Switzerland Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

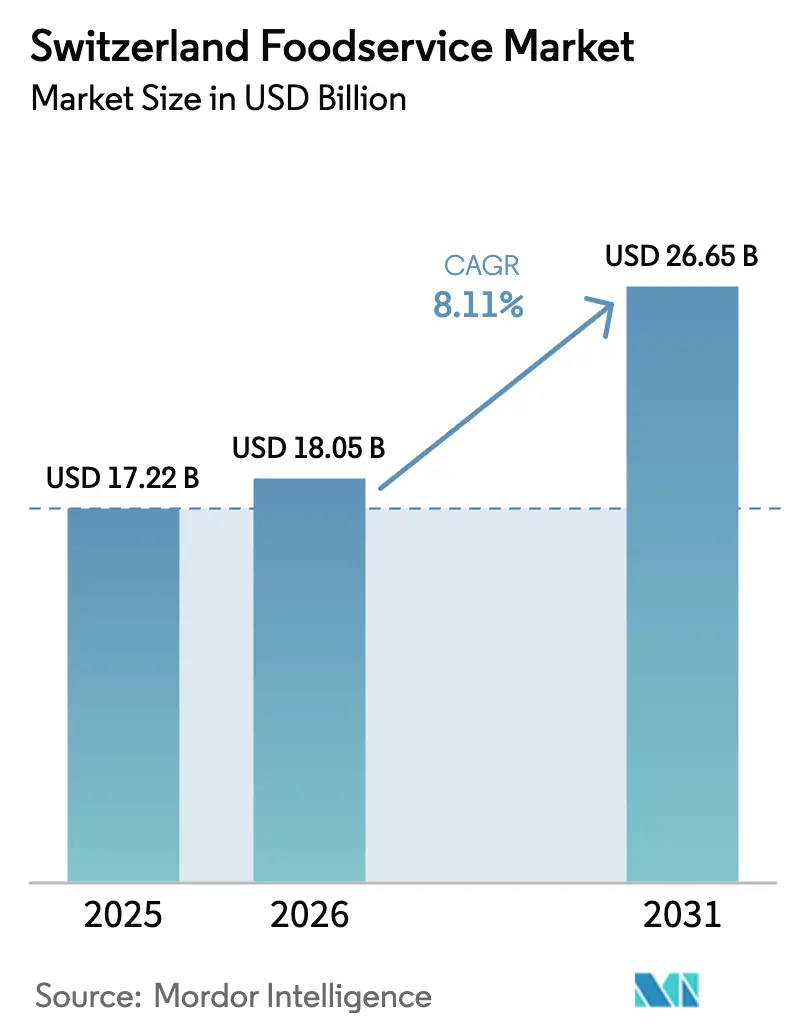

| Base Year Market Size (2025) | USD 17.22 Billion |

| Market Size (2026) | USD 18.05 Billion |

| Market Size (2031) | USD 26.65 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

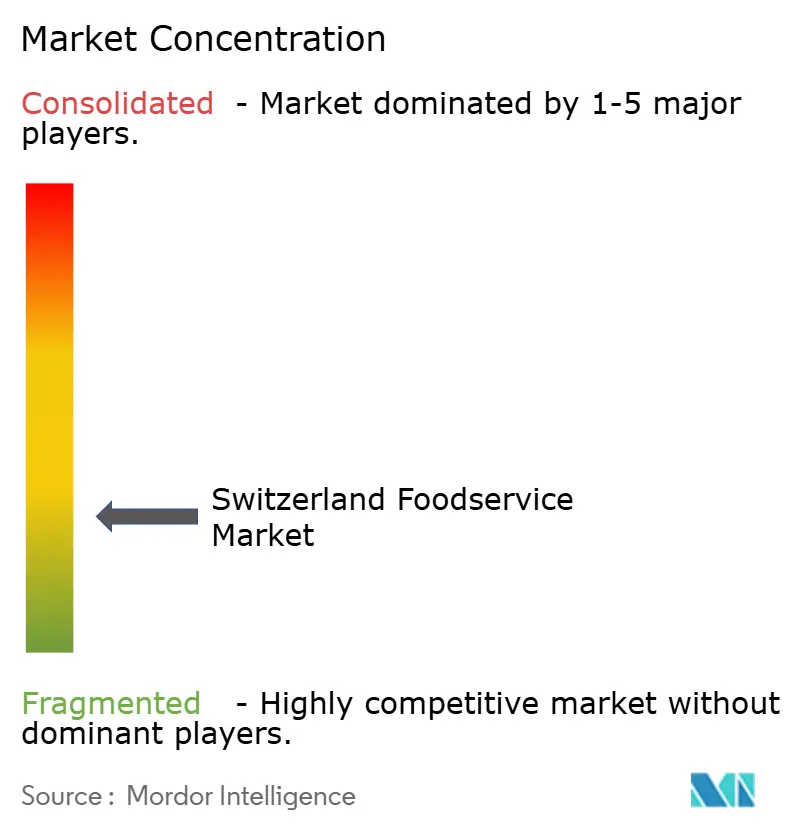

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Switzerland Foodservice Market Analysis by Mordor Intelligence

The Switzerland Foodservice Market size is projected to be USD 17.22 billion in 2025, USD 18.05 billion in 2026, and reach USD 26.65 billion by 2031, growing at a CAGR of 8.11% from 2026 to 2031. Several structural factors drive Switzerland's expansion, including its high per-capita income, increasing urbanization, and a rise in domestic overnight stays. According to the World Bank, urbanization in the central plateau reached 85% in 2024[1]Source: World Bank, "Urban population (% of total population) - Switzerland", worldbank.org. These elements collectively drive consistent consumer traffic to both restaurants and delivery services. Although European tourist arrivals have remained flat, a rise in inbound tourism has provided a cushion, while Switzerland's multicultural resident base, characterized by individuals with diverse migration backgrounds, continues to fuel demand for a variety of global cuisines. Additionally, technological advancements are playing a crucial role in shaping the market. For instance, TWINT, with its 4.2 million users, is facilitating cash-free transactions, while AI-powered demand-planning software is effectively reducing food waste in institutional settings. Furthermore, the introduction of pilot robots is transforming delivery operations, adding another dimension to the market's growth.

Key Report Takeaways

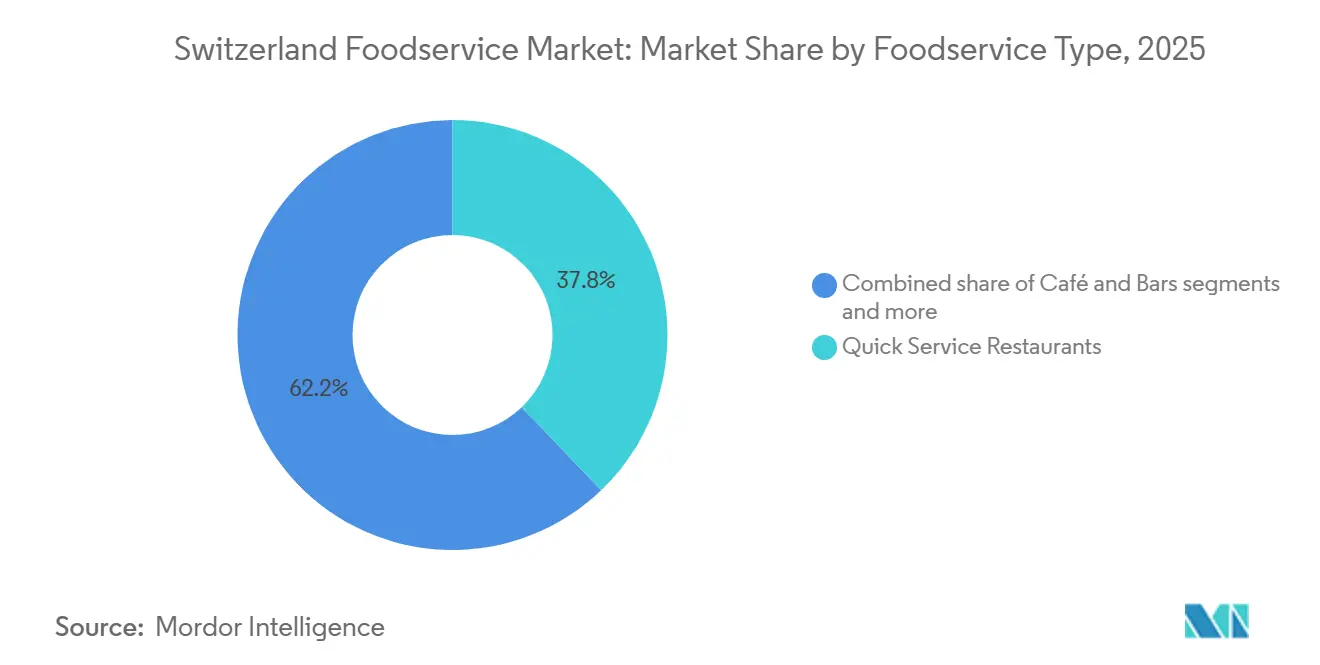

- By foodservice type, quick service restaurants held a 37.84% Switzerland foodservice market share in 2025, while cloud kitchens are projected to post an 8.21% CAGR to 2031.

- By outlet, independent operators commanded 78.51% of the Switzerland foodservice market size in 2025, but chained formats are set to advance at a 7.98% CAGR over the forecast horizon.

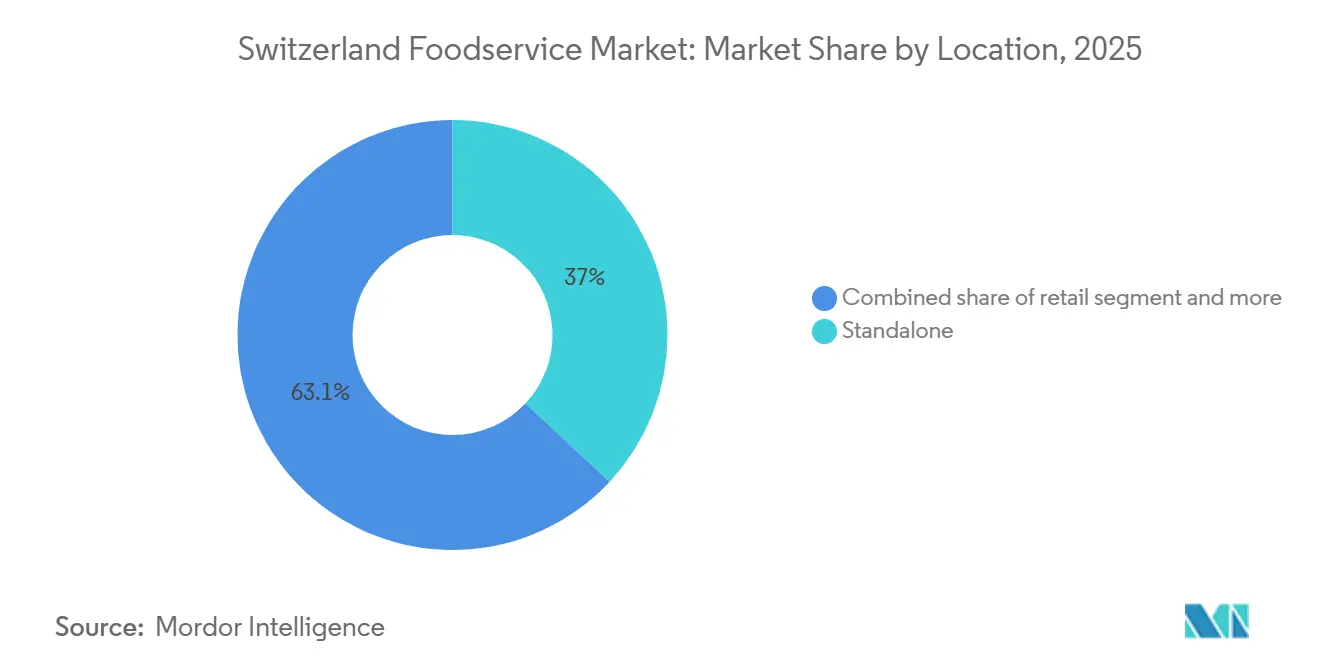

- By location, standalone sites accounted for 36.95% of revenue in 2025, and lodging-based dining is expected to expand at an 8.02% CAGR to 2031.

- By service type, dine-in generated 56.37% of spending in 2025, whereas delivery is forecast to climb at an 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Switzerland Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid café culture and coffee-chain proliferation | +1.2% | National, with concentration in Zurich, Geneva, Basel, Bern, Lausanne | Medium term (2-4 years) |

| Strong tourism industry boosts demand, especially in alpine and urban areas | +1.3% | Alpine regions (Graubünden, Valais, Bernese Oberland), urban centers (Zurich, Geneva, Lucerne) | Short term (≤ 2 years) |

| Urbanization increases reliance on convenient food options for busy lifestyles | +0.9% | Central plateau metropolitan areas, accounting for 85% of population | Long term (≥ 4 years) |

| High disposable income driving premium and specialty formats | +1.1% | National, with premium concentration in Zurich, Geneva, Zug cantons | Medium term (2-4 years) |

| Technology integration like AI menus and contactless payments enhances efficiency | +0.8% | National, early adoption in urban centers and institutional catering | Short term (≤ 2 years) |

| Population growth and immigration create diverse consumer bases | +0.7% | National, with highest immigration inflows in Zurich, Geneva, Basel | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid café culture and coffee-chain proliferation

Switzerland holds the position of Europe's third-largest exporter of roasted coffee by volume, a distinction that supports its dynamic domestic café industry. This ecosystem features intense competition between specialty coffee roasters and international chains striving to capture market share. Over recent years, consumer preferences have shifted significantly, with espresso emerging as the preferred choice among coffee drinkers, surpassing the traditional café crème in popularity. Cappuccinos and lattes have also gained traction, reflecting evolving tastes. Capitalizing on this trend of premiumization, Starbucks has announced plans to expand its presence in Switzerland by operating 90 outlets by 2026. However, the rising cost of out-of-home coffee has prompted many consumers to prepare coffee at home, leading to increased pressure on café operators to maintain profitability. Those unable to differentiate themselves through unique ambiance or specialized offerings face significant challenges in sustaining margins. Additionally, younger demographics, particularly Gen Z, are consuming less coffee overall. This group shows a clear preference for milk-based beverages and ready-to-drink coffee formats, diverging from traditional espresso-based drinks. As a result, café operators are being compelled to diversify their menus to cater to these changing preferences and remain competitive in the evolving market landscape.

Strong tourism industry boosts demand, especially in alpine and urban areas

Switzerland's renowned tourism industry, centered around its iconic Alps, such as the Matterhorn and Lucerne, and vibrant urban destinations like Zurich and Geneva, continues to thrive. This growth is fueled by a steady influx of international and domestic visitors who are increasingly seeking diverse dining experiences. These range from cafes and fine dining establishments to quick-service outlets, with a strong preference for local flavors, healthier food options, and seamless digital interactions. Consequently, the food service market in Switzerland is experiencing significant expansion. The Federal Statistical Office reported that the Swiss hotel sector recorded an unprecedented 24.4 million overnight stays during the summer tourist season, spanning May to October 2024, marking the highest level ever observed [2]Source: Federal Statistical Office, "Tourist accommodation in the 2024 summer season", bfs.admin.ch. At an altitude of 3,100 meters, the 3100 Kulmhotel Gornergrat exemplifies the integration of tourism and food services. It operates several food and beverage outlets, including Glacier Alpine Kitchen, saycheese!, Sky Lounge, Tiger Bowl, and Panorama self-service. These venues not only provide half-board packages but also curate unique experiential dining events, such as the highly popular “Dining with the Stars.” However, the concentration of tourism in specific alpine valleys and urban gateways results in pronounced seasonality. Operators in regions like Graubünden, Valais, and Bernese Oberland rely heavily on winter sports activities and summer hiking traffic to mitigate the quieter periods during the shoulder seasons.

Urbanization increases reliance on convenient food options for busy lifestyles

Urbanization in Switzerland is transforming the food service market. As urban areas become busier, residents increasingly rely on convenient, ready-to-eat meals, driving demand for quick-service restaurants (QSRs), cafes, and food delivery services. Technology, including apps and online ordering, significantly influences this shift. Additionally, a rising focus on healthier, organic options, shaped by sustainability and wellness trends, is accelerating growth, particularly in major cities. According to the World Bank, Switzerland's urban population reached 6,714,777 in 2024 [3]Source: World Bank, "World Urbanization Prospects UN", worldbank.org. Urbanization is primarily concentrated along the central plateau corridor, linking cities such as Geneva, Lausanne, Bern, Zurich, and Basel. In these areas, factors like average commute times and the prevalence of dual-income households are boosting demand for grab-and-go meals and delivery formats. Valora's Avec chain, which operates over 290 convenience outlets, introduced "The Kitchen" fresh-meal concept in May 2024. The chain plans to open seven additional locations by the end of the year and has implemented unstaffed Sunday operations through mobile app ordering. Cloud kitchens are also leveraging the high urban density. Furthermore, the Swiss Nutrition Strategy 2025-2032 advocates for plant-based and sustainable diets. This aligns with urban consumers' environmental preferences but requires investments in menu reformulation.

High disposable income driving premium and specialty formats

In Switzerland, high disposable incomes are significantly driving the demand for premium and specialty foods. Consumers are increasingly inclined to allocate more of their earnings toward dining out, indulging in unique culinary experiences such as fine dining, opting for health-conscious food choices, and purchasing gourmet or imported items. This trend has led to the growth of diverse dining formats, including cafes, upscale restaurants, and innovative hybrid models, all of which continue to thrive despite Switzerland's dependence on food imports. In 2024, the country's GDP per capita is projected to reach an impressive USD 103,998.2, firmly establishing Switzerland as one of the wealthiest nations globally [4]Source: World Bank, "GDP per capita- Switzerland", worldbank.org. This economic prosperity not only supports a sustained demand for premium dining experiences but also fosters a growing interest in specialty ingredients. Additionally, Swiss consumers exhibit a strong awareness of sustainable coffee certifications and demonstrate a willingness to pay higher prices for certified coffee beans. This behavior highlights a critical trend: in urban and affluent markets, ethical sourcing practices can effectively justify elevated price points, reflecting the value placed on sustainability and quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High labour and real-estate costs pressuring margins | -0.9% | National, acute in Zurich, Geneva, Basel, Zug | Short term (≤ 2 years) |

| Food-price inflation linked to import dependence | -0.6% | National, affecting all operators reliant on imported ingredients | Medium term (2-4 years) |

| Tight immigration caps restricting hospitality workforce | -0.5% | National, with acute shortages in alpine seasonal resorts | Long term (≥ 4 years) |

| Strong Swiss franc dampening cross-border leisure spend | -0.4% | Border regions (Basel, Geneva, Ticino), alpine resorts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High labour and real-estate costs pressuring margins

High construction and rental costs significantly influence market dynamics. Businesses, facing the brunt of these elevated costs, find themselves compelled to adapt or face potential financial strain. Full-service restaurants (FSR) have grappled with declining value sales over the past year. In Switzerland, cities like Zurich, Geneva, and Basel boast some of Europe's priciest real estate. This reality pushes operators to either adopt delivery-first models or implement premium pricing strategies to maximize revenue per square meter. McDonald's, with a USD 272 million investment program slated for 2024-2026, is prioritizing the modernization of its existing outlets over greenfield expansions. This shift underscores the challenges posed by site acquisition costs, which deter new builds. While cloud kitchens sidestep real estate costs by forgoing customer-facing spaces, they do so at the expense of heightened risk. These kitchens often grapple with delivery platform commissions, which can soar to 25-30% of the order value. In a bid to counteract rising costs, businesses are actively seeking methods to curtail food waste and refine raw material procurement.

Food-price inflation linked to import dependence

Switzerland's dependence on imported food products creates vulnerabilities for operators, particularly in the face of currency fluctuations and supply chain disruptions, even as food prices experience deflation. Since June 2025, the Swiss franc has appreciated by 1.9% on a trade-weighted basis, significantly increasing the costs of imports priced in euros and dollars. This rise in import costs exerts substantial pressure on operators' profit margins, especially for those unable to adjust their menu prices in a deflationary market environment. Smaller operators, who lack the negotiating power of larger competitors, are confronted with a challenging decision: either absorb the increased costs, which further compresses their already narrow margins, or raise prices, risking a decline in customer demand and sales volumes. This dilemma is compounded by persistently negative consumer confidence levels, which remain between -35 and -42, making it increasingly difficult for operators to sustain profitability and maintain market share in such a challenging economic climate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Outpace Traditional Formats

Cloud Kitchen formats are projected to grow at a strong 8.21% CAGR through 2031, making them the fastest-growing foodservice type. This growth is primarily driven by Future Kitchens AG, which launched a delivery-first infrastructure in March 2023, covering Zurich, Basel, Lucerne, Bern, Geneva, Lausanne, and over 20 additional cities. Quick Service Restaurants (QSRs) accounted for a notable 37.84% market share in 2025. McDonald's, with its 180 outlets, aims to reach 200 in the medium term, while new players are also entering the market. Wendy's is planning a re-entry, and Five Guys is expanding beyond Geneva and Lausanne into German-speaking regions. Full Service Restaurants (FSRs) are diversifying their offerings with cuisines such as Asian, European, Latin American, Middle Eastern, and North American, catering to Switzerland's population with immigrant backgrounds. Café and Bars are leveraging Switzerland's position as Europe's third-largest roasted coffee exporter. Starbucks plans to operate 90 outlets by 2026, and specialty coffee shops are increasingly appearing in urban areas.

Urbanization patterns are driving the transition to delivery-first models. With 85% of the population residing in the central plateau, dense catchment areas enable cloud kitchens to achieve better unit economics compared to traditional restaurants by avoiding dine-in real estate costs. However, delivery platforms impose commissions of 25-30%, redirecting these real estate savings to third-party intermediaries and squeezing operator margins. QSR formats rely on standardized menus and supply chains to sustain profitability despite rising wage costs, while FSR operators focus on offering unique experiential dining to differentiate themselves.

By Outlet: Chained Operators Gain Share Through Technology and Scale

Chained outlets are anticipated to grow at a CAGR of 7.98% through 2031. However, independent outlets maintained a significant 78.51% market share in 2025, highlighting Switzerland's market, characterized by family-owned businesses and regional specialists. Valora, operating over 290 convenience outlets, has introduced "The Kitchen" fresh-meal concept and unstaffed Sunday operations managed via a mobile app, illustrating how chains utilize technology to reduce reliance on labor.

Independent operators face notable structural challenges. They often lack the scale needed to secure favorable supplier terms, struggle to distribute technology investments across multiple locations, and encounter difficulties in attracting talent. Despite these obstacles, independents stand out with localized menus, personalized service, and strong community ties, attributes that chains find hard to replicate. The adoption of TWINT has enabled even small independents to accept contactless payments, narrowing the technological gap with chains. Meanwhile, compliance costs associated with the Swiss Nutrition Strategy 2025-2032 and the Action Plan to halve food waste by 2030 are more easily absorbed by chains. This dynamic may accelerate consolidation as independents exit the market.

By Location: Lodging-Based Foodservice Capitalizes on Alpine Tourism

Investments in alpine resorts and enhancements in urban hotel food and beverage services are driving the lodging-based foodservice sector, which is expected to grow at a CAGR of 8.02% through 2031. Standalone locations accounted for a notable 36.95% share of the market in 2025. Tourism operators are capitalizing on this growth by partnering with lodging providers to offer half-board packages and distinctive dining experiences. However, the sector faces challenges due to seasonality: alpine resorts experience significant staffing shortages during peak winter and summer seasons, a problem aggravated by immigration caps that limit non-EU worker inflows.

Retail spaces in shopping centers and travel hubs, such as airports and train stations, benefit from high foot traffic but face pressure from premium rents that reduce profit margins. Standalone restaurants, which do not rely on captive demand, must differentiate themselves through unique cuisine, appealing ambiance, or strategic location. This differentiation is essential, particularly in an environment of declining consumer confidence. Similarly, leisure venues tied to entertainment and sports facilities attract event-driven demand but struggle with low utilization during off-peak periods.

By Service Type: Delivery Accelerates as Robotics Reduce Last-Mile Costs

Delivery service is growing at an 8.22% CAGR through 2031. Despite this rapid growth, dine-in services are expected to maintain a significant presence, holding a dominant 56.37% market share in 2025. This trend highlights Switzerland's high per capita income and the population's strong preference for experiential dining, which emphasizes ambiance and service quality. The takeaway service, on the other hand, offers a middle ground by combining convenience with cost efficiency. Operators can avoid platform commissions, which typically range between 25-30%, while catering to customers who value speed and efficiency over the dining experience.

Dine-in services continue to command premium pricing due to the added value of the overall dining experience. Meanwhile, cloud kitchens, such as Future Kitchens AG, have adopted a different approach by completely eliminating dine-in infrastructure. These businesses focus their investments on advanced kitchen equipment and efficient delivery logistics to streamline operations. However, the rise of delivery services has brought environmental concerns to the forefront, particularly regarding food waste and the environmental impact of delivery packaging. To address these issues, the Action Plan aims to reduce the environmental footprint of delivery packaging by 50% by 2030.

Geography Analysis

Switzerland's single-country market demonstrates significant regional differences influenced by linguistic, topographic, and economic factors. The German-speaking central plateau, which includes Zurich, Bern, Basel, and Lucerne, has a high population density that attracts QSR chains, cloud kitchens, and institutional catering, driven by urbanization and the presence of corporate headquarters. In contrast, the French-speaking Romandy region, encompassing Geneva, Lausanne, and the Vaud canton, favors full-service restaurants that reflect Francophone culinary traditions. Geneva, in particular, benefits from its role as a hub for international organizations, which supports its business dining sector.

In the Alpine regions, Graubünden, Valais, and Bernese Oberland, luxury resorts such as The Alpina Gstaad and 3100 Kulmhotel Gornergrat drive the expansion of lodging-based foodservice. These resorts, featuring multiple food and beverage outlets, cater to ultra-high-net-worth guests. Alpine destinations, reliant on long-haul travelers, outperform border regions that are more vulnerable to fluctuations in European demand. Urban centers benefit from urbanization and a diverse population with immigrant backgrounds, which sustains demand for a variety of ethnic cuisines. Conversely, rural areas face workforce shortages, a challenge worsened by immigration caps and seasonal tourism patterns.

Border regions like Basel, near Germany and France, Geneva, close to France, and Ticino, bordering Italy, face challenges from outbound dining competition. Swiss residents often take advantage of the strong franc to dine abroad at lower costs, diverting business from standalone restaurants in these border cantons. However, lodging and travel destinations within Switzerland successfully attract incoming tourists. While the Federal Food Safety and Veterinary Office enforces consistent food safety standards nationwide, the implementation of the Swiss Nutrition Strategy varies by canton. Urban cantons such as Zurich lead the way with initiatives like "Food Save Zurich," aimed at reducing food waste.

Competitive Landscape

The Switzerland foodservice market remains highly fragmented, with independent outlets commanding a significant share despite growing chain operators. Institutional caterers, such as SV Group and Gategroup, maintain stability by securing long-term contracts with universities, hospitals, corporate clients, and airlines, shielding them from fluctuations in consumer discretionary spending. Technology is transforming the competitive landscape: chains utilize TWINT's QR-code payment network, implement AI-driven demand prediction tools like FOOD2050, which reduces CO2 emissions by 15% annually, and test robotic delivery systems like RIVR, capable of climbing stairs at 15 km/h. Meanwhile, independent operators stand out by offering localized menus, personalized service, and distinctive experiential concepts.

Switzerland's food industry includes key players such as Coop Gruppe Genossenschaft, SV Group AG, and Candrian Catering AG, alongside international brands like McDonald's Corporation and Starbucks Corporation. These companies are driving innovation by introducing plant-based products, sustainable packaging, and digital ordering systems to enhance customer satisfaction. They are also demonstrating adaptability by adopting cloud kitchen models and integrating advanced technologies into food preparation and delivery processes.

To strengthen their market position, companies are increasingly forming strategic partnerships with local suppliers, food technology firms, and delivery platforms. Their growth strategies include organic expansion through new outlet openings and inorganic growth via acquisitions, with a focus on premium locations in urban areas and transport hubs. Opportunities exist in cloud kitchens offering ethnic cuisines to Switzerland's 41% immigrant-background population, delivery-first formats targeting densely populated urban centers, and sustainability-certified products aligned with the Swiss Nutrition Strategy 2025-2032.

Switzerland Foodservice Industry Leaders

-

Candrian Catering AG

-

Coop Gruppe Genossenchaft

-

SV Group AG

-

McDonald's Corporation

-

Starbucks Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Starbucks has launched new branches in Central Switzerland, emphasizing 'resource-conserving design and sustainable solutions' to reduce its ecological footprint.

- April 2024: McDonald's has launched seven new restaurants in Switzerland. The company is actively seeking additional locations and inviting franchise inquiries as part of its expansion strategy.

- September 2023: McDonald's has introduced the McPlant to its menu to address the growing popularity of flexitarianism in Switzerland.

Switzerland Foodservice Market Report Scope

Foodservice refers to the business of preparing, serving, and selling ready-to-eat food and drinks for immediate consumption, encompassing diverse establishments like restaurants, cafes, catering, and institutions, focusing on providing meals outside the home for profit or service. The Switzerland foodservice market is segmented by foodservice type, outlet, location, and service type. By foodservice type, the market is segmented into café and bars, cloud kitchen, full-service restaurants, and quick-service restaurants. By outlet, the market is segmented into chained and independent. By location, the market is segmented into leisure, lodging, retail, standalone, and travel. By service type, the market is segmented into dine-in, takeaway, and delivery. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Cafe and Bars | By Cuisine | Bars and Pubs |

| Cafe | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafe and Bars | By Cuisine | Bars and Pubs |

| Cafe | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms