Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

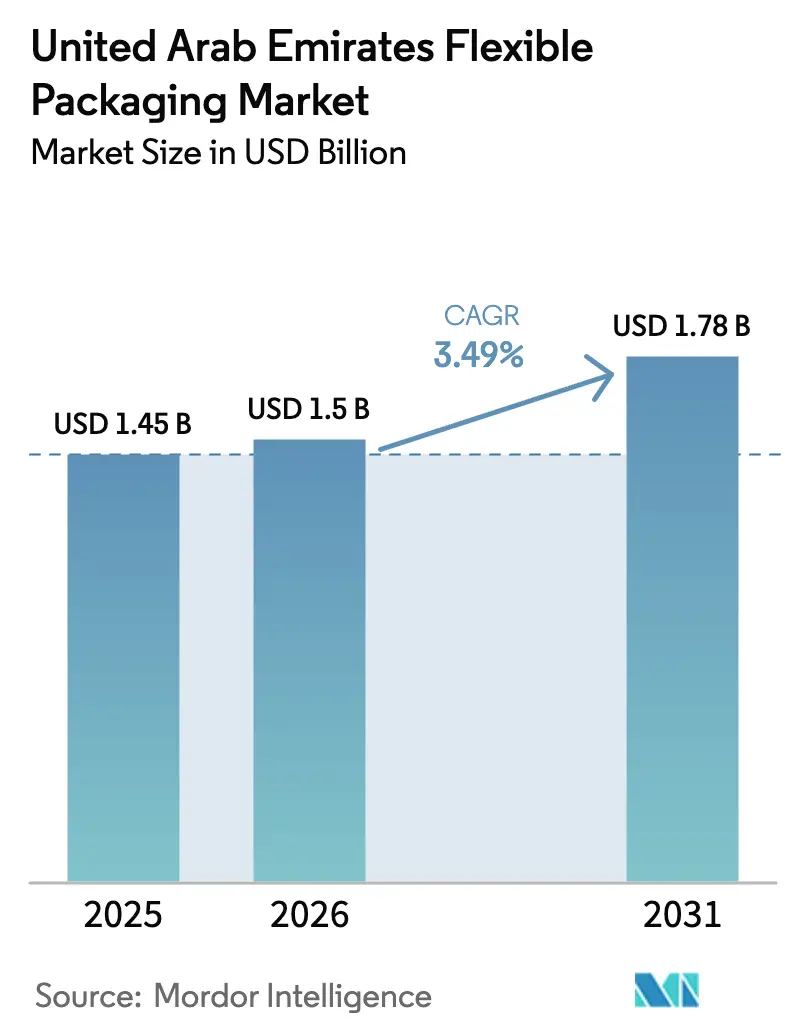

| Base Year Market Size (2025) | USD 1.45 Billion |

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 3.49% CAGR |

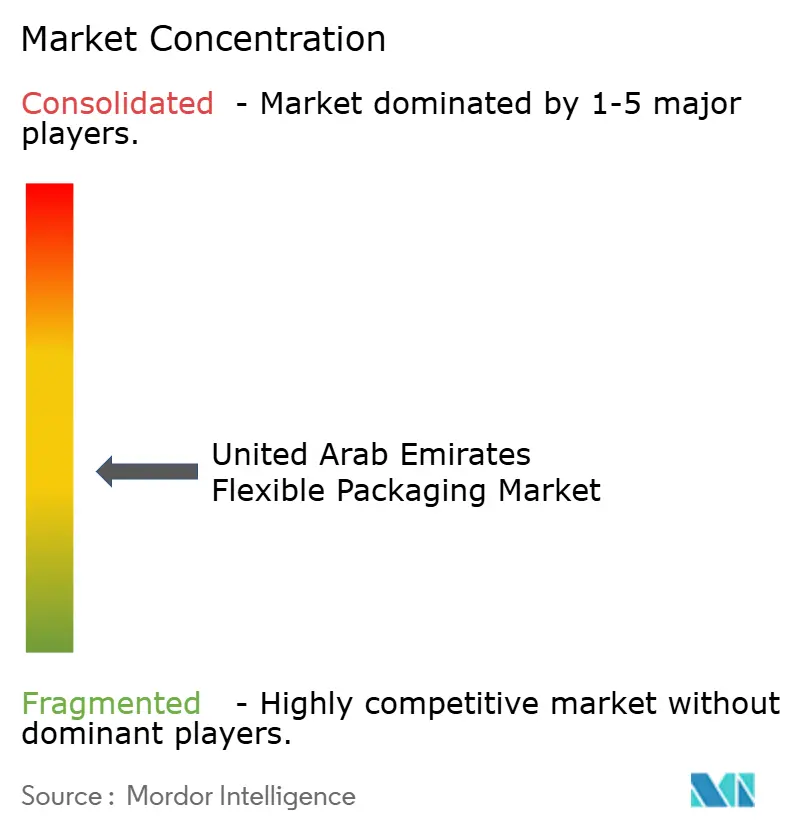

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Flexible Packaging Market Analysis by Mordor Intelligence

The United Arab Emirates flexible packaging market size was valued at USD 1.45 billion in 2025 and estimated to grow from USD 1.5 billion in 2026 to reach USD 1.78 billion by 2031, at a CAGR of 3.49% during the forecast period (2026-2031). Current expansion is shaped by mandatory recyclability rules, e-commerce growth, and halal-certified food exports that push converters toward mono-material and high-barrier structures. Material innovation offsets modest volume gains as cloud kitchens, on-demand grocery services, and retail densification favor lightweight pouches, sachets, and films that lower logistics costs while meeting strict performance requirements. The United Arab Emirates flexible packaging market also benefits from investments in domestic recycling capacity, such as the Tetra Pak–Union Paper Mills carton line that supports circular-economy targets. Supply-chain resilience has become a competitive lever; regional suppliers with diversified polymer sourcing widened their customer base during the 2024 Red Sea disruptions. Continuous regulatory alignment with the Circular Economy Policy 2071 reinforces the shift toward bio-based and fully recyclable formats, keeping price realization healthy despite input-cost volatility.

Key Report Takeaways

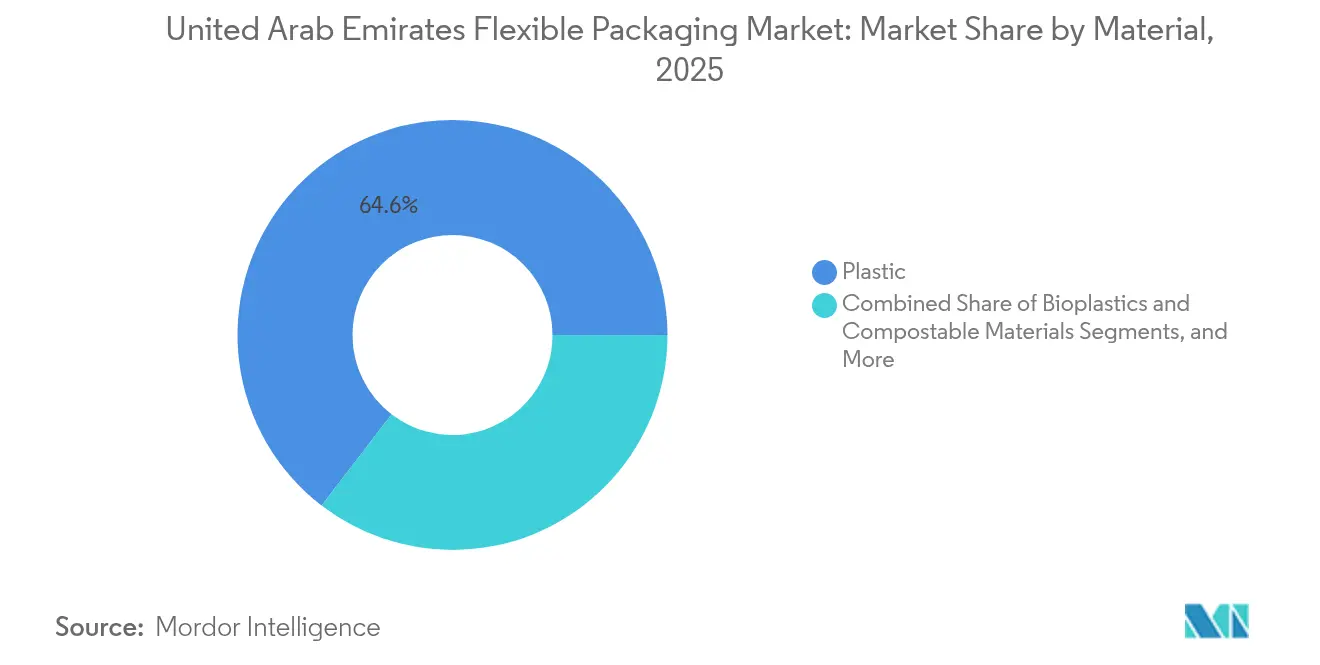

- By material, plastic formats led with 64.58% of the United Arab Emirates flexible packaging market share in 2025, while bioplastics and compostable materials are projected to grow at a 5.02% CAGR through 2031.

- By product type, bags and pouches commanded 44.62% revenue share in 2025; sachets and stick packs are forecast to record a 4.69% CAGR to 2031.

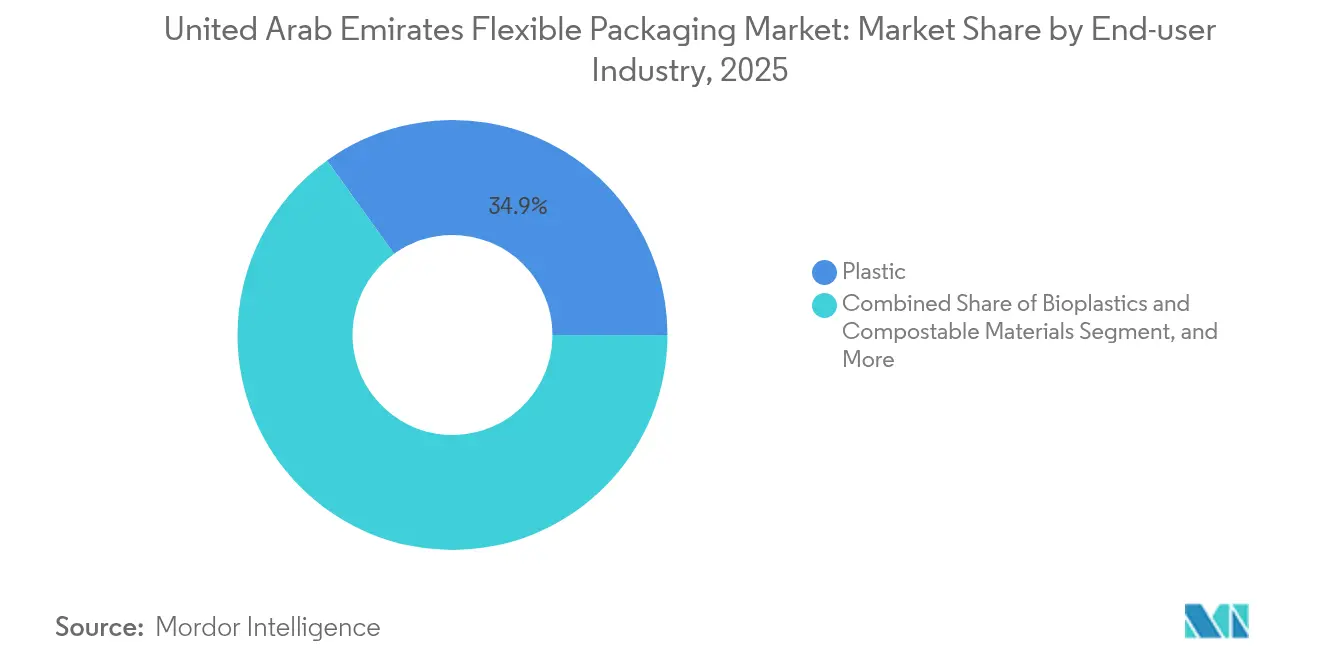

- By end-user industry, the food segment accounted for 34.92% share of the United Arab Emirates flexible packaging market size in 2025, whereas personal care and cosmetics are advancing at a 4.52% CAGR through 2031.

- By printing technology, flexography held 43.77% share in 2025, and digital printing shows the highest projected CAGR at 4.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and on-demand grocery logistics | +0.8% | Nationwide, concentrated in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Mandatory recyclability targets under Circular Economy Policy 2071 | +0.6% | Nationwide with federal enforcement | Medium term (2–4 years) |

| Surge in halal-certified F&B exports from free-zones | +0.5% | Dubai, Abu Dhabi, Sharjah free-zones | Medium term (2–4 years) |

| Rapid growth of cloud-kitchen ecosystem | +0.4% | Dubai and Abu Dhabi metro areas | Short term (≤ 2 years) |

| Dubai 2040 retail densification | +0.3% | Dubai, spillover to Northern Emirates | Long term (≥ 4 years) |

| Cold-chain meal-kit start-ups | +0.2% | Urban centers nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

E-commerce Boom and On-Demand Grocery Logistics

Last-mile delivery models flourishing in Dubai and Abu Dhabi rely on lightweight, tamper-evident pouches that reduce transport costs while protecting goods during multiple handling cycles. [1]Dubai Municipality, “Dubai 2040 Urban Master Plan,” dm.gov.ae Retail densification under the Dubai 2040 Urban Master Plan limits storage space, so brands shift to space-saving flexible packs that stack efficiently and showcase larger printable areas for required product data. Operators of cloud kitchens report 23% logistics cost savings after switching from rigid containers to high-barrier pouches, accelerating adoption across personal-care and OTC pharmaceutical lines. The United Arab Emirates Consumer Protection Law amendments, effective 2024, mandate clearer on-pack information, further favoring formats with expansive surface areas. Collectively, these factors sustain value growth in the United Arab Emirates flexible packaging market despite modest volume upticks.

Mandatory Recyclability Targets Under Circular Economy Policy 2071

Federal Law No. 12 of 2018 on Integrated Waste Management obliges producers to finance collection and recycling, driving investment in mono-material structures that meet 100% recyclability thresholds. [2]UAE Ministry of Climate Change and Environment, “Federal Law No. 12 of 2018 on Integrated Waste Management,” moccae.gov.ae Large converters leverage technical labs to redesign multi-layer laminates into single-polymer films with comparable barrier performance. Tetra Pak’s USD 0.68 million carton-recycling line with Union Paper Mills exemplifies supply-chain localization that closes material loops and supports premium pricing for certified recyclable packs. Early adopters report 15–20% export price premiums, particularly for halal-labelled foods targeting Europe, underscoring how regulation translates into market opportunity within the United Arab Emirates flexible packaging market.

Surge in Halal-Certified F&B Exports from Free-Zones

The Emirates Authority for Standardization and Metrology requires National Halal Mark labeling, catalyzing demand for high-barrier laminates that guarantee product integrity over longer shipping routes. [3]Emirates Authority for Standardization and Metrology, “National Halal Mark,” esma.gov.ae Export-oriented processors in Jebel Ali and Khalifa Industrial Zone specify multi-layer pouches with advanced oxygen and moisture barriers that command 25-30% higher unit prices than domestic equivalents. Flexible packs simplify line cleaning, limit cross-contamination risk, and enable digital traceability codes essential for halal audits, further embedding premium solutions into the United Arab Emirates flexible packaging market.

Rapid Growth of Cloud-Kitchen Ecosystem

Kitchen-as-a-service operators tripled site counts between 2024 and 2025, demanding grease-proof, heat-stable pouches that maintain food quality across temperature zones. Specialized polyethylene-based laminates with anti-fog properties outperform rigid clamshells by cutting food waste 18% during delivery windows. Small-format sachets for sauces and spices are gaining popularity as portion-control becomes integral to meal-kit economics. These operational dynamics add steady volume to the United Arab Emirates flexible packaging market and push converters toward rapid product-development cycles supported by digital printing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental and recycling concerns | –0.4% | Nationwide, consumer-driven | Medium term (2–4 years) |

| Volatile polymer resin pricing | –0.6% | Nationwide, all manufacturers | Short term (≤ 2 years) |

| Import-dependent raw-material supply chain | –0.3% | Nationwide, Red Sea disruption | Short term (≤ 2 years) |

| Scarcity of local PCR resin for food-grade films | –0.2% | Nationwide, compliance pressure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental and Recycling Concerns

Heightened consumer scrutiny over plastic waste prompts retailers to delist packs without clear recycling pathways, pressuring legacy multi-layer pouches that lack end-of-life solutions. Federal bans on certain single-use plastics advance in phases to 2026, obliging brands to shift toward certified recyclable or bio-sourced alternatives. Large FMCG groups publish supplier scorecards that link contract renewals to progress on post-consumer recycled content, compelling converters to accelerate material substitution programs. Limited curbside collection capacity, however, complicates consumer participation, exposing a gap between regulation and infrastructure that tempers near-term growth prospects for the United Arab Emirates' flexible packaging market.

Volatile Polymer Resin Pricing

Quarterly swings of up to 40% in polypropylene and polyethylene prices during 2024-2025, triggered by shipping constraints through the Red Sea corridor, eroded converter margins and delayed expansion projects. While vertically integrated groups such as Taghleef Industries mitigated shocks via multi-origin feedstock contracts, smaller players absorbed cost spikes that could not be fully passed downstream. Capital allocation toward new sustainable lines paused, moderating capacity additions and slowing innovation cycles that underpin long-run gains in the United Arab Emirates flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Regulatory Pressure Catalyzes Sustainable Alternatives

Plastic substrates accounted for 64.58% of United Arab Emirates flexible packaging market share in 2025, underscoring their entrenched performance and cost profile. However, the segment pivots toward mono-polyethylene and mono-polypropylene systems that meet cradle-to-cradle requirements at large retailers. Bioplastics and compostables, while only a fraction of current volumes, are projected to post a 5.02% CAGR, supported by incentives for certified compostable shopping bags and rising consumer willingness to pay premiums for low-carbon packs.

Sustainability mandates spur converters to co-develop bio-based high-barrier coatings with material suppliers. Taghleef Industries pilots metallocene-PE structures that deliver oxygen transmission rates below 0.3 cc/m²/day while remaining fully recyclable through existing PE streams. Such advances position polymer players to defend value even as paper and hybrid substrates nibble at low-barrier niches. Investment momentum indicates plastics will maintain lead share, yet diversification into certified compostables will incrementally broaden the United Arab Emirates flexible packaging market size.

By Product Type: Convenience Formats Dominate Portfolio Strategy

Bags and pouches secured 44.62% share of the United Arab Emirates flexible packaging market size in 2025, driven by their versatility across F&B staples, snacks, and pet food. Stand-up designs offer billboard-style graphics and reseal closures that fit e-commerce shelf-ready needs. Sachets and stick packs, though smaller in tonnage, are expected to grow 4.69% CAGR as meal-kit, nutraceutical, and cosmetic sampling models proliferate.

Regional converter Hotpack Global earmarked USD 95.3 million to build biodegradable pouch capacity, confirming the segment’s profitability trajectory. Films and wraps continue serving institutional foodservice but lose share to value-added pouch formats integrating laser-scored easy-open features. The product shift supports premium unit economics and underlines why convenience orientation will steer incremental gains in the United Arab Emirates flexible packaging market.

By End-User Industry: Food Retains Core Demand Amid Personal-Care Upswing

Food processors represented 34.92% of United Arab Emirates flexible packaging market share in 2025. Halal certification prerequisites sustain demand for high-integrity laminates across meat, confectionery, and ready-to-eat meal categories. At the same time, luxury and masstige cosmetic brands relocating filling lines to Sharjah Free Zone stimulate packaging innovation around metallized stand-up pouches and refill sachets, propelling personal care to a 4.52% CAGR outlook.

Healthcare and pharma contribute niche but high-margin demand for sterile barrier formats that satisfy GCC-wide regulatory standards. Beverage growth plateaus as returnable glass and aluminum can recovery programs gain government backing. Overall, diversified sector exposure insulates the United Arab Emirates flexible packaging market from single-segment volatility while enabling higher-value mixes.

By Printing Technology: Digital Adoption Accelerates Customization Trend

Flexography held 43.77% revenue share in 2025 thanks to cost advantages in long runs of snack food and powdered beverage films. Yet digital presses are forecast to expand at 4.91% CAGR as converters chase SKU proliferation and seasonal promotions that demand low minimum-order quantities and variable data. Early adopters deploy water-based inkjet units with food-safe chemistries, enabling real-time personalization campaigns for cross-border e-commerce clients.

Taghleef Industries’ high-gloss label films engineered for UV-inkjet compatibility illustrate material innovation aligning with printing-tech shifts. Rotogravure remains relevant for top-tier coffee and pet-food applications where photo-realistic imagery justifies cylinder investments, but new installations are rare. This digital transition reinforces agility as a critical success factor in the United Arab Emirates flexible packaging market.

Geography Analysis

Dubai and Abu Dhabi anchor demand, benefiting from free-zone clustering of food processors, personal-care fillers, and large converters that together generate the majority of transactional volume. Dubai’s retail densification strategy intensifies per-square-meter sales targets, prompting a pivot toward shelf-efficient flexible packs that sustain high turnover. Abu Dhabi’s industrial diversification funds support backward integration into masterbatch and specialty-film production, strengthening regional supply resilience.

Sharjah and Ras Al Khaimah contribute as manufacturing satellites, offering cost-effective land and labor for second-tier converters targeting GCC exports. The strategic location of Jebel Ali Port facilitates the swift re-export of packed goods to Africa and South Asia, embedding the United Arab Emirates' flexible packaging market within broader trade lanes. Nevertheless, heavy reliance on maritime routes exposes operators to freight volatility, as evidenced during the 2024 Red Sea detours that inflated transit times and polymer costs.

Government sustainability initiatives apply uniformly across emirates, but the implementation pace varies, leading to localized opportunities. Dubai pilots smart-bin collection programs that may boost feedstock for food-grade PCR, whereas Northern Emirates emphasize mechanical recycling partnerships with cement kilns for refuse-derived fuel. Together, these geographic nuances require converters to adopt multi-site production footprints and nuanced regulatory strategies to secure share gains in the United Arab Emirates flexible packaging market.

Competitive Landscape

The market remains moderately fragmented. Global players such as Huhtamaki Flexible Packaging Middle East and UFlex Limited leverage multinational R&D and procurement to service international brand owners, capturing large turnkey contracts. Regional specialists like Hotpack Packaging Industries and Arabian Flexible Packaging emphasize speed-to-market, multilingual artwork support, and smaller lot sizes suited to local SMEs.

Strategic themes center on vertical integration into recycling and bio-material compounding to comply with end-of-life mandates. Taghleef Industries opened an innovation center in Italy dedicated to mono-material barrier films, accelerating intellectual-property pipelines that cascade into Middle East operations. Hotpack Global’s greenfield biodegradable-pack plant enhances control over differentiated substrates, positioning it to win sustainability-focused tenders.

Supply-chain reliability emerged as a competitive differentiator during the 2024 freight disruptions. Firms with contingency polymer supply contracts secured incremental business when rivals rationed output. The resulting customer churn slightly rebalanced shares, but overall industry structure still reflects a cluster of 10–12 meaningful players, each carving out niches across material, product, or service specialization. This competitive fabric underpins steady yet disciplined growth in the United Arab Emirates flexible packaging market.

United Arab Emirates Flexible Packaging Industry Leaders

Integrated Plastics Packaging LLC

Arabian Flexible Packaging LLC

Huhtamaki Flexible Packaging Middle East LLC

Amber Packaging Industries LLC

Swiss Pac UAE Packaging Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ENPI Group expanded Dubai disposable food-pack operations, increasing regional coverage.

- March 2025: Hotpack Packaging Industries enlarged manufacturing and logistics facilities across multiple emirates.

- January 2025: Taghleef Industries launched its 2025 flexible-film portfolio featuring recyclable mono-material solutions for food packs.

- December 2024: Taghleef Industries added new BOPP, CPP, and barrier film lines focused on mono-material output.

United Arab Emirates Flexible Packaging Market Report Scope

The market for the study defines the revenues (USD million) generated from the sales of flexible packaging products. The study covers the flexible packaging market tracked in terms of consumption and is limited to flexible packaging products made from plastic, paper, and aluminum.

The study on the UAE flexible packaging market tracks the demand for material types such as plastic (flexible (wraps, pouches, films, stand-up pouches, tubes, sleeves, sachets, liners, etc.), paper (paper bags, liquid board, paper wraps) and metal foils (aluminum). Also, it tracks the market size in terms of revenue for the respective end-user industry verticals from the listed product types. The study factors in the impact of COVID-19 on the market studied based on the prevalent base scenarios, key themes (growing demand for single-use), and end-user vertical-related demand cycles.

By Material

| Plastics |

| Paper |

| Metal Foil |

| Bioplastic and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Labels and Sleeves |

By End-User Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverages | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Other End-user Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital |

| Other Printing Technologies |

| By Material | Plastics | |

| Paper | ||

| Metal Foil | ||

| Bioplastic and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Labels and Sleeves | ||

| By End-User Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverages | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Other End-user Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

How large is the United Arab Emirates flexible packaging market in 2026?

It is valued at USD 1.5 billion with a projected 3.49% CAGR to 2031.

Which material dominates converters’ portfolios?

Plastic substrates hold 64.58% share, though recyclable mono-material versions are rapidly replacing legacy multi-layer laminates.

Which product type is growing fastest?

Sachets and stick packs are forecast to expand at 4.69% CAGR due to portion-control demand in meal-kits and cosmetics.

Why are halal exports important for pack design?

Halal certification enforces traceability and barrier performance, driving adoption of premium multi-layer pouches favored by export processors.

How is regulation shaping innovation?

Circular Economy Policy 2071 mandates full recyclability, pushing converters toward mono-material films and investments in domestic recycling capacity.

What role does digital printing play?

Digital presses enable short-run, variable-data artwork that supports e-commerce personalization and multilingual halal labeling without costly plates.

Page last updated on: