Bag-in-Box Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

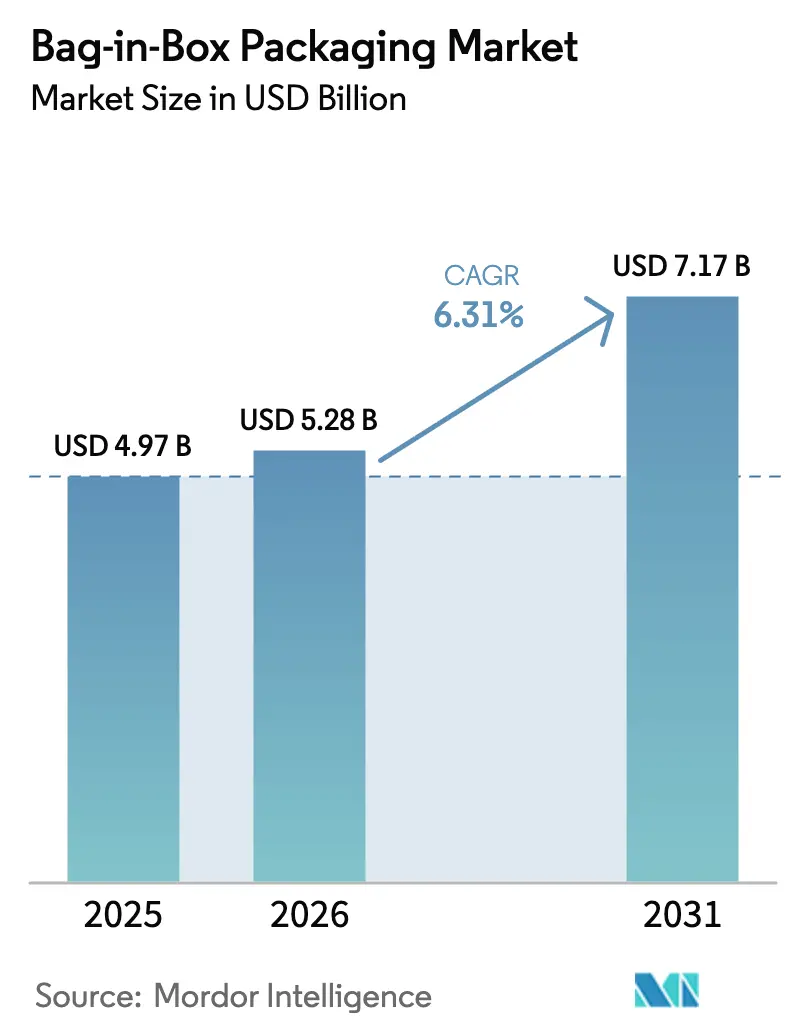

| Market Size (2026) | USD 5.28 Billion |

| Market Size (2031) | USD 7.17 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

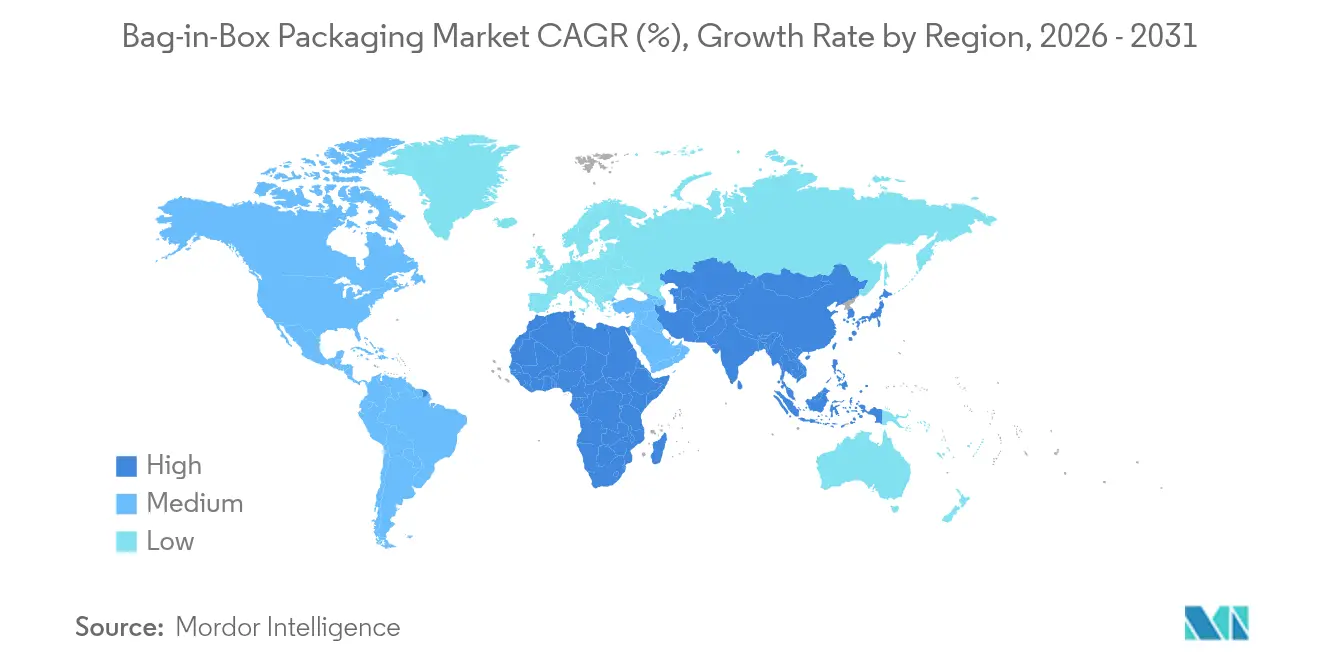

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

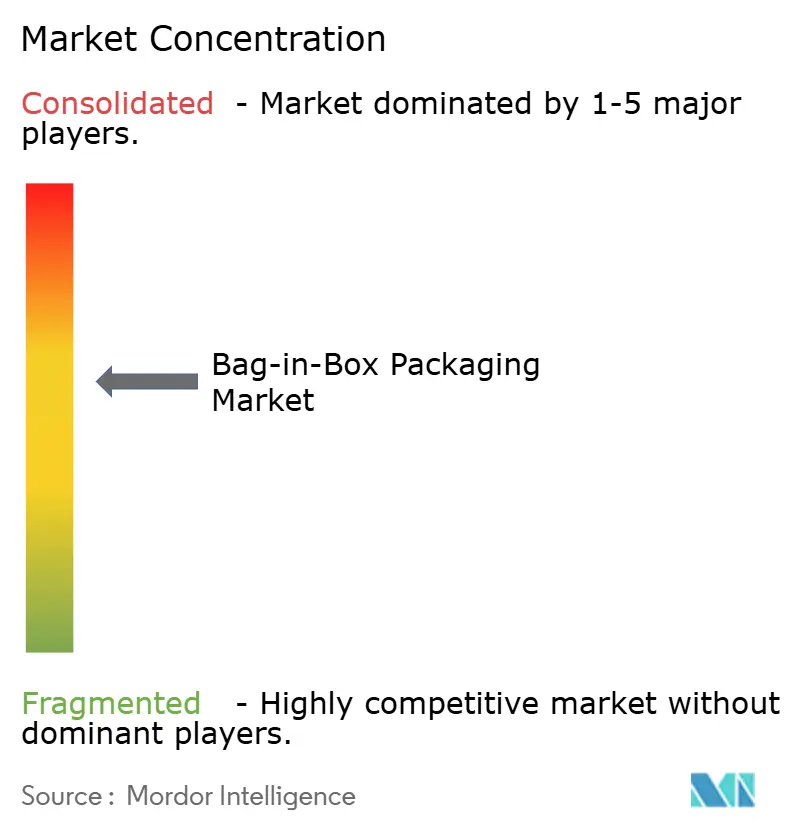

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bag-in-Box Packaging Market Analysis by Mordor Intelligence

bag-in-box packaging market size in 2026 is estimated at USD 5.28 billion, growing from 2025 value of USD 4.97 billion with 2031 projections showing USD 7.17 billion, growing at 6.31% CAGR over 2026-2031. Rising demand for low-carbon solutions, progress in barrier film technology, and regulatory pressure to improve recyclability are amplifying adoption rates across food, beverage, and industrial users. Premium wine brands continue to migrate from glass to flexible packs, using advanced oxygen-barrier films to safeguard sensory quality while trimming logistics costs. E-commerce fulfillment centers favor the format because its rectangular profile yields higher truckload density and reduces breakage during automated handling. In parallel, aseptic systems that eliminate cold-chain needs are unlocking plant-based dairy and pharmaceutical applications. Industry players with vertically integrated film, tap, and corrugated operations retain pricing power in the face of EVOH cost swings and emerging Extended Producer Responsibility fees.

Key Report Takeaways

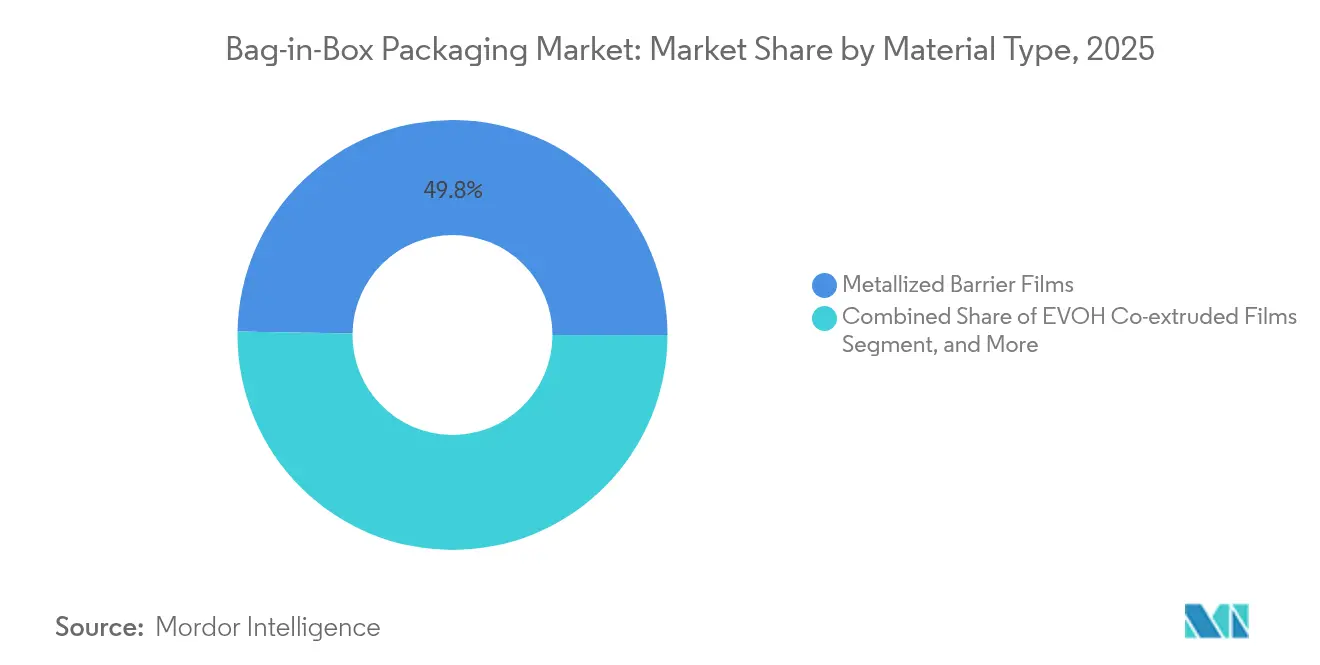

- By material type, metallized barrier films led with 49.75% of the bag-in-box packaging market share in 2025, while EVOH films posted the fastest 9.12% CAGR through 2031.

- By end-user, food applications captured 34.80% revenue share in 2025; beverages are projected to expand at a 10.18% CAGR through 2031.

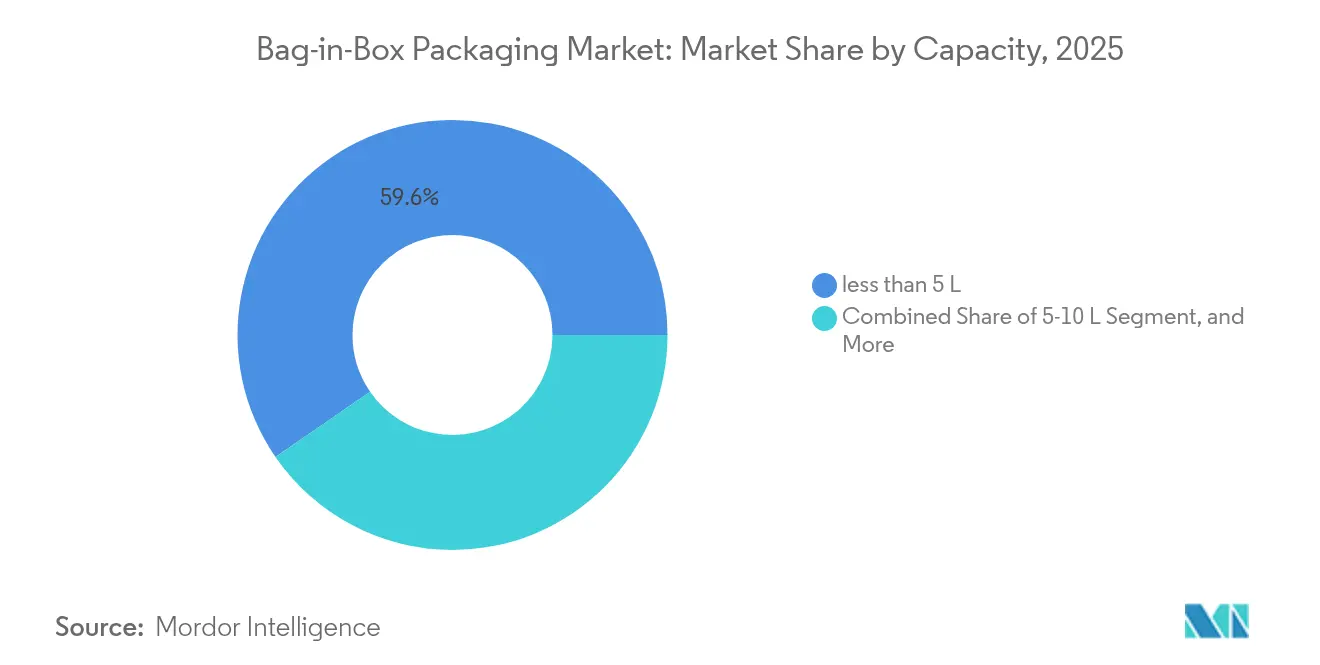

- By capacity, packs under 5 liters held 59.60% of the bag-in-box packaging market size in 2025, whereas the 5-10 liter tier is forecast to rise at an 8.30% CAGR to 2031.

- By filling technology, non-aseptic lines dominated with 69.90% share in 2025, yet aseptic systems are advancing at a 7.22% CAGR on the back of plant-based dairy and pharma demand.

- Asia-Pacific commanded 41.70% of the bag-in-box packaging market in 2025 and is projected to lead growth at 8.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bag-in-Box Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift from glass to BIB in premium wine segment | +1.8% | Global, with early adoption in France, Australia, US | Medium term (2-4 years) |

| E-commerce demand for lightweight, leak-proof formats | +1.5% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Adoption of aseptic BIB for plant-based dairy alternatives | +1.2% | Europe & North America, emerging in APAC | Medium term (2-4 years) |

| Sustainability regulations favoring low-carbon packaging | +1.0% | EU leading, North America following, APAC selective | Long term (≥ 4 years) |

| Smart-tap IoT integration enabling dispensing analytics | +0.6% | North America & EU foodservice, industrial applications | Long term (≥ 4 years) |

| Growth of micro-fulfillment grocery models needing bulk liquids | +0.8% | Urban centers globally, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid shift from glass to BIB in premium wine segment

Historical stigma around boxed wine is fading as boutique estates prove that flexible packs can preserve bouquet and shelf life when filled on high-precision lines. France lifted its boxed wine share from single digits in 2004 to 39.5% in 2017, and producers in Australia and the United States now retail three-liter cases priced up to USD 100. Oxygen-controlled EVOH layers hold dissolved CO₂ and SO₂ within tight limits, matching glass performance while slashing distribution emissions. Younger consumers value portability for outdoor occasions, which steers volume toward the bag-in-box packaging market. Brand owners also benefit from a 43% increase in pallet efficiency compared with bottles, further raising profit per shipment.

E-commerce demand for lightweight, leak-proof formats

Online grocery and direct-to-consumer alcohol channels subject parcels to multiple conveyors and sortation drops, prompting suppliers to specify burst-resistant inner bags with tamper-proof taps. A typical three-liter case weighs 60% less than glass and meets SIOC guidelines that bypass over-boxing, which trims both DIM weight and packaging tax liabilities. Brands like Milkadamia achieve 94% solid-waste reduction by shipping flat packs that expand at the filler and maintain 18-month ambient life. As parcel networks grow in Southeast Asia and Latin America, the bag-in-box packaging market gains fresh addressable volume.

Adoption of aseptic BIB for plant-based dairy alternatives

Shelf-stable oat and almond drinks require microbial control without refrigeration, and that is accomplished through sterile filling inside hermetic bags with high oxygen barriers. Tetra Pak’s integrated lines support enzymatic liquor treatment and deliver six-layer EVOH membranes that lock oxygen transmission below 0.1 cm³/m² d bar. European co-packer Boermarke boosted output eightfold after switching its portfolio to plant-based items in 2023, illustrating scalability of aseptic technology. As specialty beverages win supermarket shelf space, aseptic capacity becomes a strategic differentiator across the bag-in-box packaging market.

Sustainability regulations favoring low-carbon packaging

Extended Producer Responsibility programs reset cost equations by linking material fees to recyclability and weight. The United Kingdom will charge GBP 423 per tonne for plastic in 2025, compared with GBP 192 for glass, but bag-in-box systems offset that disparity with corrugated outer casings that already achieve 75% recycling rates.[1]UK Government, “Extended Producer Responsibility for Packaging: 2025 Base Fees,” gov.uk Minnesota’s 2024 statute demands 80% recyclability by 2029, pressuring multilayer pouches while rewarding easy-split tap designs that reach 90% recyclability after separation. Such measures reinforce the long-term pull toward the bag-in-box packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from recyclable PET "cask" pouches | -0.8% | Global, particularly in premium beverage segments | Short term (≤ 2 years) |

| EVOH and metallized film price volatility | -1.2% | Global supply chains, concentrated in Asia-Pacific production | Short term (≤ 2 years) |

| Limited curb-side recycling infrastructure for multi-layer films | -0.9% | North America & EU primarily, emerging in APAC | Medium term (2-4 years) |

| Extended Producer Responsibility (EPR) fees on composite packs | -0.7% | EU leading implementation, North America following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from recyclable PET “cask” pouches

Flat PET bottles and monomaterial spout pouches leverage existing curb-side streams, eliminating the need to separate bags from boxes. Leading Australian wineries shifted up to 85% of domestic volume into recycled-content PET containers that reduce emissions by 50% versus glass. Start-ups that market Sugarflex negative-carbon laminates intensify price competition by avoiding expensive barrier films, which may divert share from the bag-in-box packaging industry in premium categories.

EVOH and metallized film price volatility

Feedstock swings in Asia tighten supply and push up cost per kilo for high-barrier substrates. In 2024 plastic packaging expenses climbed 8.2%, with EVOH grades seeing the steepest rises. Smaller converters without long-term resin contracts face margin compression, limiting their ability to quote competitive bids and potentially slowing purchase cycles within the bag-in-box packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: EVOH films escalate premium growth prospects

Metallized films yielded the largest 49.75% share of the bag-in-box packaging market in 2025, testament to their favorable cost-to-barrier ratio. However, EVOH co-extrusions deliver a 9.12% CAGR through 2031, propelled by high-value wine and pharmaceutical applications that require oxygen ingress below 0.5 mg L⁻¹ per year. That rapid momentum positions EVOH as the primary driver of incremental revenue even as absolute tonnage remains lower than metalized counterparts. Kuraray’s EVAL resins adjust ethylene content to fine-tune gas barrier performance, thereby enabling wineries to match target shelf life while minimizing polymer weight. The bag-in-box packaging market size tied to premium films is therefore set to rise faster than commodity layers over the forecast horizon. Continuous R&D into bio-based EVOH grades and nano-clay barrier coatings is likely to unlock mono-material concepts that streamline post-consumer recycling. Leading converters such as Smurfit Westrock have pilot lines that laminate low-gauge EVOH onto corrugated inserts, illustrating how vertical integration can curb raw material cost exposure.

A second growth vector stems from corporate climate targets that oblige brand owners to publish Scope 3 emissions data. Metallized films carry a higher embodied energy profile than EVOH, which benefits from thinner gauge and lower aluminum usage. When paired with corrugated outers that already average 75% recycled fiber, EVOH solutions cut cradle-to-gate emissions by up to 30%. As large beverage groups submit CDP disclosures, procurement teams are expected to incorporate life-cycle scores alongside price per meter. This shift enlarges opportunity for suppliers who can document verified carbon footprints, and it boosts the bag-in-box packaging market across premium categories.

By End-User Industry: Beverages accelerate beyond core food demand

Food applications retained 34.80% revenue share in 2025, anchored by institutional sauces and dairy concentrates that rely on cost-driven LDPE liners. Yet beverage brands will post a 10.18% CAGR through 2031, lifting their slice of the bag-in-box packaging market size as wine, coffee, and functional drinks pivot toward flexible formats. Fine-wine producers doubled boxed volumes in 2025 as retailers granted shelf facings to USD 20-plus three-liter SKUs that address younger shoppers seeking convenient pouring. Meanwhile ready-to-drink cocktails ride the e-commerce wave, and foodservice operators adopt five-liter packs to dispense cold brew via smart taps that collect pour metrics over Bluetooth.

Industrial and personal care users add resilience to revenue streams by applying thicker, chemical-resistant films that support aerosol replacement programs. For example, disinfectant concentrates ship in 20-liter liners that integrate UN-rated fitments for closed-loop dilution, reducing transport weight by 75% compared with HDPE drums. As aseptic capability penetrates nutraceutical diluents and intravenous hydration solutions, the bag-in-box packaging market diversifies into healthcare, widening margins and reducing seasonality.

By Capacity: Mid-range formats seize foodservice and micro-fulfillment gains

Packs under 5 liters continue to dominate absolute volume at 59.60% in 2025, driven by retail wine and specialty beverage SKUs that fit kitchen refrigerators. However, the 5-10 liter tier is registering the fastest 8.30% CAGR, buoyed by quick-commerce dark stores that require compact bulk formats for back-of-house operations. The expansion at that range boosts corrugated consumption because each outer carton typically uses double-wall fluting to bear the heavier load. As a result, corrugators that co-locate with bag fitment operations capture cross-selling potential within the bag-in-box packaging market.

Mid-size formats also align with franchise menu innovations such as frozen cocktail bases, dispensing chocolate syrups, and oat concentrate for on-premise baristas. Sealing System’s automated lines fill 30 cases per minute, cutting labor costs for co-packers who manage weekly changeovers between beverage flavors. For institutional caterers, seven-liter hot-fill tolerances eliminate the need for stainless reservoirs, slashing initial capex. These advantages reinforce sustained growth in the mid-range capacity band.

By Filling Technology: Aseptic lines capture high-margin healthcare demand

Although ambient lines maintained 69.90% share in 2025, aseptic equipment will post a 7.22% CAGR by delivering shelf-stable solutions for plant-based milks, pediatric nutrition, and intravenous hydration diluents. Alfa Laval’s modular sterilization tunnels achieve log-6 spore inactivation and integrate thin-wall EVOH bags that lower residual oxygen to 0.05% after filling.That performance meets stringent USP <1207> container closure integrity norms, positioning the bag-in-box packaging market as a credible alternative to blow-fill-seal bottles in certain pharma scenarios.

Capex hurdles remain a deterrent for small wineries, therefore ambient systems will still dominate volume in commodity segments. However, the total addressable market for aseptic lines increases as processors upgrade from hot-fill HDPE to energy-efficient shelf-stable technology. Government incentives that subsidize food-loss reduction projects in the European Union further elevate return on investment for sterile filling, underpinning robust uptake through 2031.

Geography Analysis

Asia-Pacific controlled 41.70% of the bag-in-box packaging market in 2025 and is climbing at 8.20% CAGR as urban households in China and India trade up to packaged beverages with extended shelf life. Chinese converter Hansin Packing added two co-extrusion lines that raise regional EVOH film output by 25%, removing supply bottlenecks for local wine co-packers. Government programs that promote grain-based alcohol exports also spur demand for premium oxygen-barrier bags. Rising e-commerce grocery penetration in Southeast Asia drives incremental corrugated consumption, creating an integrated growth loop for the bag-in-box packaging market.

Europe presents a mature yet expanding landscape shaped by strict climate policies. The region’s packaging sector will grow from EUR 153 billion in 2024 to EUR 186 billion by 2029, and within that scope the bag-in-box packaging market draws strength from France where 44% of wine volume already uses the format. Denmark records a 65% recycling rate that favors easy-separate tap designs, while the Netherlands pledges fossil-free packaging by 2050, which accelerates contracts for mono-material EVOH films. Paper-based bottle start-ups emulate bag-in-box structural principles, validating the segment’s environmental credentials.

North America is consolidating fast. The USD 11.2 billion Smurfit Westrock merger completed in July 2024 enlarged production capacity and added a South Carolina greenfield site dedicated to bag-in-box systems. Six states have enacted EPR laws that reward light weight, which raises the competitiveness of corrugated outer casings relative to PET gallon jugs. The newly formed Wine & Spirits Solutions Group at ProMach signals more capital allocation toward line integration, highlighting the strategic value of this format.

Competitive Landscape

The bag-in-box packaging market is moderately concentrated. Smurfit Westrock, Liquibox, SIG, and Scholle IPN collectively control roughly 45% of global volume, while dozens of regional converters serve niche and private-label clients. The Smurfit Westrock merger unlocked USD 400 million in annual run-rate synergies and created 63 paper mills that secure kraft liner supply for integrated outer boxes.[3]Smurfit Westrock, “First Quarter 2025 Results,” smurfitwestrock.com Liquibox focuses on high-barrier products for dairy and bulk water, operating under Amcor following the USD 8.4 billion Amcor-Berry union that pooled R&D funds to USD 180 million per year.

Digitalization emerges as a key differentiator. Tap sensors from TappTek allow foodservice operators to track pour duration, helping brands validate pay-per-use models and reduce shrinkage. Gamer Packaging signed an exclusive distribution pact with Xolution for new cap technologies that simplify recycling by eliminating metal springs. Patent filings for vessel-activated dispensers suggest further automation that could integrate QR-based re-ordering within the bag-in-box packaging industry.

At the materials level, Accredo’s bio-based pouch secured 43 grams of CO₂ sequestration per unit, prompting incumbents to pilot sugarcane-based EVOH alternatives. Innovation therefore hinges on aligning barrier performance with circular-economy targets, and suppliers that master both stand to gain share.

Bag-in-Box Packaging Industry Leaders

-

DS Smith PLC

-

CDF Corporation

-

Smurfit Westrock

-

Mondi

-

Amcor Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smurfit Westrock reported Q1 2025 net sales of USD 7.656 billion and confirmed construction of a new South Carolina bag-in-box plant.

- February 2025: Amcor and Berry Global shareholders approved an USD 8.4 billion all-stock merger to consolidate flexible and rigid packaging portfolios.

- February 2025: ProMach formed a Wine & Spirits Solutions Group to supply integrated bag-in-box lines.

- November 2024: Smurfit Westrock introduced EasySplit Bag-in-Box that attains 90% recyclability compliance ahead of EU rules.

Global Bag-in-Box Packaging Market Report Scope

The market study tracks the demand for different types of bag-in-box packaging formats in various capacities, including 0-5 liter, 5-10 liter, and greater than 10 liter for various applications, including beverage, food, medical and pharmaceutical, personal care and home care, other end users, etc. The pricing for the raw material, that is, plastic and paper for bag-in-box packaging products, is taken into consideration along with the consumption, import, and export trends, as well as average prices, to arrive at the market revenue.

The bag-in-box packaging market is segmented by capacity (0-5 liter, 5-10 liter, and greater than 10 liter), by end-user industry (beverage, [alcoholic drinks and non-alcoholic drinks], food, pharmaceutical and medical, industrial [chemical, paintings, and coatings], personal care and homecare, and other end-use industries [automotive, agriculture, and pet food] and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Italy, and Rest of Europe], Asia-Pacific [China, India, Japan, Australia and New Zealand, Rest of Asia-Pacific], Latin America [Brazil, Mexico, Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Metallized Barrier Films |

| EVOH Co-extruded Films |

| LDPE Monolayer |

| Beverage | Alcoholic Drinks |

| Non-alcoholic Drinks | |

| Food | |

| Pharmaceutical and Medicine | |

| Industrial (Chemicals, Paints and Coatings) | |

| Personal and Home Care |

| less than 5 L |

| 5–10 L |

| >10 L |

| Aseptic |

| Non-aseptic (Ambient) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Metallized Barrier Films | ||

| EVOH Co-extruded Films | |||

| LDPE Monolayer | |||

| By End-User Industry | Beverage | Alcoholic Drinks | |

| Non-alcoholic Drinks | |||

| Food | |||

| Pharmaceutical and Medicine | |||

| Industrial (Chemicals, Paints and Coatings) | |||

| Personal and Home Care | |||

| By Capacity | less than 5 L | ||

| 5–10 L | |||

| >10 L | |||

| By Filling Technology | Aseptic | ||

| Non-aseptic (Ambient) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the bag-in-box packaging market by 2031?

The market is expected to reach USD 7.17 billion by 2031, growing at a 6.31% CAGR.

Which region leads growth in the bag-in-box packaging market?

Asia-Pacific is forecast to post the fastest 8.20% CAGR through 2031, underpinned by industrialization and rising e-commerce.

Why are beverage companies shifting to bag-in-box formats?

Beverage firms gain logistics savings, reduced carbon footprints, and longer shelf life thanks to high-barrier EVOH films and aseptic filling.

What material segment shows the fastest growth?

EVOH co-extruded films register a 9.12% CAGR through 2031 because of superior oxygen barriers needed for premium wine and pharma uses.

How do Extended Producer Responsibility laws influence adoption?

EPR fees penalize heavy or difficult-to-recycle packs, so lightweight corrugated-based bag-in-box systems help brand owners lower compliance costs.

Are aseptic lines gaining traction in the bag-in-box packaging market?

Yes. Aseptic filling is growing at 7.22% CAGR as plant-based dairy and healthcare demand year-round ambient distribution without preservatives.

Page last updated on: