Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

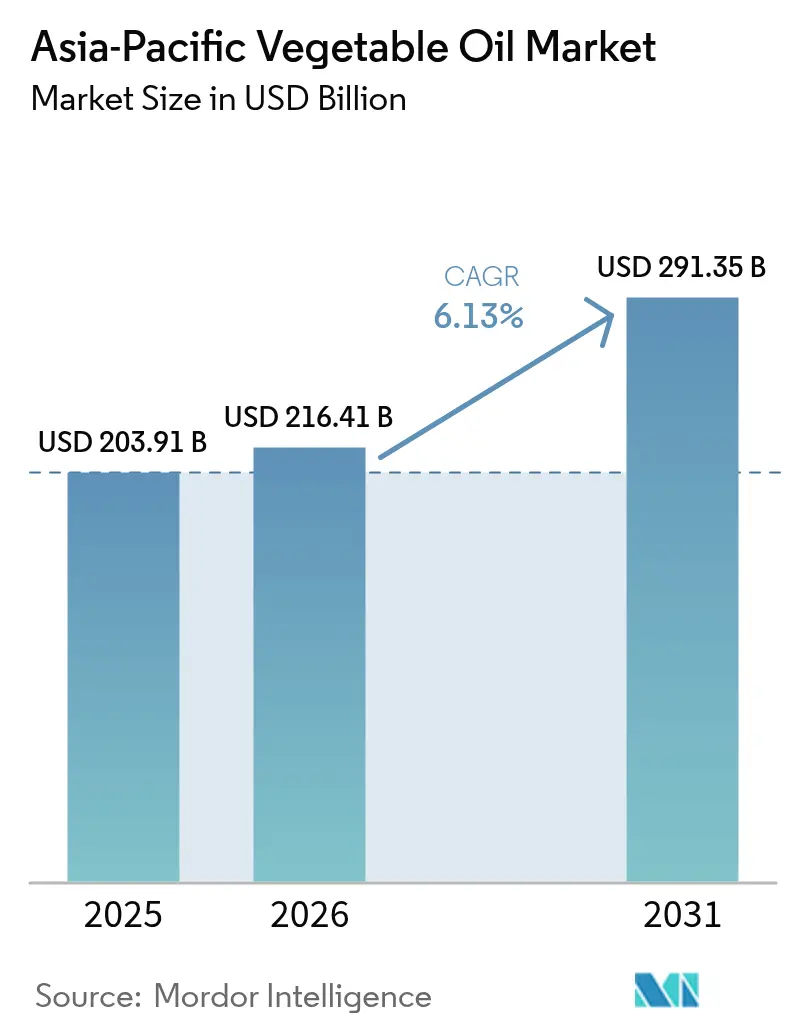

| Base Year Market Size (2025) | USD 203.91 Billion |

| Market Size (2026) | USD 216.41 Billion |

| Market Size (2031) | USD 291.35 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Vegetable Oil Market Analysis by Mordor Intelligence

Asia-Pacific vegetable oil market size in 2026 is estimated at USD 216.41 billion, growing from 2025 value of USD 203.91 billion with 2031 projections showing USD 291.35 billion, growing at 6.13% CAGR over 2026-2031. The expansion of food-service industries and government-mandated biodiesel blending programs drives this growth. Consumers are increasingly opting for healthier and minimally processed oils, which has contributed to the rapid growth of sunflower oil, making it the fastest-growing product in the market. At the same time, producers are focusing on sourcing traceable raw materials to comply with stricter regulations, such as the European Union Deforestation Regulation and country-specific labeling laws. In terms of product types, palm oil remains the dominant market player, while sunflower oil is experiencing a surge in demand. By application, food-related uses remain the largest segment, but non-food applications, such as biodiesel production, are also growing rapidly. The Asia-Pacific vegetable oil market is moderately fragmented, with numerous players competing to meet the evolving demands of consumers and regulatory requirements.

Key Report Takeaways

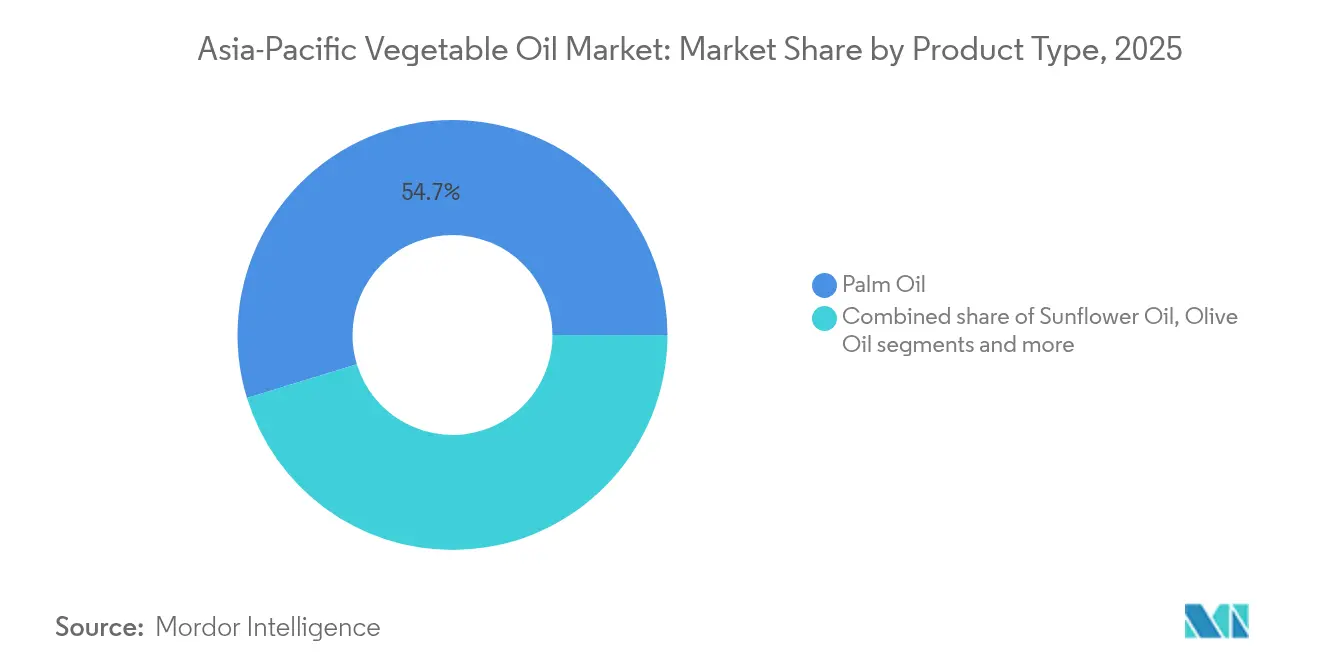

- By product type, palm oil led the Asia-Pacific vegetable oil market with a 54.74% share in 2025, while sunflower oil is forecast to expand at a 7.27% CAGR through 2031.

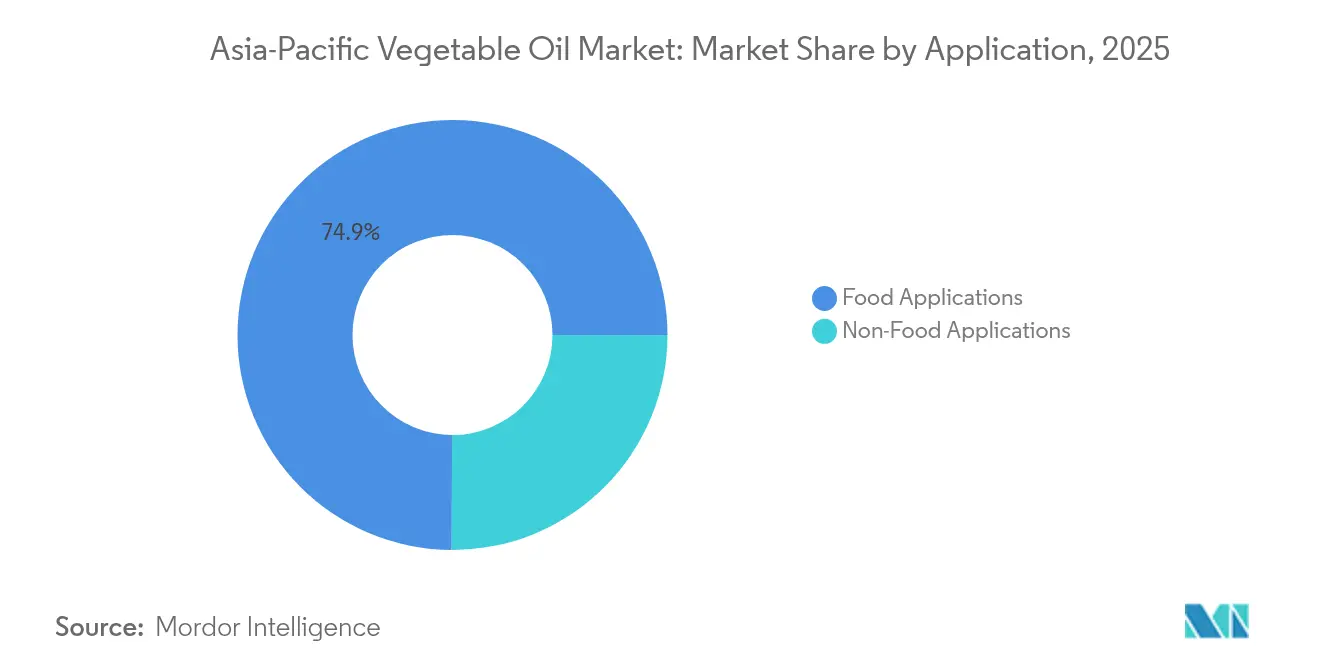

- By application, food applications accounted for 74.94% of the Asia-Pacific vegetable oil market share in 2025, whereas non-food applications are projected to advance at an 7.99% CAGR through 2031.

- By country, China accounted for 35.62% of the Asia-Pacific vegetable oil market size in 2025, and India is projected to grow at a 7.65% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Vegetable Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Changing dietary habits and greater health consciousness | +0.9% | Effects in urban China, India, and Southeast Asia | Medium term (2-4 years) |

| Rising popularity of fried, fast, and convenience foods | +1.2% | Asia-Pacific core, particularly Indonesia, Philippines, Thailand, Vietnam | Short term (≤ 2 years) |

| Strong growth of biodiesel and renewable fuel programs | +1.5% | Indonesia, Malaysia, Thailand; spillover to India and China | Long term (≥ 4 years) |

| Rising awareness of fortified and heart-healthy oils | +0.7% | Japan, South Korea, Australia, urban India | Medium term (2-4 years) |

| Increasing use of vegetable oils in pharmaceuticals manufacturing | +0.5% | China, India, Japan; export-oriented hubs in Singapore | Long term (≥ 4 years) |

| Shift towards clean-label and minimally processed oils | +0.6% | Australia, New Zealand, Singapore, urban China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of fried, fast, and convenience foods

The Asia-Pacific vegetable oil market is growing steadily as fried, fast, and convenience foods become a regular part of diets in both households and the food service sector. In India, approximately 38% of consumers frequently consume fried snacks and processed foods, as reported by Down To Earth Org in May 2024[1]Source: Down To Earth Org, "38% Indians Consume Fried Snacks And Processed Foods, Only 28% Consume Healthy Food", downtoearth.org.in. Advancements in cold chain infrastructure across the region are enabling businesses to purchase larger quantities of oils while minimizing spoilage risks. Many quick-service restaurant chains are gradually introducing blends of sunflower oil and rice bran oil to offer healthier alternatives with lower saturated fat content. In Japan, the hotel, restaurant, and institutional food service industry experienced growth of approximately 16% in 2023, reaching a market size of around USD 226.2 billion, as per the United States Department of Agriculture[2]Source: United States Department of Agriculture, "Biofuels Annual", apps.fas.usda.gov. This growth highlights the rising demand for high-performance oils that can endure repeated heating without compromising quality.

Strong growth of biodiesel and renewable fuel programs

Biodiesel and renewable fuel mandates are significantly influencing the Asia-Pacific vegetable oil market. For example, Indonesia’s B40 program, as reported by the East Asia Forum Organization, redirected around 13.9 million tonnes of crude palm oil from food-related uses in 2024[3]Source: East Asia Forum Organization, "Indonesia’s Biofuel Bet Risks Backfiring", eastasiaforum.org. The country is also moving forward with trials for its B50 program, which aims to further increase the blending of biodiesel with conventional fuels. Similarly, Malaysia has implemented its B30 initiative, while Thailand has introduced blending programs ranging from B7 to B20. These efforts reflect a regional push to promote the use of palm-based biodiesel as a renewable energy source. The primary goals of these mandates are to reduce greenhouse gas emissions and improve energy security by decreasing reliance on fossil fuels. These programs create a steady demand for vegetable oils, regardless of changes in food consumption patterns.

Rising awareness of fortified and heart-healthy oils

Awareness of fortified and heart-healthy oils is growing rapidly across the Asia-Pacific region, driven by mandatory fortification programs in countries like India, Australia, and Vietnam. These programs have increased the demand for oils enriched with nutrients such as omega-3, phytosterols, and fat-soluble vitamins. In China, approximately 50.7% of adults were reported as overweight or obese in 2023, according to PubMed Central[4]Source: PubMed Central, "The Impact of Chinese Adults’ Food Literacy on Healthy Eating Intentions Based on the Planned Behaviour Theory", pmc.ncbi.nlm.nih.gov. This growing health concern is prompting consumers to adopt healthier eating habits, thereby increasing demand for nutrient-rich oil products. Japan and South Korea lead in the consumption of premium oils, such as sesame, perilla, and rice bran oils, which are valued for their antioxidant-rich properties and health benefits. Technological advancements, such as microencapsulation, are enhancing the stability of omega-3 ingredients during high-heat cooking, thereby addressing previous challenges related to oxidative instability in fortified oils.

Shift towards clean-label and minimally processed oils

The Asia-Pacific vegetable oil market is shifting toward clean-label and minimally processed oils as consumers increasingly prioritize ethical and environmental factors in their purchasing decisions. The demand for cold-pressed and single-origin oils is growing, driven by their perceived health benefits and the expansion of shelf space in major retail chains across Australia, New Zealand, and tier-1 cities in China. To meet these evolving consumer preferences, blockchain-enabled traceability systems are being implemented. Initially adopted by Malaysian plantations to comply with the European Union's regulations on deforestation, these systems are now being extended to retail products. Branded oil packs feature QR codes that enable consumers to trace each bottle back to its farm-level origin, thereby enhancing transparency and trust.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited availability of certified organic oilseeds in the region | -0.4% | Acute in China, India, Indonesia | Medium term (2-4 years) |

| Negative perception of palm oil due to health and sustainability concerns | -0.8% | Australia, New Zealand, urban China, Japan, South Korea | Long term (≥ 4 years) |

| Regulatory inconsistencies for sustainability and labeling claims | -0.5% | ASEAN member states, spillover to China and India | Medium term (2-4 years) |

| Growing interest in functional foods that reduce dependency on added oils | -0.6% | Japan, South Korea, Australia, urban India and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Negative perception of palm oil due to health and sustainability concerns

In the Asia-Pacific vegetable oil market, palm oil is facing growing criticism due to concerns about health and environmental sustainability. Its high saturated fat content has raised health-related concerns among consumers, particularly those focused on heart health, despite studies suggesting it has neutral effects on cardiovascular health when consumed in moderation. Additionally, stricter deforestation regulations in the European Union have increased global scrutiny of palm oil production practices. As a result, many multinational companies in the region are shifting toward using palm oil certified by organizations such as RSPO (Roundtable on Sustainable Palm Oil) or MSPO (Malaysian Sustainable Palm Oil), or are opting for alternative oils that are perceived as more environmentally friendly. Furthermore, audits have revealed compliance issues among smaller palm oil producers, which has further impacted the competitiveness of palm oil.

Growing interest in functional foods that reduce dependency on added oils

The Asia-Pacific vegetable oil market is facing challenges as consumers increasingly shift toward healthier eating habits and reduce their reliance on added oils. The growing popularity of air fryers in countries like China, Japan, and South Korea is encouraging households to adopt low-fat cooking methods. Food manufacturers are moving toward producing baked snacks and spray-dried seasonings, which require less oil compared to traditional cooking methods. In Japan, older consumers are showing a preference for nutrient-dense foods, while clean eating trends in Australia are further reducing the demand for oil-heavy food products. These changes are leading to a slowdown in the per capita consumption of conventional edible oils. However, despite this trend, there is a growing demand for premium and value-added oil variants, which is helping to offset some of the decline in traditional oil consumption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Palm Dominance Meets Sunflower Surge

Palm oil is expected to continue dominating the Asia-Pacific vegetable oil market in 2025, accounting for approximately 54.74% of the market share. Its strong demand is driven by its extensive use in cooking, packaged foods, and food services. Biodiesel programs, such as Indonesia’s B40 initiative, have significantly boosted industrial demand, redirecting approximately 13.9 million tonnes of crude palm oil from edible uses. This dual demand from both the food and fuel sectors ensures steady growth, making the palm oil market less vulnerable to changes in edible oil consumption trends.

Sunflower oil is emerging as the fastest-growing product in the Asia-Pacific vegetable oil market, with a projected CAGR of nearly 7.27% through 2031. Its popularity is increasing due to its health benefits, such as being heart-friendly and having a lighter flavor, which appeals to health-conscious consumers. The rapid growth of modern retail channels in countries like Australia, India, China, and Southeast Asia has made sunflower oil more accessible to a wider audience. As consumers shift toward oils with lower saturated fat content, sunflower oil is gaining traction in both premium and mid-range market segments across the region.

By Application: Food Channels Lead, Non-Food Accelerates

In 2025, food applications accounted for approximately 74.94% of the Asia-Pacific vegetable oil market, highlighting their importance in the region. The food processing industry drives this demand by using vegetable oils in products such as baked goods, snacks, and confectionery, where they serve as spray oils, emulsifiers, and trans fat-free shortenings. The increasing demand for packaged foods and the rapid expansion of food service outlets further contribute to the dominance of edible applications. This steady demand ensures a continuous and reliable need for various types of vegetable oils throughout the year.

Non-food applications are expected to grow at a faster rate, with a projected CAGR of 7.99% through 2031, outpacing the growth of edible uses. This growth is largely driven by the energy and industrial sectors, particularly biodiesel programs such as Indonesia’s B40 and Malaysia’s B30, which require substantial quantities of vegetable oils. These initiatives not only stabilize prices but also attract investments in refining and processing infrastructure. As Southeast Asian countries strengthen their energy policies, non-food applications are expected to play an increasingly important role in the region's overall vegetable oil demand.

Geography Analysis

China accounted for 35.62% of the Asia-Pacific vegetable oil market share in 2025, driven by its position as the largest global importer of palm and soybean oils. Tier-1 cities in China are increasingly opting for healthier alternatives, such as sunflower and rapeseed oils. India ranked as the second-largest consumer, while Indonesia and Malaysia dominated regional supply with their integrated plantation-to-refinery systems catering to both edible and biodiesel needs. Japan and South Korea contributed to the premium segment, driven by high demand for sesame, perilla, and rice-bran oils, which are valued for their antioxidant properties. Australia and New Zealand focused on niche markets, offering cold-pressed rapeseed and sunflower oils targeted at affluent consumers. These mature markets set benchmarks for labeling, fortification, and traceability, which smaller markets are beginning to adopt.

India is expected to grow at a 7.65% CAGR through 2031, making it the fastest-growing market in the region. This growth is supported by tariff protections and a government initiative worth Rs 10,100 crore aimed at doubling domestic oilseed production to 25.45 million tonnes by 2030-31. Indonesia’s biodiesel policies continue to drive demand, although growth is slowing as studies on engine compatibility influence the transition from B40 to B50 biodiesel blends. Malaysia anticipates steady growth as 95% of its plantations are expected to comply with MSPO Version 2 certification by the end of 2025, aligning with EU deforestation regulations. China is projected to see moderate growth, with rising incomes in smaller cities balancing a shift toward lower-fat cooking methods. Japan and South Korea are experiencing slower growth, but their focus on premium products helps maintain value sales despite stagnant volumes.

Emerging markets such as Vietnam, the Philippines, and Singapore are becoming key demand hubs, leveraging free-trade agreements and advanced port logistics to act as transshipment and re-export centers. Thailand has gained prominence after the World Health Organization endorsed its industrial trans-fat ban in 2024, encouraging local refiners to supply reformulated oils across the Indochina region. Bangladesh and Pakistan are witnessing increased imports due to population growth and rising urban snack consumption, which are expanding their market base. Meanwhile, Cambodia and Laos are opening new opportunities for branded small-pack vegetable oils through the growth of modern retail outlets. These developing markets are focusing on flexible packaging, affordable sachet sizes, and traceability measures to meet diverse regulatory requirements in the Asia-Pacific vegetable oil market.

Competitive Landscape

The Asia-Pacific vegetable oil market is moderately fragmented, with global traders continuing to dominate the supply chain. However, regional players, such as Wilmar International Ltd. and COFCO Group, have adopted plantation-to-refinery models to reduce costs and improve efficiency. In 2024, Bunge expanded its operations in India by adding multi-oil processing capacity, ensuring flexibility and compliance with India’s fortification regulations. Olam Agri, a major palm oil supplier to India and Bangladesh, diversified its sourcing from Sumatra and Kalimantan to mitigate risks. Smaller companies are focusing on organic, cold-pressed, and fortified products to cater to the consumers who prioritize ethical purchasing decisions.

Companies in the market are adopting strategies such as integrating backward into plantations, expanding forward into branded retail products, and pursuing mergers to achieve scale. Pharmaceutical-grade and oleochemical products are experiencing the fastest growth, attracting new players to the market. Emerging technologies, such as precision fermentation and digital traceability, are expected to bring about significant long-term changes. Established players are leveraging advanced tools like AI-driven procurement, drones, and satellite imagery to reduce logistics costs and improve yield predictions across the region.

Technological advancements and strategic initiatives are shaping the competitive landscape of the Asia-Pacific vegetable oil market. Companies are increasingly focusing on sustainability and innovation to meet evolving consumer demands and regulatory requirements. By adopting modern technologies and diversifying their product portfolios, market players are positioning themselves to capitalize on growth opportunities while addressing challenges such as supply chain risks and compliance with international standards.

Asia-Pacific Vegetable Oil Industry Leaders

-

Wilmar International Ltd

-

COFCO Group

-

Musim Mas Holdings

-

Golden Agri-Resources Ltd

-

Fuji Oil Holdings Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Portugal’s premium olive oil brand, Coração do Vale, made its entry into the Indian market importing a 1,000-case container each month to cater to the growing demand for high-quality olive oil in the region.

- March 2025: Patanjali Foods Ltd. planned to set up an oil palm mill in Mizoram. This initiative aligned with the company's strategy to strengthen its presence in India's edible oil retail market.

- January 2025: Hindustan Unilever (HUL) announced the acquisition of the palm operations of Vishwatej Oil Industries, located in Kamareddy district, Telangana. This strategic move aligned with HUL's broader initiative to localize palm oil production.

- October 2024: Italian brand Tenuta Sant'Ilario introduced its premium olive oil to the South Korean market, specifically in Seoul. This launch marked the brand's strategic entry into the growing demand for high-quality olive oil in the region

Asia-Pacific Vegetable Oil Market Report Scope

The Asia-Pacific vegetable oil market is segmented by Product Type, Application, and Country. Based on Product Type, the market is segmented into palm oil, soybean oil, rapeseed oil, sunflower oil, olive oil, and others. Based on the application, the market studied is segmented into food applications and non-food applications. Based on country, the market studied is segmented into China, India, Japan, South Korea, Australia, Indonesia, Thailand, Vietnam, the Philippines, Malaysia, Singapore, New Zealand, and the Rest of the Asia-Pacific.

By Product Type

| Palm Oil |

| Soybean Oil |

| Rapeseed Oil |

| Sunflower Oil |

| Olive Oil |

| Others |

By Application

| Food Applications | Food Processing |

| HoReCa | |

| Retail | |

| Non-Food Applications | Biodiesel |

| Personal Care and Cosmetics | |

| Animal Feed | |

| Others |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Malaysia |

| Singapore |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Palm Oil | |

| Soybean Oil | ||

| Rapeseed Oil | ||

| Sunflower Oil | ||

| Olive Oil | ||

| Others | ||

| By Application | Food Applications | Food Processing |

| HoReCa | ||

| Retail | ||

| Non-Food Applications | Biodiesel | |

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Others | ||

| By Country | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Malaysia | ||

| Singapore | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific vegetable oil market in 2026?

It is valued at USD 216.41 billion in 2026 and is projected to grow to USD 291.35 billion by 2031.

Which product grows fastest in the region?

Sunflower oil is forecast to post a 7.27% CAGR, the quickest among major oil types.

Why is India’s market expanding rapidly?

Population growth, tariff protection and an INR 10,100-crore plan to double domestic oilseed output lift India at a 7.65% CAGR.

What drives non-food demand for vegetable oils?

Government biodiesel mandates such as Indonesia’s B40 absorb sizable palm volumes and support oleochemical and pharmaceutical applications.

Page last updated on: