Phosphine Fumigation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

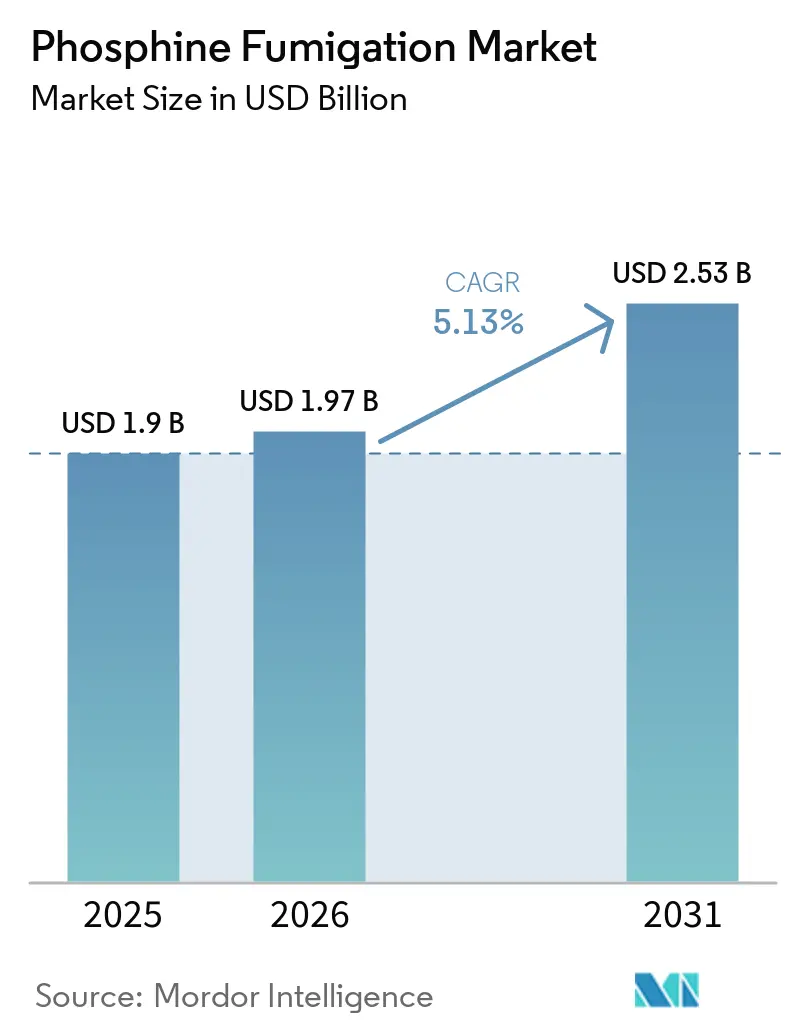

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phosphine Fumigation Market Analysis by Mordor Intelligence

The phosphine fumigation market size is valued at USD 1.9 billion in 2025 and is anticipated to grow from USD 1.97 billion in 2026 to USD 2.53 billion by 2031, registering a CAGR of 4.9% through 2026 to 2031. The phosphine fumigation market is vital for stored-product protection because it can penetrate dense grain stacks, control insects at all life stages, and leave no food-grade residues after ventilation. Its growth is driven by the expansion of modern grain storage facilities and by stricter phytosanitary regulations, which have made certified fumigation a standard in global trade. The market also benefits from the shift away from methyl bromide and increased focus on reducing post-harvest losses in staple crops. However, challenges such as rising pest resistance and stricter compliance requirements on operator certification and exposure management persist. Despite these hurdles, phosphine fumigation remains the preferred choice for bulk grain protection due to its cost-effectiveness, deep penetration, and regulatory acceptance, ensuring its continued relevance in the market.

Key Report Takeaways

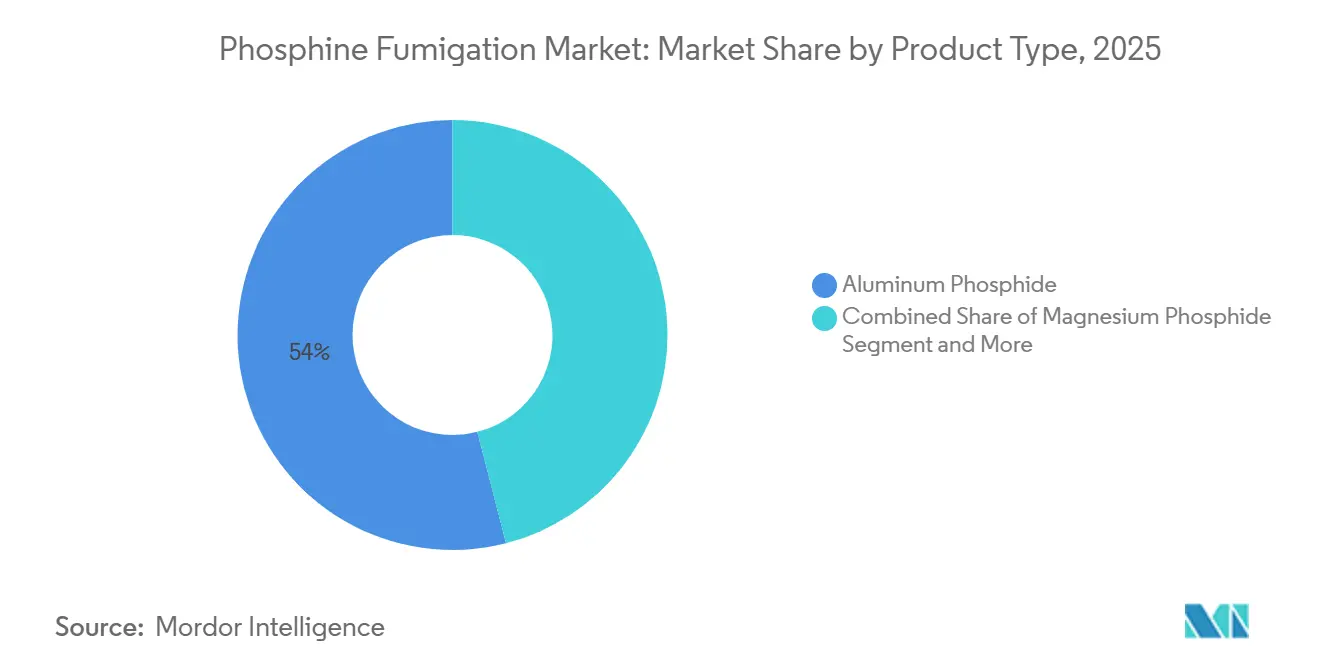

- By product type, aluminum phosphide was the largest segment with 54% of the phosphine fumigation market in 2025, while magnesium phosphide was the fastest segment registering 5.95% CAGR during 2026-2031.

- By form, solid formulations were the largest segment with 59.2% of the phosphine fumigation market size in 2025, while liquid was the fastest segment at a 6.2% CAGR during 2026-2031.

- By crop type, cereals and grains were the largest segment with 63% of the phosphine fumigation market share in 2025, whereas commercial produce and plantation accounted for the fastest growth, registering 5.9% CAGR through 2026-2031.

- By storage structure, commercial bulk silos held the largest share, accounted for 36.67% of the phosphine fumigation market size in 2025, while export containers held the fastest 6.5% CAGR through 2026-2031.

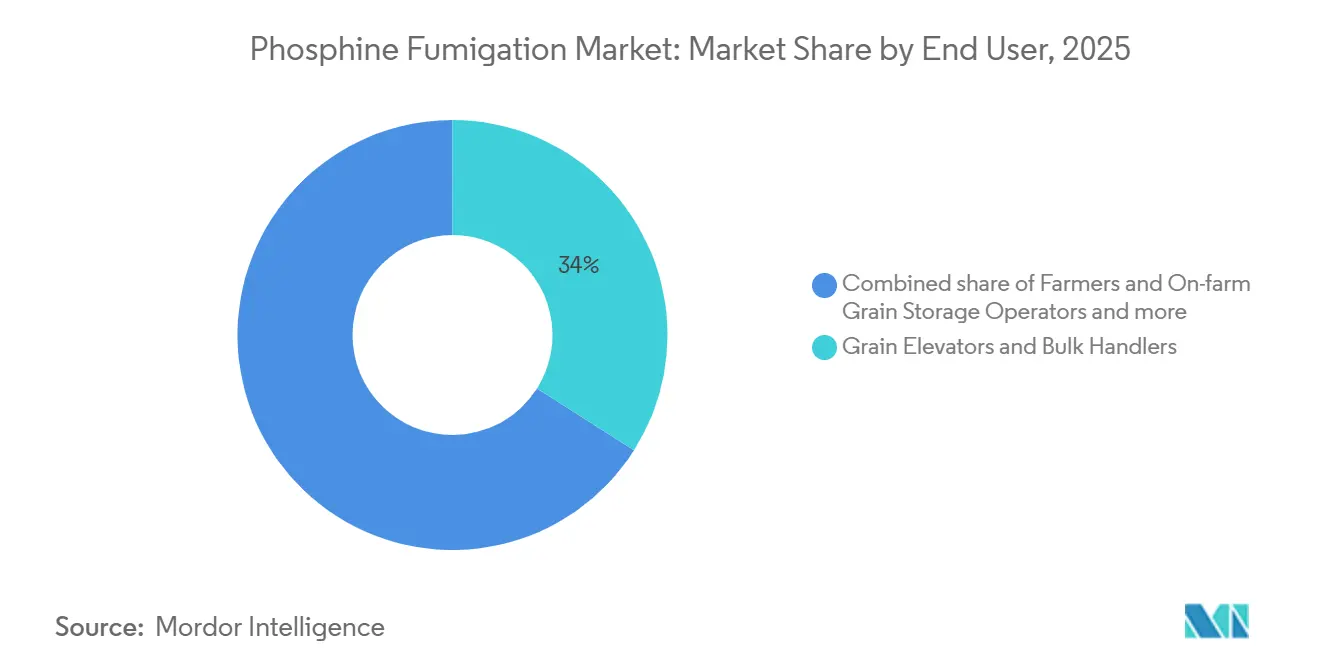

- By end user, grain elevators and bulk handlers were the largest segment with 34% of the phosphine fumigation market share in 2025, while agricultural exporters and quarantine service providers were the fastest segment registering 6.13% CAGR during 2026-2031.

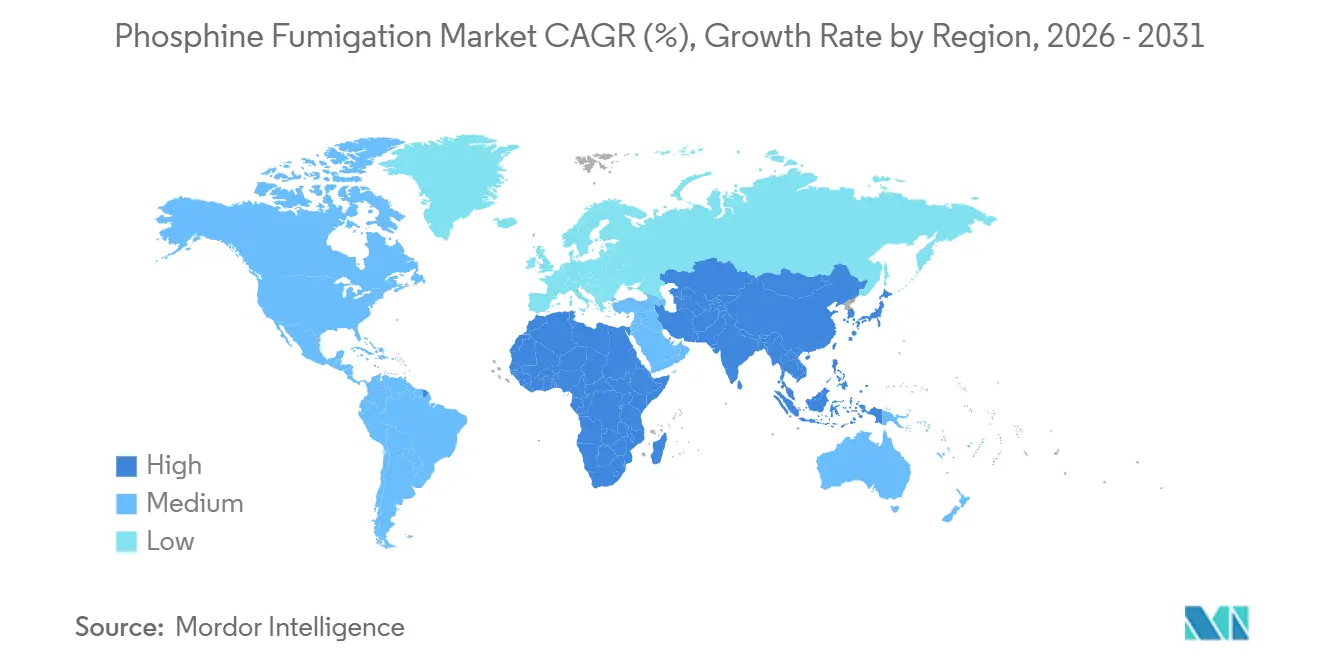

- By geography, North America held the largest share, accounting for 35.8% of the phosphine fumigation market share in 2025, while Asia-Pacific registered the fastest at 6.8% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Phosphine Fumigation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of grain silo and bulk commodity storage capacity | +1.2% | Global, with the highest intensity in India, China, Brazil, Egypt, and Saudi Arabia | Medium term (2-4 years) |

| Tighter phytosanitary compliance for grain and oilseed exports | +1.0% | Global, with the highest impact in North America, Asia-Pacific, and South America | Short term (≤ 2 years) |

| Ongoing methyl bromide substitution in agricultural quarantine treatments | +0.9% | Global, with early gains in North America, the European Union, Japan, and Australia | Short term (≤ 2 years) |

| Rising need to reduce post-harvest losses in cereals, pulses, and oilseeds | +0.8% | Asia-Pacific core, with spillover to Africa and the Middle East | Medium term (2-4 years) |

| Adoption of cylinderized phosphine, recirculation, and digital gas monitoring in grain storage | +0.5% | North America, Australia, Germany, Saudi Arabia, and organized storage in Asia | Medium term (2-4 years) to Long term (≥ 4 years) |

| Professionalization of on-farm fumigation programs and grain quality assurance workflows | +0.3% | Australia, North America, Brazil, Germany, and early-stage South and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Grain Silo and Bulk Commodity Storage Capacity

The expansion of silo and bulk storage capacity directly drives the demand for phosphine fumigation by increasing the need for regular inventory protection. New grain elevators, reserve facilities, and centralized warehouses require consistent treatment cycles to ensure long-term storage safety. This trend is critical in regions focusing on food security and transitioning to organized storage systems. The Food and Agriculture Organization of the United Nations (FAO) highlights storage infrastructure as vital for food system resilience, further validating the need for professional fumigation. Moreover, the adoption of tighter sealing standards in new facilities enhances the use of cylinderized gas and monitored application methods, strengthening the phosphine fumigation market.

Tighter Phytosanitary Compliance for Grain and Oilseed Exports

Stricter phytosanitary compliance is driving the need for certified treatment in the phosphine fumigation market. Importing countries now require detailed documentation, skilled operators, and proof of adherence to established procedures. The International Plant Protection Convention (IPPC) sets the standards for fumigation as a phytosanitary measure, ensuring consistency in international trade. The United States Department of Agriculture (USDA) Agricultural Marketing Service enforces these standards through its fumigation handbook, with non-compliance leading to re-treatment, delays, or cargo rejection. As a result, phosphine fumigation has become an essential and routine requirement in trade flows, reinforcing stable market demand.

Ongoing Methyl Bromide Substitution in Agricultural Quarantine Treatments

The phase-out of methyl bromide in quarantine and pre-shipment treatments is driving growth in the phosphine fumigation market. As of 2024, the United Nations Environment Program Ozone Secretariat reports that 97.5% of methyl bromide consumption among Montreal Protocol restricted to Quarantine and Pre-shipment (QPS) applications. These applications are used to treat commodities to prevent the spread of pests and to meet official phytosanitary trade requirements, underscoring its declining use[1]Source: United Nations Environment Programme Ozone Secretariat, “Quarantine and Pre-Shipment,” United Nations Environment Programme Ozone Secretariat, ozone.unep.org. Further restrictions are likely to shift treatment volumes toward phosphine, particularly in durable-commodity trade. Australia's 2025 update to its methyl bromide methodology reflects a global push for standardized practices in cross-border treatments. This ongoing transition positions the phosphine fumigation market to benefit significantly, especially in large grain storage, bulk transit, and warehouse operations that already comply with formal regulations.

Rising Need to Reduce Post-Harvest Losses in Cereals, Pulses, and Oilseeds

The need to minimize post-harvest losses directly ties the phosphine fumigation market to food availability and storage efficiency. The FAO reports that 13.2% of global food production is lost post-harvest but before retail, emphasizing the importance of effective storage protection[2]Source: Food and Agriculture Organization of the United Nations, “The State of Food Security and Nutrition in the World 2025,” Food and Agriculture Organization of the United Nations, fao.org. In Sub-Saharan Africa, storage losses for cereals and pulses can reach 22%, making insect control crucial even in regions with limited farm margins. Furthermore, the FAO highlighted in 2025 that storage investments are essential for reducing food price shocks and strengthening food systems. This underscores the phosphine fumigation market's critical role in ensuring reliable insect control for both private grain handling and public storage programs, ultimately supporting global food security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent operator exposure, certification, and fumigation documentation requirements | -0.8% | North America, core European Union markets, Australia, and organized markets in Asia | Short term (≤ 2 years) to Medium term (2-4 years) |

| Rising phosphine resistance in major stored grain and seed pests | -0.7% | Australia, India, Brazil, the United States, Greece, Turkey, and a wider global spread | Medium term (2-4 years) to Long term (≥ 4 years) |

| Hermetic storage and non-chemical grain protection alternatives reducing treatment frequency | -0.5% | India, Niger, Kenya, Nigeria, Bangladesh, and early-stage South and Southeast Asia | Long term (≥ 4 years) |

| Organic and residue-sensitive agricultural channels limiting fumigant use | -0.3% | North America, the European Union, Australia, and premium organic trade corridors | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Operator Exposure, Certification, and Fumigation Documentation Requirements

The phosphine fumigation market is constrained by strict worker exposure regulations and licensing requirements, such as those under Title 40 Code of Federal Regulations Part 171 in the United States, which mandate training, record-keeping, and supervision[3]Source: Electronic Code of Federal Regulations, “40 CFR Part 171 Subpart B, Certification of Pesticide Applicators,” Electronic Code of Federal Regulations, ecfr.gov. Similarly, Germany enforces strict oversight, with 109 cases of aluminum phosphide poisoning reported by the Federal Institute for Risk Assessment between 2022 and 2024. These regulations increase compliance costs and reduce the availability of certified workers during seasonal peaks in grain handling, ultimately slowing market growth in regulated regions despite rising demand.

Rising Phosphine Resistance in Major Stored Grain and Seed Pests

Phosphine resistance is an escalating concern for the fumigation market. A 2024 study published in the Journal of Pest Science by the Federal University of Viçosa (Universidade Federal de Viçosa) in Brazil found that 73% of tested populations across 13 stored-product insect species exhibited resistance. A 2025 North American study titled Geographic Distribution of Phosphine Resistance and Frequency of Resistance Genes in Two Species of Grain Beetles, Tribolium castaneum and Rhyzopertha dominica, in North America, supported by federal agricultural programs in the United States, reported resistance frequencies as high as 97% in certain grain facilities for Rhyzopertha dominica and Tribolium castaneum, driven by fumigation selection pressure. Similarly, a 2024 study titled Assessment of Phosphine Resistance in Major Stored-Product Insects in Greece Using Two Diagnostic Protocols revealed that 43.3% of 53 field populations were resistant, with some Tribolium confusum populations showing extreme resistance. These findings emphasize the urgent need for enhanced exposure times, stricter monitoring, and improved sealing practices, which are critical to mitigating resistance and ensuring the effectiveness of phosphine fumigation treatments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aluminum Phosphide Retains Structural Dominance as Magnesium Phosphide Gains Momentum

Aluminum phosphide, held the largest share of 54% of the phosphine fumigation market in 2025, remains the dominant product due to its low cost, regulatory acceptance, and ease of handling in various storage environments. Its widespread use in farm-level storage, commercial warehouses, and port-linked grain facilities ensures minimal replacement risk, while operator familiarity with its long-standing application further solidifies its position.

Magnesium phosphide, with a projected CAGR of 5.95% during 2026-2031, is gaining momentum as it addresses the need for short turnaround times in container fumigation and quarantine operations. While calcium phosphide serves niche applications, the market continues to rely on aluminum phosphide for high-volume usage. Supporting this trend, a 2025 study in Agriculture highlighted the Phosphine Tolerance Test by Detia Freyberg GmbH as a key tool for early detection of resistance in major beetle species. This diagnostic advancement strengthens the industry's ability to optimize phosphine use, ensuring established products like Aluminum Phosphide remain integral to market stability and growth.

By Form: Solid Formulations Lead Volume as Gas and Powder Formats Serve Evolving Needs

Solid formulations held the largest share and accounted for 59.2% of the phosphine fumigation market share in 2025, maintaining their lead due to ease of use, efficient distribution, and low capital requirements for treatment setups. This position is also reinforced by established grain storage standards such as China’s LS/T 1201-2020 and Germany’s TRGS 512, which continue to support the routine use of tablets and pellets. Liquid formulations are the fastest-growing segment, projected to expand at a 6.2% CAGR during 2026-2031, as storage operators increasingly value controlled phosphine release, cleaner treatment processes, and stronger compliance performance in audited food-grade facilities.

The remaining share of the form segment comes from powder formulations, which serve a smaller but still relevant role in the market. These products are mainly used in surface dusting and in structural penetration areas where tablets or liquid systems are harder to place effectively, including flat warehouse floors and narrow equipment voids. Their use remains more specialized because they address treatment needs that are limited to certain storage layouts and equipment conditions. As the market evolves, this structure shows that while solid products still anchor volume demand and liquid systems capture the fastest growth, powders continue to support specific operational gaps that other formats do not fully address.

By Crop Type: Cereals and Grains Hold the Core Demand Base Across Stored Commodities

Cereals and grains held the largest share and occupied 63% of the phosphine fumigation market share in 2025, driven by their storage in national reserves, commercial silos, and export channels requiring consistent insect control over long cycles. This dominance underscores the critical role of phosphine fumigation in preserving staple grains like wheat, rice, corn, barley, and sorghum. Simultaneously, the commercial produce and plantation segment, projected to grow at a 5.9% CAGR during 2026-2031, highlights the market's shift toward protecting higher-value crops during storage and shipment. Together, these trends reflect the market's expansion from bulk grain storage to value-sensitive crop categories.

Other segments, including oilseeds, pulses and legumes, and seeds for planting, further diversify the demand base. Oilseeds drive steady demand due to large export volumes and extended storage needs, while pulses and legumes require fumigation to prevent rapid value loss from insect damage, even in smaller storage lots. Seeds for planting, though a smaller segment, demand premium fumigation solutions to meet strict quality and phytosanitary standards. Collectively, these interlinked dynamics emphasize the growing importance of phosphine fumigation across diverse crop types, ensuring quality and economic value throughout storage and trade systems.

By Storage Structure: Commercial Grain Elevators Lead Revenue as In-transit Structures Expand Faster

Commercial bulk silos, held the largest share with 36.67% of the phosphine fumigation market share in 2025, are central to national grain movement due to their ability to handle large, recurring volumes. Their high treatment value per site and role in monitored gas delivery, recirculation, and formal documentation make them a critical revenue driver compared to smaller farm structures. Export containers, projected to grow at a 6.5% CAGR during 2026-2031, highlight the increasing integration of fumigation into trade compliance for cargo in transit.

Detia Degesch Group’s 2025 acquisition of Fumico Holding B.V. and DDD, d.o.o. Koper enhanced service capabilities in major European ports, reflecting this shift. While farm silos and grain bins contribute to volume, their lower treatment value and dispersed service delivery reduce their impact. The market is increasingly consolidating around transit structures and port-linked assets, driven by the formalization of export logistics and the emergence of higher-value opportunities in these segments.

By End User: Grain Elevators and Bulk Handlers Lead Revenue While Export-linked Services Expand Faster

Grain elevators and bulk handlers held the largest share with 34% of the phosphine fumigation market share in 2025, driven by their pivotal role in managing large grain volumes within commercial supply chains requiring frequent fumigation. Meanwhile, agricultural exporters and quarantine service providers, projected to grow at a 6.13% CAGR during 2026-2031, highlight the rising demand for certified treatments in export logistics, border compliance, and pre-shipment handling. This shift underscores the growing emphasis on organized and compliant storage solutions across the supply chain.

Farmers and on-farm storage operators contribute significant volume but have lower treatment value per account than commercial networks. Agri-warehousing and Commodity Storage Companies are gaining traction as emerging markets transition to structured storage infrastructure. Seed Companies and Seed Processing Facilities, though smaller, represent a high-value segment in which precision and compliance are critical to product quality and trade acceptance. Together, these trends point to a market increasingly focused on efficiency, compliance, and quality across all end-user segments.

Geography Analysis

In 2025, North America held 35.8% of the phosphine fumigation market share, driven by the United States, where flat storage, cylindrical bins, and terminal silos support large recurring treatment volumes. The United States also operates under strict applicator certification and fumigation procedure rules, which sustain demand for specialized service providers and higher-control gas delivery formats. Canada remains a stable secondary center where conventional treatment still performs well under lower historical resistance pressure. Mexico adds steady demand as phytosanitary treatment certification gains importance in formal grain handling and warehouse operations

Asia-Pacific, the fastest-growing region with a projected CAGR of 6.8% during 2026-2031, leads global volumes due to expanding organized storage and formalized treatment practices in India, China, and Southeast Asia. To enforce strict national biosecurity and combat rising pest resistance, China’s state grain reserve corporation, Sinograin, modernized its digital infrastructure across 900 depots in late 2024, standardizing automated, closed-loop phosphine fumigation and real-time gas monitoring, highlight its significance. Australia, despite its professionalized market, faces challenges with resistance, while Southeast Asia's growing warehousing infrastructure supports the reliable handling of agricultural exports.

Europe and Africa are projected to grow steadily during 2026-2031, with Europe emphasizing compliance-driven professional services and Africa benefiting from food security initiatives and storage upgrades. The Middle East adds to this trend by strengthening import storage systems, while South America, led by Brazil and Argentina, remains vital for recurring fumigation in large grain and oilseed storage networks. Together, these regions underscore the global shift toward organized storage and advanced fumigation practices to meet evolving regulatory and operational demands.

Competitive Landscape

The phosphine fumigation market in 2025 was moderately concentrated, with the top five players, UPL Limited, Detia Freyberg GmbH (Detia Degesch Group), Syensqo SA, Nippon Chemical Industrial Co., Ltd., and Sumitomo Chemical Company Limited, holding a significant share. Their dominance stems from technical expertise and regulatory capacity in phosphine production, registration, and stewardship, which create high entry barriers for smaller players. Customers demand not only products but also training, support, and guidance, further favoring established companies. UPL Limited, leveraging its UPL SAS distribution platform, focuses on grain-protectant fumigants to address tropical storage pest challenges, highlighting the strategic importance of combining manufacturing capabilities with field support and compliance expertise.

Competition is shaped by the interplay between product manufacturers and specialist service providers. Manufacturers benefit from registered formulations and distribution networks, while service providers excel in local execution, certified operations, and record quality. Detia Degesch Group expanded its service reach in Rotterdam, Amsterdam, and Koper through acquisitions of two specialized subsidiaries from the Belgian INTRESO Group BV including Fumico Holdings B.V. (Fumico) and DDD, d.o.o. Koper (DDD) in 2025, where the Fumico Holdings B.V. (Fumico) includes pest control service, while Rentokil enhanced its presence in Indonesia and Singapore through strategic acquisitions of Kilem Pest in 2026. These moves underline the growing importance of service networks and customer access over mere formulation ownership, emphasizing the need for integrated solutions.

As the market evolves, monitoring, resistance management, and integrated storage site support are becoming critical differentiators. Companies offering solutions for gas concentration management, treatment discipline, and resistance mitigation are better positioned than those competing solely on price. A 2025 Agriculture study on the Phosphine Tolerance Test highlights the value of faster resistance screening in improving treatment decisions. Rentokil Initial’s establishment of the Rentokil Terminix Innovation Center in Dallas in 2024 further underscores the shift toward sustainable fumigation and data-driven pest control. The market increasingly rewards firms that integrate chemical expertise, service execution, and data-led support, driving a convergence of capabilities toward comprehensive customer solutions.

Phosphine Fumigation Industry Leaders

UPL Limited

Detia Freyberg GmbH (Detia Degesch Group)

Syensqo SA

Nippon Chemical Industrial Co., Ltd.

Sumitomo Chemical Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Rentokil Initial plc acquaired Killem Pest, a Singapore-based pest control specialist, enhancing Rentokil's commercial pest control operations in Singapore. This integration strengthens Rentokil's position in the high-compliance Asia-Pacific market by combining Killem's local expertise with Rentokil's global research resources, advanced digital monitoring systems, and standardized fumigation protocols. It ensures better adherence to stringent phytosanitary regulations, particularly for phosphine fumigation of imported commodities and warehoused food products.

- September 2025: Detia Degesch Group's acquisition of Fumico Holding B.V. (Netherlands) and DDD, d.o.o. Koper (Slovenia) from INTRESO Group BV consolidates its fumigation services at key European ports, including Rotterdam, Amsterdam, and Koper. By integrating CO2 low-pressure and heat-treatment methods with phosphine, the company advances sustainable, residue-free fumigation solutions for international commodity trade, marking a pivotal shift in European port fumigation ownership.

- May 2025: Rentokil Initial Indonesia acquired Pest Terminator, a commercial pest control company operating in Bali, Surabaya, Semarang, and nearby regions. This acquisition strengthens Rentokil's presence in Indonesia, a key growth market for grain import fumigation and food manufacturing site treatments, while adding 200 employees to its regional operations.

Global Phosphine Fumigation Market Report Scope

Phosphine fumigation is the application of phosphine gas generated from metal phosphides or supplied in cylinderized blends to eliminate insects and other pests in sealed environments such as grain silos, warehouses, shipping containers, and quarantine facilities. It preserves commodity quality, safeguards food security, and supports uninterrupted trade by meeting phytosanitary and residue-limit standards while operating at ambient temperature and leaving negligible chemical residues. The phosphine fumigation market report is segmented by product type (aluminum phosphide, magnesium phosphide, and calcium phosphide), by form (solid, liquid, and powder), by crop type (cereals and grains, oilseeds, pulses and legumes, and commercial crops and plantation produce), by storage structure (farm silos and grain bins, commercial bulk silos, flat warehouses and bagged commodity stores, bunkers and temporary grain storage systems, and export containers), by end-user (agriculture, food processing, shipping, and storage), and by Geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market forecasts for all segments are provided in Value (USD).

| Aluminum Phosphide |

| Magnesium Phosphide |

| Calcium Phosphide |

| Solid |

| Liquide |

| Powder |

| Cereals and Grains |

| Oilseeds |

| Pulses and Legumes |

| Commercial Crops and Plantation Produce |

| Farm Silos and Grain Bins |

| Commercial Bulk Silos |

| Flat Warehouses and Bagged Commodity Stores |

| Bunkers and Temporary Grain Storage Systems |

| Export Containers |

| On-farm Grain Storage Operators |

| Grain Elevators and Bulk Handlers |

| Agri-warehousing and Commodity Storage Companies |

| Seed Companies and Seed Processing Facilities |

| Agricultural Exporters and Quarantine Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Aluminum Phosphide | |

| Magnesium Phosphide | ||

| Calcium Phosphide | ||

| By Form | Solid | |

| Liquide | ||

| Powder | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds | ||

| Pulses and Legumes | ||

| Commercial Crops and Plantation Produce | ||

| By Storage Structure | Farm Silos and Grain Bins | |

| Commercial Bulk Silos | ||

| Flat Warehouses and Bagged Commodity Stores | ||

| Bunkers and Temporary Grain Storage Systems | ||

| Export Containers | ||

| By End User | On-farm Grain Storage Operators | |

| Grain Elevators and Bulk Handlers | ||

| Agri-warehousing and Commodity Storage Companies | ||

| Seed Companies and Seed Processing Facilities | ||

| Agricultural Exporters and Quarantine Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the phosphine fumigation market by 2031?

The phosphine fumigation market is projected to reach USD 2.53 billion by 2031.

Which form leads the current demand in phosphine fumigation market?

Solid was the largest form, with a 59.2% share in 2025.

Which region is growing the fastest for phosphine-based treatment?

Asia-Pacific is the fastest regional segment with a 6.8% CAGR during 2026-2031, supported by organized storage growth and stronger compliance-driven treatment needs.

Why does phosphine still hold a strong position in bulk grain protection?

It remains difficult to replace because it penetrates dense grain stacks, controls pests across life stages, and clears without food-grade residue after ventilation.

How concentrated is competition among leading suppliers and service providers?

The top 5 companies accounted for dominant share of revenues in 2025, indicating a moderately concentrated market with high entry barriers and strong advantages for established operators.

Page last updated on: