Mineral Wool Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

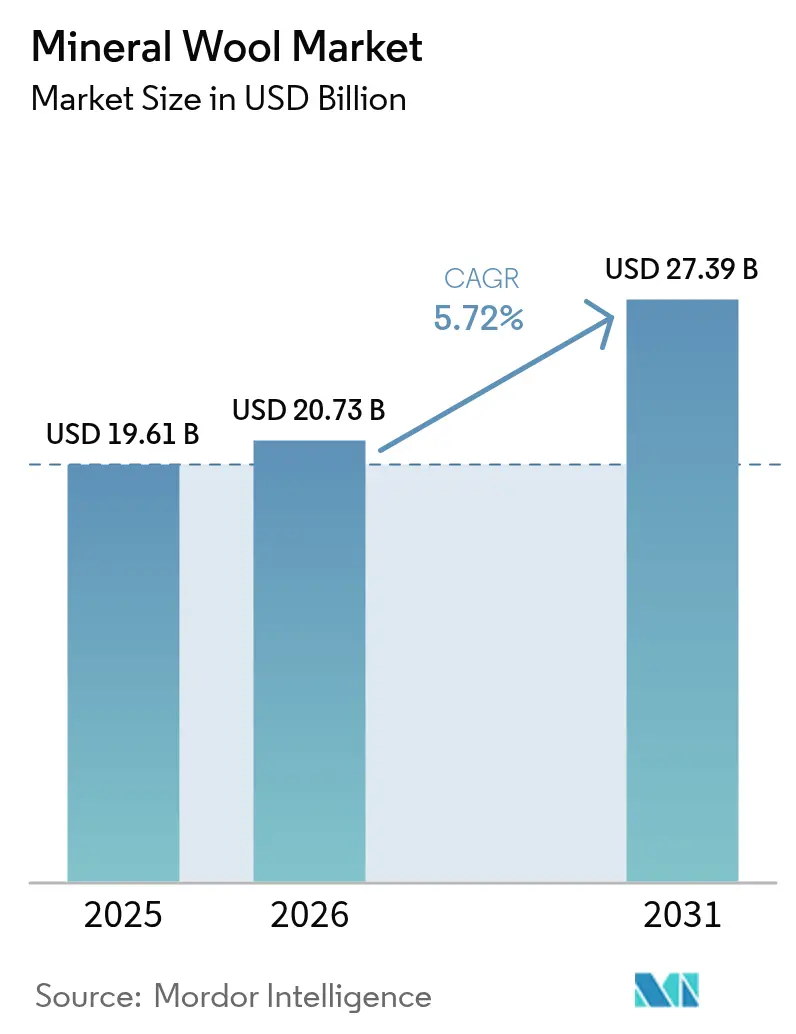

| Market Size (2026) | USD 20.73 Billion |

| Market Size (2031) | USD 27.39 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mineral Wool Market Analysis by Mordor Intelligence

Mineral Wool market size in 2026 is estimated at USD 20.73 billion, growing from 2025 value of USD 19.61 billion with 2031 projections showing USD 27.39 billion, growing at 5.72% CAGR over 2026-2031. This underscores strong momentum around decarbonized buildings, stricter fire safety mandates, and the push for a circular economy. Momentum stems from four forces: 1) continuous tightening of energy-performance codes that elevate non-combustible insulation as the default wall-cavity choice, 2) litigation risk in high-rise façades that accelerates the switch away from polymer foams, 3) a supply-side shift toward recycled-content glass wool that cuts embodied carbon and opens public-procurement doors, and 4) outsized demand from electric-vehicle battery enclosures that need mats rated above 800°C. Competitive strategies center on vertical integration into raw materials, including glass, basalt, and binders, while challengers target premium niches, such as aerogel-hybrid boards. Opportunities arise in closed-loop recycling, ultra-thin insulation for land-constrained cities, and modular prefab panels that slash on-site labor.

Key Report Takeaways

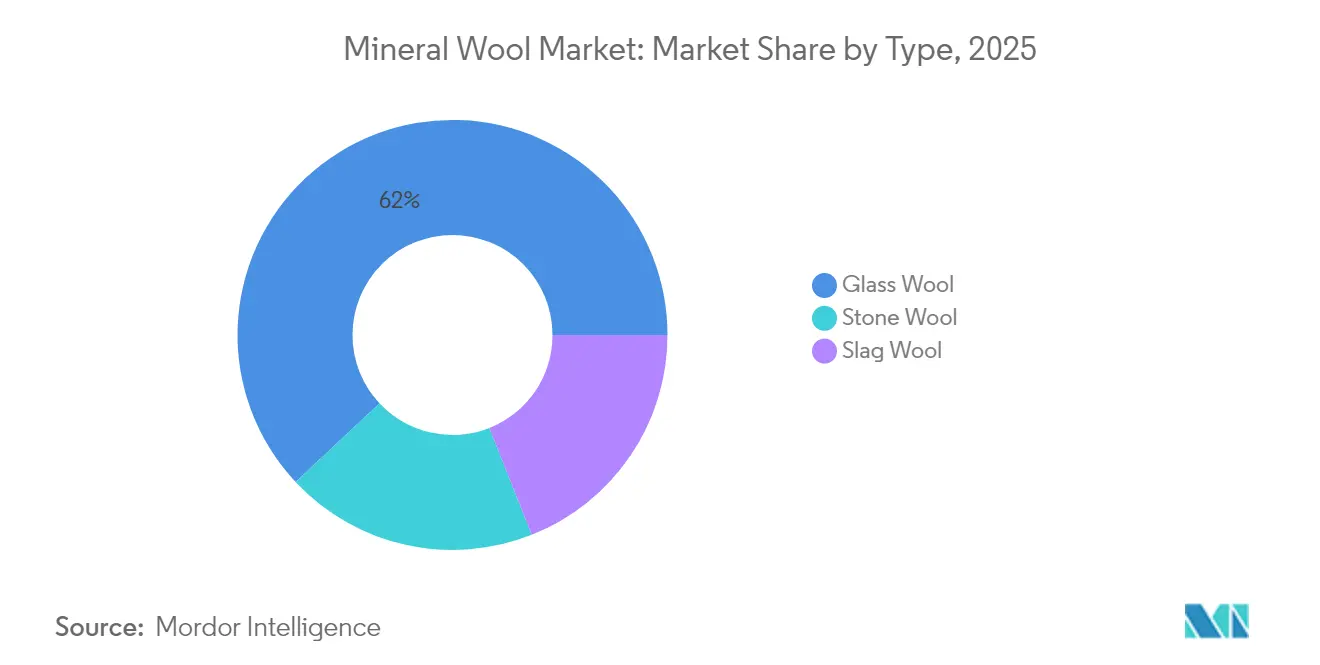

- By type, glass wool led with a 61.98% market share of the mineral wool market in 2025 and is projected to advance at a 6.78% CAGR through 2031.

- By product type, blanket formats captured 67.12% of the mineral wool market size in 2025; this product type is also the fastest-growing, with a 6.22% CAGR through 2031.

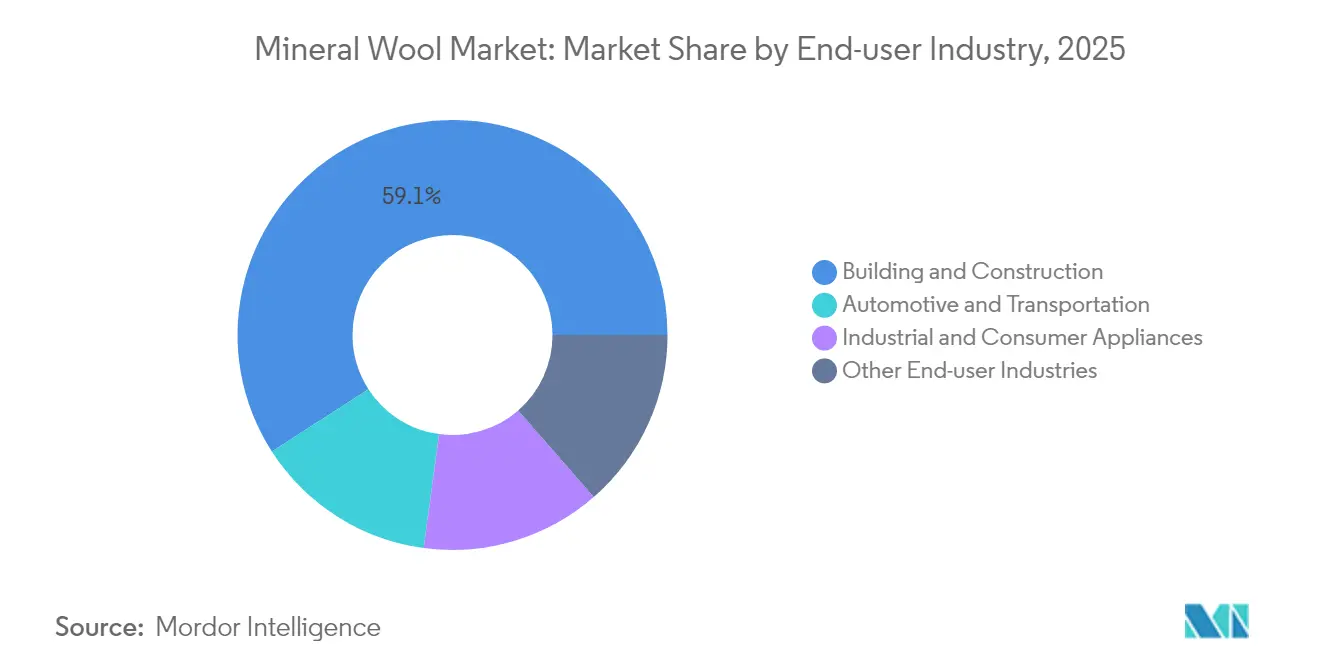

- By end-user industry, the building and construction sector contributed 59.12% of demand in 2025, and it is expected to expand at a 6.1% CAGR through 2031.

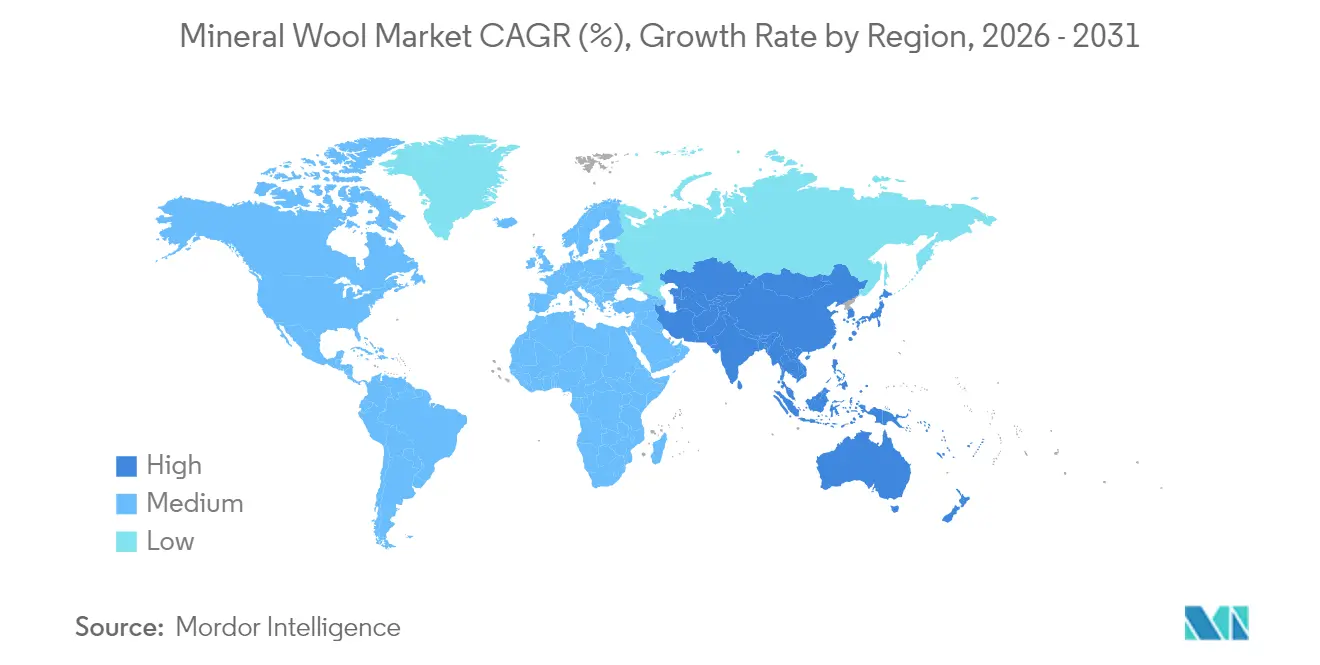

- By geography, the Asia-Pacific region accounted for 41.78% of the mineral wool market in 2025, and it is projected to post the fastest 6.25% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mineral Wool Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Building and construction boom in energy-efficient envelopes | +2.1% | Global (China, India, EU-27, North America) | Medium term (2-4 years) |

| Mandatory energy-performance and fire-safety regulations | +1.8% | EU-27, UK, China, India, Australia | Short term (≤2 years) |

| Tightening green-building codes in emerging Asia-Pacific | +1.3% | China, India, ASEAN | Medium term (2-4 years) |

| Circular-economy push for mineral-wool recycling streams | +0.6% | EU-27 | Long term (≥4 years) |

| Rise of modular prefab panels accelerating demand | +0.9% | North America, Northern Europe, Australia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Building And Construction Boom In Energy-Efficient Envelopes

Global decarbonization policies are steering retrofit budgets toward mineral-wool-based envelopes that pair air-sealing membranes with smart glazing. Regulation 2024/1681 in the EU obliges member states to renovate 3% of public buildings yearly, translating to a EUR 275 billion insulation opportunity this decade. India’s 2024 Energy Conservation Building Code overlays prescriptive U-values across 27 climate zones, while China’s DG/TJ08-205-2024 locks in 75% energy savings for new projects in Shanghai. Modular construction—scaling at 6.2% CAGR through 2024—now embeds mineral-wool cores into factory-built wall cassettes, trimming on-site labor by 40% and compressing installation schedules[1]Modular Building Institute, “2024 Modular Construction Report,” modular.org.

Mandatory Energy-Performance And Fire-Safety Regulations

Litigation over combustible façades propels the mineral wool market as regulators outlaw polymer foams in tall buildings. The UK’s 2024 update to Approved Document B bans non-A-rated insulation above 18 m, a benchmark mirrored by Australia’s National Construction Code 2025 Performance Requirement FP1.4. EU Regulation 2024/3110 extends reaction-to-fire tests to sandwich panels, closing loopholes that once favored polyurethane cores. Parallel limits on VOCs in phenolic binders, as outlined in the Industrial Emissions Directive 2024/1785, reduce foam-production costs, narrowing the price gap with mineral wool[2]European Parliament, “Regulation 2024/1681 on the Energy Performance of Buildings,” europa.eu.

Tightening Green-Building Codes In Emerging Asia-Pacific

Emerging Asia is leapfrogging legacy rules by embedding envelope thermal modeling into permit processes. India links floor-area-ratio bonuses to four-star GRIHA certification, mandating cavity insulation in most climate zones. Vietnam’s 2024 Circular 08/TT-BXD imposes energy audits for commercial buildings larger than 2,500 m², while Indonesia subsidizes mineral wool in 50,000 affordable homes. Guangzhou now requires thermal-performance reports that benchmark insulation thicknesses of 60–100 mm before project approval, signaling a shift toward performance-based design.

Circular-Economy Push For Mineral-Wool Recycling Streams

Europe produced 2.5 million tons of mineral-wool waste in 2020, yet recycling stood below 10%. Austria’s landfill ban from 2027 forces producers to build take-back loops, targeting a 30% recycling rate by 2030, which will add EUR 8–12 per m² for demolition contractors, as per BML.GV.AT. Rockwool and Knauf operate pilot plants in the Netherlands and Sweden that re-blend cleaned wool into virgin melts at a 15–20% ratio, reducing furnace energy consumption by 25%. New EU End-of-Waste criteria finalized in 2024 designate clean mineral wool as a secondary raw material, trimming cross-border shipping costs by 40%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and carcinogenicity concerns over respirable fibres | −0.7% | Global (EU-27, North America) | Medium term (2-4 years) |

| Price-driven substitution by low-cost polymer foams | −1.2% | ASEAN, Latin America, Middle East & Africa | Short term (≤2 years) |

| Volatile basalt/coke/binder input prices | −0.5% | Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Health And Carcinogenicity Concerns Over Respirable Fibres

Ambiguity around bio-solubility fragments market access. EU Note Q exempts modern fibers from carcinogen labeling if the weighted half-life in lung fluid is under 40 days, yet OSHA still mandates hazard warnings on fibers below 3 µm. Insurance premiums for U.S. contractors rose 15–25% in 2024 due to liability concerns. 3M’s 2024 patent for ≥3 µm ceramic-glass fibres achieves 1,000°C performance while sidestepping respirable-dust generation, hinting at next-generation non-respirable products.

Price-Driven Substitution By Low-Cost Polymer Foams

Mineral wool trades at a 50–60% premium to EPS and a 20–30% premium to PIR because melting basalt or cullet at 1,400 °C is an energy-intensive process. Gas-linked input spikes in late 2023 lifted rock-wool list prices by 4.8–5.9% across Europe, while petrochemical foams enjoyed 12% cheaper feedstocks. In Southeast Asia, EPS controls 65% of low-rise insulation; mineral wool penetration is <15% beyond Singapore and Malaysia, where fire codes are stricter.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Glass Wool Growth Outpaces Stone Wool

Glass wool represented 61.98% of 2025 demand and continues to expand at a 6.78% CAGR, giving it the clear lead in the mineral wool market. The segment benefits from recycled-content mandates; Recticel integrated 19.2% post-consumer cullet in 2024 and targets 25% by 2030, reducing embodied carbon by 1.2 kg CO2-eq per kg of product. Stone wool, prized for its service temperatures exceeding 600 °C in industrial settings, grows more slowly at 5.55% because its density of 120–160 kg/m³ inflates logistics costs by 40% compared with glass wool batts. Slag wool remains inexpensive in Eastern Europe and parts of China due to the abundance of blast-furnace slag; however, as steel mills shift to electric-arc technology, this outlet is expected to shrink, restraining its 4.12% CAGR growth.

Second-order effects reinforce glass wool’s ascendancy. Owens Corning reported USD 1.02 billion in insulation revenue for Q3 2024, a 6% increase, driven by glass-wool shipments across the southern United States, where code-mandated R-30 walls have become the default. Conversely, Rockwool’s Asia-Pacific sales declined 5% as Chinese builders shifted to glass-wool blankets for easier retrofitting. Ultra-thin battery-pack mats, built on glass-ceramic composites patented by 3M, create fresh high-margin niches that stone wool cannot meet owing to density constraints.

By Product Type: Blankets Dominate Residential Retrofits

Blanket insulation controlled 67.12% of 2025 volume and is tracking a 6.22% CAGR to 2031, reinforcing its dominance in the mineral wool market. Retrofits in houses built before 1990 drive demand for blankets because compressible batts can be easily installed into irregular stud bays without the need for adhesives, reducing installation labor by 30–40%. Board products, with an 18.96% share, serve curtain-wall façades and sub-grade walls where a compressive strength of more than 40 kPa is mandatory. They log a 5.63% CAGR as rainscreen cladding becomes mainstream in commercial builds.

Loose-fill commands 10.48% share, supported by a 5.86% growth path lifted by US federal tax credits that reimburse 30% of attic-insulation spend up to USD 1,200 annually. Saint-Gobain’s Isover brand introduced a bio-based binder in 2024 that reduces formaldehyde emissions by 60%, alleviating concerns about indoor air quality in schools and hospitals. Smaller niches—including stitched mats and wired blankets for marine bulkheads—collectively hold 3.44% but command premium pricing due to weight and fire-resistance needs.

By End-User Industry: Buildings Lead, EVs Accelerate

Building and construction accounted for 59.12% of mineral wool in 2025 and is projected to rise by 6.1% annually to 2031, maintaining its position as the anchor customer. North American orders leapt 8% in Rockwool’s Q3 2024 books on the back of Inflation Reduction Act subsidies targeting envelope retrofits, yet Europe stayed flat as German permits fell 20% and France postponed EPBD enforcement to mid-2025. India’s green-materials market, meanwhile, is sprinting toward USD 38 billion next year, drawing seven domestic wool makers into the GRIHA catalogue.

Lithium-ion battery packs can reach temperatures of up to 800°C in thermal runaway events, and glass-ceramic mats outperform polymer foams in both temperature tolerance and non-combustibility. Industrial and consumer appliances are squeezed by aerogel blankets that achieve equal R-values at one-third the thickness. Marine, aerospace, and other niche sectors supply the remaining 13.59%, with composite-integrated solutions chipping away at conventional wool usage.

Geography Analysis

The Asia-Pacific region dominated with 41.78% of global demand in 2025 and is projected to advance at a 6.25% CAGR to 2031, reinforcing its position at the center of the mineral wool market. Shanghai’s DG/TJ08-205-2024 code mandates 75% energy savings, effectively prescribing continuous exterior insulation, while Beijing and Shenzhen issue similar drafts. India’s revised ECBC lists prescriptive wall and roof U-values, pairing them with FAR incentives, which catalyze the uptake of mineral wool in commercial high-rises. Japan budgeted JPY 120 billion in 2024 to retrofit pre-1980 homes, and South Korea’s Green Remodeling Fund covers up to 50% of insulation costs, spurring blanket orders for multi-family towers.

In North America, Rockwool earmarked DKK 1.3 billion for new lines in Mississippi and upgrades in Ontario, ensuring local supply as demand accelerates. Owens Corning leverages its backward-integrated glass capacity to protect its 31.4% insulation EBITDA margin, even as soda-ash prices fluctuate. Canada’s 2024 budget sets aside CAD 4.4 billion for home-energy rebates, while Mexico now insists on thermal insulation in social-housing zones with >1,500 heating- or cooling-degree-days.

In Europe, construction softness in Germany, France, and Italy chills demand, though Regulation 2024/1681 obliges 3% annual retrofit of public buildings, equating to EUR 275 billion insulation spend to 2030. Eastern Europe and the Nordics offset some weakness: Poland’s Cigacice plant expansion adds 50,000 t of stone-wool capacity, and Sweden buys recycled-content boards to fulfill circular-procurement rules.

Saudi mega-projects NEOM and Qiddiya specify non-combustible insulation in high-rise towers, drawing Kingspan and Saint-Gobain investments in Dammam. Brazil now enforces roof R-values in five bioclimatic zones under Programa Casa Verde e Amarela, opening blanket demand across São Paulo and Rio Grande do Sul. The UAE updated its Green Building Regulations in 2024, obliging envelope insulation on all conditioned buildings beyond 500 m².

Competitive Landscape

The Mineral Wool market is moderately concentrated. Rockwool operates 51 plants across 39 countries and booked EUR 2.96 billion in nine-month revenue, with a 23.4% EBITDA margin, thanks to in-house basalt quarries and coke furnaces. Owens Corning generated USD 1.02 billion in Q3 2024 insulation sales and sustains a 31.4% segment margin via captive glass-fiber lines that buffer silica-sand volatility. Saint-Gobain’s High Performance Solutions arm nudged 3.3% growth against flat group sales by pivoting to aerogel and vacuum-insulated panels that deliver R-50-plus per inch, doubling mineral wool yet commanding triple-digit premiums. Niche innovators fill whitespace. Aspen-Aerogels assets boost Saint-Gobain’s ultra-thin portfolio, while TECHNONICOL’s 2024 BIM plugin slashes design time 40% for Russian and Eastern European contractors.

Mineral Wool Industry Leaders

Saint-Gobain

ROCKWOOL A/S

Owens Corning

Knauf Insulation

Johns Manville

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Knauf Insulation Romania opened a new glass mineral wool production facility in Târnăveni, Mureș County. With an annual production capacity of 75,000 tonnes, the factory can insulate approximately 200,000 homes each year.

- September 2025: Rockwool Group is set to inaugurate its new manufacturing plant in Cheyyar, Tamil Nadu. Slated to commence operations by Q2/2026, this facility will eclipse Rockwool’s current plant in Gujarat, positioning itself as a pivotal production center for stone wool insulation products in India.

Global Mineral Wool Market Report Scope

Mineral wool is a fiber made of natural or synthetic minerals or metal oxides. The synthetic form is generally referred to as synthetic materials, including fiberglass, ceramic fibers, and stone wool. The mineral wool market is segmented by type, product type, end-user industry, and geography. By type, the market is segmented into glass wool, stone wool, and slag wool. By product type, the market is segmented into board, blanket, loose wool, and other product types. By end-user industry, the market is segmented into automotive and transportation, building and construction, industrial and consumer appliances, and other end-user industries. The report also covers the market size and forecasts for the geotextile market in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of revenue (USD million).

| Glass Wool |

| Stone Wool |

| Slag Wool |

| Board |

| Blanket |

| Loose Wool |

| Other Product Type |

| Automotive and Transportation |

| Building and Construction |

| Industrial and Consumer Appliances |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Glass Wool | |

| Stone Wool | ||

| Slag Wool | ||

| By Product Type | Board | |

| Blanket | ||

| Loose Wool | ||

| Other Product Type | ||

| By End-user Industry | Automotive and Transportation | |

| Building and Construction | ||

| Industrial and Consumer Appliances | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the mineral wool market in 2026?

The mineral wool market size is USD 20.73 billion in 2026 and is projected to reach USD 27.39 billion by 2031.

Which product type holds the largest share?

Blanket insulation leads with 67.12% of 2025 volume, thanks to labor savings in residential retrofits.

Why is glass wool growing faster than stone wool?

Glass wool benefits from recycled-content mandates and lower logistics costs, supporting a 6.78% CAGR through 2031.

What drives mineral wool demand in Asia-Pacific?

Stricter energy codes in China and India, plus retrofit subsidies in Japan and South Korea, fuel a 6.25% regional CAGR.

Who are the top players in mineral wool products?

Rockwool International, Owens Corning, Saint-Gobain, Knauf Insulation, and Kingspan together generate about 55–60% of global sales.

Page last updated on: