Subscriber Data Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

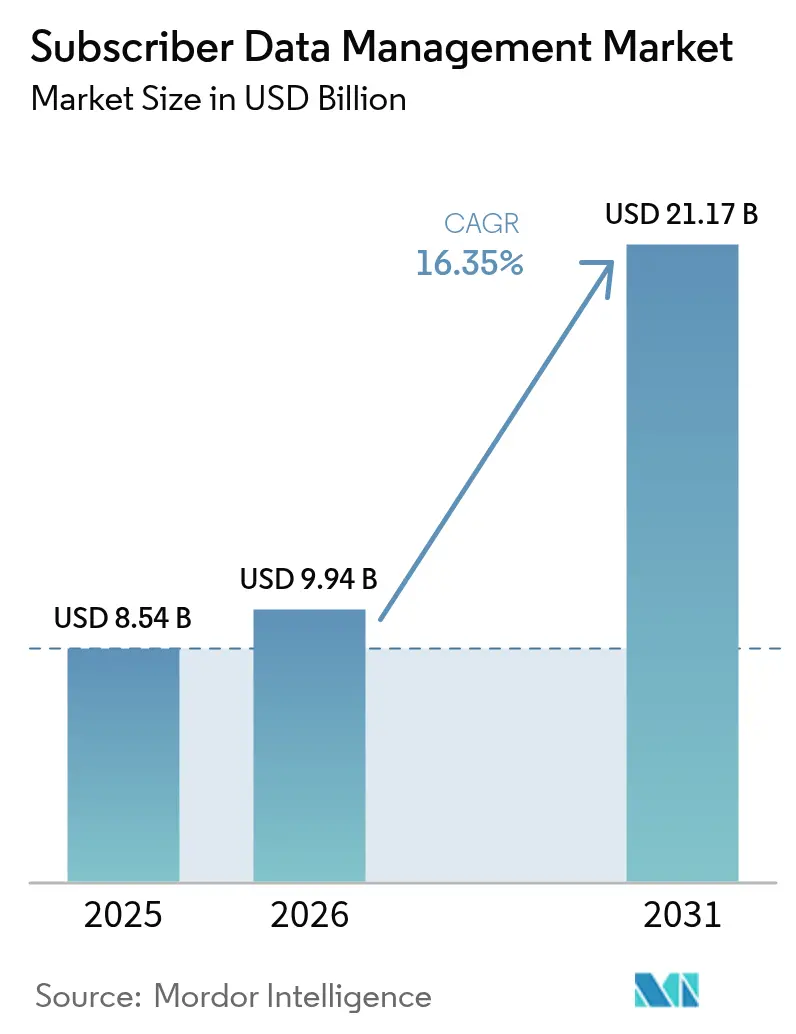

| Market Size (2026) | USD 9.94 Billion |

| Market Size (2031) | USD 21.17 Billion |

| Growth Rate (2026 - 2031) | 16.35% CAGR |

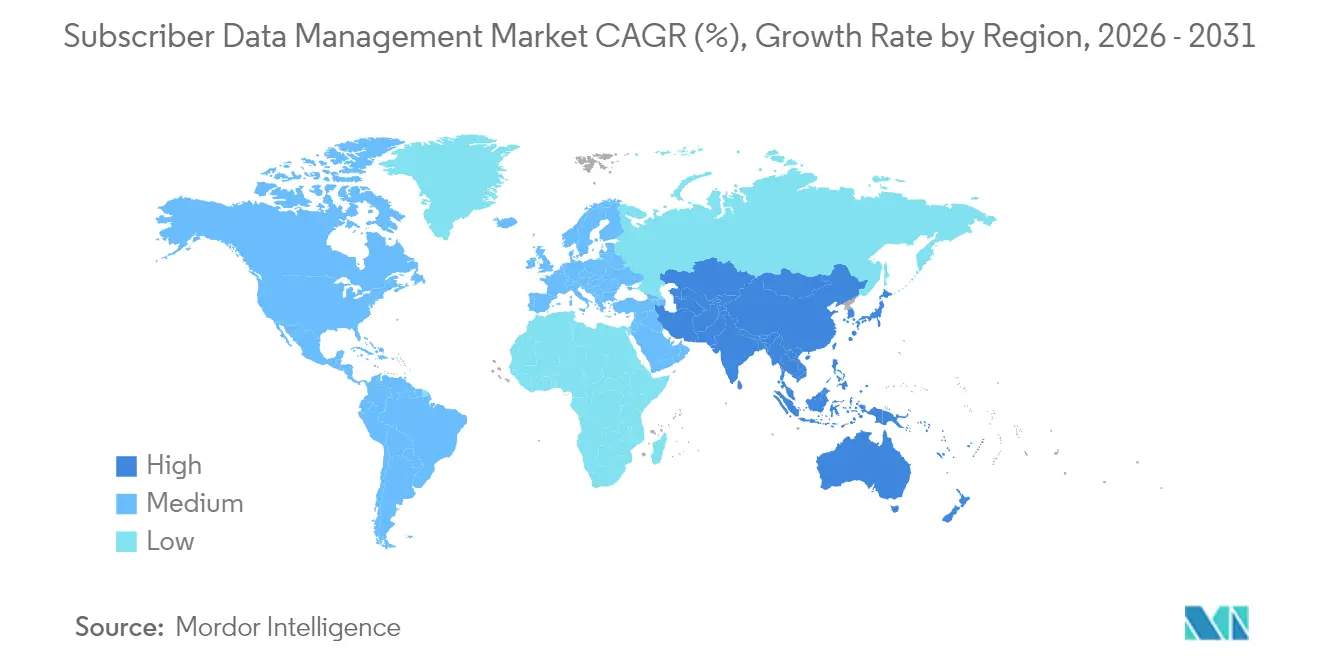

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subscriber Data Management Market Analysis by Mordor Intelligence

The Subscriber Data Management Market size was valued at USD 8.54 billion in 2025 and estimated to grow from USD 9.94 billion in 2026 to reach USD 21.17 billion by 2031, at a CAGR of 16.35% during the forecast period (2026-2031). This rapid expansion is anchored in the telecommunications sector’s shift to cloud-native cores and the spread of 5G standalone (SA) networks that demand real-time data orchestration and ultra-low-latency policy control. Operators also face mounting regulatory pressure to unify subscriber identities while connecting an ever-larger universe of IoT devices. North America holds the largest regional position thanks to extensive private-5G rollouts and strict data-sovereignty laws, yet Asia-Pacific posts the briskest growth pace on the back of China’s heavy 5G capital spend and India’s enterprise-centric private‐network programs. [1]GSMA, “The Mobile Economy Asia Pacific 2024,” GSMA, gsma.com Deployment preferences are quickly tilting toward cloud and hybrid models as operators juggle compliance with scalability, and large enterprise demand now coexists with a surging small- and medium-enterprise (SME) appetite for sophisticated data functions. Competitive intensity remains moderate: Ericsson, Nokia, and Huawei still command scale advantages, but cloud-native newcomers are applying AI to subscriber analytics, chipping away at incumbents’ share.

Key Report Takeaways

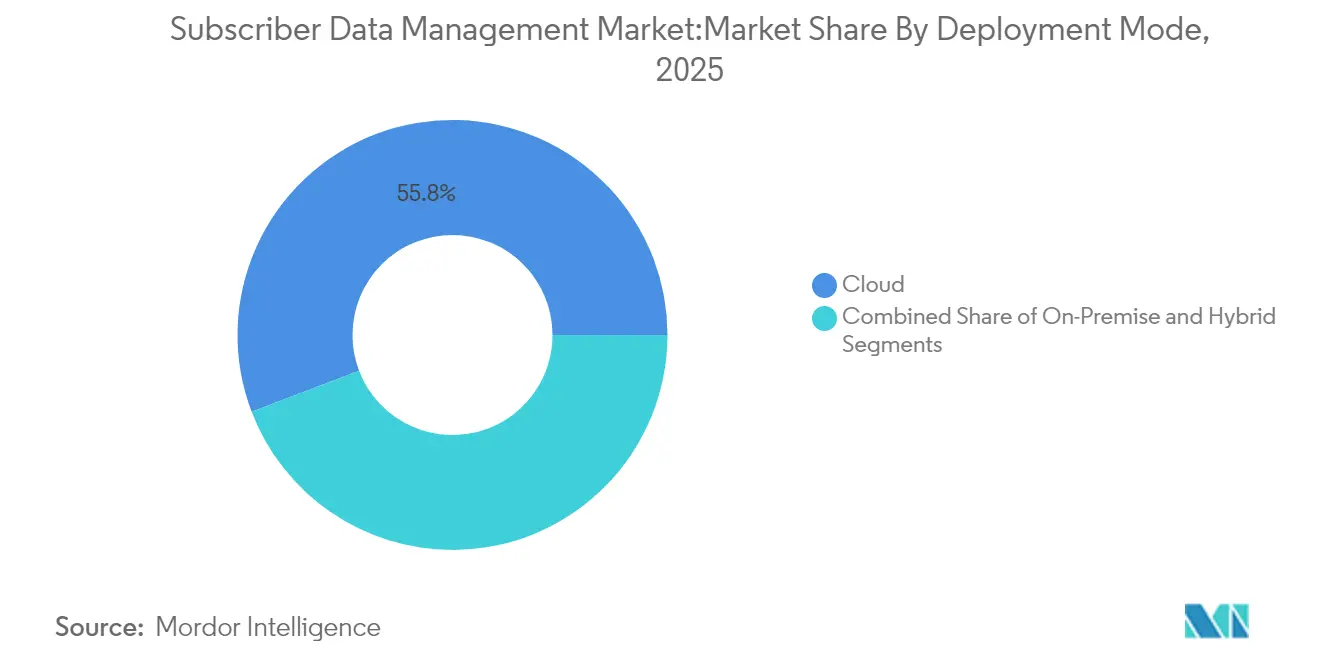

- By deployment mode, cloud deployments captured 55.80% of the subscriber data management market share in 2025; hybrid models are forecast to expand at an 18.1% CAGR to 2031.

- By organization size, large enterprises held 64.00% revenue share in 2025, while SMEs are projected to grow at a 19.1% CAGR through 2031.

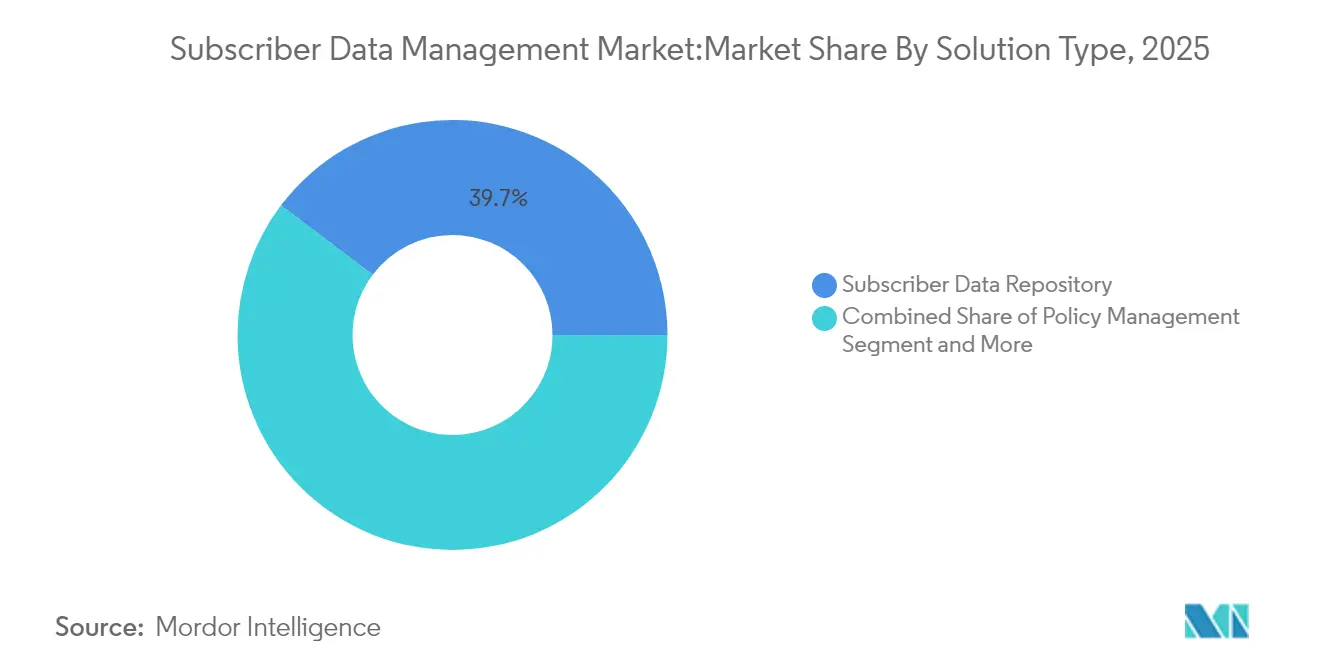

- By solution type, subscriber data repositories commanded a 39.70% share of the subscriber data management market size in 2025; identity-management solutions are set to advance at an 18.4% CAGR to 2031.

- By network type, 4G/LTE networks accounted for a 44.90% share in 2025, whereas 5G standalone networks are poised for a 18.8% CAGR through 2031.

- By end user, mobile-network operators controlled 57.40% share in 2025, while enterprises/IoT service providers exhibit the fastest growth at 19.0% CAGR to 2031.

- By geography, North America dominated with a 35.30% share in 2025, whereas Asia-Pacific is projected to grow at an 18.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Subscriber Data Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rollout of 5G networks | +3.2% | Global; APAC and North America lead | Medium term (2-4 years) |

| Shift toward cloud-native architectures | +2.8% | Global; strongest in Europe and North America | Short term (≤ 2 years) |

| Surge in IoT/mMTC device counts | +2.1% | Global; APAC manufacturing hubs | Long term (≥ 4 years) |

| Regulatory push for unified subscriber identity | +1.9% | Europe and North America primarily | Short term (≤ 2 years) |

| AI-driven real-time policy control adoption | +1.7% | Global; early adoption in developed markets | Medium term (2-4 years) |

| Private 5G and edge micro-core deployments | +1.5% | North America and Europe enterprise sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid rollout of 5G networks

Commercial 5G SA cores are now live in more than 50 nations, and China alone recorded over 800 million 5G connections in 2024. SA architecture collapses the control plane into cloud-native functions that centralize data across multiple access types, making subscriber data management the lynchpin for network slicing, enterprise SLAs, and micro-second policy execution. Mobile-core capex accelerated 32% in 2024 as operators recognized that a robust subscriber data layer underpins future monetization—illustrated by Bharti Airtel’s Ericsson-powered SA core geared to differentiated consumer and enterprise slices. [2]Ericsson, “Airtel partners Ericsson 5G Core to drive 5G evolution,” Ericsson, ericsson.com

Shift toward cloud-native architectures

Operators migrating from monolithic HSS/UDM stacks to microservices report up to 30% lower total cost of ownership, plus elastic scaling that aligns spend with traffic. Three UK’s move to a cloud core that tops 9 Tbps demonstrates how containerized subscriber data functions support in-service upgrades without downtime. MVNOs exploit the same model, using Optiva’s Google-Cloud hubs for fast launch cycles that fold in AI customer analytics.

Surge in IoT/mMTC device counts

Manufacturing plants using private 5G record 15-20% efficiency gains when subscriber data segmentation isolates sensor traffic from corporate IT flows, as AIS proved at Midea Thailand. Each device often carries its own authentication, policy, and routing attributes, multiplying data-record volume. Scalable unified-data repositories now must support millions of simultaneous IoT identities at edge micro-cores to keep latency below 10 ms for safety-critical workloads.

AI-driven real-time policy control adoption

AI engines embedded in modern policy functions study live session behavior, predict congestion, and pre-assign quality-of-service marks before bottlenecks hit, lifting customer experience metrics while trimming opex. Optiva’s cloud BSS infuses generative AI into real-time analytics so MVNOs can personalize offers and curb churn. Patent activity from Samsung and others underscores a race to embed machine-learning-based traffic classification directly inside user-plane functions for encrypted flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and sovereignty mandates | -2.1% | Europe prim.; spreading worldwide | Short term (≤ 2 years) |

| Integration complexity with legacy OSS/BSS | -1.8% | Global; mature markets hardest hit | Medium term (2-4 years) |

| Scarcity of Diameter/HTTP-2 signalling talent | -1.2% | Global, acute in developed markets | Long term (≥ 4 years) |

| Proprietary UDR schema lock-in risk | -0.9% | Global, vendor-dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and sovereignty mandates

The EU Data Act of 2024 compels cloud providers to guarantee data portability by 2027 and bars exit fees, while GDPR 2025 heightens breach-reporting and cross-border transfer hurdles. Operators must therefore redesign architectures so that sensitive subscriber attributes reside inside national borders even as roaming services traverse them, inflating compliance budgets by up to 25%.

Integration complexity with legacy OSS/BSS

Mature operators juggle decades-old BSS platforms lacking open APIs, so modern subscriber data management microservices often need costly adapters and phased migration to avoid service outages. Three UK dropped two legacy core suppliers to consolidate under Ericsson, precisely to tame that complexity. Industry studies show project overruns can hit 60% when integration scope is underestimated, driving a shift toward digital-overlay models like Qvantel’s that let carriers launch greenfield digital brands while slowly porting legacy subsystems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Models Bridge Legacy Gaps

Hybrid implementations carve out a strategic middle ground, pairing on-premises data stores for regulated identifiers with public-cloud analytics that enhance agility. In revenue terms, the segment already commands 18.1% CAGR, exceeding both pure cloud and on-premise trajectories. European multinationals facing fragmented privacy regimes increasingly select hybrid UDM topologies, storing EU citizen data within continental data centers while hosting policy-analytics functions on hyperscale clouds situated closer to user clusters. That design minimizes legal exposure yet delivers the elastic scaling prized by product teams. As hyperscalers roll out sovereign-cloud zones, operators gain further tools to fine-tune residency, propelling hybrid demand through 2031.A second growth engine stems from converged fixed–mobile operators that must harmonize broadband and wireless subscribers across legacy BSS landscapes. Hybrid footprints allow them to migrate broadband user tables at a measured pace while running 5G SA credentials from day one, avoiding big-bang cutovers. The subscriber data management market sees vendors baking automated data-placement policies into their orchestration layers so records dynamically shift between edge and core depending on latency or compliance triggers. This fluid data-plane architecture positions hybrid as the long-term default for tier-1 groups navigating divergent regional statutes.

By Organization Size: SME Adoption Accelerates

Large enterprises still dominate spending thanks to national-scale operators modernizing multi-site cores, but affordability improvements now open advanced data management to SMEs. Cloud-native subscription models turn capex into opex, matching the cash-flow realities of regional MVNOs, utility networks, or campus 5G owners. Start-ups can stand up core functions within weeks, contrasting with the multi-quarter lead times of legacy systems. The subscriber data management market size tied to SMEs is therefore set to multiply as low-code provisioning portals reduce skills barriers.Vendors also curate pre-packaged analytics that pinpoint upsell opportunities for small operators lacking data-science teams. For example, Google-Cloud-based MVNO hubs ingest call-detail records and run churn-prediction models out-of-the-box, letting SMEs target retention campaigns a full quarter sooner than before. As 5G device ecosystems diversify, niche providers serving logistics fleets or smart-grid sensors are expected to expand, cementing SMEs as a high-momentum customer segment.

By Solution Type: Identity Management Surges

Subscriber data repositories remain the backbone—housing profile, location, and policy data across 2G-to-5G eras—but identity-management solutions now post the most explosive growth. Zero-trust frameworks require fine-grained authentication, and 5G’s SUCI mechanism cloaks IMSIs to curb intercept attacks. Enterprises running private 5G for operational technology environments use the identity layer to segregate robotics, camera, and employee traffic, ensuring only authorized devices tap slice-specific resources. Consequently, identity platforms nested inside the subscriber data management market deliver both compliance and monetization upside through premium security add-ons.Advanced identity schemes also underpin seamless roaming between campus networks and macro coverage. Telecom groups now pilot multi-factor identity combining device attestation and behavioral analytics, increasing the attach rate for value-added enterprise services. These capabilities spur a virtuous cycle: richer identities enable differentiated QoS, fueling further spend on subscriber data-centric innovation.

By Network Type: 5G Standalone Momentum Builds

4G LTE remains ubiquitous, but 5G SA uptake is now unmistakable. Malaysia’s Digital National Berhad (DNB) went live with 5G Advanced features in 2025, covering remote surgery and immersive education use cases and confirming that SA cores can host latency-critical workloads at scale. Each of these applications leans heavily on the data layer to map slice policy to user identity within microseconds. The subscriber data management market therefore benefits in lockstep with SA rollouts.Meanwhile, multigenerational support persists: rural sites may stay on 3G for voice fallback, and fiber-to-the-home bundles bring fixed-access data into the same repository. Vendors thus design schemas that tag records with access-type metadata, avoiding duplicated policy logic. The net result is a steadily rising demand curve for unified data stores that knit together heterogeneous access while readying carriers for SA-driven revenue streams.

By End-user: Enterprise IoT Drives Diversification

Enterprises—especially in manufacturing, energy, and logistics—no longer rely solely on public macro networks. Instead, they commission private slices or standalone networks that require dedicated subscriber data layers. Toyota’s US material-handling operations, modernized via an Ericsson private-5G build, achieved smoother forklift routing and live inventory feeds thanks to a deterministic policy tied to each autonomous vehicle. Mobile-network operators still serve the broader consumer base, yet incremental enterprise spending will outpace retail revenue as digital-transformation budgets migrate to operational technology stacks. The subscriber data management market share linked to enterprise/IoT therefore expands faster than any other end-user cohort.MVNOs positioned on vertical niches also play a role: healthcare MVNOs promise HIPAA-grade identity assurance, while logistics MVNOs treat fleet telematics as priority traffic. Each variant leans on granular subscriber data constructs, broadening total addressable demand beyond traditional telco boundaries.

Geography Analysis

North America’s 35.30% slice of 2025 revenue reflects deep private-5G penetration across manufacturing and warehousing, plus strict sovereign-data rules that amplify demand for on-shore repositories. Verizon’s USD 20 billion fiber acquisition spree and AT&T’s fixed-wireless push exemplify the region’s infrastructure appetite, forcing cores and UDRs to scale for converged access types. Canadian carriers show similar momentum, aligning with federal road maps that require critical-infrastructure traffic to stay within national borders.

Asia-Pacific posts the highest regional CAGR at 18.2%. China’s 800-million-plus 5G user base delivers unmatched scale, and operators there plan vast IoT overlays across ports and industrial parks that hinge on robust subscriber data management market capabilities. India follows with spectrum liberalization that lets factories secure private-network licenses, spurring SME-friendly core packages. South-Korea and Japan continue to pioneer 28 GHz campus networks, each bundling AI-fueled policy analytics to assure VR/AR performance.

Europe balances solid uptake with complex compliance overhead. The GDPR 2025 revision and national prepaid-SIM identity laws, such as Norway’s, place immediate localization pressures on multi-country groups. Carriers respond by piloting sovereign-cloud clusters and encrypt-in-use techniques within the subscriber data management market to meet both performance and legal thresholds. EU funding for very-high-capacity networks adds investment firepower, though rollout tempos depend on how quickly converged operators reconcile fiber, cable, and mobile subscriber schemas into a single UDR.

Competitive Landscape

The market sits in a mid-consolidated state: three global heavyweights, Ericsson, Nokia, and Huawei, wield more than 60,000 patents each and have collectively poured over USD 100 billion into core-network R&D. Ericsson’s dual-mode UDM anchors Three UK’s record-sized packet core and underpins Vodafone Spain’s consumer SA launch. Nokia’s cloud-native CoreSuite emphasizes open API breadth, while Huawei leverages integrated radio-to-core portfolios in markets where geopolitical constraints are lighter.

Disruptors zero in on cloud delivery and AI. Oracle joined with Enea to certify a 5G subscriber-data stack on Oracle Cloud Infrastructure, positioning telcos to consume data functions as managed services. Google Cloud’s alliance with Ericsson created a pay-per-use 5G Core-as-a-Service that bundles automated life-cycle management for UDR/UDM. Start-ups such as Comviva and Netcracker package AI workbenches and broadband experience suites that link real-time customer metrics to dynamic policy shifts.

Strategically, vendors differentiate on three fronts: 1) breadth of multi-access data convergence, 2) AI embedded in policy decisions and 3) ease of legacy integration. Those excelling on all three capture the lion’s share of new SA-core awards. Patent filings around AI-based fraud detection indicate a second competitive horizon focused on privacy-preserving analytics.

Subscriber Data Management Industry Leaders

Telefonaktiebolaget LM Ericsson

Nokia Corporation

Huawei Technologies Co. Ltd.

Hewlett Packard Enterprise Co.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ericsson and Google Cloud introduced Ericsson On-Demand, a SaaS 5G core that brings elastic scaling and pay-per-use pricing to network functions.

- May 2025: Charter Communications agreed to acquire Cox Communications for USD 34.5 billion, forming a 37.6-million-subscriber cable–telecom giant.

- March 2025: Vodafone Spain selected Ericsson’s standalone 5G core for consumer services under a four-year contract.

- February 2025: Bharti Airtel partnered with Ericsson to deploy signaling, charging and policy assets for its nationwide SA network.

- February 2025: DNB Malaysia and Ericsson activated 5G Advanced features across 12 industries, boosting lower-latency use cases.

- January 2025: Three UK chose Ericsson to build Europe’s largest mobile packet core at 9 Tbps.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the subscriber data management (SDM) market as all software platforms and related services that let telecom operators store, consolidate, and monetize real-time subscriber identities, policy rules, device data, and location information across 2G, 3G, 4G/LTE, fixed, and 5G standalone cores.

Scope Exclusions: We deliberately exclude general master data management, standalone HLR/HSS hardware swaps, and non-telecom customer data platforms.

Segmentation Overview

- By Deployment Mode

- Cloud

- On-Premise

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Solution Type

- Subscriber Data Repository

- Policy Management

- Identity Management

- Location and Device Information

- By Network Type

- 2G/3G

- 4G/LTE

- 5G Stand-Alone

- Fixed/Wireline

- By End-user

- Mobile Network Operators (MNOs)

- Mobile Virtual Network Operators (MVNOs)

- Enterprises/IoT Service Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts conduct semi-structured calls and pulse surveys with mobile network engineering heads, vendor product managers, and regional network-core integrators across North America, Europe, Asia-Pacific, and the Middle East.

These conversations validate traffic growth rates, average selling prices for cloud-native SDM licenses, and migration timelines that secondary data only hints at.

Desk Research

We start with public domain sources such as the International Telecommunication Union, GSMA, 3GPP filings, regional telecom regulators, and leading operator annual reports. We then fold in industry association briefs on 5G subscriptions and IoT SIM activations.

Broader technology adoption cues are gathered from IMF macro tables, OECD broadband statistics, and patent citation trends covering cloud-native network functions.

Proprietary libraries, including D&B Hoovers for operator financials and Dow Jones Factiva for M&A cues, give our analysts additional depth.

This list is illustrative; many more documents are reviewed to frame assumptions.

Market-Sizing & Forecasting

A top-down build begins with active subscriber counts by network generation and region, which are then multiplied by modeled SDM spend per subscriber that we refine through primary price checks.

Results are cross-checked with a selective bottom-up roll-up of vendor revenues and channel checks to spot variance.

Key variables fed into our multivariate regression forecast include 5G subscription additions, IoT SIM growth, virtualized core penetration, average revenue per user, and policy-control transaction density.

Gap pockets where vendor disclosures are thin are bridged with calibrated proxies and trend smoothing before final aggregation.

Data Validation & Update Cycle

Outputs pass through anomaly scans, senior-analyst peer review, and client-side sanity checks.

Our team refreshes every twelve months and reopens the model whenever regulatory, technology, or currency shifts materially change underlying drivers.

Why Mordor's Subscriber Data Management Numbers Inspire Confidence

Published SDM values frequently diverge because each publisher selects different solution mixes, price benchmarks, and update cadences. Our disciplined scope and annual refresh ensure figures move with real-world network evolution.

Key gap drivers include whether enterprise IoT cores are counted, which price tiers are averaged, currency translation dates, and how aggressively 5G uptake is projected. By anchoring to validated operator traffic and spend ratios, Mordor avoids inflated base cases or overly conservative trajectories.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.54 B (2025) | Mordor Intelligence | - |

| USD 7.21 B (2024) | Regional Consultancy A | Counts only mobile network SDM and omits cloud-native license premiums |

| USD 9.06 B (2025) | Global Consultancy A | Uses higher per-subscriber spend drawn from tier-one operator budgets and applies a static FX rate |

| USD 6.36 B (2023) | Global Consultancy B | Bases model on legacy on-premise deployments and forecasts with linear growth, ignoring 5G step-ups |

Taken together, the comparison shows that when scope breadth, price realism, and timely refresh are aligned, as in Mordor's approach, decision-makers receive a balanced, transparent baseline they can confidently reference.

Key Questions Answered in the Report

What is the current value of the subscriber data management market?

The market stands at USD 9.94 billion in 2026 and is set to reach USD 21.17 billion by 2031.

Which region grows the fastest for subscriber data management solutions?

Asia-Pacific leads with an 18.2% CAGR through 2031 driven by China’s vast 5G footprint and India’s enterprise 5G initiatives.

Why are hybrid deployments gaining traction?

They let operators satisfy strict data-residency rules by keeping sensitive records on-premise while using public-cloud elasticity for analytics, balancing compliance and cost.

How do AI capabilities influence subscriber data management?

AI enables real-time policy tweaks, predictive congestion control and fraud detection, improving user experience and operational efficiency.

What are the primary challenges facing operators adopting modern subscriber data management?

Tightening data-sovereignty mandates raise compliance costs, and integrating cloud-native platforms with legacy OSS/BSS often leads to project delays and budget overruns.

Who are the major players in the subscriber data management market?

Ericsson, Nokia and Huawei dominate globally, while Oracle, Enea and cloud-native start-ups provide competitive alternatives focused on SaaS delivery and AI-enhanced analytics.

Page last updated on: