Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

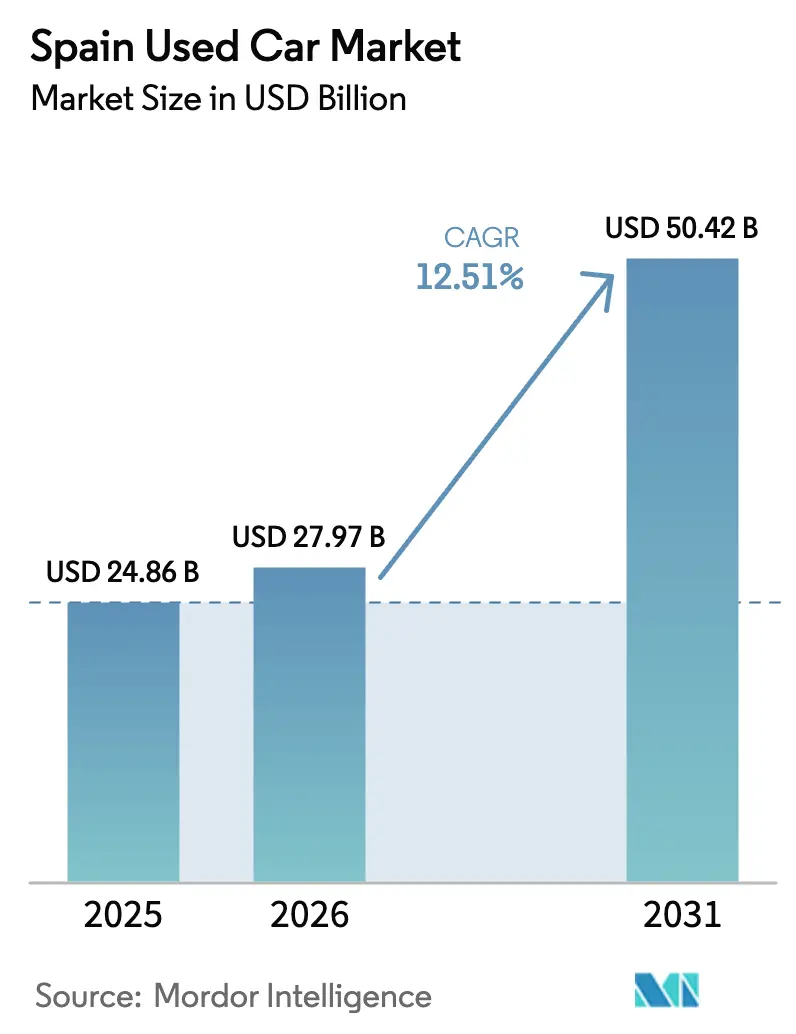

| Base Year Market Size (2025) | USD 24.86 Billion |

| Market Size (2026) | USD 27.97 Billion |

| Market Size (2031) | USD 50.42 Billion |

| Growth Rate (2026 - 2031) | 12.51% CAGR |

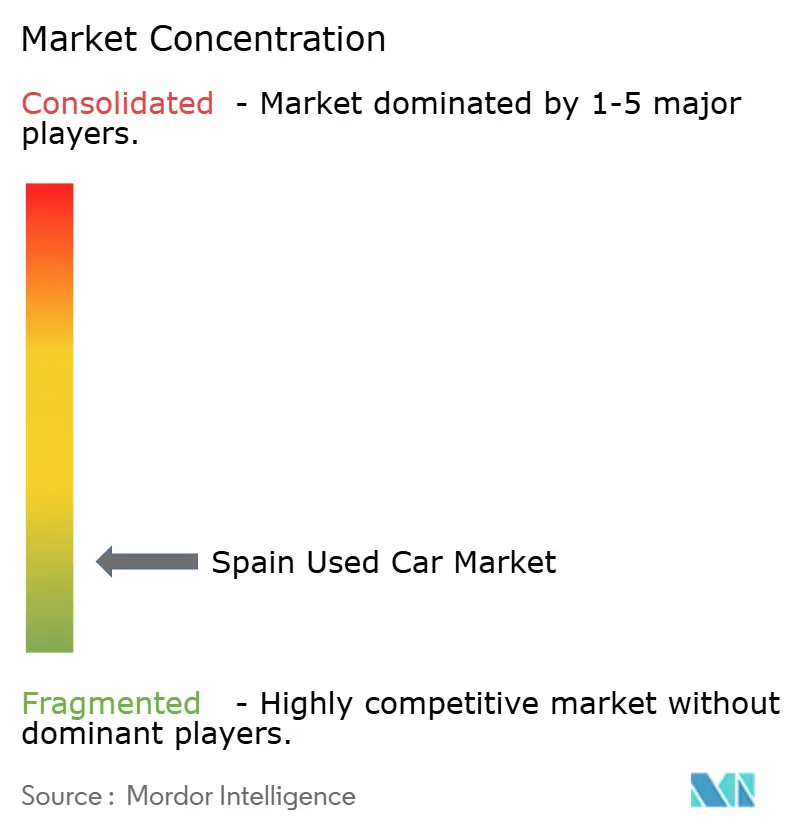

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Used Car Market Analysis by Mordor Intelligence

The Spain Used Car Market size was valued at USD 24.86 billion in 2025 and is estimated to grow from USD 27.97 billion in 2026 to reach USD 50.42 billion by 2031, at a CAGR of 12.51% during the forecast period (2026-2031), as tightening Euro 7 rules and macroeconomic caution channel buyers toward affordable second-hand mobility.[1]Directorate-General for Mobility and Transport, “Euro 7 Vehicle Emissions Proposal,” European Commission, ec.europa.eu Demand is reinforced by a national fleet whose average age exceeds 14 years, a factor that broadens the stock of trade-ins, compresses depreciation in older diesel inventory, and raises the appeal of younger, electrified models. Digital platforms that promise 2-hour home delivery and transparent vehicle-history reports are reshaping dealer economics, allowing organized players to erode the price advantage long held by unorganized lots. Regionally, Andalusia anchors sales through volume, whereas Madrid leverages higher disposable income and strong corporate fleet turnover to produce the fastest regional growth. Inventory pipelines benefit from leasing and rental operators cycling out 0-2 year-old vehicles, altering residual-value curves, and encouraging OEMs to expand certified pre-owned programs.

Key Report Takeaways

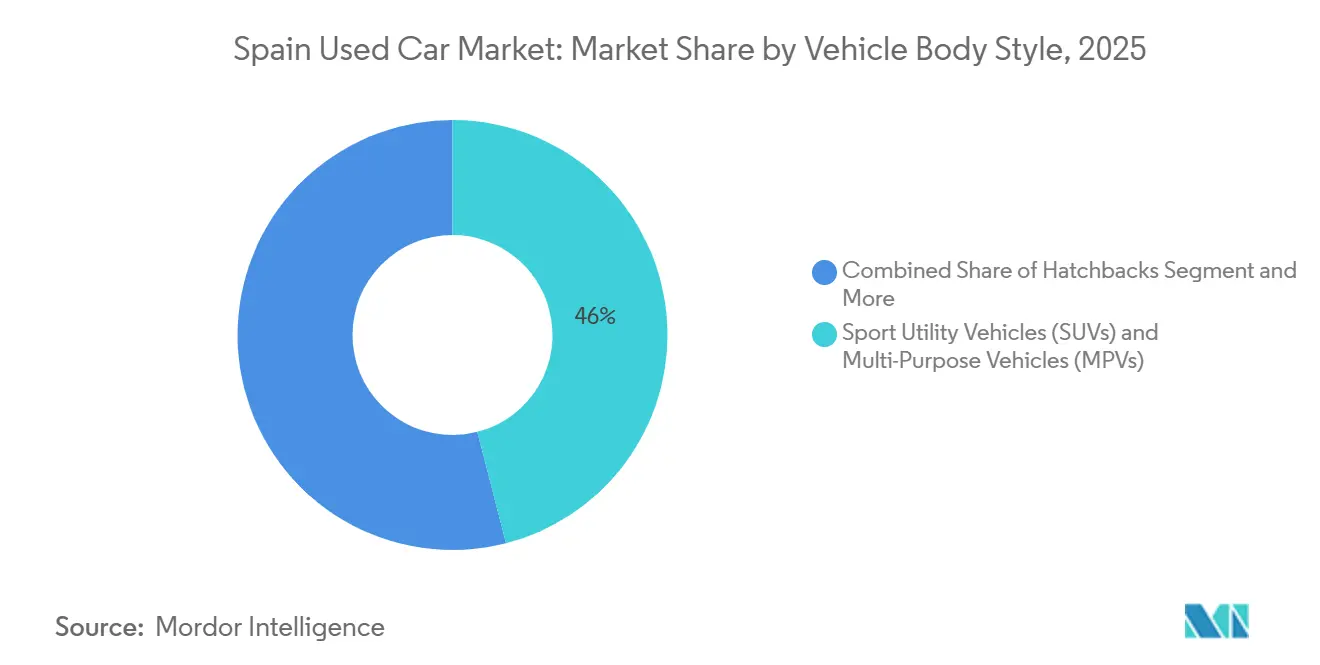

- By vehicle body style, SUVs and MPVs led with a 46.03% revenue share in 2025 and are expected to advance at a 13.45% CAGR through 2031.

- By vendor type, the unorganized segment held 66.13% of the Spanish used-car market share in 2025, while organized platforms recorded the highest projected CAGR at 14.65% through 2031.

- By booking type, offline transactions accounted for 75.25% of the Spanish used-car market in 2025; however, online bookings are expected to expand at a 15.46% CAGR through 2031.

- By fuel type, diesel accounted for 48.33% of the Spanish used-car market in 2025, and electric vehicles are projected to post the fastest growth, with a 16.21% CAGR through 2031.

- By vehicle age, the 3-5-year bracket commanded a 39.12% share of the Spanish used-car market in 2025, while units aged 0-2 years are expected to advance at a 15.08% CAGR through 2031.

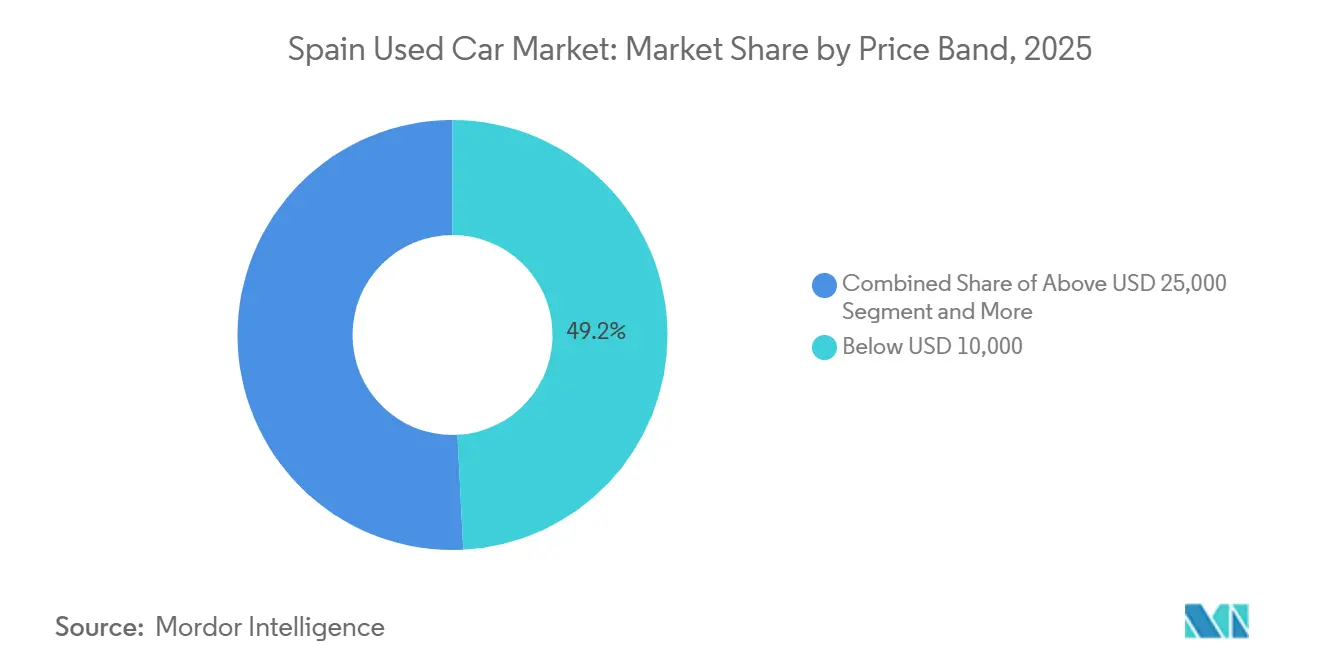

- By price band, units below USD 10,000 accounted for 49.24% of sales in 2025, while the USD 15,000-25,000 range is growing at a 13.78% CAGR.

- By customer type, individual buyers represented 86.11% of the volume in 2025, while corporate or fleet buyers are expected to log the highest 15.71% CAGR through 2031.

- By Spanish Region, Andalusia captured a 37.44% share in 2025, whereas the Community of Madrid is set to expand at a 13.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Off-Lease Fleet Adds Younger Inventory | +2.5% | National, early concentration in Madrid, Catalonia | Medium term (2-4 years) |

| EU Rules Boost Older Car Trade | +2.3% | National, with concentration in Andalusia, Catalonia, and Madrid | Medium term (2-4 years) |

| Digital Platforms and Home Delivery | +2.1% | National, early adoption in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Uncertainty Drives Value-Focused Buyers | +1.8% | National, most visible in Andalusia and the Valencian Community | Short term (≤ 2 years) |

| OEM CPO Programs Expanding | +1.6% | National, led by Madrid, Barcelona, and Seville | Long term (≥ 4 years) |

| Vehicle History Reports Availability | +1.4% | National, supported by DGT and ITV systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Supply of Off-Lease and Rental Fleet Vehicles Adds Younger Inventory

In Spain's used-car market, an unprecedented influx of near-new stock is being injected as leasing fleets, now exceeding significant volumes, return vehicles after approximately 2 years. Arval’s MotorTrade platform, a key player, annually pushes a substantial number of units and has shown remarkable growth in its Re-lease proposition, which recontracts late-model cars. Meanwhile, rental companies are disposing of cars within a shorter time frame, driving growth in the younger vehicle segment. This influx of younger vehicles not only elevates average quality and reduces reconditioning times but also bolsters the rise of certified pre-owned programs, which come bundled with warranties and roadside assistance.

EU Emissions Rules Enlarging Pool of Trade-Ins for Older ICE Vehicles

Euro 7 standards, scheduled to take effect from 2025, raise the cost of ownership for aging diesel and petrol cars, encouraging owners to dispose of non-compliant units before urban low-emission zones tighten enforcement. Spain’s fleet age of 14.2 years is driving a surge of diesel trade-ins that are now facing rapid price compression, particularly in the 6-8-year bracket[2]“Vehicle Fleet 2025,” Spanish Directorate General of Traffic, dgt.es . In a bid to hasten fleet renewal, Royal Decree Law 4/2024 offers accelerated depreciation for low-emission vehicles. This incentive is pushing fleet operators to refresh their assets at a quicker pace. Certain regions are experiencing the largest influx of older internal combustion engine (ICE) vehicles. This trend is altering the dealer landscape, as organized vendors pivot to focus on younger inventory for better margins. The uptick in supply is making consumers more price-sensitive, a trend that favors larger marketplaces adept at algorithmic pricing.

End-to-End Digital Retail Platforms With Home Delivery

Shoppers can now complete paperwork, make payments, and schedule deliveries online via platforms such as Clicars, AutoScout24, Wallapop Motors, and Coches.net. This innovation has significantly reduced the time required for the search-to-purchase process. The growing popularity of virtual storefronts highlights a sustained shift in consumer behavior. Data from GANVAM reveals that a considerable portion of buyers begin their journey online, with many completing it digitally—a trend that continues to grow steadily. Early adoption is more prevalent in urban areas such as Madrid, Barcelona, and Valencia, where smartphone use is widespread. However, rural areas show slower adoption, indicating potential for hybrid click-and-collect models. To address the lack of physical test drives, platforms now offer inspection reports and return policies, which help boost conversion rates among cautious buyers.

Economic Uncertainty Heightens Value-Conscious Consumer Behavior

In 2024, GDP growth slowed, as rising mortgage rates reduced disposable incomes and pushed households toward the second-hand market. The preference for used cars reflects a broader focus on affordability, as families prioritize financial flexibility over purchasing new vehicles. High unemployment levels and limited asset bases further constrain budgets, driving demand for more economical car options. In regions with lower economic performance, such as Andalusia and the Valencian Community, buyers are particularly sensitive to financing conditions. This has led organized vendors to strengthen partnerships with banks, offering more accessible loan terms. These dynamics support faster sales turnover at reduced profit margins, benefiting platforms that excel in scaling digital underwriting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Depreciation Risk for ICE | -1.9% | National, most acute in low-emission zones of Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Sparse Public Charging Limits | -1.5% | National, particularly outside major metros | Long term (≥ 4 years) |

| Chip-Shortage Easing Price Gap | -1.2% | National, affecting all price bands | Short term (≤ 2 years) |

| VAT and Registration Taxes | -0.8% | National, friction highest on Andalusia-to-Madrid corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Depreciation Risk for ICE Assets Amid Electrification

Transactions continue to be led by diesel units, yet these units are witnessing sharper price drops, coinciding with a significant decline in new diesel registrations. Current data indicates that young BEVs are sitting on the market for extended periods, pointing to an oversupply and potential risks to their residual value. In contrast, petrol and hybrid units are spending less time on the market. Dealers, particularly those with substantial diesel inventories, are feeling the pinch. They're slashing margins to offload stock, especially for older cars nearing their annual ITV inspections. With low-emission zone restrictions tightening in Madrid and Barcelona, the stakes are raised, steering buyers more towards hybrid options.

Sparse Public Charging Limits Residuals on Used EVs

By mid-2024, public charging point installations had fallen significantly short of the target, with fast chargers exceeding 22 kW making up only a small proportion of the total. Due to range anxiety, buyers are less inclined to pay for used Battery Electric Vehicles (BEVs), resulting in a decline in their average asking price[3]“Average Used Car Price by Region July 2025,” Ganvam, ganvam.es. In rural areas, where many households lack private parking, the pure-EV market remains inaccessible, sustaining demand for hybrids. As a result, the growth forecast for electric units faces challenges until infrastructure density improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Body Style: SUVs Capture Versatility Demand

Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles (MPVs) accounted for 46.03% of sales in 2025 and are growing at a 13.45% CAGR, outpacing hatchbacks and sedans as families seek higher seating positions and flexible cargo space. Fleet disposals supply late-model hybrids such as the Tucson and Sportage, bolstering fuel-efficient choices. The Spanish used-car market for SUVs is projected to expand further as OEMs focus new-car launches on crossover designs, ensuring a robust secondary pipeline. Hatchbacks remain popular in urban areas where parking density favors compact dimensions, yet their share declines in absolute terms.

Demand drivers include tax incentives for low-emission SUVs, improved mild-hybrid efficiency, and stronger residuals linked to consumer preference stability. As public charging improves, electrified SUVs will likely displace older diesel MPVs, raising average transaction values. The Spanish used-car market share for SUVs is therefore poised to expand by the decade’s end if current flow dynamics persist.

By Vendor Type: Organized Platforms Scale Trust

Unorganized dealers controlled 66.13% of transactions in 2025, yet organized channels are compounding at 14.65% annually by 2031. Margin compression to 3-5% is offset by financing commissions and high sales velocity. Platforms integrate miDGT reports, blockchain verification, and 14-day returns to differentiate on transparency. The Spanish used car market size attributable to organized vendors is set to expand by 2031 as rural penetration improves.

Unorganized outlets retain strength in rural areas where personal relationships and flexible cash terms persist. However, as smartphone adoption saturates and bank partnerships extend credit scoring deeper into the population, digital marketplaces gain further leverage. Their ability to guarantee vehicle quality and deliver cars nationwide within hours reshapes buyer expectations, raising switching costs back to traditional lots.

By Booking Type: Digital Channels Compress Cycles

Online bookings will grow at a 15.46% CAGR as younger buyers prioritize convenience. Virtual 360-degree tours, single-click financing approval, and two-hour delivery reduce buying friction by a step change. Offline channels remain dominant with a 75.25% share in 2025, especially among older consumers who value tactile inspection. Dealers address that gap by offering hybrid models that enable online reservations and in-person pickup within 72 hours.

Growth headwinds include cybersecurity concerns and limited broadband in sparsely populated provinces, but as 5G coverage widens, these barriers recede. The shift to online is also expanding the Spanish used-car industry’s data pool, enhancing pricing algorithms that keep listed prices close to market-clearing levels, thereby accelerating stock turnover.

By Fuel Type: Electrification Tentatively Advances

Diesel retained 48.33% of 2025 transactions, but rising low-emission zones and a significant slide in new diesel registrations curbed future share. Battery-electric cars show the fastest 16.21% CAGR, yet sparse charging limits absolute penetration. Hybrids bridge the gap, enjoying strong loyalty among SUV buyers seeking lower running costs without range anxiety. Petrol remains stable due to widespread refueling access and attractive entry prices.

Used BEV pricing deflates as technology improves, trimming the Spain used-car market's premium once attached to electrification. Until charging density reaches critical thresholds, hybrids are likely to capture most incremental share. LPG and CNG stay niche because infrastructure and OEM support lag.

By Vehicle Age: Younger Inventory Gains

Cars aged 3-5 years held 39.12% of volume in 2025, but 0-2 year units grow at 15.08% CAGR on the back of leasing and rental disposals. Buyers appreciate warranty cover, low mileage, and improved emissions compliance. Corporate fleets favor near-new cars to manage downtime, amplifying demand. Vehicles 6-8 years old lose share as ITV testing frequency rises and depreciation accelerates, particularly for diesel.

Cars older than 8 years persist in budget-sensitive provinces, yet tightening scrappage programs will gradually remove the most aged units. The quality uplift lets organized dealers expand CPO lines and capture value beyond simple margin on metal, such as subscription and re-lease offerings.

By Price Band: Mid-Market Expands

Sub-USD 10,000 cars still command 49.24% share in 2025 but will slowly cede ground to the USD 15,000-25,000 bracket, growing at 13.78% CAGR. Mid-market growth aligns with buyers trading up to younger hybrids that lower lifetime running costs. The Spanish used car market size for mid-priced cars benefits from bank financing, pushing loan affordability wider. Above-USD 25,000 units edge up via luxury SUVs that retain residual value, especially in Madrid, Catalonia, and the Basque Country.

Inflationary pressures and older-fleet scrappage gradually lift baseline pricing, compressing the lowest tier’s share. Platforms respond by extending longer loan tenures and offering warranty add-ons to justify higher ticket sizes.

By Customer Type: Corporate Fleets Accelerate

Individual shoppers accounted for 86.11% of 2025 volume, while corporate buyers grew at a 15.71% CAGR, driven by leasing penetration surpassing a notable share of new registrations. Fleet managers favor younger cars for lower downtime and predictable total cost, feeding a secondary pipeline every 24-30 months. Arval data show a substantial share of fleets already employing used cars alongside planning adoption within three years, implying a sizeable uptick in B2B demand.

The trend accelerates residual-value stability in the 0-3 year cohort and prompts organized vendors to stand up dedicated fleet channels offering maintenance packages and bulk discounts. Individual demand remains resilient for affordable models, but the corporate shift tightens the supply of the youngest stock, underpinning price floors in that bracket.

Geography Analysis

Andalusia accounted for 37.44% of transactions in 2025, due to its 8.6 million inhabitants and lower average ticket prices that favor budget-conscious households. A dense network of unorganized dealers in Seville, Málaga, and Granada supplies older diesel inventory attractive to buyers prioritizing low upfront cost. Madrid captured a smaller base yet posted a 13.05% CAGR, propelled by GDP per capita above the national mean, dynamic corporate fleet turnover, and rapid uptake of digital marketplaces that furnish home delivery across the metro.

Catalonia, anchored by Barcelona, edges up on the back of electrification demand and tech-savvy consumers comfortable with full online purchase flows. The Valencian Community records balanced growth, reflecting a mix of affordability and rising organized penetration. In contrast, the Rest of Spain sees share erosion as younger adults migrate to urban hubs and aged stock exits the fleet under scrappage schemes.

In the Basque Country, average prices are among the highest, while Madrid is close behind. Andalusia lags, influenced by a vehicle mix leaning towards older diesels. Charging infrastructure is predominantly found in Madrid and Catalonia, leading to quicker adoption of Battery Electric Vehicles (BEVs) than in rural areas. As low-emission zones expand and logistics networks streamline delivery times, the historical drawback of cross-regional purchases diminishes, signaling an ongoing geographic shift.

Competitive Landscape

Spain’s used-car arena remains fragmented, yet algorithm-driven platforms such as AUTO1, BCA, and Coches.net aggressively consolidate share by pairing low margins with high stock velocity. Their scale allows 2-hour delivery, 14-day returns, and high financing approval rates, building competitive barriers hard to replicate in single-lot operations. Hybrid models merging peer-to-peer listings with professional inventories, typified by Wallapop Motors and AutoScout24, attract substantial traffic and deepen data insights.

Disruptive finance plays include Arval Re-lease, which grew significantly year over year by offering second-hand leasing that expands access for cash-strapped buyers. Tech providers like carVertical improve transparency through blockchain histories, enabling smaller dealers to compete on trust.

Competition intensifies as organized share approaches a notable share by the decade’s close. Unorganized dealers may consolidate into franchise networks or pivot to niche offerings such as older diesel vans for rural use. Data analytics, omnichannel logistics, and captive financing will differentiate winners, while regulatory harmonization could further unlock cross-regional inventory flows, magnifying scale benefits.

Spain Used Car Industry Leaders

OcasionPlus

Clicars Spain SL

BCA Group

YAMOVIL SA

AUTO1.com GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Toyota Spain rolled out Autorola’s Fleet Monitor and Digital Showroom across its dealer network to digitize used-car remarketing.

- February 2025: Barcelona-based Dealcar raised EUR 3 million (~USD 3.1 million) in seed funding to expand its dealership SaaS and launch a new payment solution.

- February 2025: Stellantis partnered with Ayvens to recondition rental returns, reinforcing circular-economy objectives in the used-car channel.

- December 2024: CaixaBank introduced FaciliteaCoches, a dealer-only marketplace backed by bank financing, launching with 5,000 vehicles under six years and 100,000 kilometers.

Spain Used Car Market Report Scope

The scope includes segmentation by vehicle body style (hatchbacks, sedans, sport utility vehicles and multi-purpose vehicles, others), vendor type (organized, unorganized), booking type (online, offline), fuel type (petrol, diesel, electric, hybrid, others), vehicle age (0-2 years, 3-5 years, 6-8 years, above 8 years), price band (below USD 10,000, USD 10,000-USD 15,000, USD 15,000-USD 25,000, above USD 25,000), and customer type (individual, corporate/fleet). The analysis also covers regional-level segmentation, including Andalusia, Catalonia, the Community of Madrid, the Valencian Community, and the Rest of Spain. Market size and growth forecasts are presented by value in USD and by volume in units.

By Vehicle Body Style

| Hatchbacks |

| Sedans |

| Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles (MPVs) |

By Vendor Type

| Organized |

| Unorganized |

By Booking Type

| Online |

| Offline |

By Fuel Type

| Petrol |

| Diesel |

| Electric |

| Hybrid |

| Others |

By Vehicle Age

| 0-2 Years |

| 3-5 Years |

| 6-8 Years |

| Above 8 Years |

By Price Band

| Below USD 10,000 |

| USD 10,000-15,000 |

| USD 15,000-25,000 |

| Above USD 25,000 |

By Customer Type

| Individual |

| Corporate/Fleet |

By Spanish Region

| Andalusia |

| Catalonia |

| Community of Madrid |

| Valencian Community |

| Rest of Spain |

| By Vehicle Body Style | Hatchbacks |

| Sedans | |

| Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles (MPVs) | |

| By Vendor Type | Organized |

| Unorganized | |

| By Booking Type | Online |

| Offline | |

| By Fuel Type | Petrol |

| Diesel | |

| Electric | |

| Hybrid | |

| Others | |

| By Vehicle Age | 0-2 Years |

| 3-5 Years | |

| 6-8 Years | |

| Above 8 Years | |

| By Price Band | Below USD 10,000 |

| USD 10,000-15,000 | |

| USD 15,000-25,000 | |

| Above USD 25,000 | |

| By Customer Type | Individual |

| Corporate/Fleet | |

| By Spanish Region | Andalusia |

| Catalonia | |

| Community of Madrid | |

| Valencian Community | |

| Rest of Spain |

Key Questions Answered in the Report

How large is the Spain used car market today?

The Spain used car market size reached USD 27.97 billion in 2026

Which body style sells the most in Spain?

SUVs and MPVs lead, accounting for 46.03% of 2025 sales and growing faster than any other format.

Are online platforms overtaking traditional dealerships?

Online bookings held 24.75% of 2025 volume and are expanding at a 15.46% CAGR, yet offline channels remain dominant for now.

What fuel type is growing quickest in Spain’s second-hand market?

Electric vehicles post the fastest 16.21% CAGR through 2031, although hybrids currently capture broader demand due to charging limitations.

Why is Madrid the fastest-growing regional market?

Higher incomes, dense corporate fleets, and early adoption of digital purchasing push Madrid to a 13.05% CAGR through 2031.

Page last updated on: