Latin America Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.55 Billion |

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 4.48 Billion |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Telecom Tower Market Analysis by Mordor Intelligence

The Latin America Telecom Tower Market size in 2026 is estimated at USD 3.69 billion, growing from 2025 value of USD 3.55 billion with 2031 projections showing USD 4.48 billion, growing at 3.94% CAGR over 2026-2031.

Short-term growth pivots on network densification programs that support 5G rollouts, while medium-term momentum will come from large-scale spectrum auctions, rising edge-computing nodes, and sale-leaseback transactions that recycle capital for cash-constrained mobile network operators. Independent TowerCos are capturing the bulk of new tenancy contracts as operators shift to asset-light models, and renewable-powered sites are scaling rapidly in response to sustainability mandates. At the same time, municipal permitting delays and currency volatility continue to compress margins, forcing tower owners to refine hedging strategies and deepen regulatory engagement.

Key Report Takeaways

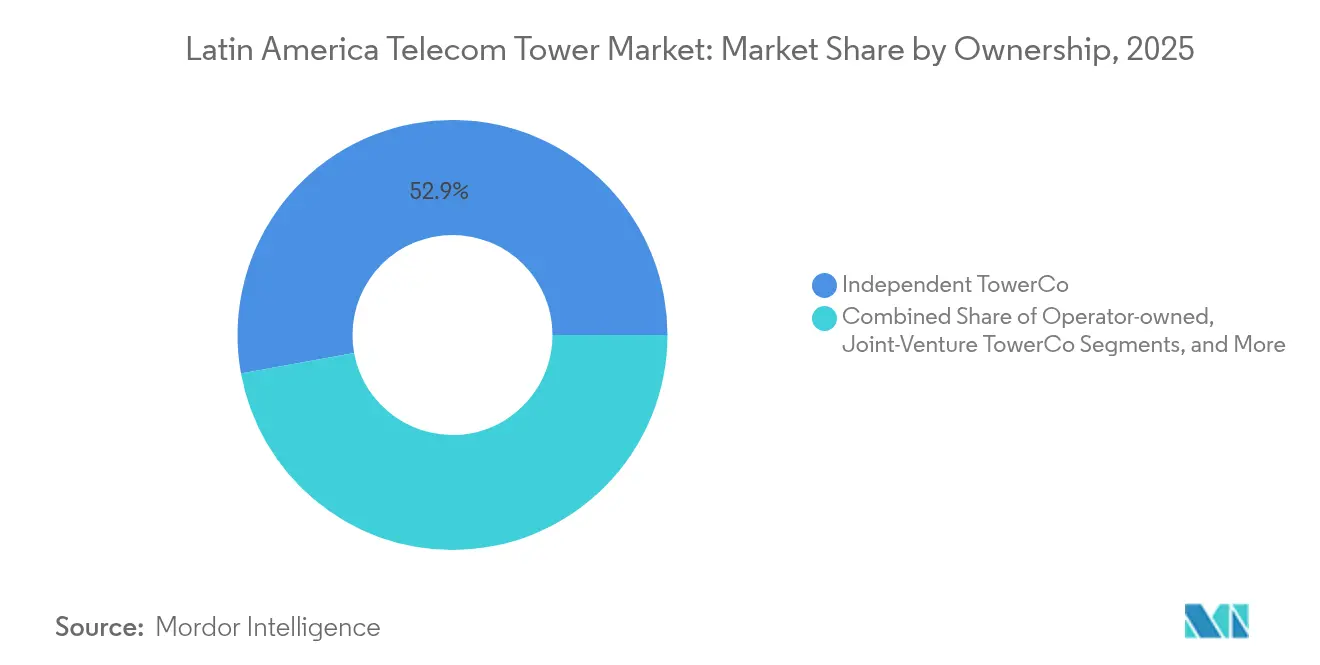

- By ownership, independent TowerCos led with 52.87% of the Latin America telecom tower market share in 2025 and are expanding at a 5.72% CAGR through 2031.

- By installation, ground-based configurations accounted for 82.55% of the Latin America telecom tower market size in 2025, while rooftop installations are set to grow at an 8.23% CAGR through 2031.

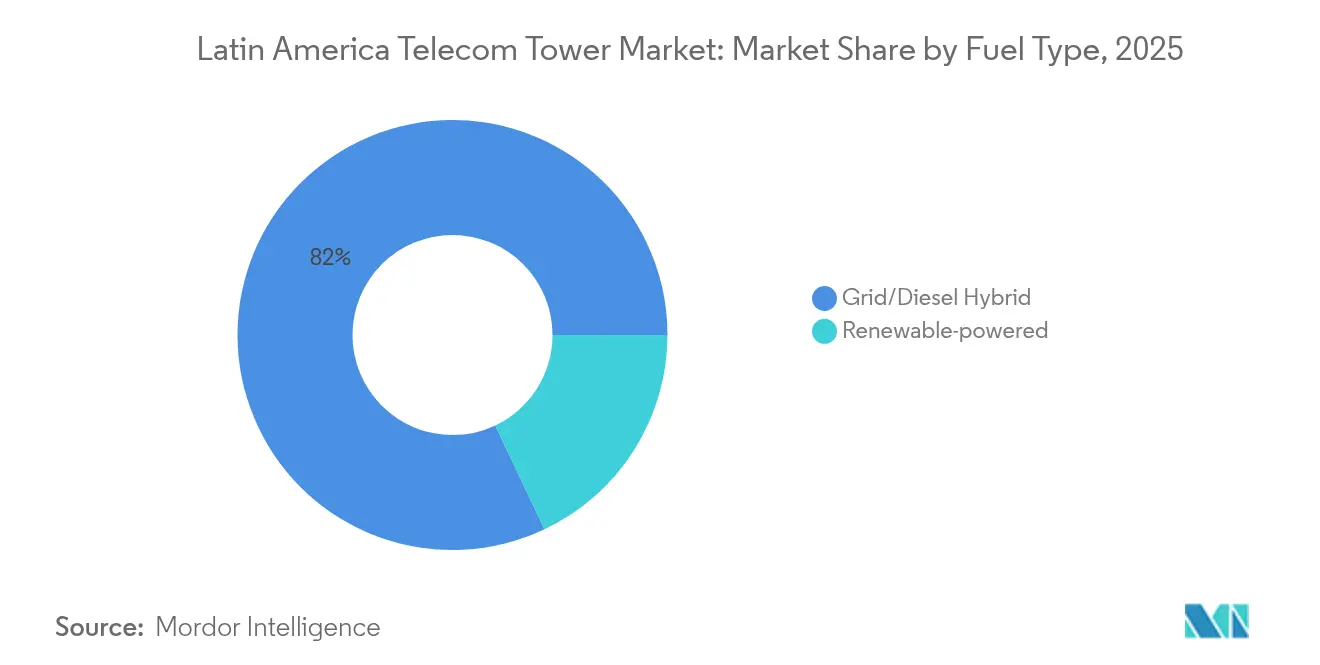

- By fuel type, grid/diesel hybrid systems captured 82.04% of the market in 2025; renewable-powered sites are advancing at a 12.74% CAGR to 2031.

- By tower type, monopoles represented 38.62% of total units in 2025; stealth/concealed towers are the fastest-growing type at a 9.74% CAGR through 2031.

- By country, Brazil held 35.27% of the Latin America telecom tower market size in 2025 and is also the fastest-expanding geography with a 5.28% CAGR expected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising 5G rollouts and related densification programs | +1.2% | Brazil, Mexico, Chile | Medium term (2-4 years) |

| Large‐scale spectrum auctions unlocking new sites | +0.8% | Mexico, Costa Rica, Paraguay | Short term (≤ 2 years) |

| Explosive mobile data-traffic growth | +0.9% | Urban Latin America | Long term (≥ 4 years) |

| Sale-leaseback initiatives by cash-strapped MNOs | +0.6% | Argentina, Colombia, Brazil | Short term (≤ 2 years) |

| Government rural-coverage funds (e.g., Brazil FUST) | +0.4% | Brazil (spillover to region) | Medium term (2-4 years) |

| Edge-computing and private-network nodes requiring micro-colocation | +0.3% | Urban Brazil, Mexico, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising 5G Rollouts and Related Densification Programs

Brazil alone needs 300,000 additional 4G antennas and 700,000 5G nodes to achieve nationwide coverage, illustrating the scale of densification underway. Mexico’s IFT-12 tender and Costa Rica’s recent 5G awards are accelerating radio upgrades, and operators increasingly favor leasing over greenfield builds to control capital intensity. Independent TowerCos benefit from multi-tenant leasing economics, while small-cell networks complement macro structures to enable network slicing for enterprise 5G services.

Large-Scale Spectrum Auctions Unlocking New Sites

Regulators have embedded rural build-out clauses into spectrum licenses, forcing carriers to construct new towers in low-ARPU areas that previously lacked commercial viability. Paraguay’s 2025 spectrum sale and Mexico’s continuing IFT auctions illustrate how policy can convert spectrum fees into tangible coverage gains. Tower companies willing to accept longer payback periods can secure first-mover advantages in underserved zones.

Explosive Mobile Data-Traffic Growth

Latin American data traffic continues to outpace existing capacity as video-rich applications proliferate in dense urban corridors. This volume drives vertical densification at current sites and horizontal expansion through small-cell overlays, boosting both tenancy ratios and the addressable colocation market. Rooftop specialists gain from landlord partnerships that bypass ground-leasing delays.

Sale-Leaseback Initiatives by Cash-Strapped MNOs

Operators pursuing asset-light strategies have accelerated tower divestitures, highlighted by SBA Communications’ USD 975 million purchase of 7,000 Millicom sites and KKR’s 1,100-tower deal with Tigo Colombia in January 2024. These transactions inject liquidity into carrier balance sheets while locking in multi-decade leases, enlarging the tower base available for independent ownership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal permitting bottlenecks and zoning caps | -0.7% | Brazil, Mexico, Colombia | Medium term (2-4 years) |

| FX volatility eroding USD-denominated lease yields | -0.5% | Argentina, Brazil | Short term (≤ 2 years) |

| Community NIMBY opposition and tower vandalism | -0.3% | Urban Brazil, Mexico | Long term (≥ 4 years) |

| Rising fiber-based small-cell substitution risk | -0.2% | Urban Chile, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Municipal Permitting Bottlenecks and Zoning Caps

Brazil still has about 5,000 antenna applications awaiting approval, some trapped in review for more than seven years. Diverse municipal criteria create inconsistent timelines, and aesthetic mandates increasingly require concealed designs, inflating capex.

FX Volatility Eroding USD-Denominated Lease Yields

The Argentine peso and Brazilian real each lost double-digit value against the US dollar during 2024, eroding USD-linked lease income for cross-border tower owners. While hedging can mitigate volatility, derivative costs compress net operating income. Domestic operators with local-currency revenues are relatively insulated, shifting competitive advantage toward regionally financed players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Drive Consolidation

Independent TowerCos controlled 52.87% of the Latin America telecom tower market in 2025, and the segment is projected to grow at a 5.72% CAGR through 2031, outpacing the overall market. Operator divestitures continue as cash-constrained MNOs unlock trapped capital, while investment funds favor predictable lease-indexed cash flows. The strategic shift allows carriers to prioritize spectrum and core-network upgrades, reinforcing the asset-light paradigm.

Joint-venture TowerCos, often structured around regulatory or local-capital requirements, are emerging as a hybrid between pure independents and captive portfolios. MNO-owned sites are expected to decline in share as additional sale-leaseback deals close. Efficient capital allocation and multi-tenant business models enable Independent TowerCos to achieve higher tenancy ratios, placing them at the center of regional consolidation.

By Installation: Rooftop Solutions Address Urban Constraints

Ground-based designs represented 82.55% of deployments in 2025, yet rooftop installations will expand at an 8.23% CAGR through 2031 as urban land prices and zoning sensitivities intensify . Brazil’s Sao Paulo and Mexico City exemplify metropolitan areas where landlords lease roof space to multiple tenants, boosting building owners’ revenue while accelerating operator roll-out timelines.

The Latin America telecom tower market size for rooftop sites is driving growth, creating a parallel ecosystem of structural engineering consultancies and rooftop aggregators. Rooftop solutions also reduce community opposition, as antennas blend into existing skylines, supporting higher frequencies essential for 5G throughput.

By Fuel Type: Renewable Integration Accelerates

Grid/diesel hybrids dominated with 82.04% share in 2025, but renewable-powered towers are projected to grow 12.74% annually through 2031 as operators decarbonize networks. Solar-hybrid deployments cut diesel use by up to 70%, trimming operating expenses and supporting corporate ESG goals.

EdgePoint Towers’ first solar-hybrid site demonstrated technical viability and OPEX savings in remote, grid-poor regions . Battery storage advances further extend autonomy. Consequently, renewable energy platforms attract climate-focused infrastructure funds, reinforcing their growth trajectory.

By Tower Type: Stealth Solutions Meet Aesthetic Demands

Monopoles accounted for 38.62% of units in 2025 due to flexible siting and moderate capex. Stealth/concealed designs, however, are growing at a 9.74% CAGR because municipalities increasingly require camouflaged infrastructure to preserve cityscapes.

Tree-mimicking poles and facade-integrated antennas command premium lease rates, offsetting higher fabrication costs. Although lattice structures remain essential for multi-tenant rural coverage, declining steel prices and modular monopole kits are narrowing the cost gap, increasing monopole adoption in semi-urban areas.

Geography Analysis

Brazil held 35.27% of the Latin America telecom tower market size in 2025 and is expected to maintain the lead with a 5.28% CAGR through 2031. Federal legislation promotes infrastructure sharing, and the BRL 4.8 billion FUST fund targets rural build-outs, such as Alcoa’s solar-powered Flextower project that delivered 4G to isolated Amazon communities . Independent TowerCos benefit from streamlined municipal codes adopted in 2024 that cap permitting timelines at 60 days.

Mexico ranks second by revenue and leverages proximity to North American data-center clusters, which stimulates edge-colocation demand along fiber routes. Ongoing IFT spectrum auctions mandate coverage in 1,450 underserved localities, translating directly into new tower builds. Chile’s robust submarine-cable gateways and renewable generation mix enhance its appeal for hyperscalers, positioning the country as a future edge-computing hub. Colombia and Peru exhibit mid-single-digit CAGRs driven by urban densification programs and rural connectivity subsidies. Security concerns in certain departments necessitate hardened tower designs, modestly lifting capex. Argentina’s macroeconomic volatility depresses near-term tower valuations, yet spectrum scarcity and data-traffic growth will eventually compel network expansion once currency risk subsides. Smaller markets such as Paraguay, Uruguay, and Costa Rica contribute niche opportunities centered on border corridors and industrial-connectivity verticals.

Competitive Landscape

Regional competition is moderately concentrated. American Tower Corporation maintains the largest footprint, leveraging country diversification to spread FX risk and negotiating power with multinationals. Sitios Latam, spun out of America Movil, exploits anchor-tenant contracts across 18 countries, while Phoenix Tower International accumulates assets in secondary markets where acquisition multiples remain lower.

Strategic moves emphasize value-added services beyond space leasing. American Tower’s edge-data-center pilot in Sao Paulo targets low-latency enterprise workloads, and Sitios Latam is rolling out hybrid-energy upgrades across Mexican sites to cut diesel OPEX. SBA Communications exited Colombia in February 2025, redeploying proceeds toward rooftop clusters in Brazil’s southern states to counter currency risk. Phoenix Tower secured creditor rights in WOM Chile’s Chapter 11 process, positioning itself to absorb 3,800 sites upon restructuring.

Consolidation is expected to continue as scale buys procurement advantages and lowers maintenance costs per tenant. However, antitrust authorities remain alert, illustrated by Argentina’s March 2025 veto of a Telecom-Telefonica merger that would have unified mobile and fixed-line dominance. Currency-matched financing and renewable-energy capabilities are emerging as differentiators for prospective buyers.

Latin America Telecom Tower Industry Leaders

American Tower Corporation (ATC)

Sitios Latam (América Móvil)

Phoenix Tower International (PTI)

SBA Communications Corporation

Torrecom Partners LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EdgePoint Towers completed its inaugural solar-hybrid tower, confirming OPEX reductions in off-grid scenarios.

- March 2025: Argentina’s government blocked the USD 1.245 billion Telecom-Telefónica merger on antitrust grounds.

- February 2025: SBA Communications divested its Colombia portfolio to an undisclosed buyer, reallocating capital to offset FX exposure in other markets.

- January 2025: Alcoa partnered with TIM Brasil to deploy solar-powered Flextower units delivering 4G in remote Amazon communities.

Latin America Telecom Tower Market Report Scope

The telecommunication market is largely concerned with the operations and provision of infrastructure for transmitting data - voice, image, sound, text, and video. To expand its network and services, the telecommunication market relies on towers, which are used to mount telecommunication networking and power equipment.

The scope of the report includes coverage of telecom towers in Latin America, a detailed analysis of key countries, key metrics, mergers and acquisitions (M&A), and developments. In addition, the report also covers country-specific regulatory landscape, ecosystem analysis, and vendor landscape details. The report is segmented by ownership (MNOs, MNO and TowerCo, and independent TowerCo), installation type (rooftop and ground-based), and country (Brazil, Mexico, Colombia, Peru, Argentina, Paraguay, and the Rest of Latin America).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Argentina |

| Mexico |

| Rest of Latin America (Panama, Costa Rica, Uruguay, Guatemala, and Others) |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed | |

| By Country | Brazil |

| Chile | |

| Colombia | |

| Peru | |

| Argentina | |

| Mexico | |

| Rest of Latin America (Panama, Costa Rica, Uruguay, Guatemala, and Others) |

Key Questions Answered in the Report

How big is the Latin America telecom tower market in 2026?

The Latin America telecom tower market size stands at USD 3.69 billion in 2026.

What CAGR is expected for the sector through 2031?

The market is forecast to post a 3.94% CAGR from 2026 to 2031.

Which ownership model holds the largest share?

Independent TowerCos lead with 52.87% of active sites in 2025.

Which fuel system is growing fastest?

Renewable-powered towers are expanding at a 12.74% CAGR due to sustainability mandates.

Why are rooftop towers gaining traction?

Rooftop sites bypass ground-lease hurdles in dense cities and support high-frequency 5G coverage.

What is the biggest restraint facing new builds?

Municipal permitting delays, particularly in Brazil, add multi-year lags to deployment timelines.

Page last updated on: