Stock Clamshell Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

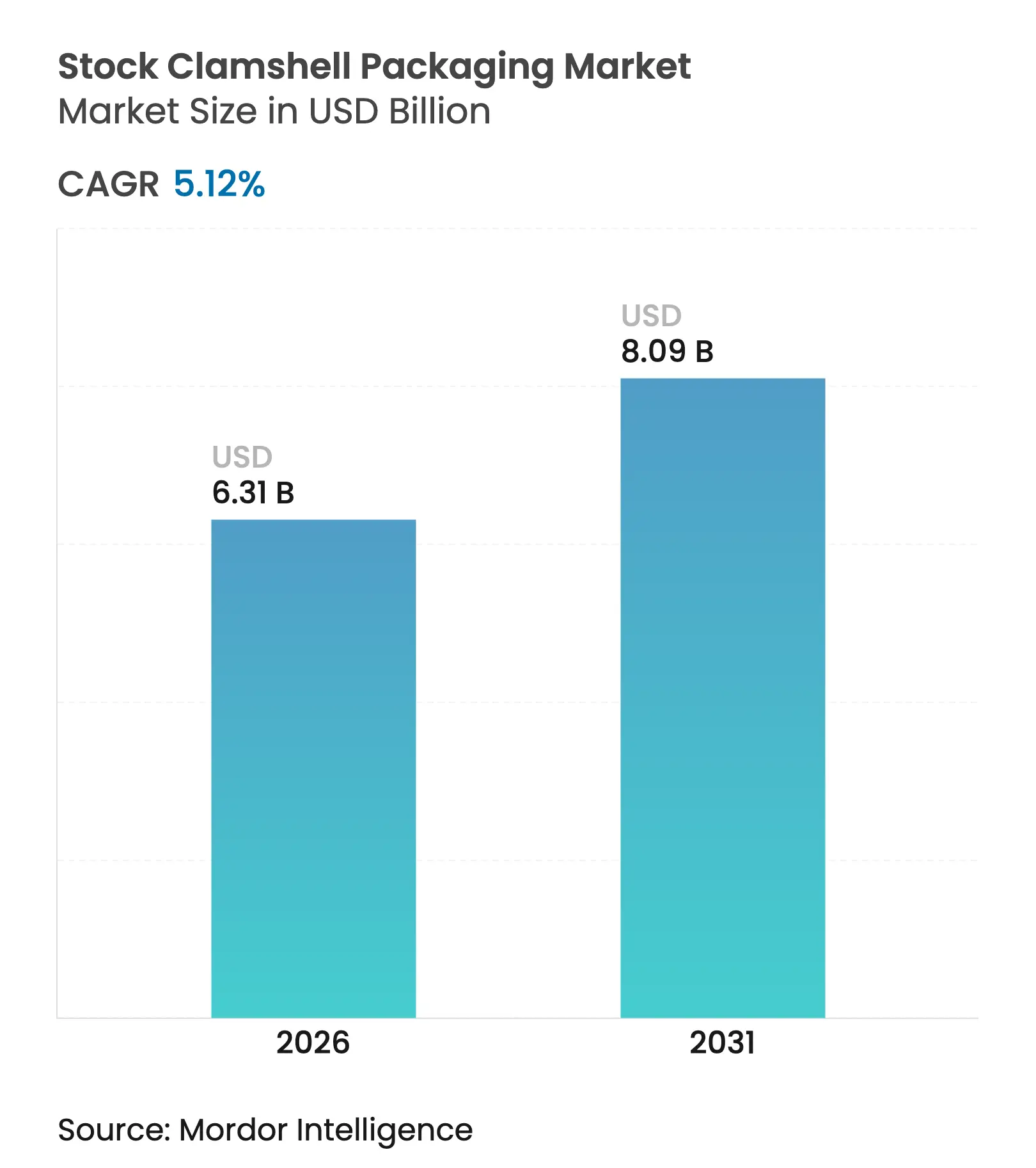

| Market Size (2026) | USD 6.31 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 5.12 % CAGR |

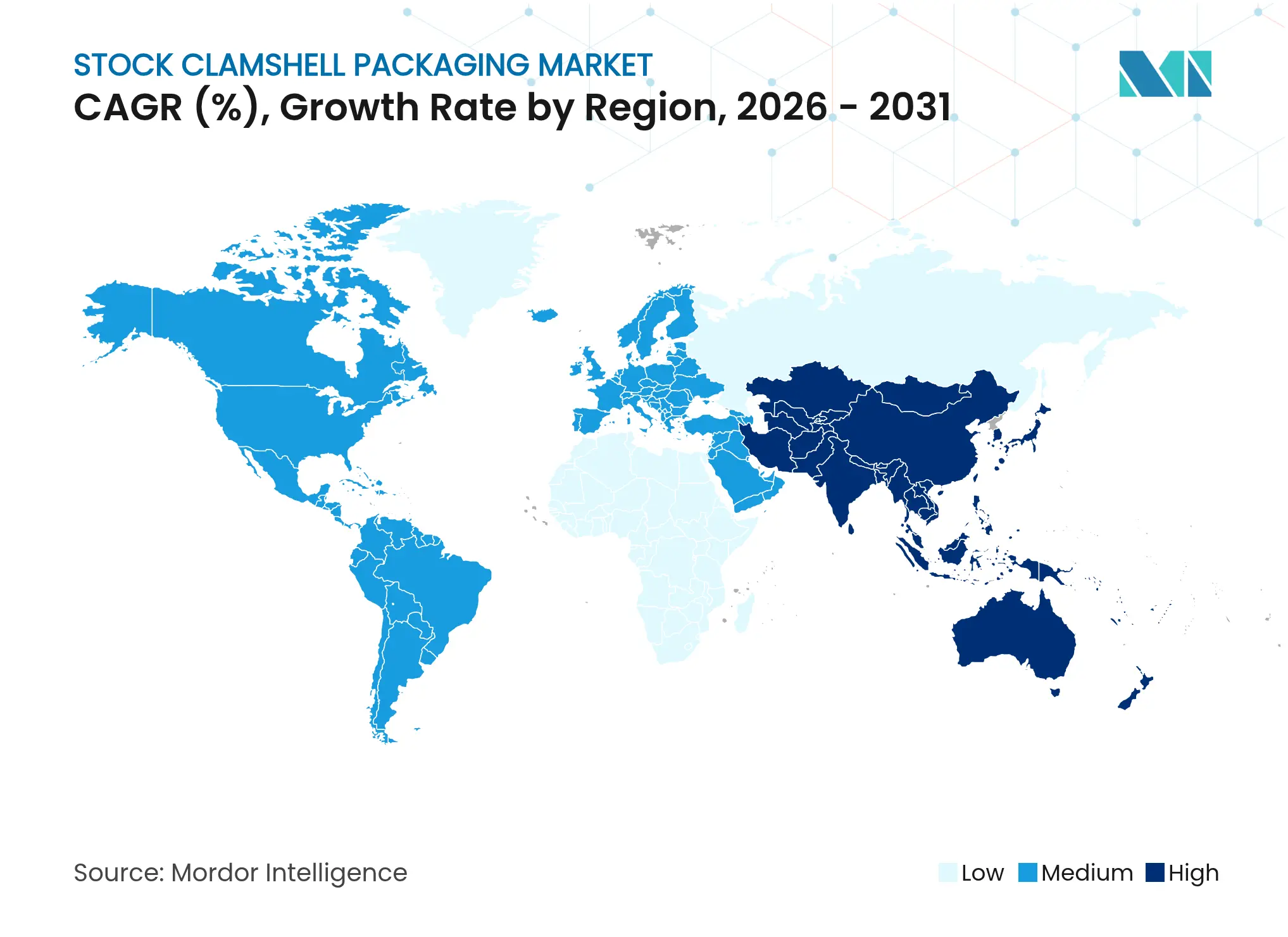

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Stock Clamshell Packaging Market Analysis by Mordor Intelligence

The stock clamshell packaging market size is expected to grow from USD 6.00 billion in 2025 to USD 6.31 billion in 2026 and is forecast to reach USD 8.09 billion by 2031 at 5.12% CAGR over 2026-2031. Sustained demand links to omnichannel grocery proliferation, municipal bans on expanded polystyrene, and commercial investments in clarified-polypropylene grades that trim resin weight by 20%. Retailers use shelf-ready, stackable formats to compress SKU counts while preserving product visibility, a shift that underpins tooling upgrades at leading thermoformers. Brand owners tighten recycled-content commitments in response to Extended Producer Responsibility laws, which in turn heighten interest in mono-material PET clamshells designed for closed-loop recycling streams. Material cost volatility remains a watchpoint as polypropylene spot prices added 9¢/lb across January–February 2025, stressing converters that lack hedging programs.

Key Report Takeaways

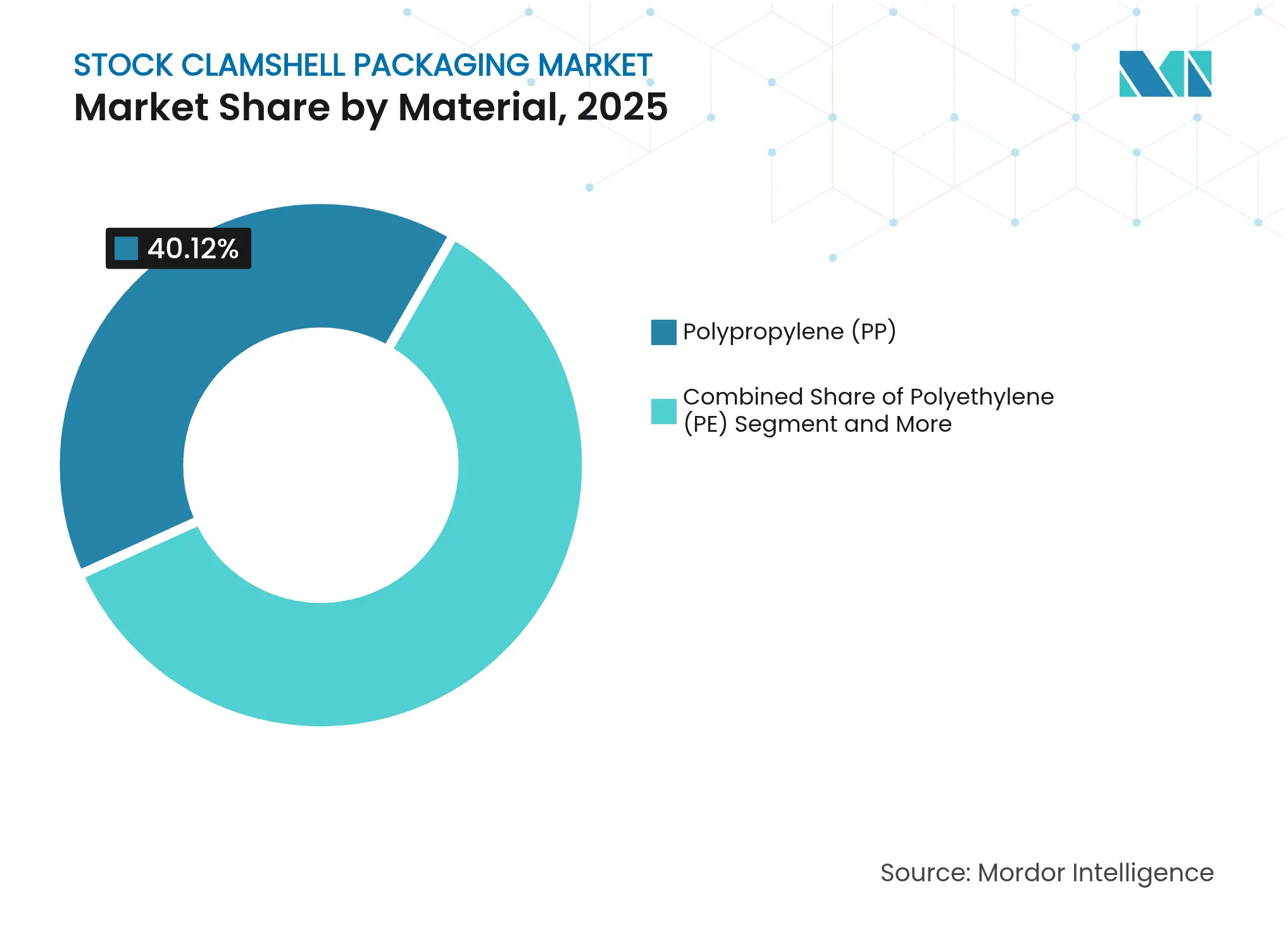

- By material, polypropylene led with 40.12% revenue share in 2025; bioplastics are poised to post the fastest 9.31% CAGR through 2031.

- By application, food packaging held 45.05% of the stock clamshell packaging market size in 2025, whereas medical devices are projected to expand at an 7.86% CAGR to 2031.

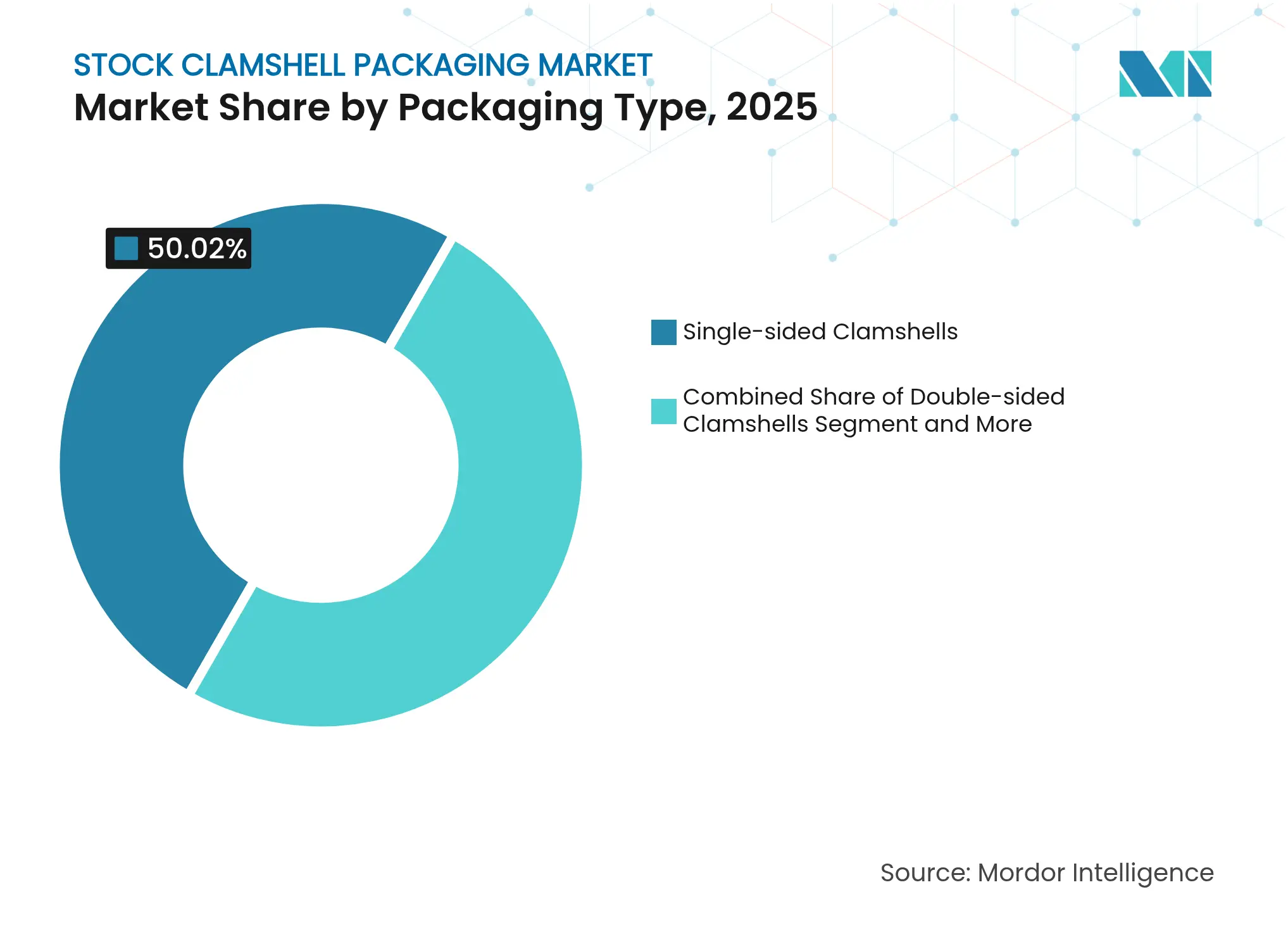

- By packaging type, single-sided clamshells captured 50.02% of stock clamshell packaging market share in 2025, yet tri-fold designs register the highest 7.12% CAGR during the outlook period.

- By distribution channel, direct sales controlled 59.65% of 2025 revenue; indirect channels record a 6.08% CAGR through 2031.

- By geography, North America commanded 38.10% sales in 2025, while Asia-Pacific accelerates at an 7.74% CAGR attributable to urbanization and capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stock Clamshell Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge

in omnichannel grocery and fresh-meal-kit delivery+

Surge

in omnichannel grocery and fresh-meal-kit delivery+

| +1.2% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:Global,

with concentration in North America and Europe |

Impact Timeline

:

Short

term (≤ 2 years)

|

Municipal

EPS bans accelerate molded-fiber clamshell uptake

Municipal

EPS bans accelerate molded-fiber clamshell uptake

| +0.9% | North America and Australia, expanding to EU | Medium term (2-4 years) | |||

Clarified-PP

grades cut resin weight ≈ 20%

Clarified-PP

grades cut resin weight ≈ 20%

| +0.7% | Global manufacturing hubs | Medium term (2-4 years) | |||

Retailer

"single-SKU" shelf-optimization favors stackable formats

Retailer

"single-SKU" shelf-optimization favors stackable formats

| +0.5% | North America and Europe retail chains | Short term (≤ 2 years) | |||

Wide-web

digital printing enables short-run rPET clamshells

Wide-web

digital printing enables short-run rPET clamshells

| +0.4% | North America and Europe | Medium term (2-4 years) | |||

EU

EPR rules drive refillable cartridge innovations

EU

EPR rules drive refillable cartridge innovations

| +0.4% | EU primary, North America secondary | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in omnichannel grocery and fresh-meal-kit delivery

Rapid growth of click-and-collect and last-mile delivery services reshapes packaging formats, pushing the stock clamshell packaging market toward designs that survive multiple handling points without losing clarity or seal integrity. Meal-kit operators standardize footprints to fit ice-packed shippers and expect tamper evidence compliant with evolving Food Contact Notification rules set by the FDA.[1]U.S. Food and Drug Administration, “Decisions for Food-Contact Notifications,” fda.govLightweight clarified-PP and rPET solutions reduce dimensional weight fees applied by parcel carriers, lowering total landed cost for subscription services that ship weekly. Disruptive demand has encouraged thermoformers to add in-line barrier-coating lines and to certify new materials for direct-food contact inside 12-month development windows, accelerating innovation cycles across North America and Western Europe.

Municipal EPS bans accelerate molded-fiber clamshell uptake

Local prohibitions on expanded polystyrene, exemplified by Los Angeles and South Australia bans effective in 2024 , abruptly eliminate legacy foam formats and trigger substitution toward molded fiber. Fiber suppliers race to scale capacity, installing dry-molded technology that consumes 80% less water and lifts throughput by 50% compared with wet pulp systems . Foodservice chains roll out marketing that highlights compostability certification to recapture customer goodwill lost to single-use plastic concerns. These bans bolster regional production of bagasse-based clamshells in Texas and Queensland, tightening domestic fiber pulp supply and pushing prices up to 18% in 2025.

Clarified-PP grades cut resin weight 20%

Milliken nucleating agents embedded in new PP formulations shorten the crystallization cycle and permit down-gauging without losing impact strength.[2]Milliken, “IRPC Debuts Milliken-Enhanced UL-Validated PP Resin Portfolio,” milliken.com Converters report 10% lower energy draw at the press and 7% faster cycle times, directly improving plant productivity. The lower specific gravity converts into freight savings of 4–6% on long-haul distribution lanes. Adoption is fastest in Asia, where OEM electronics makers specify glass-clear PP to replace brittle PS for earbuds and wearables. Supply agreements include price-escalator clauses linked to Dated Brent to hedge upstream propylene volatility, reflecting maturing risk management practices within the stock clamshell packaging market.

EPR laws incentivize mono-material PET clamshells

The European Union Packaging and Packaging Waste Regulation enforces a 30% recycled-content threshold in PET food packaging by 2030 europarl.. Fee modulation within Extended Producer Responsibility schemes punishes multi-layer blends, making single-polymer rPET clamshells the lowest-cost compliance path over a ten-year horizon. California echoes this direction with 50% post-consumer recycled content by 2030.[3]Circular Blog, “Plastic Legislative Landscape: EPR Schemes in the United States,” circular.coSupply chain visibility improves as sortation facilities add optical recognition upgrades financed through EPR pools, which lifts recovery rates and secures feedstock for bottle-to-clamshell loops. Brands highlight closed-loop attributes on-pack to fulfill ESG disclosures demanded by institutional investors.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Virgin-resin

price volatility

Virgin-resin

price volatility

| -0.8% | Global, acute in Asia-Pacific | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.8%

|

Geographic Relevance

:

Global,

acute in Asia-Pacific

|

Impact Timeline

:

Short

term (≤ 2 years)

|

High

PET-clamshell curb-side contamination rates

High

PET-clamshell curb-side contamination rates

| -0.6% | North America and Europe | Medium term (2-4 years) | |||

Brand

shift to flexible pouches

Brand

shift to flexible pouches

| -0.5% | Global, led by North America and Europe | Medium term (2-4 years) | |||

Tooling

limits for fiber-based clamshells

Tooling

limits for fiber-based clamshells

| -0.3% | Global manufacturing centers | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Virgin-resin price volatility

Polypropylene and PET contract prices swing quickly on feedstock disruptions linked to refinery turnarounds and geopolitical events, straining profit margins for converters locked into quarterly supply agreements. Smaller thermoformers cannot offset hikes through hedging or index-based pass-throughs and therefore risk order losses when bids expire. Some buyers lengthen resin call-off windows to 60 days, but credit teams resist larger working-capital exposure, creating friction across the stock clamshell packaging market.

High PET-clamshell curb-side contamination rate

Municipal MRFs struggle to capture thin-gauge clamshells that flatten and mis-sort with paper, and residual salad dressing or produce stickers degrade bale purity. FDA requirements for recycled content in direct-food contact impose higher decontamination costs, leading reclaimers to downgrade flows to fiber markets rather than closed-loop resin. Brands confront a gap between recyclability claims and actual recovery outcomes, inviting scrutiny from regulators and NGOs and dampening growth in PET formats.

Segment Analysis

By Material: Bioplastics Surge Despite PP Dominance

Polypropylene held the largest stake at 40.12% in 2025, reflecting its balanced price-performance profile and global availability. That share anchors economies of scale that secure supply continuity for produce, bakery, and general merchandise. The stock clamshell packaging market size for polypropylene applications is projected to advance at 4.38% annually amid resin light-weighting gains. Bioplastics, led by PLA and PHAs, accelerate at a 9.31% CAGR underpinned by regulatory incentives and corporate carbon commitments. Luminy PLA grades rated to 95 °C broaden entry into hot-fill deli and ready-meal lines, converting demand that once defaulted to clarified PP.

Market demand for renewable polymers deepens as retailers add front-of-pack carbon labels and publicize compostability certificates. FDA review cycles for novel biopolymer additives lengthen development lead times but ultimately validate safety for direct contact, which encourages premium price positioning. Supply expansion from US Midwest corn-to-PLA projects promises 150 kilotons new output by 2027, easing historical price premiums. With mechanical properties quickly approaching those of PP, bioplastics secure brand mandates for 100% renewable packaging across select personal-care lines, lifting volumes beyond foodservice. Continued innovations in antimicrobial PLA/PCL blends with 5% tannic acid further strengthen the case for high-value medical and food applications.

Note: Segment shares of all individual segments available upon report purchase

By Application: Medical Devices Outpace Food Growth

Food packaging generated 45.05% of 2025 revenue as transparent clamshells remain indispensable for strawberries, pastries, and snack trays sold in self-service retail environments. The segment grows at a steady 3.88% through 2031, supported by produce export volumes and fresh-cut convenience SKUs. In contrast, the medical segment registers an 7.86% CAGR, reflecting hospital investments in single-use sterile kits and point-of-care diagnostic devices that require protective plastics. The stock clamshell packaging market share for medical applications is buoyed by unit-dose delivery formats that improve surgical room efficiency and reduce cross-contamination.

Packaging validations for gamma and EO sterilization dictate PETG and HIPS selections with higher melt strength and chemical resistance, raising average selling prices by 27% versus food grades. Contract device assemblers favor snap-fit designs showcased by Dordan Manufacturing, which eliminates heat-seal steps and compresses pack-out takt times. Regulatory audits under ISO 13485 push suppliers to implement full traceability and calibrated inspection equipment, creating barriers for commodity players and reinforcing premium margins in the stock clamshell packaging industry.

By Packaging Type: Tri-fold Innovation Drives Growth

Single-sided clamshells dominated with 50.02% of 2025 shipments, sustaining large-run efficiencies for berries, cupcakes, and club-store multipacks. Nevertheless, tri-fold formats expand at 7.12% because they unlock 360-degree merchandising with built-in hang hooks for versatile planogram placement. Early adopter categories include supplements and premium hair accessories where brand storytelling relies on uninterrupted product visibility. The stock clamshell packaging market size for tri-fold formats is forecast to reach USD 2.09 billion by 2031, supported by digital printing systems that personalize graphics without labels.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Direct Sales Dominance Persists

Direct OEM relationships account for 59.65% of 2025 shipments as national retailers and global CPGs prefer specification control, dedicated customer service, and vendor-managed inventory. These clients sign multi-year agreements that lock in capacity and require joint R&D to meet upcoming EPR targets. The stock clamshell packaging market benefits from collaborative forecasting that smooths demand peaks and secures supply resilience during resin disruptions. Direct channels are also primary conduits for custom medical trays that mandate clean-room production and device-specific tooling investment.

Indirect distribution, though smaller, exhibits a 6.08% CAGR driven by regional produce growers and small appliance brands seeking standard sizes without capital-intensive tooling. Wholesalers broaden value propositions by offering graphic design, drop-ship capabilities, and post-consumer recycled content certification services. Online B2B platforms introduce programmatic quoting that matches buyers with surplus stock, monetizing idle inventory for converters and accelerating lead times for small-lot orders. These innovations push the stock clamshell packaging market toward greater transparency in price discovery and capacity utilization

Geography Analysis

North America captured 38.10% of 2025 revenue as mature grocery infrastructure, established curb-side recycling programs, and early adoption of recycled-content mandates underpin steady demand. Canadian provinces align recycling targets with US EPR laws, creating a harmonized regulatory corridor that favors cross-border supply contracts. Producers in Ohio and Ontario run integrated PET bottle-to-clamshell loops, supplying closed-loop rPET that commands a 9% premium. Retail meal-kit penetration surpasses 34% of households in 2025, sustaining above-market growth for tamper-evident clamshells suited to chilled distribution.

Europe posts mid-single-digit growth on the back of the Packaging and Packaging Waste Regulation that requires all packaging to be recyclable by 2028. Converters upgrade sortation compatibility by switching to detectable inks and mono-material hinges. The stock clamshell packaging market in Germany and France benefits from supermarket private-label investments in rPET packaging that advertises 100% bottle-grade recycled content. Eastern European plants supply surplus capacity to Western markets, leveraging lower energy tariffs from renewable projects to offset resin cost spikes.

Asia-Pacific represents the fastest rising arena, advancing at an 7.74% CAGR through 2031. Rapid urbanization, e-commerce expansion, and government campaigns against informal packaging push demand for standardized thermoformed solutions. India’s packaging sector, comprised of over 22,000 MSME firms, scales output to meet domestic food safety reforms and export standards. Chinese manufacturers double down on clarified-PP and rPET lines routed to domestic consumer electronics, while joint ventures in Vietnam and Indonesia target ASEAN agricultural exporters. Government incentives in South Korea subsidize investments in PCR testing and food-grade decontamination units, reinforcing circularity ambitions across the stock clamshell packaging market.

Competitive Landscape

Market Concentration

The stock clamshell packaging market displays moderate fragmentation. The top five suppliers account for an estimated 46% of global sales, relying on vertical integration from resin compounding through downstream printing. Competitive advantage comes from tooling depth, proprietary material blends, and service models that bundle design consultation with logistics analytics. Sustainability positioning has become a differentiator, with leading players publishing audited Scope 3 emissions and signing science-based targets to reassure brand owners.

Consolidation reshaped the field in 2024 and 2025. Novolex absorbed Pactiv Evergreen for USD 6.7 billion, uniting 250 brands and 39,000 SKUs under a common technical platform. Amcor merged with Berry Global, targeting USD 650 million synergies from procurement, footprint optimization, and unified new product pipelines that accelerate barrier innovations. These scale plays intensify bargaining leverage over resin suppliers and enable multi-regional supply commitments that de-risk customers’ just-in-time networks.

Innovation rivalry centers on lightweighting and mono-material barrier structures. Patent volumes in clarified-polypropylene resins and enzymatic PET recycling climbed 14% year over year. Pilot plants in the United States process depolymerized PET into recycled monomer that re-enters bottle-to-bottle and clamshell-to-clamshell loops, promising impurity removal thresholds suited for food contact. Fast-cycle thermoforming presses with robotic trim-in-place stackers raise labor productivity by 28%, a key differentiator as developed markets confront talent shortages and wage inflation. Regional challengers focus on niche biomedical and high-temperature applications where service intimacy can offset scale disadvantages in the wider stock clamshell packaging industry.

Stock Clamshell Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its merger with Berry Global, creating a USD 24 billion packaging leader focused on sustainable and healthcare solutions.

- April 2025: Novolex finalized its USD 6.7 billion acquisition of Pactiv Evergreen, integrating 250 brands across food, beverage, and specialty segments.

- March 2025: The European Commission enacted Regulation (EU) 2025/351 outlining stricter purity thresholds for plastic food contact materials, with compliance due by Sep 2026.

- February 2025: The EU Packaging and Packaging Waste Regulation entered force, mandating 30% recycled content in PET food packaging by 2030.

Table of Contents for Stock Clamshell Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surge in omnichannel grocery and fresh-meal-kit delivery

- 4.2.2Municipal EPS bans accelerate molded-fiber clamshell uptake

- 4.2.3Clarified-PP grades cut resin weight ? 20 %

- 4.2.4Retailer single-SKU shelf-optimization favors stackable formats

- 4.2.5Wide-web digital printing enables short-run rPET clamshells

- 4.2.6EPR laws incentivize mono-material PET clamshells

- 4.3Market Restraints

- 4.3.1Virgin-resin price volatility

- 4.3.2High PET-clamshell curb-side contamination rates

- 4.3.3Brand shift to flexible pouches

- 4.3.4Tooling limits for fiber-based clamshells

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Sustainability and Recycling Landscape

- 4.8Porter's Five Forces Analysis

- 4.8.1Bargaining Power of Suppliers

- 4.8.2Bargaining Power of Buyers

- 4.8.3Threat of New Entrants

- 4.8.4Threat of Substitute Products

- 4.8.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material

- 5.1.1Polypropylene (PP)

- 5.1.2Polyethylene (PE)

- 5.1.3Polyethylene Terephthalate (PET)

- 5.1.4Bioplastics

- 5.1.5Others Material

- 5.2By Application

- 5.2.1Food

- 5.2.2Pharmaceuticals

- 5.2.3Medical Devices

- 5.2.4Industrial Goods

- 5.2.5Consumer Goods

- 5.2.6Other Applications

- 5.3By Packaging Type

- 5.3.1Single-sided Clamshells

- 5.3.2Double-sided Clamshells

- 5.3.3Tri-fold Clamshells

- 5.3.4Clam Trays

- 5.3.5Other Packaging Type

- 5.4By Distribution Channel

- 5.4.1Direct Sales

- 5.4.2Indirect Sales

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Russia

- 5.5.2.7Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia and New Zealand

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1Middle East

- 5.5.4.1.1United Arab Emirates

- 5.5.4.1.2Saudi Arabia

- 5.5.4.1.3Turkey

- 5.5.4.1.4Rest of Middle East

- 5.5.4.2Africa

- 5.5.4.2.1South Africa

- 5.5.4.2.2Nigeria

- 5.5.4.2.3Egypt

- 5.5.4.2.4Rest of Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Visipak Inc.

- 6.4.2Placon Corporation

- 6.4.3Dordan Manufacturing Co.

- 6.4.4Rhysley Ltd.

- 6.4.5Novolex Holdings

- 6.4.6Abhinav Enterprises

- 6.4.7Andex Industries

- 6.4.8Plastech Group

- 6.4.9Amcor plc

- 6.4.10Pactiv Evergreen

- 6.4.11Sonoco Products Co.

- 6.4.12Sinclair & Rush (StockClam)

- 6.4.13Lacerta Group

- 6.4.14Fabri-Kal Corp.

- 6.4.15WestRock Co.

- 6.4.16Dart Container Corp.

- 6.4.17Transparent Container

- 6.4.18Display Pack Inc.

- 6.4.19Clamshells, Inc.

- 6.5Heat Map Analysis

- 6.6Competitor Analysis Emerging vs. Established Players

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Global Stock Clamshell Packaging Market Report Scope

Clamshell packaging consists of a single container divided into two halves, connected by a hinge. Commonly utilized for fresh produce, baked goods, retail items, and shipping trays, clamshell packaging boasts a 100% recyclability rate. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The stock clamshell packaging market is segmented by material type (Polypropylene (PP), Polyethylene (PE), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC) and Other Material Types), by application (Food, Pharmaceuticals, Medical Devices, Industrial Goods, Consumer Goods and Other Applications) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.