Military Biometrics Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 10.68 Billion |

| Market Size (2031) | USD 14.83 Billion |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

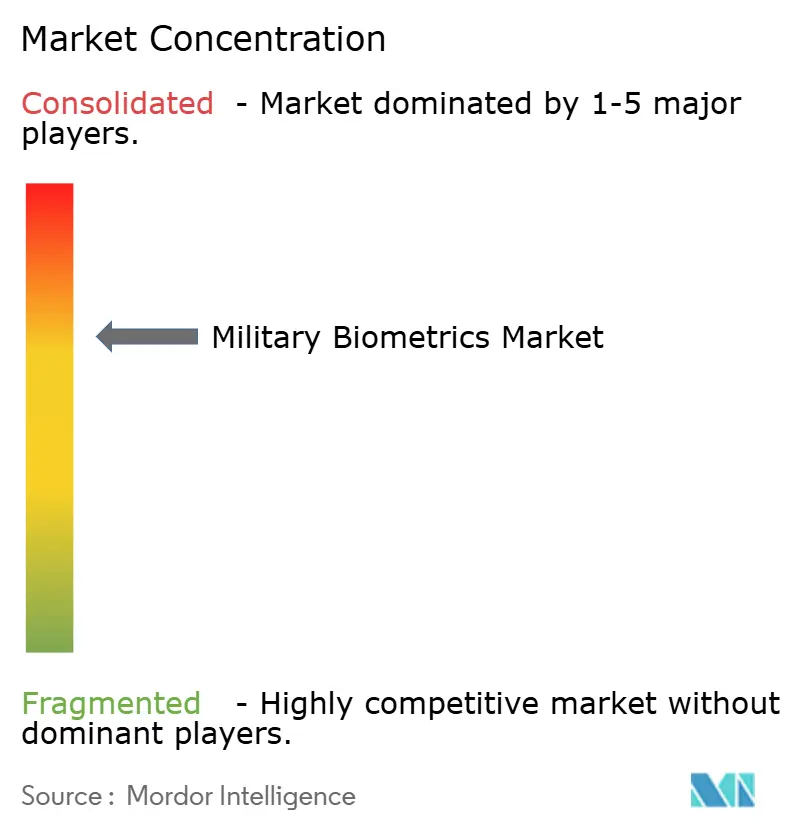

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Biometrics Market Analysis by Mordor Intelligence

The military biometrics market size is expected to reach USD 10.68 billion in 2026 and is projected to grow to USD 14.83 billion by 2031, registering a 6.80% CAGR over the forecast period. Heightened asymmetric warfare, porous borders, and NATO interoperability mandates are the primary forces shaping current demand trajectories. Meanwhile, AI-enabled accuracy improvements and declining sensor prices create new opportunities for adoption. Vendors able to combine open-standard middleware with ruggedized hardware are gaining preference as defense agencies race to meet new accuracy thresholds, and privacy requirements are fragmenting deployment architectures between on-device and cloud-based matching. The military biometrics market continues to shift toward mobile and tactical solutions, as authentication occurs at dispersed contact points in today’s irregular conflict zones. Competitive intensity is moderate; the top five suppliers rely on multi-year contracts that include refresh clauses, creating switching barriers for customers.

Key Report Takeaways

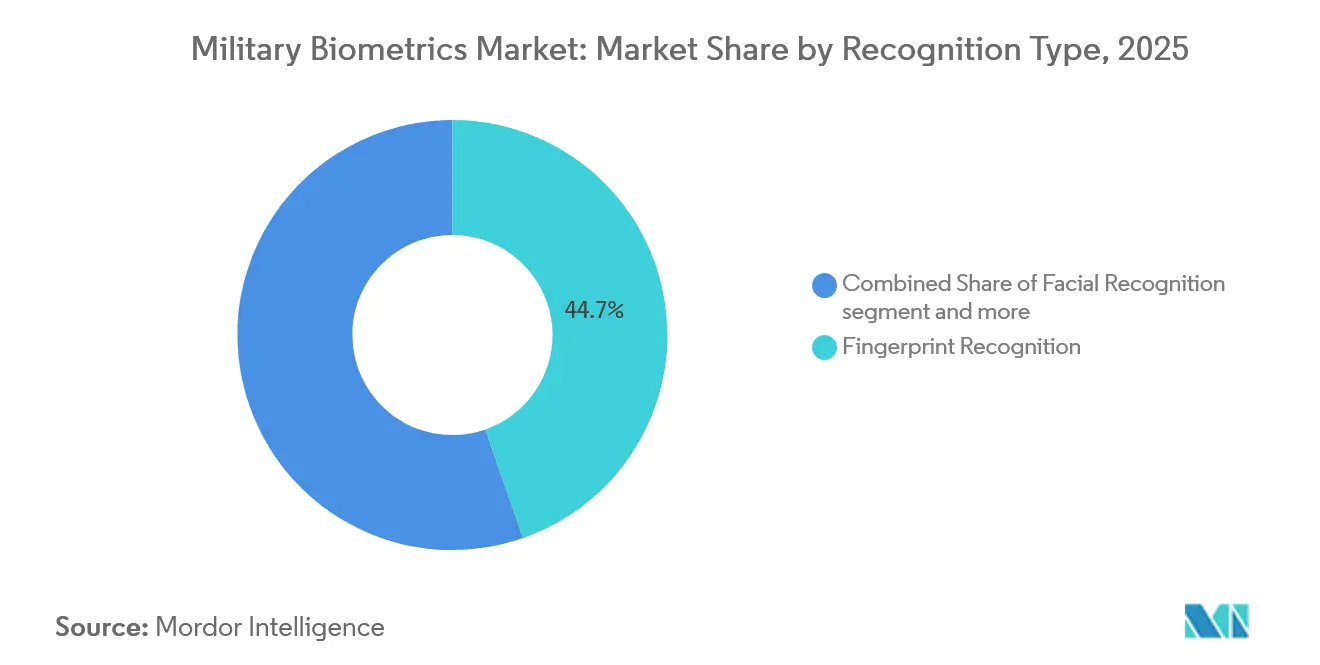

- By recognition type, fingerprint systems held 44.67% of the military biometrics market share in 2025, while voice, palm vein, and gait analytics are expected to expand at an 8.89% CAGR through 2031.

- By solution, hardware generated 61.13% of 2025 revenue; however, software is advancing at a 9.91% CAGR as defense ministries prioritize AI-ready matching engines.

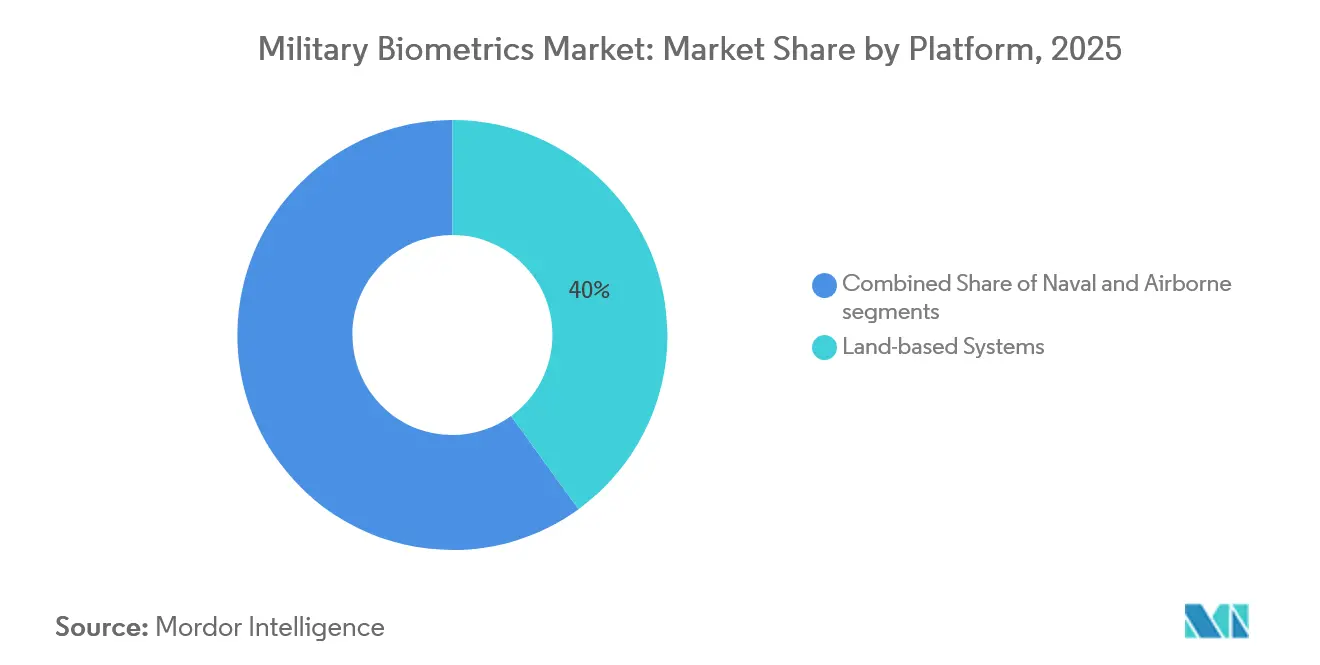

- By platform, land-based deployments accounted for 40.03% of the military biometrics market size in 2025 and are projected to grow at a 10.14% CAGR through 2031.

- By deployment environment, mobile and tactical kits dominated with a 62.89% revenue share in 2025 and are projected to rise at a 7.87% CAGR to the end of the forecast window.

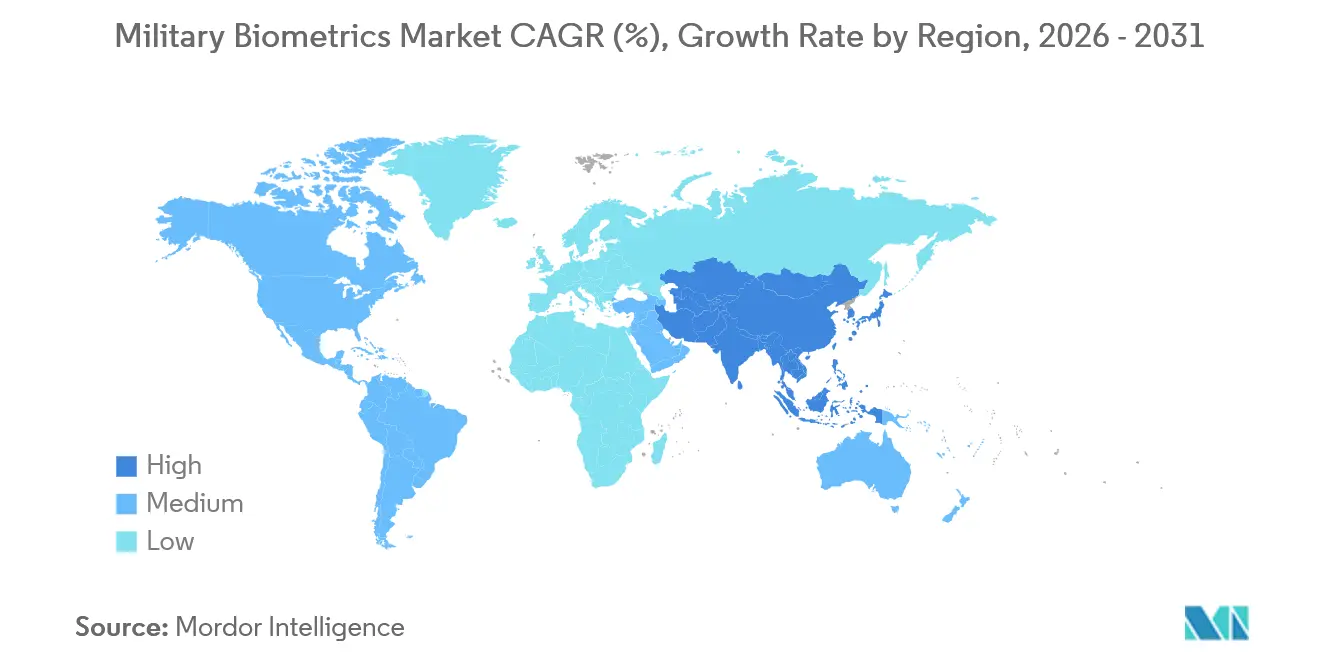

- By geography, North America accounted for 36.75% of the revenue in 2025; the Asia-Pacific region is the fastest-growing, with an 8.32% CAGR, driven by procurements from India, China, and Japan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Military Biometrics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising asymmetric warfare and border security needs | +1.8% | Middle East, South Asia, US–Mexico border | Medium term (2-4 years) |

| Government digital identity and defense modernization programs | +1.5% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Cost decline of fingerprint and facial sensors | +1.2% | Global, price-sensitive APAC and MEA | Short term (≤2 years) |

| Integration of AI/ML boosting accuracy and speed | +1.4% | North America, Europe, APAC | Medium term (2-4 years) |

| Deployment of biometric-enabled wearables for soldier authentication | +0.9% | NATO states and select APAC allies | Long term (≥4 years) |

| NATO push for interoperable multimodal biometric repositories | +1.1% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Asymmetric Warfare And Border Security Needs

Non-state adversaries and migration flows now bypass fixed checkpoints, forcing commanders to verify identities during patrols, at forward posts, and along remote deserts. The US Army enrolled 7.3 million individuals across Iraq, Afghanistan, and Syria under its Biometrics Enabling Capability, demonstrating the operational value of field kits.[1]U.S. Army, “Biometrics Enabling Capability,” army.mil India’s Border Security Force installed 1,200 mobile biometric devices along the Bangladesh and Myanmar frontiers in 2025 and cut illegal crossings by 34% within six months. Saudi Arabia integrated iris scanners with Interpol watchlists at 89 land crossings, intercepting 2,400 fraudulent entries in the first year. These precedents explain why mobile and tactical systems captured nearly two-thirds of 2025 revenue. As distributed conflict persists, the military biometrics market will continue to privilege rugged handheld devices that work beyond garrison infrastructure.

Government Digital Identity And Defense Modernization Programs

Defense ministries are synchronizing soldier and contractor credentials with nationwide electronic identification (e-ID) frameworks. The DoD awarded a USD 92 million contract in 2025 to integrate biometric verification into the Common Access Card, covering approximately 2.1 million personnel. Japan earmarked USD 120 million in fiscal 2025 to retrofit 340 facilities with multimodal gates, resulting in a 67% reduction in unauthorized-access incidents at test sites. The EU’s PESCO initiative mandates ISO/IEC 19794 compliance by 2027, accelerating middleware procurements that bridge national networks. Such programs extend verification from base entry to supply-chain checkpoints and naval docks, thereby broadening the addressable military biometrics market across asset classes and mission sets.

Cost Decline of Fingerprint and Facial Sensors

Component prices have fallen below key procurement thresholds. Capacitive fingerprint modules now cost USD 3.80 each, down from USD 12 in 2020, enabling battalion-level kit issuance. Facial cameras with embedded neural engines are expected to drop to USD 89 in 2024, supporting deployment on 250 US Coast Guard cutters under a USD 47 million upgrade.[2]Parsons Corporation, “Coast Guard Modernization,” parsons.com India’s DRDO produced an iris scanner priced at USD 180 in 2025, opening local volume orders for 12,000 units. With sensor costs falling, the budget debate shifts toward which modalities to combine rather than whether to deploy any at all, accelerating the multimodal trajectory of the military biometrics market.

Integration of AI/ML Boosting Accuracy and Speed

Neural architectures now outperform legacy minutiae extractors in dusty, low-light, and soot-covered conditions. DHS’s 2024 Biometric Rally achieved a 97.2% true-acceptance rate for ML-based fingerprint models, compared to 81.4% for earlier approaches. Oak Ridge released the BRIAR data set of 50,000 long-range body images, resulting in gait models that reached 89% accuracy at 200 meters, a breakthrough for special operations. NEC’s 2024 NeoFace upgrade slashed one-to-many search time across 10 million templates from 4.2 seconds to 0.7 seconds. These improvements meet the requirements of DoD Directive 8521.01E, which mandates 98% accuracy in operational theaters. Software refreshes are thereby outpacing hardware replacements and fueling the 9.91% CAGR in biometric-matching engines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and civil-liberty concerns over biometric databases | -1.3% | Europe and North America | Medium term (2-4 years) |

| High integration cost with legacy defense IT | -1.1% | Global, acute in Europe and North America | Short term (≤2 years) |

| Spoof-resistant tech lag in austere battlefield environments | -0.8% | Middle East, Africa, South Asia | Medium term (2-4 years) |

| Cyber-physical attacks targeting tactical biometric sensors | -0.7% | Global, contested EM environments | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Privacy and Civil-Liberty Concerns Over Biometric Databases

Regulators in democratic jurisdictions are curtailing centralized repositories. The European Data Protection Board requires that facial recognition systems used by member militaries complete matching on-device, a rule that increases per-unit costs by 40% and limits cloud deployments.[3]European Data Protection Board, “Guidelines on Military Biometrics,” edpb.europa.eu GAO’s 2025 audit identified 17 privacy gaps in DHS’s HART project, resulting in a delay of USD 214 million in spending. Canada now requires the deletion of biometric data within 90 days if no charges are filed, reducing the investigatory utility of field enrollments. Such rulings fragment the military biometrics market between jurisdictions that pursue expansive central databases and those that enforce strict local retention, complicating vendor product roadmaps.

High Integration Cost With Legacy Defense IT

Aging command-and-control networks raise middleware bills and slow rollout schedules. The US Army spent USD 340 million integrating biometrics into its enterprise personnel system after discovering that older databases could not store ISO templates natively. The UK canceled a planned upgrade on 78 frigates when bids reached USD 230 million, an amount deemed unjustifiable given their scheduled retirement in 2028. NATO’s 2024 survey found that 62% of member states cite legacy IT as their top barrier, with an average integration span of 3.7 years. These cost overruns tend to tilt procurement toward software-defined solutions that abstract legacy complexity, yet still dampen near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Recognition Type: Fingerprint Leadership Funds The Shift To Contactless Modalities

Fingerprint systems accounted for 44.67% of 2025 revenue, underpinned by 14,000 SEEK II handhelds deployed across US brigades and extensive criminal-justice precedent. Facial recognition follows, benefiting from passive capture at checkpoints where the US CBP processed 97 million comparisons in fiscal 2025.[4]CBP, “Facial Comparison Statistics,” cbp.gov Iris recognition remains a niche technology because it requires cooperative subjects; yet, the US Marine Corps installed 800 iris-enabled tablets on amphibious ships for shipboard access in 2024. The other categories, voice, palm vein, gait, and behavioral, grow at an 8.89% CAGR, as special forces favor contactless options in chemical or biological threat zones. DARPA proved gait identification accuracy of 87% at 150 meters in 2024 field trials. Palm-vein access is now tested at 120 Japanese armories, showing resilience against surface abrasion limits that plague fingerprints. Voice biometrics defended encrypted radio channels on Thales AN/PRC-163 sets, authenticating speakers in real time. Multimodal fusion is the long-term end-state. The DoD’s forthcoming tri-modal handheld solicitation highlights a channel where the military biometrics market size for hybrid devices is expected to expand through 2031.

By Solution: Software Velocity Outstrips Hardware Dominance

Hardware contributed 61.13% of 2025 sales, reflecting the capital intensity of scanners and ruggedized tablets. Yet software licenses post the steepest slope at 9.91% CAGR because neural matching upgrades can raise accuracy to the 98% directive threshold without sensor swaps. Aware recorded 34% software license growth in 2025 by retrofitting legacy readers with ML engines, which reduced false rejects by 40%. NeoFace’s sub-second searches across 10 million templates facilitate real-time border decisions in Germany, Spain, and Poland. Encryption and audit modules enhance value; DERMALOG won a USD 49 million contract by embedding blockchain audit trails to preserve evidentiary chains for federal law enforcement agencies. Hardware vendors now offer bundled subscriptions; IDEMIA’s MorphoWave Compact includes a three-year cloud matching option, reflecting the convergence. As software upgrade cycles are key, the military biometrics market will allocate a larger portion of its budget toward middleware, algorithms, and federated database management.

By Platform: Land Systems Dominate And Accelerate In Parallel

Land systems led with 40.03% of 2025 revenue and also logged the fastest 10.14% CAGR thanks to border-wall sensor arrays and vehicle-mounted stations that supplant fixed forward bases. Saudi Arabia’s USD 780 million Yemen-frontier smart fence merges cameras and ground sensors, cutting illegal crossings and validating the land-centric thesis. India equipped 450 all-terrain vehicles with biometric workstations to enroll detainees in remote Himalayan sectors. Naval platforms follow; the US Navy adopted iris gates on 22 destroyers under IDEMIA’s USD 68 million award to protect nuclear weapons lockers. Japan retrofitted eight Aegis destroyers, slashing unauthorized entries by 91%. Air systems remain smallest due to weight and power limits, although the US Air Force pilots' cockpit fingerprint locks on F-35A fighters at Nellis. The land focus confirms that the military biometrics market will continue to anchor on ground-based deployments, where threat contact is most frequent.

By Deployment Environment: Tactical Mobility Remains Imperative

Mobile and tactical deployments captured a 62.89% share in 2025, gaining traction from counterinsurgency missions that require on-the-spot identity checks. France’s Barkhane force logged 340,000 enrollments across Sahel patrols between 2020 and 2024 through rugged tablets. In 2025, India’s Central Reserve Police deployed 1,800 mobile kits in Kashmir for instant verification against a watchlist of 2.3 million records. Fixed installations account for 37.11% of spending and handle high-throughput border gates. The DoD now authenticates 18 million daily entries at 680 bases via biometric gates. The UAE processed 89 million travelers through 140 biometric lanes at two airports in 2024. Nonetheless, asymmetric foes avoid static points, ensuring that tactical kits remain the primary budget line of the military biometrics market.

Geography Analysis

North America led with 36.75% of 2025 revenue, driven by the USD 386 million CBP OBIM contract and large defense modernization budgets. Canada committed USD 180 million to integrate biometrics into its personnel management system through 2029. Mexico deployed 800 kits in 2024 for southern border patrols.

The Asia-Pacific region is growing at an 8.32% CAGR. India installed biometric gates at 198 forward posts along the Line of Actual Control in 2025, financed within a USD 420 million program. China’s Ministry of Public Security grew its border records to 1.2 billion and rolled out facial exit-entry systems at 312 crossings.

Japan funded USD 190 million for 340 base retrofits with NEC multimodal gates. South Korea selected HID Global for USD 95 million of iris scanners across 280 facilities. Europe balances GDPR privacy limits with NATO standards, investing USD 130 million to migrate Germany’s database onto a compliant backbone. The Middle East and Africa growth centers on border security fences and national service enrollment. Saudi Arabia now operates biometric checkpoints at 89 crossings, resulting in a 67% reduction in fraud.

Competitive Landscape

Market concentration is moderate. IDEMIA, Thales, NEC, HID Global, and Northrop Grumman collectively hold nearly 52% of the spend, sustained by 7- to 10-year refresh clauses and platform-wide service contracts. Hardware specialists emphasize sensor ruggedness while defense primes bundle biometrics with command-and-control suites. NATO’s ANSI/NIST-ITL 1-2024 mandate shifts the advantage toward software providers who can abstract hardware diversity, as seen in Aware’s 34% growth and M2SYS’s plug-in that reduces interoperability upgrade costs by 60%. Disruptors target gaps in the chain of custody, blockchain auditing, and anti-spoofing. DERMALOG incorporated blockchain audit trails, winning the German Federal Police award. HID Global patents pulse-oximetry spoof detection, and Thales lodged 14 multimodal-fusion patent applications between 2024 and 2025.[5]European Patent Office, “Biometric Patent Filings 2024-25,” epo.org Airborne platforms and behavioral biometrics represent untapped pockets within the military biometrics market, with US Cyber Command piloting keystroke analytics for insider-threat defense. Software-defined architectures that enable over-the-air algorithm updates are eroding legacy vendor lock-in and expanding the competitive landscape.

Military Biometrics Industry Leaders

IDEMIA

Northrop Grumman Corporation

Thales Group

NEC Corporation

HID Global

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Parsons Corporation announced that it had been awarded a contract to modernize the US Coast Guard’s (USCG) Biometrics at Sea System (BASS 2.0). The BASS platform is a vital tool for maritime law enforcement operations, enabling the Coast Guard to collect and analyze biometric data, including fingerprints and facial recognition, to verify identities, identify threats, and enhance security by connecting to national and international databases. This contract includes a five-year performance period and constitutes new work for the company.

- October 2024: Leidos, Inc. was awarded a six-year, USD 249 million Automated Installation Entry (AIE) Next Generation contract by the US Army Contracting Command for the Program Executive Office Intelligence, Electronic Warfare & Sensors. The contract assigns Leidos the responsibility of improving security measures at 92 Army and select Joint-Service installation access points globally.

- January 2024: General Dynamics' IT business (GDIT) was awarded a USD 386.4 million contract by the Department of Homeland Security (DHS) for its IT infrastructure. The company will operate and maintain the infrastructure, components, and related applications for the DHS Office of Biometric Identity Management.

Global Military Biometrics Market Report Scope

Military biometrics refers to the use of biometric technologies in military operations, enhancing security, authentication, and identification processes. In this context, a biometric system, an electronic configuration, is employed to confirm an individual's identity. These systems, equipped with various hardware and software components, capture physical inputs, analyze them, and grant authentication. Biometrics entails measuring and statistically analyzing an individual's physical and behavioral characteristics. Biometric identification safeguards entry, data, or access by leveraging human biological markers such as DNA or fingerprints.

The military biometrics market is segmented by recognition type, solution, platform, deployment environment, and geography. By recognition type, the market is segmented into fingerprint recognition, facial recognition, iris recognition, and other types of recognition. The different types include DNA recognition, finger geometry recognition, keystroke recognition, and signature recognition. By solution, the market is segmented into hardware and software. By platform, the market is classified into land-based systems, naval systems, and airborne systems. By deployment environment, the market is divided into fixed installations and mobile and tactical.

The report also covers the market sizes and forecasts for the military biometrics market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Fingerprint Recognition |

| Facial Recognition |

| Iris Recognition |

| Others |

| Hardware (Scanners, Sensors, Portable Kits) |

| Software (Matching Engines, Database, Middleware, Encryption) |

| Land-Based Systems |

| Naval Systems |

| Airborne Systems |

| Fixed Installations |

| Mobile and Tactical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Afirca | Egypt | |

| Rest of Africa | ||

| By Recognition Type | Fingerprint Recognition | ||

| Facial Recognition | |||

| Iris Recognition | |||

| Others | |||

| By Solution | Hardware (Scanners, Sensors, Portable Kits) | ||

| Software (Matching Engines, Database, Middleware, Encryption) | |||

| By Platform | Land-Based Systems | ||

| Naval Systems | |||

| Airborne Systems | |||

| By Deployment Environment | Fixed Installations | ||

| Mobile and Tactical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Afirca | Egypt | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected value of the military biometrics market in 2031?

The market is forecast to reach USD 14.83 billion by 2031 at a 6.80% CAGR.

Which biometric modality currently holds the largest revenue share?

Fingerprint systems led with 44.67% of revenue in 2025.

Which region is projected to grow the fastest through 2031?

Asia-Pacific is expanding at an 8.32% CAGR due to large-scale deployments in India, China, and Japan.

How dominant are mobile and tactical deployments?

They accounted for 62.89% of 2025 revenue and continue to rise as border and counterinsurgency missions expand.

Which companies lead market share?

IDEMIA, Thales, NEC, HID Global, and Northrop Grumman collectively hold about 52% of spending.

What technology shift is driving software growth?

AI-enabled matching engines that lift accuracy to 98% without replacing existing sensors fuel the 9.91% CAGR in software sales.

Page last updated on: