Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

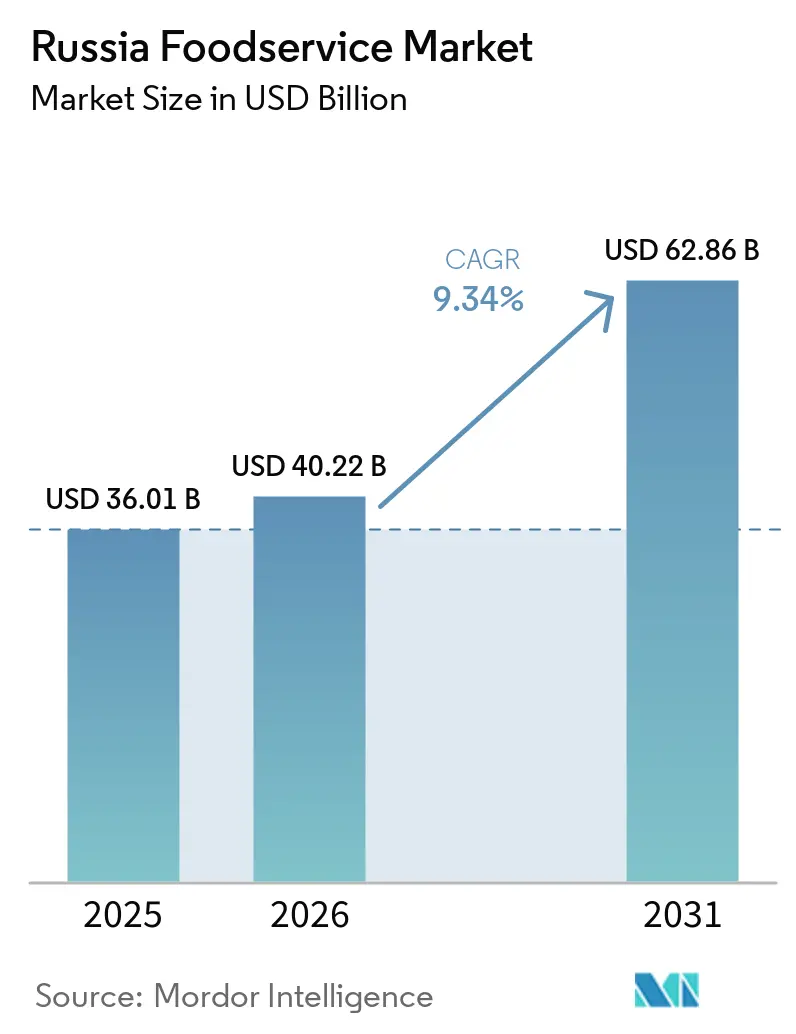

| Base Year Market Size (2025) | USD 36.01 Billion |

| Market Size (2026) | USD 40.22 Billion |

| Market Size (2031) | USD 62.86 Billion |

| Growth Rate (2026 - 2031) | 9.34% CAGR |

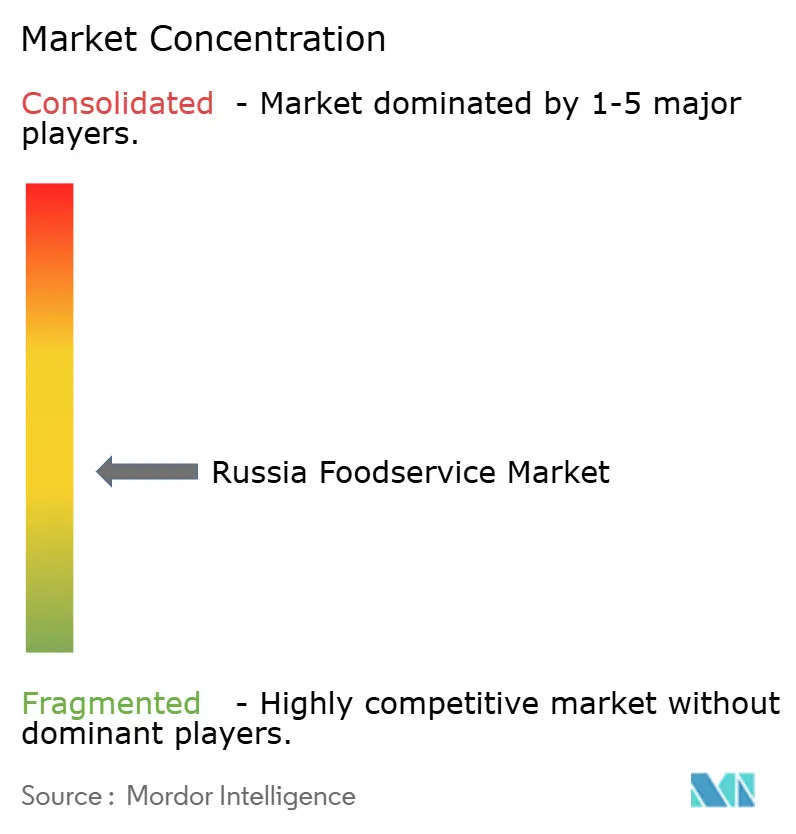

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Foodservice Market Analysis by Mordor Intelligence

The Russia foodservice market size is expected to increase from USD 36.01 billion in 2025 to USD 40.22 billion in 2026 and reach USD 62.86 billion by 2031, growing at a 9.34% CAGR over 2026-2031. The sector is shifting toward domestic ownership because international brands have exited, while franchise capital and technology adoption offset higher import costs. Quick-service formats dominate spending because consumers are trading down, yet delivery-led sales are accelerating as aggregator platforms reach smaller cities. Cashless payments, kitchen automation, and smart-supply chains help large chains protect margins even as ingredient inflation exceeds 11%. Tourism’s rebound and food-hall construction outside the two largest metros broaden demand, but sanctions, high policy rates, and strict food-safety enforcement still restrain profit growth.

Key Report Takeaways

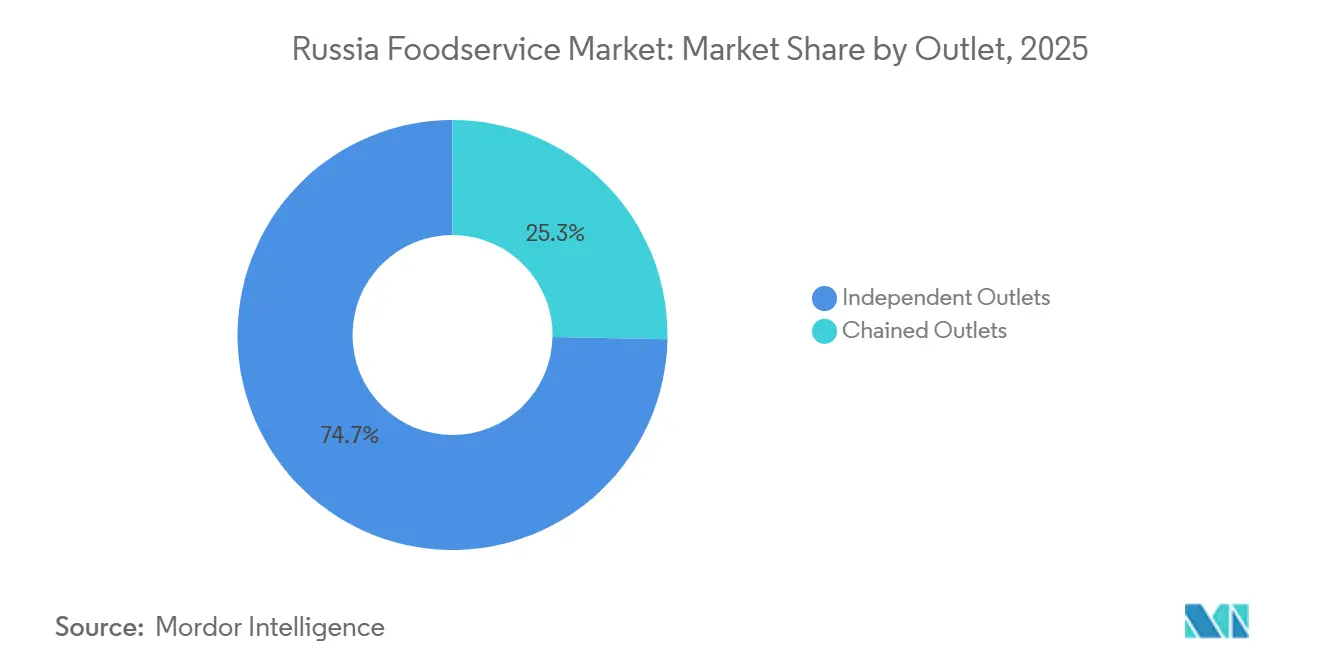

- By outlet format, chained operators held 25.32% of the Russia foodservice market share in 2025 and are projected to expand at a 9.92% CAGR through 2031.

- By service model, delivery channels accounted for 22.11% of 2025 revenue and will grow at a 9.64% CAGR to 2031, the fastest among all formats.

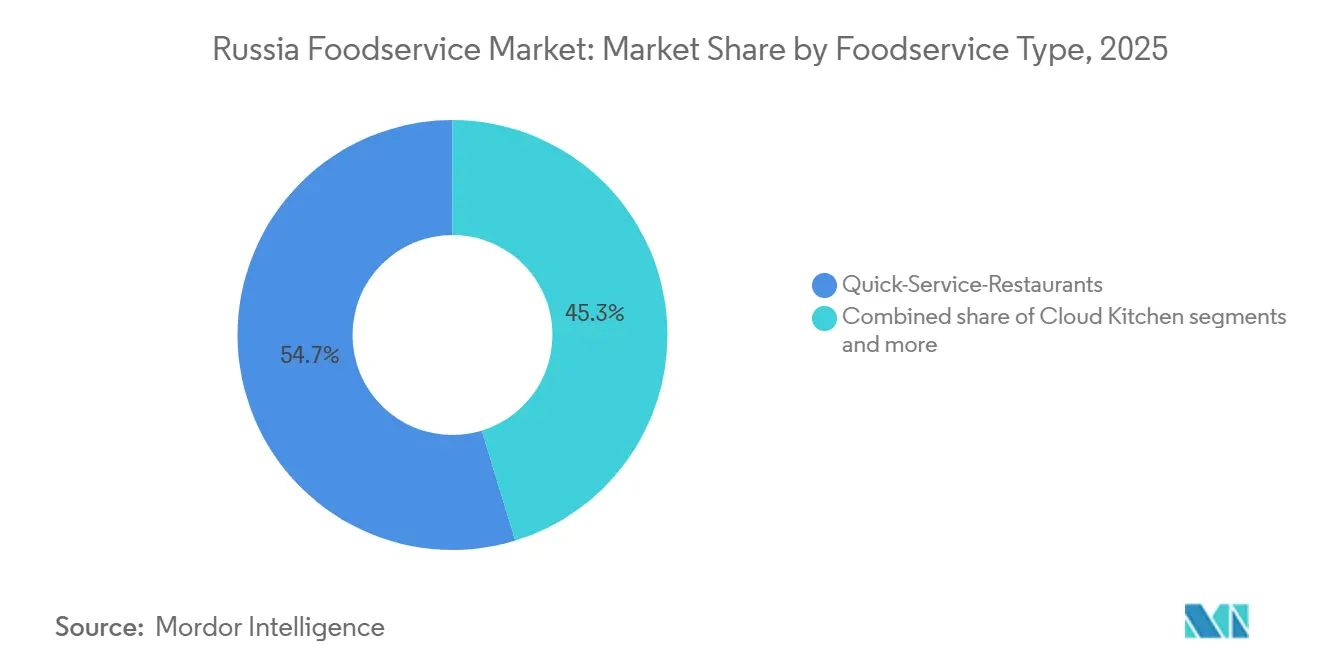

- By foodservice type, cloud kitchens accounted for only 4.27% of 2025 revenue yet are forecast to post a 10.76% CAGR to 2031, outpacing quick-service growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of domestic QSR and fast-casual chains | +2.1% | National, concentrated in Moscow, St. Petersburg, and million-plus regional cities | Medium term (2-4 years) |

| Growing penetration of online food delivery and aggregator platforms | +1.8% | National, with accelerated adoption in Tier-2 and Tier-3 cities beyond Moscow/St. Petersburg | Short term (≤ 2 years) |

| Technology adoption across foodservice operations | +1.2% | National, led by chained operators in urban markets | Medium term (2-4 years) |

| Growing demand for value-oriented dining options | +1.5% | National, particularly acute in regions with below-average household income | Short term (≤ 2 years) |

| Growing influence of western food culture | +0.9% | Moscow, St. Petersburg, and affluent urban centers | Long term (≥ 4 years) |

| Recovery in domestic tourism and mobility | +1.1% | National, with outsized impact in tourist destinations (Moscow, St. Petersburg, Black Sea resorts, Golden Ring cities) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Domestic QSR and Fast-Casual Chains

Forced localization following Western brand exits created a vacuum that domestic chains rapidly filled, with Vkusno & Tochka operating over 900 outlets by late 2024 and targeting 1,000 by 2026, generating RUB 187.4 billion (USD 2.07 billion) in revenue[1]Source: TASS, “Vkusno & Tochka Revenue and Expansion Plans,” tass.com. Stars Coffee, which acquired former Starbucks locations, expanded to 82 stores and pushed beyond Moscow and St. Petersburg into regional markets, demonstrating that brand equity can transfer when operational continuity is maintained. The franchise model accelerated this shift, outpacing the broader franchise market, as entrepreneurs leveraged proven formats to enter markets where international operators withdrew. Chained outlets, though holding only 25.32% market share in 2025, will grow at 9.92% CAGR through 2031, faster than the overall market, because institutional investors favor scalable, technology-enabled concepts over fragmented independents. Regional expansion is particularly pronounced: food-hall projects and hybrid formats combining multiple QSR brands under one roof opened 20 new locations in 2023, with 15 in regional cities, and launched 33 additional projects in 2024, signaling that demand extends well beyond Moscow's 25.3 million annual visitors.

Growing Penetration of Online Food Delivery and Aggregator Platforms

Aggregator platforms evolved from Moscow-centric services into national infrastructure, with Yandex Eda reaching 112 cities, partnering with 14,000+ restaurants, and serving 4.6 million active users in Q4 2024, while revenue surged 64% year-over-year to RUB 84.8 billion (USD 935 million)[2]Source: Yandex N.V., “Q4 2024 Financial Statements,” yandex.com. Delivery-focused operators deployed dark stores at scale, Samokat operated 2,300, Yandex Lavka 550, and Vkusville 218 by end-2024, to fulfill 15-minute delivery promises, compressing last-mile costs and enabling aggregators to offer competitive commission rates that attract smaller restaurants. This infrastructure buildout explains why delivery channels, despite holding lower share than dine-in in 2025, will grow at 9.64% CAGR through 2031. Critically, aggregator penetration in Tier-2 and Tier-3 cities accelerated in 2024, with Samokat entering Kurgan, Yoshkar-Ola, Pskov, and Petrozavodsk, extending reach into markets where independent restaurants previously lacked digital ordering capabilities. The shift also puts pressure on margins: restaurants pay 20-30% commissions to aggregators, forcing operators to optimize kitchen throughput and menu pricing to preserve profitability in a delivery-first model.

Technology Adoption Across Foodservice Operations

Digital infrastructure matured rapidly, with cashless payments accounting for 85.8% of retail turnover and the Faster Payments System (SBP) processing 13.4 billion transactions in 2024, reducing cash-handling costs and enabling dynamic pricing according to the Central Bank of Russia Payment Systems 2024[3]Source: Central Bank of Russia, “National Payment Systems 2024,” cbr.ru. The HoReCa mobile solutions market, encompassing POS systems, inventory management, and customer relationship management platforms, is driven by labor shortages that compel operators to automate order-taking and payment processing. Leading platforms such as iiko serve over 66,000 establishments worldwide, and R-Keeper serves over 65,000, with significant Russian penetration, offering cloud-based modules that integrate front-of-house, kitchen, and delivery operations. Technology adoption also extends to supply-chain visibility: X5 Retail Group's acquisition of the Nice Ice production facility (4,200 square meters, 7,000 meals per day, scalable to 70,000) in April 2024 exemplifies vertical integration enabled by real-time demand forecasting, allowing retailers to enter the ready-to-eat segment and compete directly with traditional foodservice operators. The competitive implication is stark: independent operators lacking digital infrastructure face margin erosion as chained competitors leverage data to optimize labor scheduling, inventory turns, and promotional timing, explaining why chained outlets will grow faster than independents despite starting from a smaller base.

Growing Demand for Value-Oriented Dining Options

Inflation-driven consumer downtrading reshaped demand, with food prices rising, butter up 33%, potatoes doubling, and services inflation hitting 12.67%, compressing household budgets. Consumer spending on cafés, restaurants, and delivery decelerated from 23% year-over-year growth to 6.2% in December 2025, signaling that price sensitivity now governs purchase decisions, according to Sberbank Consumer Trends 2024. Operators responded by expanding value tiers: Vkusno & Tochka's menu pricing undercuts premium QSR formats by 15-20%, while regional chains like Kroshka Kartoshka (baked-potato specialist) and Teremok (Russian pancakes) emphasize portion size and local ingredients to maintain affordability. The World Bank projects Russian GDP growth to slow from 3.2% in 2024 to 1.1% in 2026, with private consumption growth decelerating in parallel, reinforcing the structural shift toward budget-conscious formats. Franchise economics also favors value chains: lower initial investment and faster payback periods attract entrepreneurs in regions where household incomes lag behind those of Moscow and St. Petersburg. This trend explains why quick-service restaurants, which offer lower check averages than full-service establishments, captured 54.72% market share in 2025 and will sustain above-market growth. Importantly, value orientation does not imply quality degradation, operators compete on speed, convenience, and perceived freshness rather than premium ingredients, a positioning that resonates with middle-income consumers navigating persistent inflation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical instability and sanctions | -1.4% | National, with acute supply-chain disruption in Moscow and St. Petersburg due to import dependencies | Long term (≥ 4 years) |

| High inflation and economic pressures | -1.8% | National, disproportionately affecting regions with below-average household income | Short term (≤ 2 years) |

| Limited access to international brands and technologies | -0.7% | National, with greater impact on chained operators reliant on imported equipment and software | Medium term (2-4 years) |

| Strict food safety regulations | -0.5% | National, with heightened enforcement in Moscow, St. Petersburg, and major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Instability and Sanctions

Western sanctions severed established supply chains, forcing operators to substitute European suppliers with alternatives from China, Turkey, and Kazakhstan at 60-170% cost premiums, compressing operating margins from 20-25% to 10-12%. Equipment imports, commercial ovens, refrigeration units, and POS hardware, face delays and quality inconsistencies, extending restaurant buildout timelines and increasing capital expenditures. Payment-system restrictions complicate international franchising: operators cannot remit royalties or access global reservation platforms, limiting growth options for domestic chains seeking to expand beyond Russia. The exit of major international brands, Yum! Brands sold KFC operations in April 2023, and McDonald's transferred to Alexander Govor in June 2022, eliminating technical support and menu innovation pipelines that franchisees previously relied upon. Vkusno & Tochka faced immediate supply shortages, including a widely reported French-fry deficit in July 2022, illustrating the fragility of localized supply chains. Geopolitical uncertainty also deters foreign investment: private-equity firms and international restaurant groups that might otherwise enter the market through acquisitions or joint ventures are constrained by sanctions and reputational risks. The -1.4% CAGR drag from geopolitical instability will persist through the long term (≥ 4 years) as operators gradually rebuild supply chains and develop domestic alternatives, but full recovery to pre-sanction efficiency levels appears unlikely within the forecast horizon.

Limited Access to International Brands and Technologies

Sanctions and brand exits curtailed access to proprietary technologies, menu innovations, and operational best practices that international franchisors historically provided. Operators lost access to global supply-chain platforms, such as McDonald's centralized procurement system, that negotiated volume discounts and ensured consistent quality across thousands of outlets. Software licensing restrictions affect point-of-sale systems, kitchen display systems, and customer relationship platforms, forcing operators to migrate to domestic alternatives that may lack feature parity or integration capabilities. Equipment imports face delays: commercial-grade ovens, fryers, and refrigeration units from European manufacturers are subject to an embargo, and Chinese substitutes often require retrofitting or have shorter lifespans, increasing the total cost of ownership. The absence of international brand equity also constrains pricing power: Vkusno & Tochka, despite operational continuity with former McDonald's locations, cannot command the same premium as the McDonald's brand, limiting revenue per transaction. Franchise development suffers as well: domestic chains seeking to expand internationally face payment-system barriers and lack the global recognition needed to attract foreign franchisees. The -0.7% CAGR drag from limited access to international brands and technologies will persist through the medium term (2-4 years) as domestic suppliers and software developers gradually fill gaps, but the innovation deficit—particularly in menu R&D and customer-experience design—will take longer to close.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Outlet: Chained Operators Gain Despite Independent Dominance

Independent outlets held 74.68% market share in 2025, reflecting Russia's fragmented foodservice landscape, where family-owned cafés, neighborhood restaurants, and single-location QSRs dominate outside Moscow and St. Petersburg. However, chained outlets will expand at 9.92% CAGR through 2031, outpacing the overall market's 9.34% growth, as institutional capital and franchise models favor scalable concepts. Chained operators benefit from technology adoption; iiko and R-Keeper POS systems serve over 66,000 and 65,000 establishments, respectively, which reduces labor costs and improves throughput, advantages that independents struggle to replicate. Vkusno & Tochka's expansion to over 900 outlets by late 2024, targeting 1,000 by 2026, exemplifies the velocity at which domestic chains can scale when backed by experienced management and localized supply chains.

Independent operators face margin compression from inflation: food costs up 11.68% year-over-year and services inflation 12.67%, which they cannot offset through volume discounts or centralized procurement, according to Trading Economics Russia Inflation. Compliance burdens also weigh heavier on independents: Rospotrebnadzor's TR CU 021/2011 food safety regulations mandate HACCP implementation and periodic inspections, adding RUB 500,000-2,000,000 (USD 5,500-22,000) annually per outlet, costs that chained operators spread across hundreds of locations. Regional expansion by chained operators, food-hall projects opened 20 new locations in 2023, with 15 in regional cities, and launched 33 additional projects in 2024, brings professional management and capital investment to markets where independents previously faced no competition. The structural shift toward chained outlets will accelerate as aggregator platforms prioritize partnerships with multi-location operators that can guarantee consistent quality and delivery speed, leaving independents to compete on hyperlocal differentiation or niche cuisines.

By Service Model: Delivery Channels Outpace Dine-In Recovery

Dine-in service commanded 53.76% market share in 2025, reflecting consumer preference for experiential dining and social occasions, yet delivery channels will grow at 9.64% CAGR through 2031, driven by aggregator-platform expansion and dark-store proliferation. Yandex Eda reached 112 cities with 14,000+ restaurant partners and 4.6 million active users in Q4 2024, generating RUB 84.8 billion (USD 935 million) in revenue, up 64% year-over-year, while the broader online food delivery market hit USD 8.7 billion in 2024. Dark stores: Samokat deployed 2,300, Yandex Lavka 550, Vkusville 218 by the end of 2024. Enable 15-minute delivery promises that compress last-mile costs and allow aggregators to offer competitive commission rates, making delivery economically viable for smaller restaurants. Takeaway and drive-thru formats occupy the middle ground, appealing to time-pressed consumers seeking convenience without delivery fees, though these channels lack the infrastructure investment and platform effects driving delivery growth.

X5 Retail Group's acquisition of the Nice Ice production facility in April 2024, 4,200 square meters producing 7,000 meals daily, scalable to 70,000, illustrates how retailers are entering the ready-to-eat segment with vertically integrated supply chains that compete directly with traditional foodservice. Dine-in recovery faces headwinds from inflation-driven downtrading: consumer spending on cafés and restaurants decelerated from 23% growth to 6.2% year-over-year in December 2025, signaling that price-sensitive households are cutting discretionary dining, according to the Sberbank Consumer Trends 2024. Tourism recovery, 78.3 million domestic trips in 2024, up 7.8%, generating RUB 3.5 trillion (USD 41 billion) in spending, partially offsets this trend, as tourists dine out 2-3 times daily versus 0.5-1 time for residents, concentrating demand in Moscow (25.3 million visitors, up 8.5%) and other high-traffic destinations, according to the Rostourism Tourism Statistics 2024[4]Source: Federal Agency for Tourism, “Domestic Tourism 2024,” tourism.gov.ru. The service-model mix will continue shifting toward delivery and takeaway as aggregator platforms extend into Tier-2 and Tier-3 cities, where Samokat entered Kurgan, Yoshkar-Ola, Pskov, and Petrozavodsk in 2024, bringing digital ordering to markets where it was previously unavailable.

By Foodservice Type: QSR Dominance and Cloud Kitchen Disruption

Quick-service restaurants captured 54.72% market share in 2025, reflecting consumer preference for speed, value, and convenience amid inflation-driven budget constraints. Vkusno & Tochka (900+ outlets, RUB 187.4 billion revenue in 2024), Burger King Russia (1,000+ restaurants), and Domino's (200+ stores) anchor the QSR segment, leveraging standardized menus and centralized procurement to maintain affordability. Full-service restaurants face margin pressure from labor costs, unemployment at 2.5% drove wage inflation, and longer table turns that limit throughput, constraining growth relative to QSR formats. Within full-service, Asian cuisine gained traction among urban millennials, while European and Middle Eastern formats serve niche demand in affluent neighborhoods. Cafés and bars, including specialty coffee shops like Shokoladnitsa (420+ outlets) and Stars Coffee (82 stores), benefit from high-margin beverage sales and repeat-visit frequency, though coffee imports of 286,000 tonnes in 2024 (whole-bean up 15.6%, capsule up 9.4%) indicate that at-home consumption is also rising, potentially capping out-of-home growth.

Cloud kitchens, though a small segment in absolute terms, will grow at 10.76% CAGR through 2031, the fastest rate across all foodservice types, as operators eliminate rent and labor costs associated with dine-in facilities. The model aligns with aggregator-platform economics: delivery-only concepts optimize kitchen layouts for order throughput, reducing preparation time and improving delivery-speed metrics that platforms reward with higher search rankings. Retailers are also entering the segment, X5 Retail Group's acquisition of Nice Ice positions the company to produce 40,000 meals daily (upgradeable to 70,000) and capture 9% of the combined retail and HoReCa ready-to-eat market by 2026. Bakeries, ice cream parlors, and juice/smoothie bars occupy niche positions within QSR, appealing to snack-occasion demand rather than meal replacement. The foodservice-type mix will continue tilting toward QSR and cloud kitchens as inflation sustains demand for value-oriented formats and delivery penetration deepens, leaving full-service restaurants to compete on experiential differentiation or premium positioning that justifies higher check averages.

Geography Analysis

Russia's foodservice market exhibits pronounced geographic concentration, with Moscow and St. Petersburg accounting for an outsized share of revenue due to higher household incomes, tourist traffic, and density of chained operators. Moscow attracted 25.3 million visitors in 2024, up 8.5% year-over-year, generating demand for quick-service and casual-dining formats near tourist attractions, transportation hubs, and hotels, according to the Moscow Department of Tourism. The capital's foodservice infrastructure is the most mature in the country, with aggregator platforms like Yandex Eda achieving near-universal coverage and dark stores enabling 15-minute delivery across most districts. St. Petersburg mirrors this dynamic on a smaller scale, benefiting from cultural tourism and a concentration of international-brand successors such as Stars Coffee and Vkusno & Tochka. Regional cities, including Yekaterinburg, Novosibirsk, Kazan, and Rostov-on-Don, are experiencing accelerated growth as chain operators expand beyond the two largest metros: food-hall projects opened 15 new locations in regional cities during 2023 and 33 additional projects launched in 2024, bringing professional management and capital investment to previously underserved markets.

Tier-2 and Tier-3 cities represent the frontier for market expansion, driven by aggregator-platform penetration, Samokat entered Kurgan, Yoshkar-Ola, Pskov, and Petrozavodsk in 2024, and franchise-model adoption that lowers entry barriers for local entrepreneurs. However, these markets face structural headwinds: household incomes lag Moscow and St. Petersburg, inflation disproportionately affects below-average earners, and supply-chain costs are higher due to longer distribution distances. The franchise market growth in restaurant and delivery franchising signals that regional expansion is accelerating, yet operators must adapt menus and pricing to local purchasing power. Domestic tourism recovery, 78.3 million trips in 2024, up 7.8%, generating RUB 3.5 trillion (USD 41 billion) in spending, benefits regional destinations such as Black Sea resorts, Golden Ring cities, and Siberian nature tourism hubs, where seasonal demand spikes drive foodservice revenue, according to the Rostourism Tourism Statistics 2024.

Geographic disparities in technology adoption also shape growth trajectories: Moscow and St. Petersburg lead in cashless-payment penetration and POS-system deployment (iiko and R-Keeper serve 66,000+ and 65,000+ establishments respectively), whereas regional cities exhibit lower adoption rates, constraining operational efficiency. Regional operators, by contrast, rely more heavily on manual processes and face longer payback periods for technology investments. The geographic growth pattern will remain Moscow-centric in absolute terms, but regional cities will contribute an increasing share of incremental growth as chained operators and aggregator platforms extend reach, franchise models proliferate, and domestic tourism sustains demand in secondary markets.

Competitive Landscape

The Russia foodservice market exhibits moderate fragmentation, indicating that the top five players, Restaurant Brands International (Burger King Russia), Rosinter Restaurants, Vkusno & Tochka, Stars Coffee, and Yum! Brands' legacy operations hold a meaningful but not dominant share. Competition intensified following Western brand exits, as domestic chains and entrepreneurs moved aggressively to capture vacated market share: Vkusno & Tochka absorbed over 900 former McDonald's locations and generated RUB 187.4 billion (USD 2.07 billion) in revenue in 2024, while Stars Coffee acquired 82 former Starbucks outlets and expanded beyond Moscow and St. Petersburg. Franchise models emerged as the dominant growth strategy, with restaurant and delivery franchising surging within a broader franchise market, enabling rapid geographic expansion without the capital intensity of company-owned outlets.

Technology adoption differentiates leaders from laggards: operators deploying POS systems like iiko (66,000+ establishments) and R-Keeper (65,000+ worldwide) achieve 15-20% labor-cost savings through automated order-taking and inventory management, compressing payback periods to under 18 months and freeing capital for new-unit development. White-space opportunities cluster in Tier-2 and Tier-3 cities where aggregator platforms recently extended coverage, Samokat entered Kurgan, Yoshkar-Ola, Pskov, and Petrozavodsk in 2024, and franchise penetration remains low relative to Moscow and St. Petersburg. Cloud kitchens represent another frontier, with the segment projected to grow at 10.76% CAGR through 2031, yet few operators have scaled delivery-only concepts beyond pilot markets.

Retailers are also encroaching on traditional foodservice: X5 Retail Group's acquisition of the Nice Ice production facility in April 2024 positions the company to produce 40,000 meals daily (upgradeable to 70,000) and capture 9% of the combined retail and HoReCa ready-to-eat market by 2026, leveraging vertically integrated supply chains and real-time demand forecasting. Emerging disruptors include regional chains like Teremok (Russian pancakes) and Kroshka Kartoshka (baked potatoes) that emphasize local ingredients and cultural authenticity, differentiating from Western formats and appealing to consumers seeking value without sacrificing perceived quality. The competitive landscape will continue consolidating around operators that master franchise economics, deploy technology to reduce labor dependency, and secure favorable terms with aggregator platforms, while independents face margin erosion and market-share loss absent differentiation or hyperlocal positioning.

Russia Foodservice Industry Leaders

Restaurant Brands International Inc.

Rosinter Restaurants Holding PJSC

Vkusno & Tochka JSC

Stars Coffee LLC

Yum! Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: "Kroshka Kartoshka," a fast food restaurant, has opened in the new terminal of Gelendzhik airport. Situated in the departure lounge on the first floor, the eatery spans nearly 70 sq.m. Passengers can indulge in a variety of offerings, from Russian and international potato dishes to soups, sandwiches, salads, desserts, and beverages.

- July 2025: Khleburger has launched its inaugural outlet of a new fast food chain in Vladivostok, marking its entry into the region's competitive quick-service restaurant market.

- April 2024: X5 Retail Group acquired the Nice Ice production facility in Vsevolozhsky District, Leningrad Region, a 4,200-square-meter smart kitchen producing 7,000 ready-to-eat meals daily with installed capacity upgradeable to 70,000. The facility produces salads, breakfasts, hot meals, starters, sandwiches, and desserts for Pyaterochka and Perekrestok chains, positioning X5 to grow its share in the combined retail and HoReCa ready-to-eat market.

Russia Foodservice Market Report Scope

Foodservice includes the companies/restaurants that prepare meals outside the home. The scope of the Russian foodservice market is segmented by outlet type, service model, and foodservice category to deliver a structured, holistic evaluation. By outlet type, the analysis distinguishes between chained and independent outlets. By service model, the study covers dine-in, take-away, delivery, and drive-thru formats. By foodservice type, the report provides detailed coverage of full-service restaurants (FSR), quick-service restaurants (QSR), cafés and bars, and cloud kitchens. The full-service restaurant segment includes cuisine-based analysis of Asian, European, Latin American, Middle Eastern, North American, and other cuisines. The quick service restaurant segment encompasses bakeries, burger outlets, ice cream outlets, meat-based cuisine, and other quick service cuisine. The cafés and bars segment includes bars and pubs, cafés, juice/smoothie/dessert outlets, and specialty coffee and tea establishments. The cloud kitchen segment is evaluated at an overall level. For each segment, the market sizing and forecast have been done based on value (USD million).

By Outlet

| Chained Outlets |

| Independent Outlets |

By Service Model

| Dine-in |

| Take-away |

| Delivery |

| Drive-Thru |

By Foodservice Type

| Full Service Restaurants | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other Full-Service Restaurant Cuisine | |

| Quick Service Cuisine | Bakeries |

| Burger | |

| Ice Cream | |

| Meat-Based Cuisine | |

| Other Quick Service Cuisine | |

| Cafes and Bars | Bars and Pubs |

| Cafes | |

| Juices/Smoothies/Desserts | |

| Specialty Coffee and Tea | |

| Cloud Kitchen (Overall Only) |

| By Outlet | Chained Outlets | |

| Independent Outlets | ||

| By Service Model | Dine-in | |

| Take-away | ||

| Delivery | ||

| Drive-Thru | ||

| By Foodservice Type | Full Service Restaurants | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other Full-Service Restaurant Cuisine | ||

| Quick Service Cuisine | Bakeries | |

| Burger | ||

| Ice Cream | ||

| Meat-Based Cuisine | ||

| Other Quick Service Cuisine | ||

| Cafes and Bars | Bars and Pubs | |

| Cafes | ||

| Juices/Smoothies/Desserts | ||

| Specialty Coffee and Tea | ||

| Cloud Kitchen (Overall Only) | ||

Key Questions Answered in the Report

What is the current value of Russia’s foodservice sector and how much is it projected to reach by 2031?

Spending totaled USD 36.01 billion in 2025, is expected at USD 40.22 billion in 2026, and should climb to USD 62.86 billion by 2031.

Which dining format is expanding the fastest across the country?

Cloud kitchens lead with a projected 10.76% CAGR through 2031, edging out the broader quick-service segment.

How have sanctions changed restaurant operating costs?

Switching from European to Asian suppliers raised input prices by 60–170%, pushing average operating margins down from 20-25% to about 10-12%.

What explains the faster growth of domestic chains compared with independents?

Franchising, centralized procurement, and digital systems give chains scale advantages that cut labor and ingredient costs while easing compliance.

In what ways does tourism support foodservice demand?

Domestic trips rose to 78.3 million in 2024, and tourists eat out two to three times a day, lifting sales in Moscow, St. Petersburg, and resort corridors.

Page last updated on: