Laparoscopic Retrieval Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 559.8 Million |

| Market Size (2031) | USD 805.88 Million |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

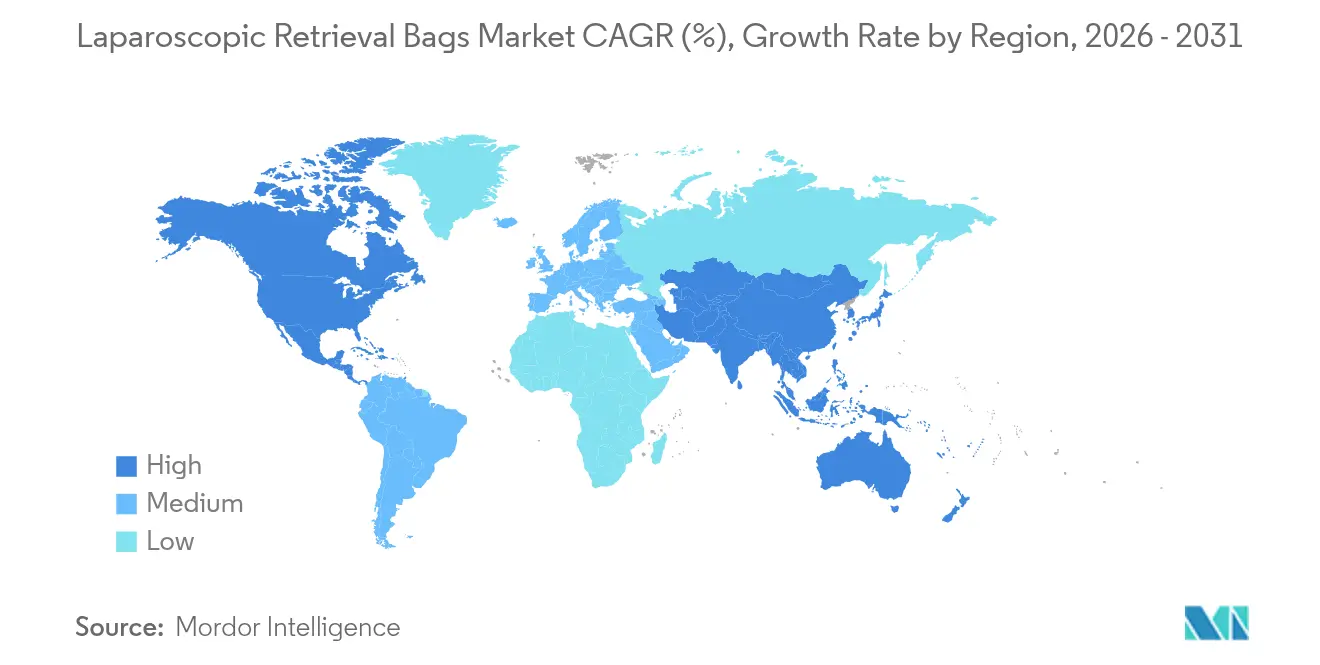

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

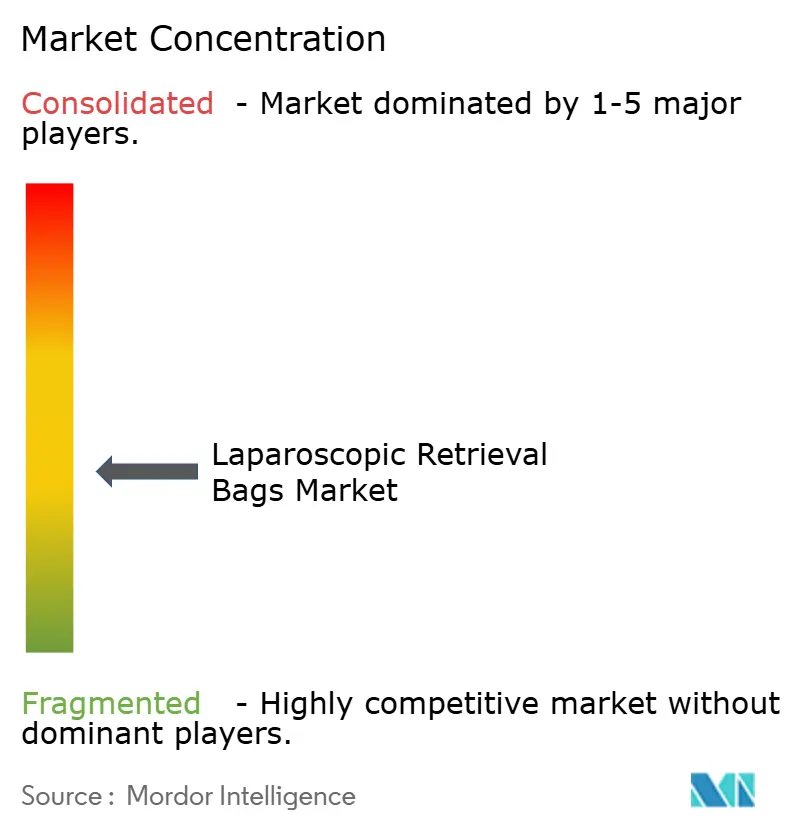

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laparoscopic Retrieval Bags Market Analysis by Mordor Intelligence

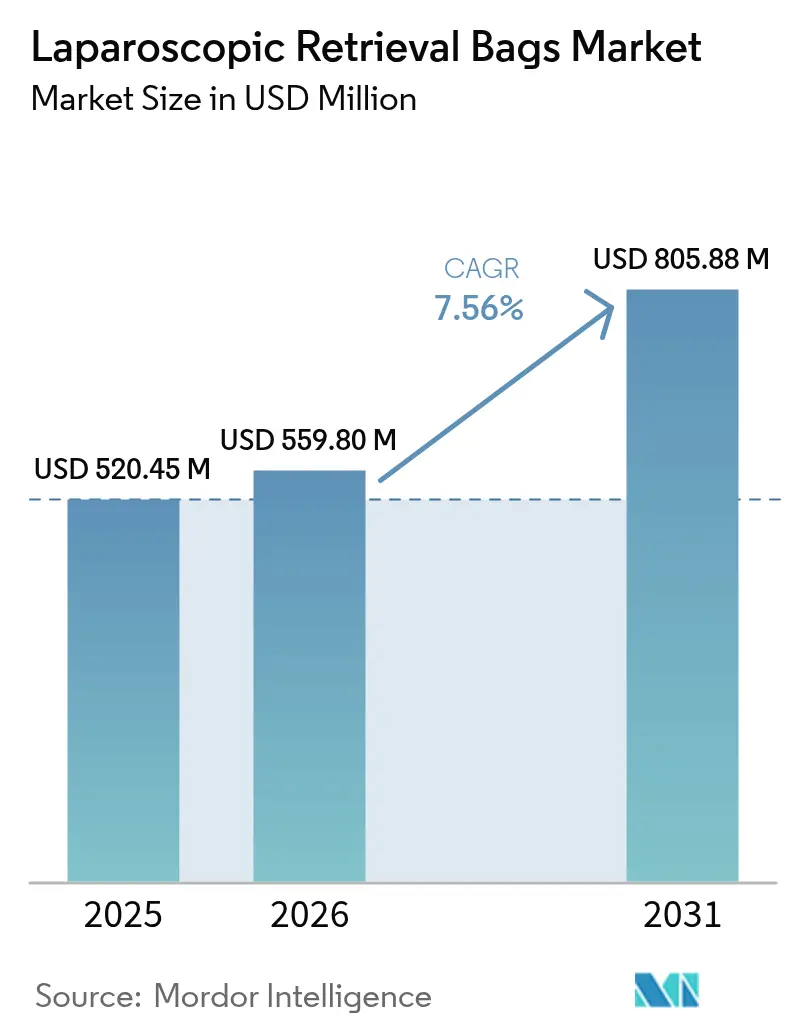

The laparoscopic retrieval bags market size in 2026 is estimated at USD 559.8 million, growing from 2025 value of USD 520.45 million with 2031 projections showing USD 805.88 million, growing at 7.56% CAGR over 2026-2031. Robust uptake of minimally invasive surgery, regulatory preferences for single-use sterile consumables, and steady product innovation in self-opening mechanisms collectively underpin this expansion. Detachable bag designs, compatibility with robotic platforms, and rising volumes of day-case laparoscopic procedures are widening procurement opportunities for vendors. Hospitals continue to anchor demand, yet ambulatory surgical centres (ASCs) are reshaping purchasing criteria by favouring cost-efficient, disposable kits. Regionally, North America retains leadership on the back of established reimbursement for advanced laparoscopy, while Asia-Pacific registers the briskest growth in step with large-scale infrastructure upgrades.

Key Report Takeaways

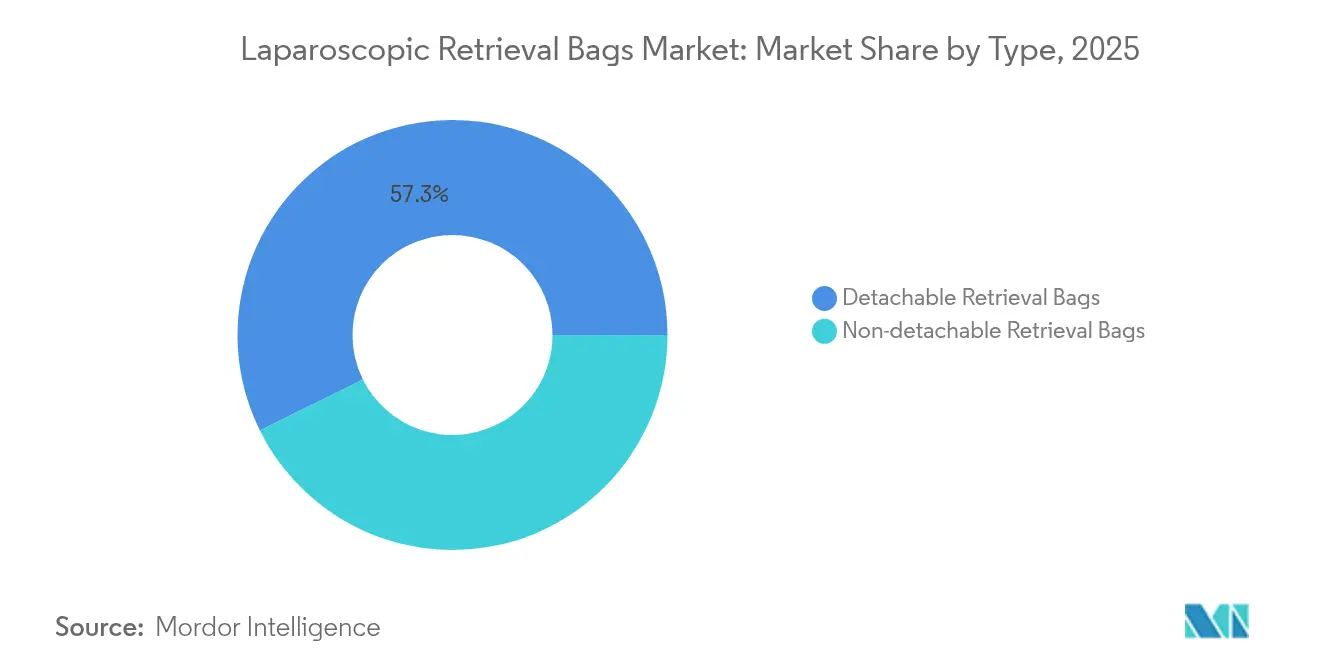

- By type, detachable systems captured 57.32% of laparoscopic retrieval bags market share in 2025, whereas the same segment is projected to expand at an 8.01% CAGR through 2031.

- By technique, manual opening commanded 61.88% of the laparoscopic retrieval bags market size in 2025, while automatic opening systems hold the highest forecast CAGR at 8.07% to 2031.

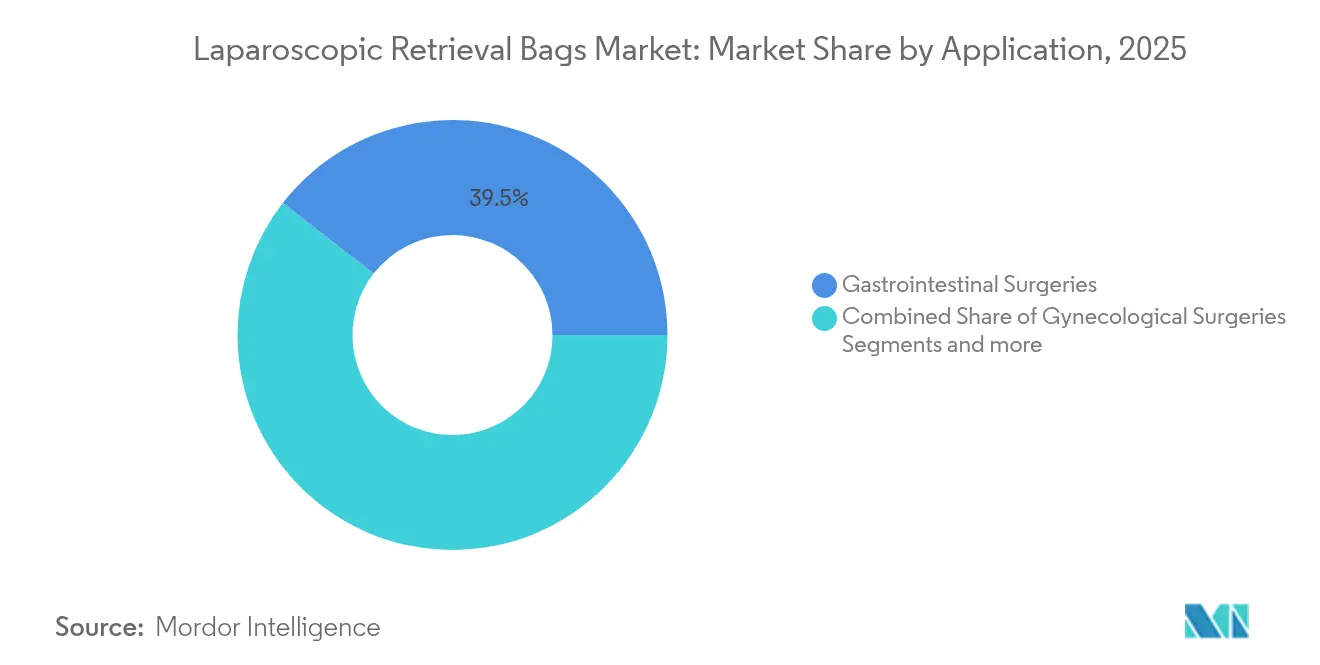

- By application, gastrointestinal surgery accounted for 39.48% share of the laparoscopic retrieval bags market size in 2025 and urology is advancing at an 8.08% CAGR through 2031.

- By end user, hospitals held 67.05% revenue share in 2025, yet ASCs record the quickest CAGR at 8.15% across the forecast span.

- By geography, North America commanded 40.76% share of the laparoscopic retrieval bags market size in 2025, while Asia-Pacific exhibits an 8.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laparoscopic Retrieval Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive surgery | +2.1% | Global with strongest effect in North America and Europe | Medium term (2-4 years) |

| Growing burden of target abdominal and pelvic diseases | +1.8% | Global, especially Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Expansion of ambulatory surgery centres worldwide | +1.2% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Technological advances in self-opening bag mechanisms | +0.9% | Global, led by United States, Germany and Japan | Short term (≤ 2 years) |

| Surge in regulations favouring single-use sterile devices | +0.6% | Europe and North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Development of biodegradable polymer retrieval bags | +0.4% | Global with early adoption in sustainability-focused markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally-Invasive Surgery

Minimally invasive techniques now represent more than 80% of select surgical categories in leading health systems, shortening length of stay by up to 3 days and lowering complication risk. New imaging platforms such as the EVIS X1 endoscopy system cleared by the FDA in 2025 have raised image quality standards, reinforcing surgeon confidence in laparoscopy [1]Olympus America, “EVIS X1 Endoscopy Platform Receives FDA Clearance,” olympusamerica.com. Training curricula increasingly centre on advanced laparoscopic skills, creating a workforce predisposed to prefer these methods. Each minimally invasive case typically necessitates a sterile extraction bag, which directly lifts unit consumption. In value-based payment environments, faster recovery and fewer infections underpin further procedure migration to laparoscopy, accelerating demand across the laparoscopic retrieval bags market.

Growing Burden of Target Abdominal & Pelvic Diseases

Colorectal cancer interventions have climbed by 15% year on year in developed economies, while gallbladder, appendiceal, and gynaecological cases add to the cumulative surgical volume. In Japan alone, the medical device sector reached USD 40 billion in 2021 and is tracking a 5.5% CAGR to 2027, signalling substantial procedure throughput growth [2]U.S. Department of Commerce, “Japan Medical Device Market,” commerce.gov. Rising obesity and diabetes rates contribute to metabolic and urological surgeries that also rely on specimen retrieval during laparoscopy. Asia-Pacific records the steepest epidemiological transition, compelling hospitals to expand theatre capacity and stock greater quantities of single-use retrieval consumables to avoid sterilisation bottlenecks.

Expansion of Ambulatory Surgery Centres Worldwide

ASC procedure throughput is forecast to surge 21%, touching 44 million cases by 2034 as payers embrace same-day discharge protocols. Their lean business model favours disposable kits free of reprocessing overhead, prompting vendors to recalibrate product lines toward low-cost, ready-to-use retrieval bags. Medicare’s widening reimbursement list for complex laparoscopic work further cements the outpatient trend. Suburban patient bases and transparent pricing strengthen ASC competitiveness, inserting new volume into the laparoscopic retrieval bags market and reshaping distribution patterns toward group purchasing entities serving ASC chains.

Technological Advances in Self-Opening Bag Mechanisms

Patent filings highlight vigorous R&D around spring-loaded, shape-memory and magnetic deployment systems that guarantee full bag opening irrespective of trocar angulation. Robotic platforms such as da Vinci 5 now integrate force-feedback, pushing suppliers to design bags that can synchronise with haptic signals. Olympus earned a 2024 patent on flexible inner shafts that embed cutting elements into detachable bag assemblies, underscoring the shift toward multifunctional retrieval solutions. Reliable automatic opening reduces dwell time inside the abdominal cavity, appealing to surgeons aiming to standardise outcomes and shorten anaesthesia exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High average selling price of premium retrieval bags | -1.2% | Global, strongest in price-sensitive emerging markets | Short term (≤ 2 years) |

| Availability of alternative specimen-removal techniques | -0.8% | Global, higher in cost-constrained systems | Medium term (2-4 years) |

| Environmental scrutiny over single-use plastics in ORs | -0.6% | Europe and North America, moving to wider markets | Medium term (2-4 years) |

| Limited compatibility with next-gen robotic trocars | -0.4% | North America and Europe where robotic use is high | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Average Selling Price of Premium Retrieval Bags

Automatic deployment features command 40-60% price premiums compared with manual bags, sparking push-back from procurement teams running cost-containment initiatives. Value-based contracts obligate vendors to furnish outcome evidence that offsets incremental spend, damping discretionary upgrades. Competitive pricing from Asian manufacturers tightens margins, while hospital formularies standardise on a narrow band of lower-cost SKUs to exploit volume discounts. This environment may temper the premium segment within the laparoscopic retrieval bags market until proven clinical advantages outweigh cost concerns.

Environmental Scrutiny Over Single-Use Plastics in ORs

Hospital sustainability committees are quantifying waste, spotlighting consumables like retrieval bags. Emerging EU packaging directives and electronic IFU requirements introduce compliance expenses for device makers [3]Emergo by UL, “EU Packaging and IFU Rules Tighten,” emergobyul.com . Although biodegradable polymers offer promising disposal benefits, regulators impose stringent biocompatibility tests that lengthen approval cycles. Health systems increasingly set waste-reduction targets, nudging purchasing departments toward vendors that commit to recycling or bio-safe materials. This adds CAPEX for R&D and may slow adoption unless performance parity with proven plastics is demonstrated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Detachable Designs Drive Market Leadership

Detachable designs captured 57.32% of laparoscopic retrieval bags market share in 2025, reflecting surgeon preference for specimen handling flexibility and compatibility with robot-assisted arms. This segment is forecast to post an 8.01% CAGR through 2031, outpacing the broader laparoscopic retrieval bags market. Innovation concentrates on secure fastening interfaces that withstand torque during extraction while enabling rapid separation once the bag reaches the umbilical port. Firms investing in robust latch geometries and radio-opaque markers facilitate fluoroscopic confirmation of complete removal, a feature valued in bariatric and oncological surgeries. Non-detachable bags occupy steady niches such as routine cholecystectomy where streamlined instrument counts matter more than modularity.

Continued miniaturisation of robotic wrists magnifies demand for slimline detachable bags that traverse 5 mm trocars without compromising specimen volume. Olympus’s flexible inner shaft technology exemplifies how detachable sub-components can incorporate active cutting or cautery, enhancing procedural efficiency while keeping bag integrity intact. As hospitals standardise on robotic theatres, the detachable cohort is expected to widen its contribution to the laparoscopic retrieval bags market size.

By Technique: Manual Opening Maintains Dominance Despite Automation Trends

Manual bags retained 61.88% of the laparoscopic retrieval bags market size in 2025 because of their familiar deployment and economical pricing, yet automatic formats post the sharpest growth at 8.07% CAGR. Manual devices benefit from simple mechanics and lower failure risk, making them the default in high-volume gallbladder or appendectomy programmes. Training curricula also reinforce comfort with traditional pull-string openings, sustaining share.

Automatic bags answer workflow variability concerns, particularly in robot-assisted suites where the surgeon operates from a console distant from the sterile field. Spring-triggered or SMA-driven rims guarantee mouth opening even at awkward angles, reducing need for ancillary grasper manipulation. Although higher cost deters deployment in budget-sensitive settings, university hospitals piloting standardised robotic pathways increasingly stipulate automatic bags for consistency. Patent activity from Boston Scientific on novel seal assemblies illustrates the competitive importance of reliability in auto-open categories. Broader availability of low-priced auto-open SKUs is expected to tilt incremental demand toward the segment over the forecast horizon.

By Application: Gastrointestinal Procedures Lead While Urology Accelerates

Gastrointestinal surgeries represented 39.48% of total consumption in 2025, securing their position as the largest application by virtue of high cholecystectomy and colorectal volumes. The segment’s entrenched laparoscopy protocols keep it a pillar of vendor sales pipelines. Hospitals purchase multiple bag sizes to accommodate variable specimen mass ranging from gallstones to partial colectomy samples, reinforcing repeat-purchase cycles within the laparoscopic retrieval bags market.

Urology, posting an 8.08% CAGR, overtakes competing specialties in growth velocity as prostatectomies and nephrolithotomies migrate to minimally invasive pathways. Reduced port diameters and delicate tissue handling requirements trigger the need for thin-film, puncture-resistant bags. Suppliers that tailor mouth diameters and deploy ease for confined pelvic spaces gain traction with urological surgeons. Focus on rapid stone extraction stimulates design tweaks such as reinforced seams and graduated capacity indicators that promote safe over-loading thresholds. Close collaboration between device engineers and urologists is therefore pivotal to sustain momentum in this high-growth niche.

By End User: Hospital Dominance Faces ASC Challenge

Hospitals generated 67.05% of total revenue in 2025 because complex oncological and bariatric procedures remain centralised in tertiary centres that possess full critical-care back-up. Integrated purchasing departments favour bundled device portfolios, allowing multinationals such as Johnson & Johnson to cross-sell retrieval bags alongside trocars and staplers. Research collaborations and clinical trial pipelines also bias hospitals toward premium auto-open devices that support protocol consistency.

ASCs, however, are projected to outpace with an 8.15% CAGR as same-day laparoscopy becomes mainstream. These centres prize consistent per-case cost and minimal reprocessing downtime, driving preference for single-use retrieval kits packaged with ancillary tools. The anticipated rise to 44 million ASC procedures by 2034 opens a fertile channel for mid-tier manufacturers able to supply quality-to-price optimised offerings. Suppliers investing in compact, all-inclusive sterile bags that shrink setup time align squarely with ASC workflow priorities.

Geography Analysis

North America posted 40.76% of global revenue in 2025, underpinned by high adoption of robotic-assisted surgery and favourable reimbursement that offsets premium consumable costs. FDA clarity on single-use device pathways accelerates time to market, and institutional review boards often require sterile retrieval for specimen integrity, supporting predictable purchasing volumes. Cross-selling across extensive device portfolios grants established vendors stable contracting leverage with group purchasing organisations.

Asia-Pacific leads growth at an 8.19% CAGR to 2031 thanks to aggressive capital expenditure on surgical infrastructure in China, India and Japan. The Japanese medical device market’s 5.5% CAGR through 2027 reflects a demographic imperative for gastrointestinal and urological procedures among ageing citizens. China’s climb toward a USD 210 billion device market by 2025 continues to open quota opportunities for international brands that localise production. India’s updated medical device ethical marketing code encourages transparency, smoothing import approvals and catalysing adoption of high-quality retrieval consumables. Public–private partnership hospitals in tier-2 cities present untapped volume pockets, further enlarging the laparoscopic retrieval bags market.

Europe shows moderate expansion driven by stringent MDR compliance that rewards quality and safety. Sustainability goals spur trials of biodegradable polymers, creating a differentiating avenue for innovators. Fragmented reimbursement across member states pressures vendors to present clear health-economic data, but consistent clinical guidelines on minimally invasive cancer surgery preserve baseline demand. Middle East, Africa and South America combine emerging private hospital chains and government modernisation schemes to supply long-run upside, though currency volatility and procurement bureaucracy can temper near-term shipments.

Regulatory Landscape

In the United States, laparoscopic specimen retrieval bags are regulated as Class II devices under FDA product code GCJ (21 CFR 876.1500), with market entry commonly pursued through the 510(k) pathway demonstrating substantial equivalence to predicate devices. Recent FDA activity within this product code includes 510(k) clearances such as DANNIKs laparoscopic single-use poly specimen retrieval system (K250411, February 2025) and Ximedicas ENDOCOLLECT specimen retrieval bag (K240635, April 2024), which continue to reflect an ongoing cadence of size, introducer, and material configurations moving through established premarket review.

In Europe, the primary framework is Regulation (EU) 2017/745 (MDR), requiring CE marking supported by technical documentation aligned to Annexes II and III and conformity with the General Safety and Performance Requirements (GSPR) in Annex I. MDR post-market obligations, including PSUR expectations for applicable device classes, and Notified Body scrutiny raise the bar for clinical evaluation, sterilization validation, and biocompatibility evidence (commonly aligned to ISO 10993) for single-use sterile consumables such as retrieval bags. In 2026, MDR implementation guidance continued to evolve, including Team-NBs April 2026 update to its best-practice guidance on MDR technical documentation, which affects how manufacturers structure and maintain dossiers during certification and surveillance cycles.

Competitive Landscape

The field remains moderately fragmented. Ethicon and Medtronic maintain strong share via expansive laparoscopic portfolios and entrenched relationships with IDNs and academic centres. Their ability to bundle scopes, trocars and staplers with retrieval bags shortens tender cycles and stabilises margins. Mid-sized players concentrate on differentiated features such as bioresorbable films or ultra-low-profile hoods tailored for single-incision surgery.

Intellectual property jockeying intensifies around deployment reliability, antimicrobial coatings and eco-friendly materials. Boston Scientific’s patent on medical seal assemblies that integrate controlled film release positions the firm to venture deeper into specimen extraction accessories. Start-ups emphasise compostable polymers and carbon-neutral manufacturing, seeking early-adopter hospitals pursuing ESG targets. Meanwhile, global players pilot recycling schemes that offset sustainability objections while protecting the single-use business model, exemplified by Ethicon’s 2025 take-back programme.

Strategic M&A continues: Medtronic’s USD 850 million purchase of Fortimedix Surgical in 2024 bolstered its minimally invasive platform with complementary energy devices that pair well with retrieval products. Partnerships with robotic firms also shape competitive dynamics, as compatibility certification can lock in consumable sales over multi-year service contracts. Overall, competition hinges on marrying clinical efficacy, cost-effectiveness and sustainability to win formulary placement.

Laparoscopic Retrieval Bags Industry Leaders

Johnson & Johnson

Medtronic

Richard Wolf GmbH

Vernacare

Purple Surgical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are building around products that reduce spillage risk and standardize retrieval in constrained access workflows, particularly as robotic-assisted and single-port techniques increase expectations for reliable deployment and controlled extraction. The 2026 signals described in the report include publication of a patent application for a laparoscopic tissue retrieval bag with integrated lifting bands to elevate the distal end of the bag for easier cutting and removal (published March 2026), aligning with a design focus on ergonomics and time-in-cavity reduction. Against the backdrop of automatic and self-opening trends already highlighted, this points to differentiation potential via reinforced film architectures, improved puncture resistance, and introducer profiles better matched to 5 mm access and next-generation trocar geometries.

Sustainability and documentation readiness are also becoming practical buying criteria, which creates room for vendors that combine single-use sterility with waste-reduction programs or materials innovation while meeting EU MDR technical documentation expectations. Ethicons 2025 extension of surgical-instrument recycling activity, together with the report-noted exploration of biodegradable polymers, shows how ESG-led procurement pressures are translating into supplier programs and R&D themes, even as performance and validation requirements remain stringent. In parallel, clinical discussions in minimally invasive gynecology around tissue containment and transabdominal manual morcellation are increasing focus on bag durability and containment behavior, supporting demand for purpose-built sizes, reinforced seams, and clearer performance labeling for higher-fragmentation specimen handling scenarios.

Recent Industry Developments

- May 2026: Surgical Principals, Inc. updated FDA GUDID device information for a LaproSac specimen retrieval pouch configuration (EMP300-RGD-3). The update indicates continued portfolio maintenance around sizing and pouch formats used in laparoscopic specimen extraction, supporting catalog breadth for tenders and formulary alignment in high-throughput OR settings.

- February 2025: DANNIKs received FDA 510(k) clearance (K250411) for its laparoscopic single-use poly specimen retrieval system under product code GCJ. The clearance expands the cleared competitive set for disposable retrieval systems and reinforces the 510(k) pathway as the primary route for differentiated single-use configurations in this category.

- April 2024: Ximedica received FDA 510(k) clearance (K240635) for the ENDOCOLLECT specimen retrieval bag offered in multiple diameters (8 mm, 12 mm, and 15 mm). Multi-size clearance supports broader procedure coverage across gastrointestinal, gynecologic, and urologic laparoscopy, strengthening supplier positioning with hospitals and ASCs that standardize around disposable extraction kits.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from laparoscopic retrieval bags used during minimally invasive surgeries to capture and remove tissue or specimens through trocar access. Revenue is counted at the point of sale to hospitals and other care settings.

Scope exclusions: Open-surgery specimen bags, non-sterile lab collection bags, and non-bag retrieval tools are excluded from this sizing.

Segmentation Overview

- By Type

- Detachable Retrieval Bags

- Non-detachable Retrieval Bags

- By Technique

- Manual Opening

- Automatic Opening

- By Application

- Gastrointestinal Surgeries

- Gynecological Surgeries

- Urological Surgeries

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, understand procedure volumes, and build a clean assumption set around usage of retrieval bags per case. We referenced public sources such as CDC procedure statistics, OECD health data, WHO health indicators, and national health ministry publications that track surgical throughput and hospital activity. We also reviewed peer-reviewed surgical journals to understand how retrieval bags are used by procedure type (for example, GI, gynecology, and urology) and to check adoption of containment practices.

On the supply side, we used company annual reports, investor presentations, product catalogs, and regulatory or recall notices to map product types and typical pricing corridors. A paid company financials and intelligence subscription was used selectively to standardize company revenue splits and to screen for smaller firms that do not publish detailed segment revenue. The desk sources listed here are illustrative only, and many additional public references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on validating what the desk sources cannot show clearly, the real purchase pattern by facility type and how pricing shifts with bag size, opening mechanism, and single-use sterilization requirements. We spoke with a mix of procurement leads, OR managers, surgeons, distributors, and product specialists across major regions. This helped triangulate usage per laparoscopic case, conversion toward self-opening designs, and typical tender timing, which were then applied consistently in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 44% |

| Mid tier: 53% | Functional/Unit leaders: 42% | EMEA: 29% |

| Smaller Players: 15% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

For sizing, we start with a top-down build that reconstructs the addressable demand pool from laparoscopic procedure volumes by major surgery groups and then applies an average bags-per-procedure factor by setting of care. After that, the totals are converted to value using average selling price ranges that differ by bag type (detachable versus non-detachable), opening technique (manual versus automatic), and common size mix. Where procedure data is reported in different formats across countries, we align it using population normalization and hospital activity indicators, then apply conservative adjustments that were validated in calls.

To keep the output realistic, we use selective bottom-up approximations as a check. These include channel feedback on unit volumes, sampled price lists from public tenders where available, and supplier revenue reasonableness versus known geographic exposure. Key model inputs include minimally invasive surgery penetration, ambulatory surgery center share, typical trocar size patterns that influence bag sizing, single-use versus limited reuse policies, and annual price movement driven by tender cycles and material costs. Forecasts are generated using scenario analysis supported by short time series smoothing, where procedure growth expectations and mix shift toward automatic opening bags are varied within ranges described by interviewees as likely. Any gaps in smaller country coverage are handled by proxying from comparable healthcare spend and procedure intensity, followed by a second pass review to avoid over-counting.

Data Validation & Update Cycle

Validation is done through multiple checks that are easy to explain and repeat, and the goal is to catch scope leaks and unrealistic pricing. We compare modeled market totals against independent signals such as procedure growth, hospital consumables spending direction, and import patterns where they are meaningful. We then revisit outliers by country or application until the driver is understood. When a major assumption changes, for example a shift in tender pricing, a sharp currency movement, or a procedural guideline update, respondents are re-contacted to confirm whether the change is temporary or structural.

Before sign-off, the model and assumptions are reviewed by another analyst, and the narrative is aligned to what the numbers are actually showing. Reports are refreshed annually, with interim updates when material events occur that can move demand or pricing. Right before delivery, a final pass is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Laparoscopic Retrieval Bags Market Sizing Compared With Other Published Estimates

Published values for laparoscopic retrieval bags can look far apart because the timing of the numbers, the currency conversion point, and how pricing is averaged across bag types are not handled the same way. Even when two studies use a similar procedure driven logic, the choice of base year and the mix assumptions for manual versus automatic opening designs can shift the final dollar total.

In practice, the spread usually comes from three places. First, whether ambulatory centers and smaller outpatient facilities are fully counted. Second, how detachable and non-detachable bags are priced when tenders reset mid-year. Third, how often assumptions are rechecked against real purchase behavior. When model inputs are refreshed close to publication, with a consistent FX timing and a clear ASP build by type and technique, fewer hidden step changes remain. This is why the update cadence used by Mordor Intelligence tends to land closer to what procurement teams describe for recent quarters.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.56 B (2026) | |

| Global Consultancy A | USD 0.31 B (2025) | Uses an earlier base year and appears to apply a lower blended ASP, which can happen when outpatient purchasing and premium self-opening designs are underweighted in the price mix. |

| Industry Publisher B | USD 0.51 B (2024) | Anchors the estimate to a different year and may not normalize FX timing and tender resets consistently, which can compress the step-up seen when procedure volumes and price points move together. |

Across the three figures, the main pattern is that year selection and pricing mix choices explain most of the difference, not a fundamentally different demand story. By tying the value build to procedure volumes, facility mix, and a transparent ASP ladder that can be rechecked in interviews, we keep the final number traceable to inputs that can be updated and repeated.

Key Questions Answered in the Report

What is the current value of the laparoscopic retrieval bags market in 2026?

The laparoscopic retrieval bags market size is USD 559.8 million in 2026 and is projected to reach USD 805.88 million by 2031.

Which segment grows fastest within retrieval bag techniques?

Automatic opening systems register the highest CAGR at 8.07% through 2031 owing to robotic surgery integration.

Why are detachable retrieval bags preferred by surgeons?

Detachable designs allow independent specimen manipulation, reduce extraction torque and align well with robot-assisted workflows.

Which region shows the strongest growth outlook?

Asia-Pacific posts the fastest regional CAGR at 8.19% driven by healthcare infrastructure expansion in China, India and Japan.

How do ambulatory surgery centres influence demand?

ASCs favour single-use, cost-efficient retrieval kits, propelling an 8.15% CAGR in this end-user segment as day-case laparoscopy rises.

What sustainability actions are key suppliers taking?

Leading companies are piloting recycling programmes and researching biodegradable polymers to address environmental scrutiny over single-use plastics.

Page last updated on: