Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.89 Billion |

| Market Size (2026) | USD 3.05 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Pet Food Market Analysis by Mordor Intelligence

Spain pet food market size in 2026 is estimated at USD 3.05 billion, growing from 2025 value of USD 2.89 billion with 2031 projections showing USD 4.02 billion, growing at 5.63% CAGR over 2026-2031. The Spanish pet food market is gaining momentum from the rapid adoption of premiumization, functional formulation, and increasing e-commerce penetration, particularly among urban millennials who view pets as family members. Regulatory clarity regarding novel proteins supports innovation even as it imposes rigorous compliance costs. Supply chain vulnerabilities present headline risks, particularly omega-3 sourcing disruptions and ingredient price volatility affecting premium product margins. Low competitive concentration allows local challengers to secure share through sustainable ingredients and direct-to-consumer models while the top three global players continue to defend scale advantages.

Key Report Takeaways

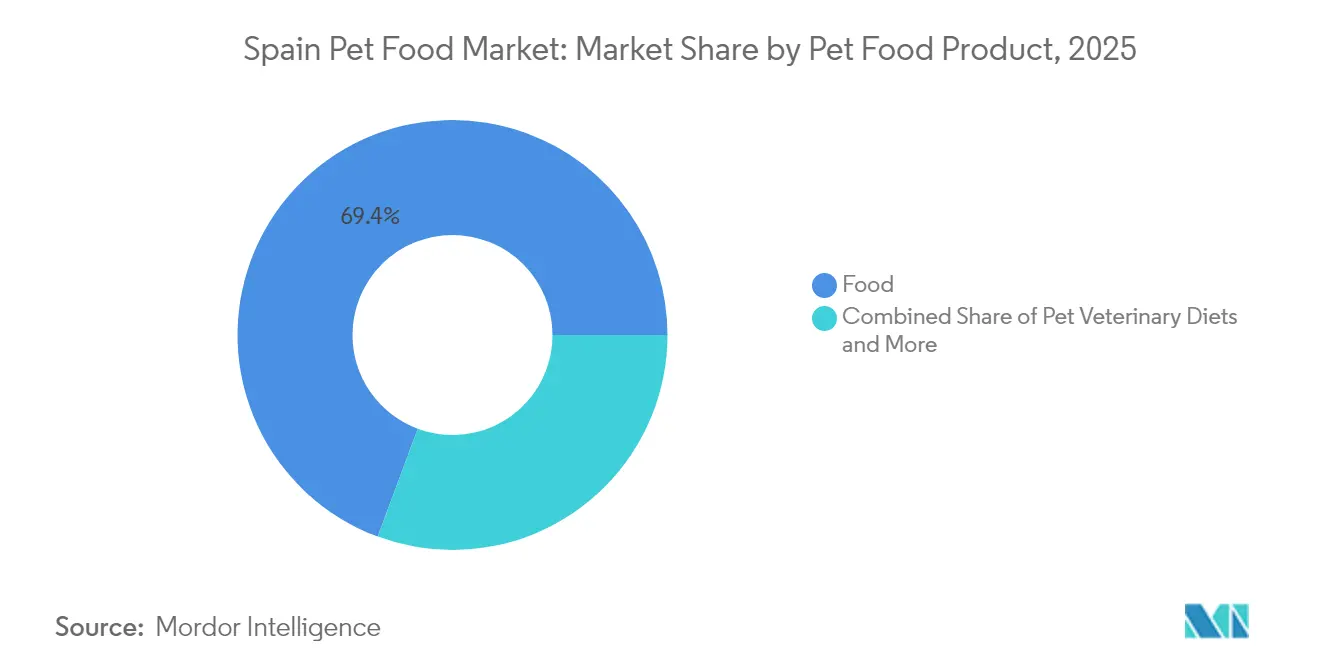

- By product category, staple food held 69.35% of Spain pet food market share in 2025, whereas treats are projected to accelerate at a 6.79% CAGR through 2031.

- By pet type, dogs led with 55.60% revenue share in 2025, while cats are poised for a 6.53% CAGR to 2031.

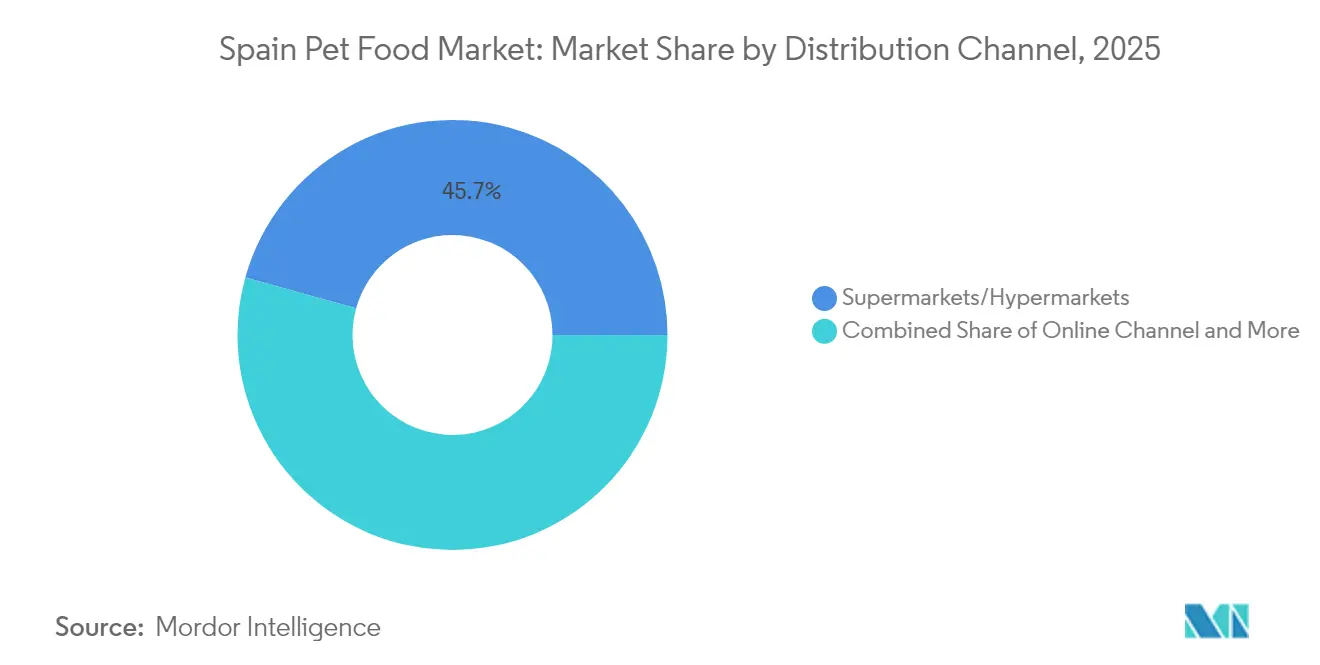

- By distribution channel, supermarkets and hypermarkets commanded 45.70% share of Spain pet food market size in 2025, but online platforms are forecast to expand at an 8.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Humanization of Pets | +1.8% | National, concentrated in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Premiumization and Functional Formulation Push | +1.5% | Urban centers, expanding to suburban markets | Long term (≥ 4 years) |

| E-commerce Penetration in Emerging Markets | +0.9% | National, with early gains in Catalonia, Andalusia | Short term (≤ 2 years) |

| Veterinary Endorsements and Prescription Diet Growth | +0.7% | National, veterinary channel focus | Medium term (2-4 years) |

| Microbiome-targeted Nutrition R&D Breakthroughs | +0.4% | National, premium segment adoption | Long term (≥ 4 years) |

| Sustainable Protein Inclusions | +0.3% | National, environmentally conscious consumers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Humanization of Pets

Spanish owners increasingly view animals as family, with 85% embracing the human-grade nutrition ethos. Organic and natural lines captured 23% share in 2024, up from 18% in 2022, reflecting readiness to pay for ingredient transparency[1]Source: AEDPAC, “Pet Population and Market Statistics 2024,” AEDPAC, aedpac.com. Millennials drive this shift by favoring premium SKUs priced above EUR 8 (USD 8.5) per kilogram, which logged 40% sales growth at specialty retailers. Brands emphasize lifestyle narratives and emotive packaging to align with this mindset. As urban households rise, Spain pet food market benefits from higher per-capita expenditure, lifting revenue resilience even during economic uncertainty.

Premiumization and Functional Formulation Push

Digestive-health recipes climbed 35% in 2024 as veterinarians recommended targeted diets for chronic conditions. Affinity Petcare’s postbiotic-enriched range recorded clinically validated gut benefits in 78% of pets, underscoring scientific proof points[2]Source: Affinity Petcare Research Team, “Postbiotic Integration Clinical Trial,” Affinity Petcare, affinitypetcare.com. Consumers also display willingness to pay for responsibly sourced proteins, with 42% favoring environmentally certified products. Insect-based formulations meet that demand while reducing carbon footprints. Spain pet food market therefore sees R&D investments in clinically backed, planet-friendly ingredients that sustain premium pricing.

E-commerce Penetration in Emerging Markets

Online pet food revenue jumped 25% in 2024, and subscription models now represent 15% of digital sales[3]Source: Eurostat, “E-commerce Statistics for Pet Products 2024,” European Commission, ec.europa.eu/eurostat. The e-commerce expansion benefits smaller brands lacking traditional retail presence, with direct-to-consumer models enabling premium pricing and customer relationship building. Regional variations emerge, with Catalonia and Madrid leading digital adoption of total pet food purchases, while rural areas maintain a preference for traditional retail channels. Technology integration includes AI-powered nutrition recommendations and telemedicine consultations, creating differentiated customer experiences that drive loyalty and repeat purchases.

Veterinary Endorsements and Prescription Diet Growth

Veterinary channel influence strengthens as pet health awareness increases, with prescription diets representing the fastest-growing segment. The prescription diet market benefits from aging pet demographics, with dogs over 7 years comprising 35% of the population and requiring targeted nutrition for joint health, cognitive function, and metabolic support. Regulatory compliance under guidelines ensures product efficacy and safety, creating barriers to entry that protect established players while maintaining consumer confidence. This trend drives partnerships between manufacturers and veterinary practices, with education programs and diagnostic tools supporting professional recommendations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility of Key Ingredients | -1.2% | National, affecting all market segments | Short term (≤ 2 years) |

| Regulatory Scrutiny on Novel Proteins | -0.8% | EU-wide, Spanish implementation focus | Medium term (2-4 years) |

| Supply-chain Disruptions in Omega-3 Sourcing | -0.6% | National, premium segment impact | Short term (≤ 2 years) |

| Rising Incidence of Pet Food Recalls | -0.4% | National, consumer confidence impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Key Ingredients

Raw material cost fluctuations create margin pressure across the pet food value chain, with protein sources experiencing price variations during 2024 due to global supply constraints and climate-related disruptions. Spanish manufacturers face particular challenges in omega-3 sourcing, where fish oil prices increased following reduced anchovy catches in Peruvian waters. The volatility affects premium product positioning, as manufacturers struggle to maintain consistent pricing while preserving profit margins. Smaller companies lack hedging capabilities enjoyed by multinational competitors, creating competitive disadvantages during periods of extreme price volatility. Consumer price sensitivity increases during economic uncertainty, potentially limiting premium product adoption and forcing manufacturers to reformulate products or accept reduced margins.

Regulatory Scrutiny on Novel Proteins

European Food Safety Authority's (EFSA) rigorous approval processes for novel protein sources create lengthy market entry timelines, with insect-based ingredients requiring extensive safety and nutritional studies before commercial authorization. The regulatory framework, while ensuring consumer safety, limits innovation speed and increases development costs for companies pursuing alternative protein strategies. Spanish implementation of EU directives adds local compliance requirements, creating additional complexity for manufacturers seeking to introduce novel formulations. The scrutiny particularly affects small and medium enterprises lacking regulatory expertise and financial resources for extensive testing protocols. Market uncertainty around approval timelines complicates investment decisions and product development planning, potentially delaying market introduction of innovative solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Premium Treats Drive Category Expansion

The food segment commanded 69.35% of Spain pet food market share in 2025, retaining primacy due to habitual purchasing and broad distribution. Treats will post the strongest 6.79% CAGR through 2031 as owners reward pets more frequently and seek dental or joint-support benefits. Dry food delivers volume efficiency, whereas wet formulas for cats focus on palatability and hydration appeal. Spain pet food market size for veterinary diets captures disproportionately high revenue because disease-specific formulas trade at price premiums, supported by clinical research.

Functional snacks fortified with glucosamine or probiotics promise incremental growth, aligning with the premiumization arc. Sustainability claims now appear across mainstream kibble, reflecting owners appetite for ethically sourced proteins. Regulatory oversight ensures transparent labeling so consumers can confidently pay extra for perceived value. Larger players bundle treat innovations with core food portfolios to deepen brand stickiness, an approach that smaller challengers mimic through limited-edition SKUs and seasonal flavors.

By Pets: Feline Growth Outpaces Canine Dominance

Dogs absorbed 55.60% of revenue in 2025 but cats will expand faster at 6.53% CAGR through 2031. Urban apartment living favors cats because of lower space requirements, and younger households delay dog adoption until later life stages. Spain pet food market size for feline wet food has risen sharply, reflecting hydration needs and urinary health positioning.

Cat owners show high responsiveness to flavor diversity, prompting brands to introduce rotational diets that limit taste fatigue. Dog nutrition trends focus on weight management and aging support due to higher prevalence of obesity and joint problems. Vaccination and microchipping campaigns boost veterinary clinic visits, indirectly reinforcing prescription diet uptake across both species. Marketers increasingly target multi-pet households, which account for 35% of owners, by offering bundle discounts and cross-species loyalty programs within Spain pet food market.

By Distribution Channel: Digital Transformation Accelerates

Supermarkets and hypermarkets retained 45.70% of Spain pet food market size in 2025 thanks to convenience and aggressive promotions. Online channels will log the highest 8.17% CAGR as subscription models lock in recurring orders and data analytics enable personalized offers. Specialty stores remain the reference point for premium segments that require professional advice, maintaining a loyal core clientele.

Omnichannel strategies gain traction; leading brands ensure consistent pricing across physical and digital touchpoints to avoid channel conflict. Spain pet food market participants also partner with veterinary e-pharmacies to bundle therapeutic diets with teleconsultations. Rural penetration of e-commerce trails, yet last-mile solutions are closing logistics gaps, suggesting continued migration of value toward online platforms.

Geography Analysis

Spain pet food market demonstrates concentrated demand in Madrid and Catalonia, which together generate around significant percentage of national revenues. Higher disposable incomes and smaller household sizes in these regions encourage expenditure on premium nutrition. Andalusia emerges as a next-wave opportunity due to rising pet adoption and expanding retail infrastructure. Northern communities such as the Basque Country and Galicia show a preference for locally produced, artisanal offerings, reinforcing regional brands.

Coastal provinces leverage proximity to fisheries, enabling fresh marine ingredients that enhance provenance claims and shorten supply chains. Valencia exhibits above-average online penetration at close to 10% of pet food purchases, reflecting tech-savvy consumers and efficient fulfillment networks. Rural Castilla-La Mancha and Extremadura remain price sensitive, favoring value kibble, though premiumization gradually diffuses as education campaigns highlight long-term health benefits.

Spain also operates as a manufacturing and export node within the European Union, shipping specialty formulas to France and Portugal while importing select niche ingredients. Tariff-free EU trade and harmonized regulations streamline cross-border commerce, yet Brexit-related freight re-routing increases costs for suppliers using United Kingdom ports. Regional veterinary networks influence adoption of prescription diets, and autonomous community subsidies for animal welfare indirectly support market expansion.

Competitive Landscape

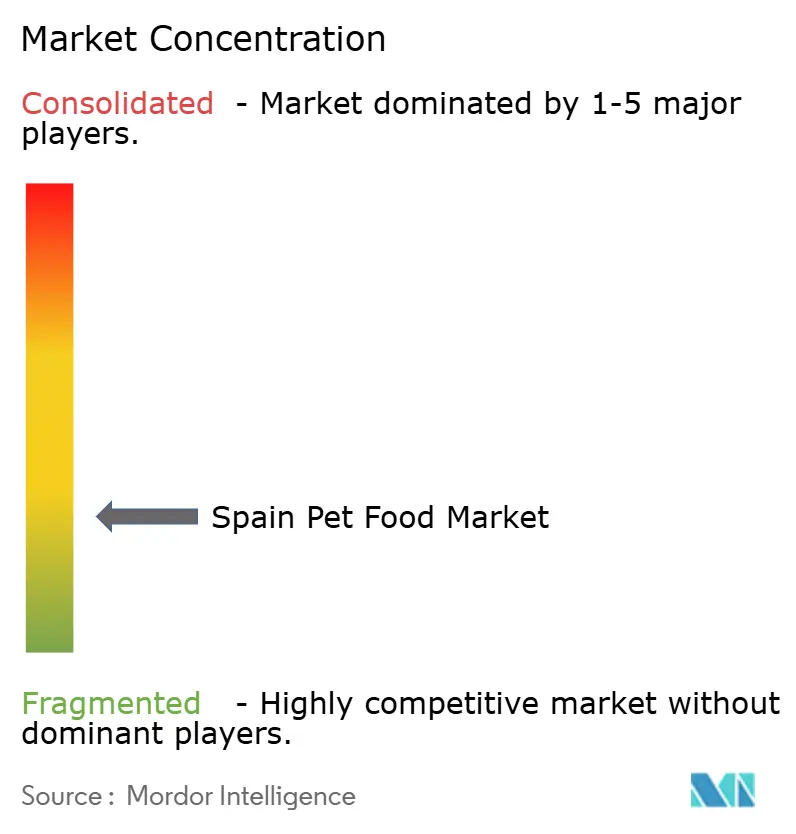

Spain pet food market displays low concentration, with Mars, Affinity Petcare, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), ADM and Nestlé Purina jointly. Mars invests in wet-food capacity at Melgar de Fernamental to serve domestic and export demand, while Affinity Petcare channels EUR 15 million (USD 15.9 million) into microbiome research that underpins next-generation functional diets. Nestlé Purina leverages global scale to maintain price competitiveness and wide distribution.

Emerging innovators, notably Tebrio and Picart Petcare, differentiate through sustainable insect protein and local ingredient sourcing. Tebrio’s Salamanca facility positions Spain as a continental hub for alternative proteins, supplying both internal demand and third-party formulators. Direct-to-consumer entrants exploit e-commerce to bypass shelf congestion, offering customizable meal plans and data-driven nutrition advice.

Strategic alliances abound; Vafo Praha aligned with retailer Kiwoko to extend premium European brands into 150 stores, underscoring the importance of in-market partners for foreign players. Investment in automation and renewable energy at new plants signals a cost and sustainability focus. Competitive intensity remains highest in treats, where low barriers enable small brands to pilot novel flavors, but scale incumbents can quickly replicate successful attributes.

Spain Pet Food Industry Leaders

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

Mars Incorporated

Nestle (Purina)

Affinity Petcare S.A

ADM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Tebrio secured an additional EUR 30 million (USD 32 million) in Series B funding to expand its insect protein production facility in Salamanca, bringing total investment to EUR 110 million (USD 116 million). The funding will support capacity expansion and product development for pet food applications, positioning Spain as a European leader in alternative protein production.

- July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. They contain vitamins, omega-3 fatty acids, and antioxidants.

- May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

Spain Pet Food Market Report Scope

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel.Pet Food Product

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft and Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

Pets

| Cats |

| Dogs |

| Other Pets |

Distribution Channel

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft and Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| Pets | Cats | ||||

| Dogs | |||||

| Other Pets | |||||

| Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms