Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

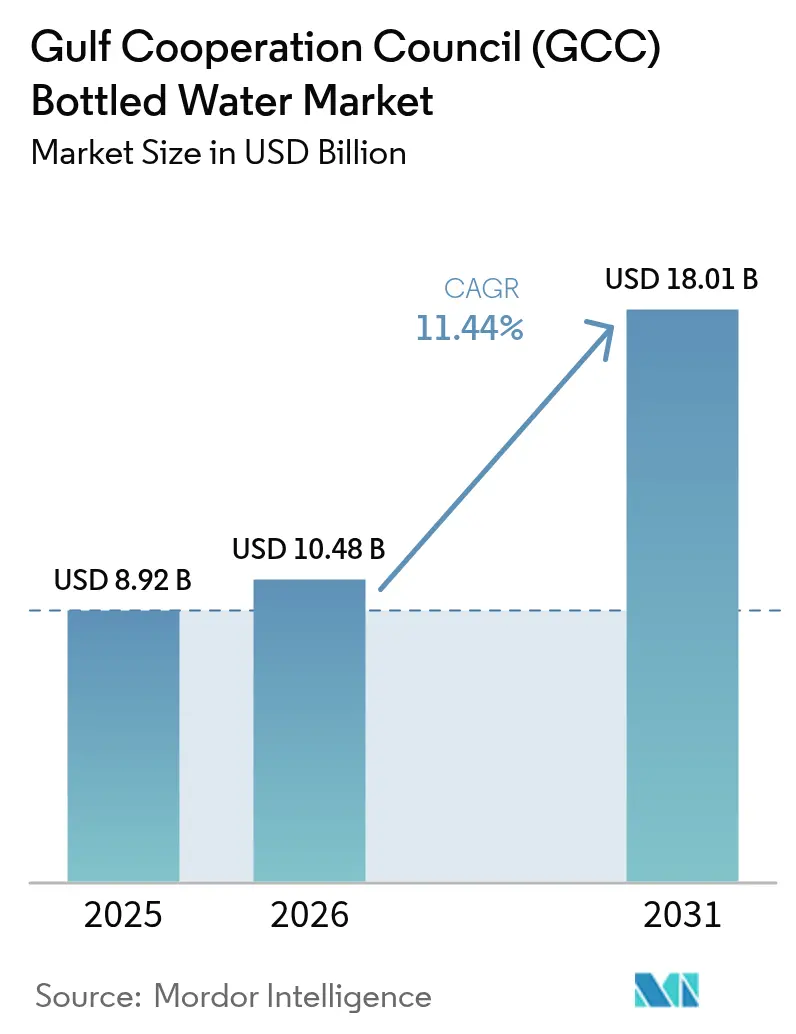

| Base Year Market Size (2025) | USD 8.92 Billion |

| Market Size (2026) | USD 10.48 Billion |

| Market Size (2031) | USD 18.01 Billion |

| Growth Rate (2026 - 2031) | 11.44% CAGR |

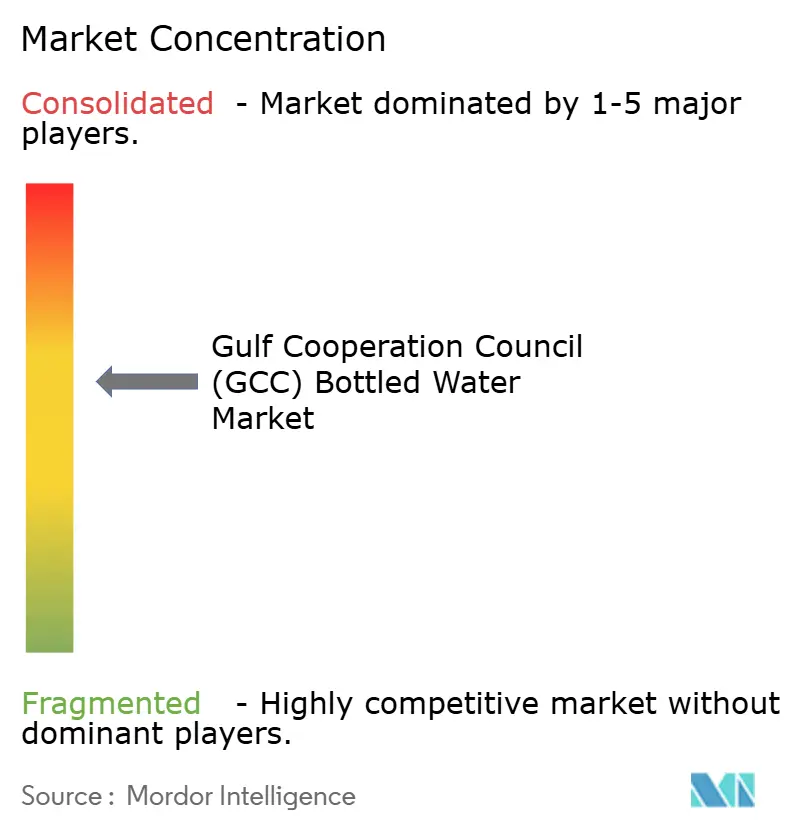

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gulf Cooperation Council (GCC) Bottled Water Market Analysis by Mordor Intelligence

The Gulf Cooperation Council (GCC) bottled water market size is projected to grow from USD 8.92 billion in 2025 to USD 10.48 billion in 2026, reaching USD 18.01 billion by 2031, with a CAGR of 11.44% during 2026-2031. The region's high heat and humidity drive consistent hydration needs, while an extensive desalination network ensures raw water availability, even amidst fluctuations in oil-linked power prices. The market is characterized by two primary consumption segments: premium glass bottles catering to hotels and events, and high-volume PET multipacks dominating retail shelves. Seasonal demand spikes, driven by tourism activities such as the Hajj in Saudi Arabia and year-round conferences in Dubai, add to the steady residential demand, prompting bottlers to diversify product formats and pricing strategies. Sustainability requirements, including Dubai's mandate for 25% recycled content in packaging starting in 2026, are influencing packaging investments, with brands increasingly adopting rPET and aluminum alternatives.

Key Report Takeaways

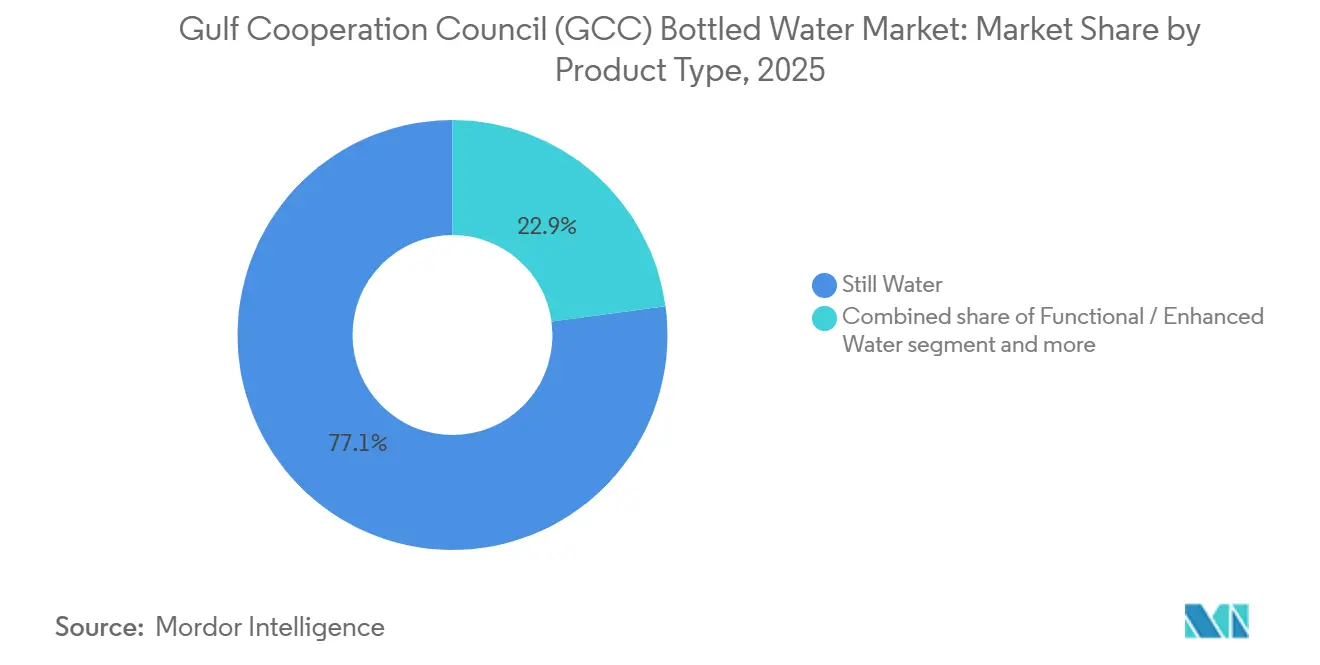

- By product type, still water held 77.14% of the Gulf Cooperation Council (GCC) bottled water market share in 2025, while functional/enhanced variants are projected to expand at a 12.59% CAGR through 2031.

- By packaging size, 331-500 mL formats captured 40.18% of 2025 revenue; the 501-1000 mL band is set to grow at an 11.55% CAGR to 2031.

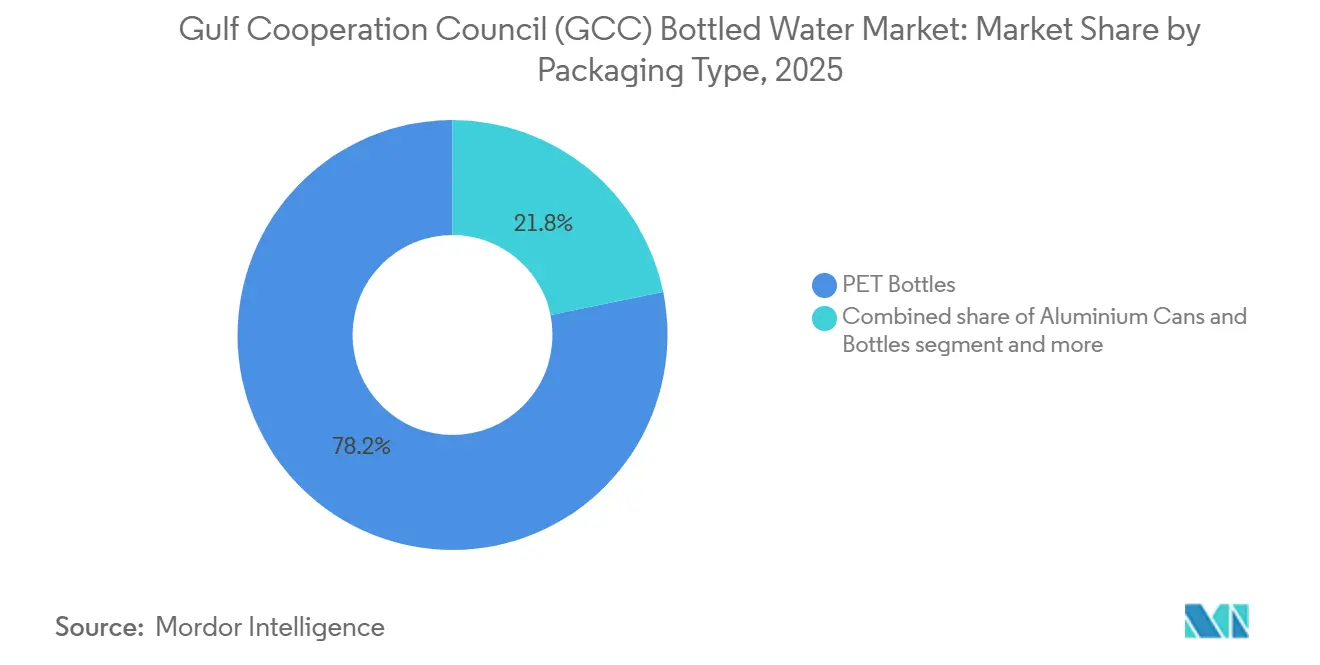

- By packaging type, PET bottles dominated with 78.21% share in 2025, whereas aluminum cans and bottles are forecast to advance at an 11.81% CAGR.

- By distribution channel, off-trade outlets accounted for 61.65% of value in 2025, but on-trade sales are tracking a 12.87% CAGR on the back of new hotels, restaurants, and entertainment venues.

- By geography, Saudi Arabia led with 33.02% of 2025 revenue, yet the United Arab Emirates is expected to post the quickest climb at an 11.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Gulf Cooperation Council (GCC) Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme climatic conditions and year-round hydration needs | +2.8% | Gulf Cooperation Council (GCC)-wide, peak impact in Saudi Arabia, UAE, Kuwait | Long term (≥ 4 years) |

| Growth of tourism industry coupled with government initiatives | +2.4% | United Arab Emirates (Dubai, Abu Dhabi), Saudi Arabia (Riyadh, Jeddah, NEOM), Qatar | Medium term (2-4 years) |

| Rising disposable incomes across Saudi Arabia and UAE | +1.9% | Saudi Arabia, United Arab Emirates, with spillover to Qatar, Bahrain | Medium term (2-4 years) |

| Innovation in packaging and portability | +1.70% | Gulf Cooperation Council (GCC)-wide, early adoption in United Arab Emirates and Saudi Arabia | Short term (≤ 2 years) |

| E-commerce and rapid-delivery expansion | +1.50% | United Arab Emirates, Saudi Arabia, Kuwait (urban centers) | Short term (≤ 2 years) |

| Marketing and premiumisation strategies by major brands | +1.20% | Gulf Cooperation Council (GCC)-wide, concentrated in high-income urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extreme climatic conditions and year-round hydration needs

Ambient temperatures exceeding 45°C for 4-5 months annually across the GCC drive non-discretionary water consumption, making demand resilient to economic downturns. Per-capita bottled water consumption in the UAE and Saudi Arabia consistently ranks among the highest globally. This is influenced by outdoor work restrictions during peak heat hours and cultural preferences for chilled, sealed beverages over tap water. The World Health Organization's 2024 guidelines on hydration in extreme heat recommend a daily intake of 3-4 liters for adults engaged in moderate outdoor activity. This aligns with observed consumption increases during Ramadan and summer months, when iftar gatherings contribute to bulk purchases [1]Source: World Health Organization, who.int. While desalination-dependent municipal water supplies meet potability standards under GSO 149:2021, taste and odor concerns often lead consumers to prefer bottled water, particularly in older residential areas where distribution infrastructure predates modern corrosion-resistant piping.

Growth of the tourism industry, coupled with government initiatives

The GCC bottled water market is experiencing steady growth, driven by tourism, pilgrimage activities, and substantial government investments in water infrastructure. The region's hot climate, high tourist arrivals, and expanding hospitality sector are key factors increasing demand for safe, packaged drinking water in hotels, airports, religious sites, entertainment venues, and transport hubs. Tourism in the GCC has demonstrated strong performance. In 2024, Qatar welcomed approximately 5 million visitors and recorded nearly 10 million room nights, with 41% of visitors coming from other GCC countries, highlighting robust intra-regional travel [2]Source: Qatar Tourism, "2024: A Year of Milestones of Qatar Tourism", qatartourism.com. Similarly, the UAE is experiencing an 11% annual growth in tourism investments, projected to reach USD 20.3 billion by 2027, according to the Ministry of Economy [3]Source: Ministry of Economy and Tourism, "Local addressable Market", moet.gov.ae. The expansion of hospitality infrastructure, including hotels, resorts, serviced apartments, and entertainment attractions, is directly contributing to increased bottled water consumption across retail and on-premise channels. In addition to tourism growth, government-led initiatives in water security are enhancing supply stability and reinforcing consumer reliance on packaged drinking water. In March 2025, the GCC established a regional water security task force, supported by USD 58 billion in environmental investments made between November 2024 and March 2025, reflecting strong policy coordination. Furthermore, the Saline Water Conversion Corporation (SWCC), the world's largest producer of desalinated water, achieved daily production exceeding 11.5 million cubic meters in 2024. While desalination strengthens national water resilience, bottled water remains the preferred choice for tourists and mobile populations due to its convenience, perceived safety, and portability.

Rising disposable incomes across Saudi Arabia and UAE

Rising disposable incomes in Saudi Arabia and the UAE are driving growth in the GCC bottled water market. Increased purchasing power is influencing consumer spending patterns, leading to a preference for packaged and premium hydration products. As household incomes rise, consumers are allocating a greater portion of their budgets to health-focused, convenient, and branded consumables, including bottled water. According to data from the General Authority for Statistics (GASTAT), the average Saudi household spends approximately SAR 18,056 per month [4]Source: General Authority for Statistics (GASTAT) , "Total Kingdom population exceeds 35 million by mid-2024", stats.gov.sa. This spending level reflects improved income stability and greater consumption capacity, fostering higher per capita expenditure on packaged drinking water. In urban areas such as Riyadh, Jeddah, Dubai, and Abu Dhabi, higher-income households are increasingly choosing branded bottled water over tap water for perceived quality, safety, mineral content, and alignment with lifestyle preferences. In the UAE, the high concentration of expatriates, robust tourism inflows, and a large working professional population further boost bottled water demand. Rising disposable incomes are also fueling premiumization trends, including growing demand for imported mineral water, alkaline water, glass-packaged water, and functional variants enriched with electrolytes or vitamins. Additionally, consumers are increasingly willing to invest in sustainable packaging options and subscription-based home and office delivery services.

Innovation in packaging and portability

Innovation in packaging and portability is driving growth in the GCC bottled water market as manufacturers adapt to changing consumer preferences for convenience, sustainability, and on-the-go consumption. In a region characterized by high temperatures, urban mobility, outdoor activities, and a robust hospitality sector, packaging functionality significantly influences purchasing decisions. Consumers are increasingly opting for lightweight, easy-to-carry, and ergonomically designed bottles that cater to active lifestyles, travel, and workplace hydration. Single-serve formats, resealable caps, sports caps, and compact bottles designed to fit car cup holders and handbags are gaining popularity, particularly among younger demographics and working professionals. Additionally, bulk multi-pack formats and large-capacity containers are driving demand in households and corporate offices. Sustainability-focused packaging innovation is also influencing market dynamics. Regional governments are promoting environmental responsibility, encouraging manufacturers to use recyclable PET, biodegradable materials, reduced plastic content, and lightweight bottle designs to lower carbon footprints. Brands are introducing recycle-ready labels, tethered caps, and eco-friendly packaging claims to meet regulatory requirements and address growing consumer awareness of environmental impact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-waste legislation raising compliance costs | -1.60% | United Arab Emirates (Abu Dhabi, Dubai), Saudi Arabia, Bahrain | Short term (≤ 2 years) |

| Market saturation with many local and international brands | -1.30% | Gulf Cooperation Council (GCC)-wide, most acute in the United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| High energy cost of desalination bottling | -0.90% | Gulf Cooperation Council (GCC)-wide, peak impact in Saudi Arabia, Oman | Medium term (2-4 years) |

| Water scarcity and resource limitations | -0.70% | Gulf Cooperation Council (GCC)-wide, long-term structural constraint | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-waste legislation raising compliance costs

Abu Dhabi's 2025 Water Quality Regulations introduce extended producer responsibility requirements, obligating bottlers to fund collection and recycling infrastructure. This is expected to increase compliance costs by an estimated USD 0.02-0.04 per unit, which may disproportionately impact smaller regional players that lack economies of scale. Additionally, the GCC Standardization Organization's draft standard on contaminant limits for mineral water, anticipated to be finalized by late 2026, will impose stricter limits on heavy metals such as lead, arsenic, and mercury. This will require bottlers to upgrade their filtration and testing protocols to avoid product recalls and potential reputational harm. Furthermore, Dubai Municipality's 2024 technical guidelines for plastic waste management establish minimum recycled content thresholds, starting at 25% by 2026 and increasing to 50% by 2030. Compliance with these guidelines will necessitate capital investments in rPET sourcing and quality assurance systems, with non-compliance penalties reaching up to AED 500,000 (USD 136,000) per violation.

Market saturation with many local and international brands

GCC holds significant bottled water brands that compete in GCC retail markets, leading to fragmented consumer attention and reduced shelf space allocations in hypermarkets. Key players such as Nestlé, Danone, and PepsiCo utilize volume rebates to secure premium eye-level shelf positioning. Price competition has intensified in the economy segment, with promotional discounts like buy-2-get-1-free and bundle offers reducing gross margins for value-tier SKUs to 12-15%, compared to 18-20% during 2020-2022. New entrants face significant barriers, as established brands maintain long-term supply agreements with major retailers, operate proprietary distribution fleets, and benefit from decades of brand recognition. As a result, niche opportunities are largely confined to ultra-premium imports or functional variants targeting specific health claims, such as alkaline pH, added electrolytes, or vitamin infusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Variants Gain Health-Conscious Traction

Still water accounted for 77.14% of the projected 2025 revenue, driven by its role in meeting everyday hydration needs and its popularity for bulk purchasing in homes, offices, and events. However, functional/enhanced water is expected to grow at a compound annual growth rate (CAGR) of 12.59% through 2031, as urban professionals and fitness enthusiasts increasingly seek products offering electrolyte replenishment, vitamin fortification, and alkaline pH levels, which are marketed as performance and wellness enhancers. Sparkling water maintains a niche market share of 5-7%, limited by cultural preferences for non-carbonated beverages and restricted shelf space in convenience stores. Despite these constraints, premium imports such as Perrier and San Pellegrino continue to have a presence in hospitality channels.

Flavored and infused water, featuring natural fruit essences and herbal extracts, is capturing a 3-4% market share by appealing to younger consumers aged 18-30, who often perceive plain water as uninteresting and prefer sensory variety without the calorie content of sugary soft drinks. Brands are increasingly fortifying water with magnesium, zinc, and B vitamins, positioning these products at a 20-40% price premium over standard still water. These variants are primarily targeted at distribution channels such as gyms, yoga studios, and corporate wellness programs.

By Packaging Size: Mid-Range Formats Drive Convenience

The 331-500 mL segment accounted for a 40.18% market share in 2025, driven by its single-serve convenience in retail, foodservice, and vending channels. Meanwhile, the 501-1000 mL format is experiencing growth at a CAGR of 11.55%, as consumers prioritize cost efficiency per liter for activities such as gym sessions, office use, and car cup holders, where larger volumes help reduce repurchase frequency. Packaging sizes under 330 mL, such as 250 mL and 200 mL, cater to specific needs like children's lunchboxes and airline services, maintaining a stable market share of 8-10%. The 1001-2000 mL range, including 1.5 L bottles, dominates home consumption with a 22-25% share, preferred for refrigerator storage and family meals.

The 2001-5000 mL segment, comprising 5 L and 6 L jugs, along with formats above 5001 mL, such as 10 L and 18.9 L water cooler bottles, collectively represent 15-18% of the market volume. These larger formats are primarily used in home and office delivery subscriptions, offering 30-40% cost savings compared to single-serve options. Packaging size preferences vary across distribution channels. Convenience stores and petrol stations tend to favor 330-500 mL formats for impulse purchases, while hypermarkets focus on 1.5 L bottles and multipacks for planned shopping trips. Online platforms show higher penetration of bulk formats, such as 5 L and 6 L, as delivery logistics mitigate the challenges of handling heavier products.

By Packaging Type: Aluminum Gains as Sustainability Narrative Strengthens

PET bottles accounted for 78.21% of the projected 2025 volume, driven by advantages such as lightweight logistics, shatter resistance, and an established recycling infrastructure. However, aluminum cans and bottles are growing at a CAGR of 11.81%, as brands capitalize on aluminum's ability to be recycled indefinitely without quality degradation and its premium positioning, which supports price premiums of 15-25% over comparable PET formats. Glass bottles, despite holding only a 4-6% market share due to their weight, fragility, and higher transport costs, dominate the ultra-premium segment (USD 3-6 per liter) in fine dining and luxury retail, where visual appeal and perceived purity outweigh logistical challenges. Other packaging formats, including pouches, cartons, and refillable containers, maintain a marginal 2-3% share. However, refillable glass and stainless steel bottles are gaining popularity within corporate sustainability initiatives and among eco-conscious consumers.

Agthia's August 2025 introduction of 100% rPET bottles for its Al Ain Water brand marks a significant milestone, showcasing the technical and economic feasibility of closed-loop recycling at a GCC scale, supported by municipal collection systems and consumer return incentives. The renewed interest in aluminum packaging is partly attributed to Ball Corporation's regional capacity expansions and partly to Gen Z and millennial consumers, who associate metal packaging with environmental responsibility. This perception is further reinforced by social media campaigns emphasizing the impact of ocean plastic pollution.

By Distribution Channels: On-Trade Accelerates with Hospitality Expansion

Off-trade channels, including supermarkets, hypermarkets, convenience stores, and online retail, accounted for 61.65% of projected 2025 sales. This growth is attributed to household bulk purchases and the increasing presence of neighborhood grocers in residential areas. However, on-trade channels are experiencing a compound annual growth rate (CAGR) of 12.87%, driven by the expansion of Saudi Arabia's entertainment sector (cinemas, theme parks, concert venues) and the UAE's hospitality industry (hotels, restaurants, cafes) under tourism-focused growth strategies.

On-trade channels benefit from significant margin advantages. Hotels and restaurants typically mark up bottled water prices by 200-400% compared to retail, resulting in higher per-unit profitability that compensates for lower sales volumes. Additionally, captive environments such as airports, stadiums, and amusement parks reduce competitive pricing pressures. The home and office delivery subsegment, categorized under off-trade but operationally distinct, relies on subscription models and bulk packaging formats (5 L, 10 L, 18.9 L) to secure recurring revenue and lower customer acquisition costs. However, this subsegment faces high churn rates as price-sensitive corporate clients frequently switch suppliers to achieve marginal cost savings.

Geography Analysis

Saudi Arabia accounted for 33.02% of 2025 revenue, supported by a population exceeding 36 million, the annual influx of 13 million Hajj and Umrah pilgrims, and Vision 2030 infrastructure initiatives such as NEOM, the Red Sea Project, and Qiddiya. These developments are driving growth in the hospitality and entertainment sectors. Bottled water consumption in the Kingdom is segmented into two distinct patterns: urban centers like Riyadh, Jeddah, and Dammam are witnessing premiumization trends with increasing demand for functional and imported brands, while rural and lower-income areas remain price-sensitive, favoring economy multipacks from local producers such as Berain, Hana, and Nova.

The United Arab Emirates, while holding a smaller share of the 2025 market, is projected to achieve the fastest geographic CAGR of 11.71% through 2031. This growth is driven by Dubai's 20.2 million overnight visitors in 2024, Abu Dhabi's regulatory push for sustainability, including a 100% rPET mandate by 2028, and a high-income expatriate population, which constitutes 88% of residents and shows a preference for premium and functional water variants. Additionally, Dubai's quick-commerce platforms, such as Talabat, Noon Minutes, and Careem Quik, enable bottled water delivery within 15-30 minutes across urban areas. This ecosystem facilitates impulse purchases through app-based transactions and allows brands to test new SKUs with minimal reliance on retail shelf space.

Kuwait, Qatar, Bahrain, and Oman collectively contribute 25-30% of GCC bottled water revenue, each influenced by unique demand factors. In Kuwait, extreme summer temperatures, often exceeding 50°C, and high per-capita income drive strong consumption levels. However, market saturation and limited population growth, currently at 4.3 million, restrict further expansion. Qatar's post-2022 FIFA World Cup infrastructure, including stadiums, metro systems, and convention centers, has institutionalized high-volume procurement for public events. This has created a captive on-trade demand, favoring bottlers with ISO certifications and efficient logistics capabilities.

Competitive Landscape

The GCC bottled water market demonstrates moderate concentration. Multinational corporations such as Nestlé, Danone, PepsiCo, and Coca-Cola collectively hold an estimated 35-40% market share. Regional players, including Agthia, Masafi, Mai Dubai, Berain, and Almarai, also maintain a significant presence. Smaller competitors focus on price differentiation, localized distribution through neighborhood grocers and independent retailers, and cultural alignment through Arabic branding and Ramadan-themed packaging.

Opportunities for growth are concentrated in three key areas: ultra-premium functional waters targeting fitness and wellness communities, subscription-based home and office delivery services featuring IoT-enabled coolers with auto-reordering capabilities, and refillable glass bottle systems aimed at corporate campuses and hotels seeking to reduce single-use plastic waste. Technology adoption varies across the market. Leading bottlers utilize route optimization software and demand forecasting algorithms to minimize logistics costs, whereas mid-tier players often rely on manual distribution planning and reactive inventory management.

Compliance with GSO standards, such as GSO 149:2021 for unbottled water and GSO 2233:2021 for nutritional labeling, is a baseline requirement. However, leading companies are pursuing additional voluntary certifications, including ISO 22000 for food safety and NSF/ANSI 60 for drinking water additives, to gain a competitive edge in on-trade channels where procurement managers prioritize risk mitigation over cost. The market's moderate concentration indicates that economies of scale in distribution and brand recognition provide competitive advantages. Nevertheless, regional players leverage their local expertise, such as understanding Ramadan consumption patterns, preferred packaging sizes, and retail credit terms, to maintain their market share against multinational competitors.

Gulf Cooperation Council (GCC) Bottled Water Industry Leaders

-

PepsiCo Inc.

-

Nestlé S.A

-

Agthia Group PJSC

-

Danone S.A

-

Masafi LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Almarai Company has acquired full ownership of Pure Beverages Industry Company, a bottled water producer in Saudi Arabia, for SAR 1.040 billion. Pure Beverages, known for its "Ival" and "Oska" brands, holds a significant position in the Kingdom's bottled water market.

- April 2025: PepsiCo has invested SAR 30 million (USD 8 million) to establish a regional research and development center in Riyadh. The center aims to drive innovation and develop products, including bottled water, tailored to regional preferences, reflecting PepsiCo's growing focus on the Middle Eastern market.

- October 2024: Nova, a brand under Health Water Bottling Co. Ltd., has entered into a partnership agreement to serve as a support partner for the SAL Jeddah GT Race 2024.

- April 2024: Health Water Bottling Co. Ltd.'s Nova brand has introduced water bottles made entirely from recycled materials. This initiative supports the sustainability goals outlined in Saudi Vision 2030 and the Saudi Green Initiative.

Gulf Cooperation Council (GCC) Bottled Water Market Report Scope

Bottled drinking water types are sometimes carbonated, sealed in bottles, and usually certified as pure. The market studied is segmented by type, distribution channel, and geography. By type, the market has been segmented into still water, sparkling water, and functional water. By distribution channel, the market has been segmented into supermarkets/hypermarkets, convenience/grocery stores, on-trade channels, home and office delivery, and other distribution channels. The report outlines the insights from countries in the region, including Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, Bahrain, and Oman. The report offers market size and forecasts in value (USD million) for the above segments.

By Product Type

| Still Water |

| Sparkling Water |

| Functional / Enhanced Water |

| Flavored / Infused Water |

By Packaging Size

| *Less than 330 mL |

| *331 mL-500 mL |

| *501 mL-1000 mL |

| *1001 mL- 2000 mL |

| *2001 mL- 5000 mL |

| *More than 5001 mL |

By Pakaging Type

| PET Bottles |

| Glass Bottles |

| Aluminium Cans and Bottles |

| Others |

By Distribution Channels

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Home and Office Space |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| Kuwait |

| Qatar |

| Bahrain |

| Oman |

| By Product Type | Still Water | |

| Sparkling Water | ||

| Functional / Enhanced Water | ||

| Flavored / Infused Water | ||

| By Packaging Size | *Less than 330 mL | |

| *331 mL-500 mL | ||

| *501 mL-1000 mL | ||

| *1001 mL- 2000 mL | ||

| *2001 mL- 5000 mL | ||

| *More than 5001 mL | ||

| By Pakaging Type | PET Bottles | |

| Glass Bottles | ||

| Aluminium Cans and Bottles | ||

| Others | ||

| By Distribution Channels | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Home and Office Space | ||

| By Geography | United Arab Emirates | |

| Saudi Arabia | ||

| Kuwait | ||

| Qatar | ||

| Bahrain | ||

| Oman | ||

Key Questions Answered in the Report

How large is the Gulf Cooperation Council (GCC) bottled water market in 2026?

The Gulf Cooperation Council (GCC) bottled water market size is USD 10.48 billion in 2026 and is forecast to hit USD 18.01 billion by 2031.

What is the expected growth rate for the Gulf Cooperation Council (GCC) bottled water market from 2026 to 2031?

Aggregate values are projected to expand at an 11.44% CAGR over the period.

Which country leads sales within the Gulf?

Saudi Arabia accounts for 33.02% of 2025 revenue owing to its scale and pilgrimage influx.

Which product segment is growing fastest?

Functional/enhanced Water variants are slated for a 12.59% CAGR as health consciousness rises.

Page last updated on: