India Bottled Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

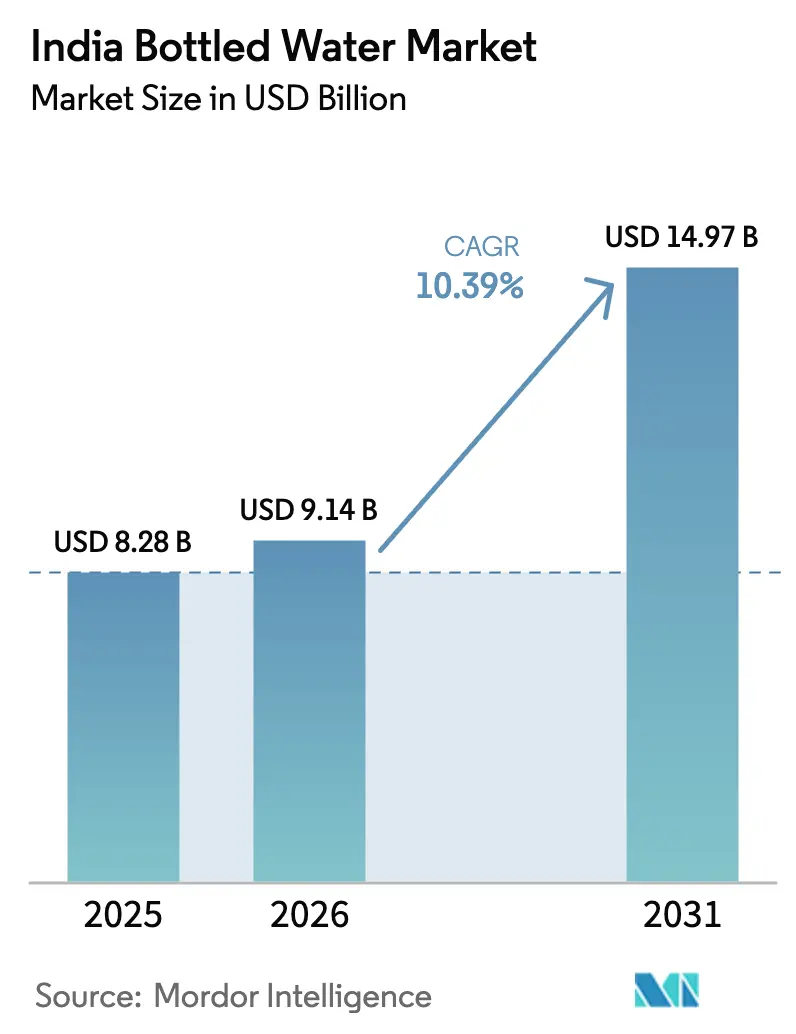

| Base Year Market Size (2025) | USD 8.28 Billion |

| Market Size (2026) | USD 9.14 Billion |

| Market Size (2031) | USD 14.97 Billion |

| Growth Rate (2026 - 2031) | 10.39% CAGR |

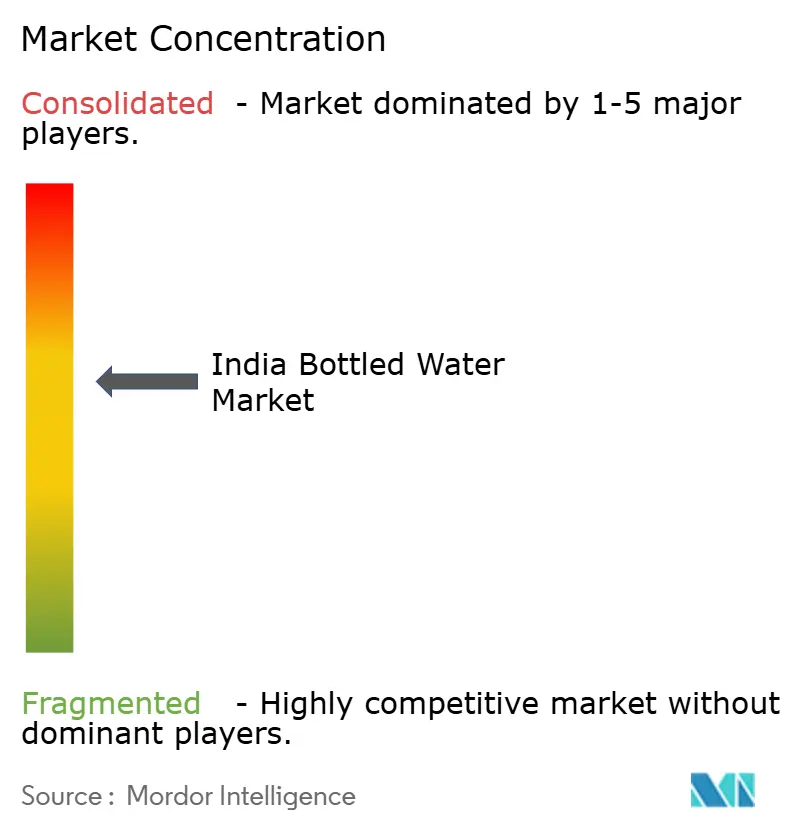

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Bottled Water Market Analysis by Mordor Intelligence

The Indian bottled water market size is expected to grow from USD 8.28 billion in 2025 to USD 9.14 billion in 2026 and is forecast to reach USD 14.97 billion by 2031 at 10.39% CAGR over 2026-2031. This growth is underpinned by a structural gap in water supply. Municipal systems are unable to keep up with the rapid pace of urbanization, prompting households and businesses to increasingly rely on packaged water as a quasi-utility. Despite government initiatives like the Jal Jeevan Mission, which has expanded tap water access, issues such as inconsistent service reliability, last-mile contamination, and groundwater depletion continue to elevate perceived risks, sustaining the demand for bottled water. Regulatory developments are also reshaping the market dynamics. The new FSSAI regulations, effective December 2024, classify packaged water as "high-risk," requiring annual third-party audits. This change poses significant challenges for smaller operators, who may struggle to meet the financial demands of compliance. Additionally, evolving consumer lifestyles are driving market growth. The interplay of infrastructure challenges, growing health awareness, and regulatory consolidation positions the Indian bottled water market for sustained multi-year expansion, making it a critical segment within the broader beverage industry.

Key Report Takeaways

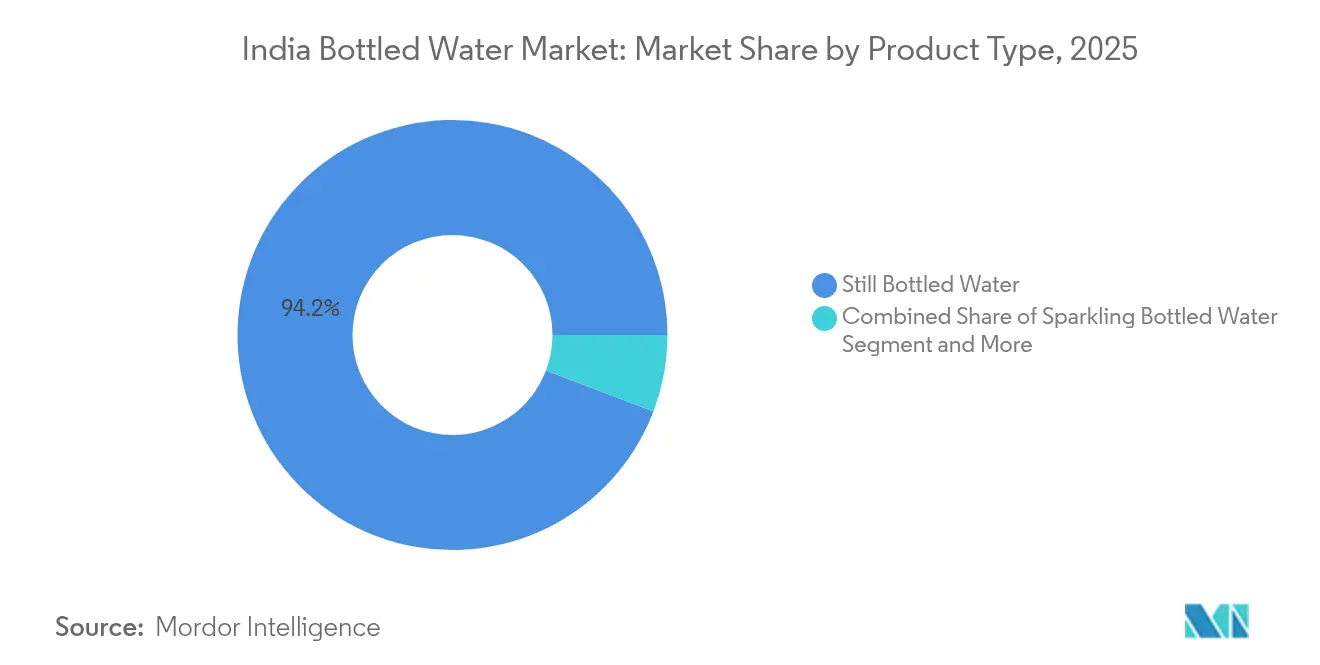

- By product type, still bottled water led with 94.21% revenue share in 2025; functional/flavoured sub-segment is projected to expand at an 10.92% CAGR to 2031.

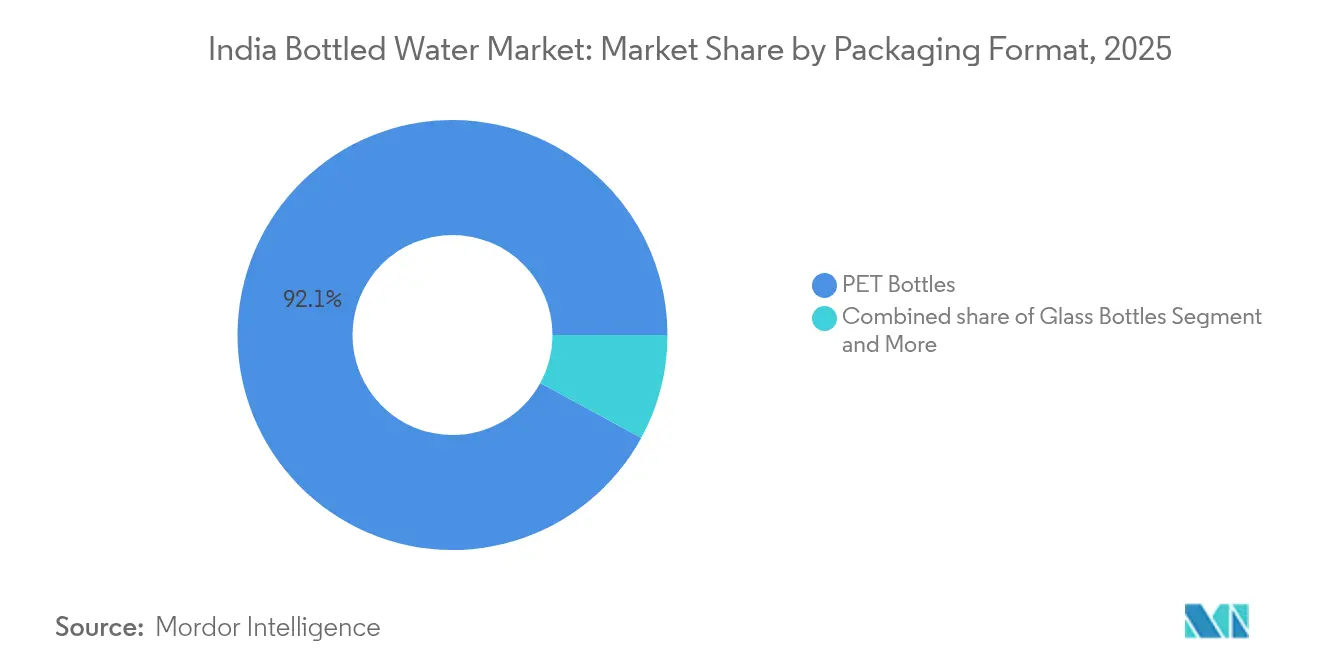

- By packaging format, PET bottles held 92.05% of the India bottled water market share in 2025, whereas cans are forecast to register an 11.49% CAGR through 2031.

- By category, the mass segment accounted for 85.12% of the India bottled water market size in 2025; the premium segment is advancing at an 11.71% CAGR to 2031.

- By distribution channel, off-trade captured 67.98% share of the India bottled water market in 2025, while on-trade is poised for a 10.74% CAGR through 2031.

- By geography, North India commanded 32.31% market share in 2025; West India is the fastest-growing region with a 12.25% CAGR expected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate public water infrastructure | +2.8% | National, with acute impact in North and East India | Long term (≥ 4 years) |

| Advertisements and promotional campaigns | +1.2% | Urban centers across all regions, Metro cities priority | Medium term (2-4 years) |

| Increased awareness of waterborne diseases | +1.8% | National, with higher impact in rural and semi-urban areas | Medium term (2-4 years) |

| Strategic expansion of food service establishments | +1.4% | Urban corridors, West and South India leading | Medium term (2-4 years) |

| Growing sustainability and eco-friendly packaging trends | +0.9% | Metro cities and premium segments nationally | Long term (≥ 4 years) |

| Increasing demand for functional water from fitness enthusiasts | +1.1% | Urban centers, particularly West and North India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inadequate public water infrastructure

Infrastructure deficits remain a significant driver of bottled water adoption, despite government investments exceeding USD 50 billion under the Jal Jeevan Mission, which aims to connect 146 million households by 2024[1]International Trade Administration , "India Water and Wastewater Treatment Industry", www.trade.gov. The challenge is further intensified by groundwater depletion, with extraction rates projected to potentially triple by 2080 due to climate change pressures. Agriculture continues to dominate water usage, consuming 62% of irrigation water and 85% of the rural water supply. The Economic Survey 2024-25 highlights the importance of adopting flexible policy-making to address uncertainties surrounding water security, suggesting that infrastructure gaps are likely to persist beyond current planning horizons. Rural areas, particularly tribal districts, face heightened vulnerability, with only 82% of households having access to improved drinking water sources. This persistent mismatch between infrastructure and demand creates long-term market opportunities, especially in regions where groundwater contamination—caused by arsenic, fluoride, and salinity—necessitates advanced treatment solutions that exceed household capabilities.

Advertisements and promotional campaigns

Companies are intensifying brand-building efforts to address market fragmentation, where 80% of the market remains unorganized, and counterfeiting continues to pose significant challenges, as highlighted by the MSME-Development Institute[2]MSME-Development Institute, "Packaged Drinking Water", www.dcmsme.gov.in. To differentiate their offerings and cater to shifting consumer demands, businesses are increasingly adopting health-focused messaging. For example, Booster Water has launched its alkaline ionized range, including Black Water variants, specifically designed for athletes and fitness enthusiasts. These products are fortified with over 70 minerals and maintain a pH level of 8.5, emphasizing their combined functionality and health benefits. The COVID-19 pandemic has further accelerated the transition toward direct-to-consumer models, driving brands to invest heavily in digital marketing strategies to enhance consumer engagement and retention.

Increased awareness of waterborne diseases

Public health concerns are driving significant market growth in India, where waterborne diseases impose an annual economic burden of approximately USD 600 million. Despite advancements in infrastructure, diarrhea rates remain persistently high, highlighting the ongoing challenges in ensuring safe drinking water access. The National Health Mission has strategically integrated water quality initiatives with health outcomes, reinforcing the critical connection between clean water availability and disease prevention. In 2024, the Indian Council of Medical Research (ICMR) expanded its FoodNet surveillance network across North-East India, addressing the heightened risks of food and waterborne pathogens in regions characterized by traditional food practices and environmental contamination[3]Journal of Medical Internet Research, "Surveillance of Food and Waterborne Pathogens in North-East India: Protocol for a Laboratory-Based Sentinel Surveillance Study", www.researchprotocols.org. Furthermore, the Food Safety and Standards Authority of India (FSSAI) classified packaged water as high-risk in December 2024, implementing stricter quality controls. While this regulatory move aims to enhance consumer safety, it paradoxically validates public concerns about municipal water supplies, further solidifying bottled water's position as a preferred and perceived safer alternative.

Strategic expansion of food service establishments

India's rapidly growing food processing sector is significantly driving the demand for bottled water, particularly through restaurant and hospitality channels. The hospitality industry's sustainability initiatives, while aimed at reducing environmental impact, are paradoxically increasing the demand for premium bottled water alternatives. For example, IHCL operates 40 facilities with in-house bottling plants that comply with FSSAI standards and actively work to eliminate single-use plastics, showcasing a shift toward eco-friendly practices. Additionally, government initiatives such as the Production Linked Incentive Scheme and the Pradhan Mantri Kisan Sampada Yojana are strengthening food service infrastructure, especially in Tier-2 and Tier-3 cities where bottled water penetration remains relatively low. This growth is accompanied by a shift in non-alcoholic beverage consumption patterns, with consumers gravitating toward options that offer convenience and perceived safety benefits.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns and plastic waste | -1.6% | National, with acute pressure in urban centers | Medium term (2-4 years) |

| Strong competition from water purifier appliances | -2.1% | Urban and semi-urban areas, particularly North and West India | Short term (≤ 2 years) |

| Consumer shift towards sustainability | -1.3% | Metro cities and premium segments, West and South India leading | Medium term (2-4 years) |

| High cost associated with functional water | -0.8% | Price-sensitive markets, rural and semi-urban areas nationally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental concerns and plastic waste

Regulatory pressures are intensifying under Extended Producer Responsibility frameworks, which now mandate higher recycled content in packaging. This creates significant compliance challenges, particularly for food-contact applications where stringent safety regulations restrict the use of recycled materials. The 2024 Single Use Plastic (Regulation) Bill aims to eliminate single-use plastics by 2025, directly disrupting traditional PET bottle packaging and compelling the industry to invest in alternative materials[4]Lok Sabha, "The Single Use Plastic (Regulation) Bill, 2024", www.sansad.in. For instance, Manjushree Technopack has adapted by operating a captive recycling plant that produces 6,000 metric tons of recycled resin annually. However, smaller manufacturers face mounting cost pressures, making compliance more difficult. Shifting consumer sentiment toward sustainability is driving market segmentation. Adding to the challenges, the Central Pollution Control Board has introduced environmental compensation guidelines for violations of the Plastic Waste Management Rules. These financial penalties disproportionately affect smaller players, many of whom lack the necessary compliance infrastructure, further exacerbating their operational and financial burdens.

Strong competition from water purifier appliances

The domestic water purifier market has witnessed significant growth in recent years, creating substantial substitution pressure on bottled water consumption. This trend is further driven by infrastructure advancements under the Jal Jeevan Mission, which reduce the perceived necessity for bottled alternatives by improving access to clean drinking water. Technological innovations in Reverse Osmosis, Ultraviolet, and gravity-based systems effectively address diverse water quality challenges. These systems not only ensure safe drinking water but also offer long-term cost efficiency compared to bottled water.Government initiatives promoting household water treatment align with broader water security and sustainability objectives. Additionally, the increasing adoption of smart water purifiers and the integration of sustainable technologies appeal to environmentally conscious consumers. These advancements provide a practical and eco-friendly alternative to single-use plastic packaging, further driving the shift toward domestic water purification solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Water Dominance Faces Functional Innovation

In 2025, Still Bottled Water commands a dominant 94.21% market share, underscoring its appeal to consumers prioritizing basic hydration and price sensitivity. This stronghold is bolstered by well-established distribution networks and cost efficiencies, ensuring still water's reach across India's varied economic landscape. Yet, this segment grapples with tightening margins, squeezed by fierce competition and the financial strains of adhering to FSSAI's newly classified high-risk regulations.

Functional and Flavored Bottled Water is the standout performer, growing at 10.92% CAGR projected through 2031. This surge is largely fueled by a growing base of health-conscious consumers and fitness aficionados. A testament to this premium push is Booster Water's debut of its alkaline ionized range, notably the mineral-rich Black Water, tailored for athletes. Nestlé's move to spin off its water and premium beverages into a distinct entity by 2025, coupled with the introduction of health-enhanced Levissima+, underscores the industry's tilt towards functional innovation. Meanwhile, while Sparkling Water carves out a niche, it reaps rewards from the broader trends of premiumization and the evolving tastes of urban consumers.

By Category: Mass Market Stability Versus Premium Growth

The premium category is anticipated to grow at a strong CAGR of 11.71% through 2031, reflecting a shift in consumer preferences toward products that offer enhanced health benefits and functional properties. This growth is underpinned by rising disposable incomes, increasing health awareness, and urbanization trends that favor premiumization. Diageo India's scheduled December 2024 launch of 'Godawan Estuary Premium Water' in collaboration with Estuary Water exemplifies strategic efforts to capture the attention of affluent and discerning consumers by delivering luxury and craft-driven experiences. Moreover, the segment's expansion is fueled by continuous innovations in functional water and sustainability-focused narratives, which resonate with environmentally conscious consumers and justify premium pricing.

The mass category remains the cornerstone of the market, commanding an 85.12% share in 2025. This dominance is attributed to India's price-sensitive consumer base and the essential need for affordable hydration solutions. The segment is particularly vital in rural and semi-urban areas, where financial constraints limit the adoption of premium products. Despite challenges such as margin pressures from regulatory compliance costs and heightened competition, the mass category benefits from economies of scale and extensive distribution networks. Additionally, with 80% of the market still unorganized, branded players have a significant opportunity to expand their footprint by emphasizing quality assurance, enhancing distribution efficiency, and addressing the growing demand for reliable and affordable water solutions.

By Packaging Format: PET Dominance Challenged by Sustainability

In 2025, PET bottles command a dominant 92.05% market share their cost efficiency, lightweight nature, and a well-established supply chain. This stronghold is not just by chance; it hinges on practical factors like transportation costs and a consumer base that's well-acquainted with PET, especially in budget-conscious markets. Yet, this segment grapples with challenges posed by Extended Producer Responsibility regulations, which push for greater recycled content, complicating matters for food-contact uses.

Leading the pack, cans are the fastest-growing packaging format, boasting an impressive 11.49% CAGR projected through 2031. Their rise is fueled by a heightened focus on sustainability and strategic premium positioning. A testament to this shift is the hospitality industry's pivot towards greener choices. For instance, Park Hyatt Hyderabad has taken a bold step, eliminating over 250,000 plastic bottles from its operations annually. Meanwhile, while glass bottles uphold their premium status, they grapple with hurdles like weight-related logistics and breakage risks, curbing their appeal in the mass market. The 2024 Single Use Plastic (Regulation) Bill, aiming for a 2025 deadline, underscores the urgency for alternative packaging solutions. Yet, for many price-sensitive consumers, the cost of these alternatives remains a pivotal concern.

By Distribution Channel: Off-Trade Dominance Meets On-Trade Innovation

In 2025, Off-Trade channels capture a commanding 67.98% market share, underscoring a clear consumer preference for the retail convenience and price comparison benefits offered by supermarkets, hypermarkets, and convenience stores. This dominance is largely attributed to the evolution of India's retail infrastructure and shopping habits that lean towards purchasing packaged goods from traditional retail outlets. Furthermore, the segment has seen a boost from the rise of e-commerce and direct-to-consumer models, a trend significantly accelerated by shifts in consumer behavior during the pandemic.

On-trade channels, buoyed by the expansion of food service establishments and a burgeoning hospitality sector, are set to witness a robust 10.74% CAGR through 2031. Interestingly, while the hospitality industry pushes for sustainability, it's inadvertently fueling a surge in premium bottled water demand. Hotels, aiming to uphold service standards, are adopting in-house bottling systems. A prime example is IHCL, which operates 40 hotels with glass water-bottling systems that meet FSSAI standards, showcasing how sustainability can spur innovation in the on-trade sector. Moreover, with government backing via the Production Linked Incentive Scheme and a 100% FDI allowance in food processing, international restaurant chains are flocking in, drawn by the promise of stringent bottled water service standards.

Geography Analysis

In 2025, North India commands a 32.31% market share, buoyed by its dense population, urbanization trends, and ongoing water quality issues in the Indo-Gangetic plain. The region's established distribution networks and the perception of packaged water as a necessity bolster its market position. Despite investments from the Jal Jeevan Mission, groundwater depletion and contamination, especially in Punjab and Haryana's agricultural zones, continue to fuel demand.

West India stands out as the region with the highest growth rate, boasting a 12.25% CAGR projected through 2031. This surge is attributed to the region's economic vibrancy, industrial growth, and a shift in consumer mindset towards health and wellness products. Industrial advancements in Maharashtra and Gujarat spur notable institutional demand. Coastal metropolises, especially Mumbai, not only champion the premium water segment but also spearhead innovations in functional water. Yet, challenges loom with water stress, especially as agriculture accounts for 72% of the nation's freshwater withdrawals, hitting hard in Gujarat's industrial and farming locales. Nevertheless, the region's affluent urban populace leans towards premiumization and functional water trends.

East and South India emerge as regions ripe for growth, each with its unique traits. East India grapples with specific water quality dilemmas. Notably, West Bengal's ADB-backed initiative aims to tackle arsenic, fluoride, and salinity issues, propelling the bottled water trend. Meanwhile, South India's tech-centric landscape and elevated education levels foster a tilt towards premium water segments and functional trends.

Competitive Landscape

The Indian bottled water market is moderately consolidated, with key players such as Parle Agro Pvt Ltd., The Coca-Cola Company, PepsiCo, Inc., Tata Consumer Products Limited, and DS Group holding a significant share. These companies maintain their dominance through extensive distribution networks and strong brand equity, ensuring widespread market reach and consumer trust.

Despite this dominance, the market remains fragmented due to the presence of numerous regional and local brands that cater to specific geographies and price-sensitive consumer segments. These smaller players, particularly active in Tier II and Tier III cities, compete by offering affordable products and leveraging their regional distribution strengths. While organized players continue to expand their footprint, the competitive landscape is dynamic, driven by frequent product innovations, brand repositioning efforts, and evolving consumer preferences. This balance between established national brands and agile regional competitors highlights the moderately consolidated nature of the market.

Significant growth opportunities exist in emerging segments such as functional water, eco-friendly packaging solutions, and rural market penetration. Rural areas, in particular, present untapped potential due to distribution challenges that limit the presence of branded players. Additionally, the hospitality sector is witnessing a shift toward in-house bottling, with 45% of Marriott hotels now operating their water bottling units. This trend reflects a growing preference for vertical integration strategies, enabling end-users to bypass traditional supply chains and reduce dependency on external suppliers.

India Bottled Water Industry Leaders

-

Parle Agro Pvt Ltd.

-

The Coca-Cola Company

-

PepsiCo, Inc.

-

Tata Consumer Products Limited

-

DS Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Rhea Raheja and Ishaan Nangia have launched Impact Water, a bottled water brand focused on sustainability and environmental responsibility. Their initiative aims to reduce single-use plastic waste by using eco-friendly packaging and supporting clean water projects. With this launch, Impact Water targets environmentally conscious consumers seeking healthier hydration choices that also make a positive impact on the planet.

- February 2025: IOTA Water has launched in North India as the country’s first bottled water infused with oxygen nanobubbles, aiming to make advanced hydration accessible to the masses. Powered by NICO Nanobubble India Co., this innovative product marks a significant step in affordable, next-generation hydration solutions, according to the brand.

- January 2025: A Kerala startup, in collaboration with the Kerala Irrigation Infrastructure Development Corporation (KIIDC), launched India’s first eco-friendly compostable water bottles under the ‘Hilly Aqua’ brand, using biodegradable materials like polylactic acid (PLA) derived from corn and sugarcane.

- August 2024: Evocus as a part of expansion partnered with hotel chains such as Marriott, Radisson, Taj, Hyatt, and Accor and hospitality groups like Impresario Entertainment and Hospitality and Speciality Restaurants. With these collaborations the company has expanded its market presence, making it available in over 250+ HoReCa Outlets Across India.

India Bottled Water Market Report Scope

Bottled water refers to drinking water packaged in glass or plastic bottles. Bottled water, such as spring, distilled, well, and mineral water are available in carbonated and non-carbonated forms.

The India bottled water market is segmented by product type and distribution channel. By product type, the market is segmented into still water, sparkling water, and functional/fortified/flavoured water. By distribution channel, the market is segmented into on-trade and off-trade. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Still Bottled Water |

| Sparkling Bottled Water |

| Functional /Flavored Bottled Water |

| PET Bottles |

| Glass Bottles |

| Cans |

| Mass |

| Premium |

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Others Distribution Channel |

| North |

| East |

| West |

| South |

| By Product Type | Still Bottled Water | |

| Sparkling Bottled Water | ||

| Functional /Flavored Bottled Water | ||

| By Packaging Format | PET Bottles | |

| Glass Bottles | ||

| Cans | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Others Distribution Channel | ||

| By Region | North | |

| East | ||

| West | ||

| South | ||

Key Questions Answered in the Report

What is the current size of India’s bottled water market?

The market is valued at USD 9.14 billion in 2026 and is projected to reach USD 14.97 billion by 2031.

How fast is India’s bottled water market expected to grow?

It is forecast to expand at a 10.39% compound annual growth rate through 2031.

Which product segment is growing the fastest?

Functional and flavoured bottled water is set for an 10.92% CAGR as health-conscious consumers seek added minerals, electrolytes and alkaline options.

Which region shows the highest growth potential?

West India leads with a projected 12.25% CAGR thanks to higher disposable incomes, industrial expansion and proactive hospitality sustainability programmes.

Page last updated on: