Ferrous Sulfate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.78 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

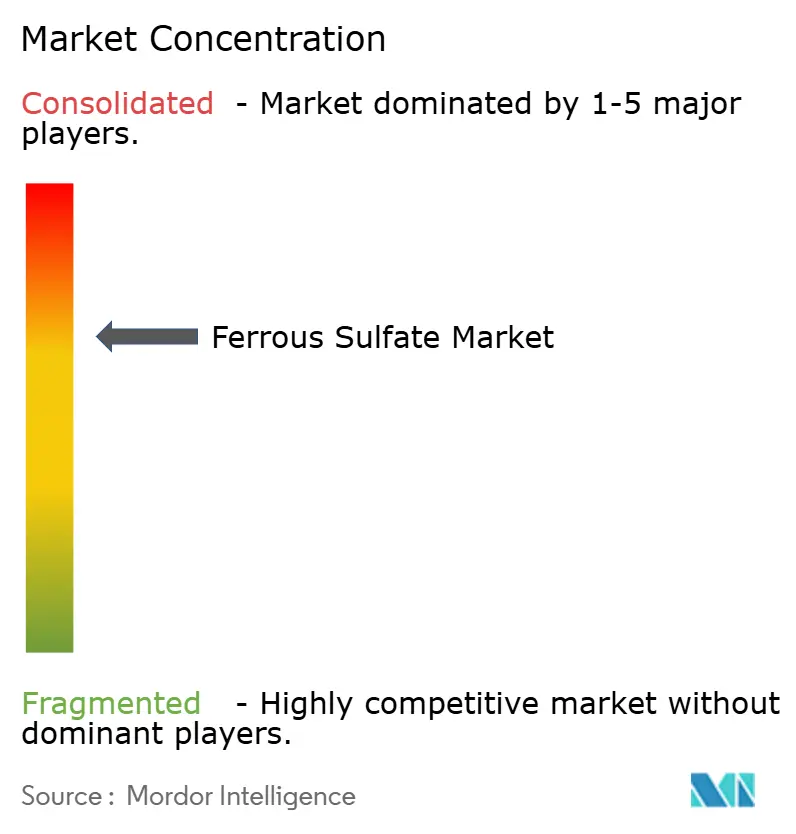

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ferrous Sulfate Market Analysis by Mordor Intelligence

The Ferrous Sulfate Market size is projected to expand from USD 2.17 billion in 2025 and USD 2.26 billion in 2026 to USD 2.78 billion by 2031, registering a CAGR of 4.21% between 2026 and 2031. The shift of titanium-dioxide producers away from captive capacities has tightened by-product supply, lifting average contract prices paid by water utilities and fertilizer blenders. Surging sulfuric-acid feedstock costs, which rose 30% year-on-year to EUR 480-500 per ton (USD 561.66-585.06 per ton) in Milan by February 2026, are compressing margins for synthetic producers even as demand from municipal wastewater plants expands. Asia-Pacific remains the principal consumption hub because of China’s phosphorus-removal mandates and India’s iron-fortified rice scheme, while Europe faces a supply shortfall after Venator Materials suspended TiO₂ output at its United Kingdom and Malaysia sites in September 2025. Consolidation is gathering pace: Kemira’s April 2025 purchase of Thatcher Group’s US iron-sulfate business and the announced 2026 takeover of SIDRA Wasserchemie point to an integrated coagulant-services model. Patent filings for liposomal ferric pyrophosphate with 2.7 times bioavailability may temper long-term growth in oral ferrous-sulfate supplements if cost parity emerges.

Key Report Takeaways

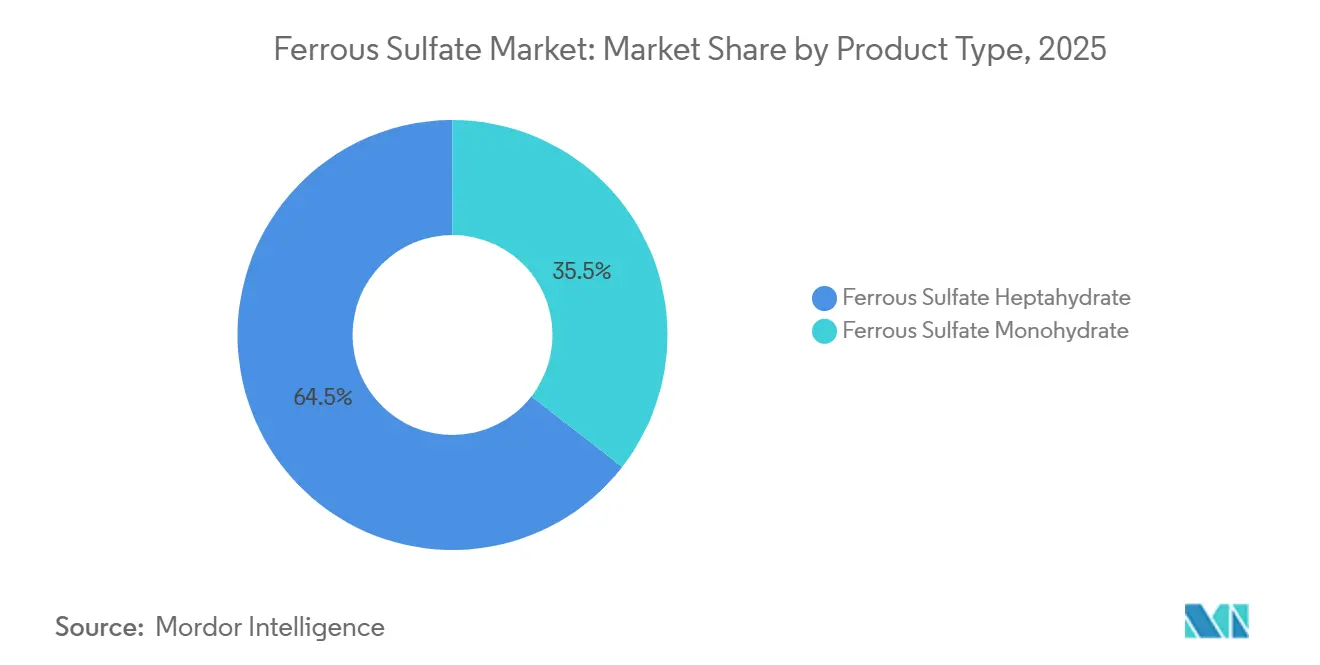

- By product type, ferrous sulfate heptahydrate held 64.47% of the Ferrous Sulfate market share in 2025, while ferrous sulfate monohydrate is set to post a 4.68% CAGR during the forecast period (2026-2031).

- By application, water treatment captured 38.61% of the Ferrous Sulfate market size in 2025; pharmaceuticals and nutraceuticals are projected to compound at 5.04% CAGR during the forecast period (2026-2031).

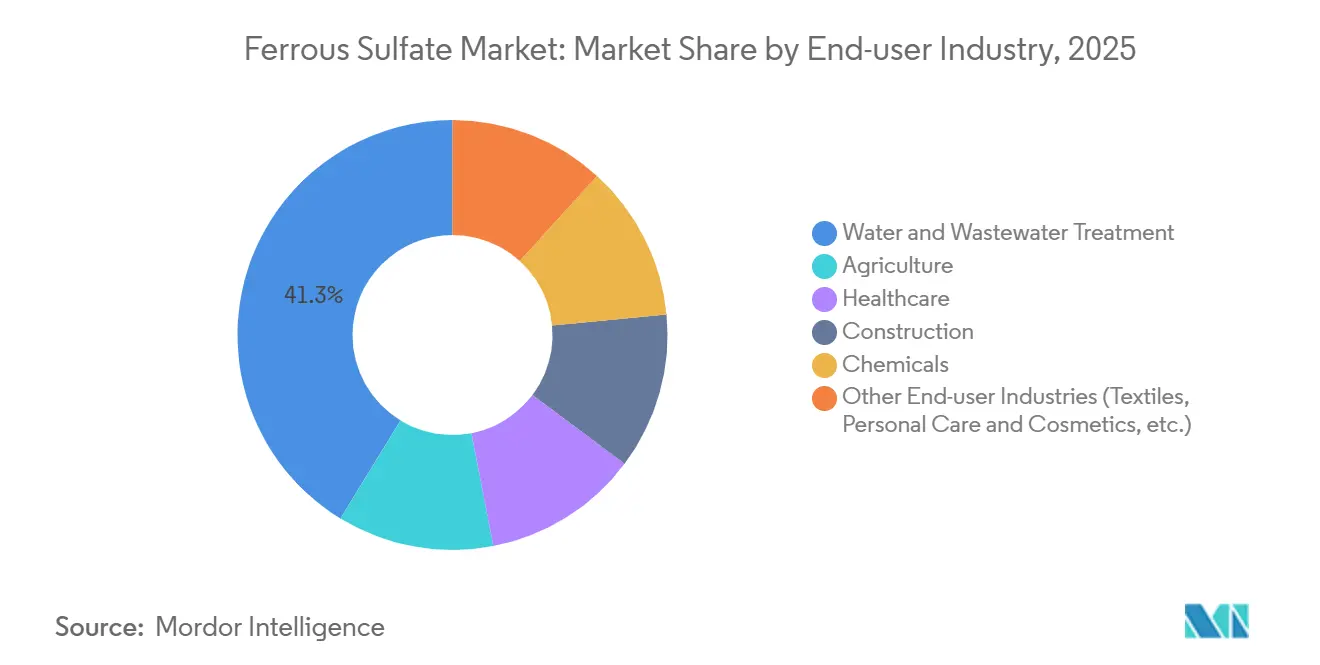

- By end-user industry, water and wastewater treatment commanded 41.28% revenue in 2025; healthcare's demand is expected to increase with a 4.97% CAGR during the forecast period (2026-2031).

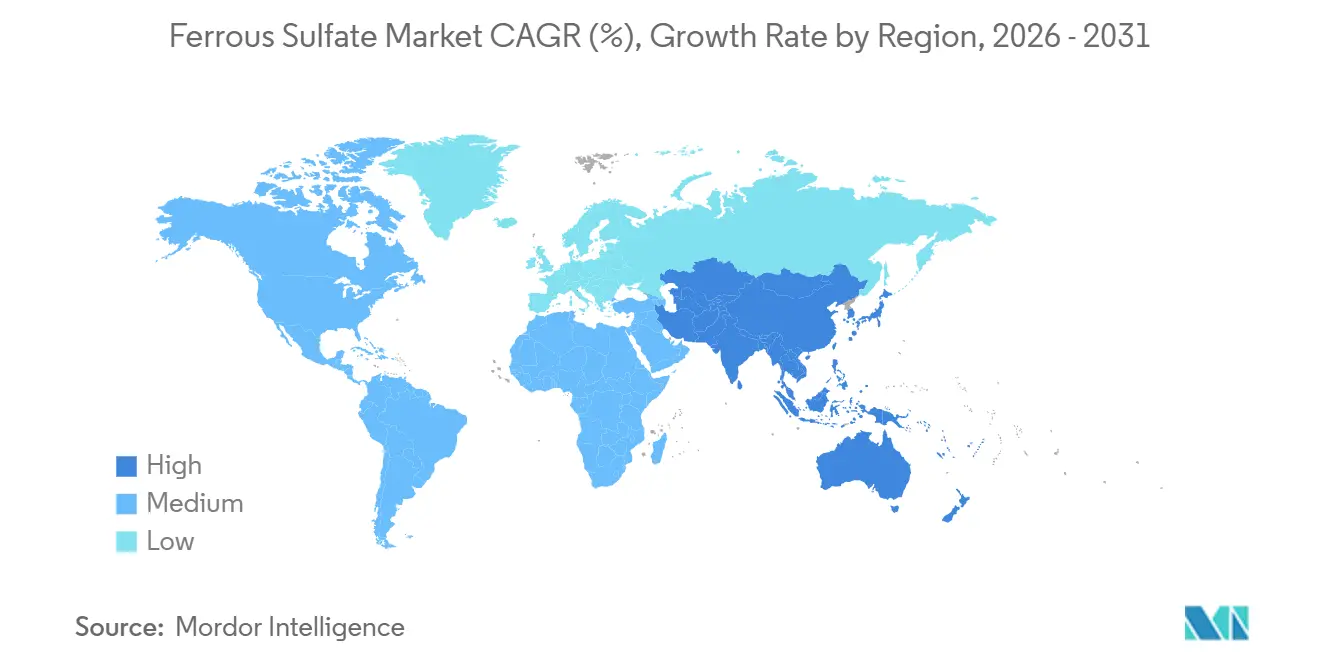

- By geography, Asia-Pacific accounted for 49.92% of the Ferrous Sulfate market size in 2025; the region is forecast to advance at a 4.92% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ferrous Sulfate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing use in wastewater treatment and water purification | +1.2% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Growth in agricultural applications as a soil amendment and fertilizer | +0.8% | Asia-Pacific, South America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Expansion of the cement and construction industry | +0.5% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| Government-led food-fortification mandates in emerging economies | +0.9% | South Asia, Sub-Saharan Africa, Southeast Asia | Short term (≤ 2 years) |

| Adoption as low-carbon coagulant alternative to aluminum salts | +0.7% | Europe, North America, North-East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Use in Wastewater Treatment and Water Purification

Tighter phosphorus-discharge limits under the European Union’s revised Urban Wastewater Treatment Directive, now requiring 0.5 mg/L in sensitive catchments by 2033, are prompting utilities to favor ferrous sulfate because it achieves lower residual phosphorus with less sludge than aluminum coagulants[1]European Commission, “Proposal for a Directive concerning Urban Wastewater Treatment,” europa.eu. Vietnam’s QCVN 40:2025/BTNMT standard, effective September 2025, cut allowable phosphorus in industrial effluents by 40%, driving textile plants to retrofit dosing systems. South Korea’s 4,397 public plants are adopting ferrous-sulfate pretreatment to raise biogas yields and meet a 50% energy-self-sufficiency goal by 2030. Saudi Arabia’s National Water Strategy targets a 43.6% increase in wastewater reuse by 2035, favoring ferrous-sulfate coagulation for cost-effective tertiary upgrades.

Growth in Agricultural Applications as a Soil Amendment and Fertilizer

India’s Union Budget 2026-27 earmarked INR 1.71 lakh crore (USD 20.5 billion) for fertilizer subsidies that include ferrous-sulfate micronutrient blends. Salt-stress field trials in coastal Bangladesh show foliar 0.5% ferrous-sulfate solutions lifting lentil yields 8-12%. Brazil’s Cerrado growers apply the salt when liming raises soil pH above 6.0, while high-value soybeans often switch to chelated iron despite higher cost. Sub-Saharan programs in Kenya and Nigeria are piloting compound NPK grades with added ferrous sulfate that could unlock as much as 80,000 tonnes yearly demand by 2030.

Expansion of the Cement and Construction Industry

China, producing 55% of global cement, is moving toward blended cements that use ferrous sulfate during grinding to curb agglomeration and save 3-5% energy. India’s metro and highway build-out is raising cement consumption by about 6-7% yearly, increasing ferrous-sulfate demand as a set retarder. GCC infrastructure projects worth over USD 2 trillion through 2030 rely on sulfate-resistant concrete, where ferrous-sulfate admixtures improve durability in marine exposure.

Government-Led Food-Fortification Mandates in Emerging Economies

India’s fortified-rice program mandates 5.20 million tonnes of kernels each year through 2028, consuming 8,000-10,000 tonnes of ferrous sulfate. Indonesia’s compulsory wheat-flour standard, introduced in 2024, demands 30-60 mg iron per kilogram, equivalent to roughly 15,000-20,000 tonnes of annual salt use. Nigeria’s initiative aims at 20 million households by 2027 and specifies ferrous sulfate for maize and vegetable oil fortification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and safety concerns in handling and transportation | -0.4% | Global, stricter in Europe and North America | Short term (≤ 2 years) |

| Regulatory limitations in food and feed additives | -0.3% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Price volatility linked to sulfuric-acid feedstock supply | -0.6% | Europe and Asia-Pacific hot spots | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health and Safety Concerns in Handling and Transportation

OSHA’s 1 mg/m³ permissible-exposure limit for soluble iron salts obliges industrial users to install dust-collection and provide respiratory protection[2]OSHA, “Chemical Exposure Limits,” osha.gov. US DOT classifies liquid ferrous-sulfate solution as UN3264, Hazard Class 8, adding up to USD 0.10 per kilogram to freight bills for long hauls. REACH requires downstream users to keep updated exposure scenarios; fines can reach EUR 500,000 per breach. Updated Safety Data Sheets from suppliers such as Thermo Fisher flag Category 1 skin-corrosion risk, prompting many plants to automate dosing to cut manual contact.

Regulatory Limitations in Food and Feed Additives

The FDA caps iron in infant formula at 12 mg/L, while EFSA permits only 750 mg/kg total iron in poultry and swine feed, curbing volume growth in premium nutrition markets. Organic-label bans in India’s rice fortification rules steer processors toward ferric pyrophosphate, a costlier alternative. Japan restricts over-the-counter supplements to 10 mg daily iron, compelling firms to register higher-dose products as prescription drugs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heptahydrate Dominance Meets Monohydrate Momentum

Ferrous-sulfate heptahydrate held 64.47% of the Ferrous Sulfate market share in 2025, owing to its easy solubility for municipal dosing and lower dust generation. Ferrous sulfate monohydrate is on track for a 4.68% CAGR through 2031 as pharmaceutical producers adopt it for controlled-release tablets cited in WO2020014738A1. Heptahydrate sells near USD 150-200 per tonne FOB in Asia, whereas monohydrate commands USD 250-300 because of its 30% iron content and tighter moisture limits. Synthetic pigment makers prefer heptahydrate for iron-oxide conversion, while monohydrate gains utility in HPMC-matrix tablets that release 60-85% iron over four hours. Anhydrous grades remain a niche electrolyte material with a global annual output of below 20,000 tonnes.

Heptahydrate’s shipping costs are rising, given that seven water molecules inflate freight weight by about 45%, encouraging some Asian exporters to build dehydration units, although a 10,000-ton plant needs roughly USD 8 million in capital. Pharmaceutical-grade monohydrate suppliers meet European and US Pharmacopoeia specifications and maintain ISO 9001 systems to ensure moisture below 1%. The patent granted to West Bengal Chemical Industries in August 2025 for liposomal ferric pyrophosphate may constrain monohydrate’s nutraceutical upside if the new format attains cost parity.

By Application: Water Treatment Anchors, Pharmaceuticals Accelerate

Water treatment dominated uses at 38.61% in 2025 as utilities sought low-sludge phosphorus removal, but pharmaceuticals and nutraceuticals are rising fastest at a 5.04% CAGR through 2031 because of national anemia programs. India’s fortified-rice mandate alone draws 8,000-10,000 tonnes of salt each year. Fertilizer and soil conditioner applications face headwinds in South America, where soil pH and organic matter levels limit iron deficiency incidence; Argentina's Pampas region, for example, exhibits negligible demand for routine ferrous sulfate applications due to pH ranges of 6.5-7.5 and organic matter above 3%. Animal feed additives are constrained by EFSA's 750 mg/kg total iron cap for compound poultry and swine feed, though ruminant feed formulations can incorporate higher levels (up to 1,200 mg/kg) due to lower oxidative-stress risk in multi-chambered digestive systems.

Patent momentum favours healthcare: Bio Therapic Italia’s EP4349345A1 proposes liposomal tablets with vitamin C for renal-disease patients, and WBCIL’s Indian Patent 569578 claims 89% encapsulation efficiency. Such advances permit lower iron doses with fewer side effects, supporting higher-margin growth even under strict FDA and EFSA caps. Other uses, textile mordants, herbicide formulations, and chemical reduction, contribute a stable 8-10% tied to industrial production.

By End-user Industry: Water Utilities Lead, Healthcare Surges

Water and wastewater utilities retained 41.28% of the Ferrous Sulfate market size in 2025 and continue to expand with new phosphorus standards in the EU and urban plants across Asia. Healthcare, covering active-pharmaceutical-ingredient makers and supplement formulators, is forecast to grow at 4.97% CAGR through 2031 on fortified staples and patent-protected delivery systems. Agriculture faces regional divergence, though nutrient uptake is region-dependent; India subsidises micronutrients, yet Brazilian soybean farmers prefer chelates despite their 2-3 times cost. Construction tracks cement output, with India’s metro-rail projects driving usage.

Healthcare’s momentum rests on fortified food policy, controlled-release research, and emerging encapsulation technologies that widen the addressable consumer group. Regulatory ceilings remain the main brake as the FDA and EFSA restrict maximum iron in infant formula and animal feed. Utilities face fewer hurdles beyond standard hazardous-materials rules, though ISO 14001 certification gains popularity to cut Scope 3 footprints.

Geography Analysis

Asia-Pacific contributed 49.92% of 2025 revenue and is projected to post the fastest 4.92% CAGR to 2031. China’s 14th Five-Year Plan tightens urban phosphorus removal and drives coagulant demand; its cement sector, producing 55% of global volume, integrates ferrous sulfate to enhance blended-cement grinding efficiency. India’s INR 1.71 lakh-crore (USD 18.2 billion) fertilizer subsidy and 5.20 million-tonne fortified-rice program anchor agricultural and nutraceutical demand. Vietnam’s QCVN 40:2025/BTNMT took effect in September 2025, lowering phosphorus discharge limits by 40% and spurring chemical retrofits. Japan and South Korea advance phosphorus-recovery projects that target vivianite sales into farm cooperatives, aligning with circular-economy policies.

In North America, Kemira’s purchase of Thatcher Group assets in April 2025 strengthens supply on the United States East Coast. The United States utilities preparing for new PFAS limits by 2031 are upgrading pretreatment trains and often adding ferrous sulfate ahead of granular activated carbon to curb fouling. Canadian demand remains stable in corn-soybean belts, while Mexico’s automotive corridors apply the chemical for chromium reduction.

Europe held a decent market share in 2025 but faces supply tightness after Venator suspended TiO₂ output in September 2025, removing up to 200,000 ton of by-product ferrous sulfate.The revised EU directive will mandate sub-0.5 mg/L phosphorus by 2033, expanding retrofit opportunities. Kemira announced a 2026 ferric-chloride expansion in Tarragona to service biogas clients, signalling a partial shift toward ferric chemistry in premium niches. In the Middle East and Africa, Saudi Arabia’s plan to raise wastewater reuse by 43.6% through 2035 using low-capex coagulation steps. South America had the least market share in 2025 and sees patchy growth; Brazil’s Cerrado still uses the salt, yet Argentina’s neutral-pH soils suppress demand.

Competitive Landscape

The Ferrous Sulfate market is moderately concentrated. Regulatory compliance increases barriers: REACH exposure-limit updates impose documentation costs that favour incumbents with automated handling systems. Non-integrated players in India, Turkey, and Mexico face 5-8 percentage-point margin swings when sulfuric-acid prices spike. The market’s fragmentation still offers opportunities for regional specialists, yet rising safety and sustainability requirements tilt competitive advantage toward vertically-integrated suppliers with secure acid and scrap-iron streams.

Ferrous Sulfate Industry Leaders

Coogee

Crown Technology, Inc.

Kemira Oyj

Rech Chemical Co. Ltd.

Venator Materials PLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Venator Materials PLC entered administration following the suspension of titanium dioxide production at its United Kingdom and Malaysia plants in September 2025, removing an estimated 300,000 tons of annual ferrous sulfate byproduct supply from Europe and Southeast Asia and tightening spot markets for water-treatment coagulants

- May 2025: Russian Vitriol Company commenced production of ferrous sulfate monohydrate, a key ingredient in fertilizers and animal feed additives, at its facility located in the Blagoveschensk priority development area.

Global Ferrous Sulfate Market Report Scope

Ferrous sulfate is an iron supplement used to treat and prevent iron-deficiency anemia by aiding hemoglobin production. It is administered orally (tablets, liquid) and is best absorbed on an empty stomach, though it can be taken with food to reduce common gastrointestinal side effects like nausea, constipation, and stomach cramps.

The Ferrous Sulfate market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into ferrous sulfate heptahydrate and ferrous sulfate monohydrate. By application, the market is segmented into water treatment, fertilizer and soil conditioner, animal feed additives, pharmaceuticals and nutraceuticals, pigment and cement industry, and other applications (mordant, formulating agent, etc.). By end-user industry, the market is segmented into agriculture, water and wastewater treatment, healthcare, construction, chemicals, and other end-user industries (textiles, personal care, and cosmetics, etc.). The report also covers the market size and forecasts for ferrous sulfate in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Ferrous Sulfate Heptahydrate |

| Ferrous Sulfate Monohydrate |

| Water Treatment |

| Fertilizer and Soil Conditioner |

| Animal Feed Additives |

| Pharmaceuticals and Nutraceuticals |

| Pigment and Cement Industry |

| Other Applications (Mordant, Formulating Agent, etc.) |

| Agriculture |

| Water and Wastewater Treatment |

| Healthcare |

| Construction |

| Chemicals |

| Other End-user Industries (Textiles, Personal Care and Cosmetics, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Ferrous Sulfate Heptahydrate | |

| Ferrous Sulfate Monohydrate | ||

| By Application | Water Treatment | |

| Fertilizer and Soil Conditioner | ||

| Animal Feed Additives | ||

| Pharmaceuticals and Nutraceuticals | ||

| Pigment and Cement Industry | ||

| Other Applications (Mordant, Formulating Agent, etc.) | ||

| By End-user Industry | Agriculture | |

| Water and Wastewater Treatment | ||

| Healthcare | ||

| Construction | ||

| Chemicals | ||

| Other End-user Industries (Textiles, Personal Care and Cosmetics, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the Ferrous Sulfate market be by 2031?

The ferrous sulfate market size is forecast to reach USD 2.78 billion by 2031, advancing at a 4.21% CAGR between 2026 and 2031.

Which application segment is expanding the fastest?

Pharmaceuticals and nutraceuticals are projected to grow at a 5.04% CAGR through 2031 as national fortification programs and patent-protected delivery systems scale up.

Why is Asia-Pacific the leading consumer region?

Strong wastewater regulations in China and Vietnam, India’s iron-fortified rice initiative and cement-sector demand keep Asia-Pacific near half of global consumption with the highest regional CAGR of 4.92%.

What is driving supply tightness in Europe?

Venator’s suspension of titanium-dioxide output removed up to 200,000 tons of by-product ferrous sulfate, while stricter phosphorus rules raise demand, widening the supply gap.

Page last updated on: