Microspeaker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.17 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

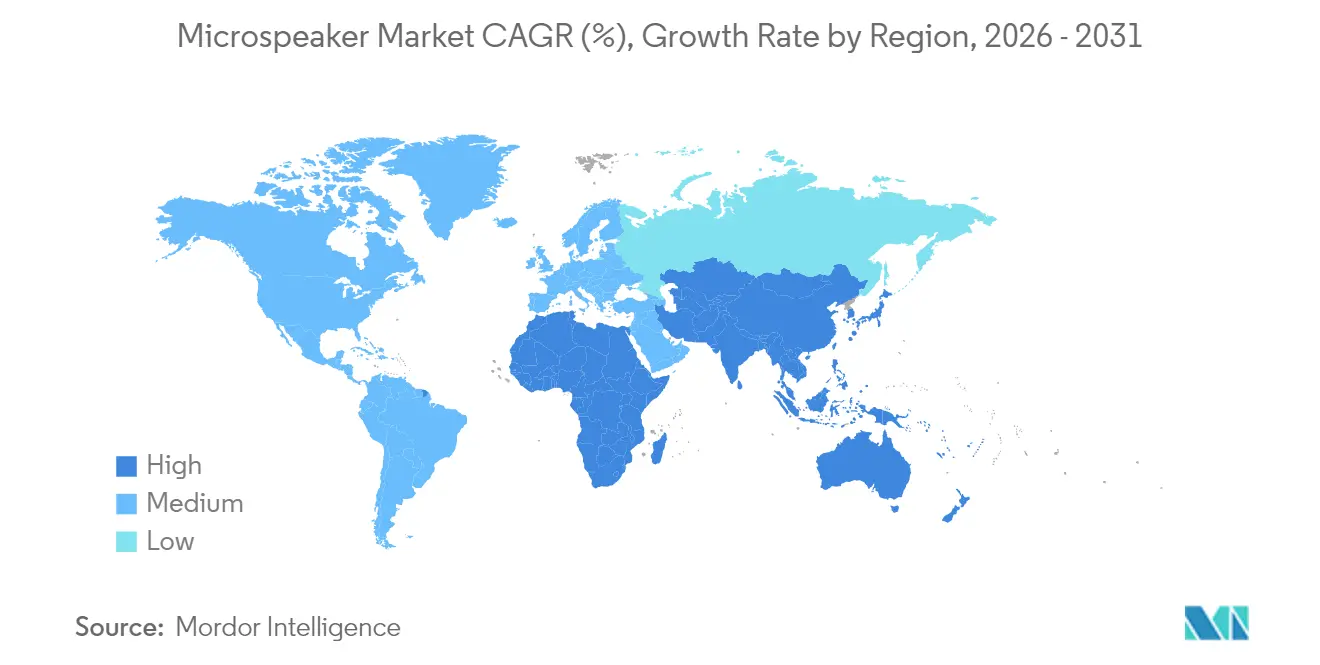

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

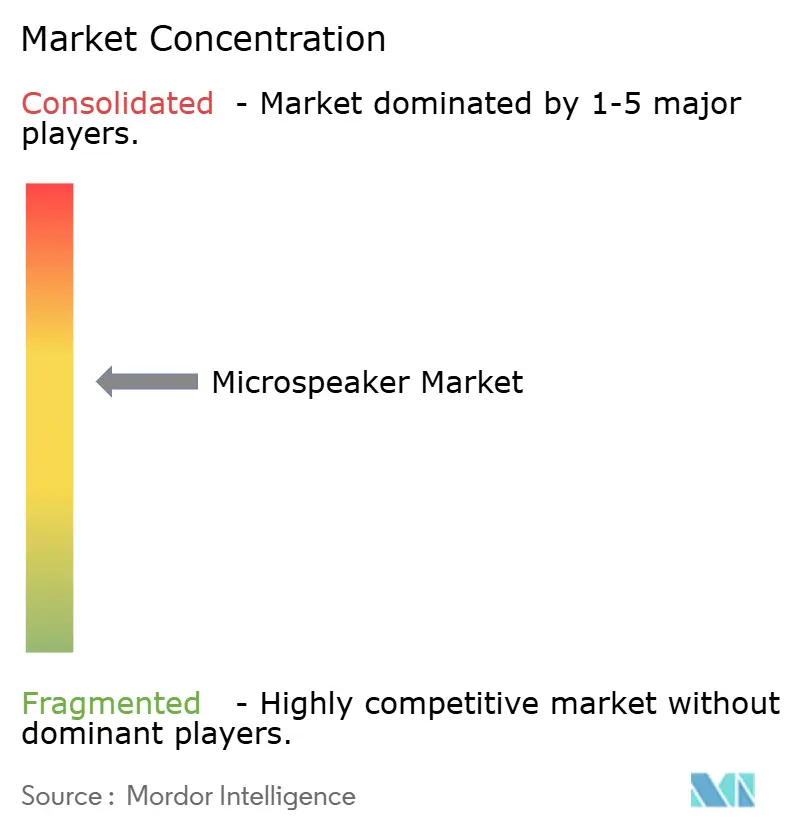

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microspeaker Market Analysis by Mordor Intelligence

The microspeaker market size is expected to grow from USD 3.98 billion in 2025 to USD 4.17 billion in 2026 and is forecast to reach USD 5.23 billion by 2031 at 4.66% CAGR over 2026-2031. Rising demand for solid-state MEMS and piezoelectric thin-film transducers, which lower energy use by 50% and enable sub-10 millimeter form factors, is reinforcing this growth trajectory. True wireless stereo (TWS) earbud shipments of 331.6 million units in 2024 highlight how hearables are displacing wired audio and creating a pull-through for next-generation components. Automotive OEMs are miniaturizing cabin audio by embedding headrest and pillar speakers, while the United States Food and Drug Administration’s over-the-counter (OTC) hearing-aid framework has opened a sizable retail channel for balanced-armature and MEMS speakers optimized for speech intelligibility. Supply-chain pivot points pecifically magnet scarcity and counterfeit risks continue to influence pricing strategies and technology choices, shaping how incumbents and new entrants allocate capital.

Key Report Takeaways

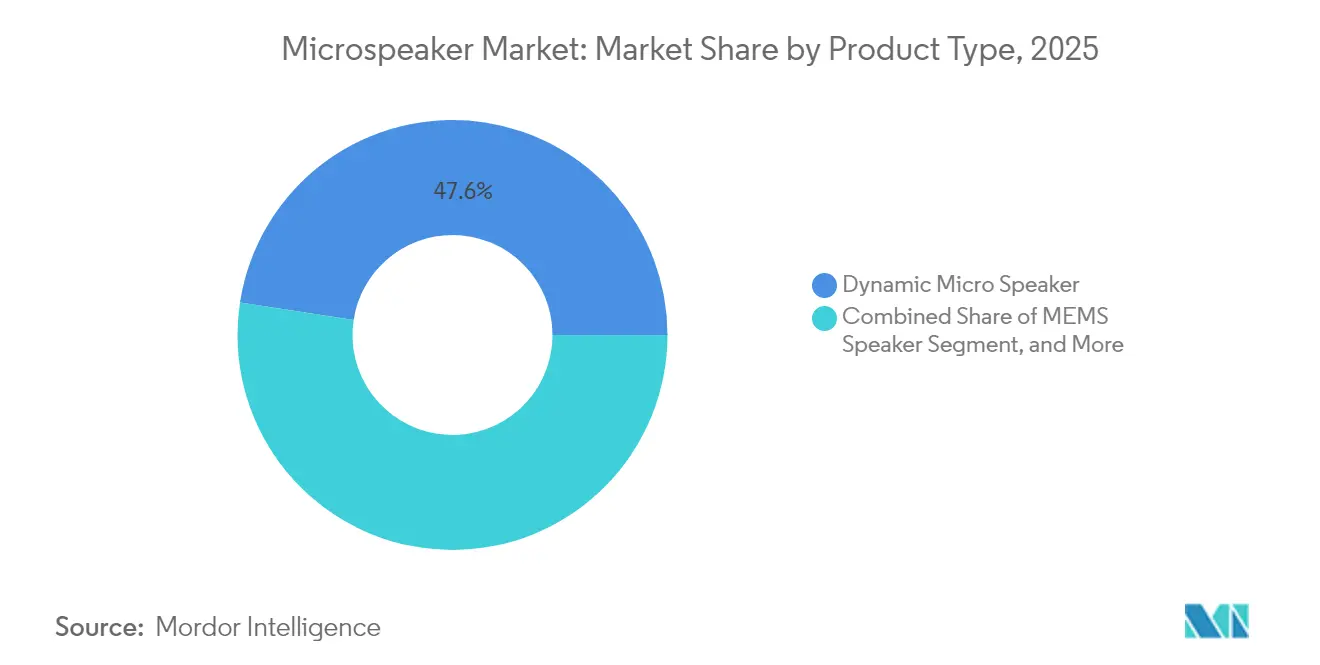

- By product type, Dynamic Micro Speakers led with 47.59% revenue share in 2025; MEMS Speakers are forecast to advance at a 5.14% CAGR through 2031.

- By technology, Electrodynamic configurations accounted for a 59.82% microspeaker market share in 2025, whereas Piezoelectric Thin-Film solutions are set to expand at a 5.98% CAGR to 2031.

- By application, Smartphones and Tablets captured 44.01% of demand in 2025, while Wearables and Hearables are projected to grow at a 5.67% CAGR over the same horizon.

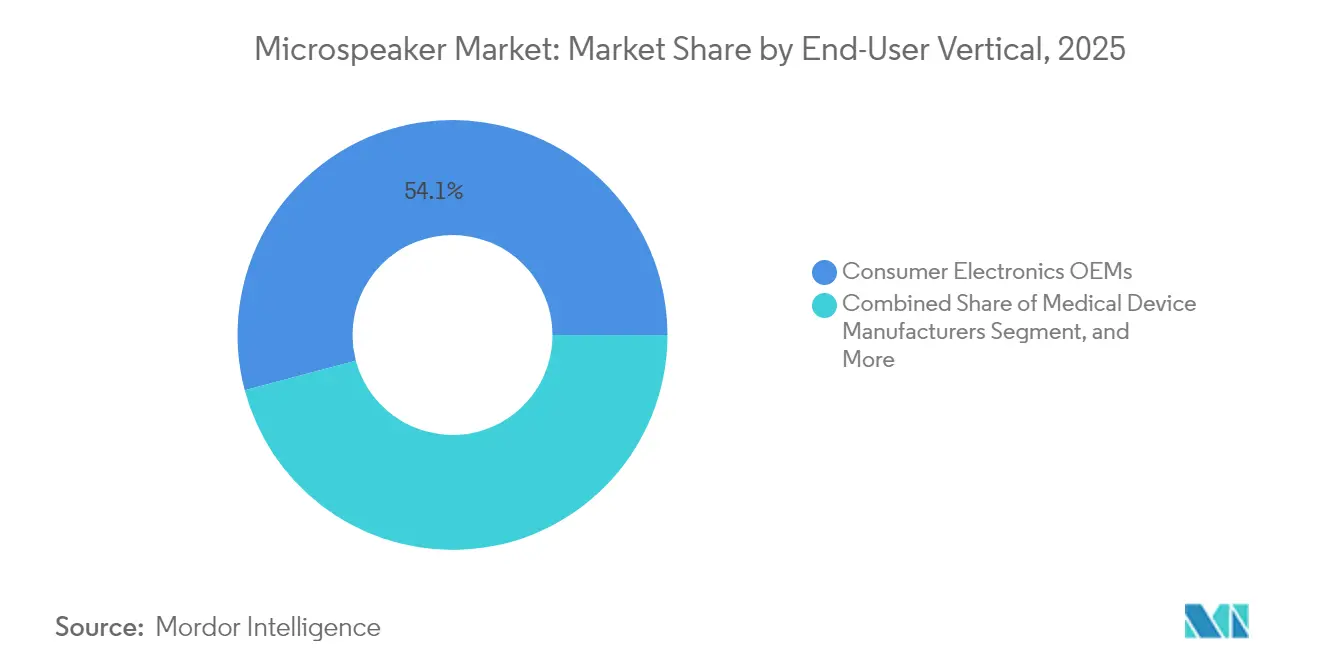

- By end-user vertical, Consumer Electronics OEMs generated 54.13% of 2025 revenue; Medical Device Manufacturers are positioned for a 6.71% CAGR on the back of the OTC hearing-aid rule.

- By size, 10–15 millimeter drivers held 48.96% of 2025 revenue, yet sub-10 millimeter units are accelerating at a 7.26% CAGR through 2031.

- By geography, Asia-Pacific commanded a 52.18% share of 2025 value, while North America is on course for a 6.17% CAGR outpacing the global average.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microspeaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of TWS Earbuds and Hearables | +1.2% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Rapid Miniaturization of Automotive Cabin Audio Components | +0.8% | North America, Europe, China | Medium term (2-4 years) |

| Emergence of MEMS Speakers With 50% Lower Energy Use | +1.0% | Global, early traction in North America and East Asia | Medium term (2-4 years) |

| Growth of Voice-First Smart Home Ecosystems | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Standardization of Bluetooth LE Audio and Auracast | +0.6% | Global | Long term (≥ 4 years) |

| Sustainable High-Modulus Diaphragm Materials | +0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of TWS Earbuds and Hearables

TWS earbud volumes rose 12.6% year-on-year to 331.6 million units in 2024, underscoring how portability and active noise cancellation are moving consumers away from wired models. The growth wave has spurred demand for sub-10 millimeter drivers that enable multi-driver arrays inside tight housings. Solid-state launches such as xMEMS Labs’ Sycamore, just 1 millimeter thick, are scheduled for mass production in 2025, signaling a design pivot toward wafer-scale speakers. Low power draw extends battery life in hearables that double as health monitors, and partnerships e.g., USound with Minami Acoustics are combining audio and ultrasonic sensing for gesture and spatial audio features.[1]USound GmbH, “USound and Minami Acoustics Partnership,” usound.com

Rapid Miniaturization of Automotive Cabin Audio Components

Automakers are migrating from centralized dashboards to distributed arrays embedded in headrests, pillars, and trim pieces, trimming harness weight by as much as 30% and enabling zoned audio. Harman International’s Seat Sonic solution exemplifies this shift by integrating microspeakers directly into seat foams. In electric vehicles, lighter audio systems translate into greater driving range and lower energy consumption. Directional alerts for advanced driver-assistance systems (ADAS) also depend on precise speaker placement, raising the premium on smaller, functionally robust transducers. Compliance with ISO 26262 safety standards is now a procurement prerequisite.

Emergence of MEMS Speakers With 50% Lower Energy Use

MEMS speakers vibrate silicon membranes via piezoelectric or electrostatic actuation, consuming roughly half the power of electrodynamic designs. USound demonstrates an 80% power reduction relative to conventional drivers, creating space for all-day hearable usage. Bosch Sensortec’s integration of Nanoscopic Electrostatic Drive (NED) technology has achieved sub-1 millimeter thickness compatible with standard CMOS flows. As volumes exceed 10 million units, wafer-scale economics allow MEMS to challenge balanced-armature price points, especially for voice-first devices running always-on keyword spotting.

Growth of Voice-First Smart Home Ecosystems

Amazon reports more than 100 million active Alexa devices, while Google Assistant is embedded in thermostats, doorbells, and appliances. Local processing on edge devices demands microspeakers that deliver reliable voice feedback with sub-200 millisecond latency while conserving standby power. The Matter protocol is improving cross-brand interoperability, prompting appliance OEMs to adopt reference designs that bundle microspeakers with wake-word silicon and acoustic echo cancellation. Multi-speaker arrays enabling beamforming and spatial audio are becoming standard in kitchens and bathrooms, extending demand beyond traditional consumer electronics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Easy Availability of Counterfeit Micro Speakers | -0.5% | Asia-Pacific, spillover to Middle East and Africa and South America | Short term (≤ 2 years) |

| Trade-Sensitive Rare-Earth Magnet Supply Volatility | -0.7% | Global, acute for non-Chinese OEMs | Medium term (2-4 years) |

| High Tooling Costs for Next-Gen MEMS Production Lines | -0.4% | North America, Europe, East Asia | Medium term (2-4 years) |

| Acoustic Performance Limits Below 200 Hz in Ultra-Thin Designs | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Trade-Sensitive Rare-Earth Magnet Supply Volatility

China controls 70% of global rare-earth mining and 90% of processing, and the December 2024 export restrictions to the United States triggered price spikes that forced OEMs to stockpile magnets or adopt ferrite substitutes that cut magnetic flux by up to 30%. Production disruptions in Myanmar amplified shortages of crucial elements such as dysprosium. The volatility pushes manufacturers to explore magnet-free technologies namely MEMS and piezoelectric speakers but the requalification cycle typically spans 18–24 months, creating a temporal mismatch between design needs and supply availability.

High Tooling Costs for Next-Gen MEMS Production Lines

Building a high-volume MEMS speaker line demands capital outlays exceeding USD 50 million for lithography and wafer bonding gear, deterring small entrants and concentrating innovation among semiconductor incumbents. xMEMS bypasses that burden by tapping third-party foundries, although it then competes for wafer allocation against higher-margin devices. Yield rates remain below 85% during early ramps, further inflating per-unit costs, and each design revision requires new photomasks costing up to USD 1 million, slowing iteration cycles versus injection-molded dynamic speakers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: MEMS Speakers Challenge Dynamic Dominance

Dynamic Micro Speakers generated the largest slice of 2025 revenue at 47.59%, underpinned by entrenched supply chains in smartphones and tablets. Balanced armature models serve audiophile in-ear monitors and hearing aids where midrange clarity offsets higher bills of material. The microspeaker market size for MEMS designs is set for a 5.14% CAGR, supported by xMEMS Sycamore and USound Conamara launches tailored to TWS earbuds and wearables. Piezoelectric architectures are gaining prominence in bezel-less smartphones that laminate drivers under displays, removing grille openings and enhancing dust resistance. Electrostatic speakers, requiring bias voltages above 100 V, remain a boutique choice in premium headphones, yet advances in low-voltage drivers could broaden appeal post-2028.

Overall, price gaps are narrowing as wafer-scale production matures, positioning MEMS and piezoelectric formats to command a double-digit microspeaker market share by 2030. Competitive pressure is forcing dynamic-speaker vendors to invest in haptics and camera modules to hedge against margin erosion. Balanced armature makers leverage medical regulatory approvals as barriers to entry, maintaining pricing power in hearing-health channels. The industry is also exploring hybrid stacks-pairing dynamic woofers with MEMS tweeters-to balance bass output with ultrathin profiles. Such combinations are likely to dominate next-generation hearables, accelerating cross-migration of materials and manufacturing know-how across the product spectrum.

By Technology: Piezoelectric Thin-Film Gains Momentum

Electrodynamic technology held 59.82% share in 2025, reflecting decades of optimization that has pushed unit costs below USD 0.50 in high-volume orders. Yet piezoelectric thin-film drivers, projected for a 5.98% CAGR, are reshaping industrial design by reclaiming screen real estate and meeting EU RoHS directives for lead-free materials. Smartphone brands adopting Synaptics display speakers have eliminated earpiece cutouts, enabling uninterrupted glass fronts and reinforcing premium aesthetics. Electrostatic MEMS approaches from USound and Bosch Sensortec bring sub-1 millimeter thickness that aligns with wearables and smart rings.

Experimental thermoacoustic devices remain cost-prohibitive and inefficient but illustrate the expanding research pool chasing differentiated acoustics. Material innovation is equally pivotal. Lead-free potassium sodium niobate films and high-modulus polymers such as PEEK are replacing traditional diaphragms, addressing sustainability requirements without sacrificing fidelity. As tooling amortizes, piezoelectric and electrostatic speakers will erode electrodynamic dominance, particularly in segments where industrial design overrides absolute loudness.

By Application: Wearables Outpace Smartphones

Although Smartphones and Tablets accounted for 44.01% of 2025 unit demand, lengthening replacement cycles and plateauing feature differentiation are slowing incremental volume. Wearables and Hearables, however, are set to outstrip broader growth at a 5.67% CAGR, fueled by health-centric earbuds, smartwatches, and augmented-reality glasses. Smart home devices embed microspeakers in thermostats and appliances to deliver local voice feedback; Amazon alone cites 100 million active Alexa units, underscoring a robust installed base. Automotive infotainment and ADAS functions are adopting distributed arrays to cut wiring and enable directional warnings.

The microspeaker market size allocated to medical devices, particularly OTC hearing aids, is expanding on regulatory liberalization, reallocating spend toward energy-efficient, medically certified balanced-armature and MEMS modules. Industrial headsets and defense systems require ruggedized transducers that meet MIL-STD-810 standards, representing a small but stable niche where long product cycles insulate suppliers from consumer volatility. Overall, diversification across wearables, automotive, and healthcare is softening the sector’s historic reliance on smartphones.

By End-User Vertical: Medical Manufacturers Accelerate

Consumer Electronics OEMs retained 54.13% procurement share in 2025, yet Medical Device Manufacturers will compound at 6.71% through 2031. The change follows the FDA’s OTC hearing-aid ruling, which removes prescription hurdles and broadens retail access. Knowles Corporation is investing in medical-grade balanced-armature capacity, targeting devices that must balance speech intelligibility with extended battery life.

Automotive OEMs are specifying cabin speakers to deliver personalized zones and ADAS prompts, a trend boosting joint engineering programs with module makers. Meanwhile, industrial equipment and aerospace contractors demand hermetically sealed, temperature-tolerant speakers for mission-critical headsets. Diversification into healthcare and automotive extends design cycles to 18–36 months, necessitating greater investment in traceability and failure-mode analysis. Suppliers able to navigate these certification paths gain durable margins and reduced exposure to consumer replacement cycles.

By Size (Driver Diameter): Sub-10 Millimeter Surge

Drivers between 10 and 15 millimeters posted 48.96% revenue in 2025, thanks to ubiquity in smartphones and entry-level earbuds. Below-10 millimeter units, however, are on a faster 7.26% CAGR as brands race to miniaturize housings without sacrificing multi-driver arrays. MEMS designs such as Sycamore, just 9 millimeters tall and 1 millimeter thick, illustrate the compression achievable when coils and magnets are eliminated. Above-20 millimeter drivers persist in premium headphones and Bluetooth speakers, where bass extension below 50 Hz remains a selling point.

Frequencies under 200 Hz are challenging for ultra-small drivers; digital signal processing and passive radiators are now standard countermeasures, albeit at added bill-of-materials cost. Longer term, bone-conduction glasses and smart rings may adopt micro-planar actuators, though commercial impact is unlikely before 2028. Miniaturization will continue to define competitive advantage across hearables and wearables, keeping sub-10 millimeter innovations central to the microspeaker market.

Geography Analysis

Asia-Pacific dominated 2025 revenue with 52.18%, anchored by China’s vertically integrated supply chain spanning diaphragm film to final assembly. AAC Technologies reported CNY 10.4 billion (USD 1.46 billion) Q3 2024 revenue, though its acoustic segment narrowed as the firm pivoted toward haptics and camera modules. GoerTek’s CNY 38.5 billion (USD 5.4 billion) H1 2024 revenue affirmed its position as a primary module partner to global smartphone and TWS brands. Japan’s Foster Electric and Sony refine high-fidelity transducers for luxury headphones, while South Korea’s Samsung files patents covering omnidirectional filters and integrated air-bone conduction modules. India is emerging as a secondary hub under production-linked incentives, yet still relies on imported magnets and MEMS dies. Vertical integration grants Chinese and broader Asia-Pacific suppliers cost leverage and rapid design cycles that competitors struggle to match, reinforcing the region’s leadership in the microspeaker market.

North America is forecast for a 6.17% CAGR to 2031, powered by the FDA’s OTC hearing-aid rule and automotive adoption of distributed audio. Knowles posted USD 170.3 million Q3 2024 revenue, and Illinois-based xMEMS raised USD 20 million to ramp Sycamore at external foundries. Proximity to U.S. auto plants in Michigan and Mexico is drawing speaker module assembly closer to final vehicle lines. Europe’s pathway is shaped by REACH and RoHS mandates pressing for lead-free and rare-earth-reduced materials. Continental’s Ac2ated Sound system vibrates interior panels to create slimline audio, adopted by German luxury automakers. Austria’s USound integrates ultrasonic sensing in MEMS speakers for gesture-driven wearables. The region’s focus on sustainability and electric vehicles aligns with piezoelectric and MEMS adoption.

South America and the Middle East and Africa remain nascent. Urban centers with high smartphone penetration are witnessing early smart-home deployments, yet tariffs and logistics challenges constrain volume. Nonetheless, commodity dynamic speakers remain the entry point for regional brands, with piezoelectric and MEMS adoption expected post-2027.

Regulatory Landscape

Microspeaker qualification and procurement increasingly reference harmonized measurement and test methods. IEC 63034:2020 defines specifications and testing for microspeakers (radiating diaphragm diameter up to 40 mm), including impedance, frequency response, distortion, and power handling. China also reinforced local compliance pathways with GB/T 44218-2024 (Methods of measurement for microspeakers), released in July 2024 and implemented from February 1, 2025, along with a group standard (T/SZAACN 00001-2023) setting general technical requirements for miniature MEMS speakers.

On product safety, the EU continued aligning standards to its newer safety framework. Commission Implementing Decision (EU) 2026/901 (adopted April 17, 2026) establishes European standards supporting the General Product Safety Regulation (EU) 2023/988, tightening expectations on traceability and conformity for consumer electronics using microspeakers. In parallel, semiconductor supply-chain policy remains an external constraint and opportunity driver for MEMS-based microspeakers, with the EU Chips for Europe Initiative 2.0 (Regulation proposal 2026/504) and US policy positioning via SEMI in 2026 emphasizing resilience, guardrails, and trade-policy alignment that affects sourcing of wafers, ASICs, and legacy magnet-dependent components.

Value Chain Analysis

The microspeaker value chain begins with raw materials and key subcomponents. Dynamic designs rely on NdFeB magnets and copper wire, hearing and premium in-ear applications typically use balanced-armature assemblies, and diaphragm films (for example, high-modulus polymers) influence efficiency and acoustic response. Manufacturing then splits between traditional coil-and-magnet assembly, which remains labor- and tooling-intensive, and solid-state MEMS/piezoelectric routes that move speaker production into semiconductor process steps (photolithography, DRIE, and wafer bonding) alongside ASIC integration. Across both approaches, testing and binning (impedance, frequency response, distortion) are key gating steps, while downstream integration is commonly handled by acoustic module suppliers and EMS partners close to final device assembly.

Partnerships show how MEMS is changing upstream and midstream roles. USound partnered with Minami Acoustics (April 2024) to accelerate adoption by global audio brands, and in September 2025 Gettop Acoustic and USound signed a strategic sales and supply agreement. Under the agreement, Gettop manufactures speakers using USound MEMS wafers and ASICs, establishing a wafer-to-module path. Hybrid module architectures also advanced into production, including OBO Pro2 commencing high-volume production of the Greip dual-input module (July 2024), which integrates a USound MEMS driver with an electrodynamic driver. This reflects a transition stage where MEMS is inserted into existing acoustic assemblies, while OEMs manage qualification cycles and multi-sourcing.

Competitive Landscape

The microspeaker market is moderately concentrated. The top five suppliers, AAC Technologies, GoerTek, Knowles, TDK, and Foster Electric, collectively hold roughly 55-60% revenue, while emerging MEMS entrants such as xMEMS, USound, and Bosch Sensortec fragment share by targeting premium niches. AAC’s acoustic revenue contraction in Q3 2024 highlights margin pressure in commoditized dynamic speakers, prompting diversification into haptics. Knowles leverages balanced-armature leadership in medical and hearable channels where regulatory barriers maintain pricing power.

Innovation semantics are shifting from mechanical tolerances to semiconductor process flows. Apple secured a patent covering flexible speakers that conform to curved surfaces, signaling form-factor convergence between audio and industrial design.[3]United States Patent and Trademark Office, “US Patent 12108200 B2,” uspto.gov Samsung’s filings on integrated air-bone conduction point toward multifunction transducers that marry audio with biometric sensing. Meanwhile, counterfeit microspeakers in Asia-Pacific erode brand equity, pushing global OEMs toward trusted suppliers with traceable sourcing.

Rare-earth magnet volatility advantages MEMS pioneers because silicon-based devices need no magnets. xMEMS’ foundry model accelerates scale without owning capital-intensive fabs, while Bosch Sensortec’s alliance with Fraunhofer IPMS spreads tooling costs across product lines. Despite high barriers, new capital continues to enter solid-state acoustics, intensifying competition and compressing incumbent margins.

Microspeaker Industry Leaders

AAC Technologies Holdings Inc.

GoerTek Inc.

Knowles Corporation

TDK Corporation

USound GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is extending solid-state and hybrid microspeaker architectures beyond classic smartphone receivers into always-on hearables, voice-first smart-home endpoints, and distributed automotive audio, where low power and thin form factors translate into clear design value. The market already shows pull from high-volume hearables, with 331.6 million TWS earbud shipments in 2024, and from OEM activity around solid-state roadmaps. xMEMS Sycamore, positioned for mass production in 2025 for TWS and wearables, also demonstrates sub-10 mm magnet-free speaker engines that directly address rare-earth supply volatility.

Another opportunity area is functional convergence, where microspeakers become part of multi-sensor and software-defined platforms rather than standalone transducers. USound and WuQi Technologies announced a biosensing partnership in May 2026 that uses existing MEMS audio hardware as part of a wearable sensing platform, supporting BOM consolidation in compact devices. On the technical pipeline, peer-reviewed work published in April 2026 in the IEEE Journal of Microelectromechanical Systems on piezoelectric MEMS loudspeaker structures aimed at improving sound pressure levels signals continued progress toward broader audio performance targets. Meanwhile, industry-facing guidance in 2026 on modulated-ultrasound MEMS speaker design discusses beamforming-capable, uniform arrays that align with Bluetooth LE Audio and Auracast use cases in public and multi-room environments.

Recent Industry Developments

- May 2026: USound announced a partnership with WuQi Technologies to deploy a proprietary sensor-free in-ear biosensing platform that leverages existing MEMS audio hardware in wearable devices. The partnership expands the use of MEMS microspeakers from audio output to multifunction hardware, supporting tighter integration and lower component count in hearables.

- September 2025: Gettop Acoustic and USound signed a strategic sales and supply agreement for MEMS speaker production, with Gettop manufacturing speakers using USound MEMS wafers and ASICs. This formalized wafer-to-module collaboration strengthens supply availability for MEMS designs and supports OEM qualification through an established manufacturing partner.

- July 2024: USound and OBO Pro2 announced the release of the Greip dual-input audio module and stated that OBO Pro2 commenced high-volume production of the design, integrating an electrodynamic driver with a USound MEMS speaker. Hybrid modules like this offer a practical adoption path for TWS and IEM makers by pairing familiar low-frequency performance with solid-state high-frequency capability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The microspeaker market is defined as revenue from very small speakers used to produce audio in compact electronic devices, where the component is integrated into the end product and sold through OEM supply chains.

Scope exclusions: We exclude external loudspeakers and audio systems that are not designed as microspeakers for thin, space-limited device builds.

Segmentation Overview

- By Product Type

- Dynamic Micro Speaker

- Balanced Armature Speaker

- MEMS Speaker

- Piezoelectric Speaker

- Electrostatic Speaker

- Other Product Types

- By Technology

- Electrodynamic

- Piezoelectric Thin-Film

- Electrostatic (CMOS-Compatible)

- Thermoacoustic

- By Application

- Smartphones and Tablets

- Wearables and Hearables

- Smart Home Devices

- Automotive Infotainment and ADAS

- Medical Devices (Hearing Aids, OTC)

- Industrial and Defense Systems

- By End-User Vertical

- Consumer Electronics OEMs

- Automotive OEMs

- Medical Device Manufacturers

- Industrial Equipment Makers

- Aerospace and Defense Contractors

- Other End-User Verticals

- By Size (Driver Diameter)

- Below 10 mm

- 10 - 15 mm

- 16 - 20 mm

- Above 20 mm

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where microspeakers are used and how volumes move by device class, then translating those volumes into value using realistic pricing and mix changes. Public and official sources such as International Telecommunication Union device and connectivity indicators, UN Comtrade trade statistics for relevant acoustic parts, U.S. International Trade Commission tariff schedules, and Eurostat industrial and electronics series help keep the demand pool grounded.

We also review standards and technical literature, including IEEE and other peer-reviewed journals, to understand how thinner form factors or new transducer designs can shift average selling prices over time. We then cross-check assumptions using company annual reports, investor presentations, trade association updates, and reputable business press. For company financials and event tracking, paid subscriptions for company intelligence, patent databases, and shipment-level trade views are used selectively when they add clarity. The sources listed here are illustrative, and many other references were used to collect, verify, and clarify the final data points.

Primary Interviews and Surveys

Primary conversations are used to pressure-test device attach rates, speaker count per device, and the price movement across dynamic designs and emerging microspeaker designs. We speak with a mix of component-side and device-side respondents, and we keep coverage balanced across major manufacturing hubs and end-demand regions so the final assumptions do not rely on one geography or one customer type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 46% |

| Mid tier: 59% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 16% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

The core model uses a top-down demand reconstruction, where shipments of key host devices are converted into microspeaker demand through attach rates and speaker count per unit, then valued using an average selling price by technology and use case. To keep the totals realistic, we corroborate the output with selective bottom-up checks, such as rolling up indicative supplier revenue coverage, sampled ASP quotes from the ecosystem, and channel feedback on mix shifts.

Key inputs in this market include smartphone and TWS hearable shipments, laptop and tablet unit trends, automotive in-cabin audio content per vehicle, and the technology mix between dynamic designs and newer microspeaker approaches, which tend to carry different pricing. We also track design-driven variables, such as thinness requirements, driver size choices, and the cadence of flagship device launches, because these factors often explain short-term ASP changes.

For the forecast, we primarily use scenario analysis tied to device shipment outlooks and mix-based ASP curves, then review them with primary respondents to align on realistic adoption speed. Where bottom-up visibility is incomplete, we handle gaps by applying conservative coverage factors and then rechecking the implied value per device against interview feedback and public shipment signals.

Data Validation & Update Cycle

Validation is done by comparing model outputs against independent signals, including implied microspeaker value per smartphone or hearable, trade movement direction, and the reasonableness of technology mix and pricing changes. When a number looks off, we revisit the assumptions behind device volumes, attach rates, or ASP progression, and we trigger follow-up outreach to resolve the mismatch before sign-off.

We run a multi-step review, with another analyst checking the calculations, units, and currency conversions before finalization. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp device shipment revisions or major pricing shocks in components. Right before delivery, we re-run the full model with the latest available inputs so clients receive the most up-to-date view.

Mordor Intelligence's Microspeaker Market Size Measured Against Other Published Estimates

Published market sizes for microspeakers often differ because groups use different timing for currency conversion, and they also update ASP and device shipment assumptions at different points in the year. Even when the same devices are discussed, small differences in speaker count per device and technology mix can push the total up or down.

Key gap drivers in this market usually come from whether pricing is modeled as a smooth curve or as step changes around major device launches, and whether the scope includes hearing-aid related demand in the same pool as consumer hearables. The refresh-led checks also matter, where currency timing and revised shipment outlooks are applied consistently across regions, which is why Mordor Intelligence keeps the estimate aligned to a defined device-demand base and repeatable ASP logic.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.98 B (2025) | |

| Global Consultancy A | USD 4.38 B (2026) | Uses a later-year starting point and may reflect a different device shipment set and price level, which can lift the value if ASPs are taken after key model launches and mix upgrades. |

| Industry Publisher B | USD 2.80 B (2025) | Often counts a narrower product boundary or applies more conservative attach rates across hearables and mobile devices, and the ASP curve may not fully reflect technology mix upgrades over the base year. |

The spread in the table is mostly explained by timing and scope choices, followed by how quickly ASP is assumed to move with technology and device mix. By tying the value build to observable host-device units and then checking the implied value per device, the model stays transparent and can be repeated when new shipment or pricing signals appear without rewriting the whole approach.

Key Questions Answered in the Report

How large is the microspeaker market in 2026?

The microspeaker market size stands at USD 4.17 billion in 2026 and is projected to reach USD 5.23 billion by 2031.

Which application will grow fastest through 2031?

Wearables and hearables lead with a forecast 5.67% CAGR, reflecting rising TWS earbud and smartwatch volumes.

Why are MEMS speakers gaining momentum?

MEMS speakers cut power draw by roughly 50%, enable sub-10 millimeter profiles, and avoid scarce rare-earth magnets, positioning them well for battery-constrained devices.

What is the biggest geographic market?

Asia-Pacific holds a 52.18% revenue share, driven by China’s vertically integrated component manufacturing ecosystem.

How will rare-earth supply risks affect the sector?

Magnet volatility raises costs for dynamic speakers and accelerates the shift toward magnet-free MEMS and piezoelectric designs.

Who are the leading companies?

AAC Technologies, GoerTek, Knowles, TDK, and Foster Electric are the largest incumbents, while xMEMS, USound, and Bosch Sensortec are prominent MEMS challengers.

Page last updated on: