Silver Wound Dressing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

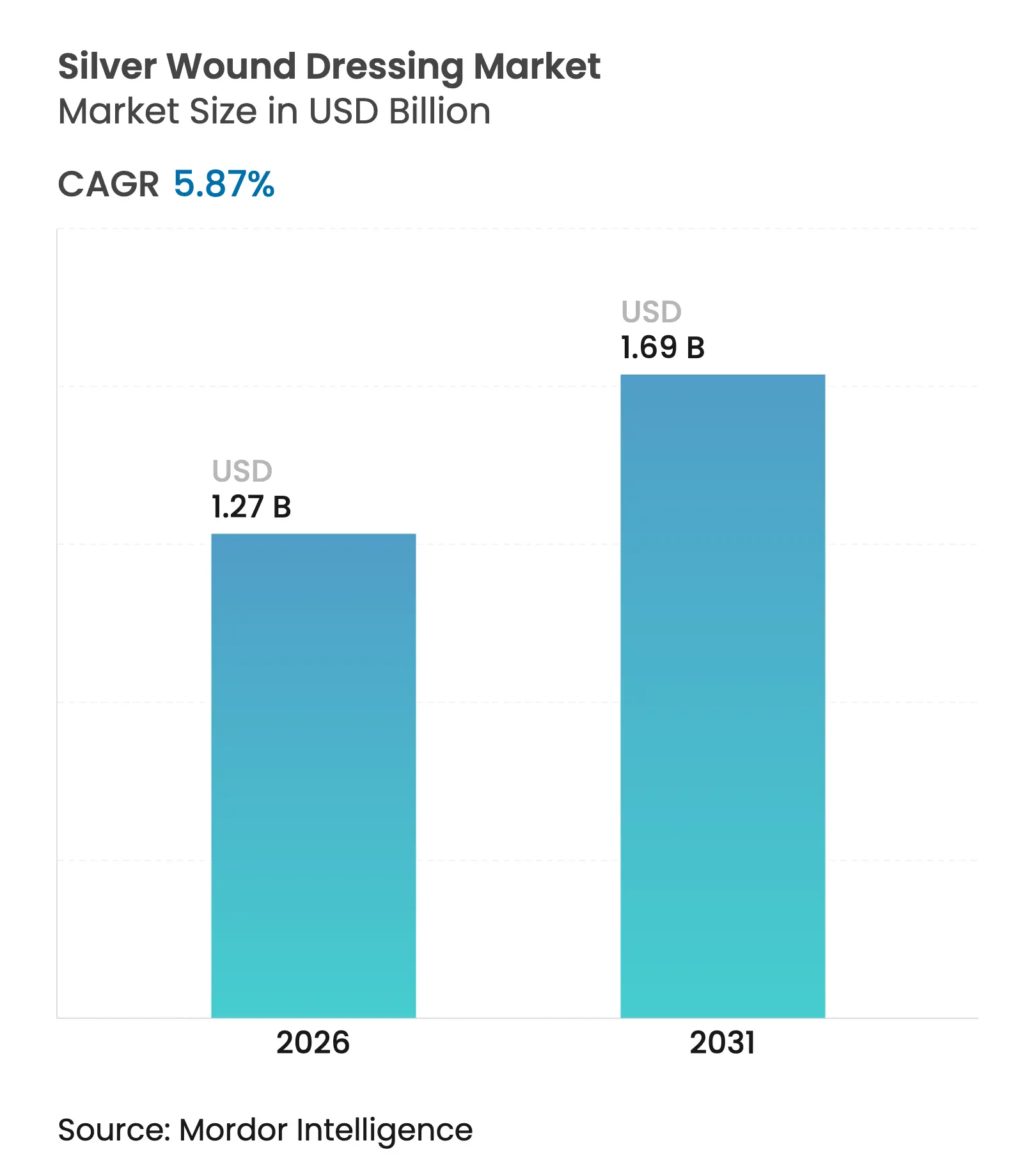

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 5.87 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Silver Wound Dressing Market Analysis by Mordor Intelligence

The silver wound dressings market size was valued at USD 1.20 billion in 2025 and estimated to grow from USD 1.27 billion in 2026 to reach USD 1.69 billion by 2031, at a CAGR of 5.87% during the forecast period (2026-2031). Rising caseloads of chronic wounds, the steady increase in elective surgeries among people over 65 years, and tightening hospital infection-control policies continue to underpin demand. Military field hospitals and disaster-relief centers procure high-silver dressings for rapid burn management, while nano-engineered formats are securing new procedural reimbursement codes that expand outpatient use. E-commerce channels are broadening direct-to-consumer access, allowing home-care patients to purchase advanced dressings quickly. On the supply side, market leaders are investing in lower-weight foam substrates and greener ionic-silver chemistries to comply with environmental discharge caps without sacrificing antimicrobial performance.

Key Report Takeaways

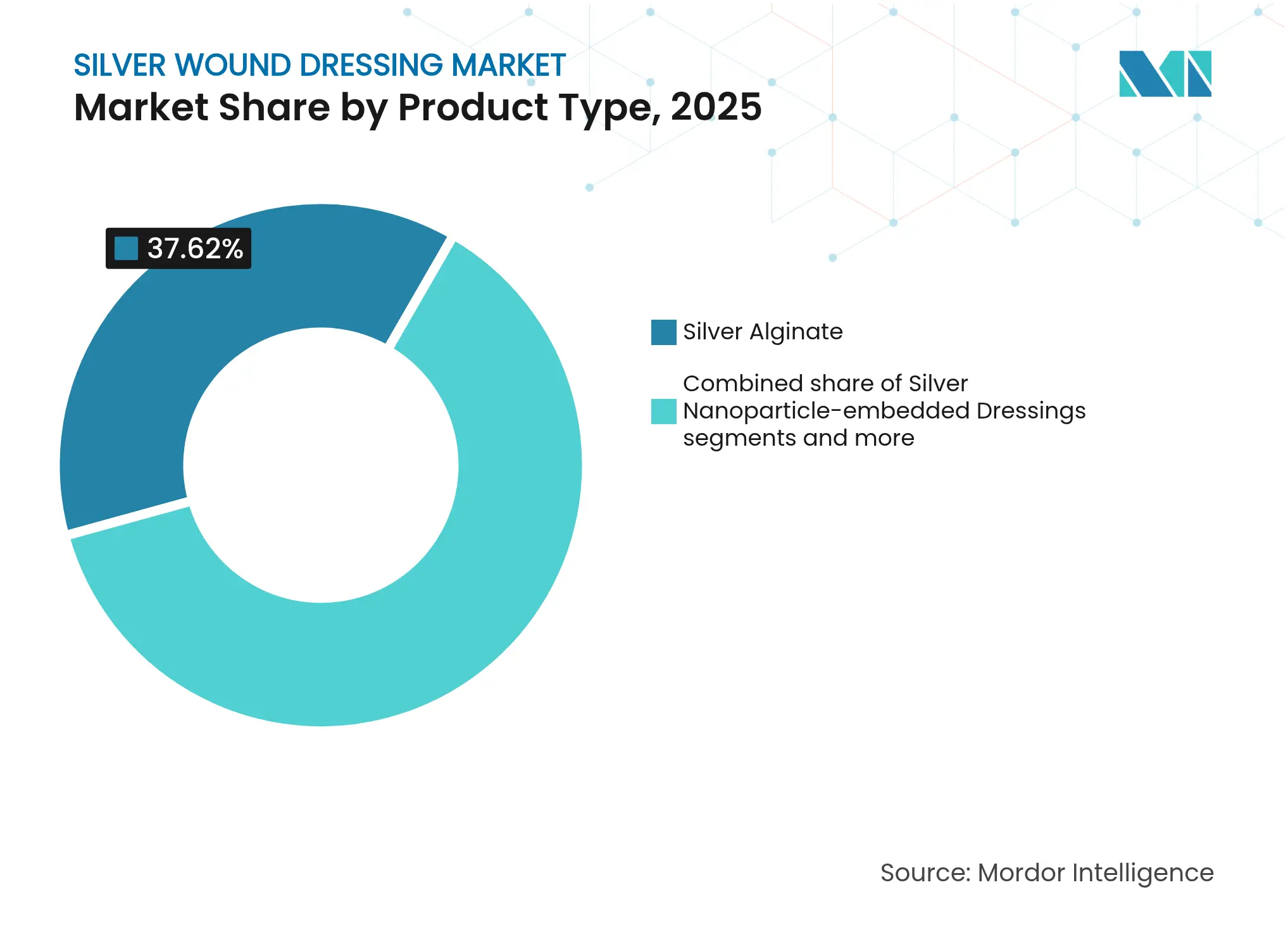

- By product type, silver alginate dressings led with 37.62% revenue share of the silver wound dressings market in 2025, Silver nanoparticle-embedded dressings are projected to advance at a 8.93% CAGR to 2031.

- By application, burns accounted for 30.88% of the silver wound dressings market size in 2025 and diabetic foot ulcers are expected to grow quickest at 9.08% through 2031.

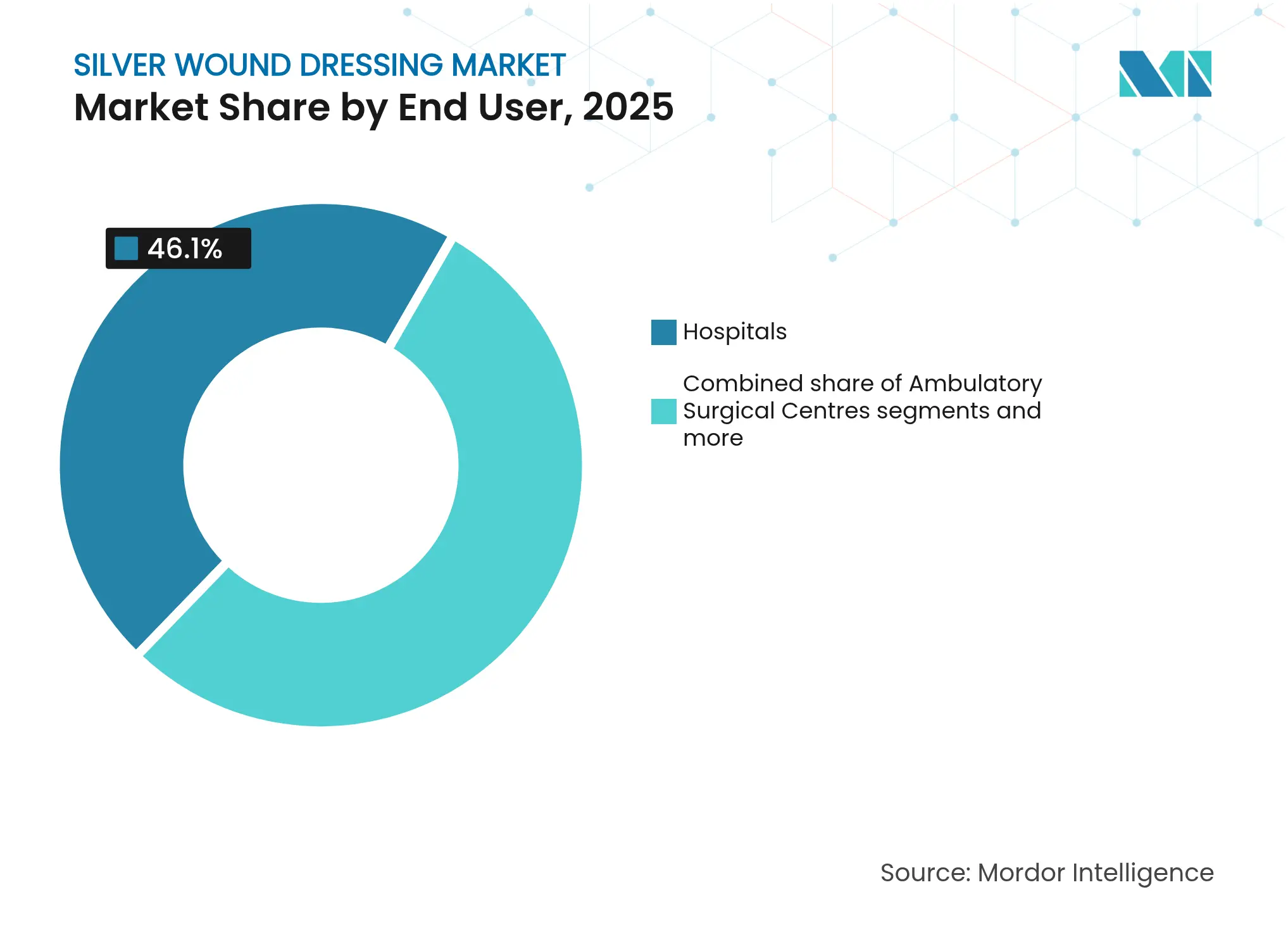

- By end user, hospitals held 46.10% of the silver wound dressings market share in 2025, whereas ambulatory surgical centers are set to expand at 10.65% CAGR during 2026-2031.

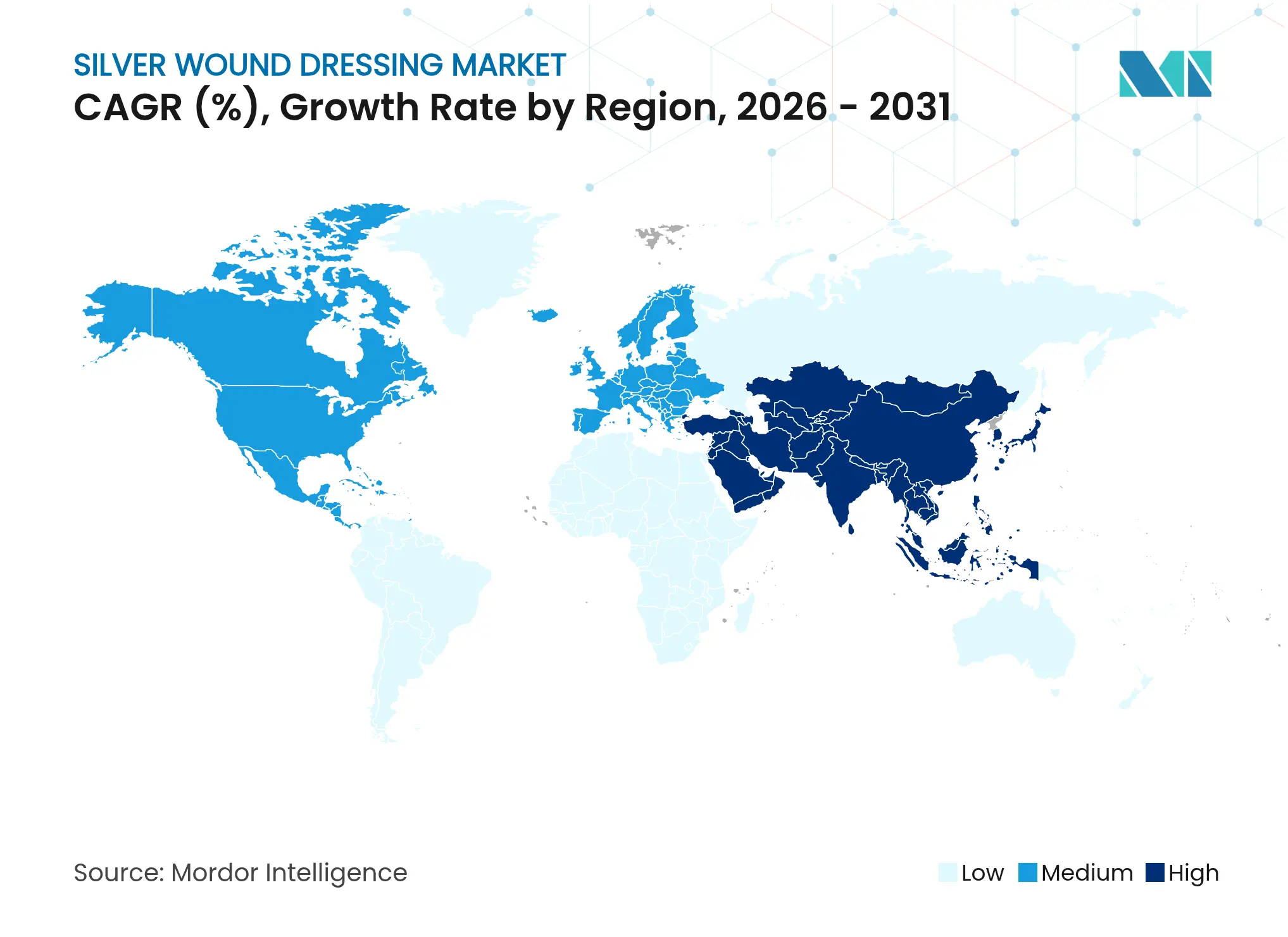

- By geography, North America captured 39.85% revenue share in 2025; Asia-Pacific is poised for the fastest 9.58% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silver Wound Dressing Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Chronic wounds & diabetes prevalence Chronic wounds & diabetes prevalence | +0.9% | North America, Asia-Pacific | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+0.9% | Geographic Relevance:North America, Asia-Pacific | Impact Timeline:Long term (≥ 4 years) |

Aging population fueling elective surgeries Aging population fueling elective surgeries | +0.7% | Europe, Japan, United States | Medium term (2-4 years) | |||

Hospital infection-control mandates favoring silver Hospital infection-control mandates favoring silver | +0.6% | Global | Short term (≤ 2 years) | |||

Military & disaster burn cases raising demand Military & disaster burn cases raising demand | +0.4% | Middle East, Africa, Latin America | Short term (≤ 2 years) | |||

Nano-engineered dressings enabling new codes Nano-engineered dressings enabling new codes | +0.5% | United States, Germany, South Korea | Medium term (2-4 years) | |||

E-commerce expansion of home-use dressings E-commerce expansion of home-use dressings | +0.3% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Prevalence of chronic wounds & diabetes

High sugar levels delay tissue repair, leading to recurrent foot ulcers among diabetics, a group that already represents more than 11% of the global adult population. Hospital audits in 2024 reported that 28% of inpatients with diabetes developed at least one chronic ulcer during their stay, prompting clinicians to shift from gauze to antimicrobially active therapies within the silver wound dressings market. The antimicrobial barrier lowers bacterial burden and shortens dressing-change intervals, which reduces nursing time. Payors in Canada and Germany accepted silver alginate codes for home-bound diabetics in 2023, broadening coverage. As prevalence rises, the therapy days per patient expand, sustaining bulk orders from group purchasing organizations. Combined, these factors elevate baseline purchasing across both acute and community settings.

Ageing population driving elective surgeries

The proportion of citizens aged 65+ surpassed 20% in Germany and Japan in 2024. Older adults undergo more orthopedic and cardiovascular procedures, surgeries that create incisions susceptible to infection. Hospital protocols now mandate silver foam dressings on prosthetic joint incisions for the first 48 hours, citing lower biofilm rates. U.S. ambulatory centers performing hip resurfacing also adopted nano-silver films after CMS reimbursed CPT code 15777 for bioactive implants in 2024. With surgical volumes climbing, demand for post-operative antimicrobial barriers follows, boosting the silver wound dressings market.

Hospital infection-control mandates favouring silver dressings

Joint Commission surveys revealed a 14% decrease in surgical site infections at institutions that included silver hydrocolloid products in standard peri-operative kits during 2023-2024. In response, hospital pharmacy & therapeutics committees added silver options to formularies, often under “infection-control” budgets immune to general cost-containment measures. Mandates typically require silver coverage for class III wounds and contaminated trauma cases. The resulting basket contracts lock in multi-year volumes and elevate average selling prices compared with standard gauze, supporting overall market expansion.

Military & disaster burn cases raising high-silver demand

Thermal injuries comprised 7% of casualties evacuated from conflict zones during 2024, according to NATO medical command updates. Field medics prefer high-silver alginate pads because they conform to irregular surfaces and sustain bactericidal concentrations for 72 hours. Similarly, wildfire-stricken regions in Australia stockpiled silver hydrogel rolls for mass casualty burns in 2025. Civil-military procurement programs often bypass traditional tenders, unlocking premium margins for suppliers while smoothing demand spikes after disasters.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Premium pricing vs. standard alternatives Premium pricing vs. standard alternatives | -0.6% | Emerging markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-0.6% | Geographic Relevance:Emerging markets | Impact Timeline:Long term (≥ 4 years) |

Environmental discharge regulations on ionic silver Environmental discharge regulations on ionic silver | -0.5% | Europe, Canada | Medium term (2-4 years) | |||

Antimicrobial stewardship limiting routine use Antimicrobial stewardship limiting routine use | -0.4% | United States, United Kingdom | Short term (≤ 2 years) | |||

Supply-chain competition for pharmaceutical-grade silver Supply-chain competition for pharmaceutical-grade silver | -0.3% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Premium pricing versus standard alternatives

Unit costs for high-silver foams remain 5-7 times higher than hydrocellular foams without antimicrobial agents, straining budgets for public hospitals in Brazil and India. Unless payors expand coverage, clinicians may reserve silver only for confirmed infection, lowering routine volume potential. Bulk purchasing agreements that bundle different advanced dressings partially offset price resistance, but sticker shock continues to hinder penetration among smaller clinics.

Environmental discharge regulations on ionic silver

The European Chemicals Agency placed ionic-silver compounds on its 2024 restricted substances roadmap, citing aquatic toxicity. Manufacturers exporting to the EU are investing in closed-loop recovery systems and lowering silver mass / cm² to meet discharge limits. Upgrades raise capital expenditures and could slow the rollout of new plants, restraining short-term supply expansion in the silver wound dressings market.

Segment Analysis

By Product Type: Silver Alginate Dominance and Nano-driven Upside

Silver alginate dressings accounted for 37.62% of the silver wound dressings market share in 2025, reflecting their high absorbency and compatibility with exudative ulcers. The segment benefits from favorable reimbursement in Japan and France and remains the first-line choice for venous leg ulcers. However, slowing growth in mature hospitals tempers volume. Silver nanoparticle-embedded dressings, though smaller by revenue, are set for the highest 8.93% CAGR, spurred by procedure-specific coding and thinner foam substrates that reduce per-case cost. Nano formulations require less elemental silver yet maintain efficacy, aligning with stewardship goals. Together, these opposing trajectories shape the near-term product mix and keep total segment revenues on an upward slope.

Innovation centers on hybrid structures that layer nano-silver within gelling fibers, improving conformability during joint movement. Leading vendors are filing for dual antimicrobial-anti-odor claims, aiming to capture outpatient podiatry clinics. With silver wound dressings market size allotted for product type anticipated to swell, suppliers that scale green chemistry plating processes stand to win hospital contracts that now include sustainability criteria. Competitive pricing pressure may intensify as Asian OEMs achieve ISO 13485 certification, enabling direct bids in the European tender market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Burns Lead, Diabetic Foot Ulcers Outpace

Burn management contributed 30.88% of the silver wound dressings market size in 2025. Specialized burn centers mandate silver foam because it minimizes dressing disruption, preserves newly formed epithelium, and delivers sustained antimicrobial activity, lowering graft failure rates. Demand spikes after natural disasters add to baseline consumption. Diabetic foot ulcers will exhibit the fastest 9.08% CAGR through 2031, buoyed by rising diabetes prevalence and expanded outpatient podiatry services. Payors in Canada and Saudi Arabia introduced bundled payments for multidisciplinary diabetic-wound care in 2024, explicitly covering advanced antimicrobials, which lifts adoption.

The pressure ulcers segment grows steadily as long-term-care facilities upgrade protocols to include silver hydrocolloid options for stage II-III sores. Surgical and traumatic wounds remain a stable share, but new OR-based stewardship rules cap prophylactic use in clean incisions. Venous leg ulcers continue to require absorptive alginate formats; however, compression therapy remains the primary driver of healing, keeping this indication’s growth moderate. Across applications, the silver wound dressings market size for infection-prone, high-exudate wounds commands premium pricing, cushioning revenue margins.

By End User: Hospitals Anchor, ASCs Gain Momentum

Hospitals held 46.10% of the silver wound dressings market share in 2025, supported by bundled procurement and standardized post-operative protocols. Teaching hospitals pioneer early adoption of nano-integrated foams, generating peer-review evidence that encourages community facilities to follow. Yet spending caps in public systems pressure formulary committees to negotiate deeper discounts, squeezing supplier margins. Ambulatory surgical centers (ASCs) will grow fastest at 10.65% CAGR as minimally invasive procedures migrate outward from hospitals. CMS reimbursement recognizes advanced dressings used in ASC-based debridement, driving initial orders even among smaller centers.

Specialty wound clinics leverage on-site hyperbaric oxygen therapy and advanced dressings to attract chronic-ulcer patients. Home healthcare expands through mail-order channels, where recurring consumption of silver hydrogels stabilizes demand. Military and emergency services comprise a niche segment but yield high per-unit revenue, especially for large-format burn sheets stocked in field kits. The shift toward outpatient settings suggests that suppliers refine packaging in smaller counts and develop educational content targeting non-hospital caregivers, sustaining the silver wound dressings market’s diversification.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 39.85% of global revenue in 2025, anchored by well-funded burn centers and integrated delivery networks that standardize silver dressing utilization. The United States alone represents over three-quarters of regional sales, supported by reimbursement codes C1846 and A6212-A6221 that cover various silver formats. Canada’s provincial health systems align formularies with national infection-prevention targets, further cementing silver adoption. Mexico, though smaller, reported 18% growth in advanced dressing imports after the public sector upgraded trauma hospitals in 2024.

Europe remains a mature yet innovation-oriented market. Germany, the United Kingdom, and France collectively account for nearly 70% of regional shipments. EU discharge directives push vendors toward lower-ion designs and eco-friendly coatings, reshaping product portfolios. Southern European countries, including Italy and Spain, still rely heavily on alginate categories due to favorable bulk-purchase contracts. Scandinavia’s e-health prescriptions facilitate direct shipments to home-care patients, adding a long-tail of repeatable sales.

Asia-Pacific will post the fastest 9.58% CAGR to 2031. China’s vast diabetic population and the government’s 2025 “Healthy Aging” roadmap spur hospital upgrades, creating steady tender volumes. India’s private-hospital boom increases elective surgery counts, opening opportunity for nano-silver films that reduce infection rates. Japan’s super-aged demographic continues to drive chronic ulcer management, but cost containment encourages switching to lower-silver hydrogels. South Korea rewards local manufacturing under its “K-Medtech” scheme, supporting domestic suppliers that co-brand with global leaders. Australia invests in disaster-preparedness stockpiles, ensuring burn-related demand remains robust. Across Asia-Pacific, growing disposable incomes and e-commerce penetration accelerate retail trade of single-use silver dressings, broadening the consumer base.

Latin America and the Middle East & Africa contribute smaller shares yet present niche opportunities. Brazil’s private insurers reimburse silver hydrogel interventions, while Argentina’s currency fluctuations complicate import planning. In the Gulf Cooperation Council, mandatory stock levels of burn dressings in trauma hospitals create predictable orders. South Africa’s mining injuries require antimicrobial exudate management, but public-sector budgets limit adoption beyond tertiary centers. Overall, diversified regional drivers balance the global silver wound dressings market trajectory.

Competitive Landscape

Market Concentration

Top suppliers include 3M, Smith & Nephew, Mölnlycke Health Care, and ConvaTec. Collectively they accounted for half of global sales in 2024, indicating moderate concentration. 3M reinforced its lead by integrating a silver-impregnated negative-pressure kit with its V.A.C. therapy in April 2024, improving healing times for complex wounds. Smith & Nephew launched a thinner silver alginate pad under the DURAFIBER brand in November 2024, positioned for diabetic foot clinics. Mölnlycke installed a closed-loop silver-ion capture system at its Finland plant in 2025 to meet EU discharge rules and secure eco-labels that influence hospital tenders.

Regional players such as Advancis Medical in the United Kingdom and Covalon Technologies in Canada leverage proprietary nanocrystal technologies to niche into outpatient niches. Kerecis, based in Iceland, blends cod-skin matrices with ionic silver, offering a biologic-antimicrobial hybrid that appeals to regenerative-medicine surgeons. Chinese OEMs scale private-label production under ISO 13485 and target Southeast Asian markets through online platforms. Competitive rivalry intensifies as e-commerce levels market access, prompting established firms to deepen service offerings like tele-wound-care support.

Price competition is tempered by strict regulatory requirements for antimicrobial claims, which elevate entry barriers. Suppliers emphasize clinical-evidence generation to maintain premium positioning, publishing randomized controlled trials in journals such as Wound Repair and Regeneration. Strategic partnerships with logistics-tech firms enable next-day delivery to outpatient centers and home-care agencies, adding a service moat around product portfolios. Overall, R&D focus converges on reducing elemental silver content while preserving efficacy, aligning with stewardship and environmental imperatives

Silver Wound Dressing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2023: Smith & Nephew partnered with the U.S. Army Medical Research Directorate to research on advanced wound management, orthopaedics and sports medicine

- May 2023: Advanced Medical Solutions Ltd initiated a clinical trial to confirm the safety and performance of Silver I Alginate Non-Woven Dressing (Hydro-Alginate) in chronic and acute wounds.

Table of Contents for Silver Wound Dressing Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Prevalence of chronic wounds & diabetes

- 4.2.2Ageing population driving elective surgeries

- 4.2.3Hospital infection-control mandates favouring silver dressings

- 4.2.4Military & disaster burn cases raising high-silver demand

- 4.2.5Nano-engineered silver dressings enabling new reimbursement codes

- 4.2.6E-commerce expansion of home-use advanced dressings

- 4.3Market Restraints

- 4.3.1Premium pricing versus standard alternatives

- 4.3.2Environmental discharge regulations on ionic silver

- 4.3.3Antimicrobial stewardship limiting routine silver use

- 4.3.4Supply-chain competition for pharmaceutical-grade silver

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Silver Alginate Dressings

- 5.1.2Silver Foam Dressings

- 5.1.3Silver Hydrocolloid Dressings

- 5.1.4Silver Hydrogel Dressings

- 5.1.5Silver Nanoparticle-embedded Dressings

- 5.1.6Others (e.g., Silver-plated Nylon)

- 5.2By Application

- 5.2.1Burns

- 5.2.2Diabetic Foot Ulcers

- 5.2.3Pressure Ulcers

- 5.2.4Surgical & Traumatic Wounds

- 5.2.5Venous Leg Ulcers

- 5.2.6Other Chronic Wounds

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Specialty Clinics

- 5.3.3Home Healthcare

- 5.3.4Ambulatory Surgical Centres

- 5.3.5Military & Emergency Services

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1GCC

- 5.4.5.2South Africa

- 5.4.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.13M Company

- 6.3.2Advancis Medical

- 6.3.3B. Braun Melsungen AG

- 6.3.4Bravida Medical (Silverlon)

- 6.3.5Cardinal Health, Inc.

- 6.3.6Coloplast A/S

- 6.3.7ConvaTec Group plc

- 6.3.8Covalon Technologies Ltd.

- 6.3.9Essity AB (BSN Medical)

- 6.3.10GEMCO Medical

- 6.3.11Hollister Incorporated

- 6.3.12Kerecis Ehf

- 6.3.13Medline Industries LP

- 6.3.14Milliken & Company

- 6.3.15Mölnlycke Health Care AB

- 6.3.16Smith & Nephew plc

- 6.3.17Urgo Medical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Silver Wound Dressing Market Report Scope

As per the report's scope, silver wound dressings are topical wound care products derived from ionic silver. It provides a moist wound environment that promotes wound recovery. The topical antimicrobial silver dressing is apt for the treatment of infected wounds. It is especially found to be most effective in wounds with bioburden or local infection and its risk.

The silver wound dressing market is segmented by product type, disease, end user, and geography. By product type, the market is segmented into hydrofiber silver dressings, nanocrystalline silver dressing, silver plated nylon fiber dressing, silver nitrate dressing, silver alginate dressing, and other product types. By disease, the market is segmented into burns, ulcers, cuts and lacerations, and other wound types. By end user, the market is segmented into inpatient and outpatient facilities. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.