Capacitive Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.43 Billion |

| Market Size (2031) | USD 43.41 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Capacitive Sensors Market Analysis by Mordor Intelligence

The capacitive sensor market size was valued at USD 32.87 billion in 2025 and estimated to grow from USD 34.43 billion in 2026 to reach USD 43.41 billion by 2031, at a CAGR of 4.74% during the forecast period (2026-2031). The expansion of the capacitive sensor market is supported by rising demand for touch-based user interfaces, growing integration of contactless controls in regulated environments, and sustained cost reductions in semiconductor fabrication. Product designers now bundle capacitive sensing with haptic feedback, biometric monitoring, and self-calibrating software, which broadens application scope from mobile handsets to automotive dashboards and surgical equipment. The capacitive sensor market also benefits from its inherent durability because the technology detects changes in electric fields without mechanical wear, making it well-suited for high-cycle industrial automation systems. Persistent constraints surrounding indium tin oxide supply are nudging manufacturers toward polymer and silver-nanowire conductors, but the transition is expected to be orderly as new materials mature.

Key Report Takeaways

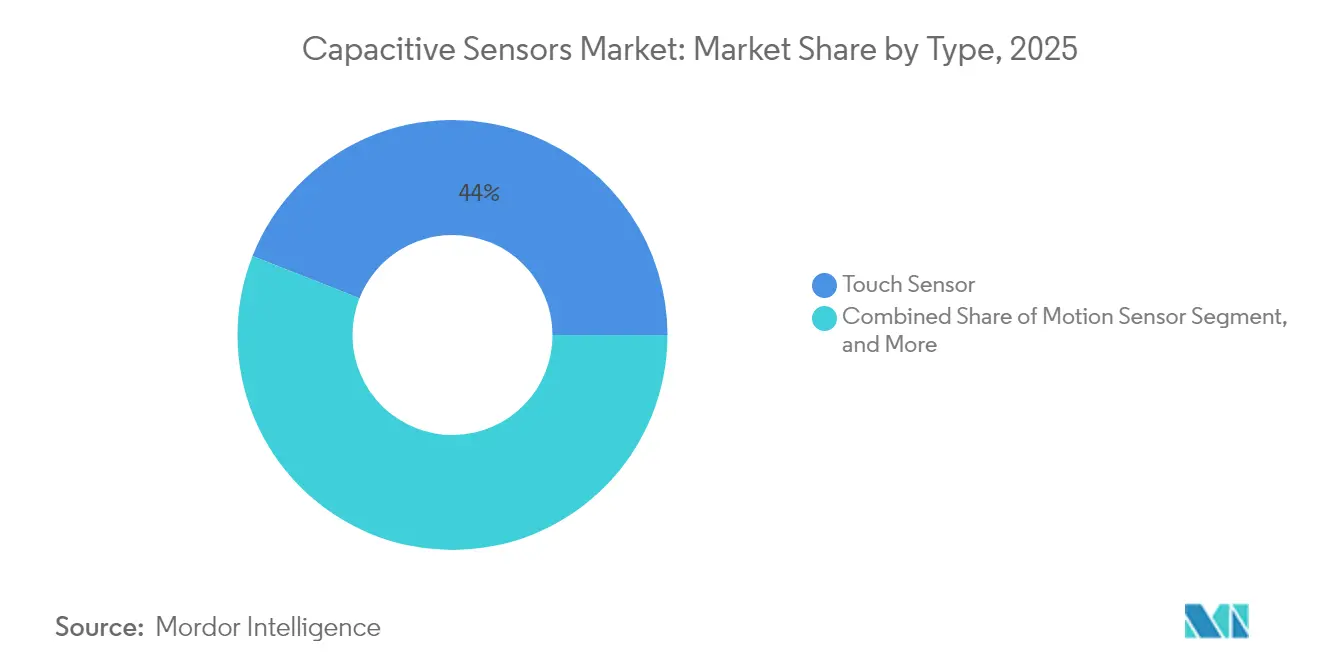

- By type, touch sensors led with a 44.02% share of the capacitive sensor market in 2025, while proximity sensors recorded the fastest 5.03% CAGR through 2031.

- By end-user industry, consumer electronics accounted for 40.35% of the capacitive sensor market size in 2025, and the healthcare sector is projected to advance at a 4.82% CAGR from 2025 to 2031.

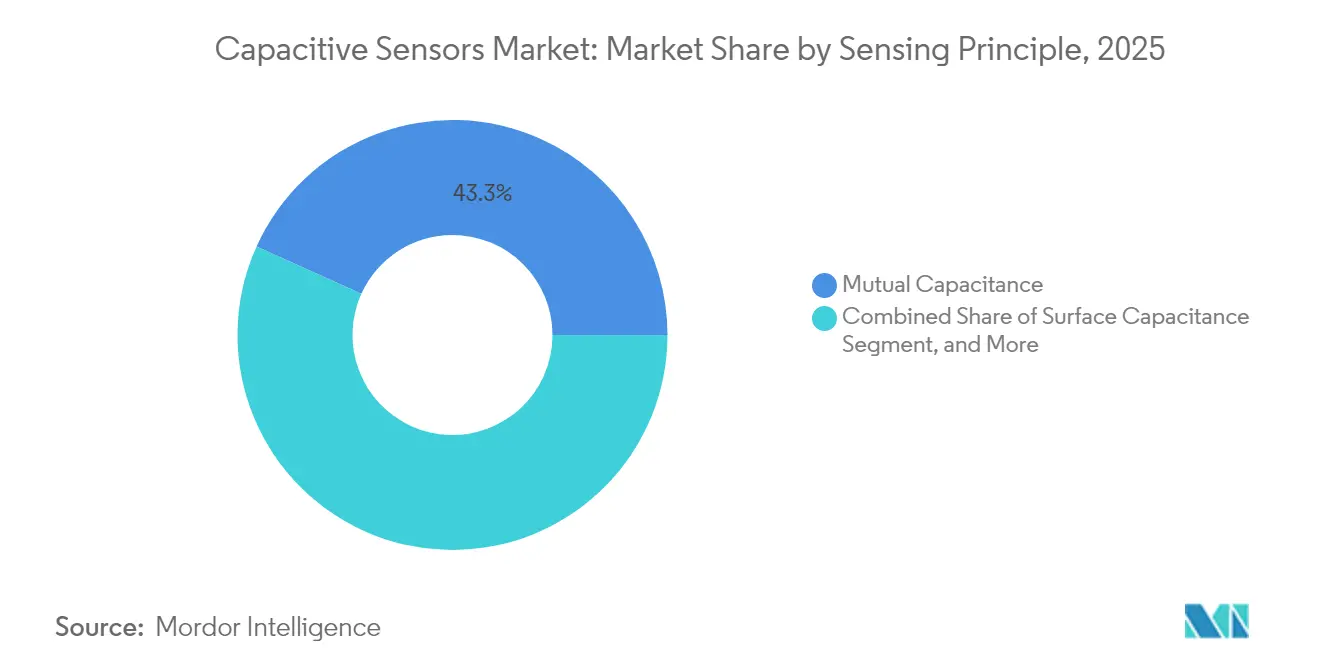

- By sensing principle, mutual capacitance captured 43.25% revenue share in 2025; projected capacitance is forecast to expand at a 5.44% CAGR to 2031.

- By form factor, surface-mount devices held a 47.62% share of the capacitive sensor market size in 2025, whereas flexible and thin-film sensors are expected to exhibit a 5.55% CAGR between 2026 and 2031.

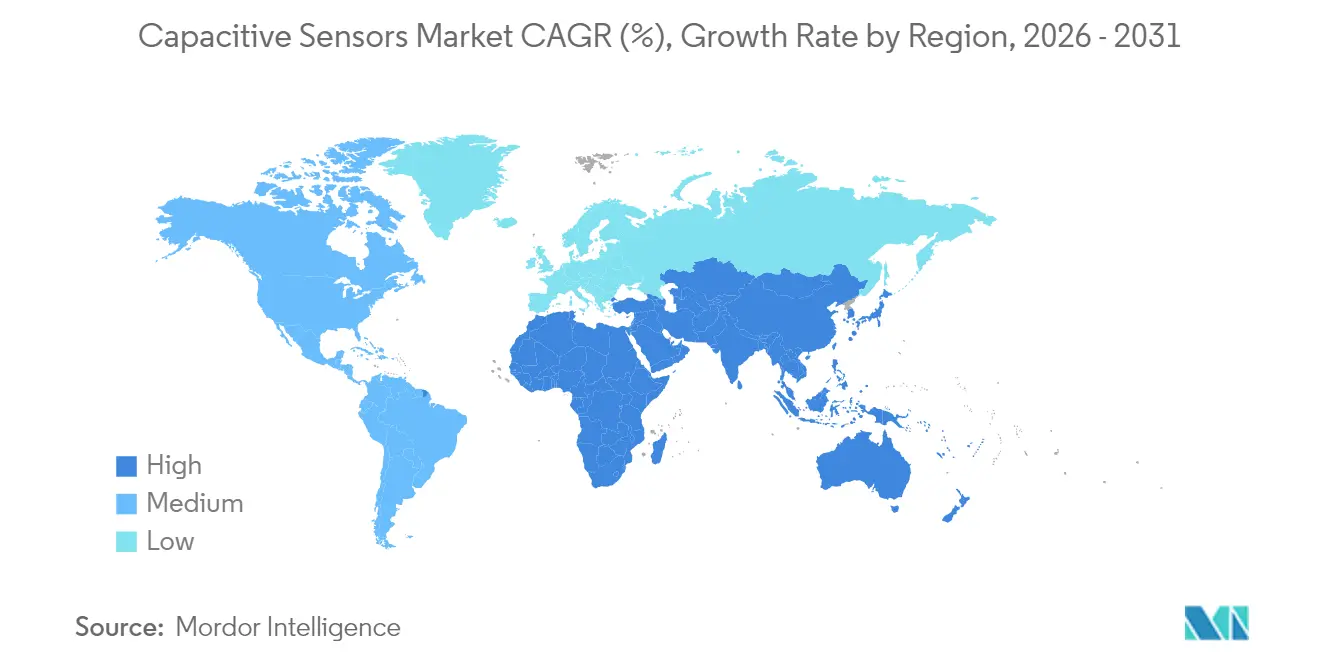

- By Geography, the Asia-Pacific region commanded 39.05% of global revenue in 2025, and the Middle East is poised for the fastest growth, with a 4.98% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Capacitive Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Capacitive Touch Screens in Consumer Electronics | +1.2% | Global, Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Increasing Integration of Capacitive Sensors in Automotive Human Machine Interfaces | +0.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising Demand for Industrial Automation and Robotics | +0.7% | Global, early adoption in Germany, Japan, China | Medium term (2-4 years) |

| Growth of Wearable and IoT Devices Requiring Low Power Capacitive Sensing | +0.9% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Emergence of Transparent Conductive Polymers as Alternative to Indium Tin Oxide | +0.4% | Global, R and D in North America and Europe | Long term (≥ 4 years) |

| Regulatory Push for Hygienic Contactless Interfaces in Food Processing and Healthcare | +0.6% | Global, stringent in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Capacitive Touch Screens in Consumer Electronics

Smartphone, tablet, and wearable device makers continue to replace resistive technologies with advanced mutual and projected capacitance. Flexible OLED production lines commissioned by Samsung in 2024 integrate projected capacitance to enable foldable displays that maintain uniform sensitivity across bending radii.[1]Samsung Electronics, “Annual Report 2024,” Samsung.com Automakers embrace the same architectures for infotainment units, steering-wheel controls, and augmented-reality head-up displays. These design choices enhance the average capacitive sensor content per vehicle, fostering volume economies that extend to industrial machinery and white goods. Meanwhile, haptic drivers embedded beneath glass enable tactile confirmation on flat surfaces, reducing accidental activations and improving accessibility for visually impaired users. Vendors are therefore prioritizing firmware toolkits that allow OEMs to fine-tune latency, set thresholds, and implement multi-finger gestures without requiring new hardware spins.

Increasing Integration of Capacitive Sensors in Automotive Human-Machine Interfaces

Euro NCAP safety protocols, updated in 2024, evaluate steering-wheel grip sensors that track driver attention through capacitive channels, driving tier-one suppliers to certify automotive-grade controllers to AEC-Q100 standards. Tesla and BMW have demonstrated that capacitive sensor arrays can reliably detect hands-on-wheel conditions, even when operators wear gloves a critical feature for Level 2+ autonomy. Capacitive surfaces are also appearing on exterior charge-port doors and interior ambient-lighting sliders, replacing mechanical switches that are susceptible to dust ingress. Because automotive EMI levels rise with electrified powertrains, suppliers now bundle differential sensing and spread-spectrum modulation to maintain immunity. Long product life cycles in the sector lock in multiyear revenue streams for qualified sensor ICs, giving automotive integrations an outsized strategic impact on the capacitive sensor market.

Rising Demand for Industrial Automation and Robotics

Capacitive proximity sensors enable collaborative robots to detect human presence at distances of up to 30 cm, allowing for safe operation without mechanical bumpers. Food processing lines appreciate the sealed, flush-mount form factors that tolerate wash-down environments, where optical sensors often fail due to steam or splashes. [2]Siemens AG, “Industrial Automation Report 2024,” Siemens.com Machine-tool OEMs utilize sub-micrometer position sensors based on capacitive technology to regulate spindle displacement, thereby enhancing yield in semiconductor lithography equipment. The adoption coincides with Industry 4.0 rollouts that require sensors to stream health metrics such as dielectric drift, which predictive-maintenance platforms convert into service alerts. These capabilities reduce unscheduled downtime, justifying premium pricing and reinforcing the value proposition of the capacitive sensor market in factory settings.

Growth of Wearable and IoT Devices Requiring Low Power Capacitive Sensing

Fitness trackers and smart rings embed capacitive electrodes that measure bioelectrical impedance for body-composition analytics, while consuming less than 10 µA in standby mode, according to. Smart clothing incorporates textile-based capacitive yarns that conform to body movement and withstand repeated washing cycles. In smart buildings, ceiling-mounted capacitive occupancy sensors detect presence without capturing images, addressing privacy concerns associated with cameras. Ultra-low-power modes combined with energy harvesting from indoor lighting extend coin-cell battery life to multiple years, accelerating IoT deployments in retail shelving and security panels. Vendors compete on algorithms that suppress drift caused by humidity and temperature, ensuring stable baselines in unconditioned spaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply shortage and price volatility of indium tin oxide | -0.8% | Global, acute in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Sensitivity to electromagnetic interference in industrial sites | -0.5% | Global, heavy industrial regions | Medium term (2-4 years) |

| Patent thickets and licensing costs for multi-touch algorithms | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Higher cost and complexity of alternative transparent conductors | -0.4% | Global, R and D centered in North America Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Shortage and Price Volatility of Indium Tin Oxide

Indium prices fluctuated by more than 40% in 2024 as mining operations in China and South Korea were disrupted by supply chain issues amid geopolitical tensions. Display manufacturers competing for the same metal exacerbated scarcity, forcing sensor vendors to lengthen lead times and carry higher inventories. Polymer conductors and silver nanowires offer potential relief but remain expensive to scale for high-volume touchscreen overlays. [3]Nature Materials, “Alternative Transparent Conductors for Flexible Electronics,” Nature.com Some OEMs redesigned user interfaces to reduce transparent conductor area, but such compromises limit gesture zones and brand differentiation. Strategic stockpiling and multi-sourcing contracts are, therefore, temporary stopgaps until alternative materials mature.

Sensitivity to Electromagnetic Interference in Industrial Environments

Arc welders, variable-frequency drives, and radio transceivers create fields exceeding 10 V/m, which can induce parasitic charges on capacitive electrodes. Without adequate shielding, controllers misinterpret noise as touches, triggering unplanned machine stops that cost manufacturers thousands of USD per minute. Differential electrode pairs, guard rings, and frequency hopping increase robustness but add bill-of-materials costs and larger board footprints. For electric vehicles, DC-DC converters and high-current busbars generate wideband emissions that require meticulous grounding strategies around cabin control units. Regulatory bodies have yet to standardize EMI benchmarks for capacitive interfaces, leaving OEMs to balance cost, reliability, and certification risk on a case-by-case basis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Touch Sensors Maintain Leadership as Proximity Adoption Accelerates

The touch-sensor subsegment retained a 44.02% revenue share within the capacitive sensor market in 2025, thanks to entrenched demand for smartphones and tablets, combined with rising installations in countertop appliances. This dominance provides stable volumes that drive wafer-level cost declines, permitting touch ICs to enter price-sensitive markets such as education tablets and entry-level cars. Touch sensors also proliferate in medical-grade monitors that must withstand chemical sterilization, where glass or polymer overlays protect electrodes without compromising accuracy. Meanwhile, developers enrich firmware with palm-rejection logic to minimize ghost touches on large panels used in conference systems.

Proximity sensors exhibit the swiftest momentum, expanding at a 5.03% CAGR to 2031 as contactless elevator panels and hospital room controls become standard. The subsegment leverages capacitive fields to detect objects through non-conductive layers, enabling liquid-level monitoring in pharmaceutical vessels where optical probes cloud over. Emerging packaging lines integrate proximity arrays around fillers to halt operation if an operator’s arm breaches safety envelopes, improving compliance with ISO 13849. Motion and position sensors, although smaller in unit volume, find profitable niches in virtual-reality controllers and precision robotics, where bidirectional resolution of under 5 µm commands margins exceed 30%.

By End-User Industry: Consumer Electronics Dominates while Healthcare Gains Momentum

Consumer electronics accounted for 40.35% of the capacitive sensor market in 2025, anchored by mobile phones that package up to five separate capacitive solutions for display input, side-key replacement, and camera AF modules. Growth is plateauing in saturated geographies, but new form factors, such as foldables and rollables, refresh replacement cycles. Gaming consoles utilize large surface capacitive panels for motion tracking, sustaining mid-single-digit growth.

Healthcare registers the highest forward trajectory at 4.82% CAGR. Regulatory frameworks that emerged in response to the COVID-19 crisis mandate touchless or wipe-friendly user interfaces for ventilators, patient terminals, and laboratory equipment. Capacitive buttons sealed under PET films meet IP67 standards, allowing for aggressive disinfection without mechanical degradation. Hospitals also deploy capacitive hand-gesture panels outside intensive-care rooms to reduce pathogen transfer. Automotive retains its historical importance, with electric cars adding capacitive charge-port lids and seat-occupancy detection, while aerospace seeks radiation-hardened parts for cockpit modernization programs.

By Sensing Principle: Mutual Capacitance Leads while Projected Capacitance Climbs

Mutual capacitance accounted for 43.25% of the capacitive sensor market size in 2025, owing to its multi-touch capability and inherent noise suppression. Two-dimensional matrices fabricated on indium tin oxide or silver nanowires register ten-finger input with sub-2 mm spacing, a requirement for professional graphics tablets and digital signage kiosks. Industrial HMIs utilize mutual capacitance, as differential electrodes effectively cancel out common-mode noise from motors.

Projected capacitance is the fastest riser, with a 5.44% CAGR. Because electrodes reside behind thicker glass, projected designs tolerate gloves and harsh cleansers, making them ideal for medical carts and outdoor payment terminals. Vendors now utilize dynamic active-guard algorithms that adjust excitation voltage to compensate for humidity drift, thereby extending deployment into cold-chain logistics, where condensation persists. Self-capacitance remains the lowest-cost approach where single-touch suffices, such as capacitive-switch replacement in appliances. Surface capacitance, although niche, persists in public ticketing kiosks, where vandal-resistant 6-mm glass is the dominant material.

By Form Factor: Surface-Mount Devices Prevail while Flexible Sensors Unlock Curved Designs

Surface-mount capacitive ICs accounted for 47.62% of the capacitive sensor market revenue in 2025, as they align with standard pick-and-place lines, enabling OEMs to integrate sensing capabilities without requiring dedicated tooling. Board-level consolidations now merge microcontroller and capacitive channels onto single packages, reducing component count and enhancing electromagnetic compatibility. Through-hole sensors, although declining, remain in high-power drives where pin strength enhances reliability during conformal coating processes.

Flexible and thin-film sensors are projected to earn a 5.55% CAGR through 2031. Roll-to-roll printed electrodes on PET and polyimide support achieve bend radii below 2 mm, making them suitable for smartwatch straps and automotive interior trim. Smart packaging inserts detect tamper events and record cumulative temperature exposure via printed capacitive arrays coupled with NFC (Near Field Communication) chips. Embedded IC sensors, which co-locate analog front-ends with microelectromechanical relays on a single silicon chip, open avenues for implantable medical devices where board real estate is scarce and reliability is paramount.

Geography Analysis

Asia-Pacific retained 39.05% of global revenue in 2025, anchored by China’s vertically integrated display and smartphone supply chains. South Korea’s panel makers scale up foldable OLED production, driving localized demand for projected-capacitance controllers, while Taiwan’s EMS providers secure strategic wafer allocations to support the notebook rebound. India’s incentives for semiconductor packaging have attracted multinational IDMs to establish bumping and test capacity, opening pathways for domestic appliance brands to adopt local sensor ICs. Japan’s robotics sector remains a premium buyer of high-accuracy position sensors, especially for semiconductor lithography stages where sub-micron control is compulsory.

North America demonstrates steady adoption across the automotive, aerospace, and medical electronics sectors. U.S. electric-vehicle makers specify steering-wheel touch sensors that resist EMI bursts generated during 800-V fast charging, fostering collaboration between Detroit's tier-one automakers and Silicon Valley startups. Canadian medical device firms are embracing projected capacitance to meet no-gap cleaning regulations for dental equipment. Europe parallels North America in maturity but channels sustainability mandates-such as circular-economy rules-into a demand for reparable capacitive panels rather than glued-in resistive touch films.

The Middle East is expected to record the fastest 4.98% CAGR through 2031. Smart-city programs in the United Arab Emirates integrate capacitive occupancy sensors within lighting poles to modulate energy consumption during periods of low traffic. Saudi Arabia’s Vision 2030 industrial zones are outfitting packaging and bottling lines with hygienic, touchless controls. South America grows moderately as Brazilian automotive plants upgrade to capacitive charge-port lids for domestic electric vehicle launches. Africa remains nascent, but fintech kiosks in Nigeria demonstrate early demand for robust touch surfaces that can withstand dust and high humidity.

Regulatory Landscape

Capacitive sensors are subject to product safety, functional safety, and electromagnetic and radio compliance requirements, which vary by end-use. In industrial automation and machinery safety applications, suppliers and OEMs typically align design and validation to ISO 13849 performance levels. For automotive HMI and touch or proximity functions that affect driver interaction, designs are carried out under ISO 26262 processes for ASIL-oriented safety cases.

Market access and conformity obligations continue to tighten by geography. In India, the Ministry of Heavy Industries mandated BIS certification for proximity switches (including capacitive sensor-based proximity devices) under IS/IEC 60947-5-2:2019, effective 10 May 2025, which increases compliance and documentation needs for imports and local supply. On the standards side, IEC published IEC 60730-2-23:2025 to set particular requirements for electrical sensors and sensing elements used in automatic electrical controls, shaping how appliance and building-automation designs specify and qualify sensor subsystems.

Value Chain Analysis

The capacitive sensor value chain begins with electrode and controller IC architecture, followed by semiconductor fabrication and packaging. It then moves into electrode or overlay material preparation (including ITO-coated glass and alternatives such as polymers, silver nanowires, or metal mesh), and finishes with module integration and end-product assembly. For high-volume touch and projected-capacitance use, production is typically split between IC design and fabrication in major Asian hubs, especially Taiwan and South Korea, specialty glass and material supply across Japan and China, and module assembly and device integration in China, Vietnam, and India, before distribution through OEM and EMS channels.

Most constraints cluster in three areas: leading-edge, noise-immune controller IC capacity (where allocations can limit deliveries); coated transparent-conductor supply, where coating-line expansions take longer to come through; and firmware and algorithm engineering for multi-touch performance, wet-touch robustness, and EMI resilience. Automotive and industrial buyers are also tightening procurement by qualifying integrated display or HMI modules (touch, display, bonding, and haptics together), while requiring dual-sourcing for critical substrates and conductor materials to reduce exposure to indium tin oxide volatility and single-source risk.

Competitive Landscape

The capacitive sensor market exhibits moderate fragmentation, with the top five suppliers accounting for nearly 55% of global shipments. Texas Instruments, STMicroelectronics, and Analog Devices leverage long-term wafer agreements and mixed-signal design expertise to package analog front-ends, digital signal processors, and LIN/CAN transceivers on a single die, thereby reducing the client's bill of materials. STMicroelectronics earmarked USD 2.9 billion for a Grenoble fab dedicated to 28-nm automotive-grade capacitive controllers, indicating strategic focus on electric-vehicle demand.

Synaptics and Cirque build differentiation on firmware by offering multi-finger gesture libraries and neural-net-based palm detection, commanding licensing fees that reach 8% of the sensor's average selling price. Patent filings in 2024 reveal a shift toward AI-augmented baseline tracking that compensates for moisture, sidestepping prior license bottlenecks. Emerging firms like Canatu and NextInput target flexible and force-sensing niches, leveraging carbon-nanotube electrodes or MEMS strain gauges layered with capacitive arrays.

Supply-chain resilience has become a core strategy. Analog Devices partnered with BMW to integrate leak-detection capacitance into battery packs, tying sensor sales to high-margin powertrain electronics. Meanwhile, Texas Instruments expanded its presence with the USD 1.8 billion purchase of Nuvoton’s capacitive sensing division, securing intellectual property for EMI suppression and gaining a Taiwanese fab that hedges geopolitical risk. Overall, competition now revolves around application-specific certifications ISO 26262, FDA Class II, or ATEX Zone 0, rather than pure pixel density, creating barriers for late entrants.

Capacitive Sensors Industry Leaders

Texas Instruments Incorporated

STMicroelectronics N.V.

Analog Devices Inc.

Microchip Technology Inc.

Omron Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Material transitions and signal-processing upgrades are creating whitespace where legacy ITO-based designs struggle, especially in large-format industrial HMIs and harsh environments. Industrial projected-capacitive (PCAP) roadmaps increasingly point to metal mesh conductors and edge-processing on PCAP controllers to improve durability, reduce costs at scale, and better reject interference from water and EMI. This is supporting deployments in factory interfaces, outdoor terminals, and regulated cleanable surfaces. The need to operate reliably around high EMI sources also creates opportunity for suppliers that can combine controller design, shielding strategies, and firmware toolchains into validated reference designs for industrial and automotive programs.

Outside consumer electronics, automation-heavy industries are adopting sensor-centric architectures that broaden addressable use cases for proximity, level, and touchless control. In mineral processing, Mineral Technologies launched the mtOne spiral automation platform in February 2026, using smart sensors for real-time control, which illustrates sensing layers being embedded into closed-loop process automation rather than used only for measurement. On the technology frontier, 2026 academic work on flexible, porous-structured capacitive pressure sensors and laser-induced graphene based designs points to a pipeline for soft-robotics and wearable interfaces where traditional rigid sensor stacks underperform, supporting continued emphasis on flexible or thin-film capacitive formats and application-specific firmware.

Recent Industry Developments

- July 2026: Ferreyros deployed Peru's first autonomous CAT R1600H underground loader fleet for Volcan, using Caterpillar MineStar Command technology with sensor-driven automation. The deployment shows how sensor-based control and monitoring are being implemented in harsh industrial environments, supporting demand for robust proximity and interface sensing within automation stacks.

- November 2025: STMicroelectronics introduced the ISM6HG256X three-in-one motion sensor for industrial IoT, combining simultaneous low-g and high-g acceleration sensing with a high-performance gyroscope. The launch strengthens industrial sensing portfolios that are increasingly paired with capacitive interfaces in connected equipment and robotics designs.

- July 2024: Euro NCAP updated 2024 safety evaluation protocols to include assessment of steering-wheel grip monitoring functions that can be implemented using capacitive sensing channels. The change increased design and validation focus on automotive-grade touch and proximity sensing in driver interaction systems and pushed suppliers toward automotive qualification and functional-safety aligned development flows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from capacitive sensors that detect changes in capacitance to sense touch, proximity, motion, or position across electronics, vehicles, industrial equipment, and other end uses, and it is measured in USD on a global basis.

Scope exclusions: This sizing excludes downstream finished devices value and services, and it counts only the sensor and related sensing component revenue rather than the full system cost.

Segmentation Overview

- By Type

- Touch Sensor

- Motion Sensor

- Position Sensor

- Proximity Sensor

- Other Types

- By End-User Industry

- Consumer Electronics

- Automotive

- Aerospace and Defense

- Healthcare

- Food and Beverages

- Oil and Gas

- Industrial Machinery

- Other End-User Industry

- By Sensing Principle

- Self-Capacitance

- Mutual Capacitance

- Surface Capacitance

- Projected Capacitance

- By Form Factor

- Surface-Mount Sensors

- Through-Hole Sensors

- Flexible/Thin-Film Sensors

- Embedded IC Sensors

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market context and to anchor key demand indicators that a capacitive sensor model needs. We reviewed public manufacturing and trade signals, along with device and vehicle production series, to identify where volumes are rising and where pricing pressure is visible.

Sources referenced include official statistics and releases such as the US Census Bureau and US International Trade Commission data, UN Comtrade for cross-country trade patterns, OECD industrial indicators, and standards and technical notes from bodies such as IEEE and IEC. We also used company filings and investor presentations to understand product mix, and we pulled reputable press and association sites for application trend direction. For company financials and patent tracking, we selectively used paid database subscriptions to cross-check timelines and technology focus. The sources listed here are illustrative only, and many other public references were also consulted for collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions helped us convert broad adoption stories into modeling inputs, especially for typical sensor content per device, pricing ranges, and how quickly newer form factors are being designed into products. We spoke with a mix of sensor ecosystem participants and demand-side stakeholders across major regions, then used follow-up questions to confirm assumptions that desk research could not fully explain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 44% |

| Mid tier: 40% | Functional/Unit leaders: 31% | EMEA: 30% |

| Smaller Players: 21% | Managers: 53% | Americas: 26% |

Market-Sizing & Forecasting

Our core model starts with a top-down build that reconstructs demand pools from end-market production and shipments, then applies capacitive sensor penetration and average content assumptions to convert those pools into sensor revenue. After the big picture is formed, we cross-check with selective bottom-up approximations such as sampled average selling price times estimated unit volume for common applications, plus channel checks to keep totals realistic.

The inputs include consumer device shipment trends for touch and proximity use, vehicle production and cockpit feature adoption for touch interfaces and position sensing, and industrial automation investment cycles for motion and control-related uses. We also track mix shifts across touch, motion, and position sensor use cases, since they can change both unit price and replacement cycles. Form factor adoption (for example, surface-mount versus flexible or thin-film) and technology mix (self-capacitance versus mutual and surface approaches) are explicitly reflected because these can move unit prices over time. When data is missing for smaller end-use pockets, we apply conservative proxy ratios from similar applications and then validate those ratios through primary expert feedback.

For forecasting, scenario analysis is used to translate macro signals into application-level growth paths, and the scenarios are then adjusted using expert consensus on pricing progression and adoption timing. The result is a forecast that can be explained on a client call, while still being driven by the specific levers that move capacitive sensor demand.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between model outputs and independent market signals, including end-market shipment series, trade direction, and observed pricing movement in common sensor categories. If a region or end-use result looks out of line, we revisit assumptions and trigger targeted follow-ups to re-check penetration, content per device, or the implied price trend.

Before sign-off, the model goes through multi-step analyst reviews that check for variance versus historical ranges and for internal consistency across regions and applications. Reports are refreshed annually, with interim updates made when material events affect demand, such as sharp shifts in device production, automotive build rates, or supply-chain pricing moves. Right before delivery, a final pass is completed so clients get the most current view available at that time.

Mordor Intelligence's Capacitive Sensors Market Size Measured Against Other Published Estimates

Published market values for capacitive sensors often differ because the scope and the timing of the estimate are not always aligned, even when the headline wording looks similar. These differences usually show up in what is counted as sensor revenue, the base year chosen, and how pricing is carried forward across the forecast.

Some sources fold a wider electronics component basket into the number, or they include adjacent touch module and subsystem value that sits above the sensor level. In Mordor Intelligence, the market is counted as capacitive sensor revenue only, and the sizing is aligned to a 2026 base value with technology and form-factor splits checked against real end-market production signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 34.43 B (2026) | |

| Global Consultancy A | USD 36.09 B (2025) | Uses a 2025 base year and appears to allow broader counting of touch and proximity related component value, which can lift the headline even if sensor unit volumes are similar. |

| Industry Publisher B | USD 29.30 B (2024) | Anchored on a 2024 base year with a different growth path and scope handling, which can pull the starting value down when pricing and higher-value applications are treated more conservatively. |

The spread across the three numbers is mostly explained by base-year choice and how strictly sensor-only revenue is separated from higher-level touch or interface hardware. By keeping the inputs tied to device and vehicle production indicators, and by re-checking pricing logic through interviews, our estimate stays traceable to clear levers that can be repeated and updated.

Key Questions Answered in the Report

What is the current value of the capacitive sensor market?

The capacitive sensor market size is USD 34.43 billion in 2026 and is projected to climb to USD 43.41 billion by 2031.

Which segment is growing fastest within capacitive sensing?

Proximity sensors show the fastest growth at a 5.03% CAGR through 2031, fueled by demand for touchless interfaces in healthcare and food processing.

How quickly are capacitive sensors adopted in vehicles?

Automotive human-machine interfaces integrate capacitive sensors at a rising 0.8% positive impact on overall CAGR, driven by new safety regulations and demand for glove-operable controls.

What material challenges affect capacitive sensor production?

Limited supply and price volatility of indium tin oxide currently restrain growth by -0.8% impact on forecast CAGR.

Which region leads global revenue?

Asia-Pacific accounts for 39.05% of worldwide capacitive sensor sales, benefiting from concentrated electronics and automotive manufacturing.

Are flexible capacitive sensors commercially viable?

Yes. Flexible and thin-film formats are expanding at 5.55% CAGR as roll-to-roll manufacturing reduces costs and supports applications in wearables and curved displays.

Page last updated on: