Synthetic Spider Silk Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

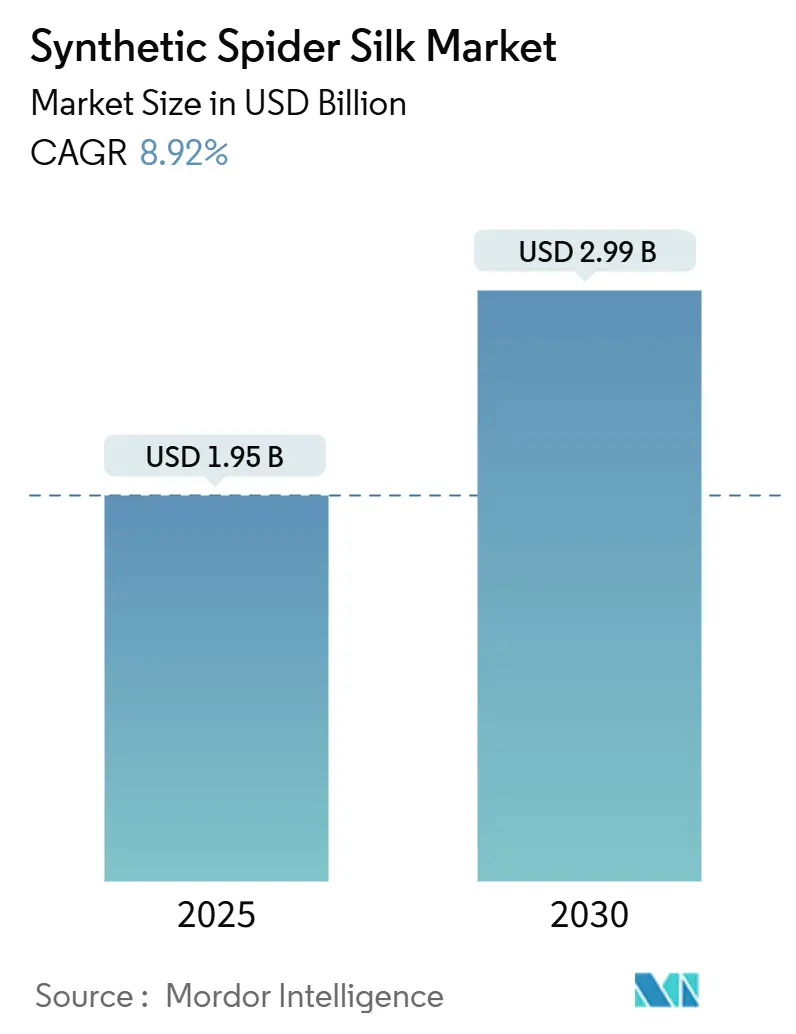

| Market Size (2025) | USD 1.95 Billion |

| Market Size (2030) | USD 2.99 Billion |

| Growth Rate (2025 - 2030) | 8.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Spider Silk Market Analysis by Mordor Intelligence

The Synthetic Spider Silk Market size is estimated at USD 1.95 billion in 2025, and is expected to reach USD 2.99 billion by 2030, at a CAGR of 8.92% during the forecast period (2025-2030). Robust demand for high-strength, lightweight biomaterials, rapid advances in microbial-fermentation platforms and mounting sustainability mandates collectively underpin the market’s acceleration. Producers have resolved key molecular-weight and yield bottlenecks, enabling industrial-scale biomanufacturing that satisfies quality specifications for aerospace, defense and advanced biomedical uses. Government funding for synthetic-biology pilots in Asia-Pacific, supportive regulatory frameworks in the European Union and U.S. defense procurement for high-performance fibers align to expand downstream adoption. Competitive intensity remains high because no single production technology or company commands a decisive cost advantage, prompting sustained R&D on photosynthetic bacteria, seeded chain-growth polymerization and hybrid protein-engineering approaches.

Key Report Takeaways

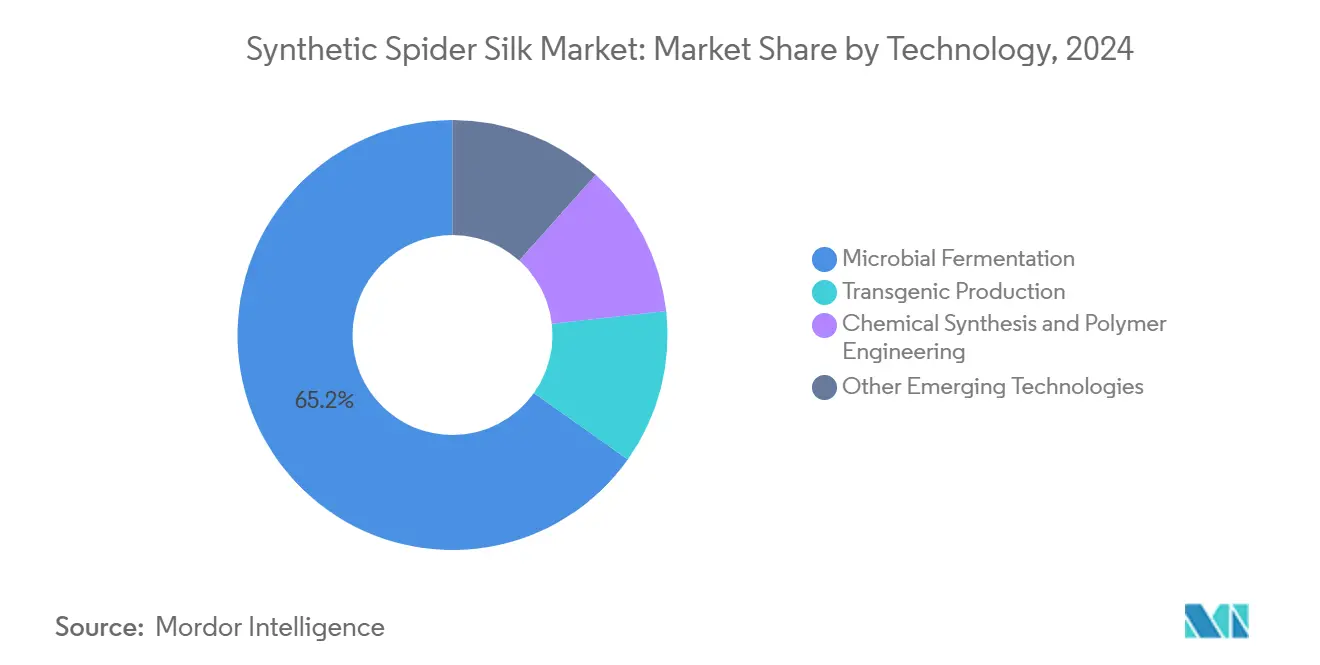

- By technology, microbial fermentation captured 65.18% of synthetic spider silk market share in 2024 while other emerging technologies are set to expand at a 9.27% CAGR to 2030.

- By product type, fibers and threads held 54.29% of the synthetic spider silk market size in 2024; nanocomposites and hydrogels are projected to advance at a 9.71% CAGR through 2030.

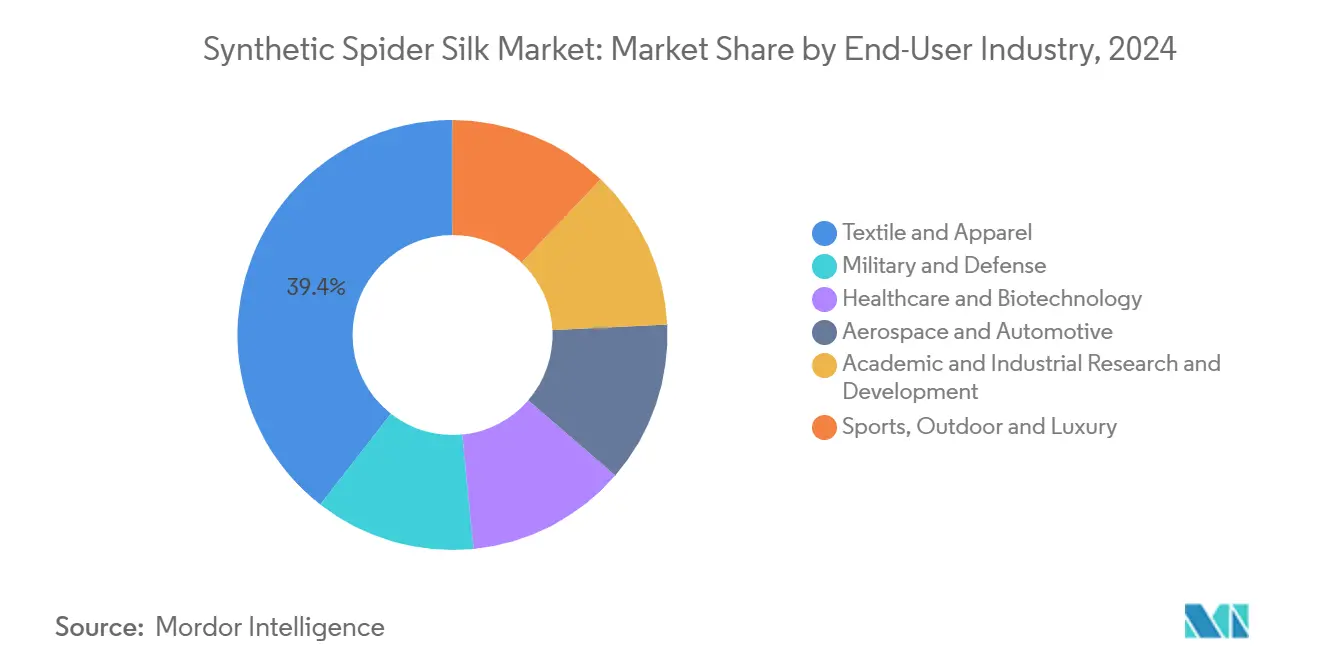

- By end-user industry, textile and apparel led with 39.44% revenue share in 2024, whereas aerospace and automotive is the fastest-growing segment at a 9.66% CAGR to 2030.

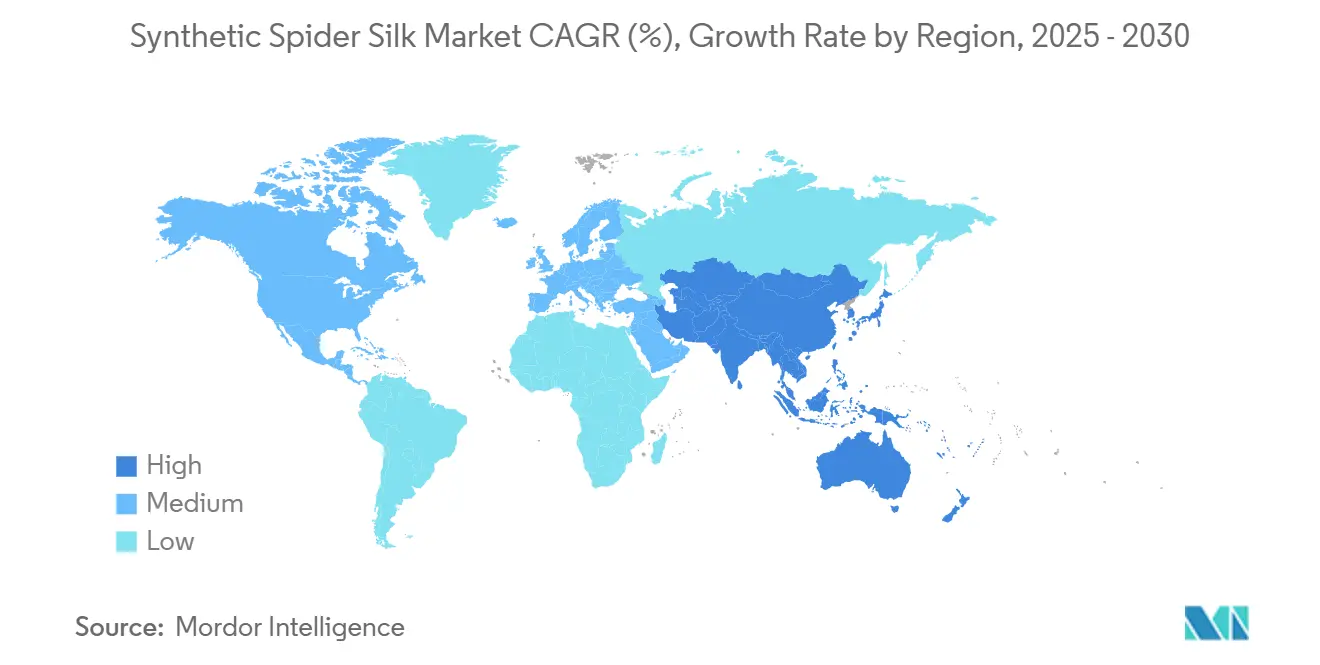

- By geography, Asia-Pacific commanded 46.51% of global value in 2024 and is progressing at a 9.58% CAGR through 2030.

Global Synthetic Spider Silk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-strength, lightweight biomaterials | +2.10% | Global, with concentration in aerospace hubs | Medium term (2-4 years) |

| Advances in synthetic biology and microbial-fermentation platforms | +2.80% | APAC core, spill-over to North America & EU | Short term (≤ 2 years) |

| Expansion of biomedical and tissue-engineering applications | +1.90% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Sustainability push for biodegradable alternatives to petro-fibers | +1.70% | EU leading, followed by North America | Medium term (2-4 years) |

| Performance biomaterials for additive manufacturing | +1.20% | Global, concentrated in industrial centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Strength, Lightweight Biomaterials

Aerospace and automotive OEMs require materials that exceed the strength-to-weight benchmarks of aluminum while cutting fuel burn and emissions, and spider silk’s tensile strength of up to 1.5 GPa rivals specialty steels while retaining exceptional ductility. U.S. military validation—exemplified by a USD 1 million Dragon Silk body-armor contract—shortened qualification cycles for civilian aircraft and vehicle components. Integration into seat structures and interior panels reduces mass without compromising crash-worthiness, supporting stricter 2027 CO₂ standards. Consumer electronics makers are concurrently trialing silk-based composites for drop-resistant housings that satisfy eco-design rules. These early wins foster cross-industry confidence, unlocking larger procurement volumes that stimulate capacity investments.

Advances in Synthetic Biology and Microbial-Fermentation Platforms

Metabolic-engineering breakthroughs in Escherichia coli now yield native-sized 284.9 kDa spidroins that spin into continuous filament with natural-silk-level toughness[1]Xiao-Xia Xia et al., “Native-Sized Recombinant Spider Silk Protein Produced in E. coli,” Proceedings of the National Academy of Sciences, pnas.org . Seeded chain-growth polymerization allows in-cell elongation, removing costly refolding steps and elevating volumetric productivity by nearly 40%[2]Christopher Hyde Bowen et al., “Seeded Chain-Growth Polymerization in Living Cells,” ACS Synthetic Biology, acssynbiology.org . Commercial fermenters in Thailand and Japan already run 500-ton-per-year lines, showing capex per kilogram below legacy aramid facilities. Ongoing pilots with marine photosynthetic bacteria that convert seawater and sunlight directly into silk proteins could trim feedstock costs by an extra 25% within three years. Collectively, these platform shifts underpin the synthetic spider silk market’s transition to multi-plant, multi-continent production footprints by 2027.

Expansion of Biomedical and Tissue-Engineering Applications

Spider silk’s immunologically inert β-sheet architecture enables scaffolds that integrate with soft tissues while biodegrading into benign amino acids. Recent in-vivo studies show wound-closure rates 30% faster than standard collagen dressings among diabetic models, stimulating hospital procurement trials in the United States and China. Silk-based hydrogels that gel in under three minutes create injectable carriers for chemotherapeutics or stem cells, satisfying minimally invasive surgery protocols. Nanocomposites embedding ZnO nanoparticles impart antibacterial activity, catering to chronic wound care where resistance to conventional antibiotics is rising. Funding from China’s USD 4.17 billion biomanufacturing program accelerates clinical translation, anchoring long-term demand growth for medical-grade fibers and gels.

Sustainability Push for Biodegradable Alternatives to Petro-Fibers

The European Union’s Strategy for Sustainable and Circular Textiles mandates a 20% reduction in fossil-based fibers by 2030, incentivizing procurement of animal-free proteins such as brewed spider silk. Life-cycle assessment suggests brewed protein uses 94% less water and emits 88% fewer greenhouse-gas equivalents than cashmere, aligning with apparel brands’ Scope 3 targets. Consumer labels highlighting biodegradability and microplastic-free credentials differentiate products in premium outdoor and luxury segments. Policymakers in the United Kingdom and Germany are drafting carbon-content labeling schemes that could further reward silk adopters with lower compliance fees. These regulatory shifts cement synthetic spider silk market positioning as a next-generation sustainable textile input.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs and scalability hurdles | -2.30% | Global, most acute in developed markets | Short term (≤ 2 years) |

| Limited commercial availability and niche applications | -1.80% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Regulatory uncertainty for GMO-derived proteins in consumer goods | -1.10% | EU and North America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Costs and Scalability Hurdles

Current silk filament prices of USD 300 per kg exceed para-aramid by more than threefold, restricting adoption to defense gear, luxury fashion and prototype aerospace panels. Fixed-cost amortization dominates unit economics until plants exceed 2,000 ton-per-year throughput, yet demand at prevailing prices covers only one-third of such capacity. Strain toxicity, inducer expense and downstream purification still account for 58% of cost of goods, despite 4-to-33-fold yield improvements in optimized E. coli lines[3]Alexander Connor et al., “Strain Optimization for Recombinant Silk Fibroin,” pubmed.gov . Without further feedstock and fermentation-time reductions, many projects risk negative margins, postponing capacity final-investment decisions beyond 2026.

Limited Commercial Availability and Niche Applications

Fewer than ten companies worldwide possess pilot lines capable of delivering more than 50 tons annually, leading to spot shortages that deter OEMs from designing spider silk into high-volume SKUs. Patent thickets—over 2,400 active families—inflate licensing costs and complicate multi-supplier qualifications. Diverse protein sequences and spinning processes produce fibers with variable modulus, hindering standardization critical for aerospace certification. These supply-chain constraints confine the synthetic spider silk market to premium capsules, demonstration contracts and research consortia, delaying mass-market diffusion until commercial plants de-risk supply security.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Fermentation Leadership With Fast-Rising Alternatives

Microbial fermentation contributed 65.18% of 2024 revenue, reflecting proven scale-up from shake-flask to 150 m³ bioreactors and consistent physicochemical performance. Spiber’s Thai flagship exemplifies economies of scale that narrow cost differentials against para-aramid by one-third. Emerging technologies—marine cyanobacteria reactors and cell-free enzymatic synthesis—advance at 9.27% CAGR, helped by lower feedstock costs and simpler purification regimes. Strategic collaborations between chemical majors and biotech startups aim to commercialize hybrid approaches that splice precision-polymer chemistry onto recombinant cores, improving UV resistance and flame retardancy.

Ventures targeting seed-and-harvest polymerization inside engineered Bacillus strains report pilot yields of 6.5 g L⁻¹, double 2023 baselines, with downstream handling steps reduced by 20 hours. Investors view these platforms as hedge bets should fermentation enzyme costs rise. Meanwhile, transgenic silkworm programs retain niche appeal for military parachute fabrics where filament length supersedes cost sensitivity; however, biosecurity regulations and long generation cycles limit scaling. By 2030, the synthetic spider silk market is expected to witness significant capacity expansion. Fermentation will dominate bulk production, while photosynthetic and hybrid methods will cater to specialized, value-added grades.

By Product Type: Nanocomposites Propel Diversification

Fibers and threads represented 54.29% of total value in 2024, underpinned by commercial yarn offerings for luxury streetwear and technical fabrics that exploit silk’s 35 MJ m⁻³ toughness. Military, sports, and outdoor brands are increasingly incorporating spider silk yarns into ballistic liners, tents, and climbing ropes, contributing to the steady growth of this cornerstone segment. Films and coatings add incremental volumes in wound dressings and flexible electronics where ultra-thin, transparent layers serve as biobarriers. The synthetic spider silk market size for films remains modest but steady.

Nanocomposites and hydrogels exhibit the highest momentum at a 9.71% CAGR, powered by tissue-engineering scaffolds, 3D-printable resins and electrically conductive gels for biosensors. Incorporating graphene or carbon nanotubes elevates modulus fivefold while maintaining cytocompatibility, cementing use in next-generation flexible batteries. Rapid gelation chemistries facilitate point-of-care injectable meshes for cartilage repair, marking a leap over slow-curing collagen analogues.

By End-User Industry: Aerospace and Automotive Lift Growth

Textile and apparel retained 39.44% share in 2024, leveraging existing spinning and dyeing infrastructure for limited-edition outdoor jackets and luxury knitwear that fetch USD 600-plus price points. The synthetic spider silk market size for apparel should hold steady as premium positioning persists. Healthcare and biotechnology contribute double-digit share owing to rising approvals for silk-based sutures and regenerative meshes.

Aerospace and automotive outpace all segments at a 9.66% CAGR, propelled by Airbus and AMSilk’s cabin-panel program targeting 2027 entry-into-service. Composite spoilers and UAV wings fabricated with silk-epoxy prepregs demonstrate 15% weight savings and superior vibration damping relative to carbon fiber. Automotive interiors integrate silk-reinforced bioplastics that meet stringent odor and VOC thresholds, aligning with circular-economy mandates. Military and defense, though smaller, sustain high margins through ballistic applications validated by the Dragon Silk project. Sports equipment, robotics and academic R&D round out a diversified demand base that buffers the synthetic spider silk market against cyclical slowdowns.

Geography Analysis

Asia-Pacific generated 46.51% of global revenue in 2024 and continues to lead at a 9.58% CAGR on the back of China’s USD 4.17 billion biomanufacturing stimulus and Japan’s Smart-Cell Project grants. Dedicated biotech industrial parks in Suzhou and Tsuruoka streamline permitting and utilities for 10 m³-plus fermenters, shortening time-to-market for new grades. India’s BioE3 initiative funnels concessional loans and R&D tax credits that encourage domestic startups to license fermentation IP and establish local spinning mills, enlarging regional capacity.

North America demonstrates significant growth, driven by U.S. defense procurement and NIH funding for biomedical silk research. Commercial volumes remain constrained by higher energy and labor costs, yet pre-orders from athletic footwear brands and med-tech firms secure off-take agreements that justify incremental capacity. Canada offers carbon-neutral electricity, appealing to low-footprint silk plants.

Europe positions spider silk as a linchpin for circular-textile goals. Regulatory clarity under the EU Biotech Regulation 2025/124 fosters GMO protein commercialization, while Horizon Europe grants seed pilot projects converting food-grade waste sugars into silk proteins. However, energy-price volatility and lengthy environmental impact assessments slow large-scale builds. Currently, South America and the Middle East & Africa hold minimal market shares, still, Brazilian petrochemical firms and Gulf sovereign funds have announced feasibility studies exploring silk-composite production, indicating latent growth as technology costs retreat.

Competitive Landscape

The synthetic spider silk market remains highly consolidated. Spiber, AMSilk, Bolt Threads and Kraig Biocraft each pursue distinct technological paths that limit direct substitution. Spiber integrates vertically from fermentation to yarn-spinning and secures collaborations with luxury houses; its 500-ton Thai plant begins commercial deliveries in late 2025. AMSilk focuses on medical and industrial coatings, leveraging proprietary purification to attain endotoxin levels below 0.01 EU mg⁻¹—critical for implantables. Bolt Threads, following its 2024 SPAC listing, concentrates on Mylo-blend performance fabrics for apparel brands and is prototyping silk-based 3D-printing resins.

Kraig Biocraft’s transgenic silkworm platform differentiates through long filament length, attracting U.S. Army funding for ballistic fabrics. The firm registered the SpydaSilk trademark in 2025 to bolster consumer branding. Partnerships dominate strategic playbooks: Airbus with AMSilk, Patagonia with Spiber, and multiple sportswear pilots exemplify co-development that de-risks end-market entry. M&A chatter revolves around specialty-chemicals majors eyeing bolt-on acquisitions to integrate bio-based performance fibers into composites portfolios. Intellectual-property cross-licensing and standardization consortia are expected from 2026 onward as OEMs demand interoperable grades. Venture capital continues funneling into photosynthetic-bacteria startups positioned to leapfrog fermentation scalability issues.

Synthetic Spider Silk Industry Leaders

AMSilk GmbH

Bolt Threads

Kraig Biocraft Laboratories, Inc.

Seevix

Spiber, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kraig Biocraft Laboratories, Inc. has secured four registered trademarks for its SpydaSilk brand, marking a key step in its efforts to commercialize innovative spider silk technology and position SpydaSilk as a premium apparel brand. The company aims to strengthen its position in the synthetic spider silk market, driving growth and innovation.

- February 2025: Kraig Biocraft Laboratories, Inc. has announced a major advancement in its genetic research program. The company's research team has successfully increased both the complexity and size of its spider silk gene insert package, marking a significant step forward in enhancing material performance.

Global Synthetic Spider Silk Market Report Scope

| Microbial Fermentation |

| Transgenic Production |

| Chemical Synthesis and Polymer Engineering |

| Other Emerging Technologies |

| Fibers and Threads |

| Films and Coatings |

| Gels and Foams |

| Nanocomposites and Hydrogels |

| Military and Defense |

| Healthcare and Biotechnology |

| Textile and Apparel |

| Aerospace and Automotive |

| Academic and Industrial Research and Development |

| Sports, Outdoor and Luxury |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Microbial Fermentation | |

| Transgenic Production | ||

| Chemical Synthesis and Polymer Engineering | ||

| Other Emerging Technologies | ||

| By Product Type | Fibers and Threads | |

| Films and Coatings | ||

| Gels and Foams | ||

| Nanocomposites and Hydrogels | ||

| By End-user Industry | Military and Defense | |

| Healthcare and Biotechnology | ||

| Textile and Apparel | ||

| Aerospace and Automotive | ||

| Academic and Industrial Research and Development | ||

| Sports, Outdoor and Luxury | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the synthetic spider silk market in 2025?

The synthetic spider silk market size is valued at USD 1.95 billion in 2025.

What is the forecast CAGR for synthetic spider silk to 2030?

Market revenue is projected to grow at an 8.92% CAGR through 2030.

Which technology dominates commercial production?

Microbial fermentation accounts for 65.18% of 2024 revenue owing to superior scalability and cost profiles.

Which region leads in both share and growth?

Asia-Pacific commands 46.51% of global revenue and is advancing at a 9.58% CAGR through 2030.

What end-use segment is expanding fastest?

Aerospace and automotive applications are set to grow at 9.66% CAGR as OEMs seek lightweight composites.

What is the main barrier to wider adoption?

High production costs—currently around USD 300 per kg—remain the primary constraint until larger plants drive economies of scale.

Page last updated on: