Sulfur Hexafluoride Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

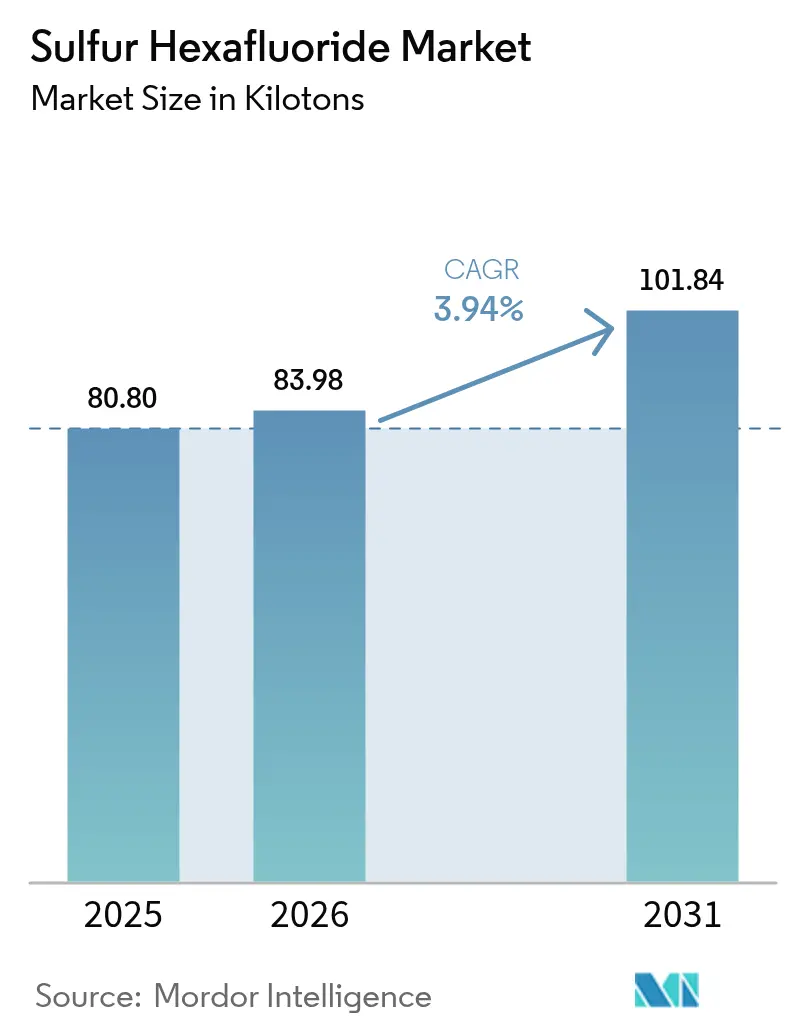

| Market Volume (2026) | 83.98 kilotons |

| Market Volume (2031) | 101.84 kilotons |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

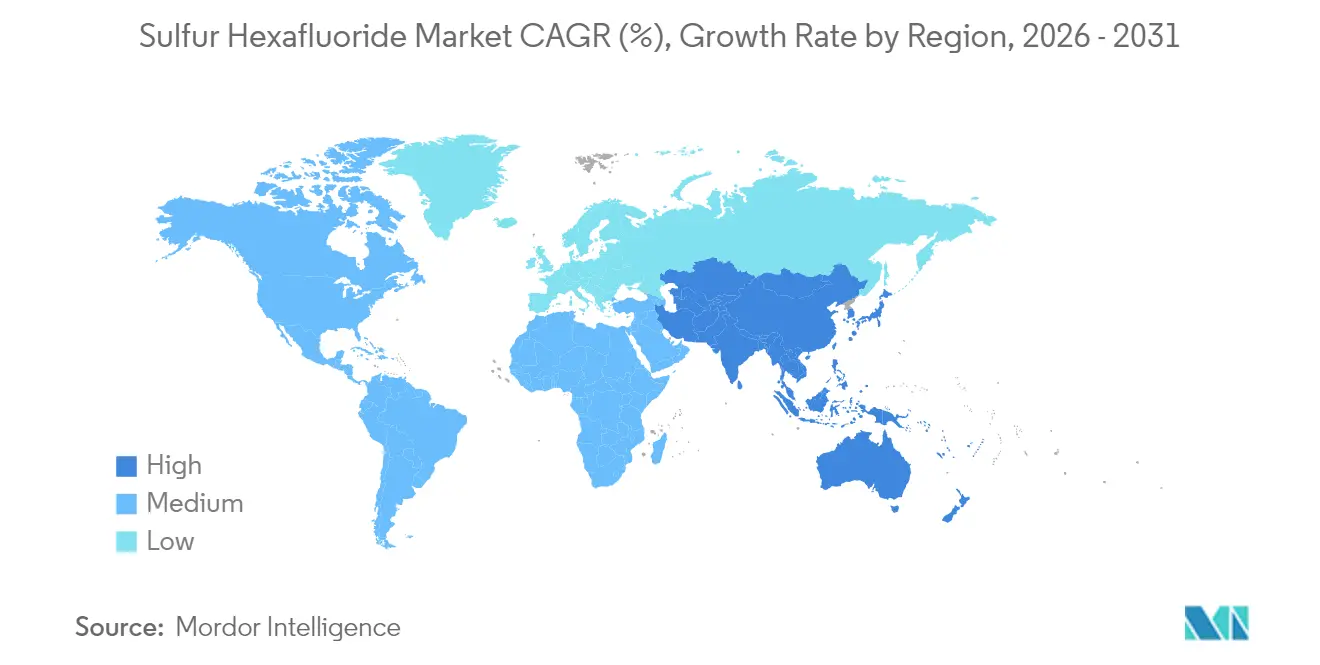

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

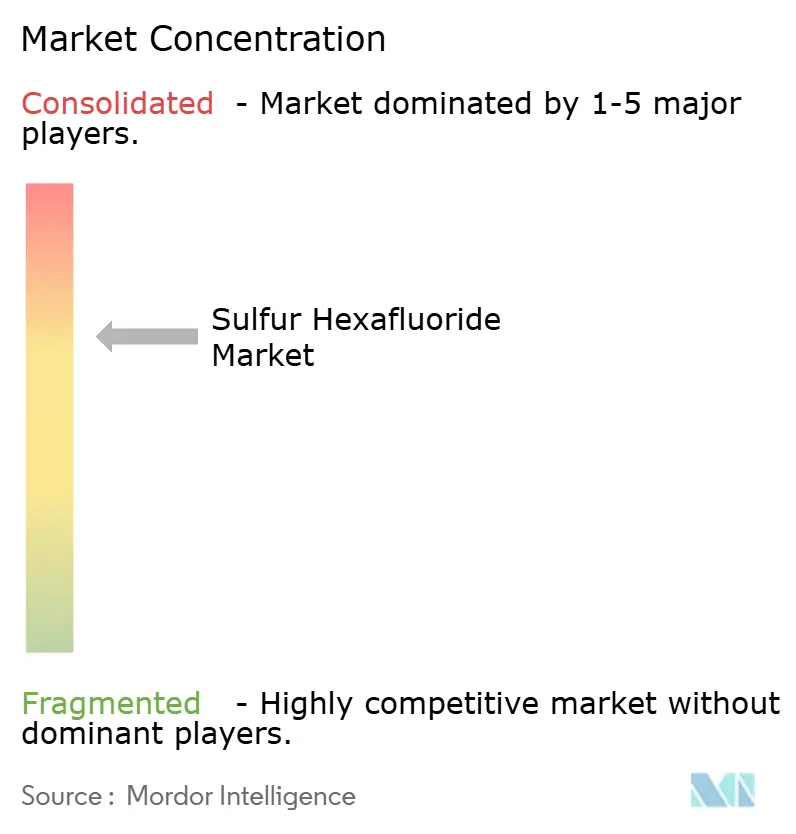

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sulfur Hexafluoride Market Analysis by Mordor Intelligence

Sulfur Hexafluoride market size in 2026 is estimated at 83.98 kilotons, growing from 2025 value of 80.80 kilotons with 2031 projections showing 101.84 kilotons, growing at 3.94% CAGR over 2026-2031. Robust grid-upgrade programs in emerging economies, surging semiconductor fabrication capacity, and offshore wind transmission projects are sustaining demand even as environmental regulations tighten. Electrical utilities continue to specify SF₆ for gas-insulated switchgear because it delivers unrivalled dielectric strength, compact footprints, and rapid energization, advantages that existing alternatives still struggle to match. Semiconductor manufacturers require ultra-high-purity SF₆ to achieve fast, clean plasma etching, and this requirement deepens as feature sizes shrink. Meanwhile, medical and magnesium die-casting uses provide incremental growth, creating diversified end-markets that help buffer regulatory shocks.

Key Report Takeaways

- By product type, Electronic/Technical Grade led with 60.72% of sulfur hexafluoride market share in 2025; ultra-High Purity Grade is projected to expand at a 4.71% CAGR between 2026 and 2031.

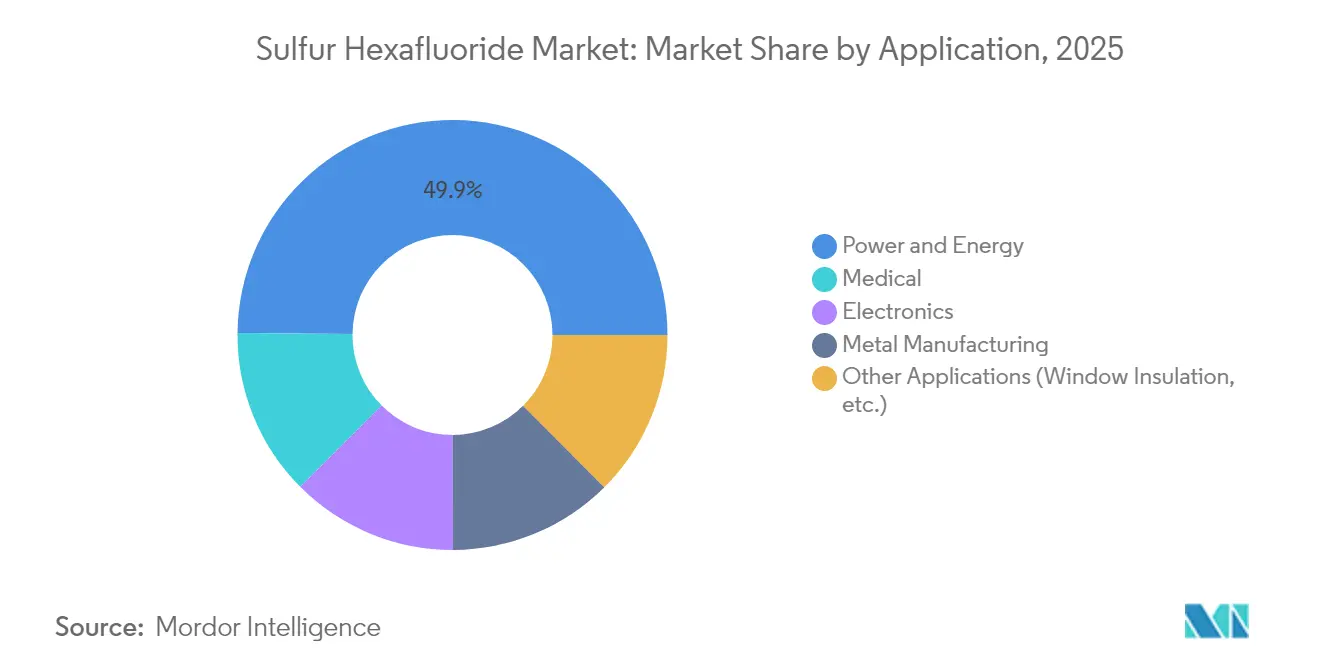

- By application, Power and Energy captured 49.85% of the sulfur hexafluoride market size in 2025 while medical applications are advancing at a 4.58% CAGR through 2031.

- By geography, Asia-Pacific commanded 47.82% revenue share in 2025; the region is forecast to expand at a 4.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sulfur Hexafluoride Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-upgrade demand in emerging economies | +1.2% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Semiconductor and LCD plasma-etching growth | +0.8% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Renewable-integrated HVDC and offshore substations | +0.7% | Global, concentrated in Europe and China | Long term (≥ 4 years) |

| Magnesium die-casting oxidation prevention | +0.4% | North America, Europe | Medium term (2-4 years) |

| Increasing demand in the medical sector | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-upgrade demand in emerging economies

China’s SF₆ emissions climbed from 2.6 Gg in 2011 to 5.1 Gg in 2021 as transmission developers installed compact gas-insulated substations to keep pace with record-setting grid expansions. India has earmarked INR 2,000 crore for network modernization that specifies SF₆ switchgear to secure voltage stability during rapid urbanization[1]Hitachi Energy, “Grid Modernization in Emerging Economies,” hitachienergy.com[. Because typical substation assets remain in service for 25 to 50 years, every installation decision effectively locks in future sulfur hexafluoride market demand. Gas-insulated stations can be energized 45% faster than air-insulated yards, a time saving valued by utilities racing to alleviate congestion. As a result, the sulfur hexafluoride market continues to deepen its presence across Asia-Pacific despite intensifying environmental policy debates.

Semiconductor and LCD plasma-etching growth

Korea’s USD 471 billion semiconductor cluster, slated to add 16 fabs by 2047, exemplifies capital flows that elevate consumption of ultra-high-purity SF₆. In deep-trench silicon etching, SF₆ generates fluorine radicals that remove material up to 100 times faster than rival gases, ensuring throughput targets for 3 nm and below nodes. Although abatement systems curb direct emissions, a portion of feedstock still reaches the atmosphere, prompting regulatory scrutiny as fabrication capacity scales. Even so, process engineers continue to specify SF₆ until drop-in alternatives can replicate its etching precision, keeping the sulfur hexafluoride market firmly embedded in advanced manufacturing value chains.

Renewable-integrated HVDC and offshore substations

Long-distance HVDC links and offshore substations require equipment that functions in space-constrained or harsh environments, conditions where SF₆-filled switchgear remains the most reliable option. Coastal wind farms frequently select gas-insulated lines to minimize platform size, despite the paradox of using a potent greenhouse gas to connect zero-carbon generators. Pilot orders for 550 kV SF₆-free breakers signal progress, yet utilities still forecast multiyear qualification phases before full fleet conversions. During this transition, renewable growth indirectly sustains sulfur hexafluoride market volumes.

Magnesium die-casting oxidation prevention

Molten magnesium readily oxidizes, producing scrap and safety risks. Injecting trace SF₆ creates MgO-MgF₂ boundary layers that shield the metal even at concentrations as low as 0.2% by volume, outperforming hydrofluorocarbon blends in high-throughput die-casting cells. Despite R&D into calcium-based modifiers, automakers scaling lightweight components prefer proven SF₆ cover-gas protocols, extending the gas’s industrial relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global-warming regulations | -1.8% | Global, led by EU and California | Short term (≤ 2 years) |

| Price volatility and export quotas | -0.9% | Global supply chains | Medium term (2-4 years) |

| Potential semiconductor-process bans | -0.6% | Asia-Pacific, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent global-warming regulations

The European Union has banned SF₆ in medium-voltage switchgear from 2026 and in high-voltage gear from 2032, forcing utilities to accelerate retrofit plans. California mandates complete phase-out by 2033 and restricts annual leak rates to 1%, compelling asset owners to fund costly monitoring systems[2]California Air Resources Board, “SF₆ Regulation for Electric Utilities,” carb.ca.gov. Similar trajectories in New York and Massachusetts compress investment horizons for SF₆-dependent assets, dampening procurement volumes in developed regions. These overlapping policies subtract 1.8 percentage points from the sulfur hexafluoride market growth outlook.

Price volatility and export quotas

SF₆ prices currently fluctuate between USD 50 and USD 150 per kg depending on purity and contract terms, reflecting concentrated production and rising compliance costsUtilities in regulated markets place advance orders to hedge against supply disruptions, tightening availability for smaller buyers. While no formal quotas exist today, policymakers are studying export controls as they refine carbon-reduction pathways, introducing an additional layer of uncertainty that can defer new equipment purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Technical Grade Leads Power Networks

The electronic/technical-grade segment accounted for 60.72% of sulfur hexafluoride market share in 2025 as utilities prioritize proven insulation performance for switchgear, breakers, and gas-insulated lines. Technical-grade SF₆ follows commodity price dynamics and benefits from established global distribution channels that permit bulk tanker deliveries to substation sites. Because retrofit projects continue through the forecast period, the segment maintains a sizable base-load volume that anchors the overall sulfur hexafluoride market.

Ultra-high-purity SF₆, while representing a smaller absolute tonnage, is forecast to expand at 4.71% CAGR, the fastest among product types, propelled by advanced semiconductor and LCD fabrication. Maintaining contaminant thresholds below parts-per-billion requires multiple purification stages, specialised cylinders, and dedicated supply chains. Suppliers that master these production protocols secure higher margins, offsetting lower volumes and providing a strategic hedge as environmental policy squeezes traditional utility demand. Collectively, the two grade tiers ensure that the sulfur hexafluoride market retains a balanced portfolio across commodity and specialty niches.

By Application: Power Infrastructure Dominates Yet Medical Use Accelerates

Power and Energy applications delivered 49.85% of the sulfur hexafluoride market size in 2025, a reflection of the gas’s unmatched dielectric and arc-quenching capabilities at voltage classes above 72.5 kV. Large infrastructure programs in Asia-Pacific, coupled with grid-reinforcement schemes in North America, sustain procurement largely through OEM service agreements that include periodic top-ups and recycling services. Because typical switchgear lifespans exceed 30 years, replacement cycles alone underpin a stable baseline for SF₆ consumption.

Medical applications register the fastest expansion at 4.58% CAGR, albeit from a small base, as retinal procedures rise in tandem with aging demographics. Ophthalmic-grade SF₆ commands premium pricing thanks to stringent sterility and packaging requirements. The contrast-agent sub-segment shows promise for cardiology and liver imaging, further widening clinical uptake. Despite its scale, the power sector’s entrenchment means regulatory changes there create the greatest swing factor for the sulfur hexafluoride market, while health-care growth offers a resilient auxiliary outlet.

Geography Analysis

Asia-Pacific dominated the sulfur hexafluoride market with 47.82% share in 2025 and is projected to log a 4.61% CAGR through 2031. China’s grid operators are installing compact 550 kV gas-insulated substations across ultrahigh-voltage corridors to accommodate record renewable capacity, a strategy that cements multi-decade SF₆ demand. India’s program to reinforce inter-state transmission uses SF₆ ring-main units to improve reliability in rapidly urbanizing load centers. South Korea’s semiconductor expansion amplifies regional ultra-high-purity volumes, while Japan positions itself as a technology demonstrator for SF₆-free solutions, creating a dual-track landscape that blends incumbent and emerging technologies.

North America shows mid-single-digit consumption growth as utilities balance ageing-asset replacements with regulatory compliance. California’s 2033 phase-out and leak caps compel early adoption of monitoring and capture systems, but grid operators in other states continue to specify SF₆ in high-voltage classes where field-ready alternatives remain scarce. Federal infrastructure funding for resilience upgrades keeps overall demand stable, although rising recycling rates help temper fresh supply needs. Canada’s linkages to California’s cap-and-trade system drive cross-border policy alignment, nudging Canadian utilities to explore SF₆-free pilots while maintaining critical spares for legacy equipment.

Europe faces the most stringent policy environment: the revised F-gas regulation bans new medium-voltage SF₆ switchgear from 2026 and high-voltage installations from 2032. Transmission system operators, led by entities in Germany and the Nordics, are piloting vacuum-interrupter and clean-air technologies but still rely on SF₆ for brownfield extensions. The United Kingdom mirrors EU limits, adding compliance costs estimated at GBP 100-280 million for retrofit programs. Southern and Eastern European utilities with slower replacement cycles face cost pressures, potentially extending limited SF₆ procurement beyond mid-decade. Latin America, the Middle East, and Africa collectively remain smaller yet high-growth territories as they expand base-line electrification and industrial capacity, offering future upside for the sulfur hexafluoride market.

Regulatory Landscape

SF6 use is being constrained through fluorinated-gas rules that target switchgear and industrial uses. In the European Union, Regulation (EU) 2024/573 (in force since March 2024) tightens controls on fluorinated greenhouse gases and forms the basis for the report's Europe-focused environment, including restrictions that remove SF6 from new medium-voltage switchgear from 2026 and set a 2032 cutoff for high-voltage installations. It also pushes lifecycle controls such as reclaimed or recycled gas use for servicing as timelines move toward 2035.

In the United States, compliance pressure is shaped by mandatory reporting plus state-level phase-down rules. EPA greenhouse gas reporting requirements (GHGRP) for electric power systems require covered owners of SF6-containing transmission and distribution equipment to quantify and report annual emissions, while California (CARB, 17 CCR 95352) sets equipment phase-out schedules for new SF6 gas-insulated equipment by voltage class and enforces stringent leak-rate expectations for utilities. Together, these frameworks increase the operational importance of leak detection, recovery, and certified handling across the installed base even where SF6 remains in service.

Value Chain Analysis

The SF6 value chain starts with fluorine chemistry feedstocks (notably hydrogen fluoride), then moves through synthesis, purification, and cylinder filling. Output is split into electronic/technical grades for power equipment and ultra-high-purity grades for semiconductor and display fabrication. Supply is moderately concentrated among global industrial gas majors (Air Liquide, Linde, Air Products) and regional specialists (for example, Fujian Yongjing and Guangdong Huate Gas in China), and stringent quality and environmental compliance requirements raise barriers to new capacity.

Downstream, electrical utilities and switchgear OEMs (including Hitachi Energy, Siemens, and GE Vernova in the report scope) procure SF6 for new equipment where permitted, as well as for top-ups and service across long-lived assets. Semiconductor fabs also depend on tightly controlled purity, packaging, and logistics. Regulatory tightening in the EU and select US states is shifting value capture toward recovery, recycling, and reclamation services, increasing the role of specialized handling equipment, certified technicians, and closed-loop cylinder logistics to reduce emissions and manage constrained availability during maintenance cycles.

Competitive Landscape

The sulfur hexafluoride industry is moderately concentrated, with a handful of global gas majors accounting for the bulk of purified supply. Air Liquide, Linde, and Air Products leverage extensive separation, liquefaction, and cylinder logistics to service utilities and chipmakers. Each firm is simultaneously investing in SF₆-free dielectrics and recovery equipment to future-proof portfolios, a dual strategy that preserves near-term revenues while addressing stakeholder decarbonization expectations. Hitachi Energy, Siemens, and GE Vernova lead equipment innovation, fielding pilot-scale vacuum interrupters and fluoronitrile blends that promise 99% lower warming potential.

Regional specialists, including Fujian Yongjing and Guangdong Huate Gas, supply domestic Chinese utilities and electronics firms, benefitting from proximity and government support. These players could capture share as global suppliers rationalize SF₆ volumes under carbon caps. Price competition remains muted because purification plants require high capital intensity and rigorous quality certification, traits that deter new entrants. Going forward, competitive advantage will stem less from price and more from integrated offerings that bundle gas recovery, certified recycling, and low-GWP retrofits—capabilities that position suppliers for a controlled transition rather than abrupt disruption.

Sulfur Hexafluoride Industry Leaders

Linde plc

Air Liquide

Air Products and Chemicals, Inc.

Solvay S.A.

Fujian Yongjing Technology Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The tightening policy environment creates a clear whitespace for circular SF6 services, not only new-gas supply, particularly in regions where installed switchgear fleets must be maintained for decades. The EU F-gas framework (Regulation (EU) 2024/573, effective March 2024) and California rules in 17 CCR 95352 both increase the practical value of end-to-end offerings that bundle gas recovery, testing, reclamation, and compliant documentation. This supports industrial gas suppliers and specialist service providers in deepening recurring revenue from the installed base, even as new-use bans expand in parts of Europe.

On the technology side, commercialization of SF6-free switchgear is changing demand patterns by shifting procurement from gas volume toward alternative-dielectric ecosystems and transition support. Utility and OEM actions show active investment in non-SF6 solutions while still requiring interim management of legacy SF6 stocks, including Hitachi Energy moving SF6-free GIS to ultra-high-voltage classes (including on-site testing milestones with TenneT Germany at 420 kV and an SF6-free 550 kV GIS order with Chubu Electric Power Grid in 2026). Schneider Electric deployments of SF6-free switchgear with Southern California Edison also reinforce this direction. Alongside these deployments, ongoing research into alternative insulating media, including published work in 2026 on bis(trifluoromethyl) sulfide mixtures and 2024 research on azeotropic alternatives, supports a pipeline of substitute options that can expand qualification activity across grid operators and OEMs.

Recent Industry Developments

- June 2026: Hitachi Energy and TenneT Germany completed on-site high-voltage testing of the world's first SF6-free 420 kV gas-insulated switchgear at the Erzhausen substation in Germany. The milestone advances validation for SF6-free solutions at transmission voltages where SF6 has historically been difficult to replace, supporting broader procurement readiness under tightening European F-gas constraints.

- May 2026: Enedis and Schneider Electric signed a four-year framework agreement to accelerate deployment of SF6-free electrical equipment across France. The structure of a multi-year utility framework helps convert pilots into scaled rollouts, improving visibility for supply chains around alternative-dielectric switchgear and related services.

- December 2024: Kanto Denka Kogyo reinforced its positioning in ultra-high-purity SF6 supply for semiconductor manufacturing, emphasizing products tailored to advanced electronics processes and regional logistics strength in East Asia. This underscores continued investment focus on electronic-grade supply chains even as utility-side regulations tighten, keeping specialty purity and packaging capabilities strategically important.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers global demand for sulfur hexafluoride (SF6) gas used across industrial and electrical applications, measured as total consumption volume across end uses and regions during the study period.

Scope exclusions: We exclude alternative insulating and etching gases that can replace SF6, and we do not count downstream equipment value such as switchgear or semiconductor tools.

Segmentation Overview

- By Product Type

- Electronic / Technical Grade

- Ultra-High Purity Grade

- By Application

- Power and Energy

- Electronics

- Metal Manufacturing

- Medical

- Other Applications (Window Insulation, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on where SF6 is used and what typically drives consumption. We rely on public sources such as energy and grid statistics from agencies like the US Energy Information Administration, international electricity and transmission indicators from the International Energy Agency, and industrial production series from sources such as the World Bank and OECD.

We also review regulatory and safety references that influence usage patterns, using sources such as the US EPA and the European Environment Agency, along with customs and trade statistics from UN Comtrade to sanity-check cross-border movement. Company filings, investor presentations, and reputable press are used to understand capacity additions, plant restarts, and demand signals from power and electronics end users. When needed, we supplement with paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records to clarify supply chains and confirm timelines. These desk sources are illustrative, and many other public references were also used for data collection, validation, and clarifying assumptions.

Primary Interviews and Surveys

Primary inputs are used to pressure-test model assumptions that are hard to observe in public data, especially application split, purity mix, and regional consumption behavior. We spoke with a mix of SF6 producers, gas distributors, equipment and service ecosystem participants, and large end users, and then cross-checked gaps with follow-up questions across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 44% |

| Mid tier: 58% | Functional/Unit leaders: 37% | EMEA: 35% |

| Smaller Players: 14% | Managers: 50% | Americas: 21% |

Market-Sizing & Forecasting

Our sizing uses a top-down reconstruction that starts from application demand pools and then converts them into SF6 consumption using practical intensity and replacement factors. For power and energy, the model is anchored on installed-base additions and maintenance cycles for gas-insulated equipment, which are then adjusted for leakage, refill rates, and regulatory handling practices.

Results are corroborated with selective bottom-up approximations, including supplier and distributor roll-ups in key countries, sampled price per kg by grade, and channel checks on typical purchase lot sizes. A few important inputs that move the totals include grid expansion and refurbishment activity, switchgear installation and service cadence, semiconductor fab capacity expansion and etch-gas usage intensity, purity grade mix, and regional handling and recovery compliance.

Forecasting uses scenario analysis supported by short-run exponential smoothing on leading indicators, then is tuned with expert feedback on regulation timelines and substitution pace. Where direct bottom-up visibility is weak in smaller end uses, we apply conservative intensity ranges and keep them consistent with observed trade flows and the interview-based usage ranges.

Data Validation & Update Cycle

Outputs are checked in several steps so the final series stays consistent by region, by application, and over time. We compare model totals against independent signals such as trade directionality, capacity change news, and implied consumption per unit of end-market activity, and then investigate variances that fall outside expected ranges.

Before sign-off, another analyst reviews assumptions and the math flow, and any unusual shifts trigger re-contacts with industry participants to confirm what changed. Reports are refreshed annually, and interim updates are made when material events occur, including regulation changes, large capacity moves, or sharp price changes. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's Sulfur Hexafluoride Market Size Compared With Other Published Estimates

Published SF6 market numbers often differ because the underlying measurement unit and included revenue pools are not the same across studies. Differences usually come from whether the estimate is built in tons versus USD, how purity grades are priced, what is treated as captive consumption, and how frequently assumptions are refreshed.

Switchgear and other gas-insulated equipment revenue sits outside Mordor Intelligence scope here, which is why value-based estimates that bundle equipment with SF6 refills and services can appear much larger than a pure gas-consumption view. The spread also widens when some sources apply a single global average price per kg, skip recovery and reuse effects, or use older currency timing for conversion and inflation assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.08 B (2026) | |

| Industry Publisher A | USD 0.31 B (2025) | Value-based sizing that can blend SF6 gas sales with adjacent service and handling revenue, and it is sensitive to assumed pricing and grade mix in 2025. |

| Industry Publisher B | USD 0.27 B (2023) | Value-based estimate that may apply broad average prices and segment definitions across grades and uses, which can shift the implied market level versus tonnage-led modeling. |

The table shows that most gaps are explained by unit choice and what gets counted as market value rather than gas volume. By keeping the scope tied to SF6 consumption drivers and then validating the implied totals with trade and interview checks, the estimate stays traceable to clear variables and can be repeated when assumptions change.

Key Questions Answered in the Report

What is the current size of the sulfur hexafluoride market?

The sulfur hexafluoride market size stood at 83.98 kilotons in 2026 and is forecast to reach 101.84 kilotons by 2031.

Which region leads global SF₆ consumption?

Asia-Pacific holds the largest share at 47.82% thanks to intensive grid expansion and semiconductor investments.

Why is SF₆ still dominant in high-voltage switchgear despite environmental concerns?

Its unmatched dielectric strength and arc-quenching ability allow compact designs and faster energization, advantages that alternative gases have yet to replicate fully.

Which application segment is growing the fastest?

Medical uses, particularly in ophthalmology procedures, are expanding at a 4.58% CAGR through 2031.

How are regulators affecting the sulfur hexafluoride market outlook?

Aggressive phase-out timelines in the EU and California subtract up to 1.8 percentage points from forecast CAGR, prompting utilities to accelerate alternative-gas pilots.

Page last updated on: