Global Tacrolimus Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 9.86 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Tacrolimus Market Analysis by Mordor Intelligence

The tacrolimus market size was valued at USD 7.39 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 9.86 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). The tacrolimus market is propelled by wider acceptance of once-daily extended-release products, growing transplant procedure volumes, and rising prescriptions for steroid-refractory autoimmune diseases. Generic penetration is accelerating after Prograf’s exclusivity loss, yet innovators sustain a premium through complex delivery platforms and robust pharmacovigilance programs. Therapeutic-drug-monitoring (TDM) technology adoption improves dose optimization and long-term adherence, mitigating toxicity risks that once limited uptake. Supply-chain security has become a strategic priority as manufacturers diversify Streptomyces fermentation sources to cope with demand spikes in Asia-Pacific.

Key Report Takeaways

- By formulation, extended-release products held 28.56% of tacrolimus market share in 2025 while intravenous preparations are forecast to expand at a 8.79% CAGR through 2031.

- By application, organ transplantation captured 38.41% of the tacrolimus market size in 2025; autoimmune diseases are projected to record a 9.91% CAGR to 2031.

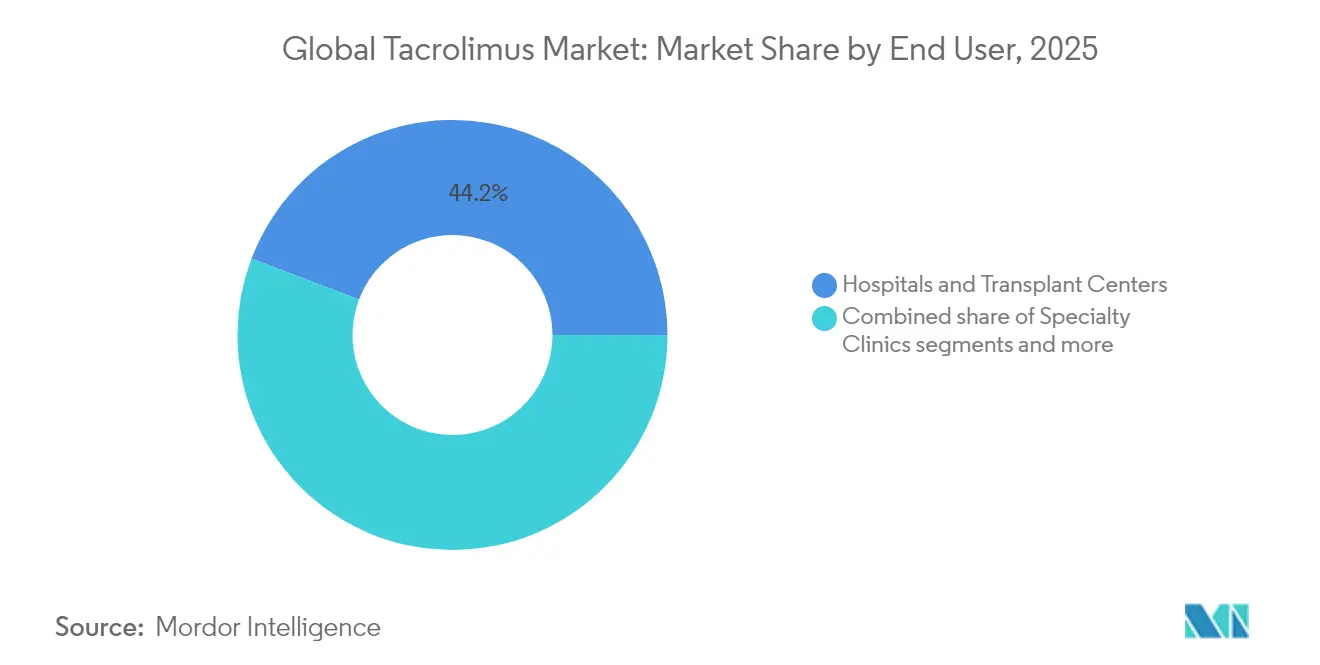

- By end-user, hospitals and transplant centers accounted for 44.22% of tacrolimus market share in 2025, whereas specialty clinics are expected to grow at a 10.48% CAGR until 2031.

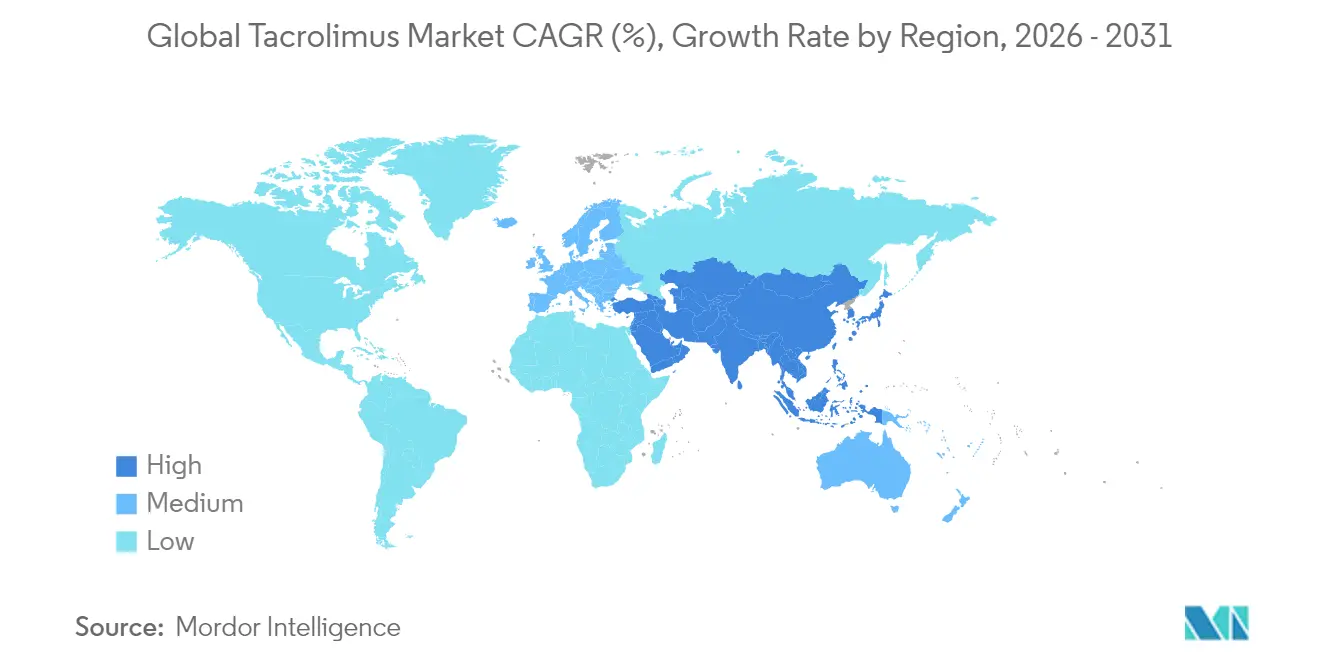

- By geography, North America led with 39.74% revenue share in 2025, and Asia-Pacific is advancing at a 9.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tacrolimus Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging post-transplant survival rates boosting long-term immunosuppressant use | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Shift from cyclosporine to tacrolimus in solid-organ transplants | +0.8% | Global, accelerated adoption in Asia-Pacific | Medium term (2-4 years) |

| Regulatory approvals for extended-release formulations | +0.7% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rising autoimmune disease burden in Asia-Pacific & Europe | +0.6% | Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Innovative drug-delivery platforms (nano-eye-drops, biodegradable implants) | +0.4% | North America & Europe, early adoption markets | Long term (≥ 4 years) |

| Precision-dosing software integrated into therapeutic drug-monitoring (TDM) systems | +0.3% | Global, with faster adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Post-Transplant Survival Rates Boost Long-Term Drug Use

Ten-year kidney graft survival now exceeds 85%, giving patients much longer exposure to maintenance immunosuppression. Higher survival translates into 40–60% more lifetime tacrolimus doses per recipient, enlarging recurring revenue streams for both innovators and generics. Clinicians increasingly choose once-daily extended-release variants, which improve adherence by simplifying complex pill schedules. Parallel growth in digital TDM platforms allows remote dose adjustment and reduces hospitalization linked to toxicity. Together, these shifts secure durable volume gains for tacrolimus through at least the next decade.

Therapeutic Migration from Cyclosporine to Tacrolimus

Large meta-analyses confirm lower acute rejection, reduced nephrotoxicity, and fewer cardiovascular events when tacrolimus replaces cyclosporine. In response, global transplant guidelines have revised first-line protocols, and more than 80% of liver-graft centers now open with tacrolimus. Rapid generic entry in Asia-Pacific removes historical cost barriers, enabling lower-income health systems to modernize regimens quickly. Hospitals also report shorter post-operative stays because tacrolimus minimizes early complications, freeing scarce ICU beds. These clinical and economic advantages sustain the formulation’s steady capture of cyclosporine share.

Rapid Regulatory Acceptance of Extended-Release Variants

Envarsus XR and similar products demonstrate smoother pharmacokinetic profiles that cut peak-trough swings linked to rejection crises. Regulators in the United States and Europe now grant priority reviews, citing clear adherence benefits and lower monitoring intensity. Patent protection until 2035 shields these variants from immediate price competition, preserving a premium of 20–30% over twice-daily capsules. Health-technology assessments in Canada and Germany show net budget savings from avoided hospital readmissions despite higher acquisition costs. Consequently, extended-release uptake is accelerating in both mature and emerging markets.

Escalating Autoimmune Disease Prevalence

Incidence of lupus nephritis, rheumatoid arthritis, and ulcerative colitis is climbing fastest in Asia-Pacific and Eastern Europe. Tacrolimus now features in multiple regional guidelines as a steroid-sparing option when standard therapy fails. Chinese health-economic models report superior quality-adjusted life-years versus cyclophosphamide, bolstering national reimbursement decisions. Pharmaceutical companies are funding large real-world registries to document long-term safety outside transplant populations. This emerging evidence base is forecast to lift autoimmune demand by double digits through 2030.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Narrow therapeutic index necessitating costly TDM | -0.9% | Global, particularly impactful in cost-sensitive markets | Long term (≥ 4 years) |

| Patent-protected LP-10/veloxis ER forms delaying price erosion | -0.5% | North America & Europe primarily | Medium term (2-4 years) |

| High nephro- & neuro-toxicity profile versus next-gen agents | -0.7% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Supply-chain vulnerability due to single-strain fermentation inputs | -0.3% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

TDM Cost Burden

Tacrolimus requires a narrow therapeutic‐index check, and monthly assays cost USD 100–200 per test, straining payer budgets in price-sensitive systems. These cumulative expenses can surpass drug acquisition costs within five years for many transplant patients. Rural hospitals across Latin America and Africa often lack calibrated chromatography platforms, forcing patients to travel long distances for blood draws. Dried-blood-spot kits reduce logistics hurdles but still rely on centralized laboratories, offering only partial relief. Until affordable point-of-care analyzers scale globally, high monitoring charges will continue to curb tacrolimus adoption in developing regions.

Extended-Release Patent Moats Slow Price Erosion

Veloxis safeguards its LP-10 once-daily coating technology with patents that run to 2035, creating a durable exclusivity window. Manufacturing requires multilayer spray deposition and real-time dissolution analytics, capabilities that most generic plants do not possess. These technical hurdles keep rivals at bay and sustain a 25% price premium over immediate-release generics. Payers in North America and Europe accept the higher list price because improved adherence lowers costly rejection-related readmissions. Consequently, extended-release pricing remains sticky, muting overall market price compression even as commodity capsules face aggressive discounting

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Extended-Release Commands Premium Pricing

Extended-release variants held 28.56% of tacrolimus market share in 2025 and generated USD 2.11 billion of tacrolimus market size that year. Superior pharmacokinetics flatten peak-to-trough swings, lowering rejection episodes and supporting once-daily adherence. Intravenous preparations, though smaller in value, are advancing at a 8.79% CAGR on wider adoption for peri-operative induction in kidney and liver grafts. Immediate-release oral generics defend volume in maintenance therapy but feel price pressure as payers bundle purchasing contracts.

Manufacturers are investing in nanocapsule suspensions, transdermal patches, and biodegradable ocular implants that promise week-long or month-long release. Coating lines capable of real-time dissolution analytics allow innovators to lock in quality differentiation and deter rapid generic replication. Pilots with 3-D-printed mini-tablets show accurate micro-dosing for paediatric use, an area still underserved by current capsule strengths. Regulatory agencies have signalled willingness to use adaptive review pathways for such technologies, provided plasma-level variability remains within established bioequivalence limits. These innovations collectively raise the technical bar for market entry while enlarging the future addressable base of complex-need patients.

By Application: Autoimmune Uptake Reconfigures Demand Mix

Organ transplantation contributed 38.41% of tacrolimus market size in 2025, anchored by kidney and liver grafts that dominate global transplant volumes. Autoimmune diseases, however, are forecast to post the quickest expansion at a 9.91% CAGR as clinical evidence validates tacrolimus in lupus nephritis, rheumatoid arthritis, and steroid-refractory ulcerative colitis. Dermatological uses such as atopic dermatitis sustain a niche through topical ointments, though growth trails systemic indications. Heart and lung transplantation remain steady but constrained by donor scarcity.

Guideline changes in Taiwan, China, and parts of Europe now list tacrolimus ahead of cyclophosphamide for second-line lupus nephritis, driving formulary wins and regional reimbursement decisions. Pooled real-world data suggest a 25% drop in hospital readmissions for autoimmune flares when tacrolimus is added to steroid-sparing regimens. Ongoing trials are testing micro-dosed tacrolimus in chronic graft-versus-host disease, an application that could create a fresh orphan-drug sub-segment. Health-technology-assessment bodies are beginning to factor lifetime productivity gains for young autoimmune sufferers, a shift that favours broader coverage. These dynamics collectively pivot overall growth momentum away from transplant-centric demand toward chronic immune-modulation markets.

By End-User: Specialty Clinics Accelerate Decentralisation

Hospitals and transplant centres captured 44.22% of tacrolimus market share in 2025, reflecting their role in acute post-operative care and early-phase TDM. Specialty clinics, however, are on track for a 10.48% CAGR as payers push follow-up care into lower-cost outpatient settings. Dermatology offices maintain durable demand for topical tacrolimus, while ambulatory-surgery centres gain relevance for same-day graft biopsies and immediate re-dosing protocols. Telepharmacy platforms enable rural clinicians to consult tertiary-centre pharmacologists for dose titration decisions.

Portable immunoassay kits and Bluetooth-enabled pill bottles let clinicians monitor trough levels and adherence without repeated hospital visits. Value-based-care contracts in the United States now reimburse speciality clinics for outcome metrics such as graft-survival days rather than visit counts, incentivising proactive dose management. In Europe, bundled-payment pilots across Spain and Germany include tacrolimus dispensing inside capitated transplant packages, formalising the hand-off from university hospitals to community nephrology centres. Large pharmacy-benefit managers are aligning with integrated specialty clinics to negotiate volume-based discounts on once-daily capsules. Together, these shifts firmly anchor long-term demand in outpatient channels and redistribute negotiating power across the supply chain.

Geography Analysis

North America accounted for 39.74% of tacrolimus market size in 2025. Established transplant infrastructure, comprehensive insurance coverage, and strict bioequivalence standards favor suppliers with strong quality systems. The FDA’s February 2025 downgrade of Accord’s generic from AB to BX underscored the reputational stakes tied to manufacturing rigor.

Asia-Pacific is the fastest-growing region at 9.21% CAGR. China’s NMPA shortened review cycles for complex generics, enabling Biocon’s January 2025 approval of three strengths in one filing. Japan emphasizes local production and post-marketing surveillance, supporting domestic suppliers, whereas India leverages cost-efficient fermenters to feed global demand.

Europe grows steadily under universal healthcare and harmonized EMA pathways. Germany, the United Kingdom, and France dominate volumes, while Eastern European markets expand as transplant programs mature. South America and Middle East & Africa progress more slowly because reimbursement gaps and limited donor networks constrain procedure counts, yet Brazil’s public-private partnerships hint at faster adoption ahead.

Competitive Landscape

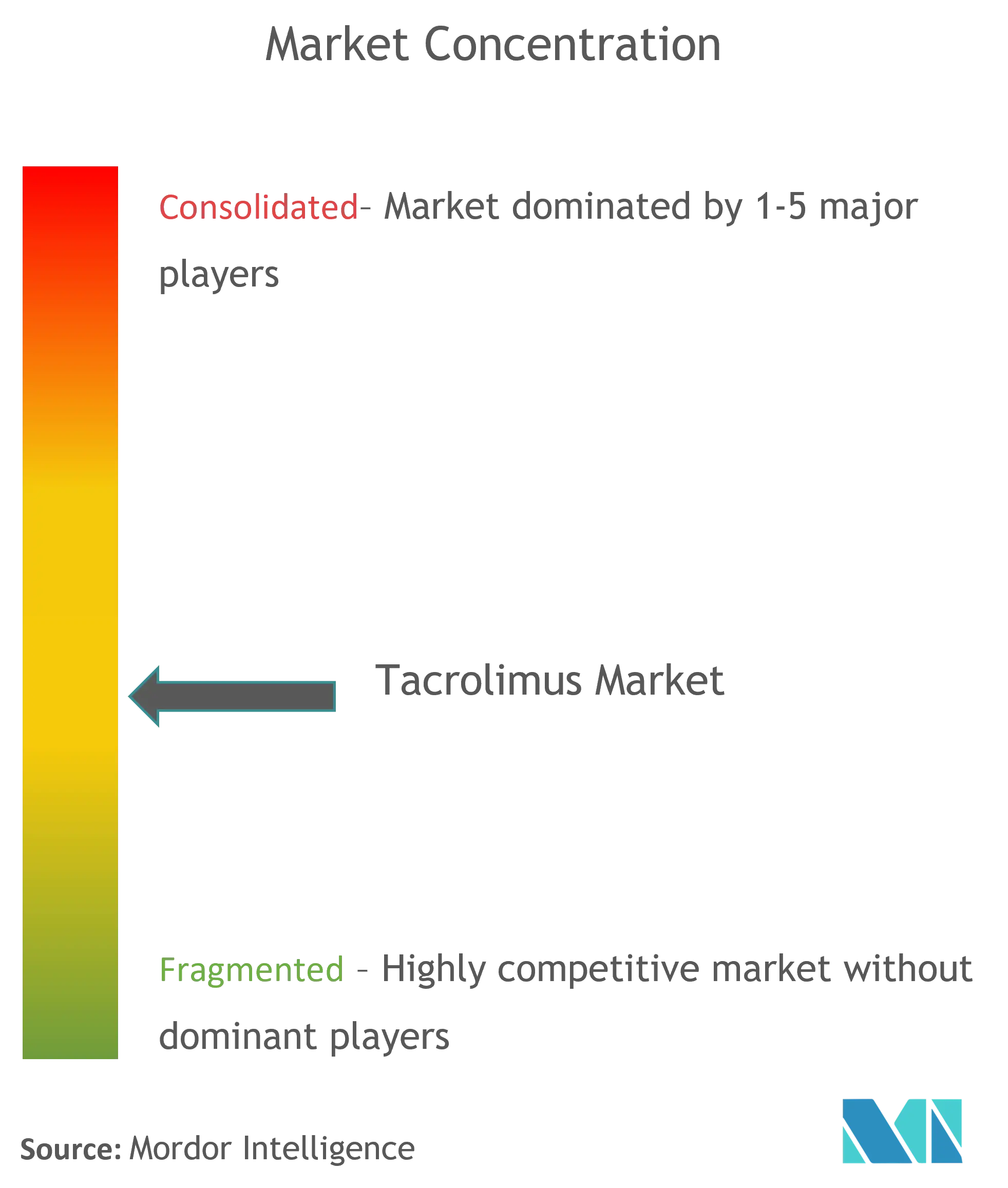

The tacrolimus market remains moderately consolidated. Astellas maintains leadership with Prograf, yet generic makers from India and the EU capture share through aggressive pricing.

Veloxis sustains a patent fence around Envarsus XR, enabling premium pricing and shielding against commoditization. Indian firms such as Dr. Reddy’s and Sun Pharmaceutical fortify positions by dual-sourcing fermentation inputs and securing FDA and EMA certifications.

Strategic focus is shifting toward service differentiation: partnerships with AI-based dosing platforms and integrated TDM services enhance value propositions. Manufacturers that diversify Streptomyces strains or co-locate production across continents mitigate supply risk and gain favor with risk-averse hospital buyers.

Global Tacrolimus Industry Leaders

Pfizer Inc.

Astellas Pharma Inc.

Lupin Pharmaceuticals Inc.

Glenmark Pharmaceuticals Inc.

Biocon Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Biocon Pharma Limited secured NMPA approval for tacrolimus capsules (0.5 mg, 1 mg, 5 mg) in China

- January 2025: Chugai, SoftBank, and SB Intuitions launched a generative-AI collaboration to shorten drug-development timelines

Global Tacrolimus Market Report Scope

As per the scope of the report, tacrolimus is a member of the class of drugs referred to as immunosuppressants. In order to reduce allergic reactions and prevent organ transplant rejection, the drug is used to effectively suppress the immune system. The tacrolimus market is segmented by Product Type (Tablets and Capsules, Injections, and Others), Application (Immunosuppression, Dermatitis, and Others), End Users (Hospitals, Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers the value (in USD million) for the above segments. The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally.

| Extended Release |

| Topical Ointment |

| Intravenous |

| Oral |

| Others |

| Organ Transplant | Kidney Transplant |

| Liver Transplant | |

| Heart Transplant | |

| Lung Transplant | |

| Autoimmune Diseases | Rheumatoid Arthritis |

| Lupus Nephritis | |

| Ulcerative Colitis | |

| Psoriasis | |

| Dermatological Conditions | Atopic Dermatitis |

| Dry Eye Disease |

| Hospitals & Transplant Centers |

| Specialty Clinics |

| Dermatology Clinics |

| Ambulatory Surgery Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Formulation (Value) | Extended Release | |

| Topical Ointment | ||

| Intravenous | ||

| Oral | ||

| Others | ||

| By Application (Value) | Organ Transplant | Kidney Transplant |

| Liver Transplant | ||

| Heart Transplant | ||

| Lung Transplant | ||

| Autoimmune Diseases | Rheumatoid Arthritis | |

| Lupus Nephritis | ||

| Ulcerative Colitis | ||

| Psoriasis | ||

| Dermatological Conditions | Atopic Dermatitis | |

| Dry Eye Disease | ||

| By End-user (Value) | Hospitals & Transplant Centers | |

| Specialty Clinics | ||

| Dermatology Clinics | ||

| Ambulatory Surgery Centers | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the tacrolimus market?

The tacrolimus market size is USD 7.75 billion in 2026.

How fast will tacrolimus sales grow through 2031?

Revenue is forecast to rise at a 4.92% CAGR, reaching USD 9.86 billion by 2031.

Which region leads global tacrolimus demand?

North America holds the largest share at 39.74% of 2025 revenue.

Which formulation segment is expanding quickest?

Intravenous preparations are advancing at a 8.79% CAGR thanks to wider acute-care adoption.

Why are extended-release products priced at a premium?

Patent protection until 2035 and complex manufacturing maintain limited competition and higher prices.

What is the main growth driver outside transplantation?

Rising autoimmune disease prevalence is propelling tacrolimus uptake in lupus nephritis and rheumatoid arthritis therapies.

Page last updated on: