Market Overview

| Study Period | 2020 - 2030 |

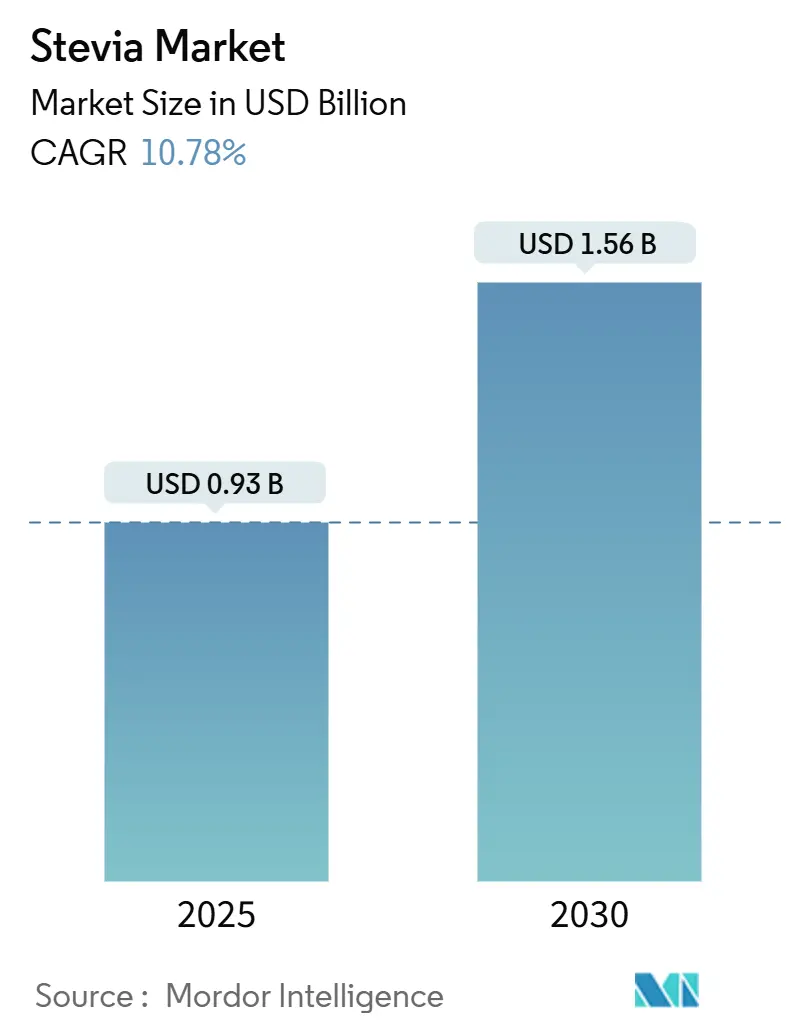

| Market Size (2025) | USD 0.93 Billion |

| Market Size (2030) | USD 1.56 Billion |

| Growth Rate (2025 - 2030) | 10.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Stevia Market Analysis by Mordor Intelligence

The Stevia market, valued at USD 0.93 billion in 2025, is anticipated to grow significantly, reaching USD 1.56 billion by 2030, with a strong CAGR of 10.78%. This growth is driven by increasing regulatory support, including FDA GRAS notices for rebaudioside M and enzyme-modified glycosides, which ensure product safety and encourage wider adoption. Rising health concerns about sugar consumption, coupled with the growing prevalence of obesity and diabetes, are pushing manufacturers to adopt plant-based alternatives, making Stevia a key solution for sugar reduction. The Asia-Pacific region remains a leader in Stevia cultivation and processing due to its scale and expertise. However, challenges such as tariff policies and scrutiny over labor practices are prompting buyers to explore alternative sourcing options. Additionally, advancements in bioconversion and precision fermentation technologies are reducing production costs and improving the taste profile of Stevia, enabling its use in a wider range of applications.

Key Report Takeaways

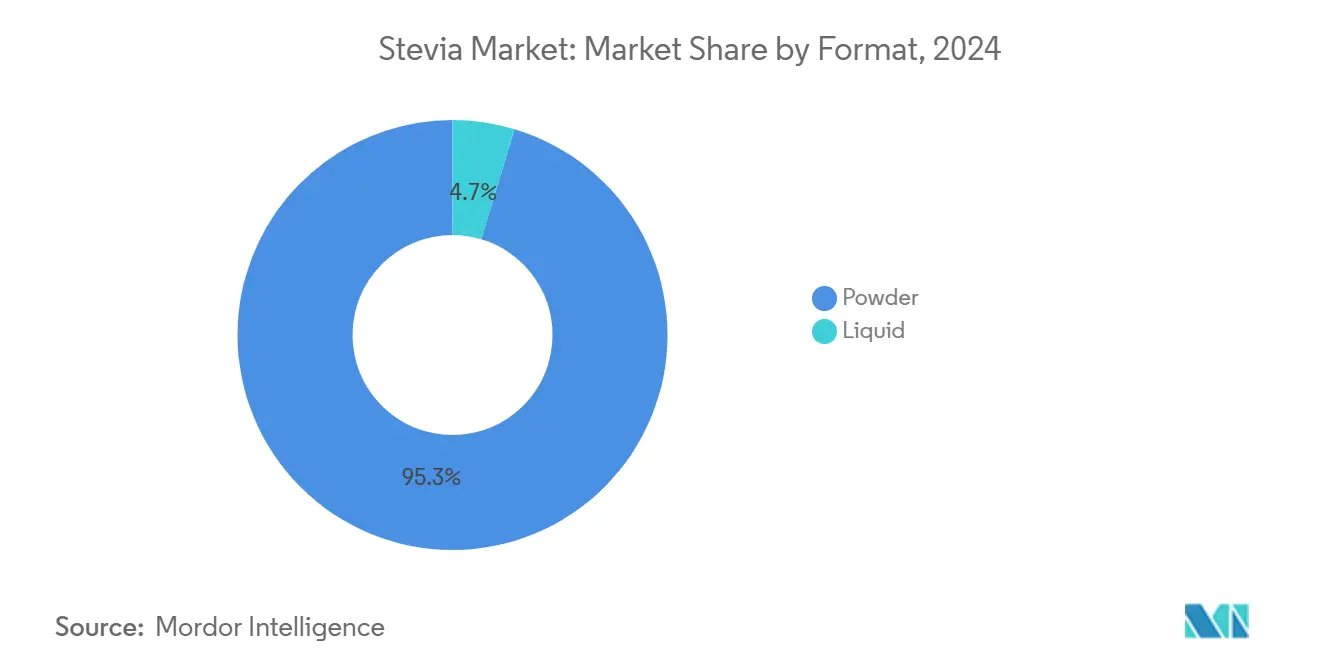

- By format, powder accounted for 95.34% of Stevia market share in 2024, while liquid formats are forecast to grow at 12.58% CAGR through 2030.

- By ingredient type, conventional variants led with an 80.34% share in 2024, whereas organic Stevia is positioned to grow at 11.43% CAGR through 2030.

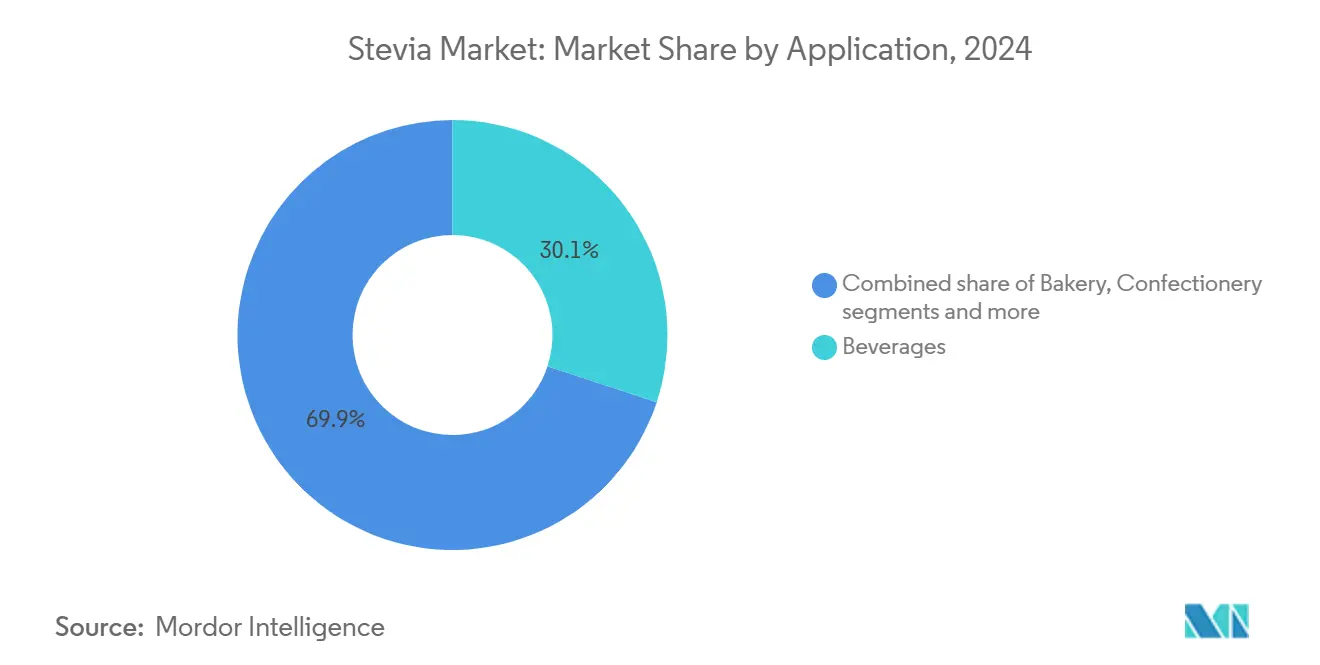

- By application, beverages captured 30.07% share of the Stevia market size in 2024 and are projected to expand at 13.21% CAGR to 2030.

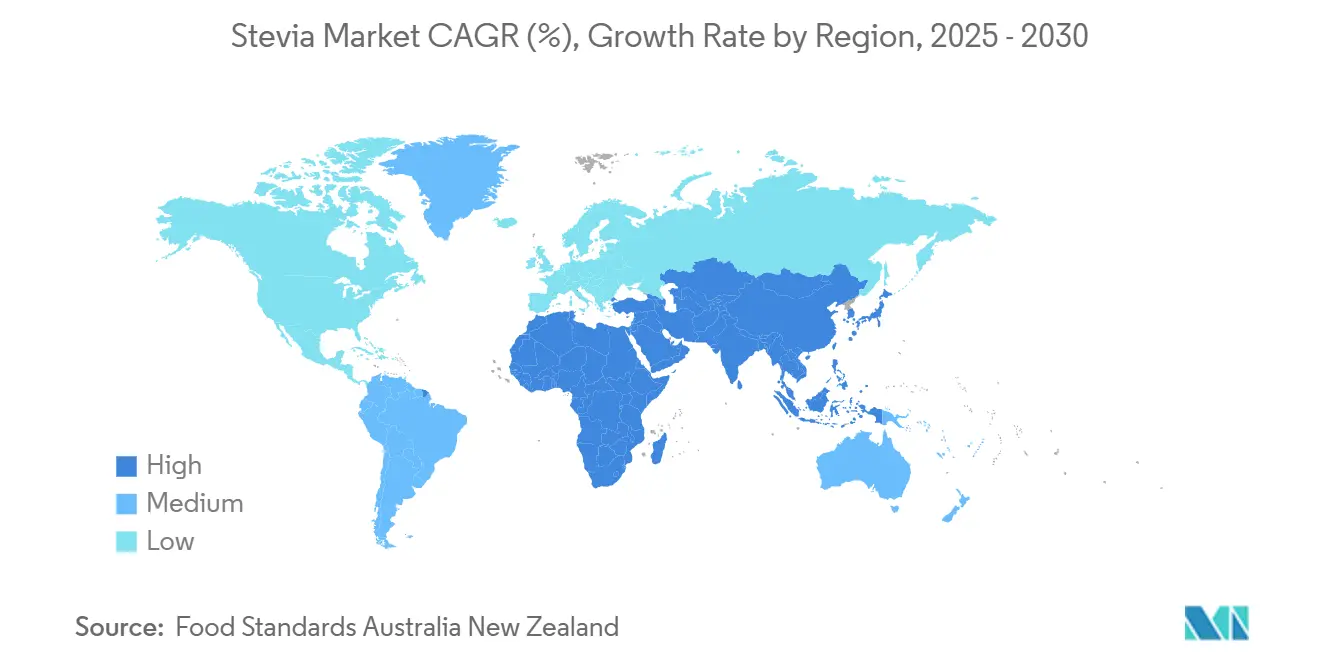

- By geography, Asia-Pacific commanded a 31.43% share of the Stevia market in 2024 and is advancing at 12.20% CAGR over the forecast horizon.

Global Stevia Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift in consumer preference toward natural and plant-based sweeteners | +2.5% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Boosting market growth surge in new product launches featuring stevia | +1.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Expanding use of stevia in pharmaceuticals and nutraceuticals | +1.2% | North America and Europe primarily | Long term (≥ 4 years) |

| Advancements in stevia extraction and processing technologies | +0.8% | Global, concentrated in major production hubs | Medium term (2-4 years) |

| Increasing prevalence of diabetes and obesity worldwide | +0.6% | Global, with acute impact in developing markets | Long term (≥ 4 years) |

| Growing use of stevia in functional and fortified foods | +0.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Shift in consumer preference toward natural and plant-based sweeteners

Consumer preference for natural alternatives to artificial sweeteners is driving stevia's dominance in the sweetener market, especially in developed markets where clean-label demands and ingredient transparency influence purchases. Regulatory advancements, like the FDA's GRAS approvals for steviol glycosides in May 2025, enhance trust by confirming safety and versatility [1]Source: U.S. Food and Drug Administration, "Recently Published GRAS Notices and FDA Letters", fda.gov. Institutional buyers, including foodservice operators and manufacturers, are also adopting stevia to meet the demand for health-conscious, sustainable products. Stevia's consistent and resilient demand positions it as a key growth driver in the sweetener market and a vital part of the industry's evolution.

Boosting the market growth surge in new product launches featuring stevia

Manufacturers are driving product innovation by utilizing stevia's versatility in beverages, dairy, and baked goods while addressing taste challenges. For example, Cargill and DSM-Firmenich's EverSweet line uses precision fermentation to create sugar-like Reb M and Reb D molecules without aftertaste. In 2024, the European Union approved fermentation-based stevia products, enabling broader launches in the region. Improved manufacturing processes are also lowering costs, making stevia a viable alternative to artificial sweeteners. Beverage leaders like Coca-Cola are investing in zero-sugar formulations, supported by better taste profiles, regulatory backing, and cost efficiencies, fostering innovation across food categories.

Expanding use of stevia in pharmaceuticals and nutraceuticals

Stevia is gaining traction in the pharmaceutical and nutraceutical sectors due to its health benefits beyond sweetness. Research shows that steviol glycosides, the key compounds in stevia, offer anti-diabetic, anti-hypertensive, and antioxidant properties, making it a functional ingredient. The FDA's "Generally Recognized as Safe" status for steviol glycosides supports their use in diabetic medications and nutritional supplements. For instance, Biologic Pharmamedical's Glyvia, a patented zero-carb sweetener, aids glucose metabolism. Stevia's natural origin and proven safety align with pharmaceutical quality standards, enabling premium pricing and long-term contracts. By entering these markets, stevia reduces reliance on the food and beverage sector and strengthens its role in high-margin pharmaceutical supply chains.

Advancements in stevia extraction and processing technologies

Technological advancements in stevia processing are addressing challenges like taste, solubility, and cost. Bioconversion and precision fermentation are driving efficiency and sustainability. Ingredion's expansion of its bioconversion facility in Malaysia highlights the industry's focus on scaling advanced technologies. Patent filings for improved rebaudioside M solubility, including PureCircle's contributions, reflect efforts to enhance product quality. Cargill's EverSweet production in Nebraska showcases fermentation-based methods reducing environmental impact and improving cost efficiency. These innovations are increasing access to high-quality steviol glycosides, particularly Reb M and Reb D, while integrating biotechnology with traditional methods to strengthen the supply chain and meet growing global demand.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in stevia leaf prices due to agricultural factors | -1.5% | Global, with acute impact in major producing regions | Short term (≤ 2 years) |

| Stringent regulatory requirements and lengthy approval processes | -1.0% | Europe and emerging markets primarily | Medium term (2-4 years) |

| Supply chain disruptions affecting product availability | -0.8% | Global, concentrated in China-dependent supply chains | Short term (≤ 2 years) |

| High production costs compared to traditional sweeteners | -0.6% | Global, most pronounced in cost-sensitive applications | Medium term (2-4 years) |

Source: Mordor Intelligence

Volatility in stevia leaf prices due to agricultural factors

Stevia producers face challenges from volatile agricultural commodity prices, unpredictable weather, and geopolitical events, which disrupt supply chains and complicate price forecasts. Concentrated production in specific regions increases risks from localized disruptions, worsened by climate change. Geopolitical tensions, such as US Customs seizing Chinese stevia extracts over forced labor concerns, highlight vulnerabilities. Tariffs on imports from China and India are driving manufacturers to diversify sourcing, raising short-term costs but boosting domestic production. Splenda's USD 50 million Florida facility, launched in March 2023, aims to reduce reliance on international markets. Companies are adopting vertical integration and exploring precision fermentation to strengthen supply chains and ensure a sustainable stevia market.

Stringent regulatory requirements and lengthy approval processes sweeteners

Regulatory hurdles worldwide challenge market entry and product innovation by extending development timelines and increasing compliance costs. For example, the European Food Safety Authority's evaluation of steviol glycosides highlights strict safety assessments that delay market access. While the US and EU have clear approval frameworks, emerging markets often lack guidelines for new steviol glycoside variants, limiting global expansion. The FDA's Generally Recognized As Safe process supports stevia applications but requires detailed documentation, causing lengthy reviews and commercialization delays. Slow regulatory harmonization and varying purity standards, labeling rules, and usage restrictions across markets further complicate compliance and increase costs.

Segment Analysis

By Format: Powder Maintains Market Leadership

In 2024, powder stevia holds a 95.34% market share, establishing itself as the preferred choice in food and beverage manufacturing. Its dominance is due to stability, long shelf life, and compatibility with production processes. The powder format is favored for its handling ease, precise dosing, and cost-effective production, making it ideal for large-scale applications. Research from the University of Hohenheim highlights its versatility, with usage levels of 160-700 mg/kg in beverages and 500-1000 mg/kg in dairy desserts [2]Source: University of Hohenheim, "Basic Formulas For The Use Of Stevia Natural Sweetener in Foodstuffs", uni-hohenheim.de. Its moisture resistance and thermal stability make it suitable for baking, where liquid formats may compromise quality.

Liquid stevia is emerging as the fastest-growing format segment, with a projected CAGR of 12.58% from 2025 to 2030. This growth is driven by technological advancements that have addressed previous challenges related to solubility and taste. The rising demand for zero-sugar beverages, which require complete dissolution and precise sweetness control, is a significant factor fueling the liquid format's adoption. Industry leaders like Coca-Cola are actively working on improving rebaudioside M solubility through innovative compositions and spray-dried formulations. Additionally, Ingredion's Clean Taste Solubility Solution showcases advancements in liquid stevia applications, enhancing both taste and functionality to meet the evolving needs of beverage manufacturers.

By Ingredient Type: Conventional Stevia Maintains Dominance

In 2024, conventional stevia holds an 80.34% market share due to cost advantages and established supply chains catering to price-sensitive food and beverage sectors. Its dominance is driven by economies of scale and processing efficiencies, enabling competitive pricing for high-volume applications. While China and India strengthen conventional supply chains, trade disruptions like US tariffs and forced labor concerns are prompting sourcing strategy shifts. Advanced cultivation practices and technologies further optimize yields and reduce production costs in key regions.

From 2025 to 2030, organic stevia is expected to grow at an 11.43% CAGR, driven by premiumization and rising demand for certified organic, clean-label ingredients. This growth aligns with the food and beverage sector's sustainability focus, as companies prioritize environmentally and socially responsible sourcing. Organic farming offers a 12.03% return on investment compared to 3.99% for conventional methods. However, supply challenges, including limited certified cultivation zones and high costs, create opportunities for premium pricing and long-term contracts with quality-focused manufacturers.

By Application: Beverages Dominate Market Position

In 2024, beverages held the largest market share at 30.07% and are projected to grow at a CAGR of 13.21% from 2025 to 2030. Growth is driven by the food and beverage industry's focus on reducing sugar and meeting demand for healthier drinks. Regulatory approvals, including FDA GRAS certifications, have enabled the use of steviol glycosides in products like carbonated soft drinks and functional beverages. Coca-Cola reported an 11% growth in its Zero Sugar line in Q3 2024, reflecting significant investments in stevia-based formulations. The industry's ability to address flavor challenges has been key to integrating stevia successfully.

The beverage industry's leadership in both market share and growth rate underscores its vital role in driving the stevia market's expansion. Manufacturers are leveraging advanced processing technologies to enhance taste profiles, making stevia-based products more appealing to consumers. Additionally, sugar taxation policies in key markets like Saudi Arabia and the UAE, where a 50% excise tax on sugar-sweetened beverages has led to reduced consumption and lower obesity rates, create a supportive environment for stevia adoption. The segment's growth is further strengthened by advancements in fermentation-based stevia production, which delivers improved taste compared to traditional extraction methods.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, the Asia-Pacific region holds a 31.43% share of the global stevia market and is projected to grow at a 12.20% CAGR from 2025 to 2030. Growth is driven by established cultivation and rising consumption in China, India, and Japan. The Indian Chemical Council highlights the region's seamless supply chain from cultivation to manufacturing. However, China's leading position faces regulatory challenges from US Customs over forced labor allegations, prompting manufacturers to reconsider sourcing. Meanwhile, India's growing stevia sector, supported by government initiatives, offers an alternative. Innovation, such as nanotechnology for stevioside accumulation, further strengthens the region's position.

North America, with established regulations and consumer acceptance, faces slower growth due to market saturation in the traditional food and beverage sectors. Tate & Lyle's partnership with Manus highlights supply chain advancements in stevia Reb M production. European markets are shifting toward premium stevia applications, driven by demand for clean-label and reduced-sugar products. Developers are addressing taste challenges with flavor-masking techniques and novel blends for dairy, beverages, and bakery products.

South America, the origin of stevia, combines cultivation expertise with emerging processing capabilities. However, macroeconomic volatility and infrastructure issues limit scalability. Producers focus on artisanal farming and sustainable sourcing, with global buyers prioritizing traceability and ESG benchmarks. Paraguay remains a hub for traditional leaf cultivation, appealing to brands seeking authenticity. In the Middle East and Africa, health awareness and regulatory support are growing, though local production is limited. Saudi Arabia and the UAE's 50% excise tax on sugar-sweetened beverages promotes stevia adoption [3]Source: The World Health Organization, "A review of sugar-sweetened beverages taxation in Saudi Arabia and United Arab Emirates", emro.who.int.

Competitive Landscape

The global stevia market is moderately fragmented, with numerous regional and international players competing for market share. Leading companies like Cargill, PureCircle (Ingredion), and Tate & Lyle hold a strong position due to their extensive distribution networks and advanced R&D capabilities. At the same time, many small and medium enterprises focus on offering unique products tailored to local tastes and niche applications. This competitive environment drives ongoing innovation in product formulations, purity levels, and blends with other sweeteners, providing manufacturers in the food and beverage industry with a wide range of options.

The rising demand for natural, zero-calorie sweeteners among health-conscious consumers is fueling market growth. The moderate fragmentation of the market ensures competitive pricing and product variety, creating opportunities for expansion across global markets. Companies are increasingly adopting advanced technologies such as bioconversion, precision fermentation, and improved extraction methods to enhance product quality and reduce production costs. For instance, Ingredion has significantly expanded its bioconversion facility in Malaysia, increasing its capacity fourfold to meet growing market demands and remain competitive.

New players utilizing precision fermentation and sweet protein technologies are disrupting traditional extraction-based business models. This shift is pressuring established companies to innovate and adapt to avoid losing market share. The competitive landscape is evolving into two distinct segments: technology-driven leaders who can command premium pricing and cost-focused producers who compete on scale and affordability.

Stevia Industry Leaders

-

Ingredion Incorporated

-

Tate & Lyle PLC

-

Archer Daniels Midland Company

-

Cargill Incorporated

-

GLG Life Tech Corp.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Arzeda expanded its ProSweet Reb M™ stevia production to over 250 metric tons annually, enabling the company to replace up to 75,000 tons of sugar each year—equivalent to 18.75 billion servings—by providing a 95%-purity, zero-calorie sweetener derived from genuine stevia leaf extract. This strategic move, which includes scaling into Europe, addresses the surging global demand from consumer-packaged goods companies for great-tasting, cost-effective alternatives to traditional and artificial sweeteners, according to the company.

- December 2024: Tate & Lyle formed a partnership with BioHarvest to develop next-generation plant-based ingredients, with an initial focus on botanical sweeteners like stevia, aiming to deliver a sugar-like taste without aftertaste using BioHarvest’s proprietary Botanical Synthesis platform. This collaboration leverages Tate & Lyle’s expertise in sugar reduction and BioHarvest’s non-GMO, sustainable technology, enabling the scalable production of plant-derived molecules that mirror the phyto-nutrients of whole plants while using less land and water.

- October 2024: Tate and Lyle and Manus partnered and introduced Stevia Reb M. The first ingredient to be jointly introduced is stevia Reb M, marking the first large-scale commercialization of an all-Americas-sourced, manufactured, and bio-converted stevia Reb M ingredient.

Global Stevia Market Report Scope

Stevia is a natural sweetener and sugar substitute extracted from the leaves of Stevia rebaudiana, a plant native to Brazil and Paraguay. The stevia market segments include product type, application, origin, and geography. The product type segment comprises powder and liquid formats. Applications include bakery, confectionery, beverages, dairy, tabletop sweeteners, and others. The origin segment divides into organic and conventional categories. Geographically, the market spans North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in USD for all segments.

| By Format | Powder | ||

| Liquid | |||

| By Ingredient Type | Organic | ||

| Conventional | |||

| By Application | Bakery | ||

| Confectionery | |||

| Beverages | |||

| Dairy | |||

| Table-top Sweeteners | |||

| Other Applications | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

By Format

| Powder |

| Liquid |

By Ingredient Type

| Organic |

| Conventional |

By Application

| Bakery |

| Confectionery |

| Beverages |

| Dairy |

| Table-top Sweeteners |

| Other Applications |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current valuation of the Stevia market in 2025?

The Stevia market stands at USD 0.93 billion in 2025, supported by regulatory confidence and sustained demand for natural sweeteners.

How fast is the Stevia market expected to grow through 2030?

The market is projected to expand at a 10.78% CAGR, reaching USD 1.56 billion by 2030.

Which application segment leads Stevia consumption?

Beverages dominate with 30.07% market share in 2024 and a projected 13.21% CAGR, driven by sugar-reduction initiatives.

Why is Asia-Pacific considered crucial for Stevia supply?

Asia-Pacific contributes 31.43% of global revenue, backed by sizable cultivation and processing infrastructure in China and India.