Magnet Wire Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 38.51 Billion |

| Market Size (2031) | USD 49.27 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

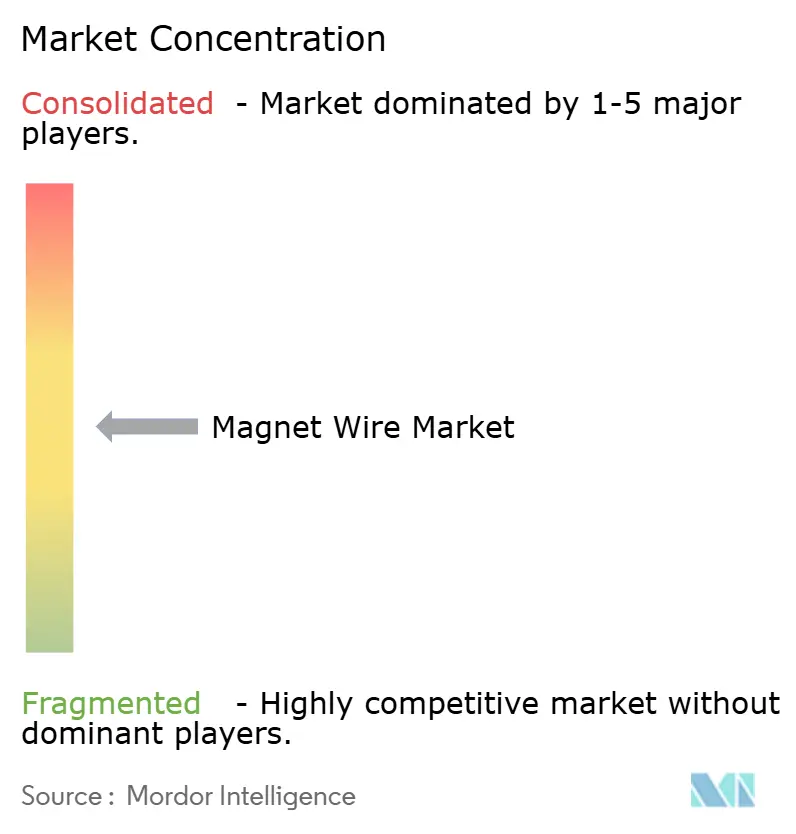

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnet Wire Market Analysis by Mordor Intelligence

The Magnet Wire Market size is expected to increase from USD 36.66 billion in 2025 to USD 38.51 billion in 2026 and reach USD 49.27 billion by 2031, growing at a CAGR of 5.05% over 2026-2031. Electrified transportation, renewable-heavy grids, and factory-automation upgrades are aligning to sustain mid-single-digit revenue growth even as design shifts trim copper volume per unit. Automakers continue replacing round conductors with hairpin-style rectangular wire to raise slot-fill density, a move that keeps kilogram pricing healthy despite material thrift. Utilities are upgrading high-voltage transformers to IEC 60317-compliant thermal classes, favoring enamel coats that tolerate 180-240°C winding temperatures. Meanwhile, copper price volatility within a 20-25% band challenges producers without hedging programs, and early adoption of PCB stators signals a future headwind in sub-10 kW motors. Suppliers able to certify recycled-content copper under The Copper Mark and to reclaim mill scrap are defending margins and winning long-term bids.

Key Report Takeaways

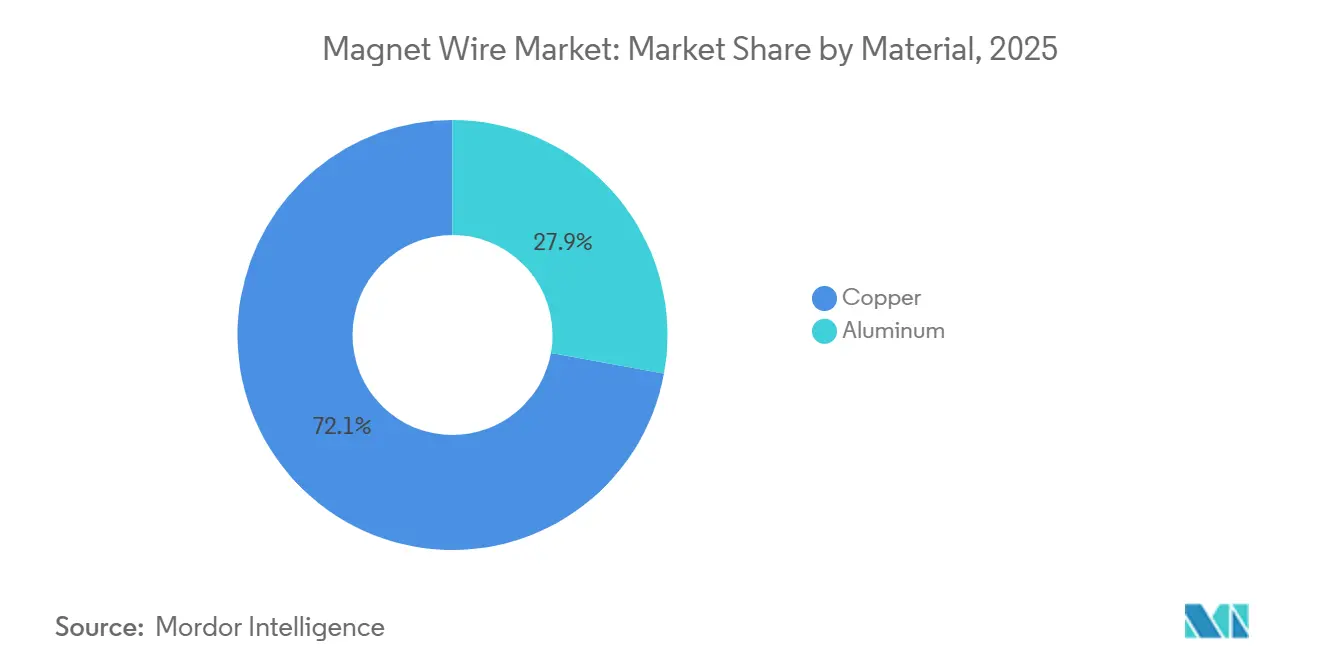

- By material, copper led with 72.13% of the magnet wire market share in 2025 and also posted the fastest 5.45% CAGR outlook to 2031.

- By insulation type, enameled wire accounted for 94.04% of 2025 revenue and is projected to expand at a 5.10% CAGR through 2031.

- By shape type, the round type accounted for the largest market share of 64.87% in 2025; however, the rectangular or flat type is poised to grow at a CAGR of 5.38% during the forecast period (2026-2031).

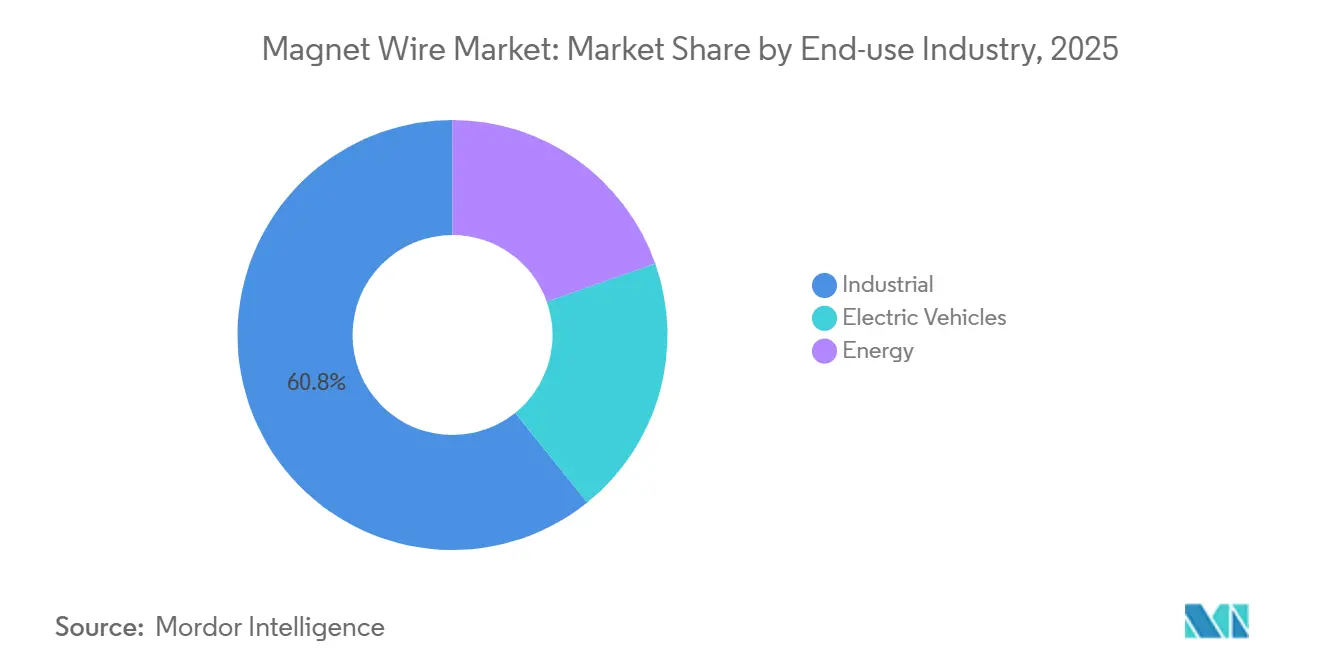

- By end-user industry, industrial had a revenue share of 60.78% in 2025, and the share of electric vehicles is poised to grow with a CAGR of 7.29% during the forecast period (2026-2031).

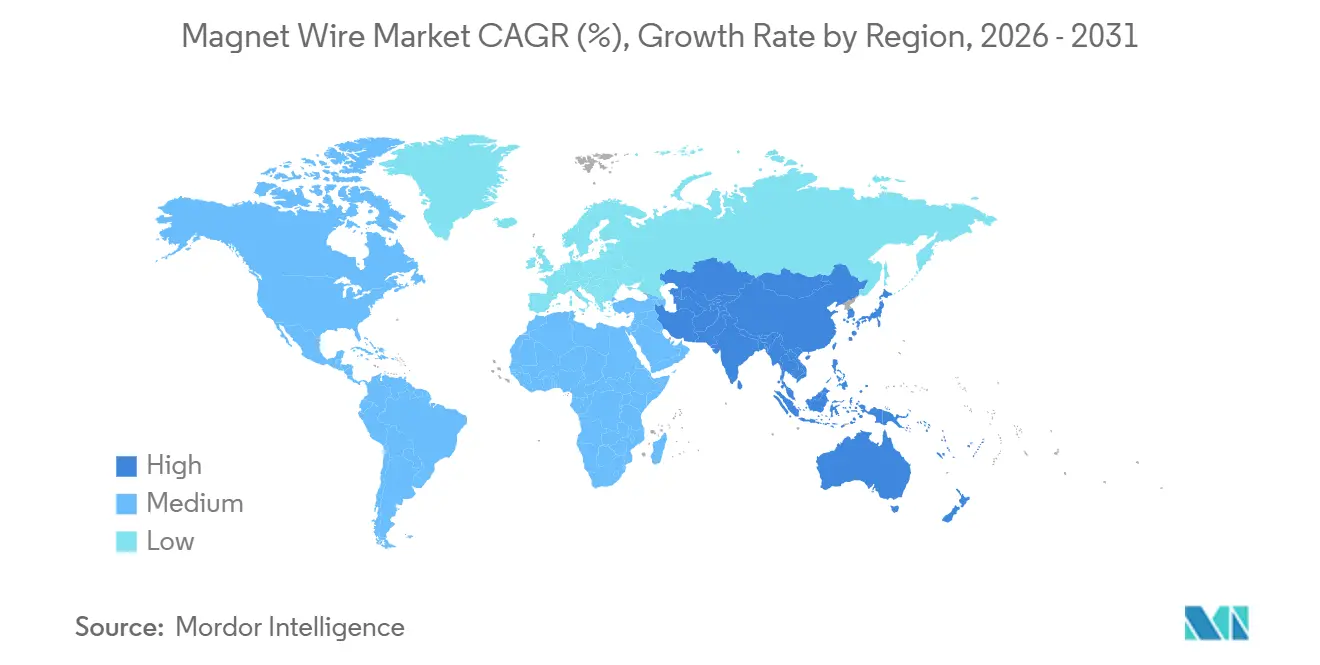

- By geography, Asia-Pacific commanded 59.15% of 2025 revenue and is on track for the quickest 6.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Magnet Wire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging electric-vehicle production | +1.8% | China, India, South Korea, spill-over to Europe | Medium term (2-4 years) |

| Expanding renewable-energy installations | +1.3% | North America, Europe, China | Long term (≥ 4 years) |

| Growing consumer-electronics output | +0.6% | China, South Korea, Vietnam, United States | Short term (≤ 2 years) |

| Rapid industrial automation and motor upgrades | +0.9% | United States, Germany, Japan | Medium term (2-4 years) |

| Demand for distributed wind micro-generators | +0.3% | Rural United States, Canada, Nordic Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Electric-Vehicle Production

First-half 2025 Chinese registrations hit 5.62 million units, lifting the national NEV fleet to 36.89 million vehicles and translating to 16,000-27,000 t of new rectangular wire demand in a single semester. India’s INR 25,938 crore PLI-Auto program requires 50% domestic value addition, prompting local traction-motor winding lines. Sumitomo Electric logged JPY 228.2 billion magnet-wire revenue in FY 2024, up 13.2%, after expanding rectangular capacity at EV hubs. Hairpin architectures elevate slot-fill density to 70-80% from the legacy 50-60%, boosting kilogram pricing despite lower conductor volume per motor. Japan’s February 2025 Green Growth Strategy commits JPY 150 trillion over 10 years, underpinning regional demand for high-grade copper conductors.

Expanding Renewable-Energy Installations

The International Energy Agency expects annual transmission-grid investment to exceed USD 200 billion by the mid-2030s, up from USD 140 billion in 2023[1]International Energy Agency, “World Energy Investment 2025,” iea.org. Every gigawatt of offshore wind needs about 200-300 t of magnet wire for step-up transformers and cable terminations, creating an outsized pull for enamel-coated copper. Siemens Energy agreed in September 2024 to shift entirely to Copper-Mark-certified recycled copper for transformers, an early proof that utilities will pay traceability premiums. China’s State Grid aims for 28 million EV chargers by 2027, each relying on 100-500 kVA distribution transformers that together will consume 40,000-60,000 t of enamel wire yearly. Faster permitting under the U.S. Inflation Reduction Act and the EU’s REPowerEU shortens the lag between wind-farm commissioning and transformer procurement.

Growing Consumer-Electronics Output

The US motor-efficiency rule announced in June 2023 requires 100-250 hp motors to meet IE4 by June 2027, a shift saving 3 quads of energy and avoiding 91.69 million t of CO₂ across three decades. ABB shows rectangular conductors can cut I²R losses by up to 12% at equal current, justifying their 15-20% price premium. Fujikura is scaling lines that hold ±2 µm coating tolerance on flat wire meant for IE4-compliant drives, spending part of its JPY 979.4 billion FY 2024 revenue on the upgrade. Proterial shipped 750,000 xEV magnet units in FY 2023 and is co-developing ferrite machines above 100 kW, pairing alternatives to heavy-rare-earth magnets with high-density copper windings. JCMA’s 116-member magnet-wire committee is coordinating common test methods so discrete suppliers can slot seamlessly into multinational OEM bills of material.

Demand for Distributed Wind Micro-Generators

DOE defines distributed wind as turbines below 100 kW near the consumption point, each embedding 20-50 kg of copper windings. IRENA identifies up to 250 GW of diesel-hybrid mini-grid retrofit potential, implying 5,000-8,000 t of extra enamel wire yearly for converters alone. IEC 60317 Class H and Class C coatings allow lighter, faster-spinning alternators that trim tower load by double-digit percentages, an edge in remote sites where crane cost dominates. Rural tenders in Sub-Saharan Africa now require ISO 9001 traceability plus disclosure of copper origin, favoring suppliers already certified under The Copper Mark. Mandates for Class F or higher insulation in India’s national small-wind standard took effect in April 2025, widening the addressable enamel-wire pool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.5% | Global, acute in Europe and India | Short term (≤ 2 years) |

| PCB stator technology replacing wound coils | -0.2% | North America, Europe | Medium term (2-4 years) |

| Compact axial-flux motors reducing wire usage | -0.2% | Europe, North America, Global premium EVs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

J.P. Morgan sees copper averaging USD 12,075/t in 2026 on a 330,000 t deficit, whereas the World Bank pegs 2025 prices closer to USD 9,700/t, framing a 20-25% swing that can eliminate producer gross margin when not hedged. IMF data show an 8.1% rally between February and August 2024, forcing quarterly escalator clauses into long-term wire contracts. Aluminum remains 39% lighter than copper at equivalent conductivity, yet faces bauxite mining caps in Guinea and elevated European smelting power tariffs, trimming its headline pricing advantage. Polyamide-imide and polyesterimide enamels rely on petrochemical feedstocks, exposing insulation costs to Brent crude volatility and periodic force-majeure events at resin plants.

PCB Stator Technology Replacing Wound Coils

Infinitum Electric’s air-core motor replaces bulk windings with etched copper on multilayer PCBs, cutting motor mass by up to 65% in HVAC fans and pump drives. Commercial deployments remain under 2% of world motor shipments, but at volumes above 50,000 units per year, automated PCB lines reach cost parity with enamel wire plus labor, framing a credible threat in sub-10 kW frames. Traditional suppliers are offsetting risk by launching ultra-thin 0.18 mm wires that approach PCB slot-fill density while retaining coil flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Copper Maintains Lead while Aluminum Plays the Weight Card

Copper accounted for 72.13% of the magnet wire market size at USD 27.8 billion in 2025 and is forecast to expand at a 5.45% CAGR to 2031[2]Sumitomo Electric Industries, “Annual Report 2024,” global-sei.com. The magnet wire market share held by aluminum benefits from a 39% lower density that appeals to space-constrained windings in aircraft actuators and long-span overhead lines. Sumitomo Electric’s FY 2024 surge reflects EV hairpin demand, while Essex Furukawa’s closed-loop model recovered 43,000 t of copper scrap, an advantage in regions that reward recycled content. Copper-clad aluminum trials continue in appliance compressors, but vibration-fatigue concerns impede large-scale automotive take-up. Certification programs like The Copper Mark elevate transparency expectations that many primary aluminum smelters have yet to match.

Pricing dynamics remain the decisive lever. J.P. Morgan’s USD 12,075/t 2026 forecast drives OEM hedging, whereas the World Bank’s softer USD 9,700/t 2025 view offers breathing room for spot buyers. Producers with integrated rod mills lock cost faster than toll-drawers, preserving EBIT margins when quotes spike. In parallel, aluminum faces power-price uncertainty: European smelters idled 500,000 t annual capacity in early 2025 after gas benchmarks climbed, complicating supply planning for wire buyers.

By Insulation Type: Enameled Wire Retains Thermal Supremacy

Enameled products captured 94.04% of 2025 revenue thanks to thin polyamide-imide and polyesterimide coats that hit Class H and Class C ratings demanded by EV traction motors and HV transformers. Covered wire serves tap-changer and repair coils but suffers a 20-30% slot-fill penalty that limits uptake in compact frames. Fujikura invested in precision nozzles capable of ±2 µm enamel uniformity on rectangular wire, preserving dielectric strength at sharp corners. Tightening IE4 motor rules in June 2027 boosts demand for higher-temperature grades able to run hotter without derating, further consolidating enamel’s position.

Resin feedstock volatility poses the main risk. Polyamide-imide monomers track crude-oil swings, evidenced when Brent gained 19% between July and October 2025, lifting enamel costs by mid-single digits. Suppliers are adopting bio-sourced diacids to cut Scope 3 emissions, a strategy that also cushions against petrochemical price shocks. JCMA test protocols now include partial discharge and corona endurance on rectangular edges to guarantee long-cycle life in high-frequency inverters.

By Shape: Rectangular Conductors Narrow the Gap

Round wire still produced 64.87% of 2025 revenue, anchored in legacy industrial motors and utility transformers whose machinery wraps best with flexible conductors. Rectangular formats, though, are growing at a 5.38% CAGR to 2031 as EVs and IE4 motors chase higher packing factors. ABB quantifies an 8-12% I²R drop when optimized cross-sections replace round strands inside identical slot volumes, an energy-savings ratio that OEMs monetize in range or label-rating uplift.

Manufacturing complexity grows: sharp-edged strips need thicker enamel on corners, forcing slower line speeds and higher reject rates until process capability stabilizes. Sumitomo Electric’s new Indonesian plant will run vision systems that check edge defectivity at 2,000 fps, a guardrail for zero-ppm targets in automotive supply chains. Round wire remains unrivaled for tight-radius coils used in relay solenoids, speaker voice coils, and miniature SMPS transformers where bend radii drop under 1.5 D.

By End-use Industry: Industrial Base Dominates but EVs Accelerate

Industrial motors generated 60.78% of 2025 revenue on steady OEM and retrofit demand, especially as factories upgrade to IE4 efficiency ahead of the 2027 deadline. The electric-vehicle slice, however, is the fastest climber at a 7.29% CAGR, adding more than 16,000 t of wire in China alone during the first half of 2025. The magnet wire market size uplift in EV traction motors outpaces combating copper thrift through hairpin geometry, keeping dollar growth intact.

Power transformers tied to offshore wind stand next in growth ranking. Each GW of installed capacity pulls 200-300 t of rectangular wire for step-up units and subsea termination coils. Consumer electronics, while lower tonnage, deliver resilient margins through fine-gauge, high-frequency enamel wire for GaN-based chargers and data-center PSUs.

Geography Analysis

Asia-Pacific anchored 59.15% of 2025 revenue, expanding at a robust 6.07% CAGR through 2031. China’s MIIT target of 15.5 million NEV sales in 2025 and State Grid’s 28 million EV-charger plan embed structural demand for both traction-motor and distribution-transformer windings. India’s PLI-Auto, PM E-DRIVE, and ACC battery incentives worth a combined INR 54,938 crore favor local wire procurement, boosting line installations in Gujarat and Tamil Nadu. Japan’s JPY 150 trillion Green Growth Strategy routes capital toward offshore wind and electrified drivetrains, sustaining demand for premium rectangular conductors. South Korea’s LS Cable & System expects its LS Eco Energy affiliate to reach USD 1.3 billion in revenue by 2030, partly through U.S. magnet-wire investments that qualify for IRA domestic-content credits.

North America shows steady replacement demand as the IE4 rule phases in and as the Inflation Reduction Act accelerates HVDC and storage projects. Essex Solutions’ USD 200 million pre-IPO raise and planned 2025 listing at USD 1.4 billion value reflect this outlook. Utilities now specify Copper-Mark-certified wire, positioning recyclers ahead of primary-copper users.

Europe trails slightly in tonnage yet leads in sustainability mandates. Siemens Energy’s 100% recycled-copper sourcing sets a procurement template likely to spread across grid operators. The REPowerEU plan is fast-tracking grid permits, lifting enamel-wire call-offs for transformer OEMs in Germany and Spain. South America benefits from Brazil’s wind boom, and the Middle East records magnet-wire spikes tied to Saudi Arabia’s NEOM builds. Africa remains small but growing where distributed wind and mini-grids replace diesel.

Competitive Landscape

The Magnet Wire market is moderately consolidated. Technology collaboration is intensifying. Proterial’s ferrite motor prototype banks on rectangular conductors to compensate for lower magnet remanence, locking in supply contracts for 2027 series production. Smaller contenders such as Tretau leverage first US plants in Indiana to qualify under domestic-content clauses, broadening customer access. Traceable recycled content has become a decisive buyer screen. Essex Furukawa documented 43,000 t of scrap reclaimed in FY 2024 and won Copper-Mark accreditation, while Siemens Energy signed a multiyear pact for closed-loop copper, both moves that embed price premiums into transformer bids.

Magnet Wire Industry Leaders

LS Cable & System Ltd.

Sumitomo Electric Industries, Ltd.

Superior Essex Inc.

Tongling Jingda Special Magnet Wire Co., Ltd

Rea

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tretau, a global magnet wire producer, announced plans to establish its first manufacturing facility outside Europe, choosing Fort Wayne, Indiana, United States, as its location. The move aims to bolster the company's service to local OEMs in sectors like electric vehicles, renewable energy, and advanced manufacturing.

- December 2025: LS Cable & System was evaluating the production of rectangular magnet wire and copper materials in the United States. Currently, LS Cable & System supplies rectangular magnet wire to automotive giants GM and Hyundai Motor.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the magnet wire market as revenue from newly manufactured copper or aluminum conductors that carry a thin insulation film and are wound into coils for motors, transformers, inductors, generators, loudspeakers, and similar electromagnetic devices. According to Mordor Intelligence, the scope tracks sales by material, insulation type, application, and geography for 2019-2030, with a 2025 baseline of USD 38.5 billion.

Scope exclusion: Bare electrical wire, power cables, and fiber-optic or signal lines are not counted.

Segmentation Overview

- By Material

- Copper

- Aluminium

- By Insulation Type

- Enameled Wire

- Covered Conductor Wire

- By Shape

- Round

- Rectangular / Flat

- By End-use Industry

- Electric Vehicles

- Energy

- Transformers

- Other Energy Types

- Industrial

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed magnet wire producers, motor OEM engineers, and bulk copper traders across Asia-Pacific, North America, and Europe to validate conversion yields, insulation mix shifts, and average selling prices, which refined our assumptions and filled data gaps spotted in desk work.

Desk Research

We first collected trade and production statistics from sources such as UN Comtrade, International Copper Study Group, and IEA EV Outlook. We then paired these with regional motor and transformer shipment data released by associations like NEMA and the Japan Electrical Manufacturers' Association. Company 10-Ks, investor decks, customs filings, and reputable business press helped us benchmark pricing spreads and verify capacity additions. Proprietary pulls from D&B Hoovers and Dow Jones Factiva supplied company-level revenue splits that sharpened segment weights. This list is illustrative; many other public and subscription sources were reviewed before numbers were frozen.

Market-Sizing & Forecasting

A top-down reconstruction starts with regional production and trade volumes, applies verified average selling prices, and is cross-checked through sampled bottom-up roll-ups of supplier revenues and channel checks. Key variables like EV production units, utility transformer shipments, renewable energy installation capacity, copper and aluminum price indices, and high-efficiency motor penetration feed a multivariate regression that produces the 2025-2030 outlook. Where bottom-up totals diverge beyond a 5% band, weights are rebalanced before finalization.

Data Validation & Update Cycle

Outputs pass anomaly scans, peer review, and senior analyst sign-off. We refresh each model annually, with interim updates triggered by material events such as price shocks or legislative changes. A last-mile sense check is run just before every client delivery.

Why Mordor's Magnet Wire Baseline Commands Reliability

Published estimates can differ markedly because firms pick different scope cut-offs, refresh cadences, and price benchmarks. Our disciplined variable set and annual audit help decision-makers rely on one consistent baseline.

Key gaps often arise when other studies omit fast-growing EV demand, apply static commodity prices, or depend on legacy pre-pandemic data that understate Asia's capacity additions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 38.5 B (2025) | Mordor Intelligence | - |

| USD 32.4 B (2025) | Regional Consultancy A | Relies chiefly on trade statistics; limited primary validation |

| USD 28.5 B (2024) | Trade Journal B | Excludes automotive and renewable installations, narrowing demand pool |

| USD 33.0 B (2025) | Global Consultancy C | Uses 2018 price deck and refreshes on a three-year cycle |

In sum, the spread shows how scope choices and aging inputs skew figures. Mordor's rigor in selecting variables, blending top-down with selective bottom-up checks, and updating yearly gives clients a transparent, repeatable view they can trust.

Key Questions Answered in the Report

How large will the magnet wire market be in 2031?

It is forecast to reach USD 49.27 billion by 2031, growing at a 5.05% CAGR from 2026.

Which material leads sales today?

Copper maintains dominance with 72.13% revenue share in 2025, outperforming aluminum on conductivity and recycling infrastructure.

Why is rectangular magnet wire gaining momentum?

Hairpin stator designs in EV traction motors raise slot-fill density to 70-80%, driving a 5.38% CAGR for rectangular profiles.

What region represents the fastest growth?

Asia-Pacific, led by China and India policy support, is expanding at about 6.07% CAGR through 2031.

How will new IE4 motor rules affect demand?

The 2027 U.S. requirement for 100-250 hp motors accelerates replacement cycles, lifting industrial demand for high-precision rectangular wire.

Page last updated on: