Psoriatic Arthritis Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

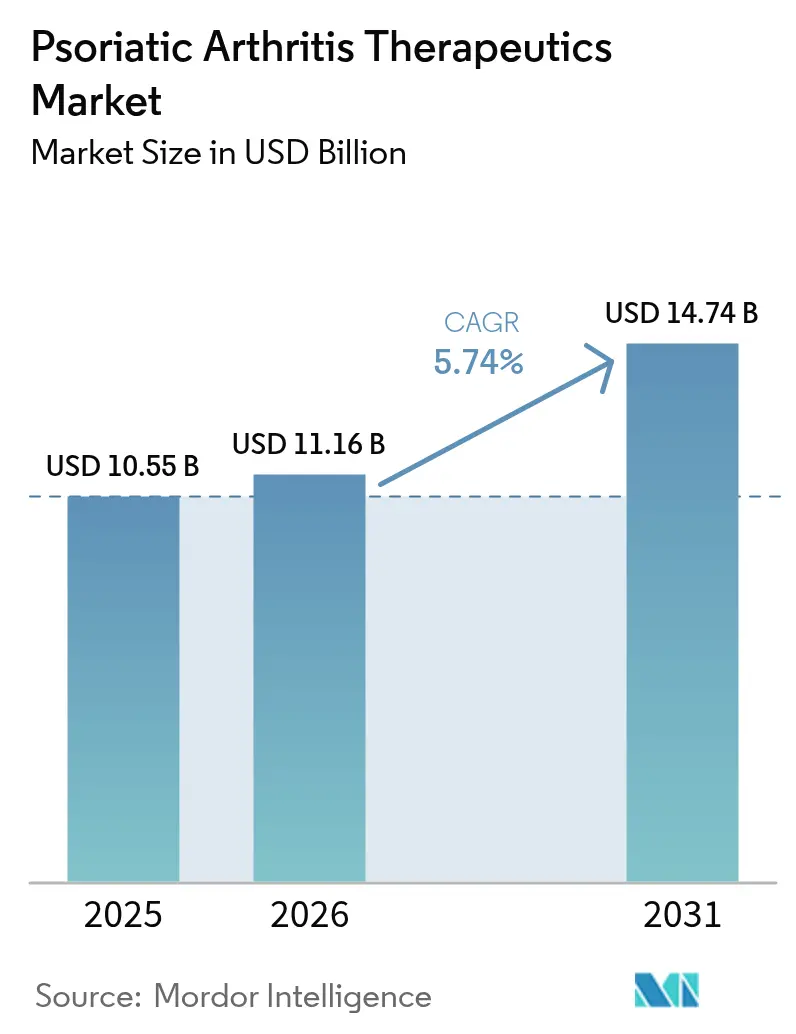

| Market Size (2026) | USD 11.16 Billion |

| Market Size (2031) | USD 14.74 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

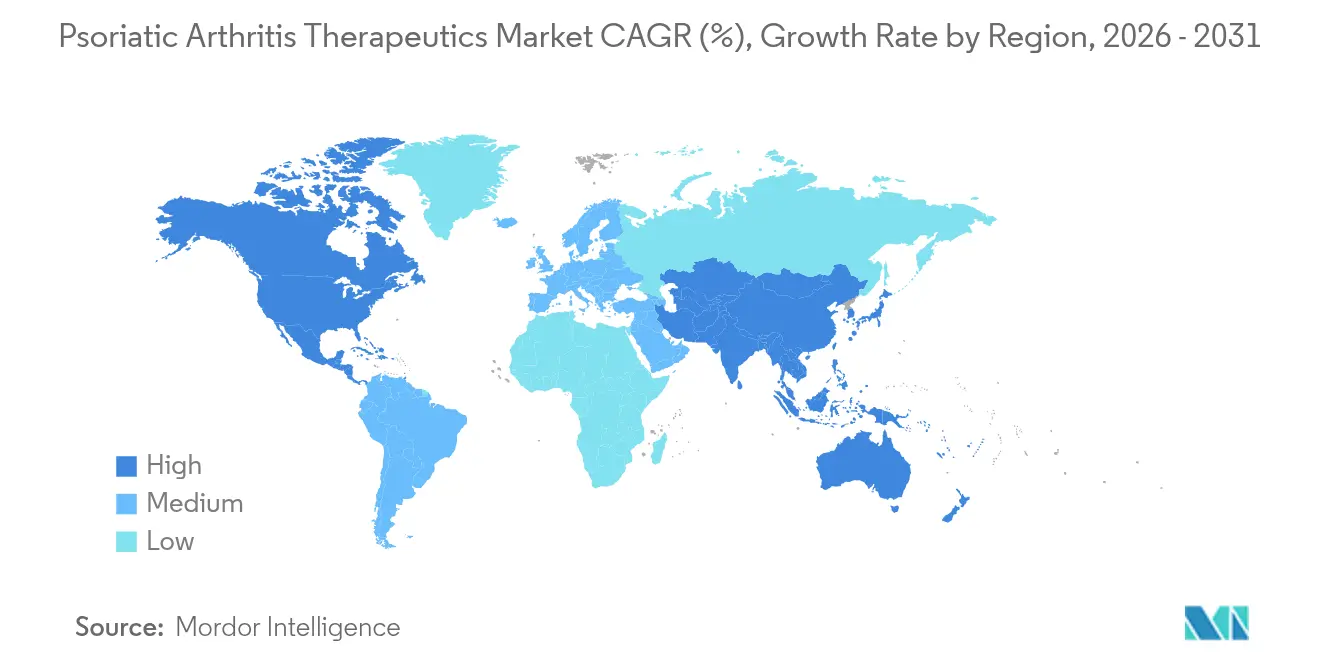

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Psoriatic Arthritis Therapeutics Market Analysis by Mordor Intelligence

The psoriatic arthritis therapeutics market size is expected to grow from USD 10.55 billion in 2025 to USD 11.16 billion in 2026 and is forecast to reach USD 14.74 billion by 2031 at 5.74% CAGR over 2026-2031. Rising disease visibility, the obesity-metabolic syndrome link, and a robust biologic launch pipeline are widening both patient pools and therapeutic choice. The 2024 approval of bimekizumab, the first dual IL-17A/F inhibitor, affirms the industry’s shift toward multi-cytokine blockade, while three ustekinumab biosimilars that entered the United States in early 2025 have introduced immediate price competition. Diagnostic latency continues to decline as rheumatologists adopt high-resolution imaging and biomarker panels, expanding early-stage intervention cohorts. Digital adherence platforms, especially tele-rheumatology services, improve medication persistence and are proving critical in under-served regions.

Key Report Takeaways

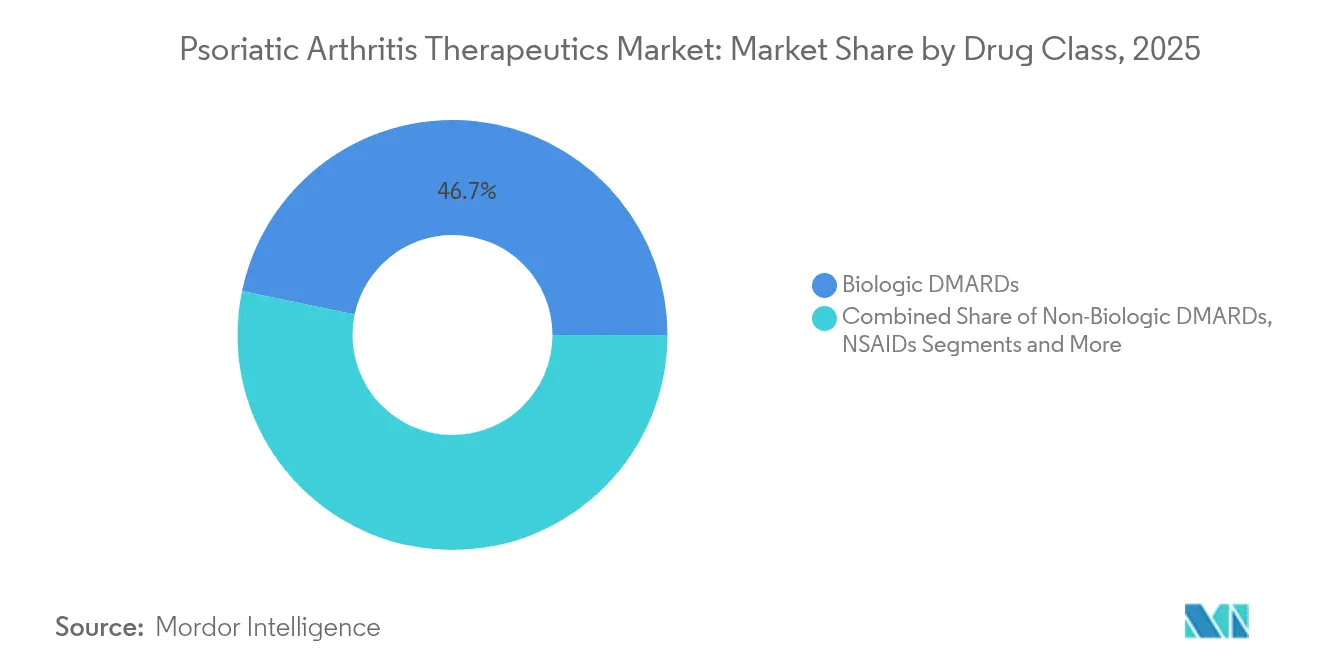

- By drug class, biologic DMARDs led with 46.72% of psoriatic arthritis therapeutics market share in 2025; non-biologic DMARDs are projected to expand at a 6.68% CAGR through 2031.

- By route of administration, parenteral formulations held 71.83% of the psoriatic arthritis therapeutics market size in 2025, while oral therapies are forecast to grow at a 6.72% CAGR to 2031.

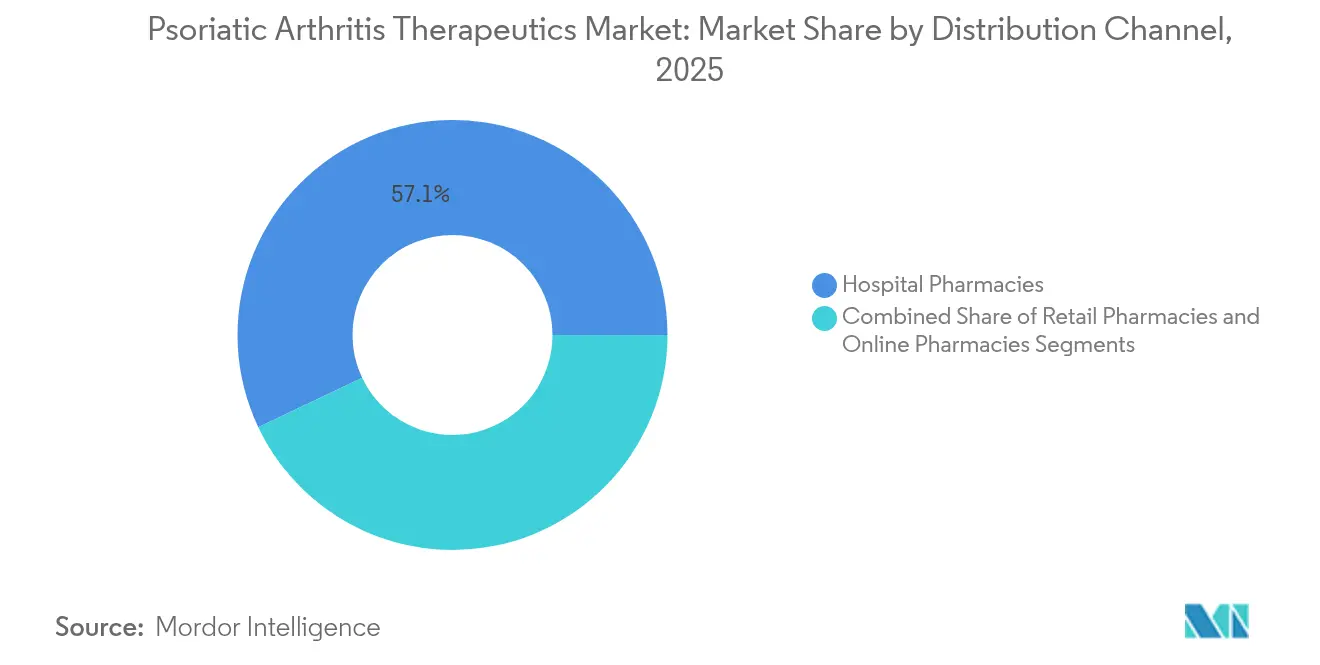

- By distribution channel, hospital pharmacies accounted for 57.05% revenue in 2025; online pharmacies exhibit the highest growth trajectory at 6.88% CAGR through 2031.

- By age group, adults accounted for 52.12% revenue in 2025; geriatric exhibit the highest growth trajectory at 6.83% CAGR through 2031.

- By geography, North America commanded 41.45% share of the psoriatic arthritis therapeutics market in 2025, whereas Asia-Pacific is advancing at a 6.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Psoriatic Arthritis Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence Linked to Obesity & Metabolic Syndrome | +1.8% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Expansion of Approved Biologic & tsDMARD Therapies | +2.1% | Global, led by US & EU regulatory approvals | Short term (≤ 2 years) |

| Earlier Diagnosis Via Imaging & Biomarker Panels | +1.2% | Developed markets initially, expanding to APAC | Medium term (2-4 years) |

| Payer Acceptance of Value-Based Contracts for Biologics | +0.7% | North America & Europe primarily | Long term (≥ 4 years) |

| Digital Adherence & Monitoring Solutions Adoption | +0.9% | Global, with faster adoption in tech-forward regions | Long term (≥ 4 years) |

| Uptake Of Biosimilar Biologics Lowering Entry Barriers | +1.5% | Global, with highest impact in Europe & emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing prevalence linked to obesity & metabolic syndrome

Obesity heightens psoriatic arthritis risk by 40-60%, and more than one-quarter of adults in high-income countries now meet metabolic-syndrome criteria, fueling sustained demand for biologic DMARDs [1]Robin C. Yi, "Therapeutic Advancements in Psoriasis and Psoriatic Arthritis," MDPI, mdpi.com. Adipose-derived cytokines amplify systemic inflammation, prompting earlier rheumatology referrals. Commercial payers increasingly acknowledge the comorbidity burden, widening coverage for advanced therapies that can reduce long-term disability costs.

Expansion of approved biologic & tsDMARD therapies

Bimekizumab’s 2024 approval delivered the first dual IL-17A/F approach and posted superior skin clearance versus ixekizumab, broadening cytokine-specific choices. Phase 3 success for deucravacitinib in March 2025 (54.2% ACR20 versus 39.4% placebo) signals a new oral option that may expand first-line use in moderate disease [2]Bristol Myers Squibb Press Release, “Sotyktu Phase 3 Results,” bms.com . Rapid label additions reduce reliance on TNF inhibitors and enable sequence-based regimens tailored to biomarker profiles.

Earlier diagnosis via imaging & biomarker panels

High-resolution ultrasound detects enthesitis before irreversible erosion, while serum IL-17 and IL-23 assays help stratify treatment early. Dermatology-embedded digital questionnaires identify up to 30% of psoriasis patients at joint-disease risk within ten years. Earlier referral supports milder-stage biologic initiation, shifting volume toward community settings.

Payer acceptance of value-based contracts

North American and European insurers increasingly tie biologic reimbursement to real-world response, offsetting acquisition costs with outcome guarantees. Contracts covering IL-23 and IL-17 agents offer rebates when skin and joint scores fail to improve, easing formulary access restrictions and supporting broader uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Care & Patient OOP Burden | -1.4% | Global, with highest impact in US market | Short term (≤ 2 years) |

| Long-Term Immunosuppression Safety Concerns | -0.8% | Global, with regulatory focus in developed markets | Medium term (2-4 years) |

| Limited Rheumatologist Capacity in Emerging Markets | -0.6% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Reimbursement Delays for Novel Targeted Agents | -0.5% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High total cost of care & patient OOP burden

Annual therapy costs span USD 45,000-80,000, with Medicare beneficiaries facing USD 4,423-6,950 out-of-pocket payments that drive 15-20% discontinuation rates. Step-therapy mandates delay biologic start by 3-6 months, increasing irreversible joint damage risk [3]Georgia Marquez-Grap, "The Impact of Step Therapy on Individuals with Psoriatic Disease in the USA: Patient and Provider Perspectives," Springer Nature, link.springer.com.

Long-term immunosuppression safety concerns

Fifteen-year surveillance links TNF inhibitors to elevated hematologic malignancy rates, albeit at 2-3 events per 1,000 patient-years, prompting intensive monitoring. FDA boxed warnings on JAK cardiovascular risk issued in 2024 dampened prescriber enthusiasm despite clinical efficacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologic dominance faces biosimilar disruption

Biologic DMARDs contributed USD 4.93 billion in 2025 and represented 46.72% of psoriatic arthritis therapeutics market share. Ustekinumab biosimilar approvals in early 2025 have already trimmed originator sales and are expected to lower brand pricing across the class. Meanwhile, non-biologic DMARDs are set to outpace at a 6.68% CAGR to 2031 as oral small molecules such as deucravacitinib expand adoption.

Cost-sensitive prescribers are cycling more patients to methotrexate plus targeted synthetics before initiating injectable biologics, creating an opportunity for hybrid sequencing strategies. Adalimumab biosimilars captured 23% of United States anti-TNF volume by late 2024 and stimulated parallel adoption in Europe, where tender purchasing amplifies price erosion. This competitive dynamic has pushed originators to pivot toward next-generation assets, such as guselkumab and risankizumab, that offer distinct mechanisms or improved dosing convenience.

By Route of Administration: Parenteral leadership challenged by oral innovation

Injectables retained 71.83% revenue share thanks to high-dose bioavailability requirements for monoclonal antibodies. Subcutaneous self-dosing every eight to twelve weeks improves adherence compared with weekly regimens, supporting sustained parenteral demand. Nevertheless, oral products delivered the fastest growth at 6.72% CAGR and could elevate their psoriatic arthritis therapeutics market size to USD 3.39 billion by 2031.

JAK and TYK2 inhibitors, including tofacitinib and deucravacitinib, are central to this shift, allowing rheumatologists to initiate therapy without injection-training infrastructure. Head-to-head trials show similar efficacy to subcutaneous comparators, with survey data indicating 78% of patients would prefer oral dosing if safety and efficacy are equivalent.

By Distribution Channel: Hospital dominance erodes to digital channels

Specialty hospital pharmacies managed 57.05% of 2025 sales, driven by complex cold-chain logistics and infusion center integration. Their embedded clinical services deliver injection education and adverse-event monitoring, which remain critical for high-risk immunosuppressants. Yet the online segment is scaling at 6.88% CAGR, aided by regulatory allowances for direct-to-patient biologic shipment and heightened telehealth adoption during the pandemic.

Digital pharmacies leverage synchronized refill reminders, doorstep delivery, and video counseling to close adherence gaps. Multi-state licensure platforms now cover 42 U.S. jurisdictions, improving specialty drug reach in rural counties where rheumatologist density is low. Pharmacy benefit managers are also channeling traffic to mail-order services that capture greater formulary rebates.

By Age Group: Adult prevalence drives geriatric growth acceleration

Adults aged 30-50 commanded 52.12% of 2025 revenue as symptom onset aligns with peak workforce participation. Biologic adherence in this group averages 65% at twelve months, materially higher than the geriatric cohort. However, the ≥65-year segment is forecast to grow 6.83% annually, reflecting global population aging and better recognition of late-onset presentations.

Geriatric care complicates dosing due to polypharmacy and immunosenescence: infection risk is two-fold greater than in younger adults, steering physicians toward IL-23 inhibitors with favorable safety signals. Pediatric disease remains uncommon but represents a strategic focus for companies pursuing life-cycle indications to extend product exclusivity.

Geography Analysis

North America retained leadership with USD 4.37 billion sales in 2025 and 41.45% psoriatic arthritis therapeutics market share. Early FDA approvals, high biologic penetration, and mature specialty pharmacy networks offset access friction from prior-authorization delays. Medicare patients still face USD 4,423-6,950 average annual out-of-pocket spending, driving discontinuation and prompting policy debates over Part D redesign. Step-therapy protocols, while intended to control spending, may postpone optimal therapy, leading to functional decline and heightened downstream costs.

Asia-Pacific posted the fastest 6.9% CAGR and could overtake Europe by 2031. Japan already treats 55.3% of psoriatic arthritis cases with biologics following guideline revisions that prioritize early intensive therapy. China and India are scaling domestic biosimilar production, trimming unit costs and making advanced care more attainable for urban middle-class populations. South Korea’s single-payer model funds risankizumab and guselkumab after managed-entry agreements that cap budget impact.

Europe’s steady growth rests on health-technology assessments that weigh clinical benefit against price, accelerating biosimilar penetration for cost containment. Outcomes-based contracts in Germany and France tie reimbursement to real-world PASI and ACR responses, influencing global price-setting strategies. Latin American markets lag owing to specialist shortages and funding constraints, yet public-private partnerships in Brazil and Argentina are expanding rheumatology clinics and subsidizing targeted agents.

Competitive Landscape

The psoriatic arthritis therapeutics market remains moderately concentrated as the top five companies—AbbVie, Johnson & Johnson, Pfizer, Bristol Myers Squibb, and UCB—collectively controlled roughly 68% of 2024 revenue. AbbVie shifted promotional focus from Humira to Skyrizi and Rinvoq ahead of biosimilar erosion, allocating more than USD 3 billion to immunology R&D in 2025. Johnson & Johnson counters biosimilar pressure on Stelara by accelerating Tremfya lifecycle studies in axial disease, while Simponi retains niche value for intravenous dosing preferences.

Bristol Myers Squibb’s deucravacitinib success underpins its oral franchise strategy amid robust rheumatology trial pipelines. UCB commercialized bimekizumab across United States and Europe within six months of approval, aided by a streamlined manufacturing network and value-based contracts with major payers. Merck’s USD 10.8 billion acquisition of Prometheus Biosciences signals renewed big-pharma interest in autoimmune expansion, with an IL-23R inhibitor scheduled to enter Phase 2 trials by late 2025.

Biosimilar challengers such as Samsung Bioepis, Alvotech, and Biocon are eroding incumbent share via aggressive discounting and rapid launch roll-outs. Their combined ustekinumab biosimilar portfolio captured 12% of United States volume within three months of launch, pressuring originator net pricing. Digital health tie-ins differentiate portfolios: companion apps track patient-reported outcomes and interface with rheumatology EMRs, improving adherence and generating real-world evidence that supports value-based reimbursement.

Psoriatic Arthritis Therapeutics Industry Leaders

-

AbbVie Inc

-

Johnson & Johnson

-

Pfizer Inc.

-

Sanofi S.A.

-

Bristol-Myers Squibb

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bristol Myers Squibb announced positive Phase 3 POETYK PsA-2 results for Sotyktu (deucravacitinib), achieving 54.2% ACR20 versus 39.4% placebo.

- February 2025: Sandoz launched Pyzchiva (ustekinumab-ttwe) across the United States, the first Stelara biosimilar made available nationwide.

- February 2025: Biocon Biologics introduced YESINTEK (ustekinumab-kfce) to United States patients, supporting market diversification.

- February 2025: Teva and Alvotech began United States distribution of SELARSDI (ustekinumab-aekn) for adult and pediatric psoriatic arthritis.

Global Psoriatic Arthritis Therapeutics Market Report Scope

As per the scope of the report, psoriatic arthritis is a form of arthritis that affects some people with psoriasis, a condition that develops red patches on the skin with silvery scales. Psoriatic arthritis therapeutics include drugs that help relieve pain, reduce inflammation, slow the progression of psoriatic arthritis, or directly target parts of the immune system that trigger inflammation.

The psoriatic arthritis therapeutics market is segmented by drug class, route of administration, and geography. By drug class, the market is segmented into nonsteroidal anti-inflammatory drugs (NSAIDs), disease-modifying antirheumatic drugs (DMARDs), immunosuppressants, biologic agents, and others. By route of administration, the market is segmented into oral, parenteral, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.

| NSAIDs |

| Non-Biologic DMARDs |

| Biologic DMARDs |

| Immunosuppressants |

| Other Drug Classes |

| Oral |

| Parenteral |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Adults |

| Geriatric |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | NSAIDs | |

| Non-Biologic DMARDs | ||

| Biologic DMARDs | ||

| Immunosuppressants | ||

| Other Drug Classes | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Age Group | Adults | |

| Geriatric | ||

| Pediatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the psoriatic arthritis therapeutics market?

The psoriatic arthritis therapeutics market was valued at USD 11.16 billion in 2026 and is projected to reach USD 14.74 billion by 2031.

Which drug class leads the psoriatic arthritis therapeutics market?

Biologic DMARDs led with 46.72% psoriatic arthritis therapeutics market share in 2025, although biosimilar launches are beginning to erode that dominance.

Why is Asia-Pacific the fastest-growing regional market?

Regulatory harmonization, expanding health-insurance coverage, and domestic biosimilar manufacturing are driving a 6.9% CAGR for Asia-Pacific through 2031.

How are biosimilars affecting market dynamics?

Ustekinumab and adalimumab biosimilars have entered multiple markets, reducing average selling prices and compelling originators to focus on next-generation therapies.

What role does telemedicine play in psoriatic arthritis care?

Tele-rheumatology expands specialist access, boosts adherence via remote monitoring, and supports the shift toward online and mail-order pharmacy channels.

Which safety concerns influence prescribing decisions?

Long-term infection and malignancy risks associated with broad immunosuppression, along with cardiovascular warnings on JAK inhibitors, guide therapy selection and monitoring protocols.

Page last updated on: