Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Speaker Market in Tablets Report is Segmented by Product Type (Dynamic Speakers, Balanced Armature Speakers, and More), Driver Size (Less Than 15 Mm, 15-25 Mm, and Greater Than 25 Mm), Application (Consumer/Personal, Education, Enterprise/Industrial, and Gaming/Cloud-gaming Tablets), Sales Channel (OEM Integrated, and After-market/Replacement), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

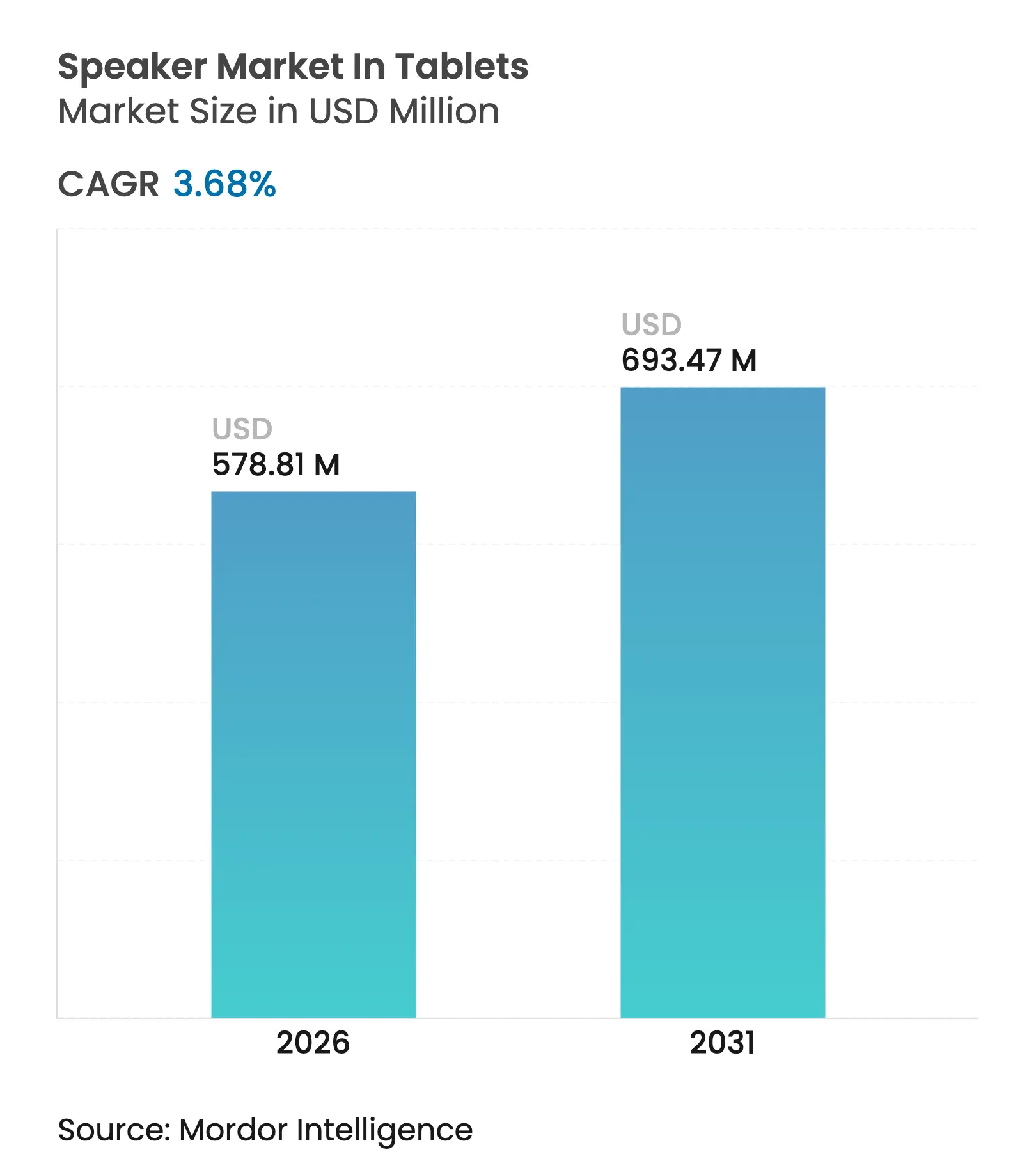

| Market Size (2026) | USD 578.81 Million |

| Market Size (2031) | USD 693.47 Million |

| Growth Rate (2026 - 2031) | 3.68 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The speaker market size in tablets size in 2026 is estimated at USD 578.81 million, growing from 2025 value of USD 558.27 million with 2031 projections showing USD 693.47 million, growing at 3.68% CAGR over 2026-2031. The return to growth stems from hybrid-work persistence, state-funded digital classrooms, and the mainstreaming of spatial-audio gaming, collectively reversing the brief pandemic-era contraction. Dynamic speakers still anchor most bill-of-materials decisions, yet MEMS advances finally cross the commercial viability threshold, tilting new design wins toward solid-state transducers. OEMs also re-evaluate supply resilience, diversifying magnet sourcing and co-designing ASIC amplifiers that unlock higher output from smaller drivers. Opportunities concentrate in Asia–Pacific, where classroom bulk orders, white-label gaming tablets, and cost-optimized component ecosystems converge. However, rising labor costs and component inflation keep margin pressures high, forcing tier-two suppliers either to embrace automated MEMS lines or exit the speaker market in tablets altogether.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Work-from-home and e-learning surge Work-from-home and e-learning surge | +0.80% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.80% | Geographic Relevance:Global, with concentration in Asia-Pacific and North America | Impact Timeline:Medium term (2-4 years) |

High-resolution streaming audio demand High-resolution streaming audio demand | +0.60% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) | |||

MEMS micro-speaker design breakthroughs MEMS micro-speaker design breakthroughs | +0.40% | Global, led by Asia-Pacific manufacturing hubs | Long term (≥ 4 years) | |||

Spatial-audio tablet design adoption Spatial-audio tablet design adoption | +0.50% | North America and EU, with Asia-Pacific adoption following | Medium term (2-4 years) | |||

Emerging-market digital classroom subsidies Emerging-market digital classroom subsidies | +0.30% | Asia-Pacific core, spill-over to MEA and Latin America | Short term (≤ 2 years) | |||

Growth of gaming-centric detachable tablets Growth of gaming-centric detachable tablets | +0.20% | Global, with early gains in North America and China | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Work-from-home and e-learning surge

Hybrid work has hardened into standard practice for many corporations; weekly video-meeting hours remain 54 % above the 2019 baseline, so tablet acoustics matter more than ever for intelligible speech. Simultaneously, public-sector education ministries in India, Indonesia, and Thailand budget for millions of classroom tablets, each with minimum loudness specs to accommodate group listening. Indian ed-tech investment nearly doubled to USD 164 million in H1 2024, signaling durable hardware procurement. Those parallel streams-enterprise and classroom-underwrite steady unit volumes even when consumer refresh cycles lengthen.

High-resolution streaming audio demand

Lossless catalogs on Apple Music and Amazon Music HD prime consumers to expect full-range fidelity from every mobile screen. The Japan Audio Society’s Hi-Res Audio seal rapidly appears on premium tablets, nudging OEMs to adopt wide-bandwidth speaker modules. Bluetooth LE Audio and aptX Adaptive codecs preserve that fidelity wirelessly, so distortion in built-in speakers becomes a purchase deterrent. Resulting upgrades in enclosure volume and tweeter count keep average selling prices buoyant inside the speaker market in tablets.

MEMS micro-speaker design breakthroughs

xMEMS Labs’ Sycamore driver compresses a full-range transducer into a 6 × 6 × 1 mm die, 1⁄7 the height of legacy coils, yet posts 22 kHz bandwidth and 120 dB SPL peaks.[1]Mark Hachman, “xMEMS Labs Unveils Game-Changing Silicon Innovations at CES,” PCWorld, pcworld.com Wafer-level assembly erases coil-winding labor and cuts ±1 dB unit variance, appealing to OEM yield targets. With unit costs forecast to fall below USD 0.90 by 2027, MEMS parts win more sockets, lifting the fastest-growing product category within the speaker market in tablets.

Spatial-audio tablet design adoption

Apple’s iPad line bakes dynamic head-tracking into multichannel arrays, normalizing 3D soundscapes for video and gaming. Android peers license Dolby Atmos or Dirac spatial engines, installing quad or hex driver sets that rely on precise phase alignment. Each extra driver multiplies transducer demand, providing a structural uplift even if total tablet shipments plateau. Gamers prize directional cues, and streaming services promote Atmos mixes to upsell subscriptions, reinforcing OEM incentives to maintain multi-speaker designs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Smartphone substitution effect Smartphone substitution effect | -1.20% | Global, particularly pronounced in mature markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.20% | Geographic Relevance:Global, particularly pronounced in mature markets | Impact Timeline:Long term (≥ 4 years) |

Inflation and supply-chain volatility Inflation and supply-chain volatility | -0.90% | Global, with acute impact on Asia-Pacific manufacturing | Short term (≤ 2 years) | |||

Shift to wireless earbuds Shift to wireless earbuds | -0.80% | Global, led by North America and EU adoption | Medium term (2-4 years) | |||

Ultra-thin bezel acoustic limits Ultra-thin bezel acoustic limits | -0.40% | Global, affecting premium tablet segments | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Smartphone substitution effect

Average smartphone diagonals now hit 6.8 inches, encroaching on small-tablet territory and reducing the need for a second screen. Flagship handsets ship with dual speakers and virtual surround, shrinking the acoustic delta versus tablets.[2]Research Group, “Microspeaker Design and Performance Analysis,” IEEE Xplore, ieee.org This erosion is most acute in mature markets, shaving 0.9 percentage points off the projected CAGR for the speaker market in tablets.

Inflation and supply-chain volatility

Neodymium magnet prices spiked 18 % between Q3 2023 and Q2 2024, while rolling lockdowns in Guangdong extended lead times for driver assemblies to 18 weeks.[3]Staff Report, “Supply Chain Disruptions in Electronics Manufacturing,” Reuters, reuters.com OEMs respond by trimming premium-audio options on entry-level tablets, tempering revenue growth even as unit shipments rise.

By Product Type: Dynamic Speakers Maintain Dominance While MEMS Accelerate

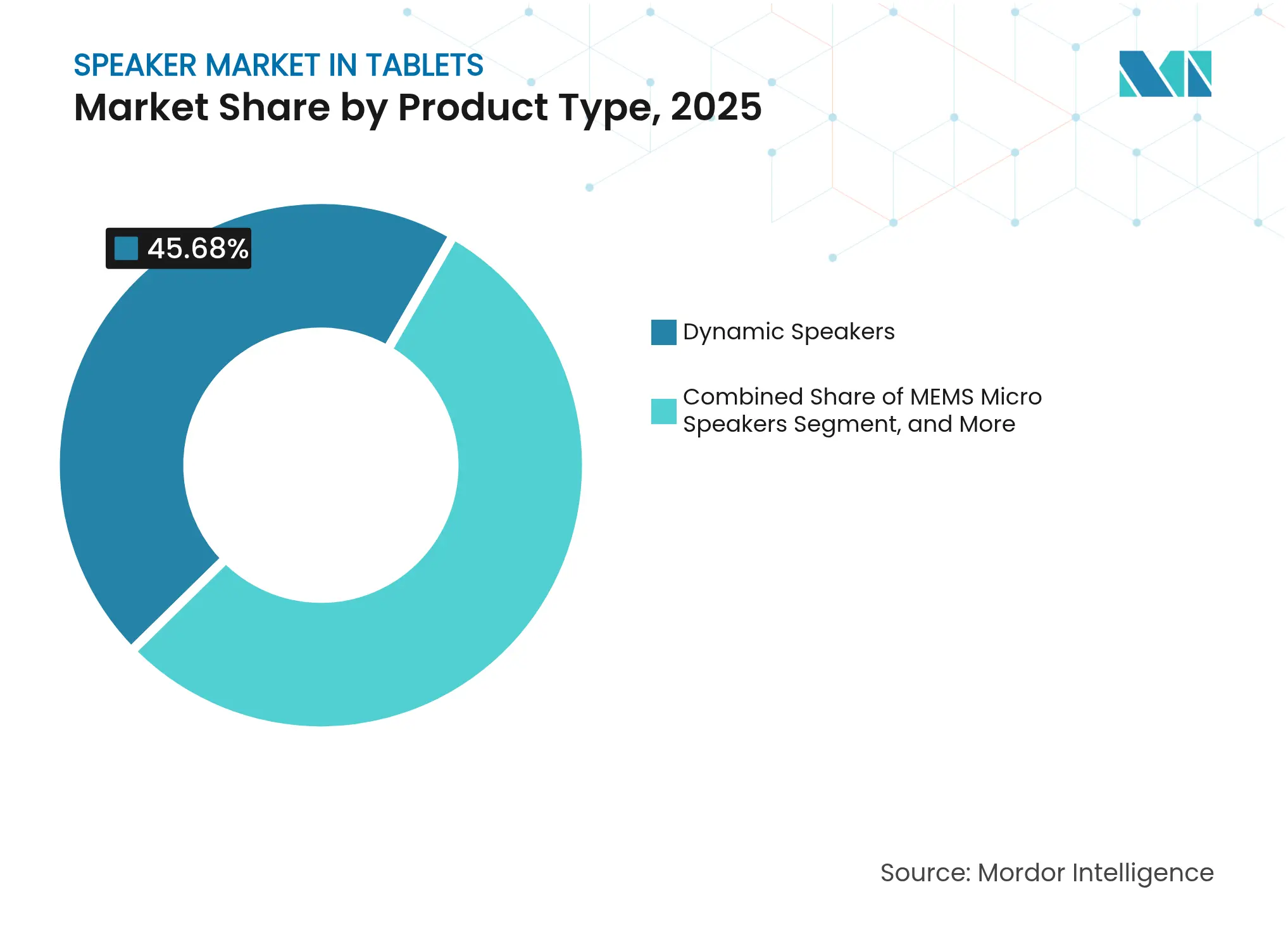

Dynamic speakers still hold 45.68% of the speaker market in tablets share, equivalent to USD 254.93 million in 2025 revenue, leveraging decades-old supply chains and cost-optimized coil-magnet architectures. MEMS micro-speakers, now expected to grow 4.71% CAGR, gain design wins in ultrathin detachables and premium e-readers where every millimeter counts. Balanced-armature units serve voice-first productivity tablets that emphasize mid-band clarity, whereas electrostatic options remain the high-cost, audiophile niche.

The competitive interplay intensifies as MEMS suppliers achieve BOM parity by 2027. Dynamic vendors counter with shorter air-gap magnets and LCP diaphragms to extend bandwidth without raising depth. OEMs likely continue splitting portfolios: dynamic for cost-sensitive SKUs, MEMS for halo models, each side reinforcing the speaker market in tablets rather than cannibalizing it.

Note: Segment shares of all individual segments available upon report purchase

By Driver Size: Mid-Range Dominance Meets Sub-15 mm Momentum

Drivers between 15 mm and 25 mm controlled 51.05% of the 2025 shipment value, balancing enclosure volume with bass reach. Yet the less-than-15 mm class will pace the field at a 4.92% CAGR, aided by spatial-audio tablets that stack multiple small drivers for beamforming. IEEE modeling shows a 3 mm diameter cut doubles cone excursion at equal SPL, but MEMS designs offset this with rigid silicon diaphragms. Larger-than-25 mm units persist in performance slates, though weight penalties limit mainstream adoption.

By Application: Gaming Tablets Outstrip All Other Niches

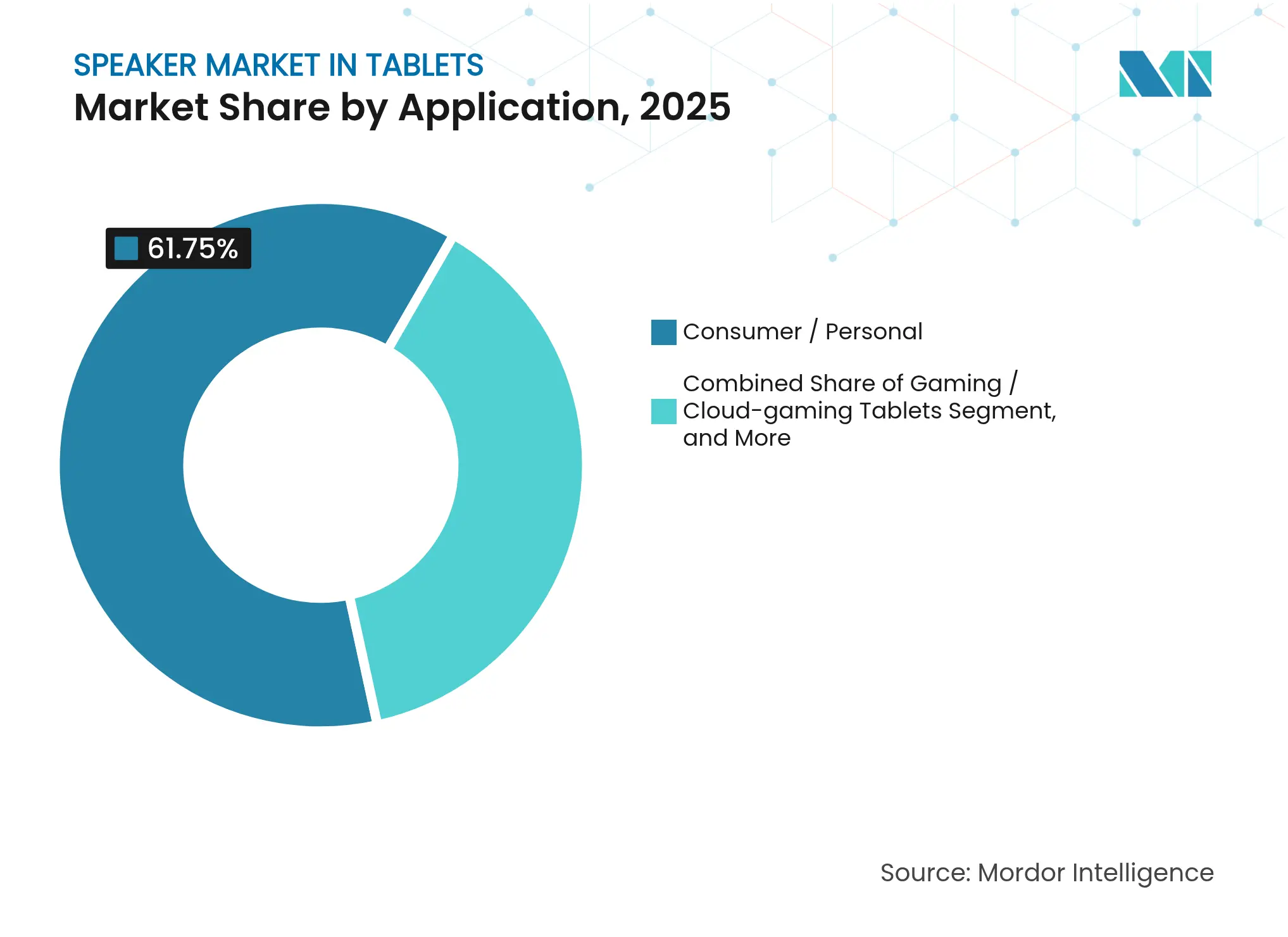

Consumer/personal use retained a 61.75% share, yet gaming/cloud-gaming tablets are set to leap 6.21% CAGR. Steam Deck’s viral success and Qualcomm’s XR2 Gen 2 gaming SoC validate portable AAA gameplay. Gamers demand quad-speaker Atmos rigs, injecting higher ASPs into each sale. Education tablets grow steadily under government tenders, but tight unit pricing restricts high-end acoustic modules. Enterprise/industrial slates prioritize durability over fidelity, generating limited transducer ASP uplift.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Aftermarket Glimpses New Life

OEM-integrated speakers still own 82.45% of the speaker market in tablets size, yet the aftermarket’s 5.88% CAGR signals fresh demand from DIY upgrade kits and right-to-repair legislation in the EU and select U.S. states. As component miniaturization simplifies adhesive-backed module swaps, specialty retailers bundle high-SPL replacements that slot into existing cutouts without jeopardizing FCC or CE compliance. Although the aftermarket remains small, its growth pace adds incremental upside.

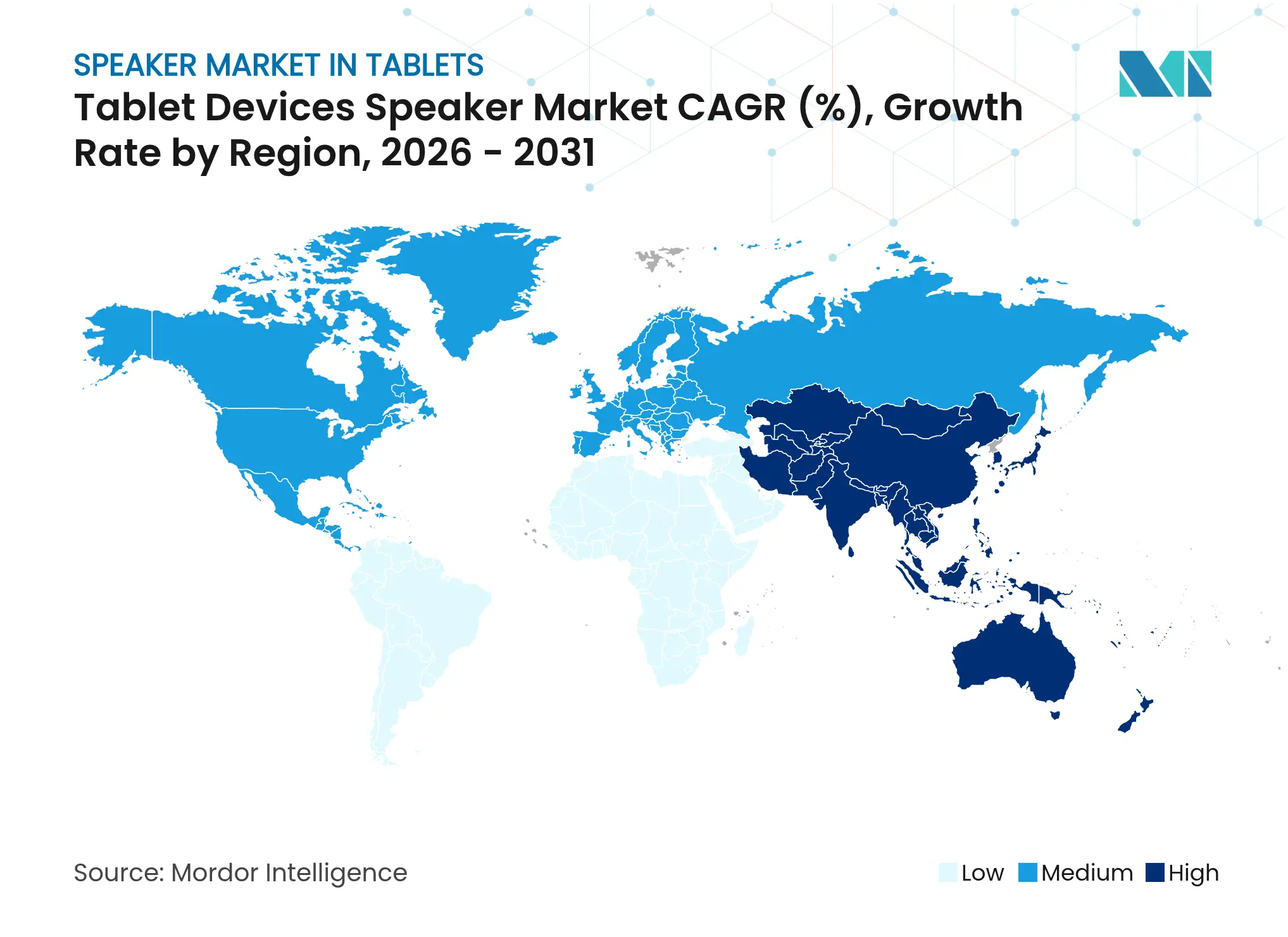

Asia–Pacific accounted for 38.12% of 2025 revenue, equal to USD 212.78 million, and is forecast to grow 6.62% CAGR. Chinese OEMs posted 73.1% shipment expansion for Xiaomi and 29.3% for Huawei, reinforcing the region’s dominance. India’s “PM eVidya” digital-classroom plan earmarks USD 1.1 billion through 2027, ensuring rolling tenders for speaker-equipped tablets. Component clusters in Shenzhen and Suzhou shorten design cycles, enabling rapid MEMS integration once costs align.

North America remains the value leader in premium tiers. Consumers here gravitate to iPad-class acoustics and early spatial-audio rollouts. ASPs sit 22 % above global norms, cushioning suppliers from volume fluctuations. Local MEMS startups partner with U.S. fabs to secure Defense Production Act incentives, seeding new capacity for 2026-2028.

Europe mirrors North America’s premium preference but layers in eco-design mandates. OEMs must document magnet provenance and recyclability per the EU Circular Electronics Initiative, nudging them toward wafer-level MEMS parts that simplify end-of-life teardown. Latin America and the Middle East and Africa remain volume-light yet gains can be lumpy; Brazil’s EduTech program and Saudi Arabia’s Vision 2030 both feature multimedia tablets, creating batch procurement spikes.

Market Concentration

The speaker market in tablets shows moderate concentration: the top five suppliers control a major market share. AAC Technologies and Goertek dominate dynamic micro-drivers, benefitting from shared R&D with smartphone contracts.

Knowles leverages balanced-armature intellectual property, while Foster Electric and TDK diversify into automotive audio to buffer cyclical consumer demand. MEMS challengers, xMEMS Labs, USound, Audio Pixels, license IP to foundries, betting on Moore-style cost curves for acoustic silicon.

Competitive strategies skew toward vertical bundles. Goertek’s joint venture with a Shenzhen DSP startup embeds proprietary tuning into amplifiers, locking OEMs into its speaker catalog. Qualcomm integrates speaker protection algorithms into Snapdragon SoCs, standardizing reference designs that quietly specify preferred driver vendors. Patent portfolios around MEMS diaphragm structures trigger cross-licensing talks as shipments climb. The fight now pivots less on magnet strength, more on firmware and supply resilience.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Transducers that convert electrical signals into sound are called micro speakers. They are used in different consumer electronics as well as for other applications.

The market study considers the micro speakers used in the production of tablets, including both legacy micro speakers and MEMS micro speakers used in tablets.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.