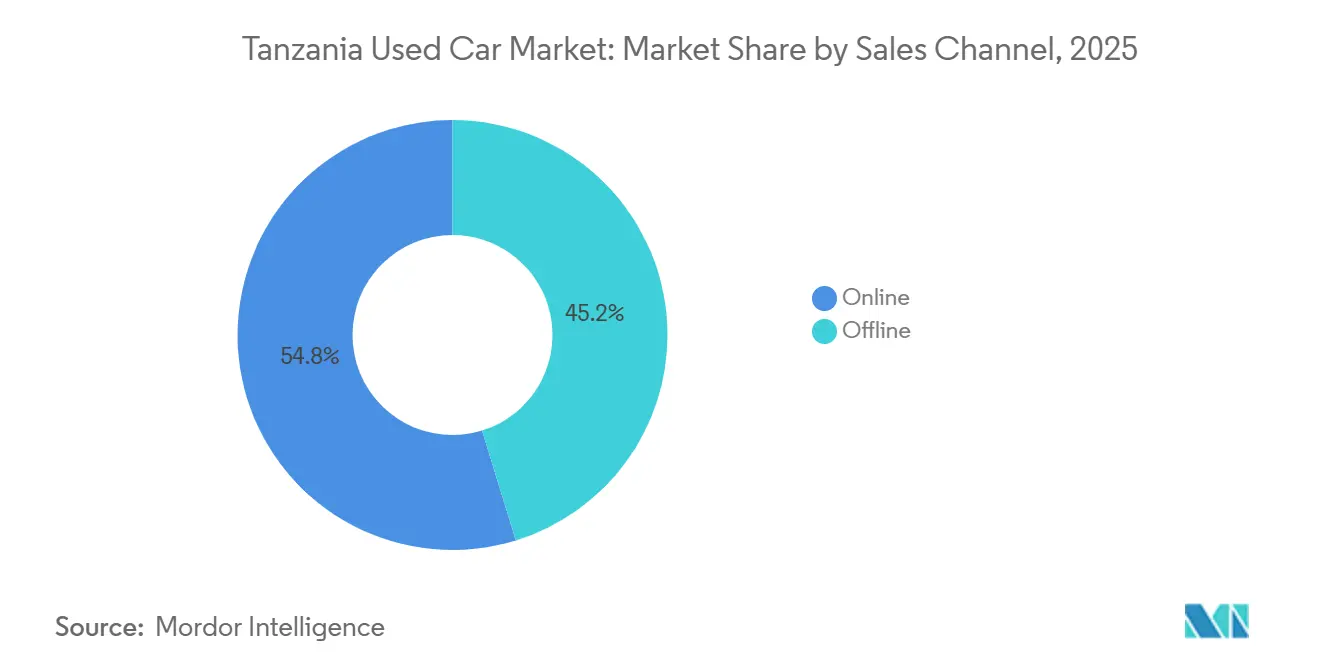

- By sales channel, online platforms commanded a 54.78% share in 2025 and are on track for an 11.57% CAGR through 2031.

- By ownership, multi-owner vehicles formed 68.85% of transactions in 2025, whereas first-owner resales are set to rise at a 9.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The contribution of Tanzania is incorporated into a multi-country and multi-region total that reflects the full breadth of industry. The used car market size by Mordor Intelligence expresses that combined magnitude.

Tanzania Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-First Digital Classifieds | +1.8% | National, concentrated in Dar es Salaam and urban centers | Medium term (2-4 years) |

| Middle-Income Aspirational Buyers | +1.6% | National, with early gains in Dar es Salaam, Arusha, Mwanza | Long term (≥ 4 years) |

| Used-Car Financing Expansion | +1.4% | National, leveraging mobile money infrastructure | Medium term (2-4 years) |

| Import Duty Rebates | +1.1% | National, supporting EV and hybrid adoption | Long term (≥ 4 years) |

| AI-Driven Pricing and Inspection | +0.9% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Inflow of Japanese Kei Cars | +0.7% | National, particularly appealing to cost-conscious segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Mobile-First Digital Classifieds

In Tanzania, the used car market is thriving, driven by mobile-first platforms. As of the first quarter of FY2025, over 80% of the population is online, with more than 56 million internet subscriptions[1]Peter Nyanje, "Tanzania’s digital boom: Internet and mobile services soar" Business Insider Tanzania, businessinsider.co.tz. Online applications seamlessly integrate mobile money payments, location-based listings, and chat features, aligning closely with local buying habits. Thamani.co.tz, a trailblazer in AI-driven appraisal services, is bridging the information gap for buyers and sellers. This heightened transparency fosters trust in remote transactions, diminishing the importance of traditional neighborhood lots. As a result, market efficiency is rising, leading to higher unit turnover across all price ranges.

Growth of Middle-Income Aspirational Buyers

Rising disposable income and 6.3% year-on-year growth in the second quarter of 2025 economic expansion are lifting household purchasing power[2]National Bureau of Statistics (NBS) - Tanzania, "Tanzania GDP Annual Growth Rate", Trading Economics, tradingeconomics.com. A younger demographic profile translates into first-time car ownership ambitions, with demand clustering around compact imports from Japan. Increasing credit uptake, reflected in annual private-sector lending growth, allows families to stretch budgets toward newer models. Controlled inflation near 3% has stabilized monthly installment planning. Collectively, these socioeconomic gains underpin sustained volume growth in the Tanzania used car market.

Expansion of Used-Car Financing Products

Fintech lenders, microfinance firms, and traditional banks are converging on digital underwriting linked to mobile-wallet data. Instant loan approvals are shortening decision cycles from weeks to days. Partnerships between telecom operators and credit providers reduce collateral hurdles, boosting approval rates for informal-sector earners. Cross-selling of insurance and maintenance plans through the same apps extends customer lifetime value for dealerships. The resulting liquidity influx invigorates organised-dealer inventory turn and supports higher average selling prices.

Import Duty Rebates for Low-Emission Vehicles

Zero-percent import duty on unassembled hybrids, together with excise exemptions for EVs and CNG units, is tilting acquisition economics toward cleaner drivetrains. Local distributors now bundle tax savings into competitive sticker prices that rival conventional petrol models. Growing CNG station rollouts increase confidence in route coverage. Combined, these measures accelerate the anticipated fuel-mix transition over the next decade in the Tanzanian used-car market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Retail Fuel Prices | -1.1% | National, affecting operational costs | Short term (≤ 2 years) |

| Tanzanian Shilling Depreciation | -1.0% | National, impacting import costs | Medium term (2-4 years) |

| Age-Cap and Emissions Rules | -0.9% | National, reducing available inventory | Long term (≥ 4 years) |

| Limited Charging Network | -0.6% | Urban centers, constraining EV segment growth | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Retail Fuel Prices

Pump-price swings unsettle household budgeting, nudging buyers toward smaller engines or alternative fuels. Temporary price relief offers only short-lived sentiment boosts, while broader oil-market gyrations keep lifetime-cost calculations fluid. Larger SUVs, therefore, suffer periodic demand dips, despite road infrastructure improvements—dealers hedge volatility through flexible financing plans that absorb sudden spikes in refueling costs. Even so, ongoing unpredictability acts as a mild drag on headline growth in the Tanzania used-car market.

Tanzanian Shilling Depreciation Vs. JPY and USD

Currency weakness inflates CIF prices on Japanese imports, directly raising sticker tags. Additional VAT and excise layers magnify end-user cost pressures. Dealers often pass fluctuations downstream, prompting shoppers to delay purchases or down-trade to older units. Hedging tools remain underdeveloped, leaving most retailers exposed. Consequently, forex volatility represents the most significant macro risk to the sustained expansion of the Tanzania used car market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Compact Formats Anchor Demand

Hatchbacks accounted for 46.95% of the used-car market share in Tanzania in 2025. Their dominance reflects tight urban parking, lower fuel bills, and favorable import duties on sub-1,500 cc engines. SUVs, though emerging fast at 11.16% CAGR, remain aspirational choices that gain traction as road upgrades spread up-country. Sedans maintain relevance for professional users, while MPVs answer family and light-commercial hauling needs.

Continued population inflows into Dar es Salaam are expected to reinforce compact-car momentum. Government duty-rebate incentives further elevate demand for fuel-efficient models, including hybrid variants of popular hatchbacks. The Tanzania used-car market for SUVs will grow steadily amid lifestyle shifts, yet compact platforms will likely remain volume anchors through 2031.

By Vendor Type: Formal Channels Gain Traction

Unorganised vendors retained a dominant 71.99% share of transactions in 2025, reflecting the weight of long-standing personal networks and cash-driven bargaining in Tanzania’s city neighborhoods. Yet organised dealers, supported by franchised importers and local banks, grew revenue at a brisk 9.44% CAGR, proving that structured warranties and transparent pricing resonate with risk-averse families. Digital storefronts showcase uniform inspection reports, narrowing the information gap that once favored aggressive street-lot haggling. Finance tie-ups further expand access, allowing salaried workers to convert mobile-money histories into formal credit scores without exhausting savings. Combined, these features chip away at the informal sector’s grip and lift consumer expectations around after-sales accountability.

Government interest in stronger consumer-protection rules signals mounting pressure on loosely regulated yards, especially as tax authorities trial e-receipt systems that track every deal. Organised players leverage working-capital lines to refresh stock quickly, so shoppers find late-model units that informal peers struggle to import. The same balance-sheet strength funds staff training and spare-parts inventories, raising service quality well beyond one-off corner lots. As digital classifieds normalize up-front vehicle histories, buyers grow less tolerant of undocumented repairs, nudging traffic toward branded showrooms. All signs therefore point to steadily rising formal penetration in the Tanzania used-car market by the decade’s close.

By Fuel Type: Transition Pathways Multiply

Petrol vehicles still ruled the forecourt, with a 64.17% share in 2025, because fueling infrastructure spans both urban and rural corridors. Battery-electric cars, though starting from a tiny base, notched a head-turning 20.29% CAGR as import duty waivers sharpened price competitiveness and early adopters embraced low running costs. Diesel retains a foothold in haulage fleets but faces tightening emissions fees that erode its traditional cost advantage. Hybrids bridge range anxiety with regenerative braking and switchable powertrains, making them a practical compromise for stop-and-go city driving. Collectively, these shifts hint at an eventual pivot away from sole reliance on petrol.

The expansion of CNG stations from 3 to 13 sites, combined with cheaper kit conversions, is persuading ride-hail operators to trial gas for predictable urban loops. Workshops in Dar es Salaam have begun stocking high-pressure cylinders, signaling supply-chain readiness for larger fleet transitions. Policy makers reinforce momentum by reiterating the 2050 all-gas mobility target, a long horizon that still shapes dealership stocking decisions today. Nevertheless, nationwide electricity reliability and the scarcity of charging points keep most private buyers anchored to petrol in the near term. The coming years will therefore feature a gradual fuel-mix rebalancing rather than an abrupt leap.

By Vehicle Age: Freshness Commands a Premium

Cars aged 3 to 5 years accounted for 38.29% of the 2025 market, hitting the affordability-versus-reliability sweet spot for middle-income households. Fresh enough to offer airbags and modern infotainment, these units also qualify for favorable insurance rates, lowering the total cost of ownership. Rising aspirations pushed sales of 0- to 2-year-old models to become the fastest-growing segment, with a 10.35% CAGR, as flexible financing softened sticker shock for tech-hungry younger professionals. Imports older than eight years now attract a steeper excise penalty, shrinking their price edge and reinforcing the drift toward newer inventory. Dealers capitalize by bundling extended-service contracts that reassure buyers chasing longer ownership cycles.

Digital odometer checks available through mobile apps reduce mileage fraud fears that historically plagued older stock, prompting shoppers to pay a discernible premium for verified kilometres. Organised yards prominently display complete maintenance histories, which amplifies trust and accelerates turnover among fresher cohorts. Meanwhile, street vendors witness longer dwell times on aging units as consumers grow skeptical of undisclosed repairs. Lending institutions echo the market mood by offering lower interest rates on vehicles manufactured after 2021, citing stronger collateral values. These intertwined incentives steadily improve average vehicle quality in the Tanzania used-car market.

By Price Segment: Budget Floor, Premium Ceiling

Vehicles priced below USD 5,000 captured 44.29% share in 2025, firmly reflecting the income ceiling for a large slice of first-time buyers. Shoppers in this band prize basic functionality over cosmetic perfection, accepting higher mileage as long as engines remain mechanically sound. Mid-range brackets up to USD 15,000 attract civil servants and SME owners eager for air conditioning, automatic gearboxes, and factory infotainment without venturing into luxury territory. The USD 20,000-to-29,999 tier posted the fastest growth rate of 11.16%, as salaried professionals upgraded to image and safety features, helped by employer-guaranteed loans. Each rung on the ladder, therefore, reflects a distinct lifestyle statement and a financing threshold.

Currency volatility occasionally inflates CIF costs, trimming model options in the upper tiers, yet sustained GDP growth keeps aspirational demand alive. Dealers hedge by quoting prices in weekly-updated shilling equivalents, cushioning sticker shock when the local currency weakens. Mobile-money credit products split down payments into bite-sized tranches, encouraging households to reach for higher trims earlier in their earning cycles. Social media testimonials from peer buyers legitimize spending beyond the entry level, fostering positive feedback loops.

By Sales Channel: Online Edge Widens

Online marketplaces secured 54.78% of revenue share in 2025 and post an 11.57% CAGR to 2031, an outcome driven by smartphone penetration, search filters, and escrow-style payment features that minimize fraud. High-resolution images and walk-around videos compress multiple lot visits into an evening’s scrolling, saving shoppers time and transport fares. Pure-play e-retailers fine-tune pages for low-bandwidth areas, letting rural buyers participate without desktop computers. Ratings and review systems surface trustworthy sellers, gradually sidelining opaque one-time listings. These user-experience gains cement digital channels as the default discovery point for Tanzania’s urban youth.

Physical yards still matter for test drives and final paperwork, so many dealers adopt hybrid approaches that meld QR-coded window stickers with chat-enabled web catalogs. Auction houses livestream gavel drops, widening bidder pools beyond Dar es Salaam and normalizing remote participation norms. Manufacturers dabble in certified-used micro-sites, promising roadside assistance and genuine parts to reduce perceived risk. Banks integrate loan calculators directly into listing pages, turning browsing into near-instant credit approval journeys. The result is an increasingly omnichannel landscape where digital convenience and physical reassurance reinforce rather than cannibalize each other.

By Ownership: Provenance Shapes Perceived Value

Multi-owner cars held a commanding 68.85% share in 2025 because their softer resale values put keys within reach of budget-constrained households. Buyers accept a few cosmetic blemishes so long as core mechanicals remain intact, viewing trade-offs as rational compromises. First-owner resales grew at a healthy 9.33% CAGR, buoyed by lenders that prefer clean ownership trails and by organised dealers that package limited warranties. Extended coverage alleviates latent worries about hidden accidents, making premium pricing more palatable to upwardly mobile consumers. Over time, this shift injects a quality gradient into the ownership spectrum that did not previously exist.

Greater data transparency is steadily eroding the information asymmetry that once protected steep discounts for multi-owner units. Mobile-app VIN look-ups now expose service gaps and insurance claims, allowing shoppers to quantify rather than guess at risk. As certainty improves, the historical gap between first- and multi-owner pricing is expected to narrow, realigning value with verifiable condition instead of anecdotal assurances. Dealers specializing in single-owner imports respond by marketing mileage guarantees and buy-back promises, reinforcing trust loops. Such dynamics gradually recalibrate consumer hierarchies in the Tanzania used-car market while preserving affordability at the base.

Geography Analysis

Dar es Salaam anchors the Tanzania used car market because the port funnels nearly all maritime imports, and the roads provide immediate access to dense consumer clusters. Dealers there enjoy shorter lead times from vessel discharge to showroom display, translating into fresher inventory. Extensive bus rapid transit lanes help residents expand their commuting zones, increasing overall car usage. Local banks also cluster their headquarters in the city, speeding credit processing for retail buyers. Consequently, the coastal capital remains the bellwether for nationwide demand shifts.

Secondary cities such as Arusha and Mwanza are showing stronger momentum as tourism, mining, and agribusiness incomes diversify regional economies. Improved trunk roads reduce haulage costs, letting dealers redistribute stock without prohibitive mark-ups. Consumers in these areas still value physical inspection, so hybrid retail models that combine online lead generation with pop-up lots emerge quickly. Mobile money ubiquity compensates for lighter branch-bank footprints, enabling on-the-spot down payments. Over time, balanced geographic diffusion should soften the historical concentration evident in the Tanzania used-car market.

Rural districts gradually join the customer base thanks to ongoing electrification projects that stimulate micro-enterprise growth. When small shops expand earnings, owners often upgrade from motorcycles to compact cars capable of reaching regional markets. Community savings groups coordinate bulk purchases from city dealers and arrange shared transport to drive units home in convoys. Although volumes remain small in absolute terms, such grassroots demand seeds future penetration. As logistics corridors like the Standard Gauge Railway mature, even remote regions will have access to inventory with fewer intermediaries, widening the physical footprint of the Tanzania used-car market.

Mordor Intelligence provides coverage of the used car market across other key regional markets, including Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Egypt, Ethiopia, Hong Kong, Finland, New Zealand, Norway, Myanmar, and Switzerland incorporating local coverage and market participation, as required.

Competitive Landscape

The competitive field, moderately concentrated, features international exporters such as Be Forward and SBT Japan that leverage scale advantages in sourcing, shipping, and after-sales parts. Their branded yards assure buyers of predictable quality and facilitate financing through partnered banks. Local platform Jiji stakes its pitch on sheer listing volume and aggressive marketing, positioning it as the default search engine for second-hand cars. Specialist fintechs like Laina Finance provide real-time loan approvals, smooth checkout flows, and strengthen customer loyalty. These intertwined services create ecosystem stickiness that smaller vendors struggle to replicate.

Street-corner dealers nonetheless persist by cultivating personal rapport, offering installment plans tailored to informal cash cycles, and accepting trade-ins that global exporters often reject—some form of loose cooperatives to jointly import containers, lowering per-unit freight costs and expanding model variety. Repair garages occasionally double as micro-dealerships, bundling mechanical reassurance for community customers. Competition thus evolves not solely on price but also on neighborhood convenience and perceived honesty. Fragmentation remains pronounced, though digital tools are slowly elevating baseline professionalism.

Strategic consolidation shapes the formal tier, exemplified by Exim Bank’s acquisition of Canara Bank Tanzania, which bolsters the credit pipeline for franchised showrooms. Technology adoption further separates leaders from laggards; AI-driven valuation engines reduce appraisal errors and speed trade-in negotiations, giving organised players an operational edge. Partnerships with insurance firms deliver bundled covers that simplify compliance for first-time owners. Meanwhile, policy incentives for cleaner vehicles prompt top dealers to pilot dedicated EV sections, signaling adaptability. Collectively, these moves maintain moderate industry concentration while leaving ample room for innovative entrants in the Tanzania used-car market.

Tanzania Used Car Industry Leaders

-

SBT Japan

-

Be Forward

-

CarTanzania

-

UsedCars.co.tz

-

Jiji

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Karimjee Mobility introduced Auto Inc., a nationwide chain of professional service stations for both new and used vehicles.

- June 2024: Absa Bank Tanzania introduced Vehicle Asset Finance (VAF), offering medium-term financing to help Tanzanians purchase new or used vehicles without full upfront payment, enhancing affordability and accessibility.

- January 2024: AUTO24.africa, a certified used car marketplace under the Africar Group and backed by Stellantis, bolsters its foothold in Africa by acquiring Kupatana, Tanzania's premier online classifieds platform.

Tanzania Used Car Market Report Scope

A used car/pre-owned vehicle, or secondhand car, is a vehicle that has had one or more retail owners. A certified pre-owned (CPO) vehicle, on the other hand, is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned. The Used Car Market comprises a wide range of companies that purchase and sell pre-owned vehicles through online and offline sales channels.

The Tanzania Used Car Market is segmented by vehicle type, vendor type, fuel type, vehicle age, price segment, sales channel, and ownership. The Tanzania Used Car Market is segmented by vehicle type, vendor type, fuel type, vehicle age, price segment, sales channel, and ownership. By Vehicle Type, the market is segmented into Hatchbacks, Sedans, Sport-Utility Vehicles (SUVs), and Multi-Purpose Vehicles (MPVs). By Vendor Type, the market is segmented into Organised and Unorganised. By Fuel Type, the market is segmented into Petrol, Diesel, Hybrid (HEV and PHEV), Battery-Electric (BEV), and LPG / CNG / Others. By Vehicle Age, the market is segmented into 0 to 2 Years, 3 to 5 Years, 6 to 8 Years, 9 to 12 Years, and Over 12 Years. By Price Segment, the market is segmented into Below USD 5,000, USD 5,000 to 9,999, USD 10,000 to 14,999, USD 15,000 to 19,999, USD 20,000 to 29,999, and USD 30,000 and Above. By Sales Channel, the market is segmented into Online (Digital Classifieds, Pure-play e-Retailers, and OEM-Certified Platforms) and Offline (OEM-Franchised Dealers, Multi-brand Dealers, and Physical Auctions). By Ownership, the market is segmented into First-owner Resale and Multi-owner. The report provides market size and forecast by value (USD) and volume (units) for all the above segments.

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Organised |

| Unorganised |

| Petrol |

| Diesel |

| Hybrid (HEV and PHEV) |

| Battery-Electric (BEV) |

| LPG / CNG / Others |

| 0 to 2 Years |

| 3 to 5 Years |

| 6 to 8 Years |

| 9 to 12 Years |

| Over 12 Years |

| Below USD 5,000 |

| USD 5,000 to 9,999 |

| USD 10,000 to 14,999 |

| USD 15,000 to 19,999 |

| USD 20,000 to 29,999 |

| USD 30,000 and Above |

| Online | Digital Classified Portals |

| Pure-play e-Retailers | |

| OEM-Certified Online Stores | |

| Offline | OEM-Franchised Dealers |

| Multi-brand Independent Dealers | |

| Physical Auction Houses |

| First-owner Resale |

| Multi-owner |

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| Sport-Utility Vehicles (SUVs) | ||

| Multi-Purpose Vehicles (MPVs) | ||

| By Vendor Type | Organised | |

| Unorganised | ||

| By Fuel Type | Petrol | |

| Diesel | ||

| Hybrid (HEV and PHEV) | ||

| Battery-Electric (BEV) | ||

| LPG / CNG / Others | ||

| By Vehicle Age | 0 to 2 Years | |

| 3 to 5 Years | ||

| 6 to 8 Years | ||

| 9 to 12 Years | ||

| Over 12 Years | ||

| By Price Segment | Below USD 5,000 | |

| USD 5,000 to 9,999 | ||

| USD 10,000 to 14,999 | ||

| USD 15,000 to 19,999 | ||

| USD 20,000 to 29,999 | ||

| USD 30,000 and Above | ||

| By Sales Channel | Online | Digital Classified Portals |

| Pure-play e-Retailers | ||

| OEM-Certified Online Stores | ||

| Offline | OEM-Franchised Dealers | |

| Multi-brand Independent Dealers | ||

| Physical Auction Houses | ||

| By Ownership | First-owner Resale | |

| Multi-owner | ||

Key Questions Answered in the Report

How fast is the Tanzania used car market expected to grow through 2031?

It is projected to register a 7.35% CAGR between 2026 and 2031.

Which vehicle type sells the most in Tanzania’s pre-owned segment?

Hatchbacks account for nearly half of all units sold, reflecting urban driving needs.

Why are online platforms gaining ground in Tanzania?

Mobile-first classifieds integrate payments, financing, and rich listings that streamline the buying process for smartphone users.

What policy incentives support electric vehicles in Tanzania?

The 2024 finance act set import duty at 0% for unassembled hybrids and waived excise tax on EVs and CNG vehicles.

How does currency volatility impact used-car prices?

Shilling depreciation against the Japanese yen and US dollar raises import costs, which often translate into higher retail prices.

Page last updated on: