Aluminium Potash Sulphate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminium Potash Sulphate Market Analysis by Mordor Intelligence

The Aluminium Potash Sulphate Market size is projected to be USD 1.28 billion in 2025, USD 1.34 billion in 2026, and reach USD 1.68 billion by 2031, growing at a CAGR of 4.59% from 2026 to 2031. Municipal water-treatment programs, which use alum as a coagulant, drive demand resilience. Circular-economy approaches, such as utilizing electro-Fenton sludge and aluminum scrap, are reducing carbon footprints by up to 75%. This development strengthens procurement cases in regions with carbon pricing. In Europe, regulatory clarity on permissible aluminum levels in cosmetics is encouraging formulators to transition to pharmaceutical-grade potash alum, supporting higher-margin volumes. The Asia-Pacific region leads capacity expansions in textile and leather processing. Furthermore, digital business-to-business (B2B) platforms are enabling small and medium-sized enterprises (SMEs) to access small-lot liquid-alum purchases. These factors collectively maintain stable pricing, even as Chinese export-duty adjustments tighten the supply of virgin bauxite.

Key Report Takeaways

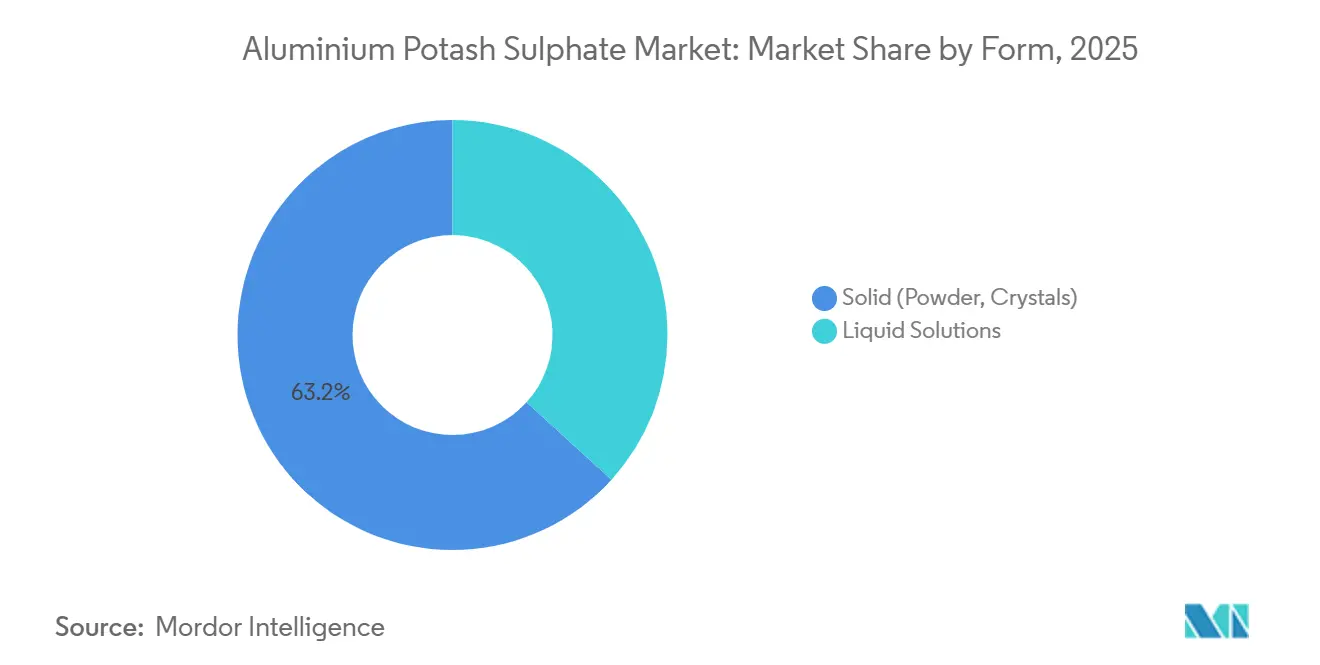

- By form, solid powder and crystal formats commanded 63.24% of aluminium potash sulphate market share in 2025, while liquid solutions recorded the fastest growth at 5.51% CAGR to 2031.

- By grade, industrial-grade alum led with 60.56% share of the aluminium potash sulphate market size in 2025; pharmaceutical and cosmetic grades are forecast to expand at 5.83% CAGR through 2031.

- By application, water and wastewater treatment held 46.22% share of the aluminium potash sulphate market in 2025, whereas cosmetics and personal care are advancing at 6.11% CAGR to 2031.

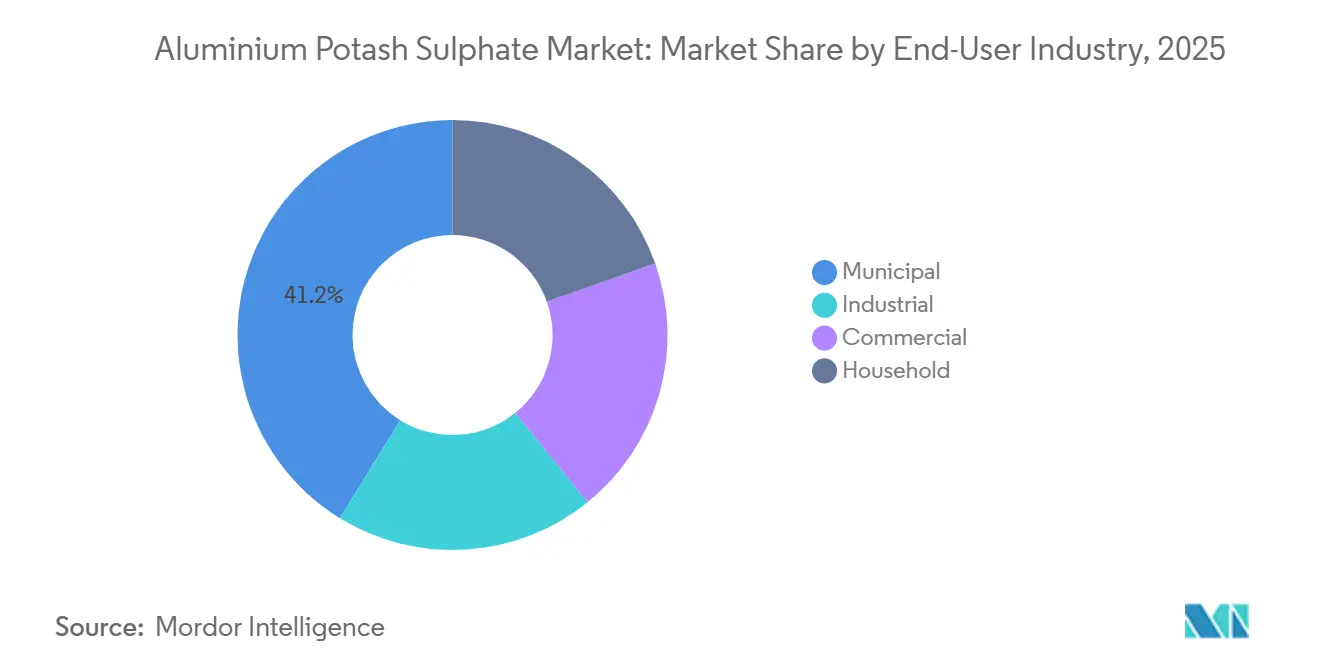

- By end-user industry, municipal utilities accounted for 41.23% of demand in 2025, but the household segment is projected to grow fastest at 5.89% CAGR during 2026-2031.

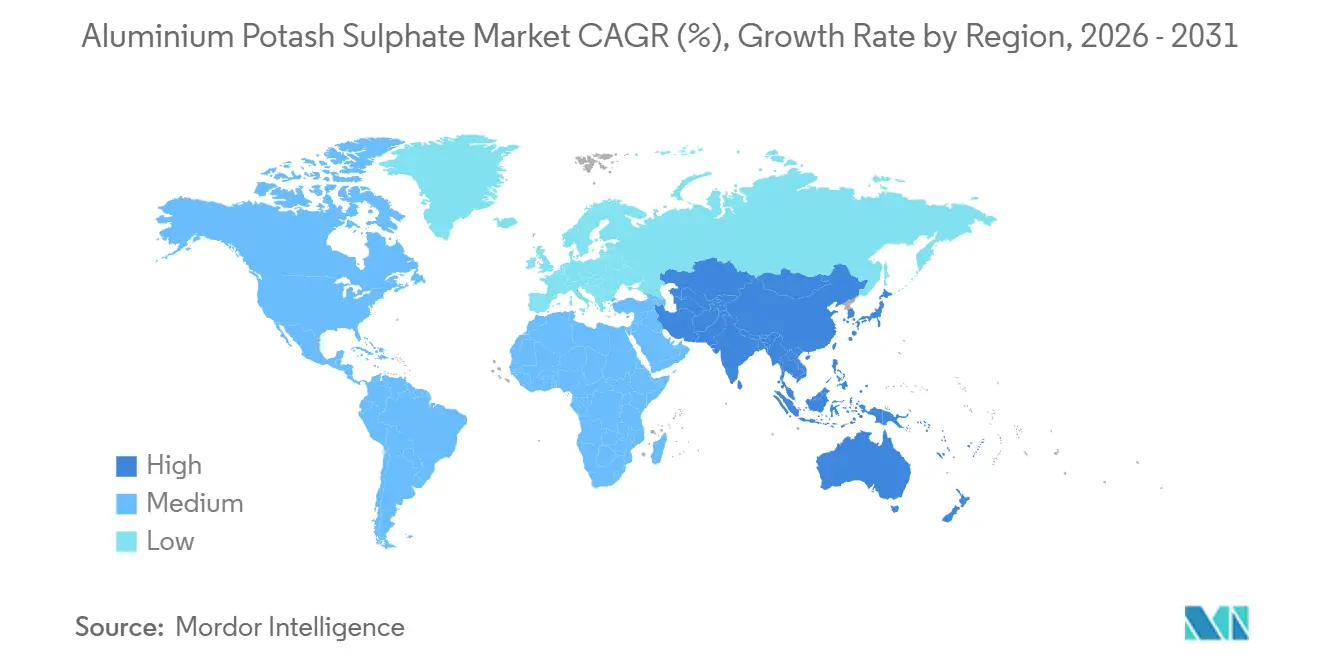

- By geography, Asia-Pacific captured 46.88% revenue share in 2025 and is set to register a 5.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aluminium Potash Sulphate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased use in natural deodorants and personal-care astringents | +0.9% | Global, with the strongest uptake in North America and the EU | Medium term (2-4 years) |

| Expansion of textile and leather processing in Asia-Pacific | +1.2% | APAC core (India, China, ASEAN), spill-over to South Asia | Long term (≥ 4 years) |

| Up-cycling of aluminium waste into high-purity potassium alum | +0.7% | Global, early adoption in China, the EU, and North America | Medium term (2-4 years) |

| Adoption in plant-based meat processing as clean-label firming agent | +0.4% | North America and the EU, emerging in APAC urban centers | Short term (≤ 2 years) |

| Digital-direct B2B distribution unlocking SME demand | +0.6% | Global, concentrated in digitally mature markets (North America, EU, urban APAC) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Use in Natural Deodorants and Personal-Care Astringents

In April 2024, regulators endorsed potassium alum's safety at specific concentrations. This approval led to an increase in natural deodorant launches across both mass and premium markets. Clinical studies indicate that 2-5% formulations reduce underarm odor in less than two weeks with minimal irritation. This enables brands to promote a plant-based narrative without blocking sweat ducts. Formats such as roll-ons and gels, particularly those using hydrogel carriers, are attracting consumers. Additionally, transparent ingredient labels are aligning with the preferences of clean-beauty consumers. Private-label retailers in the United States and Germany are now placing alum crystals alongside synthetic antiperspirants, reflecting broader market acceptance. Suppliers certifying particle sizes under 10 micrometers (µm) for sprays are experiencing increased sales volumes.

Expansion of Textile and Leather Processing in Asia-Pacific

As apparel and footwear production shifts from China to India, Vietnam, and Bangladesh, regional processors are increasing their mordanting and tanning capacities. China's export duties of up to 30% on aluminum products are tightening global alum feedstocks, prompting downstream buyers to secure multi-year supply contracts. European Union (EU) regulations limiting chromium effluent are accelerating the transition to aluminum-based tanning agents, which are less toxic. Furthermore, India's Production Linked Incentive scheme for textiles is driving alum consumption. Multinational leather brands are implementing purchasing scorecards that prioritize suppliers using lower-carbon alum, encouraging mills to adopt waste-aluminum valorization methods.

Up-Cycling of Aluminium Waste into High-Purity Potassium Alum

Pilot plants in France and the United States are converting aluminum scrap and electro-Fenton sludge into alum that meets United States Pharmacopeia (USP) specifications, achieving carbon intensities 50-70% lower than traditional methods. Innovations such as two-stage acid leaching followed by ammonium hydroxide (NH₄OH) precipitation are achieving 95-97% purity and are economically viable when disposal-fee credits are considered. Municipal water utilities adopting on-site regeneration are reporting procurement savings of USD 0.20 per cubic meter (m³) of treated water. EU circular-economy mandates and extended-producer-responsibility schemes are driving market adoption. However, challenges persist regarding trace heavy metals, though ISO 17025-accredited testing laboratories are addressing these quality-control issues.

Adoption in Plant-Based Meat Processing as Clean-Label Firming Agent

Potassium alum's Generally Recognized as Safe (GRAS) status provides a regulatory pathway for its use at low parts per million (ppm) levels to strengthen plant-protein matrices, enhancing bite and water retention without synthetic phosphates[1]Samruddhi Gajbhiye et al., “Pharmacological & Physiochemical Properties of Potash Alum,” ijpsjournal.com . Initial commercial launches in North American retail chains have received positive sensory feedback. However, brands must disclose aluminum on ingredient lists, necessitating consumer education. Formulators are capping residual aluminum below 1 milligram (mg) per serving to comply with European Food Safety Authority (EFSA) tolerable limits. This texture improvement supports a 10-15% price premium over traditional vegan burgers. Pilot lines in Singapore and Tokyo are exploring co-processing with konjac and pea protein to cater to local flavor preferences.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter limits on aluminium in foods and cosmetics | -0.8% | EU and North America, emerging in APAC | Medium term (2-4 years) |

| Geopolitical potash-supply volatility (sanctions, export bans) | -0.6% | Global, acute in EU dependent on Belarus/Russia potash | Short term (≤ 2 years) |

| High energy intensity of alum crystallisation limiting green credentials | -0.5% | Global, most material in carbon-regulated markets (EU, California) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Limits on Aluminium in Foods and Cosmetics

Formulators are required to either reduce aluminum levels or invest in analytical verifications due to maximum aluminum thresholds set by the European Scientific Committee on Consumer Safety (SCCS) opinion and increasing consumer scrutiny[2]Directorate-General for Health and Food Safety, “SCCS – Final Opinion on the Safety of Aluminium in Cosmetic Products,” EUROPA.EU . Germany's regulations prohibit uncoated aluminum from coming into contact with acidic foods, necessitating retrofits for coatings and reducing the demand for bulk aluminum. Additionally, testing for nanoform exclusions introduces additional laboratory costs. These regulations enhance consumer safety but also impact growth, particularly in sectors like spray deodorants and acidic pickling.

Geopolitical Potash-Supply Volatility

Despite partial relief from United States (U.S.) sanctions, Belarus's transit bans via Lithuania are affecting the European Union's (EU) potash supplies, leading to increased aluminum production costs. European buyers are sourcing from Canada and Israel at higher freight costs. Meanwhile, Asian producers are utilizing Russian rail routes but face risks from potential changes in export controls. Spot potash prices increased by 17% year-on-year in the first quarter (Q1) of 2026, prompting downstream users to shift from annual to quarterly pricing negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Solutions Gain Traction

In 2025, solid powder and crystal formats held a 63.24% share of the aluminium potash sulphate market, supported by advantages such as dense storage, established dosing equipment, and cost-efficiency. Liquid solutions are projected to grow at a 5.51% compound annual growth rate (CAGR) through 2031. This growth is driven by digital channels enabling small and medium enterprises (SMEs) to avoid on-site dissolution tanks, reducing capital expenditures. Field trials in France demonstrated that electro-Fenton sludge can replace 50% of purchased liquid alum without affecting coagulation efficiency. Municipal utilities continue to prefer dry forms for their bulk storage stability, while craft cosmetic producers opt for pre-dissolved grades to minimize dust exposure. Additionally, hybrid concentrate pouches designed for automated dispensers are merging traditional formats, allowing suppliers to market both.

North America is experiencing significant growth in liquid solutions due to the Occupational Safety and Health Administration (OSHA) dust-exposure limits encouraging liquid dosing. Conversely, textile mills in the Asia-Pacific region maintain powder-feed systems due to lower labor costs and established supply chains. As containerized shipping becomes more efficient, the economics of liquid freight improve, addressing previous challenges associated with water weight. The competitive landscape will depend on suppliers' ability to ensure shelf-life stability and prevent microbial growth in aqueous solutions.

By Grade: Pharmaceutical and Cosmetic Grades Outpace Industrial

In 2025, industrial grades accounted for 60.56% of the aluminium potash sulphate market, driven by applications in water treatment and textile mordanting. Pharmaceutical and cosmetic grades are forecast to grow at a 5.83% CAGR through 2031, supported by European Union (EU) regulations on particle sizes for aerosols, which effectively require near-United States Pharmacopeia (USP) purity. Price premiums of 30-50% are encouraging producers to invest in recrystallization and inductively coupled plasma mass spectrometry (ICP-MS) analytics. Food-grade alum occupies a middle ground, catering to baking and the growing plant-protein market, which demands Generally Recognized as Safe (GRAS) compliance but not full pharmacopeial standards.

Producers implementing closed-loop rinsing and high-efficiency particulate air (HEPA) filtration are achieving heavy-metal baselines below 10 parts per million (ppm), meeting Nordic eco-label standards. While industrial buyers in Asia-Pacific remain cost-focused, cosmetics exporters in South Korea are increasingly requiring European Pharmacopeia (EP)/USP certification to meet EU import standards. This segmentation divides the aluminium potash sulphate market into volume-driven industrial channels and value-driven specialty segments, encouraging dual-line manufacturing strategies.

By Application: Cosmetics and Personal Care Surge

Water and wastewater treatment led the aluminium potash sulphate market in 2025, accounting for 46.22% of usage due to long-standing municipal contracts. However, the cosmetics and personal care segment is projected to grow at a 6.11% CAGR through 2031. This growth is driven by the increasing popularity of natural deodorants, now widely available in U.S. drugstores and EU supermarkets. Peer-reviewed studies have shown that 3% alum roll-ons provide 24-hour efficacy without causing irritation associated with chlorohydrate, prompting reformulations by brands.

Textile and leather industries are experiencing steady growth, supported by capacity expansions in the Asia-Pacific. The plant-based meat processing sector, while still emerging, presents growth opportunities for food applications, a segment traditionally limited to pickling and baking. Pharmaceutical applications, such as topical hemostats and bladder irrigation, remain niche but command premium pricing. Suppliers can capitalize on cross-application synergies by repurposing high-purity streams for both cosmetic and medical uses, optimizing asset utilization.

By End-User Industry: Household Segment Accelerates

In 2025, municipal utilities accounted for 41.23% of demand. However, household adoption of natural crystal deodorants is growing at a 5.89% CAGR. The "one-ingredient" trend, amplified by social media influencers, is resonating with consumers. E-commerce platforms in the United States are reporting double-digit growth in sales of alum sticks. Industrial sectors, including tanneries and paper mills, are increasingly blending virgin and recovered alum to optimize costs and meet environmental, social, and governance (ESG) targets. Commercial institutions, such as hotels and hospitals, are adopting liquid alum for on-site grey-water recycling, favoring turnkey dosing skids that reduce maintenance requirements.

Household penetration remains low in emerging markets, but rising disposable incomes indicate potential for growth. Municipal segments are expected to continue driving base-load volumes, creating economies of scale that lower per-unit costs for smaller segments. Suppliers who balance large contracts with flexible stock-keeping unit (SKU) offerings are well-positioned to capture diverse revenue streams in the aluminium potash sulphate market.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.88% of the aluminium potash sulphate market share and is projected to achieve a 5.81% compound annual growth rate (CAGR) through 2031. China's 711 million-ton bauxite reserves, along with its export-duty regime, are tightening the supply of alum feedstock. This has led processors in India and Vietnam to explore alternative supply chains and invest in scrap-based alum production. Japan and South Korea are utilizing high-purity alum in semiconductor-grade water systems, while ASEAN nations are expanding their textile and leather industries under favorable trade agreements. Regional growth is supported by urbanization, stricter wastewater standards, and policies promoting a circular economy.

North America demonstrates stable municipal demand, with notable growth in household and cosmetics applications. The United States Environmental Protection Agency’s (EPA) nutrient criteria continue to drive alum dosing for phosphorus removal, maintaining baseline consumption. Proximity to Saskatchewan potash ensures a reliable feedstock supply, while Mexico's maquiladora industries are increasingly adopting high-purity water treatment solutions.

Europe, operating under stringent Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) and Scientific Committee on Consumer Safety (SCCS) regulations, is experiencing increased demand for pharmaceutical-grade alum with precise particle-size control. Geopolitical disruptions in potash supply have raised costs, but circular economy incentives are encouraging aluminum-scrap utilization. Germany and France are key markets for cosmetics applications, while Nordic utilities are implementing renewable-powered crystallisation to meet low-carbon procurement requirements.

South America and the Middle East & Africa are emerging markets in this sector. Brazil's sanitation programs and Saudi Arabia's desalination pre-treatment initiatives are driving baseline growth. However, logistical challenges and limited analytical capacity are constraining short-term expansion. Multilateral infrastructure funding is expected to enhance market penetration over the next decade.

Competitive Landscape

The aluminium potash sulphate market is moderately fragmented. Global distributors Avantor, Thermo Fisher Scientific, and Merck KGaA utilize validated supply chains and Good Manufacturing Practice (GMP) warehousing to maintain a strong presence in pharmaceutical-grade product channels. Regional producers such as Amar Narain Industries in India and Zibo Dazhong in China focus on competitive pricing strategies for industrial-grade tenders. Companies adopting circular economy practices are converting aluminum dross into alum, leveraging Environmental, Social, and Governance (ESG) credentials to secure contracts with European municipalities.

Technological advancements emphasize decarbonized crystallization. For example, Bouhoufani et al. have demonstrated an electro-Fenton sludge valorization process that can replace up to 60% of purchased alum and reduce wastewater treatment costs by USD 0.24 per cubic meter. In the United States and Germany, digital marketplaces are disrupting traditional distributors by offering transparent pricing and rapid fulfillment, prompting incumbents to integrate e-commerce capabilities.

Strategic collaborations between potash miners and alum refiners aim to manage feedstock price volatility. Additionally, cosmetics brands are entering into offtake agreements for low-nanoform grades. Mergers and acquisitions are increasingly targeting specialty purification firms capable of meeting aerosol particle-size requirements. Competitive intensity is significant in Asia-Pacific industrial segments, while pharmaceutical and cosmetic sectors benefit from higher barriers to entry and stable margins.

Aluminium Potash Sulphate Industry Leaders

Merck KGaA

Thermo Fisher Scientific Inc.

Hengyang Jianheng Industry Development Co., Ltd.

Zibo Dazhong Edible Chemical Co., LTD.

HOLLAND COMPANY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bouhoufani Y. et al. reported that anodic aluminum dissolution in electro-Fenton systems facilitates the in-situ production of aluminum potassium sulfate, reducing pharmaceutical wastewater treatment costs by up to 50%. This approach offers a cost-effective solution by leveraging the chemical properties of aluminum potassium sulfate in the treatment process.

- March 2025: Gajbhiye published a review in the International Journal of Pharmaceutical Sciences (IJPS), confirming the Generally Recognized As Safe (GRAS) status of aluminum potassium sulfate. The study also verified the stability of a deodorant formulation containing alum over a 24-month period, providing valuable support for regulatory filings.

Global Aluminium Potash Sulphate Market Report Scope

Aluminium Potash Sulphate, also referred to as potash alum, is a naturally occurring mineral salt. This colorless, crystalline compound is utilized as an astringent, antiseptic, and coagulant. Potash alum is commonly applied to stop minor bleeding, treat and purify water, preserve pickles, and as a natural deodorant.

The aluminium potash sulphate market is segmented by form, grade, application, end-user Industry and geography. By form, the market is segmented into solid (powder, crystals) and liquid solutions. By grade, the market is segmented into industrial grade, food grade, and pharmaceutical/cosmetic grade. By application, the market is segmented into water and wastewater treatment, textile and leather processing, cosmetics and personal care, food and beverage additives, pharmaceuticals and medical, paper and pulp industry, and other (photography, fireproofing, agriculture). By end-user Industry, the market is segmented into municipal, industrial, commercial, and household. The report also covers the market size and forecasts for aluminium potash sulphate in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Solid (Powder, Crystals) |

| Liquid Solutions |

| Industrial Grade |

| Food Grade |

| Pharmaceutical/Cosmetic Grade |

| Water and Wastewater Treatment |

| Textile and Leather Processing |

| Cosmetics and Personal Care |

| Food and Beverage Additives |

| Pharmaceuticals and Medical |

| Paper and Pulp Industry |

| Other (Photography, Fireproofing, Agriculture) |

| Municipal |

| Industrial |

| Commercial |

| Household |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Solid (Powder, Crystals) | |

| Liquid Solutions | ||

| By Grade | Industrial Grade | |

| Food Grade | ||

| Pharmaceutical/Cosmetic Grade | ||

| By Application | Water and Wastewater Treatment | |

| Textile and Leather Processing | ||

| Cosmetics and Personal Care | ||

| Food and Beverage Additives | ||

| Pharmaceuticals and Medical | ||

| Paper and Pulp Industry | ||

| Other (Photography, Fireproofing, Agriculture) | ||

| By End-User Industry | Municipal | |

| Industrial | ||

| Commercial | ||

| Household | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the aluminium potash sulphate market be by 2031?

The Aluminium Potash Sulphate Market size is projected to be USD 1.28 billion in 2025, USD 1.34 billion in 2026, and reach USD 1.68 billion by 2031, growing at a CAGR of 4.59% from 2026 to 2031.

Which region leads to the demand for aluminium potash sulphate?

Asia-Pacific held 46.88% of global revenue in 2025 and remains the fastest-growing region at a 5.81% CAGR.

What grade segment is expanding fastest?

Pharmaceutical and cosmetic grades are forecast to grow at 5.83% CAGR due to stringent purity needs in natural deodorants and sprays.

Why are liquid alum solutions gaining popularity?

Digital B2B channels let SMEs buy pre-dissolved alum, avoiding on-site mixing gear and dust-exposure issues, which drives a 5.51% CAGR for liquids through 2031.

Page last updated on: