Sports Coaching Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

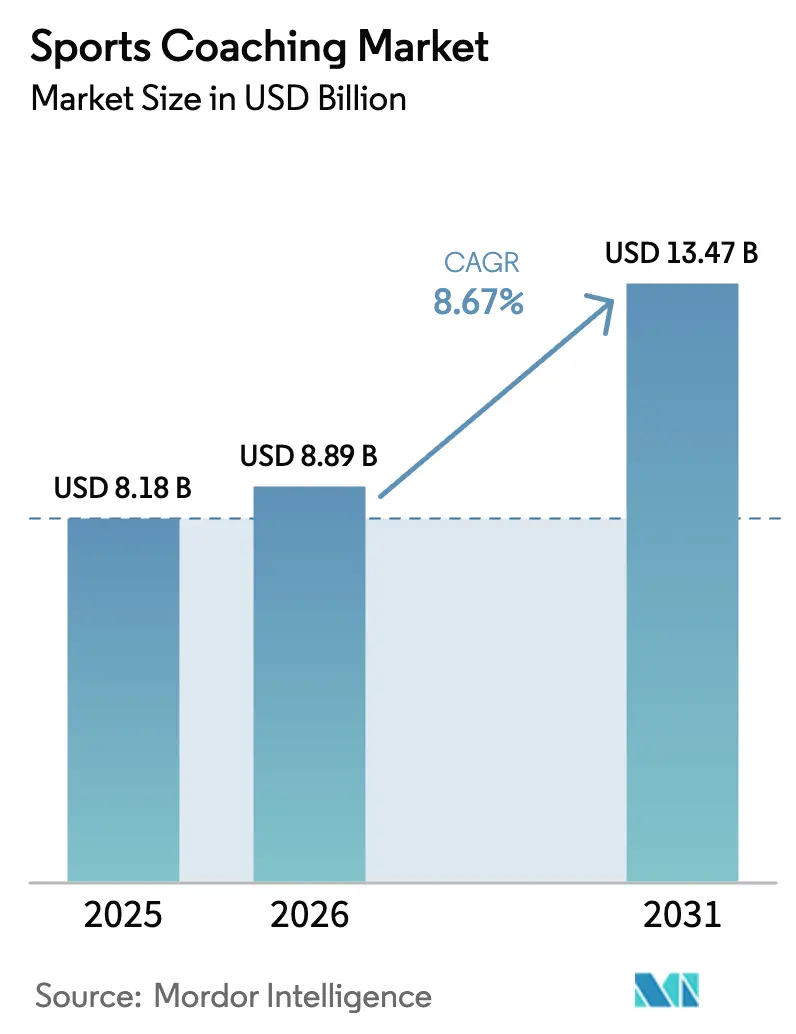

| Market Size (2026) | USD 8.89 Billion |

| Market Size (2031) | USD 13.47 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

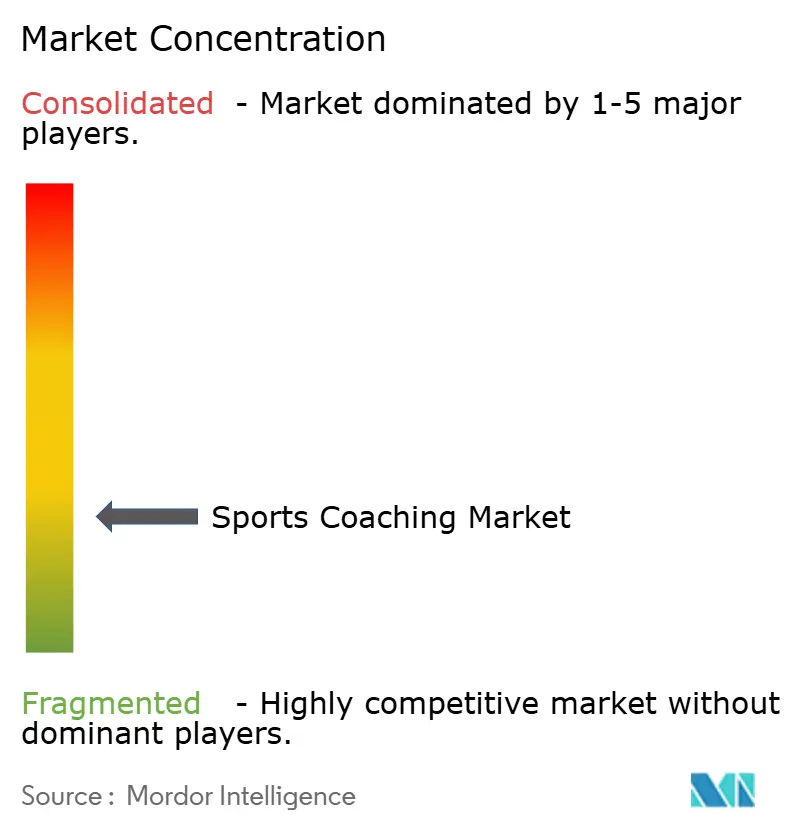

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports Coaching Market Analysis by Mordor Intelligence

The sports coaching market size is expected to grow from USD 8.18 billion in 2025 to USD 8.89 billion in 2026 and is forecast to reach USD 13.47 billion by 2031 at 8.67% CAGR over 2026-2031. Adoption of AI-enabled performance tools, rising fitness consciousness, and government-backed school-sports mandates fuel this steady climb. Wearable sensors and virtual-reality drills let coaches deliver data-rich feedback at scale while boosting measurable results. Private-equity interest evident in premium academy buyouts confirms that technology-powered models can sustain attractive margins. Accessible online platforms widen reach into underserved demographics, creating dual revenue streams that blend physical and digital sessions. Regionally, North America still commands the largest slice, but the Middle East is closing the gap thanks to large-scale Vision 2030 funding earmarked for sports infrastructure [1]Source: Government of Saudi Arabia, “Vision 2030 – Quality of Life Program,” vision2030.gov.sa.

Key Report Takeaways

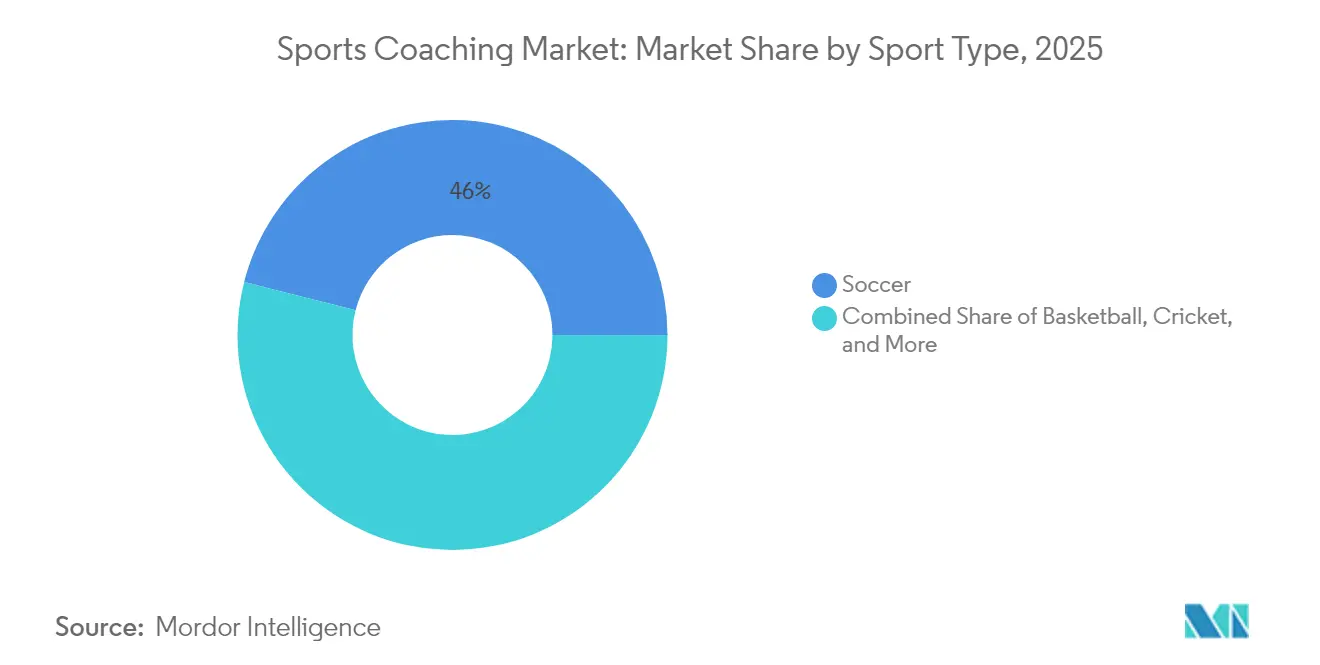

- By sport type, soccer led with 46.03% of sports coaching market share in 2025, while niche and emerging sports coaching expanded at a 14.22% CAGR through 2031.

- By coaching form, virtual coaching platforms held 15.74% CAGR, contrasting with academy and institutional models that retained 52.13% revenue share of the sports coaching market size in 2025.

- By coaching mode, offline delivery retained 60.45% of the sports coaching market size in 2025, but online coaching recorded 12.91% CAGR as hybrid adoption surged.

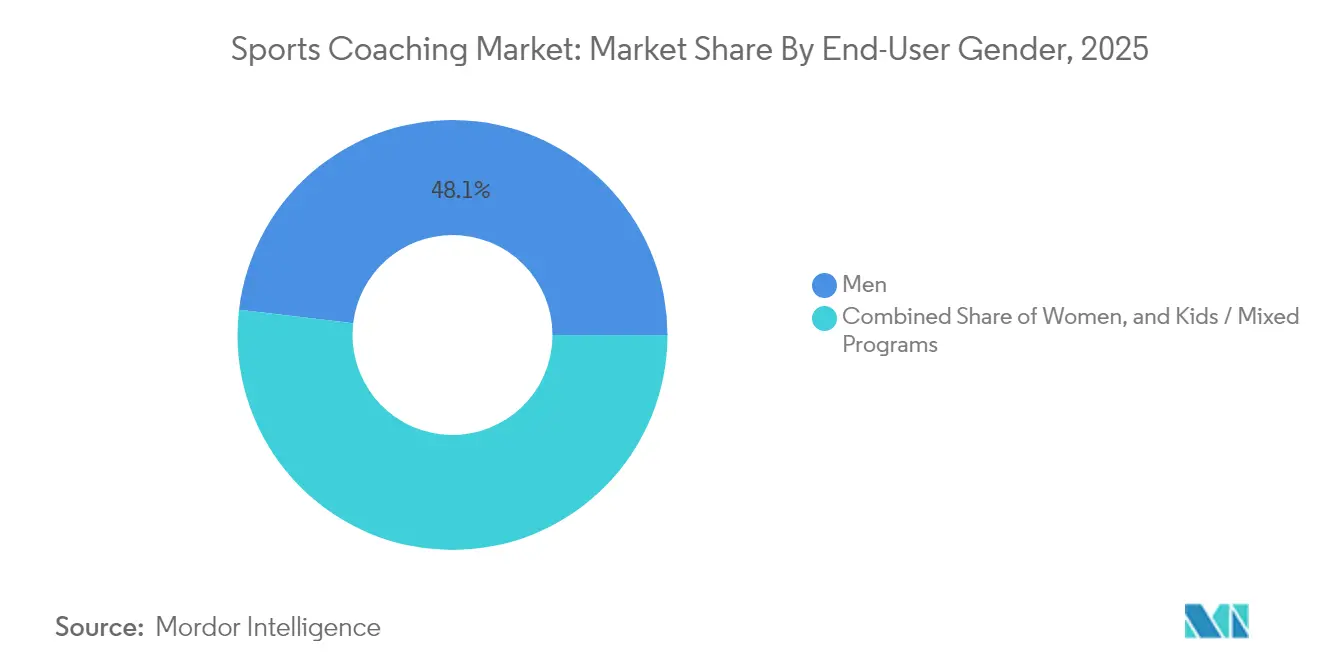

- By end-user gender, men’s coaching accounted for 48.12% share, whereas women’s coaching posted the fastest 10.48% CAGR, showing clear demographic expansion in the sports coaching market.

- By age group, the 12-18 segment captured 39.22% of sports coaching market share in 2025; the 36-plus cohort grew at 10.27% CAGR on the back of adult fitness programs.

- By geography, North America held 41.78% revenue share in 2025 while the Middle East advanced at an 9.44% CAGR in the sports coaching market.

- IMG Academy, Challenger Sports, US Sports Camps, I9 Sports, and CMT Learning Ltd are among the leading companies in the sports coaching industry.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sports Coaching Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global sports participation and health awareness | +2.1% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Government funding and school-level sports mandates | +1.8% | North America, Middle East, Asia-Pacific core | Long term (≥ 4 years) |

| Professionalization of sports academies and camps | +1.5% | Global, with early gains in North America, Europe, Middle East | Medium term (2-4 years) |

| Integration of wearables, AI and data analytics in coaching | +2.3% | North America and Europe core, spill-over to APAC | Short term (≤ 2 years) |

| Niche-sport boom spurring specialty coaching | +0.9% | North America, Australia, with expansion to Europe | Medium term (2-4 years) |

| Women-specific sponsorship unlocking female coaching demand | +1.2% | Global, with strongest impact in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration of Wearables, AI and Data Analytics in Coaching

Intelligent sensors coupled with algorithmic insights are reshaping skill acquisition. Modern platforms convert biometric readings into customized drills, allowing one coach to supervise many athletes in real time. The resulting efficiency solves historic scalability problems and supports subscription pricing that locks in predictable monthly income. Predictive alerts flag fatigue patterns before they spark injuries, adding a preventive healthcare dimension that insurers increasingly reward. Up-front device costs still deter smaller academies, yet falling hardware prices are likely to ease adoption across community programs.

Government Funding and School-Level Sports Mandates

Public-sector initiatives broaden the sports coaching market by reducing participation costs and standardizing coach quality. California’s Certified Wellness Coach Scholarship Program supports training pipelines for 25,000 new wellness-oriented coaches through 2025, offering grants of up to USD 35,000 to trainees who commit to year-long service in schools and community centers [2]Source: California Department of Health Care Access and Information, “Certified Wellness Coach Scholarship Program,”.. Community Grants funnel USD 20 million toward free youth sports and recreation sessions in underserved neighborhoods, creating paid coaching roles and expanding access [3]Source: District of Columbia Department of Parks and Recreation, “Rec for All Community Grants,” dpr.dc.gov.. Such programmes elevate minimum service standards while anchoring demand with public funds.

Women-Specific Sponsorship Unlocking Female Coaching Demand

Corporate sponsors are channeling fresh capital into women’s leagues, lifting athlete pay and widening the need for specialized coaching staff. Women’s elite sports revenue is set to hit USD 2.35 billion in 2025, a 25% jump from 2024, enabling franchises to invest in female-focused training curricula. The WNBA’s USD 2.2 billion media deal secures long-term budgets that include coach development stipends. New certifications dedicated to female biomechanics command premium fees, especially in basketball and soccer where participation spikes intersect with brand-backed equality pledges.

Professionalization of Sports Academies and Camps

Elite academies increasingly bundle academics, nutrition, and sport science into year-round campuses that resemble collegiate environments. The USD 1.25 billion sale of IMG Academy to BPEA EQT in 2024 demonstrates investor belief in scalable, outcomes-driven coaching models. These multi-sport hubs hire top-tier staff, invest in analytics labs, and monetize international student pipelines, driving higher average revenues per athlete than seasonal camps. Expansion plans across Asia highlight the portability of the academy blueprint when backed by credible brands and capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of personalized coaching programs | -1.4% | Global, with strongest impact in emerging economies | Short term (≤ 2 years) |

| Shortage of certified coaches in emerging economies | -0.8% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Data-privacy and IP risks in AI-driven coaching platforms | -0.6% | North America and Europe core, expanding to APAC | Medium term (2-4 years) |

| E-sports siphoning youth from physical-sport coaching | -0.4% | Global, with strongest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Personalized Coaching Programs

Youth participation remains price-sensitive. Families in the United States spend an average of USD 883 per child each season, prompting many low-income households to opt out. The layering of AI subscriptions and wearable sensors inflates fees, concentrating adoption among affluent communities and potentially capping total addressable volume. Scholarship pools and community grants temper the divide but often fall short of true demand.

Shortage of Certified Coaches in Emerging Economies

Demand often outpaces supply in Asia, Africa, and parts of Latin America, where rapid sports uptake collides with limited training infrastructure. Few local universities offer coach-education pathways, and experienced professionals migrate abroad for higher pay. International bodies deliver workshops, yet long-term retention hinges on domestic accreditation systems, sustained funding, and cultural alignment around coaching as a respected career.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sport Type: Soccer Dominance Faces Emerging Sport Disruption

Soccer accounted for 46.03% of the sports coaching market size in 2025, supported by standardized licensing systems and multi-tier leagues that channel athletes from grassroots to professional ranks. Established academies feed predictable revenue, while global media rights expose local players to international benchmarks. Cricket and basketball follow closely, leveraging robust fan bases and year-round competitive calendars to justify investment in specialized coaching. Simultaneously, the rapid growth of pickleball, padel, and other lifestyle sports captures adult segments seeking social fitness, pushing their combined revenue up at 14.22% CAGR. These niche sports require tailored instruction, offering experienced coaches new specialization options with minimal entry costs.

The widening sport mix diversifies income for platform providers that curate multiple disciplines under one subscription. Virtual-reality drills now support track-and-field starts and volleyball serves, emphasizing transferable sensor ecosystems. Soccer’s dominance will persist, yet its share may erode slowly as federations for emerging sports secure sponsorship and broadcast deals, fueling certified-coach demand outside legacy hubs.

By Coaching Form: Virtual Platforms Transform Service Delivery

Academy and institutional programs held 52.13% of sports coaching market share in 2025, reflecting parent confidence in year-round, objective-based frameworks that merge schoolwork and performance analytics. Such venues monetize dorm housing, meal plans, and tournament hosting, cushioning seasonal revenue swings. Concurrently, virtual platforms are expanding at 15.74% CAGR by overlaying AI-powered breakdowns on user-uploaded videos and synchronizing remote group sessions. The shift enables rural athletes to access elite instruction without relocation while allowing coaches to monetize intellectual property through digital courseware.

Hybrid strategies increasingly pair on-site camps with virtual follow-ups, keeping athletes engaged through the off-season and improving retention. Performance-consulting add-ons—such as dietary tracking or biomechanics labs—offer cross-sell potential. As broadband access widens and latency diminishes, virtual-first providers are likely to capture a larger slice of discretionary spend, though in-person academies will remain indispensable for sports requiring complex tactical feedback.

By Coaching Mode: Hybrid Models Bridge Digital–Physical Divide

Traditional in-person sessions still produced 60.45% of the sports coaching market size in 2025, mainly because tactile correction and real-time micro-adjustment are critical for risk-intensive skills. Multi-sport community centers leverage this preference by bundling court rentals and group instruction, stabilizing cash flow. Yet online coaching is advancing at 12.91% CAGR as high-definition streaming and motion-tracking apps replicate elements of face-to-face engagement. Individuals schedule asynchronous feedback loops, sending training clips and receiving annotated returns within hours, reducing logistical friction.

Dual-mode programs are flourishing. Athletes can complete baseline assessments virtually, attend intensive weekend clinics for live drills, then return to remote monitoring. Such choreography maximizes coach utilization rates, lowers travel costs, and broadens geographic reach. Over time, expect an equilibrium where hybrid packages become standard, using in-person checkpoints to deepen relationships while data dashboards sustain daily practice guidance.

By End-User Gender: Women’s Segment Drives Demographic Expansion

Men’s programs held 48.12% revenue in 2025, underpinned by deeply entrenched school and professional league systems that funnel continual demand for specialized tactical and strength conditioning. However, women’s coaching is outpacing overall growth, recording a 10.48% CAGR as sponsorship dollars flow into female leagues. Increased media coverage has elevated role-model visibility, fortifying grass-roots enrollment. Specialized curricula consider injury patterns unique to female physiology, differentiating service value and commanding premium fees.

Kids and mixed-gender formats remain pivotal entry points, yet adult women returning to sport for wellness reasons represent a rapidly monetizing niche. As governing bodies mandate equal facilities and coaching budgets, providers able to supply certified female coaches or gender-informed modules will enjoy a first-mover advantage. Digital communities amplify word-of-mouth, accelerating adoption in regions where cultural norms once limited female participation.

By Age Group: Adult Fitness Trends Reshape Market Demographics

Youth ages 12-18 retained 39.22% share in 2025 within the sports coaching market because competitive scholastic structures demand consistent skill refinement and exposure events. Coaches align training cycles with college-scouting calendars, converting performance metrics into scholarship opportunities. Travel-team ecosystems amplify spending intensity, with data dashboards now central to recruitment decisions.

Adults aged 36 and above posted the fastest 10.27% CAGR by prioritizing preventive health and social engagement over competition. Programs combine low-impact conditioning, technique simplification, and injury-managed progressions, encouraging sustained participation. Corporate wellness stipends also feed this category, integrating lunchtime clinics and virtual follow-ups that fit tight work schedules. For providers, adult retention rates are often higher than youth cohorts, creating annuity-like revenue when programs align with lifestyle goals.

Geography Analysis

North America maintained a 41.78% share of the sports coaching market size in 2025, propelled by high disposable income, widespread high school athletics, and mature certification pathways. Public initiatives—such as California’s target to certify 25,000 coaches—complement private sector innovation, creating a robust talent pipeline. Clubs increasingly embed data scientists alongside coaching staff, mirroring professional league practices and satisfying parent demand for quantifiable progress. Adult recreational leagues and corporate sponsorship of wellness clinics widen revenue streams, insulating providers from youth-only demand cycles.

The Middle East posted the highest 9.44% CAGR as governments earmarked sports for economic diversification. Saudi Arabia’s USD 453 million 2024-2025 sports budget funds stadium upgrades, talent academies, and mass-participation programs, driving structural demand for certified coaches. Private investors receive incentives to build mid-scale facilities, with entry tickets ranging from SAR 10 million to SAR 80 million. Global brands seek licenses to operate academies, strengthening knowledge transfer and accelerating coach education.

Asia–Pacific follows, buoyed by a USD 240.4 billion physical-activity economy and rising middle-class ambitions. Urban parents view sport as both a scholarship gateway and an antidote to sedentary lifestyles. China invests in campus-linked academies, whereas India’s private schools bundle cricket and football coaching to attract enrollments. Europe, owning legacy club structures, demonstrates steady incremental growth as federations focus on digital-upskilling existing coach rosters. Latin America and Africa trail but show upside once coach accreditation frameworks and funding catch up with participation enthusiasm.

Competitive Landscape

Market structure remains moderately fragmented. Long-standing camp operators such as Challenger Sports, US Sports Camps, and I9 Sports dominate regional niches, while IMG Academy leverages scale, brand equity, and now BPEA EQT capital to extend globally. The latter’s integration with Nord Anglia Education unlocks distribution across 33 countries, embedding sport in academic calendars. Mid-tier academies emulate this template, bundling boarding and advanced analytics to capture premium student segments.

Technology disruptors exploit algorithmic coaching to drive volume without proportionate labor costs. Hudl’s 2024 acquisition of StatsBomb appended granular soccer data to its video suite, giving 230,000 teams broader insight layers. Start-ups deploy subscription models with tiered feature sets—from tactical heatmaps to injury-risk scoring—creating entry-level options for community clubs. Wearable makers partner directly with coaching platforms, seeking recurring software revenue rather than one-off device sales.

Private equity’s interest signals forthcoming consolidation. Operators with defensible curricula and multi-sport scalability will likely attract capital looking for roll-up plays. Conversely, small seasonal camps may pivot to niche specialty offerings or ally with digital platforms to stay relevant. Cost management remains essential: families’ price sensitivity and public-school budgets cap fee ceilings unless evidenced performance ROI is clear.

Sports Coaching Industry Leaders

IMG Academy

Challenger Sports

US Sports Camps

I9 Sports

CMT Learning Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Hudl completed the acquisition of StatsBomb, integrating advanced analytics with its global video suite to enhance coach decision-making workflows.

- August 2024: KKR completes acquisition of Varsity Brands from Bain Capital and Charlesbank.

Global Sports Coaching Market Report Scope

Sports coaching is a special process of preparation for sportspeople based on scientific principles aimed at improving and maintaining higher performance capacity in different sports activities. The sports coaching market is segmented by type, application, and geography. By type, the market is segmented into professional and non-professional. By application, the market is segmented into soccer, basketball, swimming, baseball, cricket, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers market size and forecasts for the sports coaching market in value (USD) for all the above segments.

| Soccer |

| Basketball |

| Cricket |

| Baseball |

| Tennis |

| Volleyball |

| Track & Field |

| Rugby |

| Pickleball & Other Emerging Sports |

| Academy / Institution Coaching |

| Camps & Clinics |

| Personal 1-on-1 Training |

| Group Training Programs |

| Virtual Coaching Platforms |

| Sports Analytics and Performance Consulting |

| Offline |

| Online |

| Blended / Hybrid |

| Men |

| Women |

| Kids / Mixed Programs |

| Below 12 Years |

| 12 - 18 Years |

| 19 - 35 Years |

| 36 Years and Above |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Sport Type | Soccer | |

| Basketball | ||

| Cricket | ||

| Baseball | ||

| Tennis | ||

| Volleyball | ||

| Track & Field | ||

| Rugby | ||

| Pickleball & Other Emerging Sports | ||

| By Coaching Form | Academy / Institution Coaching | |

| Camps & Clinics | ||

| Personal 1-on-1 Training | ||

| Group Training Programs | ||

| Virtual Coaching Platforms | ||

| Sports Analytics and Performance Consulting | ||

| By Coaching Mode | Offline | |

| Online | ||

| Blended / Hybrid | ||

| By End-User Gender | Men | |

| Women | ||

| Kids / Mixed Programs | ||

| By Age Group | Below 12 Years | |

| 12 - 18 Years | ||

| 19 - 35 Years | ||

| 36 Years and Above | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the sports coaching market?

The sports coaching market is valued at USD 8.89 billion in 2026 and is projected to grow to USD 13.47 billion by 2031 at a 8.67% CAGR.

Which sport accounts for the largest coaching demand?

Soccer dominates with 46.03% revenue share due to its global participation base and mature certification pathways.

Who are the key players in Sports Coaching Market?

IMG Academy, ISM Sports, Elle Football Academy, ESM Academy and Khelomore Sports are the major companies operating in the Sports Coaching Market.

Why is the Middle East considered a high-growth region for coaching?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Sports Coaching Market?

Government funding—such as Saudi Arabia’s USD 453 million sports budget—and Vision 2030 diversification goals fuel infrastructure projects that require large numbers of qualified coaches.

How fast are virtual coaching platforms growing?

Virtual platforms recorded a 15.74% CAGR, the fastest among coaching forms, as remote analytics and AI tools support scalable instruction.

What are the main factors restricting market growth?

High program costs and a shortage of certified coaches in emerging economies reduce participation and limit expansion potential.

Which demographic segment is expanding the quickest?

Adults aged 36 and above demonstrate a 10.27% CAGR as wellness-oriented individuals seek structured, injury-aware coaching programs.

Page last updated on: