Laboratory Equipment And Disposables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 40.73 Billion |

| Market Size (2031) | USD 58.86 Billion |

| Growth Rate (2026 - 2031) | 7.64% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Equipment And Disposables Market Analysis by Mordor Intelligence

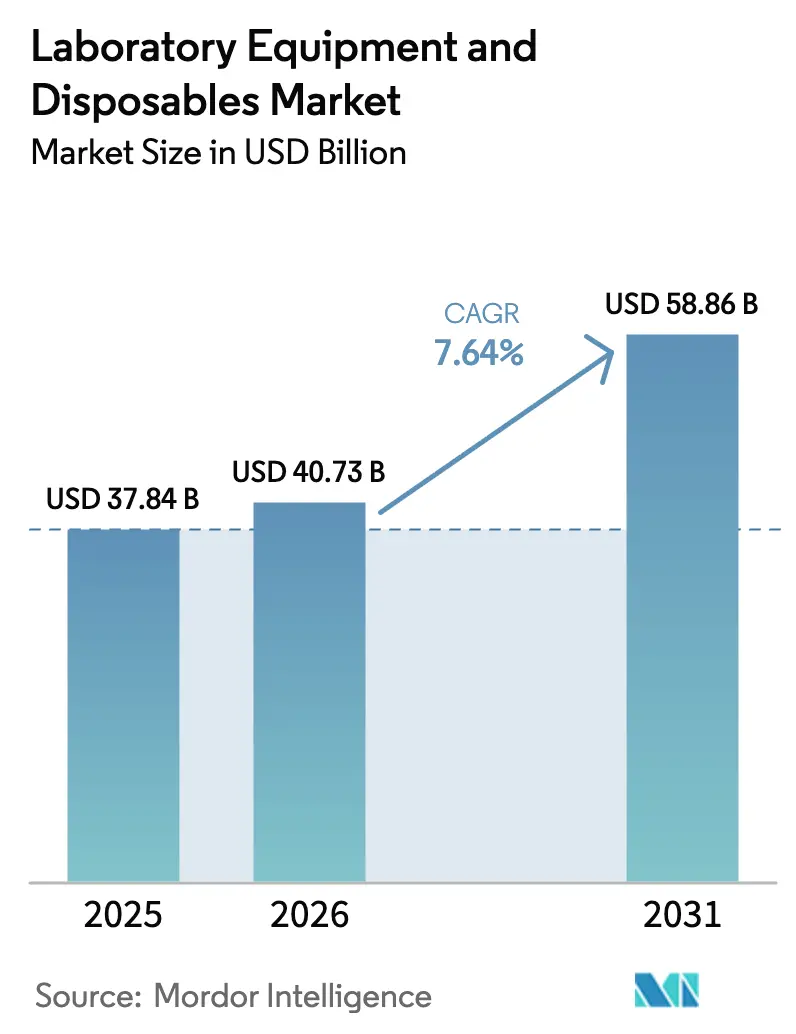

The Laboratory Equipment And Disposables Market size is projected to be USD 37.84 billion in 2025, USD 40.73 billion in 2026, and reach USD 58.86 billion by 2031, growing at a CAGR of 7.64% from 2026 to 2031.

In 2024, leading pharmaceutical companies are expected to allocate approximately USD 190 billion to biopharmaceutical R&D. This significant investment is driving strong demand for analytical instruments as firms prioritize accelerated discovery timelines. Concurrently, hospitals and reference laboratories are expanding their testing capacities, driven by the global burden of non-communicable diseases, which account for 41 million deaths annually. This trend is fueling increased adoption of automated systems for chemistry, hematology, and molecular testing. Additionally, advancements in automation and single-use technologies are reducing equipment replacement cycles and boosting consumables demand. Public-sector net-zero mandates are further incentivizing suppliers to demonstrate low-carbon operations and implement effective take-back programs. Although near-term pressures on plastics margins and extended regulatory timelines for new diagnostic platforms may moderate growth, these factors are not expected to hinder the overall expansion trajectory.

Key Report Takeaways

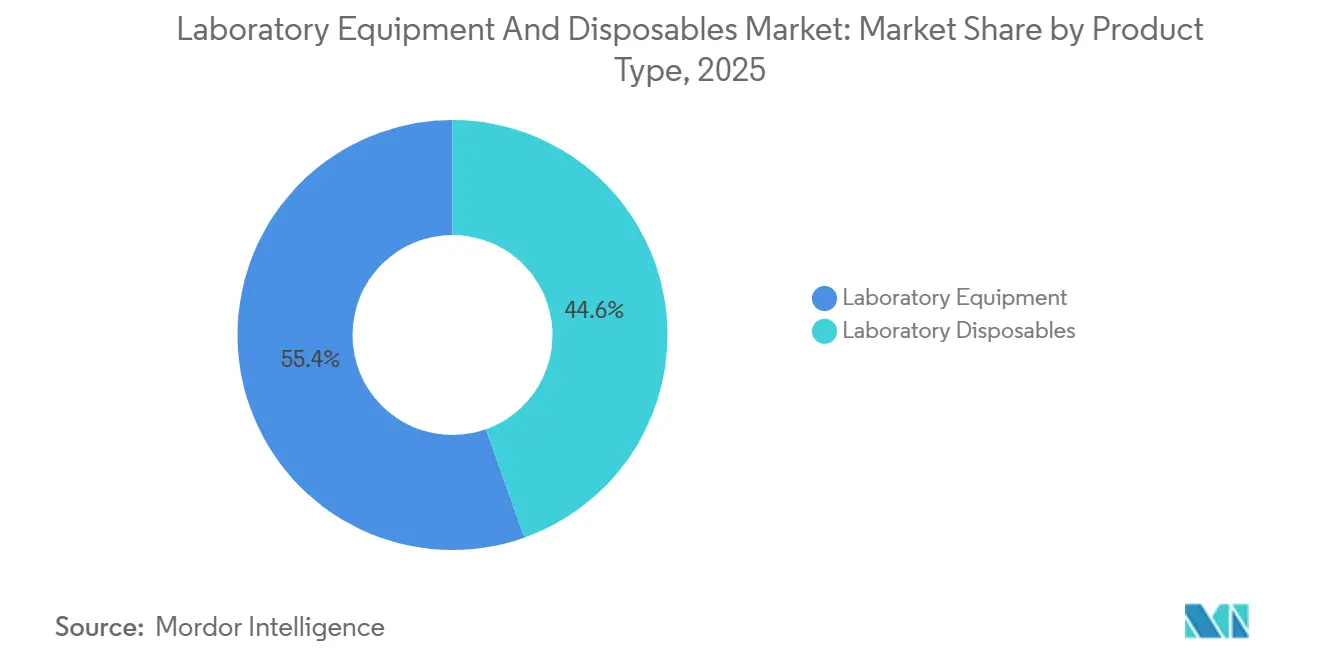

- By product type, laboratory equipment accounted for 55.43% of revenue in 2025, whereas disposables are forecast to expand at a 9.54% CAGR through 2031.

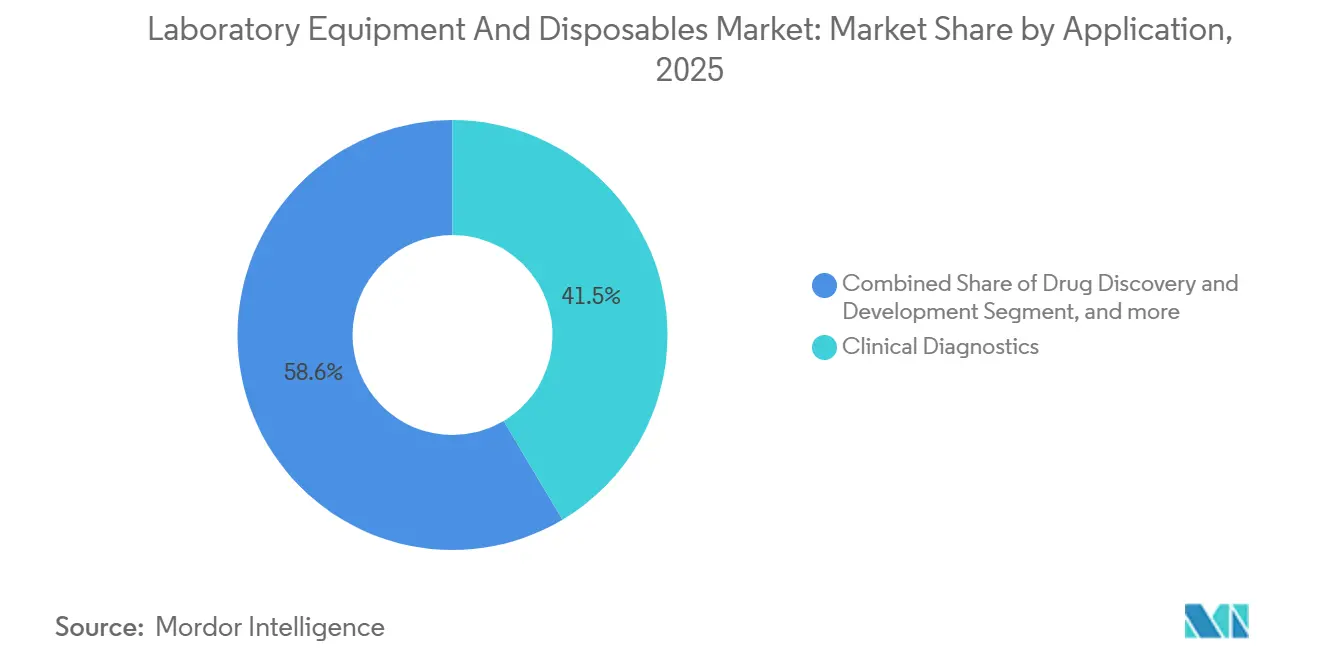

- By application, clinical diagnostics led with 41.45% of the laboratory equipment & disposables market share in 2025, while genomics and proteomics are set to advance at a 9.76% CAGR through 2031.

- By end user, hospitals and clinics captured 46.54% spending in 2025, yet contract research organizations are projected to grow at a 10.43% CAGR to 2031.

- By geography, North America accounted for 42.65% of revenue in 2025; Asia-Pacific is the fastest-growing region, with an 8.54% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laboratory Equipment And Disposables Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Biopharmaceutical R&D Budgets | +1.8% | North America, Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| Rising Prevalence of Chronic Diseases Driving Diagnostic Testing | +1.5% | Global, especially Asia-Pacific and North America | Long term (≥ 4 years) |

| Growing Adoption of Automation and High-Throughput Lab Systems | +1.3% | North America, Europe, emerging Asia-Pacific hubs | Medium term (2-4 years) |

| Convergence of Lab-On-Chip Manufacturing With Disposable Platforms | +1.0% | Global, strongest in point-of-care markets | Long term (≥ 4 years) |

| Government Net-Zero Procurement Mandates for Laboratory Infrastructure | +0.7% | Europe, North America, early Asia-Pacific adopters | Long term (≥ 4 years) |

| Venture-Backed Open-Access Lab Networks Accelerating Equipment Turnover | +0.6% | North America, Europe innovation clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Biopharmaceutical R&D Budgets

Drug makers face a collective patent-expiry cliff that threatens USD 150 billion in sales by 2027, prompting record investment in discovery and process-development labs. Industry R&D outlays climbed to roughly USD 288 billion in 2024, with Merck, Johnson & Johnson, and Roche each deploying more than USD 15 billion. Capital is channelled into liquid-handling robots, UHPLC, and next-generation sequencing, all of which underpin higher demand for precision instruments. Rising cell-and-gene-therapy pipelines further elevate needs for flow cytometers, digital PCR, and closed-system bioreactors. As sponsors push for faster IND filings, laboratories modernize to shorten cycle times.

Rising Prevalence of Chronic Diseases Driving Diagnostic Testing

Non-communicable ailments account for 74% of global mortality, led by cardiovascular disease, cancers, respiratory disorders, and diabetes. Diabetes alone is expected to affect 783 million adults by 2045, sustaining orders for HbA1c analyzers and continuous-glucose-monitoring lab components[1]International Diabetes Federation, “IDF Diabetes Atlas 2025,” idf.org . Cancer incidence could reach 35 million new cases by 2050, driving increased hospital demand for immunohistochemistry platforms and liquid biopsy workflows. In the United States, 60% of adults present at least one chronic condition, keeping chemistry and hematology systems fully utilized. Large chain laboratories, notably Quest Diagnostics and LabCorp, each exceeded USD 2 billion in Q3 2024 revenue, underlining the diagnostic-testing tailwind.

Growing Adoption of Automation and High-Throughput Lab Systems

Laboratories deploy automation to offset skilled-labor shortages and tighten quality control. QIAGEN plans three new sample-prep instruments by 2026, complementing its QIAcube and QIAsymphony lines. Agilent’s ADS 2 and Infinity III LC series improve dilution accuracy and speed in QC labs. MilliporeSigma’s partnership with Opentrons embeds open-source robotics into reagent workflows, while Bio-Rad’s 2024 acquisition of Stilla Technologies enlarged its digital-PCR suite. Such systems cut turnaround times, boost reproducibility, and feed laboratory-information-management systems for real-time analytics.

Convergence of Lab-On-Chip Manufacturing with Disposable Platforms

The United Kingdom, United States, and European Union now embed life-cycle emissions criteria in public lab-equipment tenders. Vendors must document carbon footprints, offer take-back of used consumables, and slash energy draws. Thermo Fisher and Sartorius pledge operational carbon neutrality by 2030, aligning with these mandates. Suppliers without retrofit capabilities risk exclusion from lucrative government contracts, accelerating consolidation in disposables.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Prices of Medical-Grade Polymers and Specialty Resins | -0.9% | Global, acute in regions reliant on Asian polymer imports | Short term (≤ 2 years) |

| Lengthy Validation and Certification Cycles for New Instrument Platforms | -0.6% | Global, notably Europe under IVD-R and North America under FDA | Medium term (2-4 years) |

| Emerging Circular-Economy Regulations Curtailing Single-Use Disposables | -0.4% | Europe, North America, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Shortage of Cross-Skilled Automation and Data-Science Personnel | -0.3% | Global, most pronounced in developing R&D hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Medical-Grade Polymers and Specialty Resins

Medical-grade polypropylene and polyethylene experienced triple-digit price swings in early 2025 following supply disruptions, compressing margins for pipette-tip and cell-culture-flask makers[2]British Plastics Federation, “Polymer Market Update Q1 2025,” bpf.co.uk. Corning cited resin volatility as a headwind to its USD 1.2 billion life-sciences revenue in Q3 2024, while Thermo Fisher acknowledged customer resistance to pass-through pricing. Smaller vendors lacking long-term contracts must absorb spikes or cede share to vertically integrated rivals. Moves toward recycled or biodegradable plastics, though environmentally positive, introduce cost premiums that many laboratories still hesitate to pay.

Lengthy Validation and Certification Cycles for New Instrument Platforms

Gaining FDA 510(k) clearance takes 3-12 months, whereas PMA approvals for high-risk diagnostics can take up to 3 years[3]U.S. Food and Drug Administration, “Premarket Approval (PMA) Process,” fda.gov. Europe’s IVD-R requires notified-body reviews even for moderate-risk devices, further lengthening timelines. ISO 13485 quality-system certification adds documentation and audit burdens, nudging innovators toward incremental, rather than disruptive, upgrades. Illumina’s NovaSeq X underwent multi-year global validations before its 2024 commercial launch, underscoring the capital and time barriers even the best-funded players face.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Outpace Equipment on Single-Use Adoption

Disposables are on track to eclipse traditional hardware growth, advancing at a 9.54% CAGR through 2031, even though equipment retained 55.43% revenue in 2025. The shift reflects biopharma’s move to single-use bioreactors that trim cleaning validation and cross-contamination risk. Analytical instruments, notably LC-MS and ICP-MS, still anchor capital budgets, with Waters and Agilent securing pharmaceutical QC contracts. General lab fixtures—centrifuges, incubators, biosafety cabinets—see lengthened replacement cycles as hospitals stretch capital budgets via service agreements.

Plasticware and glassware dominate the consumables basket, with Corning and Thermo Fisher serving cell-culture, filtration, and general laboratory needs. Filtration media for monoclonal-antibody purification buoy MilliporeSigma and Sartorius orders. Clean-room disposables, from gloves to sterile garments, rise in step with GMP enforcement. Emerging lab-on-chip diagnostics integrate reagents into single-use cartridges, creating ancillary demand from companies such as Abbott and Roche Diagnostics.

By Application: Genomics and Proteomics Surge on Precision Medicine

Clinical diagnostics accounted for 41.45% of revenue in 2025, benefiting from large installed bases of chemistry and immunoassay analyzers. Genomics and proteomics are the fastest movers, projected at a 9.76% CAGR, supported by Illumina’s NovaSeq X and Bruker’s Timstof platforms that cut per-sample costs for whole-genome and proteomic screens. Drug-discovery labs continue to invest in automated liquid handlers and high-content imagers as total industry R&D hit USD 288 billion in 2024.

Academic budgets remain tight, increasing reliance on shared core facilities and open-access hubs such as LabCentral. Industrial and environmental labs deploy GC-MS and ICP-MS to meet ISO 17025 requirements for contaminant testing, while clinical labs adopt mass spectrometry workflows through partnerships such as LabCorp’s alliance with Roche. Single-cell multi-omics and spatial transcriptomics platforms from 10x Genomics and Bio-Rad promise integrated end-to-end solutions that further propel spending.

By End User: CROs Accelerate on Outsourcing Wave

Hospitals and clinics absorbed 46.54% of outlays in 2025, yet contract research organizations are poised for a 10.43% CAGR as sponsors seek variable-cost models. Charles River logged USD 1.02 billion in Q3 2024 revenue, reflecting demand for discovery and safety labs, while IQVIA forecast up to USD 15.6 billion full-year sales across clinical services. Pharmaceutical majors maintain core discovery labs but outsource late-stage work to CROs to conserve capital.

Universities and government institutes depend on NIH and EU Horizon funding cycles, pushing many to adopt shared-resource models that require instrument turnover every 3 to 5 years. Open-access networks further lower entry barriers for start-ups, creating predictable refresh demand. Reference laboratories such as Quest and LabCorp blend routine and specialty testing, investing heavily in next-generation sequencing and flow cytometry to capture higher-margin assays and meet CLIA or ISO 15189 quality mandates.

Geography Analysis

North America generated 42.65% of 2025 sales, buoyed by dense biopharma clusters in Boston, San Francisco, and Research Triangle Park. NIH appropriations of USD 47 billion in fiscal 2024 and venture-capital inflows above USD 20 billion keep the laboratory equipment & disposables market vibrant. Thermo Fisher reported Q3 2024 revenue of USD 10.6 billion, with North America as its leading region. Tight FDA and CLIA oversight elevate demand for compliant platforms, while hospital reference labs deploy NGS and mass spectrometry to support personalized-medicine initiatives.

Asia-Pacific is forecast to grow at an 8.54% CAGR, powered by China’s CDMO build-out, India’s burgeoning diagnostics chains, and Japan’s precision-instrument exports. WuXi AppTec and WuXi Biologics are erecting multi-billion-dollar facilities that require extensive chromatography, filtration, and single-use hardware. BGI’s sequencing centers field thousands of instruments, and South Korea’s upgrades to cell-therapy capacity fuel orders for closed-system bioreactors.

Europe maintains a significant position through Germany’s chemical powerhouse, the United Kingdom’s research universities, and France’s public-health labs. Stringent IVD-R and MDR rules favor established suppliers such as Roche Diagnostics, Siemens Healthineers, and Danaher’s Beckman Coulter. NHS sustainability mandates push for energy-efficient analyzers and circular consumables. Elsewhere, GCC states ramp clinical capacity, South Africa bolsters infectious-disease labs, and Latin American markets adopt reagent-rental models to offset currency volatility.

Competitive Landscape

Market concentration is moderate. Thermo Fisher, Danaher, and Agilent leverage integrated portfolios of instruments, reagents, and multi-year service contracts to deepen customer lock-in. Thermo Fisher’s USD 17.4 billion PPD acquisition signaled its extension into contract research, while Danaher’s Cytiva and Pall divisions extend their reach from discovery to bioproduction. Waters, PerkinElmer, and Bio-Rad pursue bolt-on deals—such as Waters’ 2024 acquisition of Wyatt Technology—to fill capability gaps.

Niche entrants focus on lab-on-chip microfluidics and cloud-connected automation. Venture-backed LabCentral and BioLabs replace ownership with access, refreshing equipment every few years and guaranteeing vendors repeat business. Automation specialists Tecan and Hamilton integrate robotics with LIMS to cut error rates and labor costs. ISO 13485 and 17025 compliance remains costly, reinforcing incumbent advantages and slowing disruption.

Laboratory Equipment And Disposables Industry Leaders

Agilent technologies Inc

Bio-Rad Laboratories

Brucker Corporation

Sartorius AG

PerkinElmer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: INTCO Medical, one of the world's leading manufacturers of disposable gloves, launched its exclusive patented Syntex Synthetic Disposable Latex Gloves product. Breaking natural latex boundaries, Syntex redefines glove quality, safety, and performance.

- April 2025: Syntegon launched a new filling machine for ready-to-use (RTU) nested syringes.

- January 2025: Dynarex Corporation, one of the leading medical supply companies, launched LabChoice, a dynamic new line of laboratory products designed to meet the evolving needs of a wide range of industries, including healthcare, education, research, food & beverage, and other fields requiring precision tools.

Global Laboratory Equipment And Disposables Market Report Scope

As per the scope of the report, laboratory equipment refers to the various tools and instruments used by scientists in a laboratory. This includes glassware, tools, and laboratory instruments to collect, process, and store specimens. Disposables, such as gloves and masks, are disposable products used for convenience during fieldwork.

The Laboratory Equipment and Disposables Market is Segmented by Product Type (Laboratory Equipment and Laboratory Disposables), Application (Clinical Diagnostics, Drug Discovery and Development, Genomics and Proteomics, Academic and Research, and Industrial and Environmental Testing), End User (Hospitals and Clinics, Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, and Contract Research Organizations), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Laboratory Equipment | Analytical Instruments | Spectroscopy Equipment |

| Chromatography Systems | ||

| Microscopes & Imaging Systems | ||

| Other Instruments | ||

| General Lab Equipment | Centrifuges & Separators | |

| Incubators & Ovens | ||

| Autoclaves & Sterilizers | ||

| Other Equipments | ||

| Laboratory Disposables | Plasticware & Glassware | Pipettes & Tips |

| Petri Dishes | ||

| Test & Culture Tubes | ||

| Others | ||

| Filtration & Separation Supplies | Membrane Filters | |

| Syringe & Vacuum Filters | ||

| Centrifugal Filters | ||

| Clean-Room Consumables | Gloves | |

| Gowns & Masks | ||

| Wipes & Swabs | ||

| Clinical Diagnostics |

| Drug Discovery & Development |

| Genomics & Proteomics |

| Academic & Research |

| Industrial & Environmental Testing |

| Hospitals & Clinics |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Laboratory Equipment | Analytical Instruments | Spectroscopy Equipment |

| Chromatography Systems | |||

| Microscopes & Imaging Systems | |||

| Other Instruments | |||

| General Lab Equipment | Centrifuges & Separators | ||

| Incubators & Ovens | |||

| Autoclaves & Sterilizers | |||

| Other Equipments | |||

| Laboratory Disposables | Plasticware & Glassware | Pipettes & Tips | |

| Petri Dishes | |||

| Test & Culture Tubes | |||

| Others | |||

| Filtration & Separation Supplies | Membrane Filters | ||

| Syringe & Vacuum Filters | |||

| Centrifugal Filters | |||

| Clean-Room Consumables | Gloves | ||

| Gowns & Masks | |||

| Wipes & Swabs | |||

| By Application | Clinical Diagnostics | ||

| Drug Discovery & Development | |||

| Genomics & Proteomics | |||

| Academic & Research | |||

| Industrial & Environmental Testing | |||

| By End User | Hospitals & Clinics | ||

| Pharmaceutical & Biotechnology Companies | |||

| Academic & Research Institutes | |||

| Contract Research Organizations | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the Laboratory equipment & disposables market in 2031?

It is forecast to reach USD 58.86 billion, rising at a 7.64% CAGR between 2026 and 2031.

Which product category is expanding fastest?

Disposables lead growth, propelled by single-use bioreactor adoption and are set for a 9.54% CAGR through 2031.

Why are genomics and proteomics seeing rapid uptake in laboratories?

Higher-throughput platforms such as Illumina’s NovaSeq X and Bruker’s Timstof cut per-sample costs, boosting demand for sequencing and proteomic workflows.

How are sustainability mandates affecting purchasing decisions?

Government net-zero procurement frameworks favor energy-efficient instruments and recyclable consumables, influencing supplier selection in Europe and North America.

Which end-user segment is growing fastest?

Contract research organizations are projected to expand at a 10.43% CAGR as pharmaceutical sponsors outsource preclinical and clinical laboratory work.

Page last updated on: