Cobalt Sulphate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

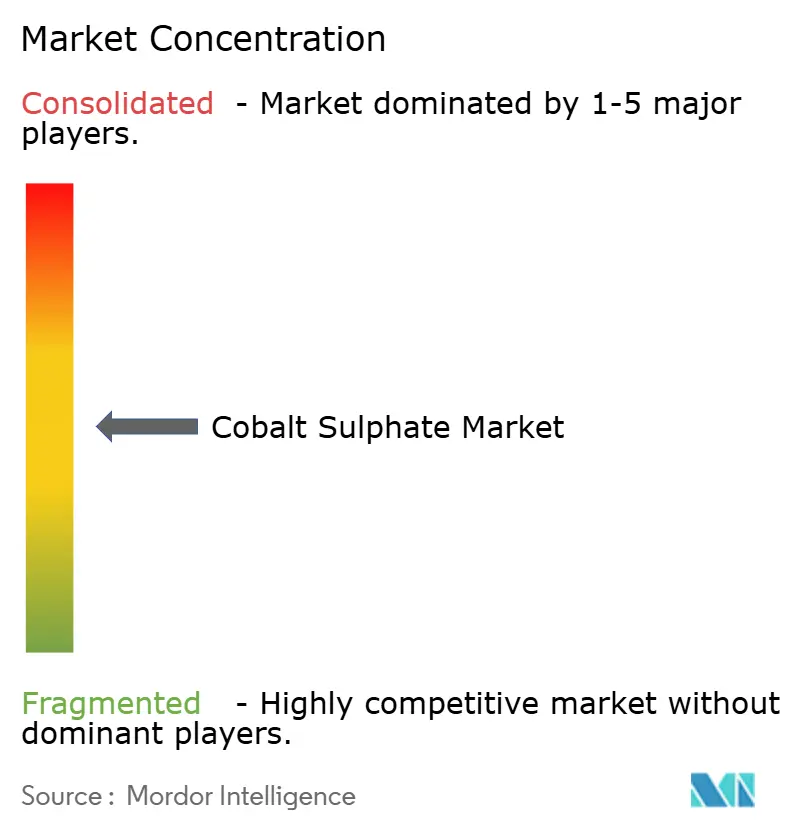

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cobalt Sulphate Market Analysis by Mordor Intelligence

The Cobalt Sulphate Market size is expected to increase from USD 1.72 billion in 2025 to USD 1.81 billion in 2026 and reach USD 2.35 billion by 2031, growing at a CAGR of 5.33% over 2026-2031. Western supply-chain-localization mandates in the United States and the European Union are steering capital toward domestic refining even as lithium iron phosphate chemistries captured 51% of global battery production in 2024, trimming cobalt intensity per kilowatt-hour. Indonesia’s rise from a negligible mined supply in 2020 to 12% in 2024, with expectations of 22% by 2030, is reshaping the cobalt sulphate market cost curve through nickel HPAL by-product flows. Battery-grade material commanded 76.22% of demand in 2025 because ultra-high-nickel cathodes require tighter purity even while lowering absolute cobalt loading. A 92% price spike following the Democratic Republic of Congo’s four-month export ban in 2025 underscored the cobalt sulphate market vulnerability to single-country concentration. China Molybdenum’s 114,000-ton 2024 output created a 36,000-tonne surplus, depressing prices until Beijing’s strategic reserve purchase of 16,600 tons stabilized the cobalt sulphate market in late 2025.

Key Report Takeaways

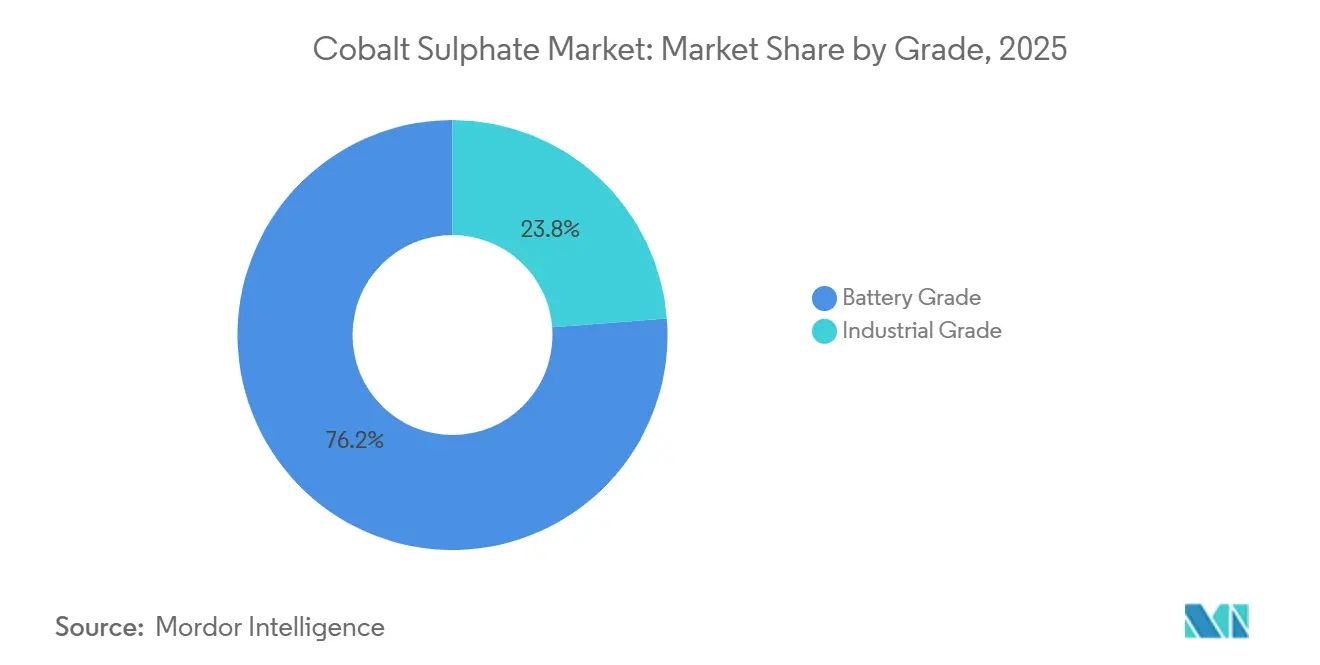

- By grade, Battery Grade material led with 76.22% of the Cobalt Sulphate market share in 2025 and is projected to expand at a 5.57% CAGR through 2031.

- By application, the batteries segment accounted for 71.56% share of the Cobalt Sulphate market size in 2025 and is on track for a 5.44% CAGR to 2031.

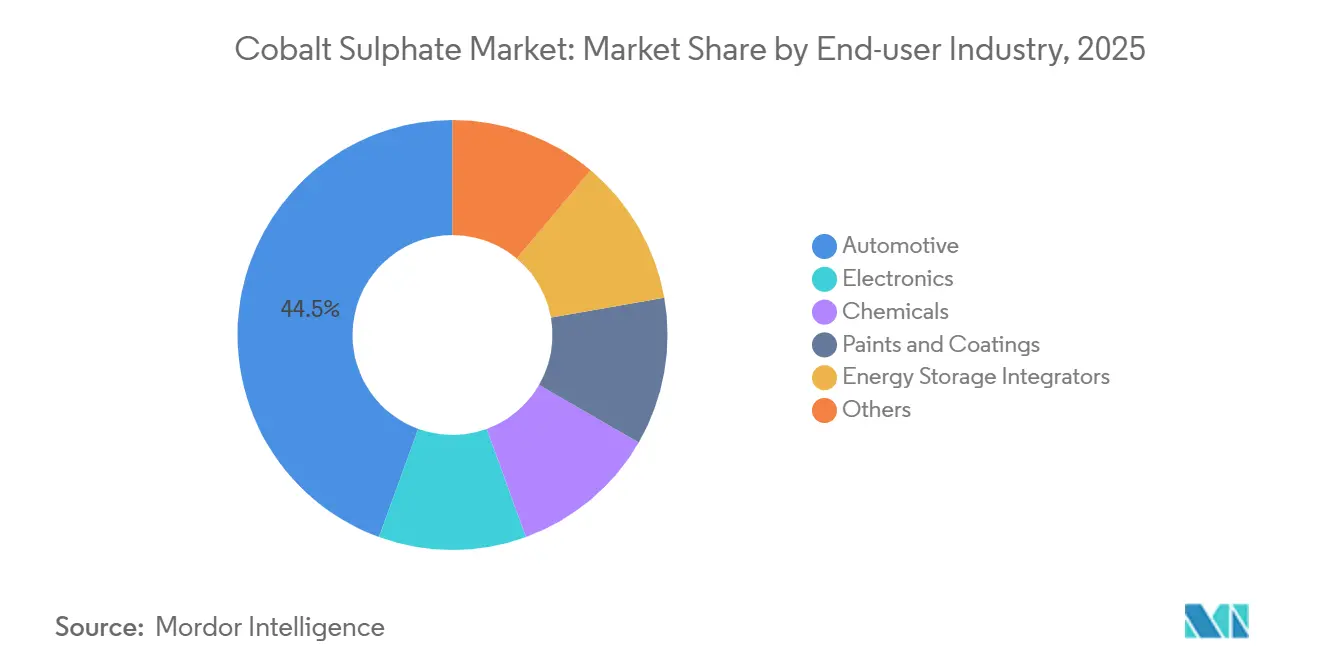

- By end-user industry, automotive captured 44.45% share in 2025, while Energy Storage Integrators are expected to record the fastest 6.11% CAGR during the forecast period (2026-2031).

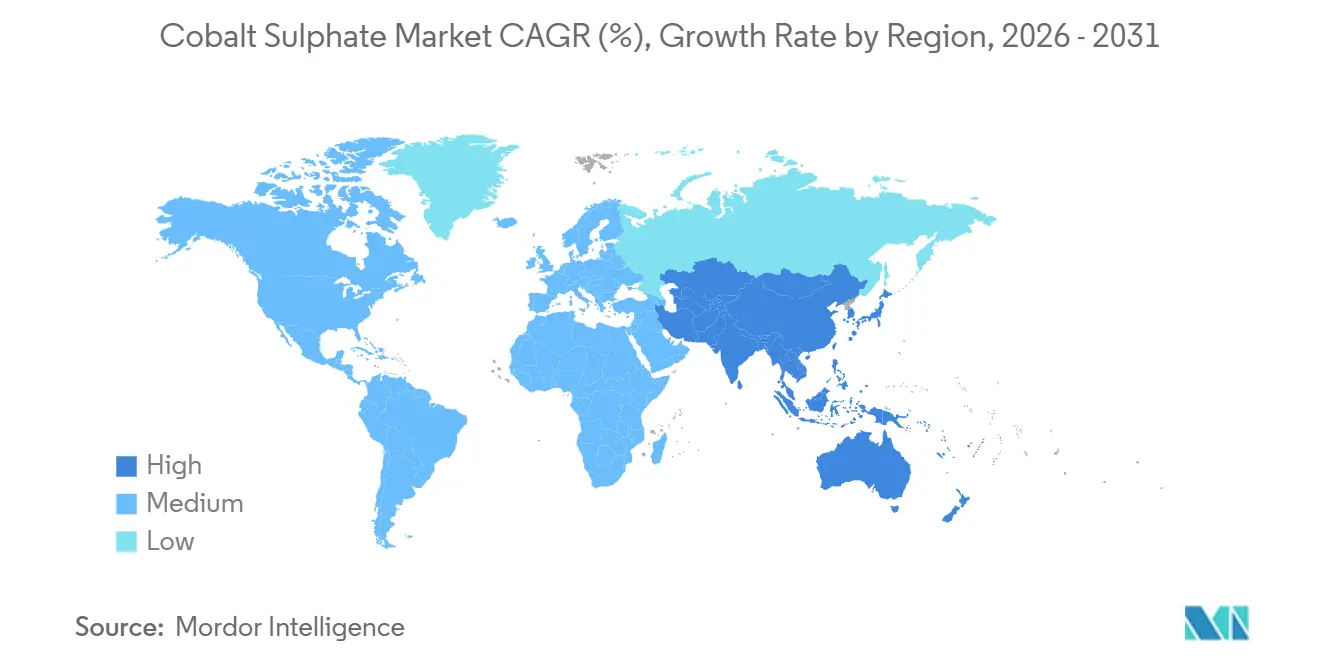

- By geography, Asia-Pacific held 61.34% of the Cobalt Sulphate market share in 2025 and is advancing at a 5.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cobalt Sulphate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-scale LFP + LMFP storage pivot needs Co-rich stabilizer additives | +0.4% | Global, early uptake in China, EU, North America | Medium term (2–4 years) |

| Western supply-chain localization subsidies (IRA, EU CRM Act) | +1.5% | North America & EU, spill-over to Canada, Australia | Short term (≤ 2 years) |

| Nickel by-product expansions raising low-cost CoSO₄ output | +1.0% | Indonesia HPAL core, Philippines, New Caledonia | Medium term (2–4 years) |

| AI-server thermal-management fluids using CoSO₄ inhibitors | +0.2% | Global data-center hubs | Long term (≥ 4 years) |

| Recycled cobalt sulfate from high-Ni battery streams | +0.7% | EU, China, North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Western Supply-Chain Localization Subsidies Drive Refining Capacity Outside China

Roughly USD 2 billion in announced projects since 2023 are flowing into North American and European cobalt sulphate market refineries as the Inflation Reduction Act and the EU Critical Raw Materials Act seek to cut Chinese dependence. Electra Battery Materials secured CAD 100 million (USD 71.57 million) for a 6,500 tons per annum Ontario plant backed by U.S. Department of Defense funding and a long-term LG Energy Solution offtake, illustrating defense-led underwriting when spot prices alone would not justify construction[1]Electra Battery Materials, “Ontario Refinery Budget Approval,” electrabatterymaterials.com. South Korea has earmarked 45.8 trillion won in financing and a 10 trillion-won stockpile to lower single-country reliance below 50% by 2030, complementing a 2026 Canada-Korea memorandum on battery metals.

Nickel-By-Product Expansions in Indonesia Reshape Cost Curves

GEM’s Qingmei Bang and Huayou’s MHP hubs ship cobalt at marginal cost, undercutting primary mines such as Jervois’ Idaho Cobalt Operations, which halted in 2024 and filed Chapter 11 in 2025. Life-cycle analyses show Indonesia HPAL routes carry 70% higher greenhouse-gas footprints than DRC-China hydromet processes, putting low-cost output at odds with EU carbon-footprint declarations. As cobalt becomes a residual from nickel revenue, production responds to nickel, not cobalt, signals, complicating price discovery in the cobalt sulphate market.

Recycled Cobalt-Sulfate Streams Offer Supply Flexibility Amid Regulatory Mandates

The EU Battery Regulation requires 16% recycled cobalt in new cells by 2031, and digital battery passports become mandatory in 2027. Recycled cobalt totaled 22,000 tons in 2024, 8% of supply, and could hit 25% of demand by 2040 when first-wave EVs retire. Huayou and GEM each operate integrated recycling lines exceeding 10,000 tons per annum, while Umicore’s Hoboken plant processes scrap but saw rechargeable-battery-materials revenue fall to EUR 1.99 billion in 2024 from EUR 2.59 billion in 2023. The U.S. FY 2026 National Defense Authorization Act widens foreign-entity-of-concern exemptions for recycled feed, opening regulatory arbitrage for domestic black-mass refiners. OECD diligence guidance now applies to recycled streams, limiting informal operations and reinforcing traceability in the Cobalt Sulphate market.

Grid-Scale Energy Storage Chemistries Evolve Toward Mid-Nickel Formulations

In 2025, Europe installed 20+ GWh of battery storage, with projections exceeding 200 GWh by 2030. LFP dominated 70% of deployments due to its long cycle life and low costs, while mid-nickel chemistries and CATL's Shenxing LMFP battery offered higher energy density and improved performance. In 2023, CATL began mass production of cobalt-free sodium-ion batteries, projected to cost USD 40/kWh by 2027 with 160 Wh/kg energy density. The European Union (EU) Battery Regulation, effective February 2025, mandates carbon-footprint declarations and cobalt audits, favoring suppliers compliant with the Responsible Minerals Initiative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ESG and human-rights scrutiny in DRC artisanal mines | -0.5% | DRC-origin chains, global downstream | Short term (≤ 2 years) |

| Rapid cathode thrifting and LFP share gains | -1.1% | Global, China leads LFP | Short term (≤ 2 years) |

| Recycled-content mandates dampen virgin demand post-2029 | -0.4% | EU first, North America next | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ESG and Human-Rights Scrutiny Constrains DRC Artisanal Mining Supply

Artisanal operations delivered about 5-6% of DRC cobalt in 2024, yet allegations of child labor have pushed battery makers toward zero-tolerance sourcing policies[2]Fair Cobalt Alliance, “Artisanal Mining Assessment 2024,” faircobaltalliance.org. While 82% of refined cobalt was RMAP-conformant in 2024, the residual volume exposes auto OEMs to reputational hazards. Industrial sites like ERG’s Metalkol and CMOC’s Tenke Fungurume have secured Copper Mark and PwC assurance, but enforcement across the 255,000 km² Copperbelt is inconsistent. South Korea’s 2024 strategy to cut single-source exposure mirrors the U.S. Department of Defense’s USD 20 million Electra investment, highlighting geopolitical diversification in the cobalt sulphate market. Contract clauses referencing ISO 26000 and OECD due diligence are becoming standard, excluding smaller miners lacking audit capacity.

Rapid Cathode Thrifting and LFP Market-Share Gains Reduce Cobalt Intensity

LFP captured 51% of global battery output in 2024, lifting its share by 50% year on year and trimming cobalt demand forecasts by about 25% versus pre-2023 outlooks. Cobalt-bearing chemistries fell to 49% of the battery mix, while Korean producers now mass-produce 95%-nickel cathodes with only 2-3% cobalt. Huayou’s 9-series cathodes topped 60% of its ternary shipments in H1 2025, proving that purity premiums, not volume, underwrite battery-grade sales. India’s Production-Linked Incentive scheme expects LFP to constitute 70% of domestic output by 2030, reinforcing thrifting trends in the Cobalt Sulphate market. The International Energy Agency now projects no sustained market deficit until the early 2030s as by-product supply expands alongside chemistry shifts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Battery-Grade Purity Commands Premium Amid Cathode Evolution

Battery-grade material captured 76.22% of 2025 demand, and its Cobalt Sulphate market size for this segment is expected to grow at a 5.57% CAGR during the forecast period (2026-2031). Industrial-grade is advancing at a slower pace as catalysts, pigments, and plating applications grow in line with GDP.

Tighter impurity thresholds, less than or equal to 10 ppm metals and less than or equal to 50 ppm sulfate, allow battery-grade to command a 30-50% premium over industrial grades, a spread likely to widen as ultra-high-nickel cathodes become mainstream. Electra’s Ontario plant will supply 6,500 tons per annum of battery-grade cobalt, or 27% of ex-China output, when commercial production starts in 2027. Industrial producers such as Eastmen Chemicals ship over 300 tons monthly to 25 countries, signaling a stable but less regulated niche. The Cobalt Sulphate market nevertheless remains bifurcated, with premium pricing tied to Responsible Minerals Assurance Process certification.

By Application: Batteries Dominate Yet Face Chemistry-Driven Headwinds

Batteries held 71.56% share in 2025, with Cobalt Sulphate market size in this segment projected to expand at 5.44% CAGR during the forecast period (2026-2031).

Electric-vehicle batteries consumed roughly 95,000 tons of cobalt in 2024, yet LFP’s ascent restrains demand acceleration. Portable electronics absorbed 67,000 tons, buoyed by post-pandemic device shipments. Petrochemical catalysts, especially in desulfurization and polyester, underpin industrial-grade flows, whereas pigments continue to have a steady demand for cobalt blue ceramics. As regulatory recycled-content quotas apply only to battery uses, non-battery segments face no comparable supply mandates, leaving them as a small but steady ballast for the Cobalt Sulphate market.

By End-user Industry: Energy Storage Integrators Outpace Automotive Growth

Automotive retained 44.45% of demand in 2025, yet energy storage integrators will lead growth at 6.11% CAGR owing to mid-nickel chemistries that balance energy density and cycle life. Electronics also represented a substantial share of cobalt use as consumer devices rebounded.

Chemicals, paints, and other industrials are expanding at low-to-mid single-digit rates. South Korea’s 2024 financing package to raise domestic precursor output underscores the pivot toward localized supply chains. Meanwhile, grid projects in Europe surpassed 20 GWh installed capacity in 2025 and could exceed 200 GWh by 2030, anchoring long-run demand in the Cobalt Sulphate market.

Geography Analysis

Asia-Pacific commanded 61.34% Cobalt Sulphate market share in 2025 and should advance at 5.89% CAGR through 2031, buoyed by China’s 78.6% refined output and Indonesia’s HPAL surge. Beijing’s 16,600-ton strategic purchase in 2024 helped stabilize prices after China Molybdenum’s surplus, affirming state intervention capacity in the Cobalt Sulphate market.

In North America, the Inflation Reduction Act and Electra’s 6,500 tons per annum Ontario plant could lift the Cobalt Sulphate market size regionally by 2031. Sherritt’s 2,729-tonne Alberta refinery remains the continent’s only significant producer until 2027, while Jervois’ Idaho mine stays on care-and-maintenance.

Europe’s share hinges on the EU’s 40% processing target and 16% recycled-cobalt mandate. Umicore’s Belgian and Finnish assets processed 18,500 tons in 2024, though margins tightened as auto cathode demand softened. South America and MEA, dominated by the DRC’s 62% mined share, remain price setters; the 2025 DRC export ban that spiked sulfate prices 92% within six weeks exemplifies that leverage.

Competitive Landscape

The Cobalt Sulphate market is moderately fragmented. Losers include stand-alone miners like Jervois that lack by-product revenue, whereas European refiners face shrinking spreads amid softer EV uptake. China’s National Development and Reform Commission signaled willingness to backstop domestic producers by drawing on strategic reserves, a policy tool unavailable to most Western competitors, thereby influencing pricing power within the Cobalt Sulphate market.

Cobalt Sulphate Industry Leaders

Huayou Cobalt Co., Ltd.

Glencore

GEM Co., Ltd.

CMOC

Umicore

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Cobalt Blue Holdings Limited signed a binding agreement with Iwatani Australia Pty Limited to advance the Kwinana Cobalt Refinery (KCR) in Western Australia. KCR will be Australia’s first cobalt refinery, with an initial capacity of 3,000 tons per annum of battery-grade cobalt sulphate or metal.

- May 2025: Cobalt Blue Holdings Limited partnered with Glencore to supply cobalt hydroxide feedstock to the Kwinana Cobalt Refinery. Glencore will meet up to 50% of KCR's feedstock needs for three years, starting with commercial operations. This development is expected to strengthen the cobalt sulfate market as the Kwinana Refinery begins production.

Global Cobalt Sulphate Market Report Scope

Cobalt Sulphate is a red-colored, water-soluble inorganic compound, primarily existing as a heptahydrate. It is widely used in lithium-ion battery manufacturing, electroplating, and as a cobalt source in agriculture (animal feed and fertilizers). Key applications include pigment preparation for porcelain and as an intermediate in cobalt mining.

The Cobalt Sulphate market is segmented by grade, application, end-user industry, and geography. By grade, the market is segmented into battery grade and industrial grade. By application, the market is segmented into batteries, catalysts, drying agents, electroplating, pigments and dyes, and other applications. By end-user industry, the market is segmented into automotive, electronics, chemicals, paints and coatings, energy storage integrators, and others. The report also covers the market size and forecasts for cobalt sulphate in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Battery Grade |

| Industrial Grade |

| Batteries |

| Catalysts |

| Drying Agents |

| Electroplating |

| Pigments and Dyes |

| Other Applications |

| Automotive |

| Electronics |

| Chemicals |

| Paints and Coatings |

| Energy Storage Integrators |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Battery Grade | |

| Industrial Grade | ||

| By Application | Batteries | |

| Catalysts | ||

| Drying Agents | ||

| Electroplating | ||

| Pigments and Dyes | ||

| Other Applications | ||

| By End-user Industry | Automotive | |

| Electronics | ||

| Chemicals | ||

| Paints and Coatings | ||

| Energy Storage Integrators | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Cobalt Sulphate market in 2031?

Cobalt Sulphate market is forecast to reach USD 2.35 billion by 2031 from USD 1.81 billion in 2026 at a CAGR of 5.33%.

Which grade leads demand in the cobalt sulphate market?

Battery-grade cobalt sulfate commanded 76.22% share in 2025 and will remain dominant through 2031.

Which region is the largest producer of refined cobalt sulfate?

Asia-Pacific, led by China’s major share of global refined output in 2024.

What was the impact of the 2025 DRC export ban on cobalt-sulfate prices?

Prices spiked 92% within six weeks after the ban was announced.

Page last updated on: