Styrenic Block Copolymers (SBCs) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 3.29 Million tons |

| Market Volume (2031) | 3.99 Million tons |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

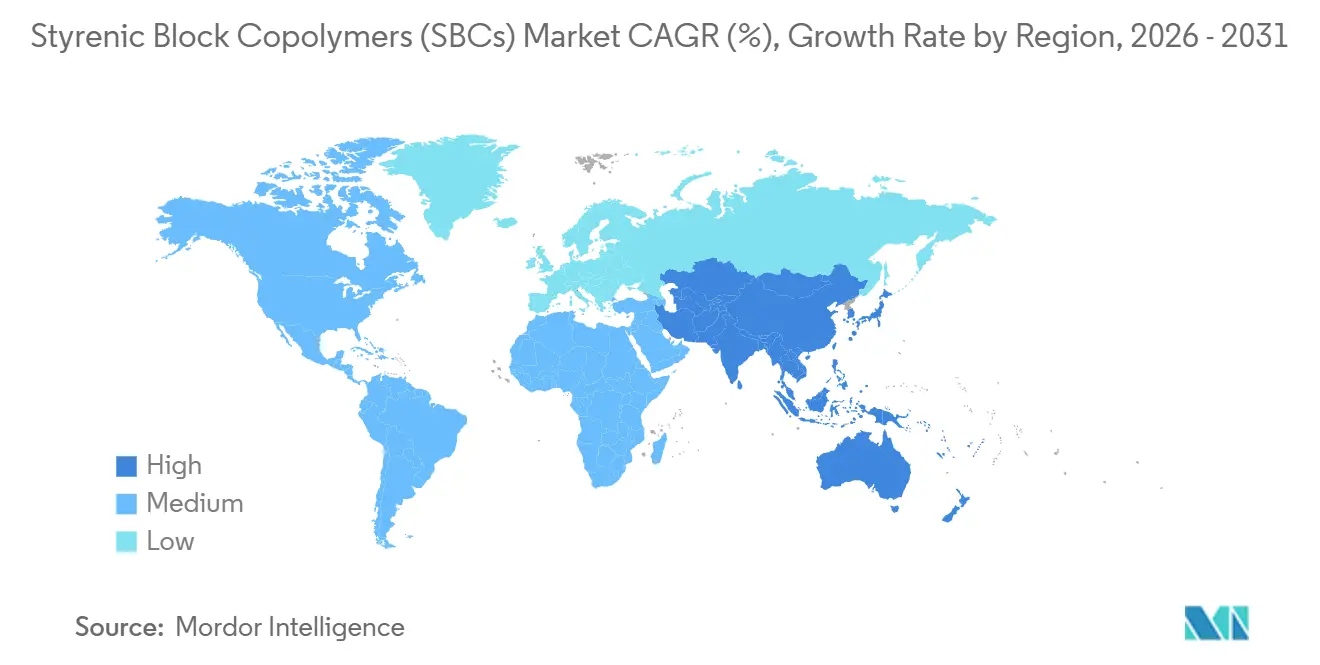

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

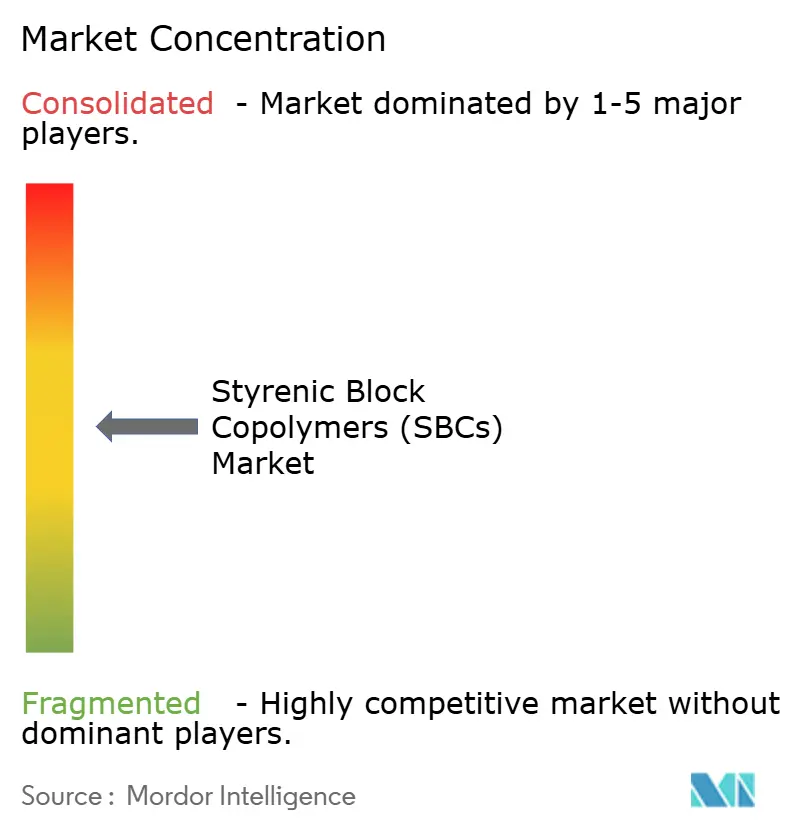

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Styrenic Block Copolymers (SBCs) Market Analysis by Mordor Intelligence

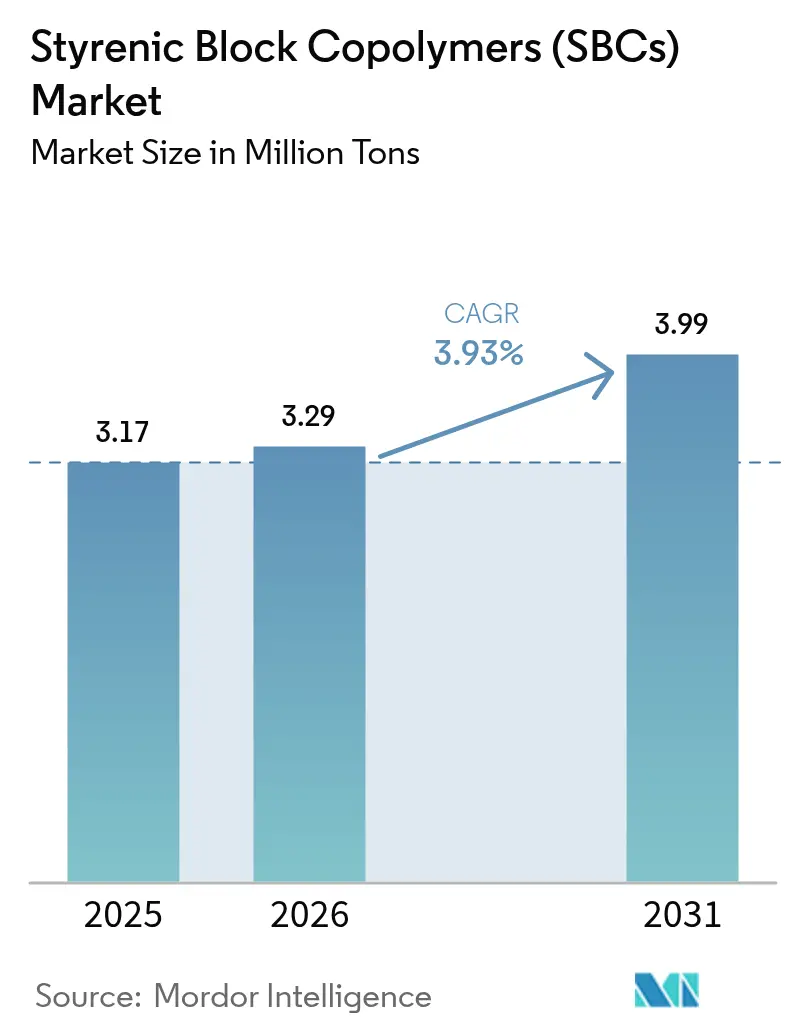

The Styrenic Block Copolymers Market size is expected to grow from 3.17 Million tons in 2025 to 3.29 Million tons in 2026 and is forecast to reach 3.99 Million tons by 2031 at 3.93% CAGR over 2026-2031. Sustained road and rail expansion in Asia-Pacific, regulatory mandates for recycled asphalt in the European Union and United States, and rising use of hydrogenated grades in adhesives anchor long-term demand. Feedstock price swings tied to crude benchmarks squeeze margins for producers without captive styrene or butadiene but also encourage backward integration and supply-chain partnerships. Electric-vehicle makers are piloting sulfonated SBC films for next-generation capacitors, signalling future specialty applications that could offset packaging share losses to polyolefin elastomers. Patent expiries on legacy hydrogenated products have unlocked lower-cost Asian capacity, intensifying price competition yet widening end-market access for formulators.

Key Report Takeaways

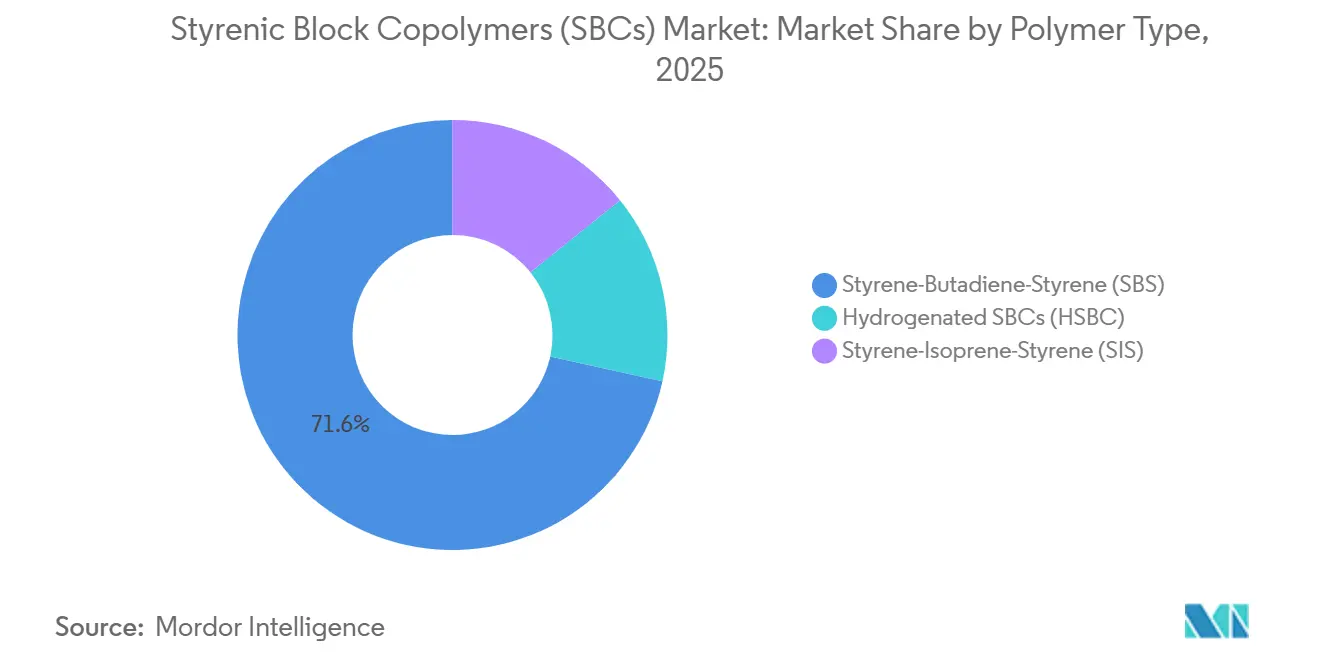

- By polymer type, styrene-butadiene-styrene (SBS) led with 71.55% of the styrenic block copolymers market share in 2025, while hydrogenated SBCs (HSBC) registered the highest projected CAGR at 4.47% through 2031.

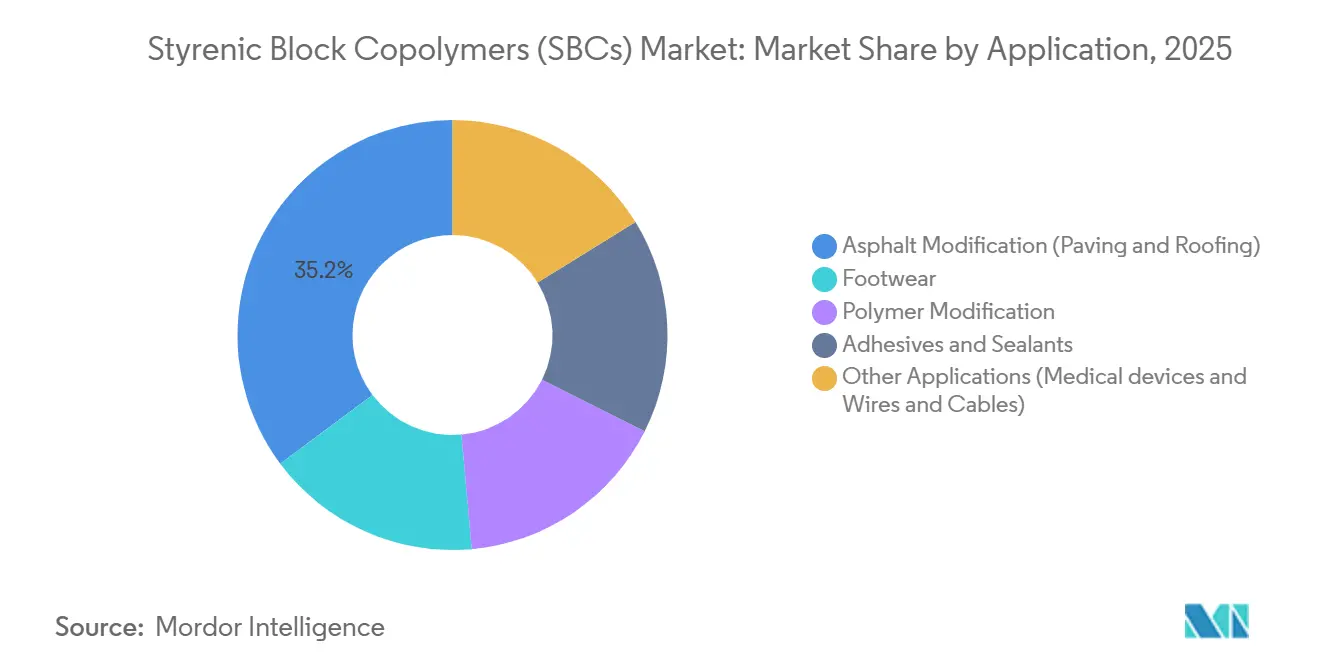

- By application, asphalt modification (paving and roofing) captured 35.22% of the styrenic block copolymers market size in 2025 and is advancing at a 4.15% CAGR through 2031.

- By geography, Asia-Pacific accounted for 57.71% of of the styrenic block copolymers market share in 2025 and is set to expand at the fastest regional CAGR of 4.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Styrenic Block Copolymers (SBCs) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asphalt-Recycling Mandates in European Union and United States | +1.2% | North America NS EU | Medium term (2-4 years) |

| Asia-Pacific Infrastructure Boom (Expressways, Waterproofing) | +1.5% | APAC core, spill-over to Middle-East and Africa | Long term (≥ 4 years) |

| Pandemic-Driven Rise in Single-Use Hygiene Films | +0.4% | Global | Short term (≤ 2 years) |

| Patent Expiry of Kraton's HSBC Grades Unlocking New Entrants | +0.6% | Global, with early gains in China and India | Medium term (2-4 years) |

| Sulfonated SBCs for Next-Gen EV Capacitors | +0.3% | APAC and North America EV hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Asphalt-Recycling Mandates in European Union and United States

Road agencies in the European Union and United States are required to raise reclaimed asphalt pavement content, and many specify polymer modifiers to restore binder elasticity. SBS improves rutting resistance and cracking tolerance in RAP-rich mixes, which extends pavement life by up to one-third according to 2024 field studies. Procurement is shifting toward performance-based specifications that favor suppliers with validated field data, driving consistent demand through 2028. States such as California and Texas already mandate SBS-modified binders for interstate work, advancing medium-term volume growth. This regulation underpins a steady baseline for the styrenic block copolymers market even when new road construction slows.

Asia-Pacific Infrastructure Boom (Expressways, Waterproofing)

China approved more than 8,000 kilometers of new expressways in 2025 and specifies polymer-modified asphalt for heavy-traffic corridors[1]National Development and Reform Commission, “Expressway Expansion Approvals,” ndrc.gov.cn . India’s National Infrastructure Pipeline allocates USD 1.4 trillion to transport projects through 2030, with 40% directed to roads that increasingly stipulate SBS binders. Tunnel and bridge waterproofing also draw demand because SBS membranes remain flexible under monsoon conditions, supporting elevated growth beyond highways. Southeast Asian countries are following a similar pattern as logistics corridors expand. The sustained project pipeline drives the highest regional growth contribution to the styrenic block copolymers market over the forecast horizon.

Pandemic-Driven Rise in Single-Use Hygiene Films

During the COVID-19 period, consumption of SBC-based soft films for masks and medical drapes rose sharply, and 2025 levels remain higher than pre-2020 due to entrenched hygiene preferences. SIS delivers skin-contact comfort and breathability, while SEBS is specified for catheter tubing that requires biocompatibility. Aging demographics in developed markets continue to support premium disposable products, maintaining a structural uplift in demand. Although stockpiles stabilize, ongoing healthcare spending underwrites a durable base for hygienic film grades within the styrenic block copolymers market.

Patent Expiry of Kraton’s HSBC Grades Unlocking New Entrants

The 2023-2024 lapse of key hydrogenated patents removed licensing hurdles, allowing Asian producers to launch SEBS and SEPS at prices 15-20% below incumbents. LG Chem and Sinopec quickly commercialized new lines, prompting a price rebalancing that widens adoption in adhesives and medical devices. Incumbents respond by accelerating functionalized derivatives that bond to polar substrates and by deepening technical support. The competitive reset is most evident in Asia-Pacific yet gradually spreads to global supply chains, enlarging the accessible pool for the styrenic block copolymers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of Crude-Linked Styrene and Butadiene Feedstocks | -0.8% | Global | Short term (≤ 2 years) |

| Asphalt-Free Cold-Mix Road Technologies | -0.3% | North America and EU temperate zones | Medium term (2-4 years) |

| POE/POP Elastomers Replacing SBCs in Packaging | -0.5% | Global, with concentration in flexible packaging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility of Crude-Linked Styrene and Butadiene Feedstocks

Styrene prices jumped 35% and butadiene 28% in early 2025 after outages at Gulf Coast crackers, reducing non-integrated producer margins by up to 300 basis points[2]U.S. Energy Information Administration, “Styrene and Butadiene Price Trends,” eia.gov . Integrated majors absorbed shocks more readily due to captive monomer supply. Smaller firms in Europe and North America lacked pricing leverage and implemented temporary surcharges or curtailed spot sales. This short-term volatility discourages discretionary expansion and prompts contractual feedstock hedging. The exposure underscores the importance of vertical integration for cost resilience in the styrenic block copolymers market.

Asphalt-Free Cold-Mix Road Technologies

Cold-mix asphalt that cures at ambient temperature avoids polymer additives and reduces paving costs by up to 30% for low-traffic surfaces. Pilot projects in the Netherlands and selected U.S. municipalities confirm adequate performance for bike lanes and rural roads. Durability still falls short for interstate highways, which limits the addressable substitution. The technology nonetheless chips away at demand in niche segments within temperate zones, creating a moderate headwind for SBS volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Hydrogenation Drives Premium Shift

Styrene-Butadiene-Styrene (SBS) dominated the 2025 volume with 71.55%, reflecting its cost-effective performance in paving, roofing, and footwear. Hydrogenated SBCs (HSBC) are expanding fastest at a 4.47% CAGR through 2031, supported by their UV resistance and thermal stability in adhesives and medical devices. The styrenic block copolymers market size for hydrogenated grades is projected to accelerate as Asian producers narrow the pricing differential and as new catalyst systems cut hydrogenation energy use. Regional feedstock profiles influence the mix because butadiene availability favors SBS, while isoprene supports SIS facilities. Regulatory compliance under REACH and TSCA further shapes product portfolios by slowing the entry of unregistered chemistries.

HSBC gains traction in wire and cable jackets that require ozone resistance and low-temperature flexibility. SIS maintains a niche in hot-melt adhesives for hygiene products due to superior tack, yet is limited by yellowing under UV light. The gradual shift toward hydrogenated grades exemplifies a premiumization trend that can cushion average selling prices within the styrenic block copolymers market, even as commodity applications remain volume-heavy.

By Application: Asphalt Modification Anchors Growth

Asphalt modification (paving and roving) accounted for 35.22% of 2025 volume and is growing at a 4.15% CAGR through 2031. Polymer-modified binders prolong pavement life by improving viscoelastic balance, which supports rising adoption across Asia-Pacific expressways and North American resurfacing programs. Roofing membranes extend the same performance logic to building envelopes, especially in hurricane-prone regions.

Footwear exploits SBC elasticity and abrasion resistance in midsoles and outsoles, with athletic brands driving color-customized compounds. Adhesives and sealants are migrating from SIS toward HSBC for higher heat resistance amid e-commerce logistics. Polymer modification in engineering plastics delivers impact strength but competes with cheaper styrene-ethylene copolymers, tempering its growth. Specialty niches such as medical devices and capacitor films provide margin upside and diversify the application portfolio of the styrenic block copolymers market.

Geography Analysis

Asia-Pacific contributed 57.71% of global volume in 2025 and will grow at a 4.32% CAGR through 2031, outstripping every other region. Expressway construction in China and India, waterproofing demand in Southeast Asian mass-transit projects, and the clustering of footwear and electronics manufacturing all reinforce sustained consumption. Local producers benefit from proximity to butadiene feedstock and supportive industrial policies that encourage capacity additions. Government infrastructure budgets create a predictable baseline that keeps the styrenic block copolymers market in the region on a strong upward trajectory.

In North America, federal infrastructure funding, combined with state-level recycled asphalt mandates, underpins steady SBS demand for highway resurfacing. Adhesive and sealant grades also gain from the rapid growth of e-commerce packaging. Integrated producers with Gulf Coast feedstock access hold a structural cost edge, which helps sustain investment despite mature road networks.

In Europe, EU Circular Economy Action Plan lifts polymer-modified binder usage in RAP-rich mixes, yet flat new-road construction keeps absolute growth subdued. Strict REACH compliance raises barriers for new entrants, protecting incumbent suppliers but also slowing innovation. Packaging applications face substitution from polyolefin elastomers, which trims growth potential for SBCs in that segment. Nevertheless, roofing membranes and specialty adhesives maintain a stable demand core within the regional styrenic block copolymers market.

South America and the Middle-East and Africa combined held a lower global volume. Brazil’s toll-road concessions, Saudi Arabia’s airport expansions, and Nigeria’s urban roads all specify SBS-modified asphalt to combat extreme climate stresses. These regions remain sensitive to public-finance cycles but offer long-term upside as life-cycle cost considerations gain traction in procurement.

Competitive Landscape

The top five producers, such as Kraton, LG Chem, Sinopec, TSRC, and Dynasol Group, control about 48% of global capacity. This moderate concentration enables pricing discipline in specialty grades yet still allows regional challengers to scale. Patent expiries on hydrogenated products enable Chinese and Korean firms to launch SEBS and SEPS lines at lower costs, compelling incumbents to differentiate through technical service and accelerated innovation. Vertical integration into styrene and butadiene delivers a margin hedge during feedstock spikes, and companies without that integration increasingly form supply alliances or pursue upstream acquisitions.

Process advances such as continuous polymerization cut batch variability and energy consumption, which appeals to medical and adhesive customers that demand tight molecular-weight control. Initiatives like Kuraray’s solvent-free SEBS route reduce volatile organic compound emissions and align with tightening environmental regulations. Strategic investments concentrate in Asia-Pacific, where demand grows fastest, but firms also pursue joint ventures near key customers, such as INEOS’s stake in a Malaysian compounder to strengthen service in Southeast Asia. Specialty product development, including sulfonated and bio-based SBC grades, opens new revenue streams and fortifies intellectual-property positions that can sustain premiums within the styrenic block copolymers market.

Styrenic Block Copolymers (SBCs) Industry Leaders

Dynasol Group

Kraton Corporation

LG Chem

Sinopec

TSRC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Kraton Corporation announced that it had ceased the production of hydrogenated styrenic block copolymers (HSBCs) at its plant in Berre, France. The company continued producing unhydrogenated SBCs at the same facility.

- February 2025: Kraton Corporation and Formosa Petrochemical obtained ISCC PLUS certification for their Hydrogenated SBCs (HSBC) Joint Venture plant in Mailiao, Taiwan. This certification enabled the production of SBCs with up to 70% certified renewable content.

Global Styrenic Block Copolymers (SBCs) Market Report Scope

Styrenic block copolymers (SBCs) are a class of thermoplastic elastomers that process like plastic and behave like rubber, mainly due to the physical crosslink inherent in the SBC structure. When the SBC material is stretched, those crosslinks bring it back to its original shape. SBCs can be made from raw materials such as butadiene, styrene, and isoprene. They have a two-phase structure composed of hard polystyrene end blocks and soft rubber mid-locks. SBCs are used in asphalt modification, rigid thermoplastic impact modification, and the production of soft plastic elastomer.

The styrenic block copolymers market is segmented by polymer type, application, and geography. By polymer type, the market is segmented into styrene-butadiene-styrene (SBS), styrene-isoprene-styrene (SIS), and hydrogenated SBCs (HSBC). By application, the market is segmented into asphalt modification (paving and roofing), footwear, polymer modification, adhesives and sealants, and other applications (medical devices, wires, and cables). The report also covers the market size and forecasts for the styrenic block copolymers (SBCs) in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Styrene-Butadiene-Styrene (SBS) |

| Styrene-Isoprene-Styrene (SIS) |

| Hydrogenated SBCs (HSBC) |

| Asphalt Modification (Paving and Roofing) |

| Footwear |

| Polymer Modification |

| Adhesives and Sealants |

| Other Applications (Medical devices and Wires and Cables) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Polymer Type | Styrene-Butadiene-Styrene (SBS) | |

| Styrene-Isoprene-Styrene (SIS) | ||

| Hydrogenated SBCs (HSBC) | ||

| By Application | Asphalt Modification (Paving and Roofing) | |

| Footwear | ||

| Polymer Modification | ||

| Adhesives and Sealants | ||

| Other Applications (Medical devices and Wires and Cables) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Turkey | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the styrenic block copolymers market?

The styrenic block copolymers market stands at 3.29 million tons in 2026 and is forecast to reach 3.99 million tons by 2031.

Which region contributes most to styrenic block copolymer market demand in 2025?

Asia-Pacific accounted for 57.71% of the styrenic block copolymer market demand in 2025.

Why are hydrogenated SBCs gaining momentum through 2031?

Hydrogenated SBCs (HSBC) provide superior UV stability and thermal resistance, and recent patent expiries have lowered their cost, enabling faster adoption in adhesives and medical devices.

How do asphalt recycling mandates influence SBC usage?

Regulations requiring higher reclaimed asphalt content raise demand for SBS modifiers that restore binder performance, supporting medium term growth in North America and the European Union.

Page last updated on: