Sulfur Dioxide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

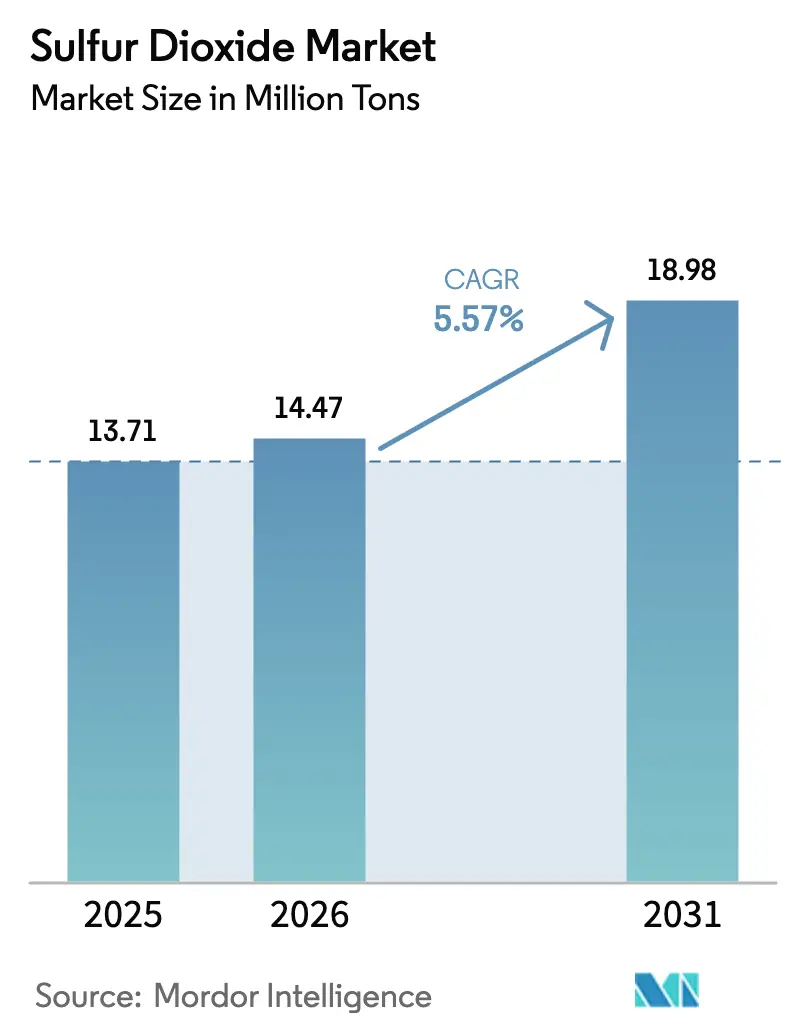

| Market Volume (2026) | 14.47 Million tons |

| Market Volume (2031) | 18.98 Million tons |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sulfur Dioxide Market Analysis by Mordor Intelligence

The Sulfur Dioxide Market size was valued at 13.71 million tons in 2025 and is estimated to grow from 14.47 million tons in 2026 to reach 18.98 million tons by 2031, at a CAGR of 5.57% during the forecast period (2026-2031). Tight integration between legacy chemical-intermediate demand and high-purity electronics uses is widening price bands across grades, while form-factor preferences are shifting toward solid bisulfites for logistics safety. Semiconductor-grade consumption is scaling with record wafer-fab capital expenditure, even as fertilizer-linked sulfuric-acid tonnage retains volume leadership. Asia-Pacific dominates thanks to new sulfur-burn units feeding fertilizer, battery-metal leaching, and advanced-node fabs, with India and China each adding sulfuric-acid capacity tied to phosphate and nickel value chains. Supply risks stem from coal-plant retirements curbing flue-gas desulfurization by-product recovery, nudging merchant prices upward and favoring vertically integrated producers able to swing between commodity and ultra-high-purity output.

Key Report Takeaways

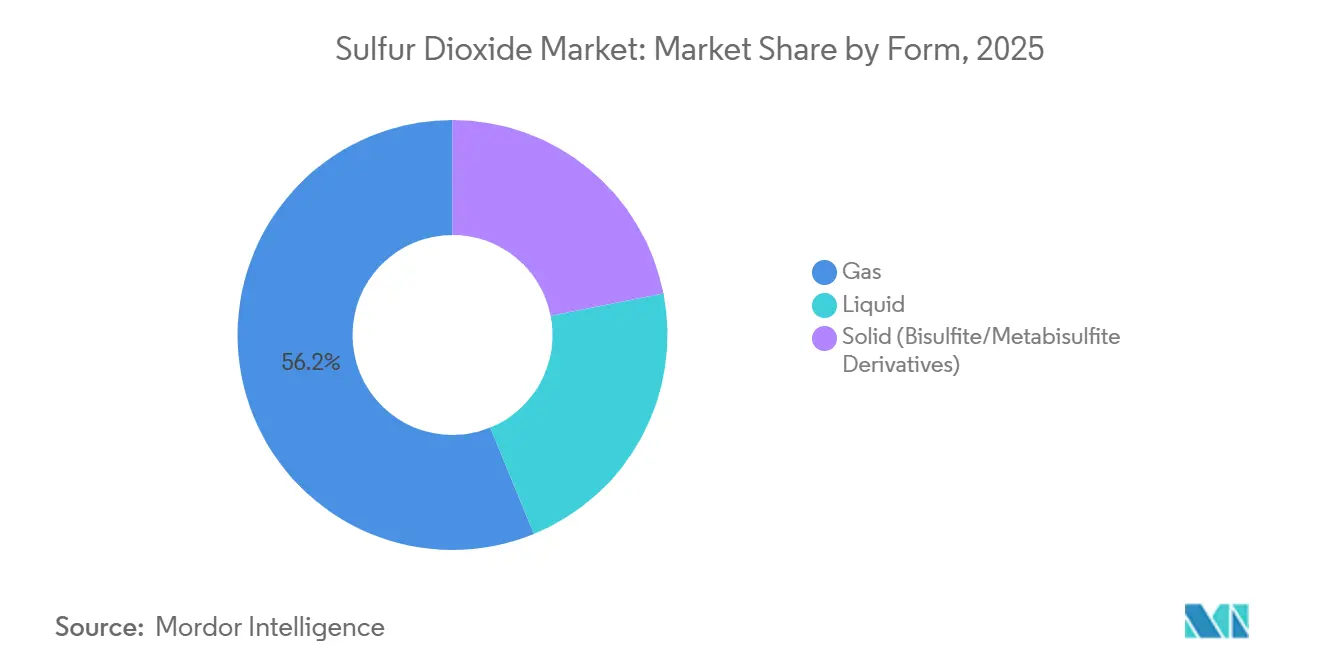

- By form, gas held 56.18% of the Sulfur Dioxide market share in 2025, while solid (bisulfite/metabisulfite derivatives) are forecast to expand at a 5.87% CAGR during the forecast period (206-2031).

- By purity grade, less than 99% (technical grade) accounted for 48.94% of the Sulfur Dioxide market size in 2025, while greater than 99% (ultra-high-purity grades) are projected to grow at a 5.98% CAGR during the forecast period (206-2031).

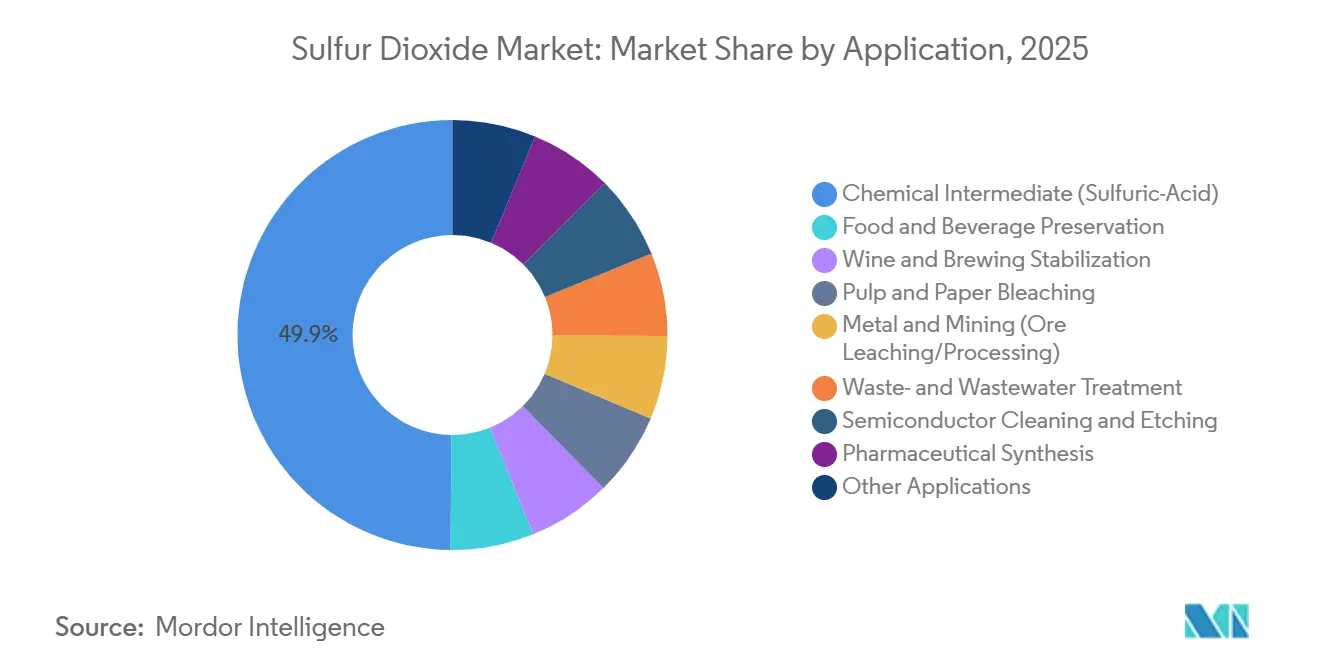

- By application, chemical intermediate (sulfuric acid) contributed 49.86% of the Sulfur Dioxide market size in 2025, while semiconductor cleaning and etching is advancing at a 6.15% CAGR during the forecast period (206-2031).

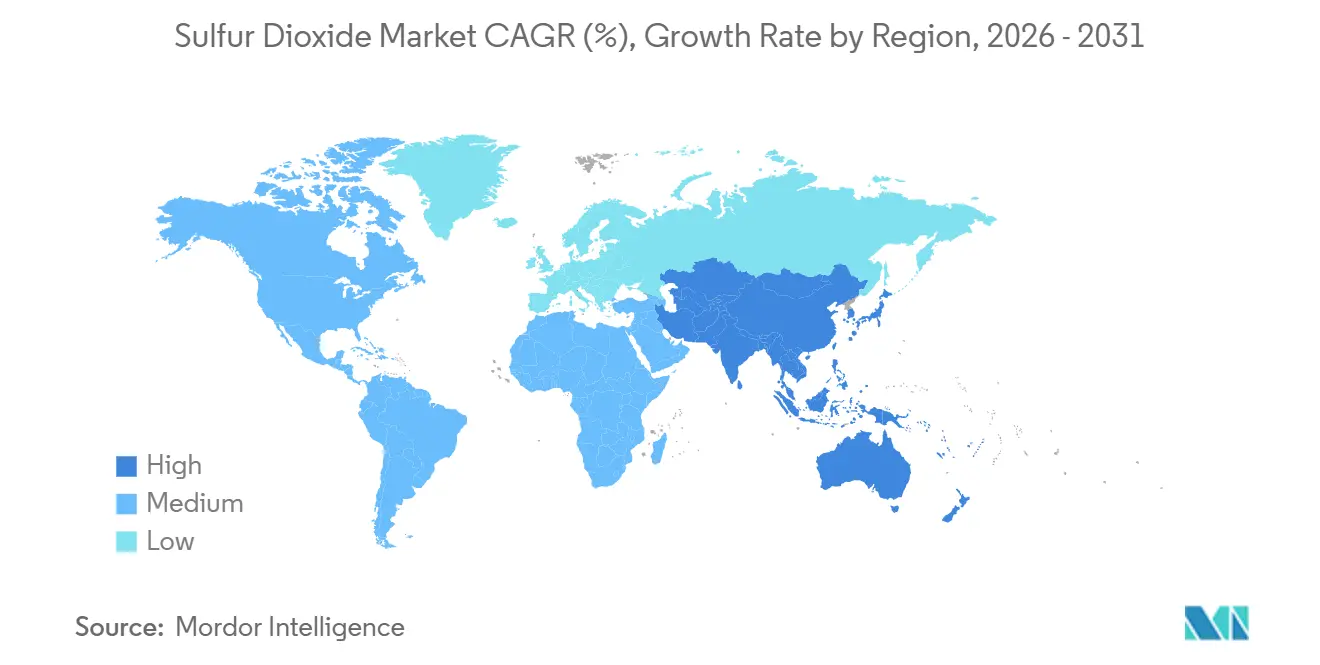

- By geography, Asia-Pacific commanded 50.46% of the Sulfur Dioxide market share in 2025 and is progressing at a 6.04% CAGR during the forecast period (206-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sulfur Dioxide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use in sulfuric-acid and chemicals | +2.1% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Expansion of pulp and paper bleaching capacity | +0.9% | Asia-Pacific, South America, Nordic Europe | Medium term (2-4 years) |

| Industrial disinfectant and fumigant adoption | +0.6% | Global, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Surge in synthetic gypsum for green building | +0.8% | Asia-Pacific core, North America secondary | Medium term (2-4 years) |

| Emerging SO₂-based battery electrolyte additives | +0.3% | Asia-Pacific pilot programs, North America R&D labs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Use in Sulfuric-Acid and Chemicals

Sulfuric-acid manufacturing anchors global SO₂ offtake because no substitute exists for phosphate-fertilizer acidulation or copper-ore leaching. India added 1.2 million tons per annum of new acid capacity across Coromandel International, Paradeep Phosphates, and Gujarat State Fertilizers during 2024-2025, each tied to captive rock-phosphate conversion. China’s spot sulfuric-acid price rose from CNY 400/ton (USD 54.50/ton) in Q1 2025 to CNY 520/ton (USD 73.78/ton) by December as Middle-East sulfur exports tightened. Hydrometallurgical nickel laterite leaching at Morowali and Weda Bay consumed 800,000 tons of acid in 2025, up 33% on higher EV-grade nickel-sulfate output. Semiconductor-grade acid, derived from more than 99.9% SO₂, commands 3 to 5 times technical-grade pricing, prompting BASF to expand ultra-pure capacity at Ludwigshafen in April 2025. The dichotomy of high-volume fertilizer cycles versus high-margin electronics uses is locking the Sulfur dioxide market into a two-track structure that persists through 2031.

Expansion of Pulp and Paper Bleaching Capacity

Pulp mills in Asia and South America are outpacing Western closures, driving incremental SO₂ demand. Grasim’s 750 tons per day dissolving-pulp line at Vilayat integrates sulfite pulping for viscose fiber, while Shandong Bohui added 500,000 tons per annum bleached-kraft output adopting SO₂ sequences in 2025. Norske Skog’s Skogn mill cut specific SO₂ emissions to 12.3 kg per air-dried ton in 2025 via scrubber upgrades. Nouryon and Arauco are piloting closed-loop bisulfite regeneration in Brazil, targeting a 30% cut in fresh sulfur. Regulatory frameworks such as the EU Industrial Emissions Directive and China’s sector rules necessitate flue-gas scrubbers, reinforcing medium-term growth[1]Nouryon, “Bisulfite Regeneration Pilot Program,” nouryon.com.

Industrial Disinfectant and Fumigant Adoption

SO₂ fumigation remains the preferred method for preserving grapes, dried fruits, and select wines because it penetrates deeply and dissipates under ventilation. EFSA’s Nov 2025 assessment confirmed safety below 2,000 milligrams per kilogram thresholds, while the US Food and Drug Administration (FDA) retains identical limits for dried fruits and 150-300 milligrams per kilogram for wine classes. Waste-water plants in Arcata, CA, and Forest City, NC, documented routine SO₂ dechlorination in 2025 facility reports. ASEAN produce exporters still favor SO₂ over phosphine for rapid, low-residue treatment. Near-term expansion hinges on food-safety compliance, with longer-term uptake moderated by emerging antimicrobials[2]EFSA Panel, “Use of Sulfites in Dried Apricots,” efsa.europa.eu.

Surge in Synthetic Gypsum for Green Building

FGD scrubbers create synthetic gypsum that wallboard makers prize for purity and proximity. China mandated more than or equal to 30% recycled content in Tier-1 residential non-structurals from 2025, while the US Environmental Protection Agency (EPA)’s Coal Combustion Residuals rule treats Flue Gas Desulfurization (FGD) gypsum as beneficial use. Yet 15-20 GW of European coal closures in 2025-2026 are tightening supply and pushing natural-gypsum imports higher. India generated 25 million tons of FGD gypsum in 2025 with 70% utilization after cement and wallboard offtakes. Regions retiring coal face a paradox of recycled-content mandates but shrinking by-product streams, lifting price volatility through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health hazards and complex handling | -0.7% | Global, with stricter enforcement in North America and EU | Short term (≤ 2 years) |

| Phase-out of coal power curbing captive supply | -0.9% | Europe primary, North America secondary, China plateau | Medium term (2-4 years) |

| Electrochemical substitutes in semiconductor etching | -0.4% | Asia-Pacific fab clusters, North America pilot lines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Hazards and Complex Handling

SO₂ is a severe respiratory irritant; OSHA (Occupational Safety and Health Administration) caps 8 hours of exposure at 5 parts per million (ppm), while the National Institute for Occupational Safety and Health (NIOSH) recommends 2 parts per million (ppm). December 2024 EPA rules tightened the 1-hour ambient standard and expanded monitors, adding cost for sulfur-burn facilities. Semiconductor fabs must meet SEMI S2 (Semiconductor Manufacturing Equipment), keeping routine emissions below 1% of occupational limits and installing abatement costing USD 0.5-2 million per tool. These compliance burdens deter small users and consolidate volume with large industrial customers that maintain dedicated EHS (Environment, Health, and Safety) systems.

Phase-Out of Coal Power Curbing Captive Supply

Coal generators historically supplied half of merchant SO₂ via FGD recovery; Europe’s 15-20 GW of retirements in 2025-2026 cut synthetic gypsum streams and tighten feedstock for wallboard and cement. US coal share fell from 20% in 2024 toward an expected 10% by 2031, while China’s fleet plateaued at 1,100 GW with more than 95% FGD penetration, limiting further recovery gains. Tightened supply elevates spot prices and shifts bargaining power to sulfur-burn plants and refineries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Gas Dominates, Solids Accelerate on Logistics Benefits

Gas-phase SO₂ accounted for 56.18% of the Sulfur Dioxide market share in 2025 as sulfuric-acid towers, scrubbers, and fabs require continuous gas feed. The segment benefits from entrenched infrastructure but faces heightened compliance costs under stricter ambient standards. Solid (Bisulfite/Metabisulfite Derivatives), though smaller, are growing at 5.87% CAGR as food-preservers and pharma plants favor low-pressure, transportable inputs that cut insurance premium outlays. The Sulfur Dioxide market size for solids is projected to rise steadily through 2031 on ASEAN demand, while gas retains a majority share in China and India, where large-scale acid plants dominate.

Liquid SO₂ occupies a logistic midpoint, serving batch specialty-chemical makers and municipal plants. Chemtrade’s Polytec acquisition strengthens its distribution of liquid cylinders and bisulfite blends across North America. Regulatory pressures in Vietnam and Thailand steer small users from gas toward solids, yet high-volume industrial sites will continue ordering bulk gas to maintain process continuity.

By Purity Grade: Technical Volume Leads, Ultra-High-Purity Climbs Fastest

Technical-grade SO₂ held 48.94% of 2025 volume, underpinning fertilizer, pulp, and FGD applications. Food-and-pharma grade fulfills strict monographs, sustaining moderate demand in preservation and synthesis niches. Ultra-high-purity grades, though only a sliver of the Sulfur Dioxide market size, will post the quickest growth at 5.98% CAGR to 2031 as Taiwan, the US, and the European Union (EU) ramp 3-nm fabs. TSMC’s USD 52-56 billion 2026 capex and BASF’s Ludwigshafen expansion exemplify upstream investments in more than 99.9% SO₂ supply. Commodity-price swings influence technical grades, whereas ultra-pure volumes earn 3-5 times premiums, supporting supplier margin resilience across cycles.

By Application: Acid Intermediate Anchors Volume, Semiconductor Etching Outpaces Growth

Sulfuric-acid synthesis absorbed 49.86% of SO₂ in 2025, reflecting persistent fertilizer and hydrometallurgical leverage. Indonesia’s nickel-leach parks consumed 800,000 tons of acid during 2025, widening the commodity anchor. Semiconductor cleaning, although less than 2% of overall tonnage, advances at 6.15% CAGR through 2031, leveraging high-margin pricing that shields suppliers from commodity downturns. Food preservation, pulp bleaching, and wastewater dechlorination provide steady mid-tier demand, while battery-electrolyte additives remain prospective until after 2029.

Geography Analysis

Asia-Pacific dominated the Sulfur Dioxide market in 2025 with 50.46% share and is projected to log 6.04% CAGR during the forecast period (2026-2031). China’s sulfuric-acid spot price escalation signaled tight sulfur availability, while India’s 1.2 million tons per annum capacity additions firm fertilizer-sector pull. Taiwan, Japan, and Korea anchor ultra-high-purity uptake for semiconductor nodes, and ASEAN regulations spur demand for point-of-use abatement systems, indirectly boosting bisulfite sales.

North America ranked second on the back of Gulf Coast sulfuric-acid clusters and new fab projects in Arizona and Texas. Linde’s USD 400 million Louisiana ASU (Air Separation Unit) will co-produce liquid SO₂, and Chemtrade’s Polytec buyout broadens turnkey water-treatment offerings. EPA’s tighter 1-hour ambient standard raises compliance expenses but also accelerates technology refresh toward closed-loop systems that favor large suppliers.

Europe trails on volume because coal retirements erase captive FGD streams; however, BASF’s Ludwigshafen ultra-pure expansion highlights a pivot toward precision chemistry targeting the region’s nascent advanced-node fabs. Nordic pulp operations maintain niche bisulfite use, while synthetic-gypsum scarcity is hiking natural-gypsum imports. South America’s demand is led by Brazilian eucalyptus mills adopting closed-loop bisulfite regeneration, and Middle East & Africa volumes hinge on refinery sulfur recovery and South African mining.

Competitive Landscape

The Sulfur Dioxide market is moderately concentrated. Barriers to entry remain high because plants require air-quality permits, specialty metallurgy, and handling infrastructure. Nonetheless, specialty-chemical firms like Zhejiang Jianye gain share in pharma-grade packets by promising tighter lead times and technical support. Over 2026-2031, suppliers capable of toggling between commodity tonnage and semiconductor-grade slates are poised to outperform purely commodity players.

Sulfur Dioxide Industry Leaders

Linde plc

AIR LIQUIDE

Messer Group GmbH

Air Products and Chemicals Inc.

Taiyo Nippon Sanso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DTE Energy Company, which operates a refinery on Zug Island in Detroit, was ordered by the District Court for the Eastern District of Michigan, United States, to pay a penalty of USD 100 million due to violations related to sulphur dioxide pollution. These ruling underscores the increasing emphasis on stringent adherence to sulphur dioxide regulations.

- July 2025: India's Environment Ministry granted exemptions to most of the country's coal-fired plants, relieving them from the mandatory installation of FGD systems, aimed at reducing sulphur dioxide emissions.

Global Sulfur Dioxide Market Report Scope

Sulfur dioxide is a colorless, pungent, and toxic gas primarily produced by burning fossil fuels (coal/oil), industrial processes, and volcanic activity. It is a major air pollutant contributing to acid rain and severe respiratory issues, such as asthma and bronchitis. It is also used in industry and as a preservative in wine.

The Sulfur Dioxide market is segmented by form, purity grade, application, and geography. By form, the market is segmented into gas, liquid, and solid (bisulfite/metabisulfite derivatives). By purity grade, the market is segmented into less than 99% (technical grade), 99.0% - 99.9% (food and pharma grade), and greater than 99.9% (ultra-high purity). By application, the market is segmented into chemical intermediate (sulfuric acid), food and beverage preservation, wine and brewing stabilization, pulp and paper bleaching, metal and mining (ore leaching/processing), waste- and wastewater treatment, semiconductor cleaning and etching, pharmaceutical synthesis, and other applications (fumigation and disinfection and synthetic gypsum production). The report also covers the market size and forecasts for sulfur dioxide in 17 countries across major regions in volume (tons).

| Gas |

| Liquid |

| Solid (Bisulfite/Metabisulfite Derivatives) |

| Less than 99% (Technical Grade) |

| 99.0% - 99.9% (Food and Pharma Grade) |

| Greater than 99.9% (Ultra-high purity) |

| Chemical Intermediate (Sulfuric Acid) |

| Food and Beverage Preservation |

| Wine and Brewing Stabilization |

| Pulp and Paper Bleaching |

| Metal and Mining (Ore Leaching/Processing) |

| Waste- and Wastewater Treatment |

| Semiconductor Cleaning and Etching |

| Pharmaceutical Synthesis |

| Other Applications (Fumigation and Disinfection and Synthetic Gypsum Production) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Gas | |

| Liquid | ||

| Solid (Bisulfite/Metabisulfite Derivatives) | ||

| By Purity Grade | Less than 99% (Technical Grade) | |

| 99.0% - 99.9% (Food and Pharma Grade) | ||

| Greater than 99.9% (Ultra-high purity) | ||

| By Application | Chemical Intermediate (Sulfuric Acid) | |

| Food and Beverage Preservation | ||

| Wine and Brewing Stabilization | ||

| Pulp and Paper Bleaching | ||

| Metal and Mining (Ore Leaching/Processing) | ||

| Waste- and Wastewater Treatment | ||

| Semiconductor Cleaning and Etching | ||

| Pharmaceutical Synthesis | ||

| Other Applications (Fumigation and Disinfection and Synthetic Gypsum Production) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What was the global Sulfur Dioxide market size in 2025, 2026 and its growth outlook to 2031?

The Sulfur Dioxide Market size was valued at 13.71 million tons in 2025 and is estimated to grow from 14.47 million tons in 2026 to reach 18.98 million tons by 2031, at a CAGR of 5.57% during the forecast period (2026-2031).

Which form segment is expanding fastest?

Solid bisulfite and metabisulfite derivatives lead growth at a 5.87% CAGR owing to safer logistics and food-grade demand.

How much Sulfur dioxide market share did Asia-Pacific hold in 2025?

Asia-Pacific captured 50.46% of global volume in 2025 and is set for the highest regional CAGR at 6.04%.

Why is ultra-high-purity SO₂ demand rising in semiconductors?

Advanced-node fabs require more than 99.9% purity sulfuric acid for wafer cleaning, spurring a 5.98% CAGR in ultra-high-purity SO₂ through 2031.

Page last updated on: