Silk Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silk Protein Market Analysis by Mordor Intelligence

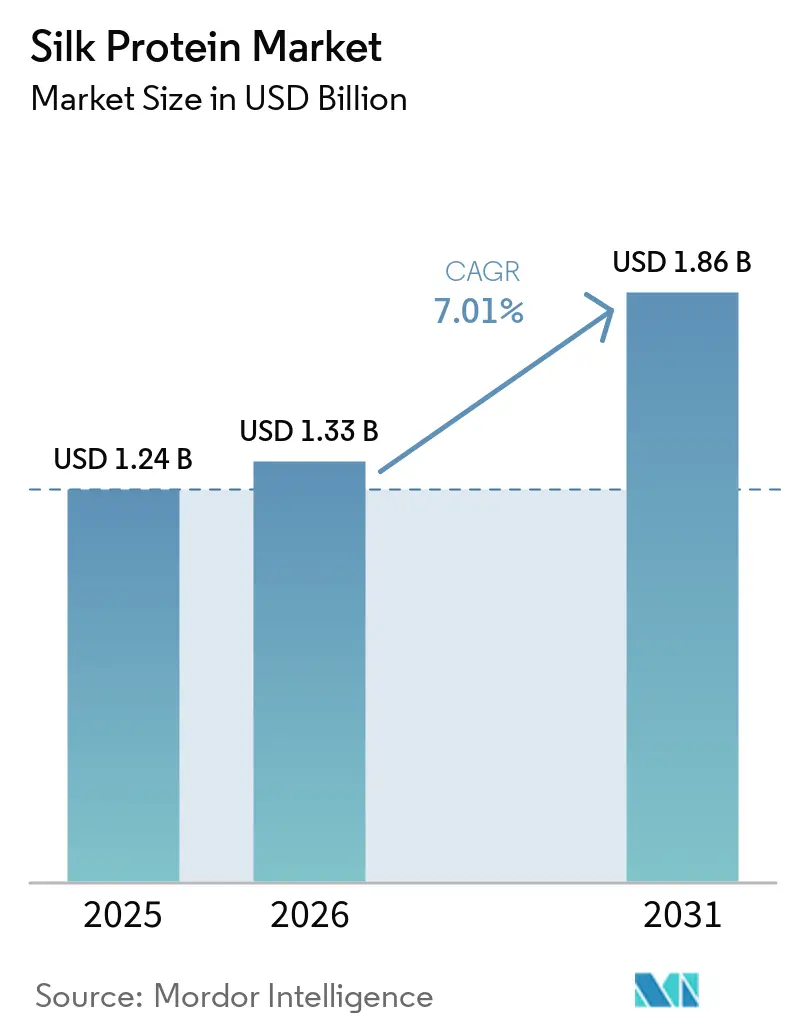

The Silk Protein Market size is expected to grow from USD 1.24 billion in 2025 to USD 1.33 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at 7.01% CAGR over 2026-2031. Consumer demand for natural, multifunctional ingredients is encouraging cosmetic and personal-care formulators to replace petrochemical-based polymers with silk peptides. Hospitals are validating fibroin dressings, which reduce post-operative complications and associated costs. Investments in precision-fermentation platforms are increasing due to their ability to deliver batch-consistent proteins without dependence on cocoon quality. The Asia-Pacific region is expanding both conventional sericulture and fermentation processes, maintaining its cost advantage while Europe and North America focus on near-shored supply to meet regulatory requirements. With financing rounds exceeding USD 50 million, leading developers are securing multi-year offtake contracts. These contracts lower unit costs and accelerate the transition from commodity extraction to engineered molecules.

Key Report Takeaways

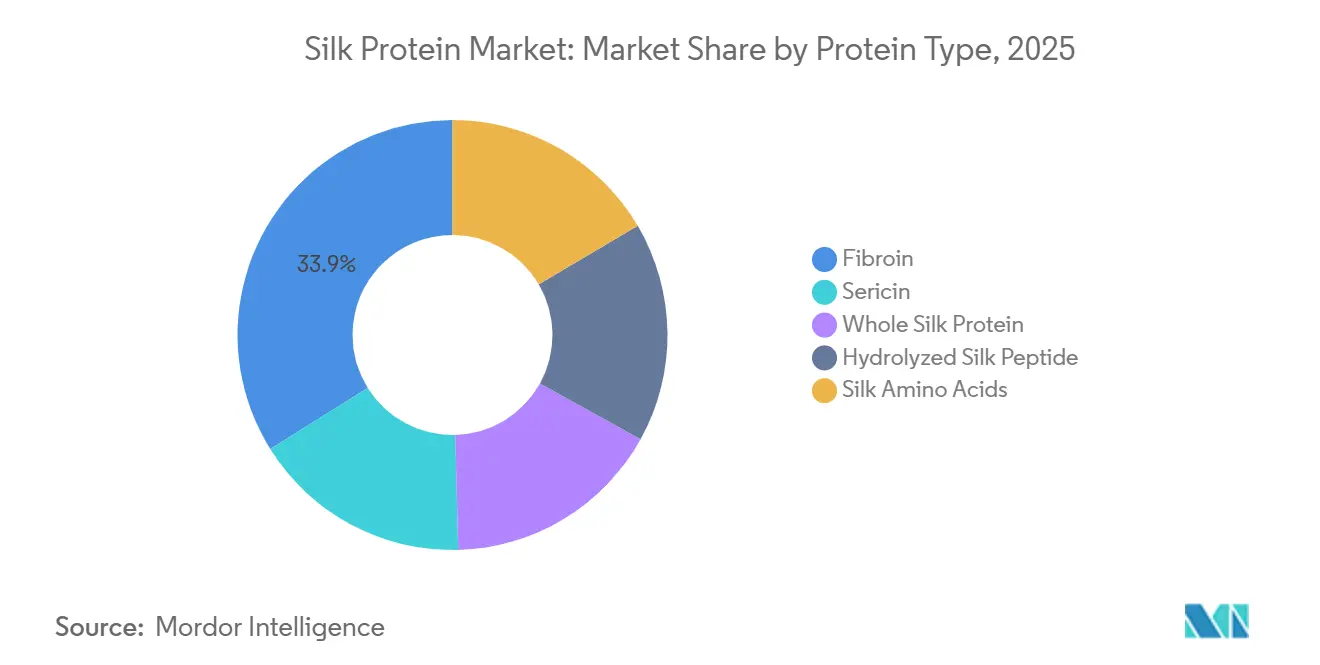

- By protein type, fibroin led with 33.89% of the silk protein market share in 2025; hydrolyzed silk peptide is projected to advance at a 7.78% CAGR through 2031.

- By form, powders accounted for 58.02% of volume in 2025, while nano-formulations are forecast to expand at an 8.02% CAGR through 2031.

- By application, cosmetics and personal care contributed 38.82% revenue in 2025, yet coatings and adhesives are projected to advance at an 8.22% CAGR to 2031.

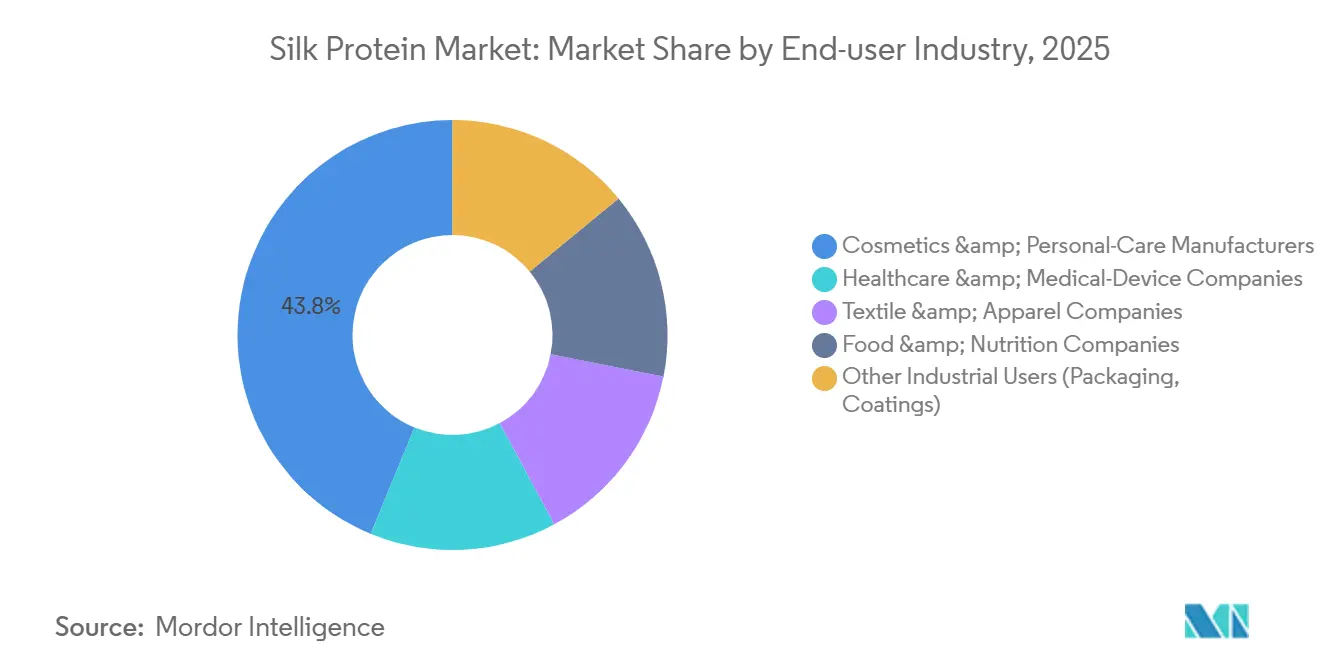

- By end-user industry, cosmetics manufacturers held 43.79% of demand in 2025, whereas healthcare companies are expected to record the highest growth at 7.77% CAGR to 2031.

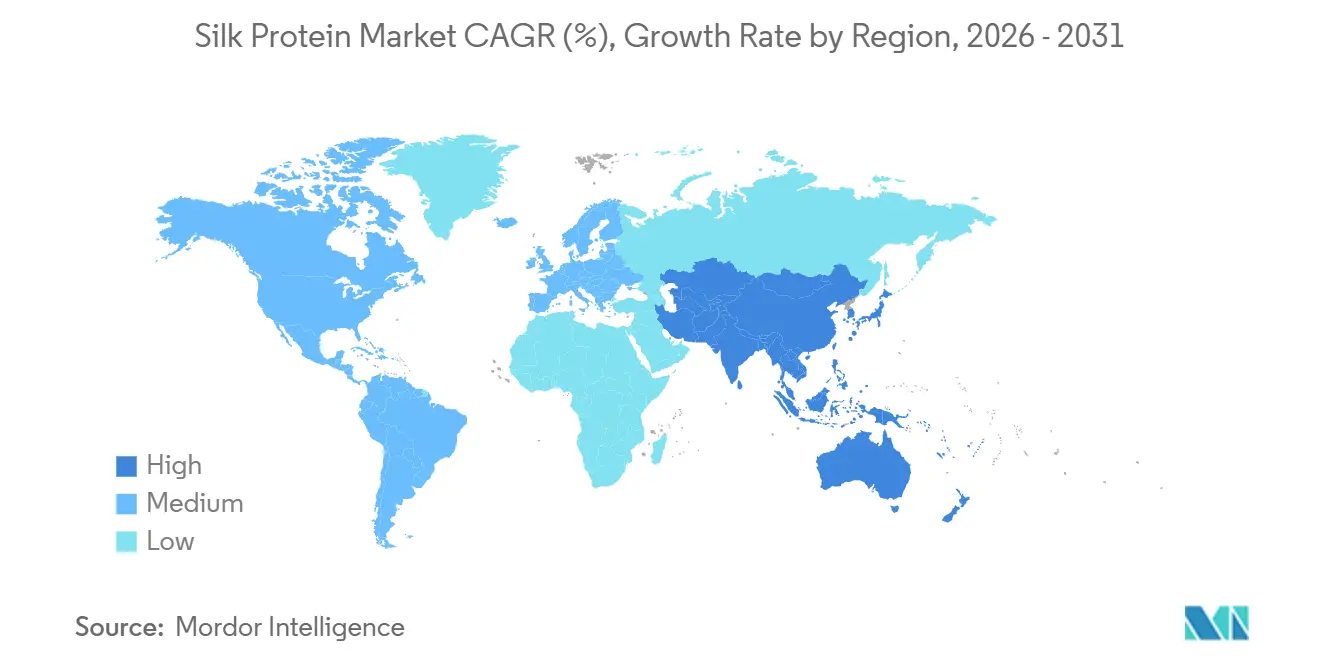

- By geography, Asia-Pacific dominated with a 41.03% share in 2025 and is poised to grow at an 8.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silk Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural and functional ingredients in cosmetics | +1.8% | Global, with premium penetration in North America, Europe, and Japan | Medium term (2-4 years) |

| Surging biomedical use (wound dressings, drug delivery) | +1.5% | North America and Europe (clinical adoption), Asia-Pacific (manufacturing scale-up) | Long term (≥ 4 years) |

| Rising interest in sustainable and biodegradable textiles | +1.3% | Europe (regulatory mandates), North America (brand commitments), Asia-Pacific (production capacity) | Medium term (2-4 years) |

| Regulatory push for microplastic alternatives in personal care | +1.0% | Europe (EU 2025 mandate), North America (state-level bans), spillover to ASEAN | Short term (≤ 2 years) |

| Breakthroughs in recombinant/microbial silk-protein production | +0.9% | North America and Europe (R&D hubs), Asia-Pacific (fermentation scale-up in Thailand, Japan) | Long term (≥ 4 years) |

| Expansion of plant-based recombinant silk platforms lowering CAPEX | +0.5% | Global, with early commercial traction in Europe and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Natural and Functional Ingredients in Cosmetics

Recognizable proteins are gaining importance as clean-beauty labels focus on proven performance in shorter testing cycles. A vegan fermentation-derived silk, launched in 2024, achieved a sevenfold reduction in visible pore area within fifteen minutes, surpassing synthetic polymers and meeting European Union (EU) claims substantiation rules. Legacy sericin, traditionally sourced from cocoons, is being reintroduced as an anti-wrinkle film former. Premium brands, priced at USD 98 per 30 milliliters, reported a replenishment rate exceeding 40% in 2026 e-commerce data. The dual approval of both topical and ingestible formats in Japan and South Korea enhances value capture, as a single extraction campaign services two profit centers. Retailers replacing banned microplastics are integrating silk peptides into existing formulation lines with minimal equipment changes, reducing conversion costs and accelerating compliance. The combination of efficacy data and sustainability narratives has expanded silk proteins from niche Asian stock-keeping units (SKUs) to mainstream Western assortments.

Surging Biomedical Use in Wound Dressings and Drug Delivery

Hospital buyers are transitioning from polypropylene meshes to silk fibroin scaffolds. These silk scaffolds demonstrate zero hypersensitivity reactions and result in savings of USD 465.91 per arthroplasty case[1]ChemSusChem, “Fine Structural Analysis of Degummed Fibroin Fibers,” chemistry-europe.onlinelibrary.wiley.com . A Phase III trial in Japan achieved 90% wound-bed preparation within two weeks, outperforming hydrocolloids and supporting reimbursement approval. Laboratory studies showed that silver-treated silk reduced Escherichia coli counts by 95%, meeting infection-control protocols without silver-ion toxicity. The tunable degradation profiles of fibroin films enable direct delivery of antibiotics or growth factors to wounds, reducing the need for systemic dosing. Additionally, the U.S. Food and Drug Administration's (FDA) "Generally Recognized as Safe" status for edible silk coatings has initiated pre-Investigational New Drug (pre-IND) discussions for oral drug carriers, indicating potential for silk-based therapeutics.

Rising Interest in Sustainable and Biodegradable Textiles

Spring 2026 fashion shows featured luxury brands presenting recombinant silk garments that used 97% less water than conventional silk, aligning with the Science Based Targets initiative's tier-three supply chain objectives. European brands are increasingly demanding certified microplastic-free materials. Engineered spider-silk fibers, which achieve abrasion resistance without shedding, are gaining traction. In China, factoryized silkworm rearing has scaled to forty thousand tons annually, ensuring consistent quality. Meanwhile, advancements in fermentation yields are bringing pricing parity closer for Western mills. Ethical-consumer segments are showing interest in peace-silk options, which harvest empty cocoons, expanding marketing opportunities. New International Organization for Standardization (ISO) definitions recognizing structural proteins with greater than or equal to 80% purity are enabling unified labeling, streamlining audits, and accelerating adoption.

Regulatory Push for Microplastic Alternatives in Personal Care

The EU's 2025 ban on intentionally added microplastics in rinse-off products has driven immediate reformulation efforts. Silk-based microcapsules, co-developed by the Massachusetts Institute of Technology (MIT) and BASF, provide fragrance retention while fully degrading in wastewater, ensuring compliance. Fragmented U.S. regulations, stemming from state bans in California and New York, are influencing market dynamics. Suppliers with global regulatory acceptance are securing national account tenders. Silk, with its established International Nomenclature Cosmetic Ingredient (INCI) name and decades of safe use, navigates regulatory pathways more efficiently than newer biopolymers. Silk's versatility is further demonstrated in the food sector, where silk-sericin composites extended tomato shelf life and complied with migrant-labor pesticide-residue standards, showcasing its applicability across multiple regulated markets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High extraction and purification costs | -1.2% | Global, with acute pressure in North America and Europe, where labor costs exceed those in the Asia-Pacific region | Medium term (2-4 years) |

| Variability in raw-silk quality and supply constraints | -0.9% | Asia-Pacific (sericulture dependence), spillover to global supply chains | Short term (≤ 2 years) |

| Allergenicity and regulatory uncertainty for ingestible silk peptides | -0.6% | North America and Europe (incomplete GRAS pathways), Asia-Pacific (faster approvals but fragmented standards) | Long term (≥ 4 years) |

| Limited scalability of sericulture outside Asia-Pacific | -0.4% | Latin America, the Middle East, and Africa (nascent sericulture infrastructure) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Extraction and Purification Costs

Purifying sericin from degumming wastewater involves energy-intensive processes such as dialysis and freeze-drying, which increase costs to USD 15-88 per kilogram, exceeding commodity pricing[2]Chemical & Engineering News, “Spiber Raises Funding for Fermented Fibers,” cen.acs.org . Small-scale extractors face challenges in securing capital for low-temperature alkali treatments that enhance tensile strength by 50%. Evonik's automated production line in Slovakia, operational since 2025, has not disclosed unit economics, indicating the continued need for premium market positioning. Approximately 50,000 tons of sericin are discarded annually. A technological advancement in cost-effective purification methods could significantly increase supply and reduce prices. While extraction remains more cost-efficient than fermentation, which has yet to surpass the 1,112 milligrams per liter (mg/L) benchmark, scaling extraction outside Asia is constrained by the lack of comparable labor cost advantages.

Variability in Raw-Silk Quality and Supply Constraints

In 2024, China experienced a loss of over 900,000 silkworm-rearing trays due to pesticide contamination, tightening the global cocoon supply. India increased its production to 38,913 metric tons in 2024 through government subsidies, but fiber uniformity continues to vary based on farm size and feeding practices. Controlled-feed factories in Zhejiang have improved consistency but require significant capital investment, which many regions lack. Experimental cellulose-nanofiber diets have shown potential to enhance fibroin strength but remain in the pre-commercial phase. Consequently, cosmetic and biomedical formulators are securing fermentation volumes at premium prices to mitigate supply risks, adding pressure on traditional sericulture regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Fibroin Dominance Masks Peptide Momentum

In 2025, fibroin captured 33.89% of the silk protein market, primarily in textile yarns and implantable scaffolds. Hydrolyzed silk peptide, projected to grow at a 7.78% compound annual growth rate (CAGR), benefits from its soluble formats that easily disperse in serums and beverages. Whole silk protein, valued for its high molecular integrity in protective coatings, sees modest volumes due to its cost. Sericin, previously discarded, now finds commercial use in anti-aging films, supported by licensing from DSM-Firmenich. Silk amino acids, penetrating deeper skin layers, secure a premium position in lineage-care products.

Recombinant technologies are redefining boundaries, allowing preset molecular weights in silico. AMSilk’s 139.9-kilodalton (kDa) biomimetic variant offers cashmere-like softness, while Spiber’s library caters to injection-moldable resins. Peptide adoption gains traction from a Korean trial, highlighting elevated natural killer (NK)-cell activity at a daily dose of 7.5 grams. Thus, the choice of protein type will increasingly hinge on functional performance over extraction methods.

By Form: Powder Incumbency Confronts Nano-Form Disruption

In 2025, powders dominated with 58.02% of the volume, a testament to the established spray-dry infrastructure in China and India. While powders boast a multi-year shelf life and easy freight, they fall short on bioavailability compared to finer particles. Nano-formulations, projected to grow at an 8.02% CAGR, benefit from precision electrospinning, producing fibers below 100 nanometers (nm) that expedite wound closure. Liquids, favored in private-label original equipment manufacturer (OEM) channels for their batching simplicity, face limitations in natural-label claims due to preservatives.

Despite electrospinning throughput rarely exceeding kilograms per hour, capping nano-form supply, the performance premium draws biomedical firms seeking targeted adhesion. While powders will remain a staple for bulk textiles, nano-forms are poised to dominate emerging medical and high-end cosmetic niches, indicating a bifurcated supply chain.

By Application: Cosmetics Lead as Coatings Accelerate

In 2025, cosmetics secured 38.82% of the revenue, supported by an established International Nomenclature of Cosmetic Ingredients (INCI) listing and consumer familiarity. Coatings and adhesives, however, are set to outpace with a forecasted 8.22% CAGR through 2031, driven by European Union (EU) microplastic regulations favoring silk-based films for packaging. Biomedical applications are expanding, utilizing zero-reaction fibroin meshes to reduce surgical readmissions. Luxury apparel brands leverage recombinant fibers for their narrative on animal welfare, while food coatings await regulatory approvals in North America and Europe.

By 2026, silk-tannic-acid adhesives achieved lap-shear values close to 420 kilopascals (kPa), rivaling cyanoacrylates but offering full biodegradability. Electronics manufacturers are testing silk barriers on wearable sensors, ensuring durability for up to 15 wash cycles. While cosmetics maintain their lead, they are set to share the growth spotlight with packaging films as regulations tighten.

By End-User Industry: Healthcare Gains on Cosmetic Incumbency

In 2025, cosmetic brands represented 43.79% of the demand, utilizing silk for its moisture retention, film-forming capabilities, and sensory appeal. However, healthcare firms are on the rise, projected to grow at a 7.77% CAGR, supported by increasing clinical evidence for fibroin in wound-care products. Textile brands are adopting recombinant silks to achieve circularity targets, though widespread adoption depends on achieving price parity. Operators in food and nutrition are proceeding cautiously, as Generally Recognized as Safe (GRAS) recognition remains incomplete in the United States. However, in late 2025, India’s regulator advanced sericin protein to Stage 7.

Surgeons are drawn to the cost advantages of fibroin over synthetic meshes, and infection-control committees value the non-cytotoxic properties of silver-laden silk. While the luxury segment of apparel absorbs current premiums, the mass-market fast fashion sector is awaiting scale-up.

Geography Analysis

In 2025, Asia-Pacific accounted for a 41.03% market share and is projected to grow at an 8.32% compound annual growth rate (CAGR) through 2031. This growth is primarily driven by China, which represents 53% of the global raw silk market, and by India's modernization initiatives supported by federal funding. Countries such as Thailand, Japan, and South Korea are establishing fermentation plants, strengthening the region's supply chain for the biomedical and cosmetic industries. In North America, the transition from import reliance to domestic production is evident, with Canon Virginia's new production line set to launch in 2026, supported by state incentives. In Europe, regulatory frameworks play a significant role; for example, Evonik's facility in Slovakia produces several tons of spinning-grade powder monthly, meeting the demand of the local premium textile market.

North America's market share, though smaller, is increasing as brands prioritize onshore, animal-free supplies. Canon Virginia's new production line highlights this cross-sector interest. Additionally, academic spin-outs in California are achieving fermentation yields nearing 900 milligrams per liter (mg L-¹). U.S. state subsidies aimed at rural job creation are positioning silk biotechnology as a key economic development driver. In Canada, pilot plants in Ontario are combining corn-based feedstocks with green hydroelectricity to produce zero-carbon silk inputs.

Europe is balancing stringent environmental regulations with its industrial capabilities. The European Union's (EU) microplastic ban is driving demand for biodegradable film-formers, and Evonik's Slovak facility is addressing this need by supplying regional cosmetics manufacturers through long-term tolling agreements. France's Ajinomoto fermentation hub, equipped with 100 cubic meter (m³) reactors, integrates Asian expertise into the European market. Additionally, Eastern European governments are offering tax holidays for biotech parks to attract further investments.

South America and the Middle East face challenges such as limited mulberry cultivation and insufficient capital for bioreactors. However, Asia-Pacific's combination of cocoon farming and industrial fermentation positions it for sustained growth, surpassing other regions. Protectionist sourcing regulations, however, may lead to redundant capacity in Western markets.

Competitive Landscape

The silk protein market is moderately concentrated. Top players include AMSilk GmbH, Evonik Industries AG, Bolt Threads Inc., Croda International plc, and dsm-firmenich. Recombinant technology leaders secure venture capital to scale precision fermentation for consistent production, while Asian extractors maintain cost efficiency by operating near cocoon farms. Evonik’s partnership strategy enables ingredient multinationals to manage risks while maintaining quality assurance oversight, a model adopted by fragrance company Givaudan for its Silk-iCare line.

Strategic initiatives focus on funding and offtake agreements. In September 2025, AMSilk raised EUR 52 million (USD 60.74 million) to establish a Slovak facility for producing multi-ton spinning-grade powder using renewable energy. Spiber secured JPY 10 billion (USD 0.06 billion) to expand its Thai Brewed Protein plant's capacity threefold and enter the packaging resins market. Canon Inc., a leader in imaging technology, has diversified into silk bio-production, highlighting the material's cross-industry applications. Spiber’s patent portfolio, comprising 673 documents covering blended yarns to protein nanofiber processes, creates significant entry barriers for competitors.

Growth opportunities exist in coatings, adhesives, and ingestibles. Silk-tannic-acid glues show potential for surgical applications, while sericin peptides are pending final Generally Recognized as Safe (GRAS) approval in the United States. Suppliers capable of reducing purification costs or improving fermentation titers are likely to gain market share rapidly. Collaborations in luxury apparel serve as promotional platforms, while mainstream textiles remain focused on cost considerations. Overall, companies that integrate upstream fermentation with downstream application expertise are well-positioned to capitalize on expanding profit opportunities.

Silk Protein Industry Leaders

AMSilk GmbH

Croda International Plc

Bolt Threads Inc.

dsm-firmenich

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: TIBD Co., Ltd. entered into a strategic alliance with FINECO Ltd. to commercialize Silk Crystal fibroin delivery systems, a technology derived from silk protein, for cosmetic formulators in Thailand and the ASEAN (Association of Southeast Asian Nations) region.

- September 2025: Evonik Industries AG and AMSilk GmbH have commissioned a renewable-powered production line in Slovakia, designed to produce several tons per month of spinning-grade silk proteins. This facility represents a significant step in the sustainable production of bioengineered silk proteins, which are used in various industrial and consumer applications.

Global Silk Protein Market Report Scope

Silk protein, an amino-acid-rich natural protein, is derived from the cocoons of silkworms, primarily the Bombyx mori species. It consists of 70-80% structural fibroin and 20-30% adhesive sericin. Silk protein is utilized in skincare for moisture retention, hair care for enhancing shine, and in biomedical engineering as a biodegradable material.

The silk protein market is segmented by protein type, form, application, end-user Industry, and geography. By protein type, the market is segmented into fibroin, sericin, whole silk protein, hydrolyzed silk peptide, and silk amino acids. By form, the market is segmented into powder, liquid, and nano-formulation. By application, the market is segmented into personal care and cosmetics, biomedical and pharmaceutical, textiles and fabrics, food and dietary supplements, and coatings and adhesives. By end-user Industry, the market is segmented into cosmetics & personal-care manufacturers, healthcare & medical-device companies, textile & apparel companies, food & nutrition companies, and other industrial users (packaging, coatings). The report also covers the market size and forecasts for silk protein in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Fibroin |

| Sericin |

| Whole Silk Protein |

| Hydrolyzed Silk Peptide |

| Silk Amino Acids |

| Powder |

| Liquid |

| Nano-formulation |

| Personal Care and Cosmetics |

| Biomedical and Pharmaceutical |

| Textiles and Fabrics |

| Food and Dietary Supplements |

| Coatings and Adhesives |

| Cosmetics & Personal-Care Manufacturers |

| Healthcare & Medical-Device Companies |

| Textile & Apparel Companies |

| Food & Nutrition Companies |

| Other Industrial Users (Packaging, Coatings) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Protein Type | Fibroin | |

| Sericin | ||

| Whole Silk Protein | ||

| Hydrolyzed Silk Peptide | ||

| Silk Amino Acids | ||

| By Form | Powder | |

| Liquid | ||

| Nano-formulation | ||

| By Application | Personal Care and Cosmetics | |

| Biomedical and Pharmaceutical | ||

| Textiles and Fabrics | ||

| Food and Dietary Supplements | ||

| Coatings and Adhesives | ||

| By End-user Industry | Cosmetics & Personal-Care Manufacturers | |

| Healthcare & Medical-Device Companies | ||

| Textile & Apparel Companies | ||

| Food & Nutrition Companies | ||

| Other Industrial Users (Packaging, Coatings) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the silk protein market expected to grow by 2031?

The Silk Protein Market size is expected to increase from USD 1.24 billion in 2025 to USD 1.33 billion in 2026 and reach USD 1.86 billion by 2031, growing at a CAGR of 7.01% over 2026-2031.

Which segment will show the highest growth through 2031?

Coatings and adhesives are forecast to register the fastest 8.22% CAGR as brands replace microplastic films with biodegradable silk coatings.

Why is Asia-Pacific the largest regional contributor?

The region combines low-cost sericulture with expanding fermentation plants in China, India, Thailand, and Japan, giving it a 41.03% share in 2025 and the quickest 8.32% CAGR.

What drives healthcare adoption of silk proteins?

Clinical studies show silk fibroin dressings eliminate hypersensitivity reactions and save USD 465.91 per surgery, encouraging hospitals to switch from synthetic meshes.

Page last updated on: