Qatar Private K-12 Education Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

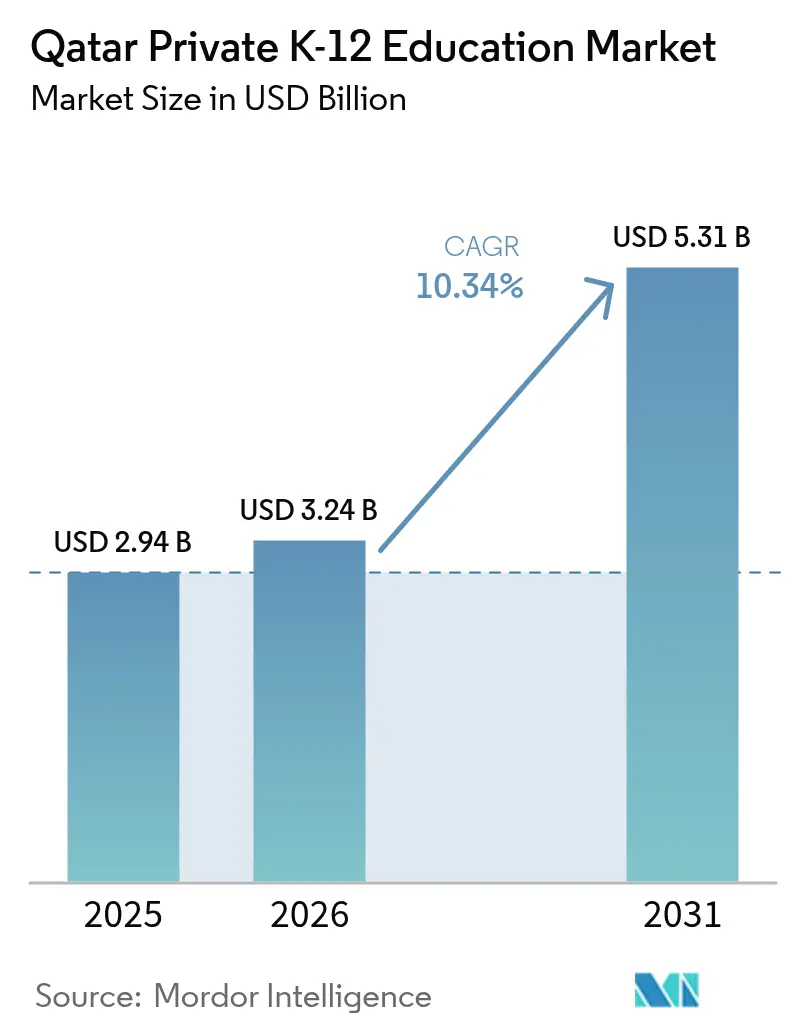

| Base Year Market Size (2025) | USD 2.94 Billion |

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 10.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Private K-12 Education Market Analysis by Mordor Intelligence

The Qatar Private K-12 Education Market size is expected to increase from USD 2.94 billion in 2025 to USD 3.24 billion in 2026 and reach USD 5.31 billion by 2031, growing at a CAGR of 10.34% over 2026-2031.

This healthy growth trajectory stems from population expansion, rising expatriate inflows, and policy support embedded in Qatar National Vision 2030.[1]Qatar Ministry of Education and Higher Education, “Education Annual Statistics,” MOEHE.gov.qa Strong enrollment momentum reflects an 85.40% population surge since 2008, with expatriates generating 75% of live births and posting 24.30% year-on-year growth in 2024. Primary education currently commands the largest revenue share at 34.74%, while secondary education exhibits the fastest segment CAGR at 6.29% through 2030. British curricula dominate with a 44.33% share, although American programs are scaling swiftly at an 8.24% CAGR as families seek U.S. university pathways. Geographically, Doha Municipality holds 63.24% share, yet Al Wakrah Municipality is expanding at 9.16% CAGR as new residential corridors unlock demand.

Key Report Takeaways

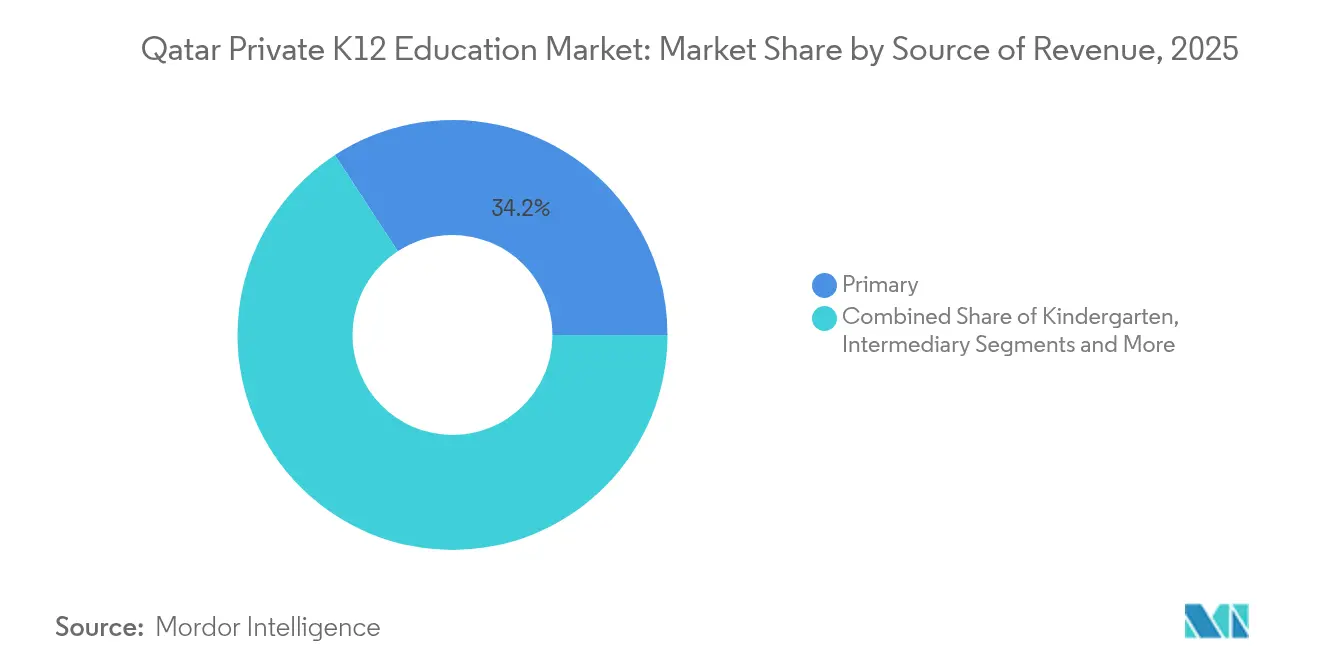

- By source of revenue, primary education held 34.21% of the Qatar private K-12 education market share in 2025, and secondary education is projected to expand at a 6.05% CAGR through 2031.

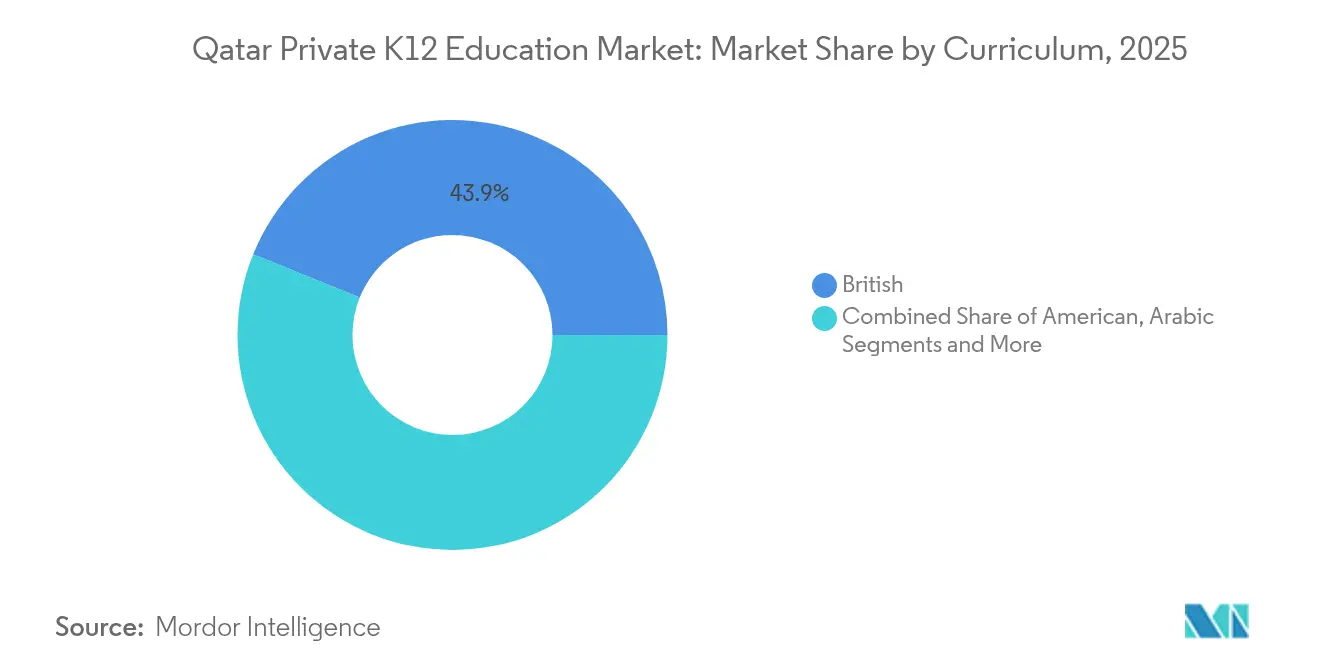

- By curriculum, British programs accounted for 43.88% of the Qatar private K-12 education market size in 2025, while American curricula are forecast to grow at an 8.1% CAGR to 2031.

- By nationality, expat students accounted for 81.22% of the Qatar K-12 market share in 2025, while local students are expected to grow the quickest with a 6.92% CAGR during 2026–2031.

- By region, Doha Municipality led with 62.58% of the Qatar private K-12 education market share in 2025; Al Wakrah Municipality is on track to record the highest regional CAGR at 8.97% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Private K-12 Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising expatriate population boosts demand for international curricula | +2.8% | Qatar-wide, concentrated in Doha and Al Rayyan | Medium term (2-4 years) |

| Government-backed Qatar National Vision 2030 encourages private investment | +2.1% | National, with priority zones in Education City and free zones | Long term (≥ 4 years) |

| Higher household incomes sustain premium tuition affordability | +1.7% | Doha Municipality and Al Wakrah Municipality | Short term (≤ 2 years) |

| Quest for multilingual proficiency linked to global university pathways | +1.9% | Qatar-wide, strongest in expatriate communities | Medium term (2-4 years) |

| PPP frameworks granting 100% foreign ownership in free-zones | +1.3% | Qatar Free Zones and designated investment areas | Long term (≥ 4 years) |

| Corporate-funded K-12 seats to attract post-FIFA industrial talent | +0.8% | Industrial zones and corporate districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Expatriate Population Boosts Demand for International Curricula

Non-nationals accounted for 75% of live births and recorded 24.30% growth in 2024, outpacing nationals at 20.90%[2]Gulf Times Staff, “Expats record higher than national average growth in live births,” GulfTimes.com. . Enrollment pressure is acute in British and American tracks as the 15-24 age cohort grows 8.50%, foreshadowing heightened secondary demand. With 241,332 students already in private schools 48,319 of whom are Qatari nationals operators recognize the cross-cultural appeal of internationally benchmarked programs. Corporate relocations feeding Qatar’s LNG and logistics build-out further accelerate seat uptake. Waiting lists topping 4,800 students at single Indian campuses underscore unmet capacity. Consequently, operators continue fast-tracking expansions and double-shift rosters to capture surging foreign-led demand.

Government-Backed Qatar National Vision 2030 Encourages Private Investment

The state devoted USD 4.91 billion, or 9% of its 2023 budget, to education and has earmarked PPP pipelines worth USD 1.1 billion to build 45 new public schools.[3]U.S. Department of Commerce, “Qatar – Education Training and Equipment,” Trade.gov Policy directives aim to double pre-primary enrollment to 88% by 2030, creating fresh white space for kindergarten operators. Foreign investors obtain 100% ownership in free-zone campuses, receive subsidized utilities, and enjoy land grants that improve project IRRs. The Educational Voucher Programme lowers out-of-pocket costs for Qatari families, expanding the premium addressable base. Capital-intensive projects now clear regulatory hurdles faster as the Ministry streamlines approvals, bolstering pipeline visibility for both domestic and global chains.

Higher Household Incomes Sustain Premium Tuition Affordability

Hydrocarbon receipts elevate disposable incomes, enabling families to fund annual fees that can exceed QR 80,000 (USD 22,000) per child. Affluent expatriate enclaves in Lusail, West Bay and Al Wakrah underpin demand for super-premium campuses equipped with Olympic swimming pools and 700-seat auditoriums. Corporate packages for engineers and finance professionals include K-12 subsidies, reducing price sensitivity. Regulatory mandates to cap classes at 30 students increase per-pupil costs, yet operators maintain margin discipline through tiered fee structures. The balance between premium positioning and operational efficiency remains central to profitability strategies over the medium term.

Quest for Multilingual Proficiency Linked to Global University Pathways

Parents prize credentials that secure direct entry to top-tier universities abroad. British curricula retain primacy via GCSE and A-Level structures, while American programs gain momentum as U.S. university applications climb. Mandatory Arabic and Islamic studies for Arab passport holders compel schools to integrate local subjects without diluting foreign standards. Partnerships with institutions such as MIT and The Juilliard School enrich STEM and arts pathways, differentiating high-end schools. Interdisciplinary enrichment activities, including UNICEF-backed sustainability challenges, help students cultivate global competencies valued by admissions offices worldwide.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High tuition fees strain mid-income families | -1.4% | Qatar-wide, most acute in secondary education | Short term (≤ 2 years) |

| Regulatory caps on class size elevate operating costs | -0.9% | National, affecting all licensed private schools | Medium term (2-4 years) |

| Shortage of bilingual STEM teachers amid Saudi giga-project pull | -1.8% | Qatar-wide, critical in mathematics and sciences | Medium term (2-4 years) |

| Premium-school saturation in Doha triggers discount wars | -1.1% | Doha Municipality premium segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Tuition Fees Strain Mid-Income Families

Annual charges topping QR 80,000 (USD 22,000) place pressure on middle-income expatriates, especially those with multiple children. The 30-student class-size ceiling raises staffing ratios and utilities usage, compelling schools either to lift fees or trim cost centers. Five leading Indian schools responded by introducing afternoon shifts to serve price-sensitive families, an initiative that filled 4,800 wait-listed seats. Voucher schemes ease costs for Qatari households but exclude many expatriates, sustaining affordability gaps. As a defensive measure, mid-tier operators bundle bus transport and extracurriculars at subsidized rates to defend volumes.

Shortage of Bilingual STEM Teachers Amid Saudi Giga-Project Pull

Saudi Arabia’s mega-projects entice bilingual STEM talent with lucrative packages, tightening educator supply in Qatar. The Ministry’s Tomouh scholarship offers QR 25,200 (USD 6,930) monthly stipends to nurture local teachers, yet near-term gaps persist. Private chains recruit globally, absorbing higher relocation costs and introducing on-site professional development to stem turnover. Qatar Foundation’s teacher-exchange programs with European universities help bridge skills doldrums, though scale-up takes years. Schools that secure stable pipelines of math and computer-science faculty will gain competitive advantage as technology curricula broaden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Revenue: Primary Education Anchors Growth Momentum

Primary education captured 34.21% of the Qatar private K-12 education market share in 2025, benefiting from compulsory schooling rules and favorable demographics. Secondary grades, however, are forecast to clock a 6.05% CAGR to 2031 as aging expatriate cohorts stay longer and focus on university readiness. The Qatar private K-12 education market size for secondary education is expected to widen in absolute terms by more than USD 400 million over the forecast horizon, generating outsized margin contributions for operators offering A-Level, IB, and SAT preparation pathways. Kindergarten demand aligns with policy targets aiming for 88% pre-primary participation, spurring rapid licensing of nurseries in Al Wakrah and Al Rayyan. Mid-cycle segments, such as intermediary grades, allow curriculum switchovers, and schools employ enrichment modules on coding, emotional intelligence, and Arabic literacy to retain students across transition years. Capacity pressure remains most intense in lower grades, driving Indian campuses to adopt double-shift models that add nearly 2,000 incremental seats per school. Operators able to leverage technology for personalized learning see higher retention in secondary, thereby maximizing lifetime tuition value.

Second-cycle expansion underscores a strategic focus on high-tuition years. Qatar Foundation’s expansion of the Tariq Bin Ziad School network into preparatory and secondary blocks exemplifies investment in grades where fee intensity peaks. IB Middle Years Programme adoption from grade 6 onwards broadens international credential options and enhances brand equity. As digital competence becomes a core Ministry requirement, vendors supplying coding bootcamps and robotics labs experience a revenue uplift tied to curriculum integration. In parallel, the Educational Voucher Programme shields Qatari nationals from fee shocks, encouraging sustained enrollment through grade 12.

By Curriculum: British Dominance Persists Amid American Acceleration

British tracks represented 43.88% of the Qatar private K-12 education market size in 2025, relying on entrenched parental trust in GCSE and A-Level rigor. American curricula, though smaller, are projected to grow 8.1% annually, bolstered by multinational corporate transfers and rising U.S. college matriculation ambitions. The Qatar private K-12 education market share of CBSE programs remains robust among the 750,000-strong Indian diaspora, and DPS Modern Indian School’s five-year QNSA accreditation in 2025 signals quality elevation in that segment. Arabic programs satisfy cultural and regulatory imperatives, with dual-stream schools weaving Islamic studies seamlessly alongside IGCSE content. Emerging French and German pathways cater to embassy personnel and energy multinationals, expanding linguistic diversity. Super-premium entrants like GSM’s Qetaifan Island North campus plan to house both British and IB tracks under one roof, reflecting parental appetite for curriculum optionality. Accreditation cycles are increasingly synchronized with market expectations, and schools obtaining ten-year international validations can justify higher tuition premiums.

Regulatory guidance stipulates core Arabic and Islamic instruction for Arab passport holders through Year 9, compelling curricular designers to embed these subjects without overloading student timetables. Technology infusion in coursework, such as mandatory robotics modules, differentiates forward-leaning schools. Operators that maintain transnational articulation agreements with overseas universities create downstream value propositions attractive to globally mobile families.

By Nationality: Post-World-Cup Legacy Accelerates National Participation

Foreign pupils represented 81.22% of private-school enrolment in 2025 across 334 licensed institutions, mirroring the country’s sizable expatriate workforce. Implemented in 2008, Qatar's tuition-voucher system provides financial subsidies for Qatari families, facilitating access to private education for a significant portion of local children. The Public-Private Partnership Schools Development Program will deliver eight new campuses annually through 2027, each designed with sustainability and disability provisions that exceed Ministry accreditation standards. Post-World-Cup infrastructure keeps construction and tourism projects active, sustaining expatriate headcounts and therefore fee revenue. These dynamics allow operators to diversify curricula while still satisfying obligatory Islamic studies and Arabic-language requirements.

National enrolment is projected to expand at a 6.92% CAGR to 2031 as voucher values rise and eligibility widens, making premium education more attainable for Qataris. Qatar National Vision 2030 positions education as a centrepiece for economic diversification, channelling public funds into teacher-training and STEM upgrades that elevate school quality. The country’s Education City, which hosts branch campuses of leading global universities, provides aspirational pathways that encourage private-school parents to maintain K-12 spending. Ongoing mega-projects in LNG expansion and smart-city development continue to draw engineers and managers, preserving expatriate demand even as Qatari uptake grows. Together, these drivers create a dual-segment model that underpins long-term market resilience.

Geography Analysis

Doha Municipality controlled 62.58% of the Qatar private K-12 education market in 2025, leveraging economic centrality and over 140 international campuses concentrated in West Bay, Education City, and Lusail. Yet space constraints and premium-school saturation spur expansion along the southern corridor, helping Al Wakrah post a leading 8.97% CAGR through 2031. The Qatar private K-12 education market size for Al Wakrah is projected to more than double, aided by expressway links to Hamad International Airport and new waterfront housing.

Al Rayyan enjoys spill-over demand as government housing schemes attract young Qatari families seeking proximity to stadium precincts. Al Khor & Al Thakhira Municipality hosts joint-venture campuses like Al Khor International School serving LNG complexes, showcasing an employer-funded model capable of rapid scale. The Rest of Qatar category remains under-penetrated but stands to benefit from Vision 2030 logistics investments that improve school commute times.

Growth patterns mirror infrastructure rollouts. Doha’s metro enhances catchment overlap, yet price competition intensifies as operators offer scholarships and bundled transport to maintain occupancy. In Al Wakrah, land availability allows expansive campuses with sports academies and maker spaces, aligning with rising expectations among middle-income expatriates. Supply-demand mismatch persists in northern rural districts, hinting at future micro-campus models and e-learning hybrids.

Competitive Landscape

The private K–12 education market in Qatar is moderately concentrated, with the five largest school groups Qatar Foundation Schools, GEMS Education, Nord Anglia Education, and two regional players together accounting for a significant portion of student enrollment. Qatar Foundation Schools benefit from government support, strong research partnerships, and expertise in dual-language instruction. GEMS Education operates a network of British and American curriculum schools, while Nord Anglia Education distinguishes itself by incorporating global programs such as the UNICEF sustainability challenges. Although the market favors large, well-funded organizations due to high capital requirements and strict licensing rules, smaller niche providers continue to succeed by focusing on areas like special-needs education or single-language learning environments.

Strategic moves show a pivot toward super-premium builds, M&A for scale, and technology partnerships. GSM’s Qetaifan Island North campus, opening 2026, exemplifies investment in experiential facilities that justify five-figure annual fees. Qatar Foundation is expanding Tariq Bin Ziad School into secondary grades, capturing lifecycle revenue and reinforcing bilingual excellence. Indian operators augment capacity via double-shift adoption and campus extensions to counter oversubscription. Concurrently, talent shortages push chains to sign global recruitment pacts and launch in-house teacher academies, safeguarding instructional quality.

White-space segments include special-needs provision and STEM enrichment. Qatar Foundation’s Warif and Renad academies signal growing prioritization of inclusive education. Robotics contests for students with disabilities showcase early-stage EdTech integration. Platform scalability depends on digital adoption, yet capex for ICT labs remains manageable compared with sports infrastructure, aiding mid-tier entrants. Overall, differentiation hinges on curricula breadth, faculty quality and partnership ecosystems. [4]Ministry of Education and Higher Education Qatar, “Al-Hidaya for Girls Organizes an Educational Robot Competition,” MOEHE.gov.qa

Qatar Private K-12 Education Industry Leaders

GEMS Education

Nord Anglia Education

Doha College

Sherborne Qatar

King’s College Doha

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DPS Modern Indian School achieved five-year QNSA accreditation, elevating standards in the CBSE segment .

- December 2024: Noble International School inaugurated a new campus to serve rising Indian expatriate demand.

- October 2024: Qatar Foundation agreed to expand the Tariq Bin Ziad School network with dedicated preparatory and secondary blocks.

- August 2024: Tariq Bin Ziad School opened a preparatory wing offering the IB Middle Years Programme.

Qatar Private K-12 Education Market Report Scope

A comprehensive background analysis of the Qatar Private K12 Education market, covering the current market trends, restraints, investment analysis and detailed information on various segments and competitive landscape of the education industry.

| Kindergarten |

| Primary |

| Intermediary |

| Secondary |

| American |

| British |

| Arabic |

| CBSE |

| Other Curriculum |

| Expat Students |

| Local Students |

| Doha Municipality |

| Al Rayyan Municipality |

| Al Wakrah Municipality |

| Al Khor & Al Thakhira Municipality |

| Rest of Qatar |

| By Source of Revenue | Kindergarten |

| Primary | |

| Intermediary | |

| Secondary | |

| By Curriculum | American |

| British | |

| Arabic | |

| CBSE | |

| Other Curriculum | |

| By Nationality | Expat Students |

| Local Students | |

| By Region (Qatar) | Doha Municipality |

| Al Rayyan Municipality | |

| Al Wakrah Municipality | |

| Al Khor & Al Thakhira Municipality | |

| Rest of Qatar |

Key Questions Answered in the Report

How large is the Qatar private K12 education sector in 2026 and what CAGR is expected to 2031?

The sector generated USD 3.24 billion in 2026 and is forecast to climb to USD 5.31 billion by 2031, reflecting a 10.34% CAGR.

Which curriculum format captures the biggest share among private schools in Qatar?

British programs lead with 43.88% share in 2025, supported by established GCSE and A-Level pathways that resonate with expatriate families.

What geographic area shows the fastest growth in student enrollment?

Al Wakrah Municipality is expanding at a 8.97% CAGR through 2031 as new housing and transport links draw families beyond Doha’s core.

What are the main regulatory incentives for foreign investors entering Qatar's private K12 education?

Public-Private Partnership frameworks grant 100% foreign ownership in free zones, provide subsidized utilities, and streamline licensing, lowering barriers to large-scale campus development.

How significant is the teacher shortage and which subjects are most affected?

Competition from Saudi giga-projects has tightened supply, especially for bilingual STEM educators in mathematics, physics, and computer science, creating recruitment pressure across Qatar.

Page last updated on: